Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 29.78 Billion |

| Market Size (2031) | USD 38.49 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

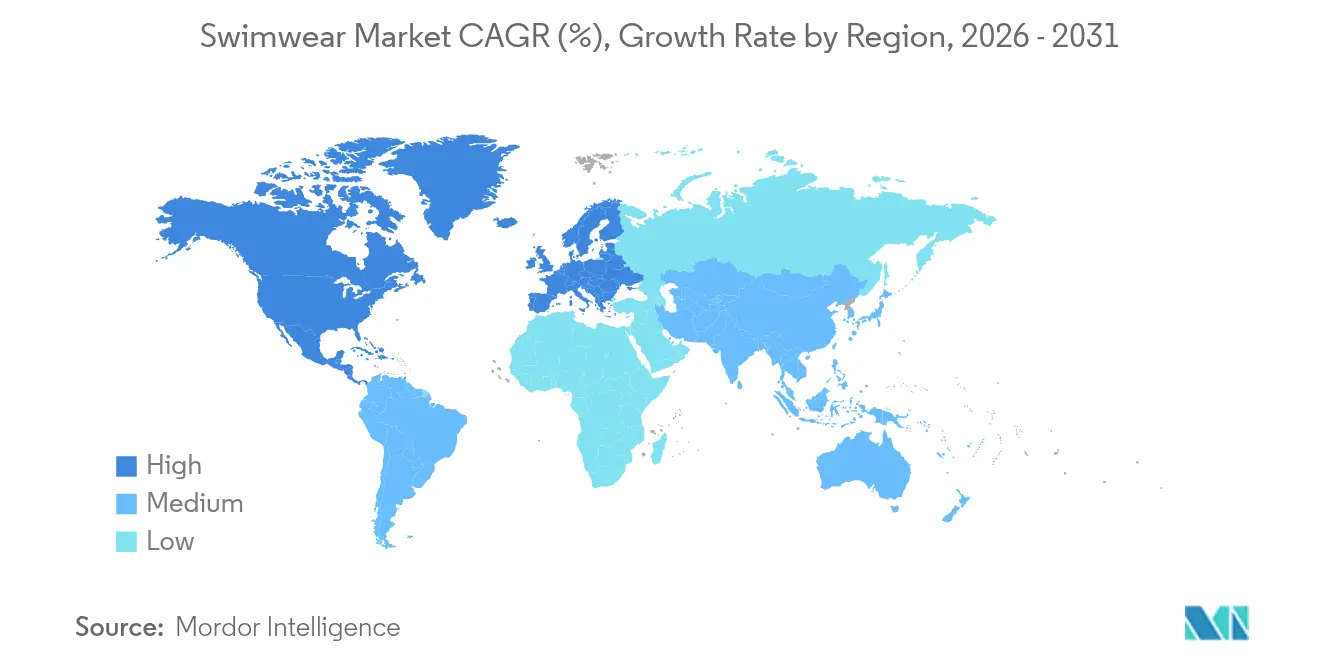

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

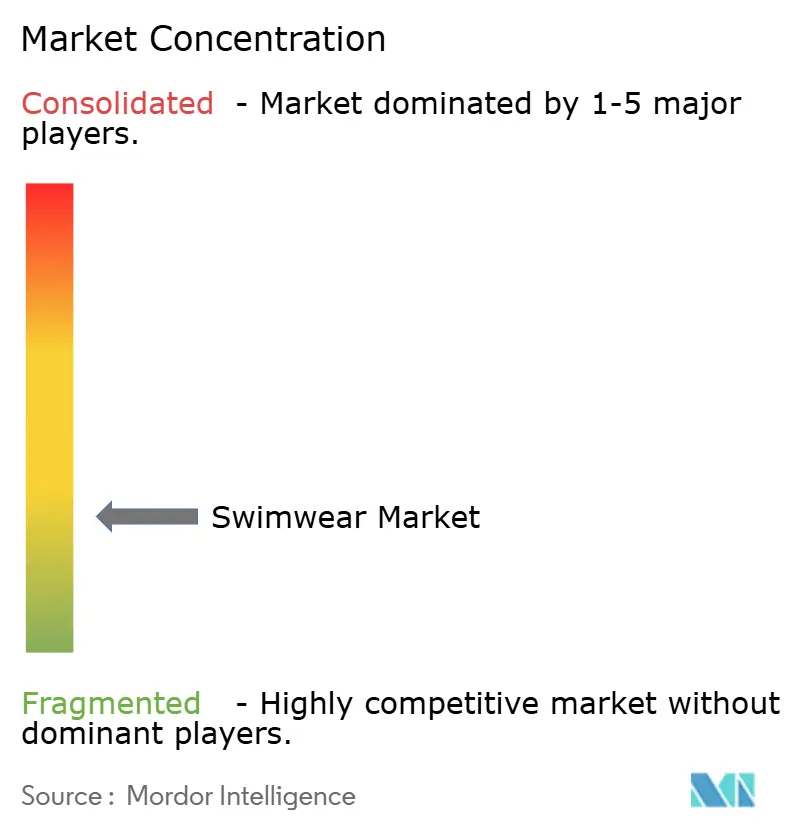

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Swimwear Market Analysis by Mordor Intelligence

The swimwear market size was valued at USD 28.29 billion in 2025 and estimated to grow from USD 29.78 billion in 2026 to reach USD 38.49 billion by 2031, at a CAGR of 5.27% during the forecast period (2026-2031). This growth is buoyed by wellness tourism, year-round aquatic programs, and breakthroughs in material science, turning eco-friendly fibers into top-tier fabrics. A March 2025 survey by the European Travel Commission revealed that 16% of European travelers favored Spain as their top sun and beach holiday destination. Brands merging recycled yarns with inclusive sizing are now gracing mainstream shelves, not just niche corners[1]Source: European Travel Commission, "Monitoring Sentiment for Intra-European Travel", www.etc-corporate.org. Meanwhile, savvy inventory planning is helping retailers navigate seasonality challenges. In Europe and select U.S. states, regulatory backing is fast-tracking the adoption of recycled yarns. Furthermore, public investments in pools and waterfronts are broadening demand, reaching beyond the usual coastal hotspots.

Key Report Takeaways

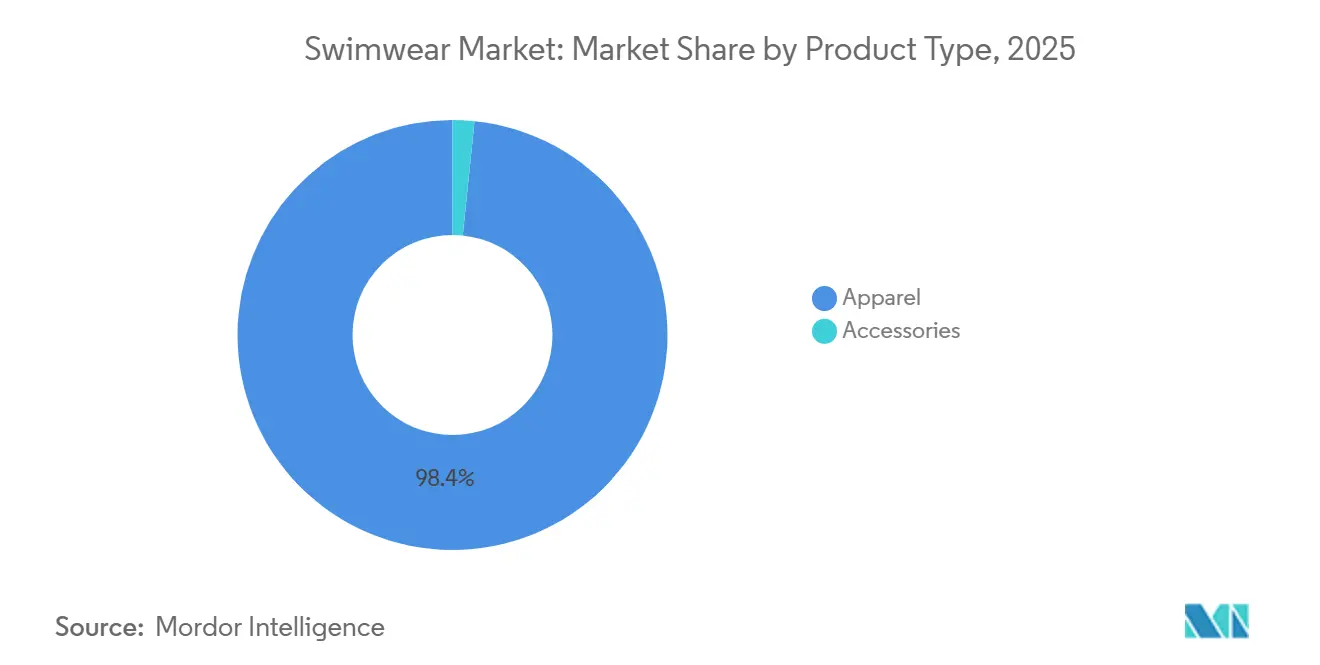

- By product type, apparel led with 98.37% revenue share in 2025; accessories are projected to advance at a 5.57% CAGR through 2031.

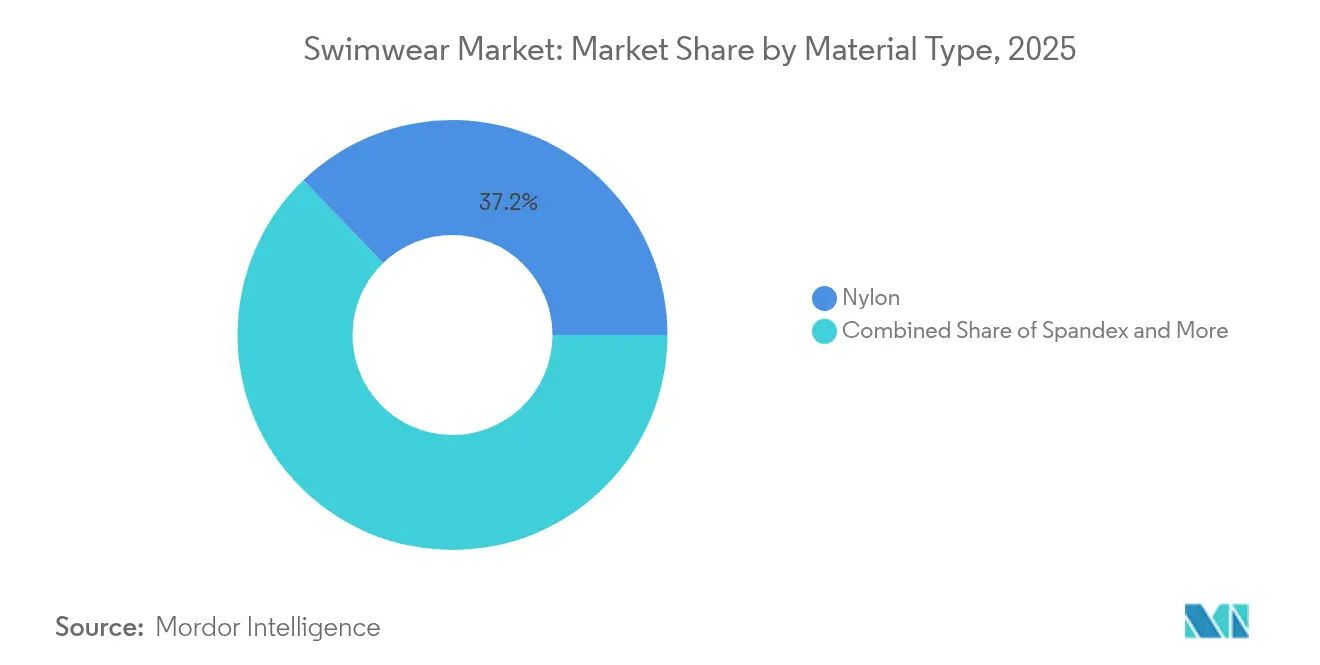

- By material, nylon captured 37.22% of the swimwear market share in 2025, while spandex is forecast to expand at a 6.07% CAGR.

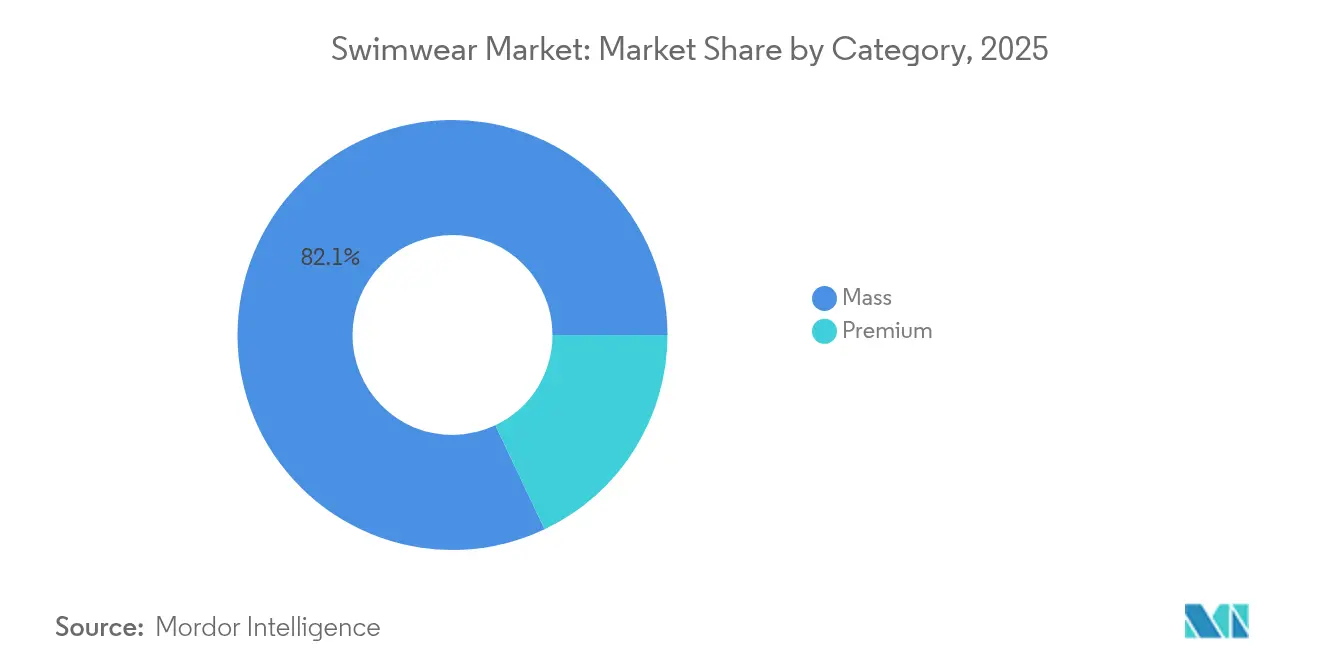

- By category, the mass market accounted for 82.05% of the swimwear market size in 2025; the premium segment is growing at a 6.22% CAGR to 2031.

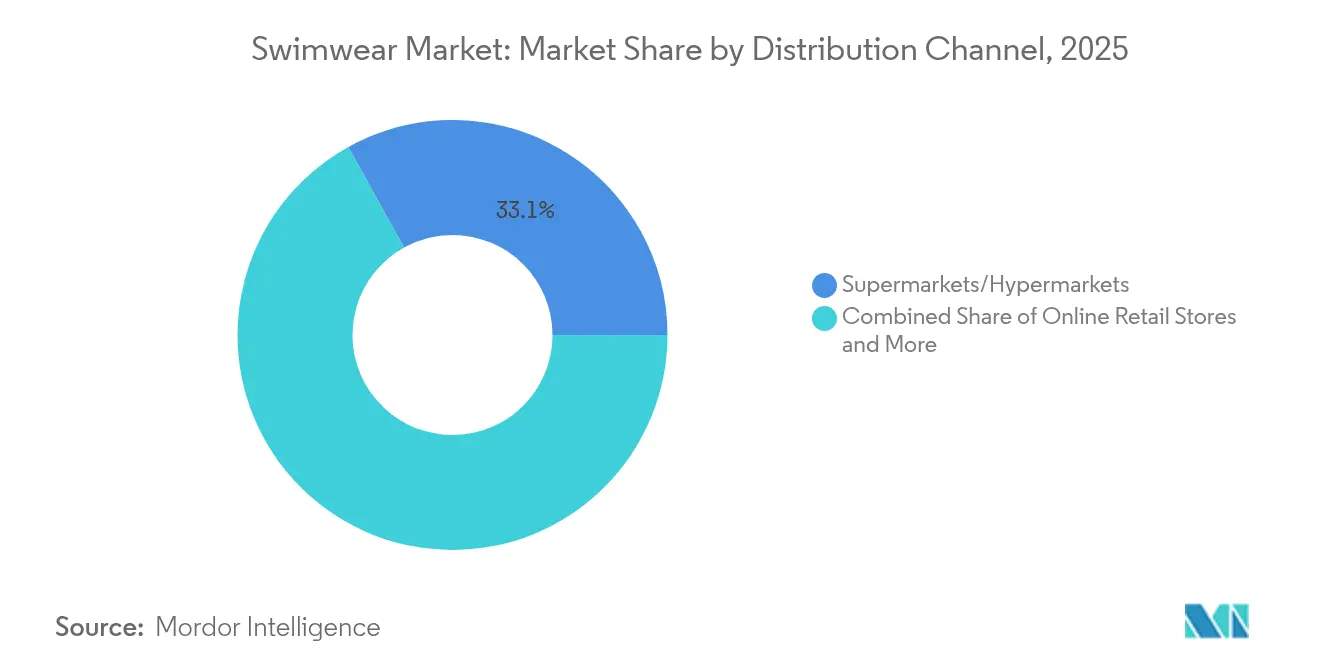

- By distribution channel, supermarkets and hypermarkets held a 33.05% share of the swimwear market in 2025, whereas online retail stores recorded the highest projected CAGR at 7.58%.

- By geography, North America controlled 32.21% revenue in 2025; Asia-Pacific is the fastest-growing region, poised for a 6.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Swimwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Popularity of Recreational Water Activities | +0.8% | Global, with concentrated impact in North America and Europe | Medium term (2-4 years) |

| Technological Innovations in Fabrics | +0.9% | Global, led by Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Expansion of Water Sports and Leisure Facilities | +0.7% | North America and Europe are primary, Asia-Pacific is emerging | Medium term (2-4 years) |

| Advances in Swimwear Technology | +0.6% | Global, with research and development concentrated in developed markets | Long term (≥ 4 years) |

| Rise of Athleisure and Multifunctional Swimwear | +0.5% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Innovative and Fashion-Forward Designs | +0.4% | Global, with luxury segment leadership in Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Recreational Water Activities

In January 2024, New York unveiled its USD 150 million NY SWIMS initiative, marking the most significant public swimming investment since the New Deal era. This initiative underscores the government's ongoing commitment to making aquatic recreation more accessible. The funding is directed towards 37 projects in underserved communities, tackling challenges like facility construction and the historical shortage of lifeguards, both of which have hindered participation rates. Scandinavian cities are reimagining their urban water infrastructure, turning former industrial harbors into vibrant swimming venues. Copenhagen's harbor swimming initiatives, for instance, not only draw in residents and tourists but also spur a fresh demand for inclusive swimwear designs. Data from the Sports and Fitness Industry Association reveals a rise in water sports participation among Americans, jumping from 15.7% in 2023 to 16.5% in 2024[2]Source: Sports & Fitness Industry Association, "2025 Sports, Fitness, and Leisure Activities Topline Participation Report", sfia.users.membersuite.com. Urban planning is increasingly prioritizing community-centric recreational opportunities, a shift that's paralleled by a surge in swimwear consumption in cities. This trend isn't confined to traditional beach locales; even inland cities are crafting artificial beaches and swimming complexes. Moreover, by embedding aquatic facilities within mixed-use developments, the industry is witnessing a stabilization of seasonal demand fluctuations, leading to a more consistent year-round market.

Technological Innovations in Fabrics

Driven largely by applications in swimwear and sportswear, the demand for spandex fiber is accelerating, mirroring a broader evolution in performance textiles. Today, about 80% of apparel in the U.S. features spandex, showcasing its adoption beyond just athletic wear. Addressing environmental concerns without compromising on performance, sustainable innovations have emerged, such as LYCRA EcoMade fiber, crafted from renewable materials, and ECOModa-100, derived from recycled spandex waste. In a bid to lessen environmental footprints, companies like Hyosung TNC are channeling investments into biobased production methods, viewing sustainability as a competitive edge rather than mere compliance. Furthermore, the integration of smart textiles in swimwear is revolutionizing the industry, offering features like real-time monitoring, intelligent drag reduction, and energy harvesting. This evolution is shifting swimwear's role from passive clothing to active performance enhancers. Brands that are willing to delve into advanced material science research and development stand to gain a unique edge, as the fusion of sustainability and performance carves out distinct differentiation opportunities.

Expansion of Water Sports and Leisure Facilities

Aquatic infrastructure development now spans beyond just traditional swimming pools. It includes adventure sports facilities, therapeutic wellness centers, and multi-generational recreational complexes. By integrating splash pads, playgrounds, and educational programming, swimming facilities are evolving into comprehensive destinations. This evolution not only drives longer visits but also boosts household swimwear purchases. Responding to demographic shifts favoring active aging and family-centric recreation, private sector investments in water sports facilities are on the rise. These facilities are increasingly designed for accessibility, catering to diverse age groups and physical capabilities. Recognizing the link between aesthetic environments and consumer spending, operators are influenced by resort wear trends in their facility designs. The growth of indoor aquatic centers allows for year-round programming, helping to stabilize demand fluctuations that have historically affected swimwear retailers and manufacturers. As reported by the Russian Federal State Statistics Service, Russia boasted over 6,700 swimming pools in 2023, with numbers steadily climbing over the past decade[3]Source: Russian Federal State Statistics Service, "Russian Statistical Yearbook 2024", ssl.rosstat.gov.ru. Specialized therapeutic and rehabilitation swimming programs are carving out niche market segments, driving demand for adaptive swimwear designs, and fueling growth in the inclusive swimwear category.

Advances in Swimwear Technology

Performance enhancement technologies, once exclusive to competitive swimming, are now making waves in recreational markets. Features like chlorine-resistant fabrics, UV protection ratings, and compression attributes have transitioned from luxury to standard. Smart textiles are revolutionizing swimwear, embedding sensors for stroke analysis, heart rate monitoring, and water temperature tracking, effectively turning swimwear into a wearable tech platform. Innovations in drag reduction, initially crafted for competitive swimmers, are now finding their way into recreational products, underscoring a consumer trend willing to pay a premium for enhanced performance. Fabric treatments that offer quick-dry properties, antimicrobial protection, and color retention not only address practical concerns but also extend product lifecycles and reduce the frequency of replacements. The fusion of sustainable materials with performance technologies is reshaping the industry's approach, challenging the age-old trade-offs between environmental responsibility and functional excellence. Ongoing research into bio-based performance fibers and closed-loop recycling systems signals a commitment to long-term sustainability, ensuring that technical specifications for aquatic applications remain uncompromised.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeiting and Grey Market Products | -0.9% | Global, concentrated in the luxury segments | Short term (≤ 2 years) |

| Raw Material Cost Volatility | -0.7% | Global, with manufacturing concentration in the Asia-Pacific | Medium term (2-4 years) |

| Seasonal Demand Fluctuations | -0.5% | Northern Hemisphere markets primarily | Short term (≤ 2 years) |

| Intense Competition and Brand Saturation | -0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeiting and Grey Market Products

Counterfeiting and grey market products harm the global swimwear market by eroding consumer trust, damaging brand reputations, and causing financial losses to legitimate businesses. Counterfeit swimwear, sold through unauthorized channels and online platforms, creates unfair competition with low-priced replicas that undermine authentic products. These knock-offs, often of inferior quality and non-compliant with safety standards, risk consumer safety and diminish the appeal of luxury swimwear. Grey market trading disrupts distribution channels, causing regional price inconsistencies and confusion for retailers and consumers. A January 2024 EUIPO study revealed intellectual property violations cost the EU clothing sector nearly EUR 12 billion annually, 5.2% of legitimate sales, and 160,000 jobs. Luxury swimwear brands, with higher profit margins and brand recognition, are prime targets for counterfeiters. In May 2025, the European Anti-Fraud Office (OLAF) seized over 1.8 million counterfeit fashion items, including swimwear, across the EU. Sustainable swimwear lines, like Nike's Icon Collection in 2021 and others using ECONYL regenerated nylon yarn, face competition from non-eco-friendly counterfeits online. These illicit markets divert sales from ethical manufacturers, forcing brands to invest heavily in brand protection and authentication technologies to safeguard intellectual property and rebuild consumer trust.

Raw Material Cost Volatility

Disruptions in the textile supply chain are exacerbating traditional commodity price fluctuations. U.S. tariffs are adding further cost pressures on swimwear manufacturers who depend on imported materials. Starting April 2025, a universal 10% import tariff will come into effect. This, alongside country-specific increases targeting major textile exporters, is set to alter global sourcing strategies and pricing structures. Vietnam's tariffs are set to surge from 4.82% to 50.82%, and China's will jump from 4.4% to 38.4% as of May 2025. These hikes compel manufacturers to either scout for alternative sourcing regions or absorb the heightened costs, which in turn, squeeze profit margins. The cotton supply chain grapples with challenges stemming from extreme weather events, trade disputes, and stringent sustainability regulations. These regulations, especially those addressing forced labor concerns, are notably impacting regions like Xinjiang, China. Transparency mandates and sustainability regulations, rolled out by the EU and U.S., are inflating compliance costs. However, they also bestow a competitive edge upon vertically integrated manufacturers boasting traceable supply chains. The volatility in raw material prices is complicating inventory management for manufacturers. They find themselves in a delicate dance, trying to optimize costs while navigating the uncertainties of demand in seasonal markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel's Dominance Drives Innovation

In 2025, apparel captured a commanding 98.37% share of the market, underscoring its broad appeal across competitive, recreational, and fashion segments. The accessories category, encompassing items like cover-ups, beach bags, and protective gear, is the fastest-growing segment, boasting a 5.57% CAGR through 2031. This growth signals an expansion beyond core garments, enhancing average transaction values and deepening customer engagement. While men's swimwear enjoys steady demand for both athletic and leisure purposes, kids' swimwear sees a boost from rising participation in swimming programs and family aquatic activities. Women's competitive swimwear leads the charge in integrating smart textiles, with features like performance monitoring sensors and UV exposure tracking soon making their way to recreational and men's swimwear.

Across all categories, inclusive swimwear design principles are gaining traction. By incorporating adaptive features for diverse body types and physical capabilities, brands are broadening their market reach beyond conventional demographics. As swimwear increasingly doubles as resort wear, product development is evolving, catering to its growing role in various social and recreational settings. Demand patterns fluctuate by product type: women's fashion swimwear hits pronounced seasonal peaks, whereas men's and children's swimwear, driven by athletic and educational needs, enjoy steadier year-round demand.

By Material Type: Sustainability Reshapes Fiber Selection

In 2025, nylon commands a 37.22% market share, lauded for its durability and cost-effectiveness. Meanwhile, spandex is on a rapid ascent, boasting a 6.07% CAGR, fueled by rising performance demands and comfort preferences. Innovations in sustainable materials are reshaping traditional fiber choices. Alternatives like recycled nylon and bio-based spandex are carving out a niche in the market, even with their premium price tags. Leading the charge in sustainable material adoption, Europe showcases ECONYL, a recycled nylon sourced from fishing nets and carpet waste, exemplifying circular economy principles without compromising on performance. While polyester is celebrated for its quick-dry and UV protection features, the fabric landscape is also witnessing a surge in bio-based fibers and smart textiles embedded with advanced functionalities.

Brand positioning is increasingly dictating material choices. Premium segments are gravitating towards sustainable and high-performance fibers, whereas the mass market is striking a balance between cost and functionality. However, integrating recycled content isn't without challenges; it demands tweaks in the supply chain and rigorous quality control. Yet, those manufacturers who invest in sustainable sourcing find themselves with a competitive edge. Spandex's rising demand isn't just a trend; it's a reflection of the broader athleisure movement. Swimwear designs now prioritize stretch and recovery, making them versatile for both aquatic and terrestrial activities.

By Category: Premium Growth Accelerates

In 2025, the mass market category commands a dominant 82.05% share, underscoring its price sensitivity and global accessibility. Meanwhile, premium segments are on a growth trajectory, boasting a 6.22% CAGR through 2031. This surge is fueled by a focus on sustainability, innovative performance, and brand strategies that command higher prices. Consumers are increasingly willing to pay a premium for sustainable materials, ethical manufacturing, and superior functionality, presenting lucrative opportunities for brands in the premium segment. This shift from mass to premium underscores a broader consumer trend prioritizing quality over quantity. Here, longer product lifecycles and less frequent replacements justify the initial higher costs.

Growth in the premium category is predominantly seen in developed markets, where disposable incomes are higher and environmental consciousness is pronounced. In contrast, the mass market continues to flourish in emerging economies, buoyed by a burgeoning middle class. Premium products, now infused with tech features and sustainable materials, stand out in the market, bolstering both profit margins and brand loyalty. Distribution strategies diverge by category: premium brands lean towards direct-to-consumer channels and immersive retail experiences, whereas mass market products anchor themselves in traditional retail partnerships, often competing on price.

By Distribution Channel: Digital Commerce Transformation

In 2025, supermarkets and hypermarkets command a 33.05% market share, leveraging broad accessibility and seizing impulse purchase opportunities. Meanwhile, online retail stores are on a growth trajectory, boasting a 7.58% CAGR, underscoring the rising tide of digital commerce adoption and direct-to-consumer strategies. Specialty stores carve out their niche, offering expert consultations and fitting services, a crucial touchpoint for the performance and premium swimwear segments. The online retail surge is fueled by expanded size ranges, cutting-edge virtual fitting technologies, and tailored recommendations, all addressing the age-old challenges of swimwear shopping. Beyond the mainstream, alternative distribution channels like resort retail, pop-up stores, and subscription services emerge, broadening avenues for customer engagement and acquisition.

Digital commerce shatters geographic barriers, granting specialized brands, especially those championing sustainable or inclusive designs, unfettered global market access. Augmented reality fitting tools and size recommendation algorithms seamlessly integrate into the online shopping experience, alleviating concerns tied to swimwear purchases. Omnichannel strategies shine by marrying online discovery with in-store fulfillment, striking a balance between inventory optimization and customer convenience. Social media's pervasive influence redefines distribution channels, morphing them into potent marketing platforms. Here, influencer collaborations and user-generated content play pivotal roles, swaying purchase decisions across diverse demographic segments.

Geography Analysis

In 2025, North America accounted for 32.21% of global revenue, buoyed by a strong indoor-aquatic infrastructure, a surge in resort tourism in Florida and the Caribbean, and a notable demand for inclusive swimwear catering to adaptive sports. The U.S. is actively piloting municipal grants to broaden pool access in low-income areas, creating a demand that spans both mass and premium price tiers. Meanwhile, Canada sees contributions from its youth swim initiatives, and Mexico capitalizes on cross-border shopping and resort retail.

Asia-Pacific emerges as the fastest-growing region, boasting a 6.34% CAGR. China's textile export prowess shines, with apparel shipments hitting USD 159.14 billion in 2024, ensuring global brands have a steady supply. India, eyeing USD 65 billion in textile exports by FY 26, is drawing investments into modern mills focused on recycled yarns, thanks to its Production-Linked Incentives. In Southeast Asia, tourism hotspots like Thailand and Indonesia see a retail boom during holidays, while Australia’s sun-safety mandates ensure UPF-rated garments are top of mind for consumers.

Europe stands at the crossroads of fashion heritage and eco-conscious leadership. Following the EU Green Deal's extended producer-responsibility schemes, Europe has fast-tracked recycled-fiber adoption, channeling research and developmen funds into circular design. While Germany and France lead in import volumes, Poland is witnessing a surge, thanks to its e-commerce boom. South America and the Middle East and Africa, though still emerging, show promise; Brazil's vibrant surf culture nurtures brand incubators, and Gulf nations are aligning swimwear purchases with their burgeoning water-park infrastructure.

Competitive Landscape

In the swimwear market, the landscape is moderately fragmented, with the top five players accounting for an estimated 35% of the market's revenue. Major athletic brands harness proprietary fabric labs to introduce lines that are both chlorine-proof and quick-drying. In contrast, luxury brands focus on limited-edition prints and artisanal details, appealing to affluent consumers. Meanwhile, mid-tier brands carve out their niche by using entirely recycled materials, being transparent about wage practices, and offering an inclusive size range from XXS to 6XL.

Investing in technology has become a pivotal focus. Pioneering brands are integrating Bluetooth stroke-count sensors and color-changing yarns that signal UV overexposure, setting a high bar for potential imitators. Brands selling directly to consumers harness data analytics to curate micro-collections tailored to regional preferences, streamlining the journey from design to store and minimizing surplus stock. Collaborations between fiber innovators and established brands expedite lab discoveries into market-ready products, exemplified by joint ventures exploring sugarcane-based elastane.

There's a noticeable uptick in mergers and minority acquisitions. Major athletic brands are snapping up boutique eco-labels to bolster their authenticity, while venture capitalists are pouring funds into startups championing algae-based polymers. Retailers are striking deals for exclusive capsule collections, ensuring foot traffic and fostering partnerships where design intellectual property is exchanged for prime store visibility. Service providers specializing in take-back and recycling services are capitalizing on extended producer responsibility regulations, cementing their role as vital partners in the shifting competitive landscape.

Swimwear Industry Leaders

-

Pentland Group PLC

-

Adidas AG

-

Puma SE

-

Nike Inc

-

Arena SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nike Swim unveiled its Spring/Summer 2025 collection, which features bold, modern, and sustainable offerings. The line included new lifestyle products made from recycled materials, emphasizing both style and eco-consciousness. The women's collection included one-piece, midkini, and bikini styles with vibrant colors and streetwear-inspired designs.

- April 2025: Canadian retailer Left launched its Spring 2025 collection, which featured elevated one-pieces and functional swimwear. The brand, known for its buttery-soft Italian fabric, introduced new styles with cool cutouts and flattering curvature. The collection also highlighted versatile designs that transition from the water to everyday wear.

- February 2024: Retailer Hunkemöller introduced its 2024 swimwear collection, which offered a wide array of bikini tops and bottoms. The collection included various styles like padded triangle tops, high-waist cheeky bottoms, and bandeau bikinis. It also featured shaping swimsuits and beachwear to cater to different customer preferences.

- January 2024: Calzedonia released its Swimwear 2024 collection, which included a range of bikinis, swimsuits, and beachwear cover-ups. The line focused on inclusive sizing and diverse cuts and colors. Key trends featured are shiny, crinkle, terrycloth, and crochet fabrics, as well as timeless classics and shaping options.

Global Swimwear Market Report Scope

A swimwear is a piece of clothing worn during water-based activities or sports, such as swimming or sunbathing.

The swimwear market is segmented by type, distribution channel, and geography. By product type, the market is segmented into women's swimwear, men's swimwear and goggles and swim caps. By distribution channel, the market is segmented into online stores and offline stores. The study also provides an analysis of the swimwear market in emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, and Middle-East and Africa.

For each segment, the market sizing and forecast have been done on the basis of value (in USD).

By Product Type

| Apparel | Swimsuits |

| Bikinis | |

| Tankinis | |

| Swim Trunks /Shorts | |

| Swim Briefs/Jammers | |

| Rash guards | |

| Others | |

| Accessories (Caps, Goggles, etc.) |

By Material Type

| Nylon |

| Polyester |

| Spandex |

| Other Fabric Types |

By Category

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Netherlands | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| New Zealand | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Apparel | Swimsuits |

| Bikinis | ||

| Tankinis | ||

| Swim Trunks /Shorts | ||

| Swim Briefs/Jammers | ||

| Rash guards | ||

| Others | ||

| Accessories (Caps, Goggles, etc.) | ||

| By Material Type | Nylon | |

| Polyester | ||

| Spandex | ||

| Other Fabric Types | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Netherlands | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| New Zealand | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the swimwear market?

The segment is valued at USD 29.78 billion in 2026.

How fast is the market expected to grow through 2031?

It is forecast to increase at a 5.27% CAGR, reaching USD 38.49 billion by 2031.

Which region shows the highest growth momentum?

Asia-Pacific leads with a projected 6.34% CAGR thanks to manufacturing expansion and urban leisure trends.

What material innovations dominate product development?

Recycled nylon and biobased spandex blends are at the forefront, balancing performance with lower environmental impact.

How are distribution channels shifting?

Online retail stores are expanding the fastest, supported by virtual fit technology and direct-to-consumer models.

Which category is gaining value fastest?

Premium swimwear lines are advancing at a 6.22% CAGR as consumers trade up for sustainability and performance features.

Page last updated on: