Hair Brush Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.70 Billion |

| Market Size (2031) | USD 7.90 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

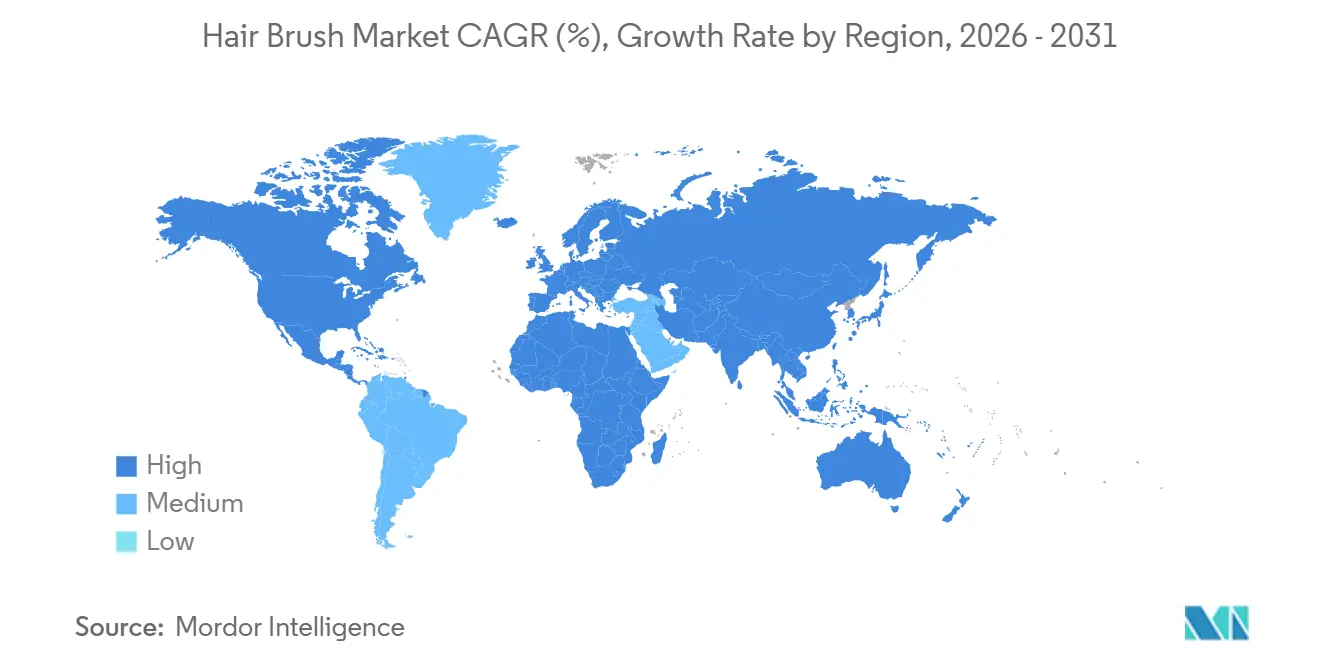

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hair Brush Market Analysis by Mordor Intelligence

The hair brush market was valued at USD 5.40 billion in 2025 and reached USD 5.70 billion in 2026, with projections indicating growth to USD 7.90 billion by 2031 at a CAGR of 6.59% during the forecast period of 2026-2031. This growth reflects a shift in the hair care industry, where brushes are increasingly viewed as integral components of multi-step at-home styling routines rather than basic utility items. This shift has driven category growth, as expanded distribution channels provide access to previously underserved consumer groups. Additionally, rising consumer awareness of hair health, scalp care, and damage prevention is influencing purchasing decisions, leading to increased demand for specialized brushes designed for detangling, minimizing breakage, enhancing scalp stimulation, and catering to specific hair textures. In response, manufacturers are focusing on product differentiation by offering paddle, cushion, vent, and thermal brushes tailored to various styling and treatment requirements. Furthermore, the rapid growth of e-commerce and the influence of social media-driven beauty education have enhanced consumer access to premium and niche brush categories, boosting adoption beyond traditional mass-market products.

Key Report Takeaways

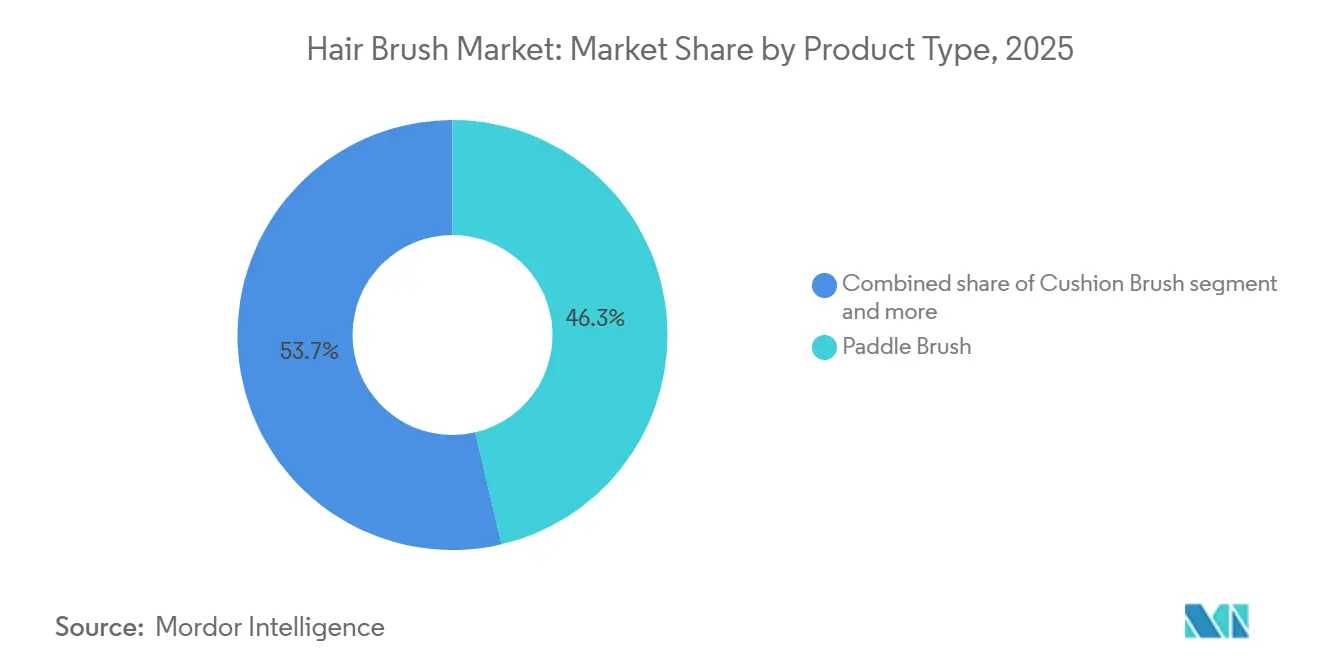

- By product type, paddle brushes captured 46.34% of the 2025 market, while cushion brushes are advancing at a 7.59% CAGR through 2031.

- By material, synthetic retained an 80.19% share of the hair brush market size in 2025, while the organic/natural segment is forecast to grow at an 8.83% CAGR through 2031.

- By application, personal commanded 78.76% of demand in 2025, whereas professional is expanding fastest at 8.37% CAGR between 2026-2031.

- By price range, mass accounted for 80.40% of 2025 revenue, while premium is the fastest-growing segment, with a 7.81% CAGR through 2031.

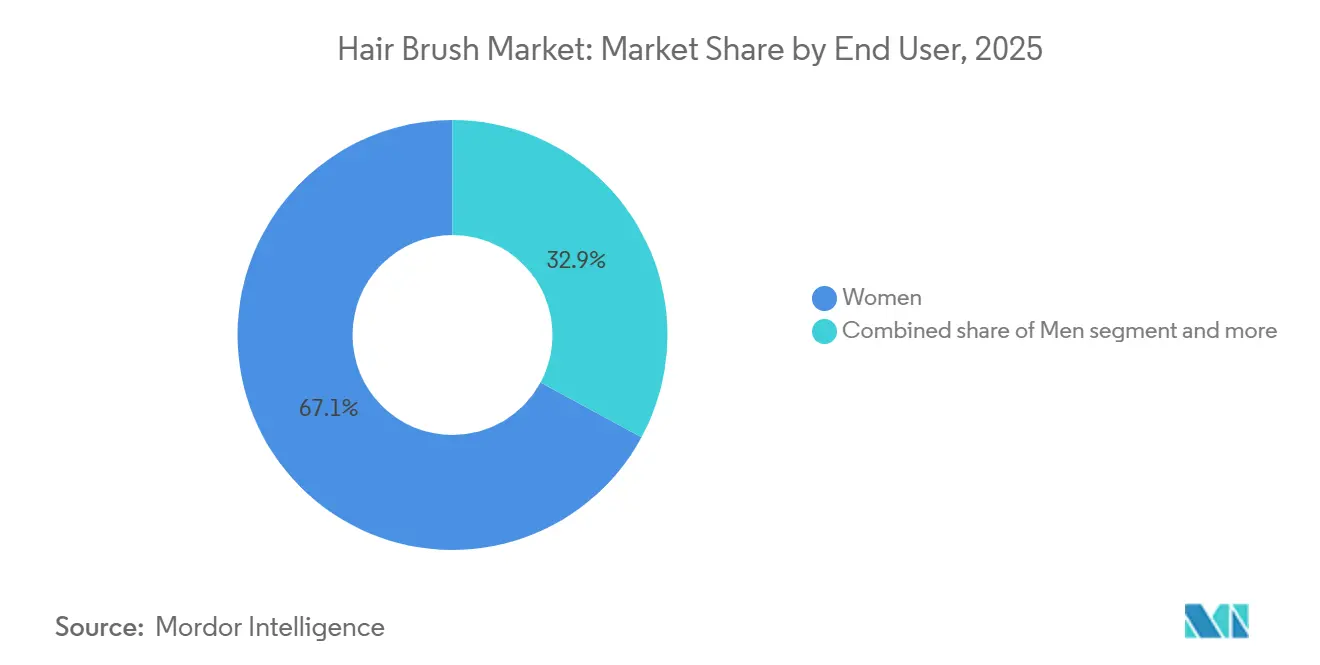

- By end user, women accounted for 67.11% of demand in 2025, whereas men are expanding fastest at a 7.86% CAGR between 2026-2031.

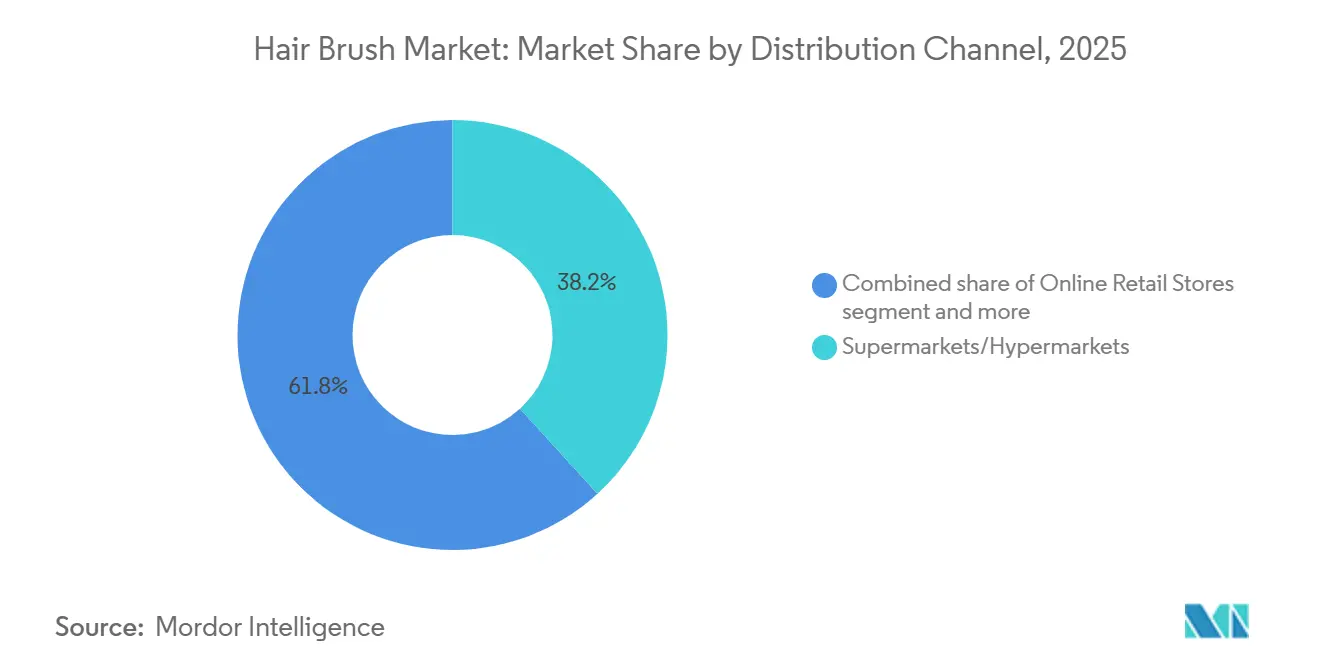

- By distribution channel, supermarkets/hypermarkets accounted for 38.22% of 2025 revenue, while online retail stores are expanding at 9.04% CAGR through 2031.

- By geography, Europe accounted for 32.02% share in 2025, while Asia-Pacific is the fastest-growing region with 7.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hair Brush Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness of hair care and personal grooming | +1.2% | Global | Short term (≤ 2 years) |

| Rising male grooming and self-care expenditure | +0.9% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Influence of social media, beauty bloggers, and influencers on specialized hair care tools | +1.0% | Global, primary in Asia-Pacific and North America | Short term (≤ 2 years) |

| Advancements in brush technology, including ionic, heated, and smart designs | +1.1% | Global, higher adoption in premium markets | Medium term (2-4 years) |

| Rising demand for eco-friendly and sustainable hair care products | +0.7% | Europe and North America | Long term (≥ 4 years) |

| Premium hair care routines beyond shampoos and conditioners | +0.8% | Global, with growing traction in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing awareness of hair care and personal grooming

Increasing consumer awareness regarding hair health, appearance management, and preventive hair care is a key factor driving the growth of the hair brush market. Hair brushes are now perceived not just as grooming tools but as essential products for maintaining scalp health, minimizing hair breakage, enhancing detangling efficiency, and supporting styling routines tailored to various hair types. This shift is evident in the growing consumer expenditure on hair care products. According to the U.S. Bureau of Labor Statistics, annual spending by American consumers on hair care products rose from USD 86.45 per consumer unit in 2023 to USD 101.14 in 2024, marking a year-over-year increase of nearly 17% [1]Source: Bureau of Labor Statistics, "Consumer Expenditure Surveys", bls.gov. This increase in spending reflects a broader consumer inclination to invest in products and accessories that aid in hair maintenance and styling. Consequently, there is a rising demand for premium and specialized hair brushes. As consumers place greater emphasis on hair wellness alongside personal grooming, manufacturers are experiencing increased adoption of high-value brushes designed to address specific hair concerns. This trend is driving both volume growth and category premiumization in the global hair brush market.

Rising male grooming and self-care expenditure

The growing focus on male grooming, personal appearance, and self-care is becoming a key driver for the hair brush market. While traditionally dominated by female consumers, the market is now experiencing increased participation from men as grooming routines evolve to include hair styling, beard maintenance, scalp care, and overall hair health management. Consumers increasingly perceive grooming as an integral part of personal wellness and professional presentation, prompting a shift towards specialized grooming tools instead of basic hair maintenance products. This trend is particularly prominent among younger demographics, who are more inclined to invest in styling accessories and adopt structured grooming routines. Consequently, the expanding male grooming market is enlarging the consumer base for hair brushes and driving consistent demand across both mass-market and premium product segments.

Influence of social media, beauty bloggers, and influencers on specialized hair care tools

The increasing influence of social media platforms, beauty influencers, hairstylists, and digital content creators is a significant factor driving the demand for specialized hair care tools, including hair brushes. Consumers are increasingly turning to online tutorials, product reviews, haircare routines, and styling demonstrations to guide their purchasing decisions. This has led to heightened awareness of the benefits offered by various brush types tailored to specific hair textures, concerns, and styling needs. Platforms such as Instagram, TikTok, YouTube, and Pinterest have elevated hair care from a basic grooming activity to a personalized and educational category, encouraging investments in tools like detangling brushes, paddle brushes, thermal brushes, scalp-massaging brushes, and natural-bristle brushes. The impact of social media is particularly pronounced in beauty-conscious markets across the Asia-Pacific region. For instance, survey data indicates that Instagram was one of the most popular social media platforms in South Korea, with approximately 45.8% of respondents identifying it as their most frequently used platform[2]Source: Korea Information Society Development Institute, stat.kisdi.re.kr. The widespread use of visually driven platforms like Instagram provides brands, beauty influencers, and haircare professionals with an effective medium to educate consumers on advanced haircare practices and promote specialized grooming tools.

Premium hair care routines beyond shampoos and conditioners

The hair care industry is experiencing a significant shift toward premiumization, with consumers increasingly allocating their spending to high-performance grooming and styling tools in addition to traditional products like shampoos and conditioners. This trend is supported by the rising concentration of affluent consumers in key markets. As of January 2026, the United States had approximately 935 billionaires, indicating notable growth in high-net-worth consumer segments with substantial purchasing power for premium personal care products [3]Source: Tax Fairness Organization, "U.S. BILLIONAIRES GOT $1.5 TRILLION RICHER IN TRUMP’S FIRST YEAR", americansfortaxfairness.org. Similarly, in the United Kingdom, around 2.62 million individuals had a net worth exceeding USD 1 million in 2024, excluding the value of their primary residence [4]Source: UBS, "Global Wealth Report 2025", global-wealth-report-09072025.pdf. The global expansion of affluent and upper-middle-income populations is driving demand for premium beauty and grooming products, including advanced hair brushes designed for performance, aesthetics, sustainability, and professional-grade functionality. In response, manufacturers are increasingly focusing on innovation,

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long product lifespan resulting in infrequent replacement cycles | -1.1% | Global | Long term (≥ 4 years) |

| Availability of counterfeit and low-quality imitation products affecting premium brand sales | -0.9% | Asia-Pacific, online channels globally | Short term (≤ 2 years) |

| Fragmented market with intense competition leading to price wars and margin pressure | -0.8% | Global | Medium term (2-4 years) |

| Environmental criticism of plastic-based grooming accessories | -0.6% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long product lifespan resulting in infrequent replacement cycles

The extended functional lifespan of hair brushes serves as a significant restraint on market growth, as it reduces purchase frequency and limits opportunities for recurring sales. Unlike consumable hair care products such as shampoos, conditioners, serums, and styling treatments that require regular replenishment, hair brushes can remain functional for several years with minimal maintenance. Consequently, demand is primarily replacement-driven rather than consumption-driven, resulting in a slower purchasing cycle. For many consumers, a hair brush is perceived as a durable household item rather than a product requiring frequent upgrades, particularly in the mass-market segment where basic plastic brushes sufficiently meet everyday grooming needs. While premium and hair-type-specific brushes have introduced new growth opportunities, the durable nature of the product continues to constrain replacement rates, thereby limiting the overall market's growth potential. Thus, the long lifecycle of hair brushes remains a structural challenge for industry players aiming for sustained volume growth.

Availability of counterfeit and low-quality imitation products affecting premium brand sales

The presence of counterfeit and low-quality imitation hair brushes presents a considerable obstacle to the growth of the premium hair brush market. As the demand for branded and specialized grooming tools rises, unauthorized manufacturers are increasingly producing low-cost replicas that imitate the appearance of established products but lack comparable material quality, durability, and performance. These imitation products are particularly common in online marketplaces and price-sensitive regions, where consumers often prioritize affordability over brand authenticity. The availability of these cheaper alternatives frequently diverts sales from premium manufacturers, hindering their ability to fully benefit from the growing interest in advanced hair care tools. In addition to revenue losses, counterfeit products can erode consumer confidence in premium brands when imitation brushes fail to meet expectations. The use of inferior materials, poorly designed bristles, and inadequate construction can result in hair breakage, scalp irritation, reduced durability, and subpar styling performance, ultimately damaging consumer perceptions of the original brand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Paddle Brushes Lead, Cushion Designs Gain Traction

In 2025, paddle brushes held a 46.34% share of the hair brush market. This dominance is attributed to their versatility across various hair textures, making them suitable for a wide range of consumers. Additionally, their compatibility with blow-drying techniques enhances their appeal among both professional stylists and individual users. Paddle brushes are widely adopted in salon environments for their efficiency in styling and smoothing hair, while their ease of use and effectiveness have also made them a popular choice for home use. These factors collectively contribute to their leading position in the market.

Cushion brushes are expected to be the fastest-growing product type, with a CAGR of 7.59% during 2026-2031. This growth is driven by increasing consumer demand for scalp-comfort features and the segment's alignment with flexible-base ionic designs. Round brushes maintain a stable position in professional blowout and volumizing applications, while vent brushes are gaining popularity on social media platforms due to their faster-drying capabilities. Detangling brushes, popularized by brands such as Tangle Teezer and The Wet Brush, have transitioned from niche products to mass-market staples, with ongoing innovations in bristle geometry ensuring their continued relevance. Other types, including teasing brushes and boar-bristle specialty formats, achieve above-average margins by catering to specific professional use cases.

By Material: Synthetic Dominates, Natural and Organic Materials Set the Growth Pace

Synthetic materials, including plastic, nylon, and mixed bristle configurations, accounted for 80.19% of the 2025 market share due to their lower manufacturing costs, consistent quality, and compatibility with ionic emitter integration. These materials are widely preferred by manufacturers as they offer scalability and uniformity in production processes. However, the growth of natural materials faces a structural supply-side constraint. Sourcing high-quality boar bristles and certified FSC bamboo at a commercial scale presents logistical challenges, including limited availability of raw materials and the complexities of maintaining sustainable sourcing practices. This creates a competitive advantage for brands that establish secure and reliable supply chains early, ensuring consistent access to these resources.

Organic and natural materials, such as bamboo, wood, boar bristles, and natural rubber cushion configurations, represent the fastest-growing category, with a compound annual growth rate (CAGR) of 8.83% projected for 2026-2031. This growth rate is the highest among all market segments and is driven by three key factors: increasing consumer preference for sustainable materials, premium brand narratives emphasizing craftsmanship, and heightened regulatory pressures in Europe. These regulations, under the EU Green Deal, progressively restrict the use of plastic packaging and materials. Additionally, the shift towards organic materials is supported by growing environmental awareness among consumers, who are increasingly seeking products that align with their values of sustainability and eco-friendliness. This trend is further amplified by brands leveraging storytelling to highlight the artisanal quality and environmental benefits of natural materials, thereby appealing to a broader audience.

By Application: Personal Use Anchors Volume, Professional Channels Command Margin

The personal use segment accounted for 78.76% of the global hair brush market in 2025, representing the largest application category. This dominance is attributed to the consistent and widespread need for daily hair grooming, detangling, styling, and maintenance within households. Increasing consumer awareness about hair health, scalp care, and appearance management has driven the adoption of specialized brushes in personal care routines.

The professional use segment is anticipated to achieve the highest CAGR of 8.37% during the forecast period. This growth is supported by the ongoing expansion of salons, barbershops, beauty studios, and professional hairstyling services globally. Professional hairstylists are increasingly using specialized brushes designed for blow-drying, thermal styling, volumizing, precision styling, and hair treatment applications, leading to higher product usage and replacement rates compared to household users.

By Price: Mass Segment Provides Scale, Premium Tier Leads Relative Growth

The mass-market segment accounted for 80.40% of the global hair brush market in 2025, making it the leading price-range category. This dominance is primarily due to the essential role of hair brushes in daily grooming and the widespread availability of affordable options through supermarkets, hypermarkets, pharmacies, convenience stores, and online platforms. Consumers in both developed and emerging markets continue to prefer cost-effective brushes that fulfill basic grooming, detangling, and styling requirements.

The premium segment is anticipated to grow at the fastest CAGR of 7.81% during the forecast period. This growth is driven by increasing consumer interest in specialized hair care tools that provide enhanced functionality and promote hair health. Demand is rising for premium brushes with features such as natural bristles, ergonomic designs, anti-static properties, scalp-massaging capabilities, sustainable materials, and salon-grade performance. Greater awareness of hair damage prevention, scalp health, and personalized hair care routines is motivating consumers to transition from conventional brushes to higher-value alternatives.

By End User: Women Drive Volume, Men Are the Fastest-Growing Segment

Women accounted for 67.11% of the hair brush market in 2025, reflecting consistent historical purchasing trends in personal care accessories. This dominance is attributed to the higher frequency of hair care routines among women, which drives demand for a variety of brush types, including detangling, styling, and volumizing brushes. Additionally, women are more likely to invest in premium and specialized brushes, further solidifying their significant share in the market. The children's segment contributes a modest yet stable incremental volume, with detangling brushes driving most category growth as parents prioritize low-breakage and pain-free brushing solutions.

The men's segment is projected to grow at a CAGR of 7.86% from 2026 to 2031, supported by the sustained expansion of the global male grooming category. Vent brushes, cushion brushes, and detangling formats are increasingly being included in male grooming kits alongside products like clay and pomade, as multi-step grooming routines become more common among men. This shift has created a cross-sell opportunity that was largely absent five years ago. A key consideration for brand strategy: male buyers in this category tend to exhibit lower brand loyalty, making retail shelf prominence and ergonomic packaging design more effective in driving conversions than brand heritage—an opportunity for new market entrants.

By Distribution Channel: Mass Retail Holds Share, Online Channels Drive Competitive Intensity

The supermarkets and hypermarkets segment accounted for 38.22% of the global hair brush market in 2025, establishing itself as the largest distribution channel. This dominance is attributed to extensive product visibility, a wide consumer base, and the ability to offer a diverse range of hair brushes across various price points. Consumers often purchase hair brushes during routine personal care and household shopping, making supermarkets and hypermarkets a convenient and preferred choice.

The online retail stores segment is anticipated to achieve the fastest CAGR of 9.04% during the forecast period, driven by the rapid expansion of e-commerce platforms and evolving consumer purchasing habits. Online channels offer access to a broader selection of hair brushes, including premium, professional-grade, eco-friendly, and hair-type-specific options that may not be easily available in traditional retail stores. Additionally, the growing impact of social media marketing, beauty influencers, product reviews, and digital advertising has further boosted online sales of grooming products.

Geography Analysis

In 2025, Europe accounted for 32.02% of the global hair brush market, making it the largest regional market. This dominance is attributed to high consumer spending on personal care products, strong awareness of hair health and grooming, and the widespread use of premium beauty and styling tools. European consumers increasingly focus on specialized hair care solutions, driving demand for premium brushes designed for detangling, scalp care, styling, and damage prevention.

The Asia-Pacific hair brush market is projected to grow at the fastest CAGR of 7.18% during the forecast period. This growth is driven by rising disposable incomes, rapid urbanization, and increasing beauty consciousness among consumers. The region's large population, expanding middle-class demographic, and growing emphasis on personal grooming present significant opportunities for market expansion. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are experiencing increased adoption of specialized hair care products as consumers become more aware of hair health, styling, and scalp wellness.

Across both developed and emerging markets, the hair brush industry benefits from evolving consumer preferences for comprehensive hair care routines and advanced grooming solutions. Europe continues to lead as the largest market due to its mature beauty and personal care landscape. However, Asia-Pacific is expected to contribute the highest incremental growth during the forecast period. North America remains a significant market, supported by strong consumer spending on premium grooming products and increasing demand for specialized styling tools. These regional dynamics are driving manufacturers to expand product portfolios, enhance omnichannel distribution strategies, and introduce innovative brush designs tailored to diverse consumer needs, hair types, and styling preferences.

Competitive Landscape

The hair brush market is moderately fragmented, with no single company holding a dominant market share. High-volume players such as Conair LLC and Spectrum Brands Holdings (through Remington) focus on supply chain efficiency, extensive mass-retail distribution, and competitive pricing to maintain their market presence. These companies aim to cater to a broad consumer base by offering affordable and widely available products. In contrast, technology-focused premium brands like Dyson and GHD emphasize advanced product engineering and innovation, targeting consumers willing to pay a premium for high-performance and technologically advanced products.

This strategic division is reflected in recent product developments: volume players leverage co-branding and retailer partnerships to expand their reach and drive sales. For instance, Wet Brush's March 2026 collaboration with Hill House Home at Ulta and FHI Heat's expansion into Walmart are aimed at creating additional purchase opportunities and enhancing brand visibility. On the other hand, premium brands prioritize innovation and intellectual property, as demonstrated by Wet Brush's patent-pending ionic infusion brush and Dyson's RFID nozzle-recognition system in the Airwrap Coanda 2X. These innovations highlight their focus on delivering unique features and advanced functionality to differentiate themselves in the market.

Additionally, specialized professional brands, including Denman International, Olivia Garden International, Ibiza Hair, and Tek Salonsystem, continue to exert competitive pressure on larger players within salon distribution channels. These brands leverage their deep technical expertise and focus on specification-driven purchasing to cater to professional stylists and salon owners. By offering high-quality, specialized products tailored to professional needs, they challenge the dominance of larger incumbents, where technical performance often takes precedence over mass-market scale.

Hair Brush Industry Leaders

-

Conair LLC

-

Denman International Limited

-

Tangle Teezer Limited

-

Mason Pearson Bros. Ltd.

-

G. B. Kent and Sons plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Tangle Teezer unveiled a limited-edition collaboration with The Devil Wears Prada, presenting exclusive versions of its Ultimate Detangler and Mini Ultimate Detangler brushes. These brushes feature a metallic red design inspired by the iconic fashion franchise. The launch highlights Tangle Teezer's detangling technology while leveraging entertainment-themed branding, reflecting the rising demand for premium, collectible hair care accessories created through brand and pop-culture partnerships.

- March 2026: Wet Brush introduced a limited-edition collaboration with Hill House Home, a lifestyle brand recognized for its romantic prints and feminine designs. The collection includes Wet Brush's bestselling Original Detangler featuring IntelliFlex bristles, along with silk scrunchies, headbands, and claw clips adorned with Hill House Home's signature floral, gingham, trellis, and striped patterns. This collaboration blends fashion with practical haircare solutions.

- March 2026: FHI Heat has expanded its retail partnership with Walmart by launching the Hello Kitty and Friends UNbrush, a limited-edition collaboration with Sanrio. This product is available exclusively at Walmart stores and Walmart.com. The collection integrates FHI Heat's UNbrush detangling technology with character-themed designs, aligning with the increasing trend of merging beauty tools with entertainment and lifestyle brands.

Global Hair Brush Market Report Scope

| Round Brush |

| Vent Brush |

| Paddle Brush |

| Cushion Brush |

| Detangling Brush |

| Others |

| Synthetic | Plastic |

| Nylon | |

| Mixed synthetic bristles | |

| Organic/Natural | Wooden brushes |

| Bamboo brushes | |

| Boar-bristle brushes | |

| Natural rubber cushions |

| Personal |

| Professional |

| Mass |

| Premium |

| Men |

| Women |

| Children |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Beauty Stores |

| Online Retail Stores |

| Drug Stores/Pharmacies |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Round Brush | |

| Vent Brush | ||

| Paddle Brush | ||

| Cushion Brush | ||

| Detangling Brush | ||

| Others | ||

| By Material | Synthetic | Plastic |

| Nylon | ||

| Mixed synthetic bristles | ||

| Organic/Natural | Wooden brushes | |

| Bamboo brushes | ||

| Boar-bristle brushes | ||

| Natural rubber cushions | ||

| By Application | Personal | |

| Professional | ||

| By Price Range | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Beauty Stores | ||

| Online Retail Stores | ||

| Drug Stores/Pharmacies | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the hair brush market by 2031?

The market is expected to reach USD 7.90 billion by 2031, growing at a CAGR of 6.59% from 2026 to 2031.

Which region is expected to grow the fastest in the hair brush market?

Asia-Pacific is projected to be the fastest-growing region, registering a CAGR of 7.18% during 2026–2031.

Which product type holds the largest share in the hair brush market?

Paddle brushes held the largest market share at 46.34% in 2025.

Which distribution channel dominates the global hair brush market?

Supermarkets/hypermarkets dominated the market with a 38.22% share in 2025.

Page last updated on: