Admission Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

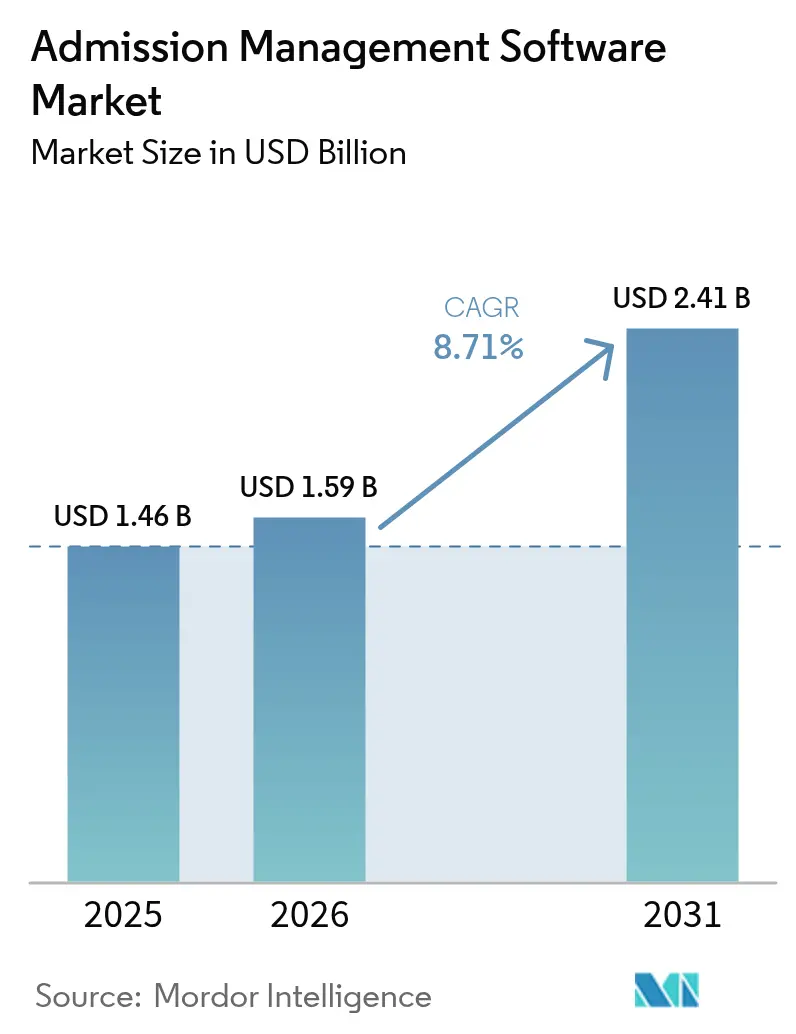

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 8.71% CAGR |

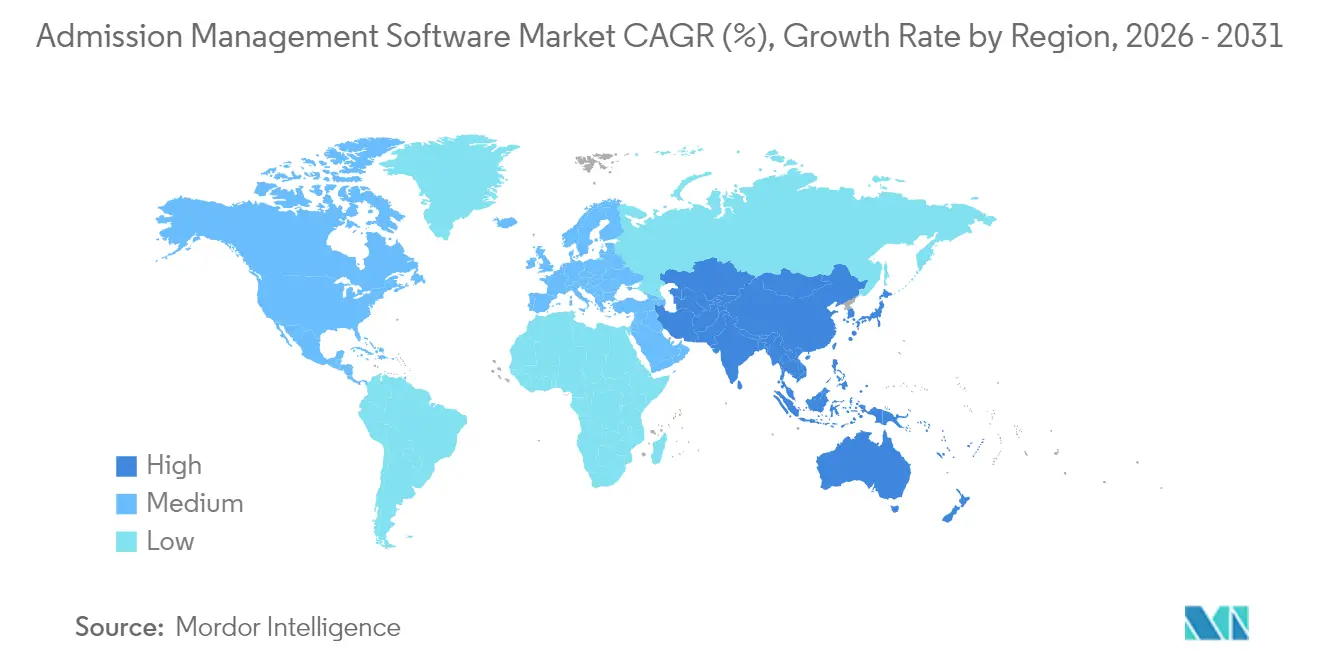

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

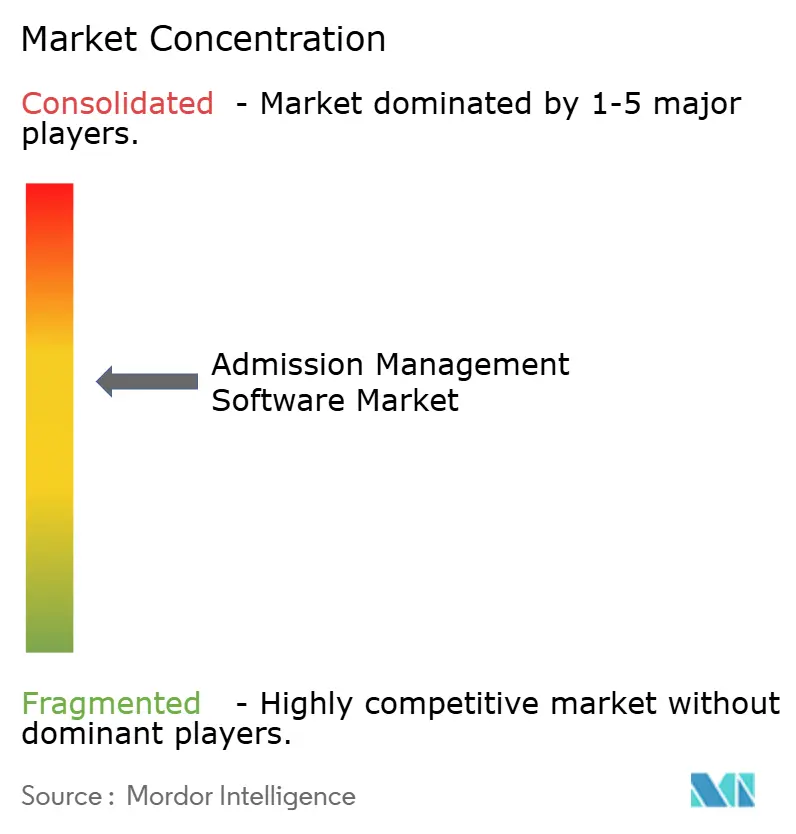

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Admission Management Software Market Analysis by Mordor Intelligence

The admission management software market size was valued at USD 1.46 billion in 2025 and estimated to grow from USD 1.59 billion in 2026 to reach USD 2.41 billion by 2031, at a CAGR of 8.71% during the forecast period (2026-2031). The market’s fast rise mirrors the shift from third-party cookies to first-party data, the race for real-time funnel insights, and cloud cost efficiencies that make large-scale click-stream ingestion affordable. Retail and e-commerce platforms are leading adopters because incremental conversion gains translate directly into revenue, while privacy regulations are prompting enterprises to modernize data-collection mechanisms. Intense competition is emerging between full-stack vendors that bundle analytics with broader cloud portfolios and specialist vendors focused on richer behavioural insights. The admission management software market is also shaped by talent shortages in event-stream engineering, pushing demand for managed services and low-code integration tools.

Key Report Takeaways

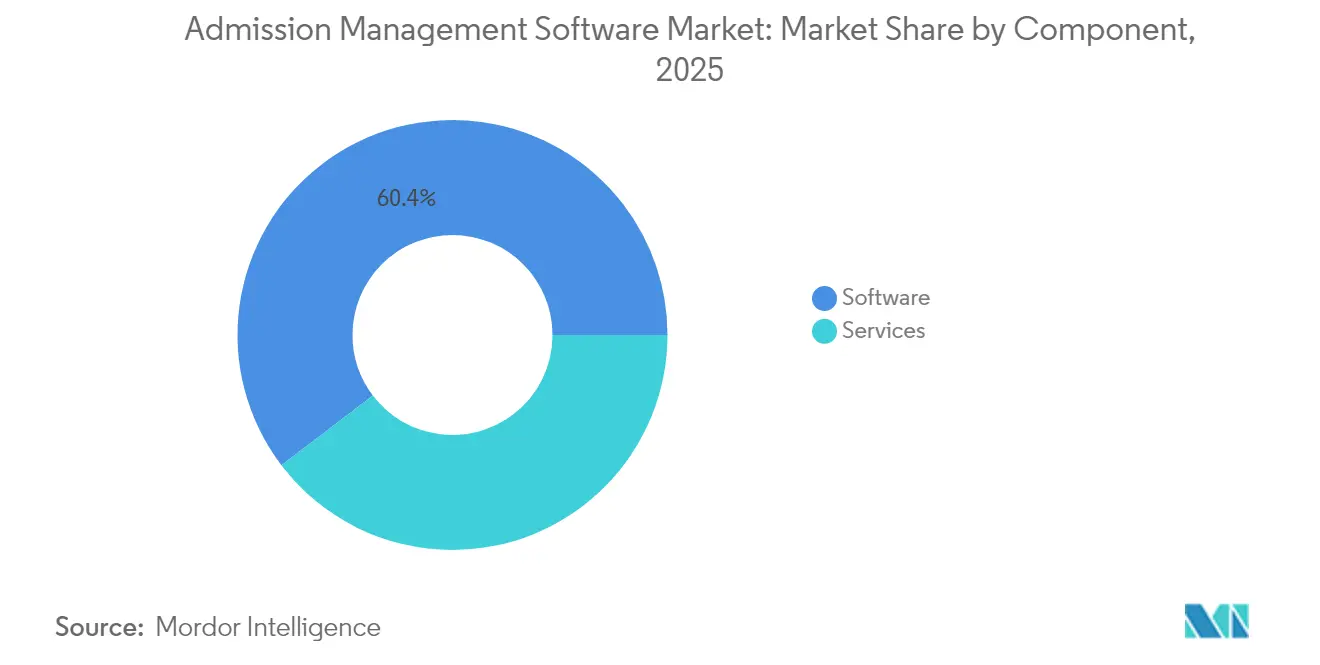

- By component, software led with 60.35% of the admission management software market share in 2025; services are on track for the fastest 13.05% CAGR to 2031.

- By deployment mode, the cloud segment accounted for 67.75% share of the admission management software market size in 2025 and is expanding at a 14.02% CAGR.

- By application, click path and website optimization held 38.10% revenue share in 2025, while customer analysis is advancing at 15.02% CAGR through 2031.

- By industry vertical, retail and e-commerce commanded 23.85% of the admission management software market size in 2025.

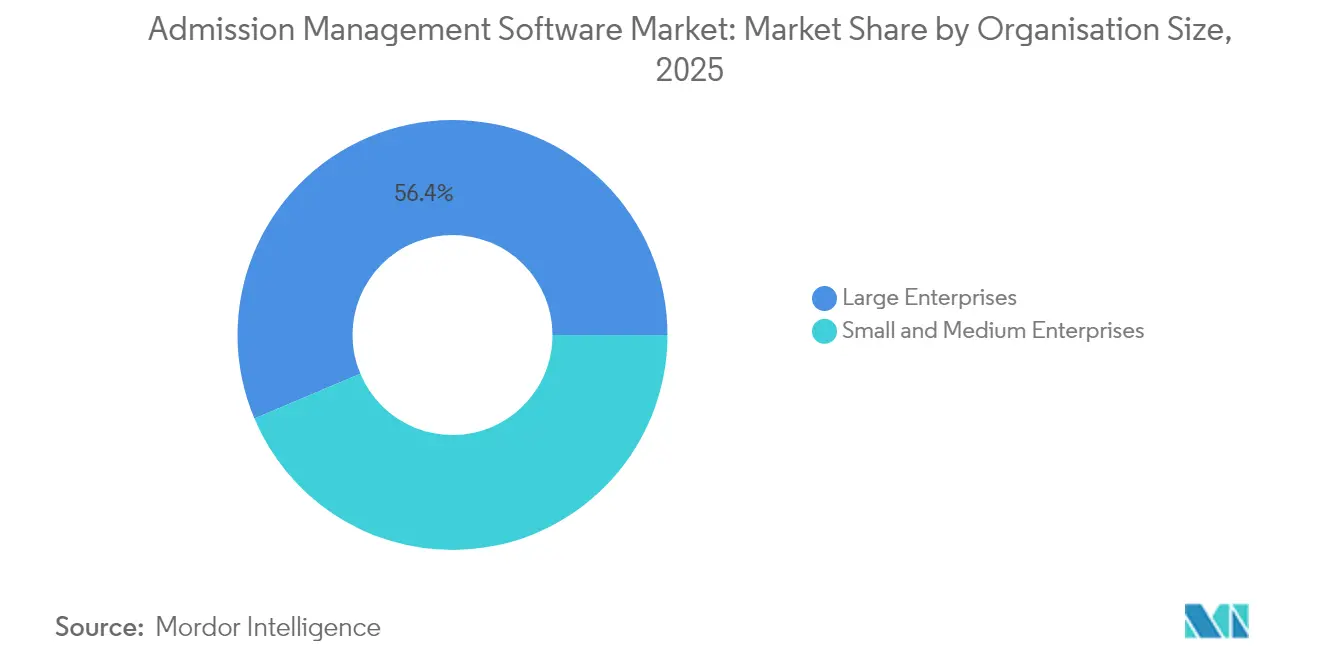

- By organization size, large enterprises controlled 56.35% share in 2025, whereas small and medium enterprises exhibit a 13.76% CAGR.

- By geography, North America captured 41.10% of 2025 revenue; Asia-Pacific is poised for a 15.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Admission Management Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phasing-out of third-party cookies | +2.1% | North America and EU lead, global spillover | Medium term (2-4 years) |

| Real-time personalisation for e-commerce | +1.8% | North America, APAC hubs | Short term (≤ 2 years) |

| Cloud cost efficiency for click-stream data | +1.4% | Global, pronounced in emerging markets | Medium term (2-4 years) |

| Digital-marketing ROI pressure | +1.2% | Primarily North America and EU | Short term (≤ 2 years) |

| Edge browser analytics (Wasm) | +0.9% | EU and California first movers | Long term (≥ 4 years) |

| Retail-media network monetisation | +0.8% | North America dominant, expanding to Europe and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Phasing-out of third-party cookies fuels first-party analytics

Google’s shifting cookie-deprecation schedule created a sense of urgency rather than relief. Enterprises that invested early in cookieless pipelines now highlight stronger consent compliance and richer first-party datasets, prompting competitors to accelerate similar upgrades. Vendors are embedding Privacy Sandbox workflows and customer data platforms into the admission management software market, enabling unified profiles across web, mobile and owned media. Early adopters anticipate smoother transitions as regulatory scrutiny intensifies.

E-commerce push for real-time personalization and conversion lift

Personalisation has become table stakes. Retailers report sales uplifts of about 20% when product recommendations react instantly to clicks, driving heavy demand for streaming analytics and low-latency decision engines. The admission management software market benefits because point-and-click tooling lets marketers launch dynamic offers without deep coding skills, while machine learning models surface next-best actions within milliseconds of each interaction.

Cloud cost efficiency enables massive click-data ingestion

Hyperscalers now offer consumption-based pricing tuned for stream processing, lowering unit costs for ingesting terabytes of event data. Mid-market firms that once settled for sampled datasets can afford full-fidelity tracking, unlocking granular behavioural insights. This cost shift underpins the admission management software market’s migration away from on-premises builds toward elastic, pay-as-you-go architectures that auto-scale with campaign peaks.

Digital-marketing ROI pressure drives journey analytics

With budgets scrutinised, marketers need proof that a given touchpoint produced incremental revenue. Cross-channel attribution stitched together by the admission management software market correlates spend to sales in near real time, guiding budget reallocations toward high-yield segments. Platforms integrate visual dashboards that translate complex pathing data into straightforward “what worked” narratives for executives.

Restraints Impact Analysis of Admission Management Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global privacy regulations | -1.6% | EU and California lead, worldwide adoption | Short term (≤ 2 years) |

| Integration complexity across tech stacks | -1.2% | Enterprise deployments worldwide | Medium term (2-4 years) |

| Browser anti-tracking (ITP, ETP) | -0.8% | Safari and Firefox user bases | Short term (≤ 2 years) |

| Scarcity of event-stream engineering talent | -0.7% | Most acute in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global privacy regulations tighten data collection

Nineteen US states added stricter consent mandates in 2025, while GDPR fines rose, forcing analytics pipelines to reduce personally identifiable data. Vendors that bundle automated consent management within the admission management software market gain favour, yet privacy filters remove some behavioural detail, limiting model accuracy and restraining overall CAGR.

Integration complexity across streaming stacks

Enterprises juggle legacy web-analytics tags, CRM data, and mobile SDKs. Harmonising schemas in real time requires scarce specialists adept at Kafka, Snowflake and micro-batch ETL tooling. Delayed implementations slow procurement cycles, though pre-built connectors and no-code transformation layers are easing the barrier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Admission Management Software Market Segment Analysis

By Component:

Services close the gap on softwareThe software segment held 60.35% of admission management software market share in 2025, underscoring the primacy of platforms that map every click to revenue outcomes. Yet services revenue is rising at a 13.05% CAGR because enterprises need hands-on help aligning data governance, privacy and machine-learning models with business goals. The admission management software market relies on integrators to orchestrate complex hybrid cloud topologies and fine-tune user-journey dashboards.

A second growth driver is changing management. Large rollouts often fail when end-users cannot interpret new metrics. Advisory partners therefore bundle enablement workshops, experimentation playbooks, and continuous optimisation audits. As privacy rules evolve, recurring compliance assessments expand services billings, narrowing the gap with pure-play licences.

By Deployment Mode:

Cloud cements supremacyCloud deployments captured 67.75% of admission management software market size in 2025 and are scaling at a 14.02% CAGR. Elastic compute absorbs traffic surges during seasonal campaigns, while managed security controls help satisfy emerging cross-border data regulations. Real-time AI features—such as automated anomaly flags—tend to launch first on SaaS editions, further accelerating cloud preference.

On-premises persists in sectors with strict data-sovereignty clauses, but most of these organisations are introducing hybrid patterns that keep sensitive identifiers inside the firewall yet stream event aggregates to cloud analytics engines. Over the forecast window, existing licence renewals increasingly convert to SaaS, reinforcing the admission management software market’s subscription-based revenue mix.

By Application:

Customer analysis races aheadClick-path optimisation remained the largest slice at 38.10% in 2025, but customer analysis applications are now the growth star with a 15.02% CAGR. Businesses want to spot churn risk, predict next-order items, and segment high-lifetime-value cohorts. Embedding these models inside engaging visual workflows differentiates leading platforms.

As maturity grows, firms shift budgets away from static dashboards toward predictive scoring and prescriptive recommendations. The admission management software market accordingly invests in embedded machine-learning frameworks and low-code model builders that shorten deployment cycles and cut dependence on data-science headcount.

By Organization Size:

SME uptake acceleratesLarge enterprises still produced 56.35% of 2025 revenue thanks to multi-brand, multi-channel complexity that mandates enterprise-grade tooling. However, SME subscriptions are rising at 13.76% CAGR as vendors introduce freemium tiers, step-by-step onboarding, and auto-generated insights. Lightweight SDKs eliminate the need for deep engineering talent, letting lean teams track funnels within hours.

Growing SME adoption expands total addressable volume, though average deal sizes remain smaller. Vendors counterbalance this by automated upsell paths—advanced feature unlocks and pay-per-event tiers—keeping the admission management software market’s revenue curve steady.

By Industry Vertical:

Retail and e-commerce dominate, but healthcare and travel climbRetail and e-commerce generated 23.85% of 2025 revenue because basket-level insights convert directly to purchase uplift. Media, BFSI and telecom follow, each seeking richer engagement metrics. Healthcare adoption is climbing as patient portals integrate behavioural nudges to improve appointment adherence, while airlines and OTAs apply journey analytics to reduce booking abandonment. These sector expansions diversify the admission management software market, cushioning exposure to single-industry cycles.

Cross-vertical demand is unified by the same objective: interpreting granular user events to personalise touchpoints. Industry-specific templates—HIPAA-compliant schemas for healthcare, PCI-aligned flows for payment data—help vendors penetrate regulated niches without heavy custom coding.

Geography Analysis

North America Admission Management Software Market

North America delivered 41.10% of global revenue in 2025 due to high digital-commerce penetration, mature cloud infrastructure, and concentration of leading vendors. Enterprises in the region treat analytics as a make-or-break competency, funnelling budgets into AI augmentation and privacy-by-design frameworks. While growth is slowing as adoption saturates, wallet share remains high because buyers expand use cases within the same platforms, sustaining account-based revenue.

Europe Admission Management Software Market

Europe ranks second, driven by GDPR-induced demand for platforms that blend insight depth with strict consent controls. Vendors localise data-hosting options and integrate multilingual consent banners, boosting uptake in Germany, France and the Nordics. The admission management software market benefits from pan-EU data-transfer rules that favour providers offering in-region datacentres and advanced security certifications. Growth is steady as organisations embed analytics deeper into marketing resource-management workflows.

APAC Admission Management Software Market

Asia-Pacific is the flash-growth engine, forecast to log a 15.38% CAGR. Mobile-first consumer behaviour in India, Indonesia and the Philippines requires multi-device identity stitching, pushing local firms to adopt event-stream analytics early. Generative-AI-centric feature sets resonate with digitally native start-ups eager for low-code insight extraction. Regional governments’ push for cross-border data flows and cloud adoption further enlarges the admission management software market, especially in e-payments and super-app ecosystems.

Regulatory Landscape

Admission management software vendors operate under student-data privacy and security obligations that shape product architecture, hosting, and integration choices. In the United States, the Family Educational Rights and Privacy Act (FERPA, 20 USC 1232g) constrains disclosure and re-use of personally identifiable information from education records, which pushes institutions and providers toward consent management, role-based access controls, and data-minimization practices when handling applications, supporting documents, and decision communications.

In Europe, the EU Artificial Intelligence Act (Regulation (EU) 2024/1689) raises compliance requirements when AI is used in determining access or admission to educational institutions by classifying such use cases as high-risk. This emphasis falls on documented risk management, data governance, logging, transparency, and human oversight, and public educational institutions are also required to perform a Fundamental Rights Impact Assessment before deploying high-risk AI in admissions. Separately, proposed US legislative activity such as S. 3063 (119th Congress) points to ongoing scrutiny of third-party education technology contracting and could tighten expectations for vendor controls around student data handling.

Value Chain Analysis

The value chain starts with data capture and intake at the institution level, where applicants submit forms, documents, test scores, and fees through web portals and communication workflows. Core platform providers supply the admissions and enrollment layer (application workflow, document management, communications, decisioning, and analytics), and they typically integrate into the institution’s system-of-record stack, especially the Student Information System (SIS) and adjacent ERP and finance modules. In practice, the ecosystem often runs through two operational pillars: an SIS that maintains the authoritative student record, and an admissions CRM that manages prospect-to-applicant funnel activity, messaging, and yield analytics.

Implementation and distribution flow through direct enterprise sales to higher education and K-12 systems, procurement frameworks, and an active services layer of system integrators and campus IT teams that handle integrations, identity and access management, and data governance. Key dependencies include cloud infrastructure providers for hosting and scalability, API and integration tooling to connect CRM, SIS, and finance systems, and compliance alignment (for example, FERPA-driven controls and accessibility requirements). Integration complexity and scarcity of specialized talent increase the role of services partners and packaged connectors, which can shorten deployment timelines and reduce risk across heterogeneous campus stacks.

Competitive Landscape

The admission management software market is moderately fragmented. Adobe, Google and Microsoft leverage wide ecosystems—advertising, CMS, productivity suites—to cross-sell analytics modules. Their breadth appeals to enterprises seeking consolidated procurement and unified data fabrics. Specialist vendors such as Amplitude, Mixpanel and Contentsquare focus on depth, offering granular session replay, in-app funnel diagnostics, and lightweight experimentation layers that attract product teams.

Platform consolidation is intensifying larger players acquire niche tools to plug capability gaps (for example, session replay or predictive churn scoring). Simultaneously, start-ups differentiate via privacy-preserving approaches—edge-processed metrics and synthetic identifiers—to win accounts wary of regulatory risk. Patent filings around WebAssembly-based browser analytics and differential privacy illustrate a pipeline of innovation that could realign competitive standings over the next five years.

Pricing models are also diverging. Full-stack suites bundle analytics with CDPs and marketing-automation, creating multi-year commitments. Point-solution vendors emphasise transparent per-event or per-seat rates, appealing to cost-sensitive SMEs. Services partners play a pivotal role in stitching together mixed stacks, shaping vendor shortlists. Overall, buyer power is rising as switching costs fall, nudging providers to prioritise open APIs and out-of-the-box integrations to retain clients.

Admission Management Software Industry Leaders

Adobe Inc.

Google LLC

International Business Machines Corporation (IBM)

Microsoft Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Admission Management Software Market Companies Covered in this Report

- Adobe Inc.

- Google LLC (Google Analytics / GA4)

- Microsoft Corp. (Azure Data Explorer)

- IBM Corp. (Tealeaf / Watson CX)

- Oracle Corp. (Oracle CX Suite)

- SAP SE (Customer Data Platform)

- Amplitude Inc.

- Mixpanel Inc.

- Heap Inc.

- Piano Analytics (AT Internet)

- Contentsquare SA

- FullStory Inc.

- Quantum Metric Inc.

- Snowplow Analytics Ltd

- Hotjar Ltd

- Crazy Egg Inc.

- Matomo (Innocraft Ltd)

- Piwik PRO SA

- Twilio Inc. (Segment CDP)

- Yandex Metrica (YANDEX LLC)

Market Opportunities and Future Outlook

Institution-level and national-level digitization programs are creating whitespace for admissions platforms that combine end-to-end applicant journeys with compliant AI assistance, cybersecurity controls, and deeper integration into SIS and finance workflows. A clear example is the UAE Ministry of Higher Education and Scientific Research upgrading its Edu Hub national registration and admissions platform with AI-powered capabilities in 2026, which raises expectations for standardized digital intake, faster decision cycles, and unified student-journey orchestration across participating institutions.

Procurement signals also point to demand for AI-enabled admissions platforms that connect to entrenched campus systems rather than operating as standalone tools. In 2026, the University of Sunderland issued a procurement market engagement notice for an AI-enabled admissions platform designed for end-to-end applicant journeys and integration with core systems such as SITS and CAS Shield, reinforcing pull toward interoperable architectures, automation in offer-making and case handling, and governance-ready AI features. In parallel, EDUCAUSE reporting in 2026 that 46% of students encountered a security threat in the past academic year strengthens the case for cybersecurity and privacy-by-design as buying criteria, leaving room for vendors that pair workflow automation with stronger security posture and auditable data controls.

Recent Industry Developments in Admission Management Software Market

- June 2026: EducationDynamics acquired NetNatives to expand its enrollment marketing capabilities with international student recruitment technology. The move strengthens end-to-end recruitment and conversion workflows for institutions competing for cross-border enrollments, and increases competitive pressure on platform vendors bundling marketing, admissions communications, and analytics.

- May 2026: Blackbaud announced a strategic investment in Student First, an AI-enabled student information system provider, with integration goals spanning enrollment, financial aid, and finance workflows. The investment supports tighter coupling between admissions-facing processes and the SIS and finance backbone, reinforcing a platform direction where institutions seek fewer disconnected systems.

- April 2026: Niche announced a collaboration with Huron to connect Niche behavioral student data with Huron enrollment and financial aid revenue forecasting models. This expands the use of real-time market and engagement signals in admissions planning, raising the bar for analytics-driven enrollment strategy features embedded in admissions management stacks.

Admission Management Software Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers software and related services that help education providers run the admissions journey, starting from inquiry handling and application capture and ending at enrollment confirmation. The value includes tools for forms, communications, document checks, fee workflows, and reporting that supports admission decisions.

Scope exclusions: standalone learning management systems, general finance or HR suites, and student information tools that do not directly manage the application-to-enrollment workflow are excluded.

Segments Covered in This Report

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-premise

- By Application

- Click Path and Website Optimization

- Customer Analysis

- Basket Analysis and Personalization

- Traffic Analysis

- Website / App Performance Optimization

- By Industry Vertical

- Retail and E-commerce

- Media and Entertainment

- BFSI

- Telecommunications and IT

- Travel and Hospitality

- Healthcare

- Others

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the boundaries of what counts as admission management and to build a realistic demand pool by geography and institution type. We use public education statistics and operating indicators from sources such as the US National Center for Education Statistics (NCES), UNESCO Institute for Statistics, the World Bank education datasets, OECD education indicators, and national education ministry portals where available.

For supply and pricing, we review public company filings, product brochures, implementation case studies, press releases, and procurement notices from government and public institutions to understand typical module bundles and support terms. A paid subscription that aggregates company financials and news was used selectively to cross-check revenue direction and major contract announcements. The sources listed above are illustrative only, and many other public materials were also referenced for data collection and validation checks.

Primary Interviews and Surveys

Primary work is used to validate what institutions actually buy, how often they replace admission systems, and how pricing changes by deployment model and institution size. We spoke with software providers, implementation partners, and admission operations leaders across major regions, then used their input to confirm adoption assumptions, typical contract structures, and realistic year-by-year ASP movement.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 19% | APAC: 39% |

| Mid tier: 42% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 19% | Managers: 49% | Americas: 26% |

Market-Sizing & Forecasting

The core model starts from a top-down demand reconstruction, where institution counts and applicant volumes are translated into an addressable software spend based on adoption and spend-per-institution ranges. Those totals are then stress-tested through selective bottom-up approximations, such as sampled pricing by module bundle, channel checks on implementation intensity, and revenue reasonableness checks for a shortlist of visible suppliers.

Key inputs used in the model include the number of higher education and K-12 institutions by region, application volume trends and digitization rates, cloud versus on-premises mix, average contract duration and renewal cycles, and the share of institutions buying services (implementation, training, and support) along with software. Where bottom-up visibility is thin for smaller providers, gaps are handled using normalized spend bands by institution size and conservative service-attach assumptions, which are then rechecked in interviews.

Forecasting is done using scenario analysis supported by multivariate regression on stable drivers, mainly institution growth, digital admissions penetration, and budget priority signals discussed by respondents. The final forecast is adjusted when primary feedback indicates clear step-changes, such as policy-driven digitalization or faster cloud migration in specific regions.

Data Validation & Update Cycle

Validation is done by triangulating model outputs against independent signals, including education enrollment trends, procurement activity patterns, and observed pricing ranges for common module bundles. Outliers are investigated, assumptions are revisited, and a second analyst review is completed before sign-off so the logic stays consistent across regions and years.

The study is refreshed on an annual cycle, and interim checks are triggered when there are material events like major policy changes, large M&A activity, or sharp pricing shifts tied to cloud migrations. Before delivery, we do a final scan of the latest public updates and re-contact a small set of respondents when a key input shows unusual variance.

Mordor Intelligence's Admission Management Software Market Size Compared With Other Published Estimates

Published market sizes for admission management software can differ even when the topic name looks the same, because the counting rules are not consistent across studies. Differences usually come from what is included with the software, which education users are counted, and how pricing is carried forward in the forecast years.

By tracking deployment mix changes and service attachment rates, Mordor Intelligence keeps the 2026 value tied to what institutions pay for admission workflow software plus related services, instead of blending it into broader student systems or unrelated campus modules. Some estimates also mix in corporate training enrollment tools or use a single global ASP uplift, which can move totals up or down depending on the assumed pace of cloud adoption and renewal pricing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.59 B (2026) | |

| Industry Publisher A | USD 1.52 B (2024) | Uses an earlier base year and appears to include corporate training and certification bodies alongside education institutions, which changes the demand pool and shifts totals when adoption is assumed to rise quickly. |

| Research Portal B | USD 1.59 B (2024) | Applies a wider feature scope across student management functions and uses a higher near-term growth path, which can inflate the counted revenue beyond admission workflow software and its related services. |

The spread in values is largely explained by scope boundaries and the year used as the starting point, followed by how cloud migration and service revenues are treated in the model. When the demand pool is built from institution and applicant activity signals and then checked with realistic contract and pricing patterns, the result stays easier to trace and repeat year to year.

Key Questions Answered in the Report

What is the current value of the admission management software market?

The admission management software market size is USD 1.59 billion in 2026.

How fast will the admission management software market grow?

The market is projected to expand at a 8.71% CAGR, reaching USD 2.41 billion by 2031.

Which region leads in revenue?

North America holds 41.10% of 2025 revenue, ahead of Europe and Asia-Pacific.

Why are cloud deployments preferred?

Cloud captures 67.75% share because elastic compute reduces the cost of ingesting and analysing large click-stream volumes.

Which application segment is growing fastest?

Customer analysis applications are advancing at a 15.02% CAGR as firms seek predictive insights into churn and lifetime value.

How are privacy regulations affecting adoption?

Stricter rules like GDPR and CCPA push enterprises to platforms with built-in consent and data-minimization tools, influencing vendor selection and slowing implementations that lack compliance features.

Page last updated on: