Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

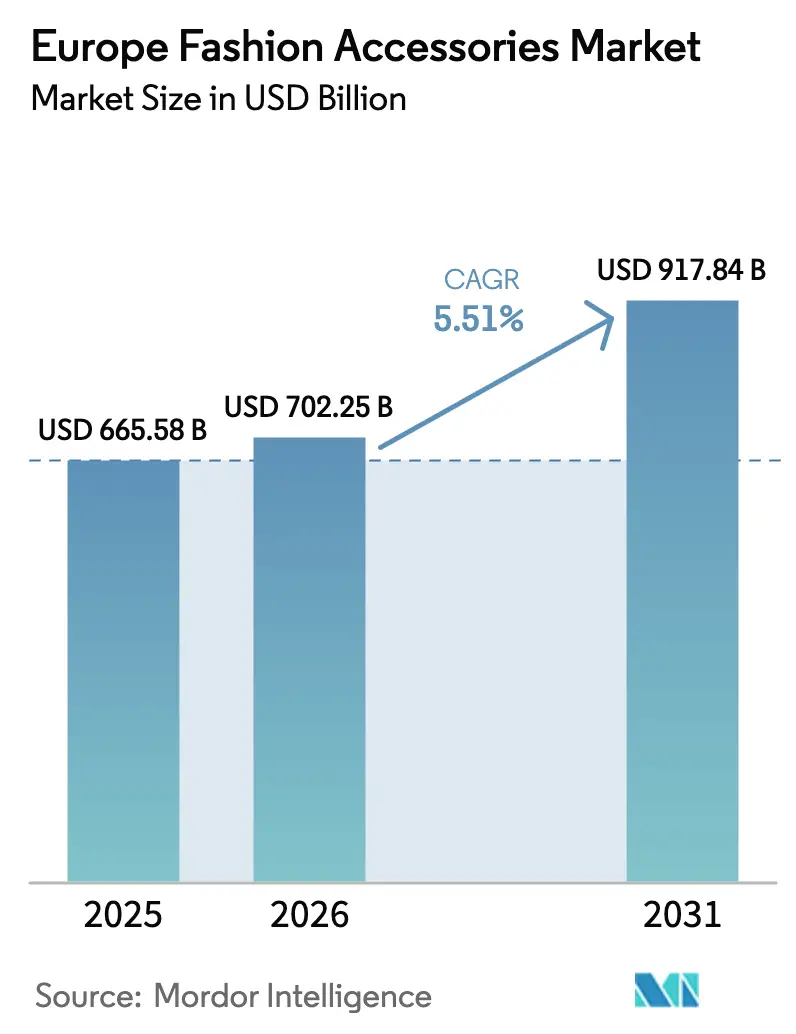

| Base Year Market Size (2025) | USD 665.58 Billion |

| Market Size (2026) | USD 702.25 Billion |

| Market Size (2031) | USD 917.84 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

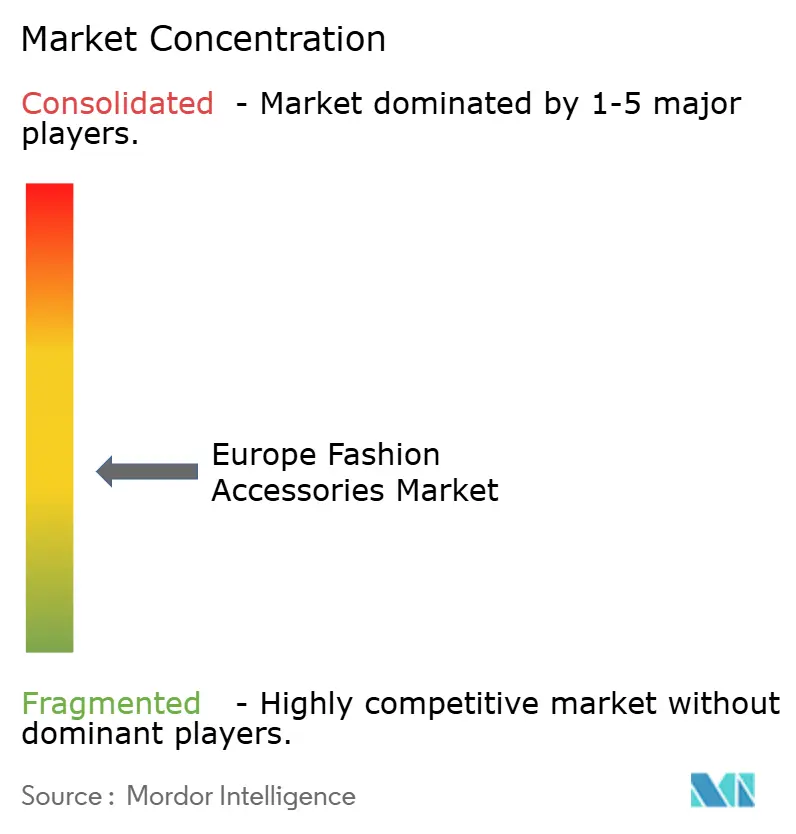

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Fashion Accessories Market Analysis by Mordor Intelligence

European Fashion Accessories market size in 2026 is estimated at USD 702.25 billion, growing from 2025 value of USD 665.58 billion with 2031 projections showing USD 917.84 billion, growing at 5.51% CAGR over 2026-2031. The market's expansion is driven by multiple factors, including changes in consumer lifestyles, increased household expenditure, favorable demographics, and rising demand for branded products. Europe maintains its position as a resilient luxury consumption hub despite global economic challenges, with the market benefiting from technological innovation and sustainability mandates. The sector demonstrates remarkable pricing power and brand loyalty, insulating it from typical discretionary spending cuts. The growing emphasis on eco-fashion further strengthens market growth, reflecting evolving consumer preferences toward sustainable and environmentally conscious products.

Key Report Takeaways

- By product type, apparel led with 59.02% of European fashion accessories market share in 2025, whereas watches are poised to grow the fastest at a 5.78% CAGR through 2031.

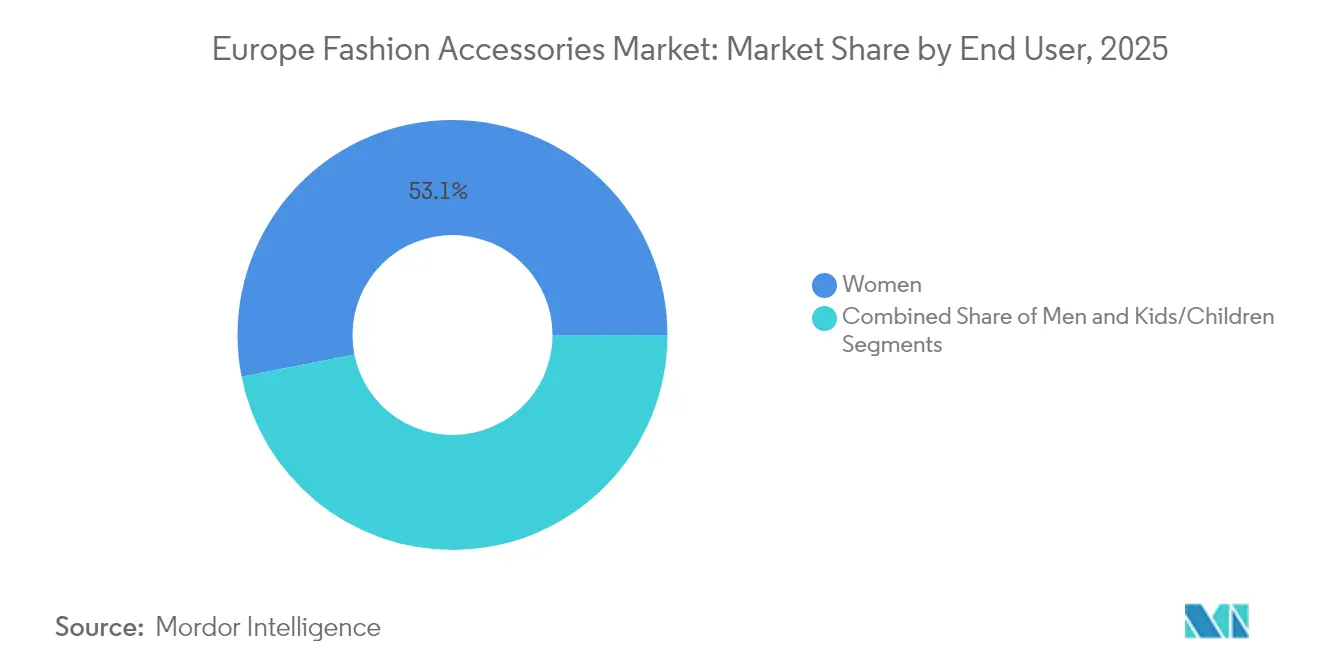

- By end user, women accounted for 53.11% of the European fashion accessories market in 2025; the children’s segment is projected to expand at a 6.14% CAGR to 2031.

- By category, mass accessories held 63.92% of the European fashion accessories market size in 2025, while premium offerings are advancing at a 6.45% CAGR through 2031.

- By distribution channel, offline stores retained 65.98% share of the European fashion accessories market in 2025, though online platforms are set to record a 6.86% CAGR to 2031.

- By geography, the United Kingdom captured 16.63% of the European fashion accessories market share in 2025 and Spain is expected to post the highest 7.25% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Fashion Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Advancements in Terms of Design and Raw Material | 1.2% | Regional, with concentration in Germany and France | Medium term (2-4 years) |

| Strong Demand From Inbound Tourist | 1.8% | UK, France, Italy, Spain resort markets | Short term (≤ 2 years) |

| Increasing Demand For Luxury Products | 1.5% | UK, Germany, France core markets | Long term (≥ 4 years) |

| Rising Demand For Sportswear From Fitness-Conscious Consumers | 0.9% | Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Sustainability and Ethical Production | 0.8% | EU-wide, strongest in Germany and Netherlands | Long term (≥ 4 years) |

| Influence of Social Media and Celebrity Endorsements | 1.1% | Regional, particularly strong in UK and France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Terms of Design and Raw Material

The integration of artificial intelligence and 3D printing technologies is transforming the European fashion market by reducing product development cycles from months to weeks and minimizing material waste. 3D printing enables manufacturers to create intricate designs, prototype rapidly, and produce customized accessories with reduced material wastage. The technology allows for complex geometries and innovative material combinations that were previously impossible with traditional manufacturing methods. The convergence of technology and fashion continues with Dolce Vita's April 2025 partnership with HILOS for on-demand 3D printed footwear, highlighting the market's evolution toward mass customization. These technological integrations enable fashion brands to offer personalized experiences through connected accessories while creating additional revenue streams in traditional craft-based segments.

Strong Demand From Inbound Tourist

Tourism's resurgence in Europe has significantly influenced the fashion accessories market by creating a luxury spending multiplier effect. The shift in consumer preferences toward experiential luxury has positioned accessories as portable status symbols and travel mementos, driving demand for lightweight, versatile pieces suitable for various occasions. Duty-free retail has evolved with brands establishing flagship stores in airports and resort destinations to capture tourist spending before it disperses to local markets. According to UN Tourism, Europe recorded 747 million international arrivals in 2024, representing a 5% increase from 2023, supported by strong intraregional demand [1]Source: UN Tourism, “International tourism recovers pre-pandemic levels in 2024,” unwto.org . However, the geographic concentration of tourist spending exposes brands to risks from geopolitical tensions and travel restrictions, making diversification across tourist source markets essential for European fashion accessories brands.

Increasing Demand For Luxury Products

Luxury accessories market demonstrates remarkable resilience in Europe, driven by generational wealth transfer and increasing adoption among younger demographics. The region's rising disposable income and growing preference for luxury products, coupled with a GDP per capita of USD 59.05 thousand in 2024 according to IMF, fuel market expansion[2]Source: International Monetary Fund, “World Economic Outlook Database,” imf.org . The strong presence of established luxury fashion houses like Louis Vuitton, Gucci, and Prada influences consumer purchasing behavior, while the growing middle-class population's aspirations for premium fashion accessories further stimulate market growth across European countries. The digital transformation of luxury retail, including enhanced e-commerce platforms and virtual try-on experiences, has created additional channels for market penetration and customer engagement. Furthermore, the increasing focus on sustainable and ethically produced luxury accessories aligns with European consumers' environmental consciousness, driving demand for responsibly manufactured premium products.

Rising Demand For Sportswear From Fitness-Conscious Consumers

Consumer preferences for technology-integrated accessories are reshaping the European fashion accessories market. Market growth shows a notable shift beyond traditional athletic categories, with athleisure accessories such as performance watches and fitness-tracking jewelry becoming lifestyle statements. This evolution has created demand for sport-specific accessories that combine functionality with fashion appeal. Sustainability concerns are influencing product development, as brands focus on recycled and bio-based materials that meet performance requirements while addressing environmental consciousness. The integration of health monitoring capabilities with fashion is generating opportunities for accessories that provide biometric feedback while maintaining aesthetic appeal, positioning wellness as a luxury lifestyle category. This trend is exemplified by the December 2024 collaboration between Gucci and Ōura, which produced an 18-karat gold smart ring. The ring's ability to track vital health metrics, including heart rate, respiratory rate, temperature, and sleep stages, while maintaining premium aesthetics, demonstrates the market's evolution toward tech-integrated fashion accessories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Counterfeit Products | -0.8% | Regional, particularly affecting online channels | Short term (≤ 2 years) |

| Supply Chain Disruptions | -1.2% | Regional, with acute impact on Italy and Germany | Medium term (2-4 years) |

| Fluctuating Raw Material Prices | -0.6% | Regional, particularly affecting leather and textile segments | Short term (≤ 2 years) |

| Rising Trade Barriers and Tariffs | -1.1% | EU-US trade corridor, broader global impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit Products

Counterfeiting inflicts substantial damage on the fashion industry, as evidenced by the European Union Intellectual Property Office's (EUIPO) January 2024 report, which revealed annual losses of EUR 16 billion across Europe's clothing, cosmetics, and toy sectors, representing 5.2% of their total revenue [3]Source: European Union Intellectual Property Office, “Counterfeit goods cost EU industries billions of euros and thousands of jobs annually,” euipo.europa.eu .The proliferation of lower-priced counterfeit items appeals to cost-conscious consumers, weakening the market position of authentic luxury brands and diminishing their long-term brand equity. The challenge intensifies as counterfeit operations establish production facilities near target markets and employ advanced manufacturing methods that blur the distinction between genuine and fake products, thereby impeding market growth. The rise of e-commerce platforms has further complicated this issue, providing counterfeiters with additional channels to distribute their products while making it increasingly difficult for consumers to verify product authenticity. Additionally, the financial impact extends beyond direct sales losses, as legitimate brands must allocate significant resources to anti-counterfeiting measures and legal actions to protect their intellectual property rights.

Supply Chain Disruptions

Red Sea shipping disruptions have created significant inflationary pressures across European fashion supply chains, particularly affecting Italy's fashion sector, which heavily depends on Asian fiber and fabric imports worth over EUR 50 billion annually. The OECD projects these disruptions could contribute an additional 0.4 percentage points to consumer price inflation, affecting accessories pricing and consumer demand [4]Source: Organisation for Economic Co-operation and Development, “OECD Economic Outlook 2024,” oecd.org . Thesituation is particularly challenging for the accessories segment due to its complex supply chains spanning multiple countries for different components. While European brands are increasingly adopting nearshoring strategies to establish production facilities closer to consumption markets, the transition requires substantial investment and time to develop local manufacturing capabilities that can match the cost efficiencies of established Asian supply networks. The extended shipping times and increased freight costs have forced many fashion brands to maintain higher inventory levels, impacting their working capital and operational efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Dominance Faces Watch Innovation

Apparel dominates the market with a 59.02% share in 2025, driven by athleisure trends and seasonal refresh cycles that generate consistent purchases across price segments. The footwear segment benefits from sneaker culture and performance-fashion convergence, while watches demonstrate the highest growth potential at 5.78% CAGR through 2031, combining traditional craftsmanship with smart technology. Handbags maintain premium positioning despite slower volume growth, and wallets adapt to digital payment trends through multi-functional designs.

The accessories market continues to evolve with changing consumer preferences, where jewelry shows resilience through investment appeal and personalization trends, including the rise of lab-grown diamonds and sustainable materials. Sunglasses maintain year-round relevance beyond seasonal utility, exemplified by successful collaborations like Saint Laurent x Ray-Ban. This transformation reflects broader lifestyle changes where accessories serve both functional and identity expression purposes, with technology integration enabling premium pricing and differentiation across all categories.

By Category: Mass Market Stability Versus Premium Growth

Mass category accessories dominate with a 63.92% market share in 2025, leveraging established retail networks and price-sensitive consumer segments to maintain volume stability. However, premium segments are growing at a 6.45% CAGR through 2031, driven by consumers' willingness to invest in quality, sustainability, and brand prestige. This market bifurcation creates strategic challenges for mid-market brands, which face increasing pressure from both value competitors and accessible luxury alternatives.

The growth in premium accessories is underpinned by consumers viewing high-quality items as long-term investments that maintain value while providing emotional satisfaction. Meanwhile, mass market players focus on rapid product cycles and value engineering to capture fashion trends at accessible price points. Both segments approach sustainability differently - premium brands emphasize craftsmanship and durability, while mass market manufacturers incorporate recycled materials and circular business models to meet regulatory requirements and consumer expectations.

By End User: Women Lead While Children Accelerate

Women constitute 53.11% of market demand in 2025, demonstrating higher consumption rates across handbags, jewelry, and fashion accessories. While men's accessories gain momentum through expanding fashion consciousness and evolving workplace dress codes, the kids/children segment shows the strongest growth potential with a 6.14% CAGR through 2031, driven by early luxury exposure and parents' investment in quality accessories for special occasions.

Generational preferences significantly influence product development, with Generation Z prioritizing sustainable materials and authentic brand narratives while maintaining luxury aspirations. This shift aligns with broader demographic trends, particularly in the children's segment, where delayed parenthood among affluent consumers who focus spending on fewer children creates opportunities for premium positioning in traditionally value-oriented categories.

By Distribution Channel: Offline Resilience Meets Digital Growth

Offline stores continue to dominate the accessories market with a 65.98% share in 2025, highlighting consumers' preference for physical retail experiences where they can touch products and receive personalized service. While online channels are projected to grow at 6.86% CAGR through 2031, this represents a complementary shift rather than a replacement, as successful brands integrate digital capabilities with traditional retail to enhance the overall shopping experience.

The retail landscape is evolving through technological integration, with e-commerce platforms implementing virtual try-on features, augmented reality tools, and social commerce capabilities to improve online engagement. Physical stores are simultaneously transforming into experiential spaces that prioritize brand storytelling and customer interaction. Despite accelerated digital adoption during the pandemic, the tactile nature of accessories and their significance in gift-giving maintain the relevance of brick-and-mortar locations, particularly in luxury and premium segments where personalized service remains a crucial component of the purchase journey.

Geography Analysis

The United Kingdom dominates with a 16.63% market share in 2025, leveraging London's position as a global fashion capital and its robust luxury retail infrastructure. The UK market demonstrates resilience through its high-net-worth consumer base and established shopping districts that drive tourist spending, while successfully adapting to post-Brexit trade adjustments through modified supply chains and pricing strategies.

Spain leads market growth with a projected 7.25% CAGR through 2031, driven by tourism recovery and increasing domestic affluence. This growth complements the established markets of Germany, France, and Italy, where strong economic fundamentals, heritage luxury brands, and manufacturing excellence continue to shape the accessories landscape, despite challenges like Red Sea shipping disruptions affecting Italian supply chains.

The market further diversifies through emerging opportunities in the Netherlands, Poland, Belgium, and Sweden. Poland's increasing leather accessories imports, the Netherlands' advanced e-commerce adoption, Belgium's luxury retail expertise, and Sweden's sustainability leadership collectively contribute to the market's evolution and growth potential.

Competitive Landscape

The European fashion accessories market demonstrates moderate fragmentation, with established luxury conglomerates like LVMH, Kering, and Richemont dominating premium segments through brand portfolio diversification and vertical integration. Mid-market players face increasing competition from direct-to-consumer brands that bypass traditional retail markups, while emerging disruptors gain market share through sustainability positioning and digital-native strategies, particularly among younger demographics who prioritize brand values over heritage.

Technology adoption has become a crucial differentiator in the market, with companies investing in blockchain authentication, AI-powered personalization, and augmented reality experiences to enhance customer engagement and operational efficiency. Strategic partnerships between fashion brands and technology companies are increasingly important for innovation, enabling the combination of traditional craftsmanship with modern capabilities to create distinctive value propositions.

The market is experiencing significant changes in retail strategy and distribution models. The emergence of rental and resale platforms presents both challenges and opportunities, requiring brands to balance exclusivity with accessibility while addressing circular economy demands. Companies continue to expand their physical retail presence, as exemplified by Birkenstock's new store opening on King's Road in Chelsea, London in March 2025, which focuses on providing comprehensive product experiences to customers.

Europe Fashion Accessories Industry Leaders

Inditex SA

Kering SA

Richemont SA

Chanel SA

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bagzone Lifestyles Pvt. Ltd. launched Akiki London, a luxury handbag brand. The brand integrates London's cultural elements with craftsmanship from European and Asian artisans, emphasizing personalized design aesthetics.

- May 2025: Huawei unveiled its “Fashion Next” collection in Berlin, headlined by the HUAWEI WATCH 5 with enhanced interaction features that bridge fashion and technology.

- February 2025: Steve Madden completed the acquisition of Kurt Geiger, strengthening its European luxury footwear footprint and expanding distribution channels across the United Kingdom.

- December 2024: Marks & Spencer broadened its collaboration with First Insight to accelerate digital transformation and improve customer centricity across all clothing lines.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Europe's fashion accessories market as yearly retail and wholesale revenue from newly manufactured personal adornment items, jewelry, watches, handbags, small leather goods, belts, hats, eyewear, scarves, and sport-inspired add-ons, purchased by men, women, and children across every price tier in the 27 EU members plus the United Kingdom, Norway, and Switzerland. According to Mordor Intelligence, the base-year 2024 market totals USD 665.6 billion and is forecast through 2030.

Scope exclusion: Pre-owned, rental, and purely virtual accessories are excluded.

Segmentation Overview

- By Product Type

- Footwear

- Apparel

- Wallets

- Handbags

- Watches

- Sunglasses

- Jewelery

- By End User

- Men

- Women

- Kids/Children

- By Category

- Mass

- Premium

- By Distribution Channel

- Offline Stores

- Online Stores

- By Geography

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with brand merchandisers, department-store buyers, third-party logistics providers, and leading e-tail platforms in France, Italy, Germany, Spain, and the Nordics. These discussions refined average selling prices, re-export ratios, and online share, letting us confirm or adjust desk findings.

Desk Research

We opened our work with Eurostat retail indices, UN Comtrade import flows, EUIPO counterfeit-seizure logs, and ECB consumer-spend lines that fix volume and price corridors. Trade bodies such as CEC and the Fédération de la Haute Couture et de la Mode, brand 10-Ks, and news drawn through Dow Jones Factiva clarified channel mix. Questel patent trends and supplier ledgers in D&B Hoovers added technology and cost context. The sources listed are illustrative; many other public and subscription materials supported evidence collection and cross-checks.

Market-Sizing & Forecasting

We rebuild totals with a top-down lens that starts from household apparel and footwear outlay and landed accessory imports, then aligns for penetration. Selected bottom-up checks, supplier revenue roll-ups and sampled online orders, reconcile outliers before a single baseline is locked. Tourist arrivals, luxury price indices, online fashion share, counterfeit seizures, extended producer responsibility fees, and disposable income per head feed a multivariate regression and scenario analysis to 2030; any gaps are bridged with weighted regional proxies vetted during expert calls.

Data Validation & Update Cycle

Outputs clear peer review, variance tests against historic series, and currency audits. Models refresh each year, with interim updates when tariff shifts or comparable shocks occur, and a final analyst sweep precedes release.

Why Mordor's Europe Fashion Accessories Baseline Earns Trust

Published estimates differ because firms choose dissimilar product baskets, convert currencies in varying ways, and refresh on uneven cadences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 665.6 B (2025) | Mordor Intelligence | - |

| USD 236.7 B (2024) | Regional Consultancy A | Omits footwear add-ons; FX fixed at 2023 average |

| USD 183.4 B (2024) | Industry Analytics B | Counts direct-to-consumer online only; drops duty-free and wholesale |

The contrasts show how tighter scopes and lighter validation compress values, whereas our disciplined variable selection, annual refresh, and multi-source triangulation give decision-makers a dependable, transparent baseline.

Key Questions Answered in the Report

What is the current value of the European fashion accessories market?

The market is valued at USD 702.25 billion in 2026 and is projected to grow at a 5.51% CAGR to 2031.

Which product category holds the largest share?

Apparel leads with 59.02% of 2025 revenue due to constant wardrobe refresh cycles and athleisure popularity.

Which segment is forecast to grow the fastest?

Watches are expected to register the highest 5.78% CAGR through 2031, fuelled by smart-analog hybrids.

What role do online channels play in accessories sales?

Online accounted for 34.02% of 2025 sales and is set to rise at a 6.86% CAGR, complementing physical stores rather than replacing them.

Which country is the biggest market within Europe?

The United Kingdom holds 16.63% share thanks to London’s luxury retail concentration and resilient affluent consumer base.

How are brands mitigating supply chain disruptions?

Firms accelerate near-shoring to Eastern Europe, invest in digital inventory visibility and diversify suppliers to cushion freight volatility.

Page last updated on: