Government Cloud Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

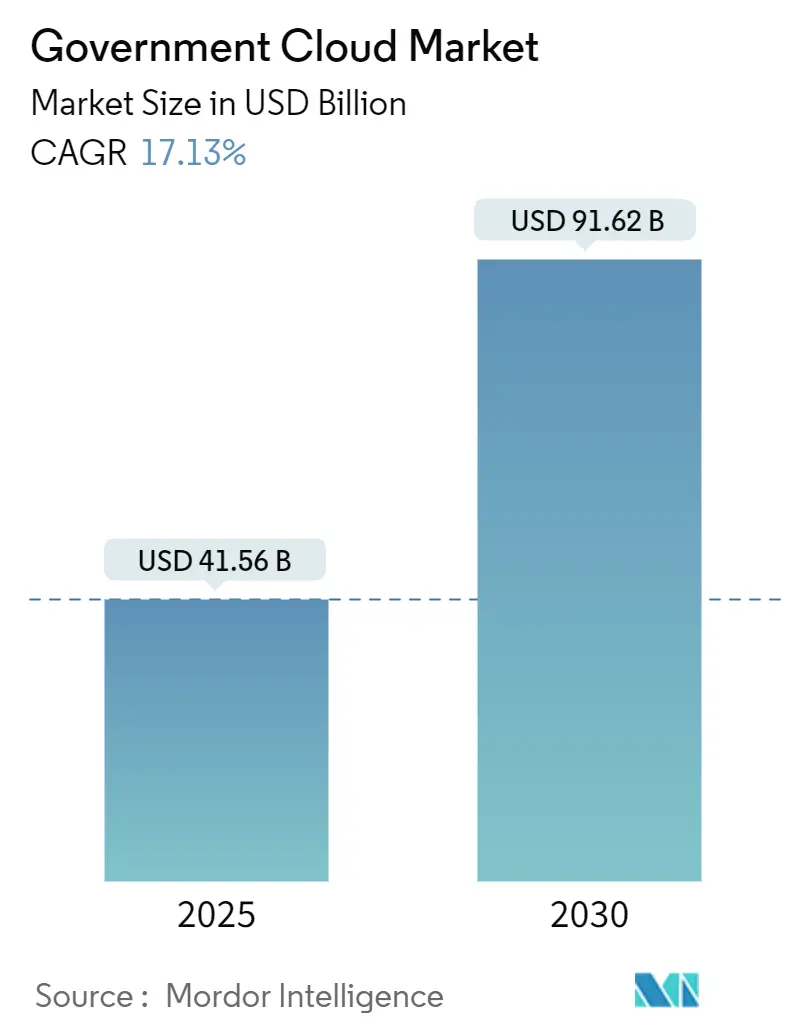

| Market Size (2025) | USD 41.56 Billion |

| Market Size (2030) | USD 91.62 Billion |

| Growth Rate (2025 - 2030) | 17.13% CAGR |

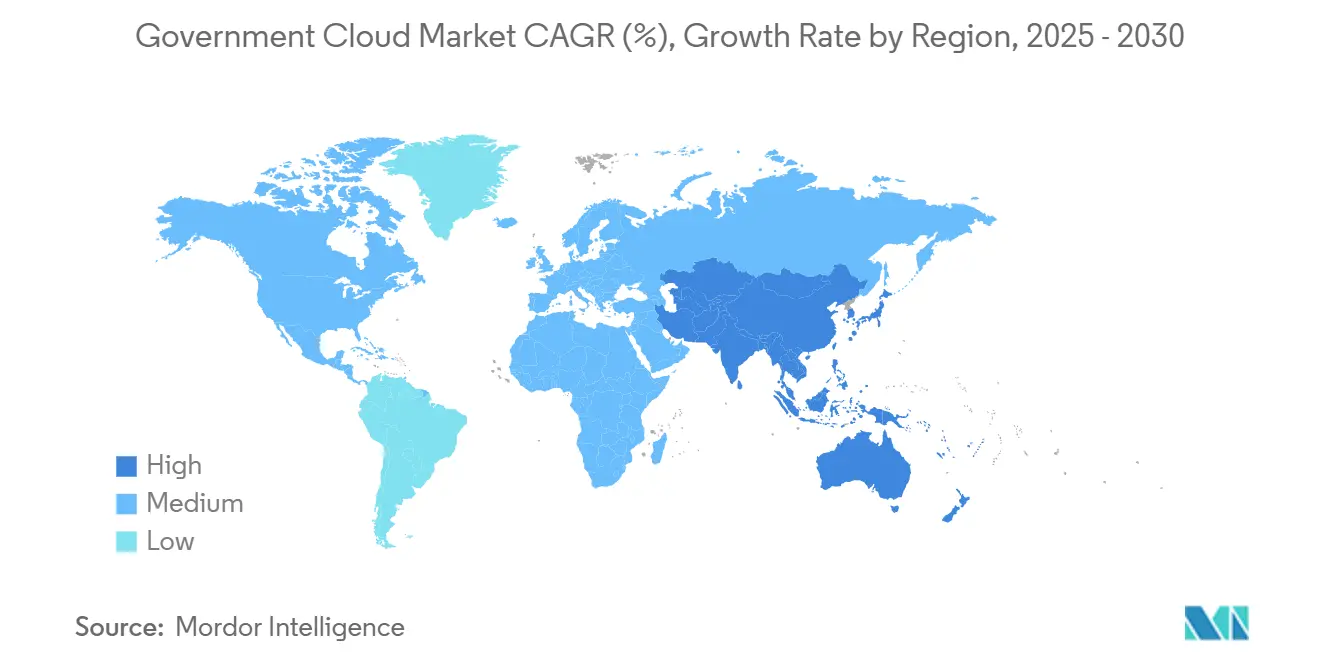

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Government Cloud Market Analysis by Mordor Intelligence

The government cloud market size is USD 41.56 billion in 2025 and is projected to reach USD 91.62 billion by 2030, reflecting a 17.13% CAGR over the forecast period. Agencies are replacing on-premises workloads with sovereign-ready cloud regions to satisfy data-residency rules while still achieving the cost efficiencies of hyperscale platforms. Hybrid multicloud architectures are gaining traction as policymakers demand flexibility, vendor optionality, and zero-trust security baselines. Rapid growth in analytics and AI workloads is pushing demand for GPU-rich instances and confidential-computing services that can handle sensitive datasets without compromising compliance. At the same time, procurement reform in North America and the European Union is accelerating contract consolidation, creating larger deal sizes but also higher entry barriers for new vendors.

Key Report Takeaways

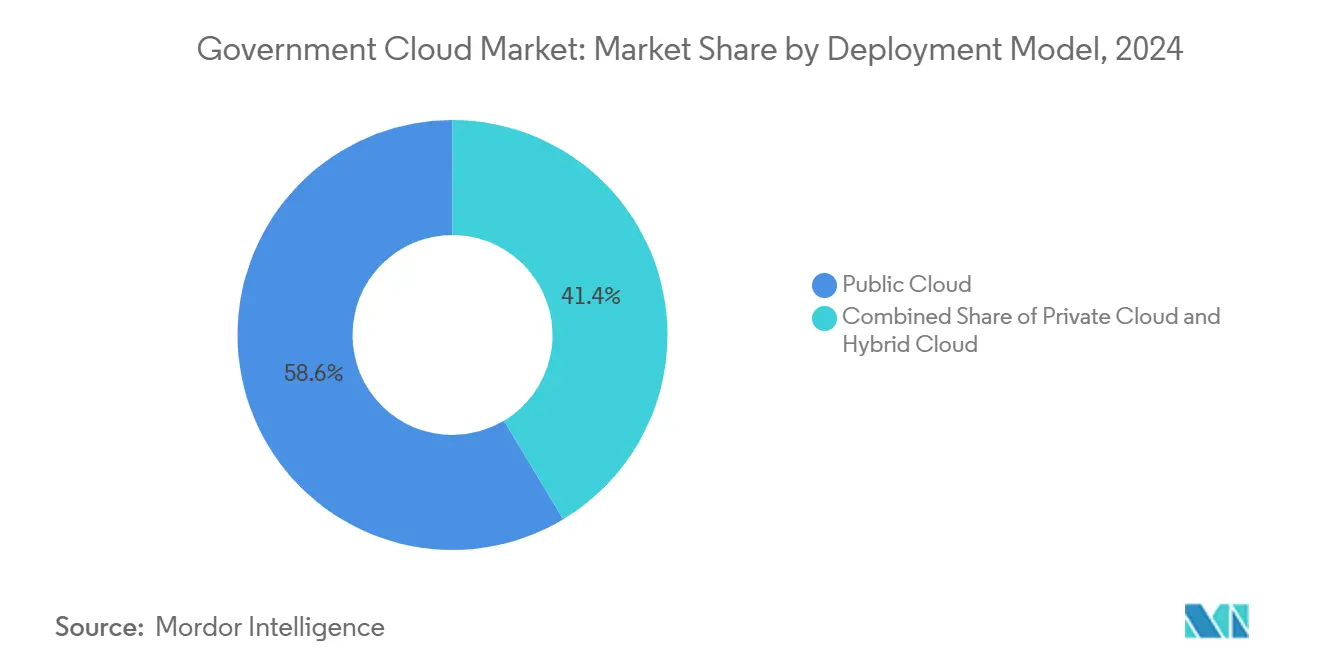

- By deployment model, public cloud led with 58.62% of government cloud market share in 2024, while hybrid cloud is forecast to advance at an 18.78% CAGR through 2030.

- By delivery model, Software-as-a-Service captured 47.62% share of the government cloud market size in 2024; Platform-as-a-Service is projected to expand at an 18.56% CAGR between 2025-2030.

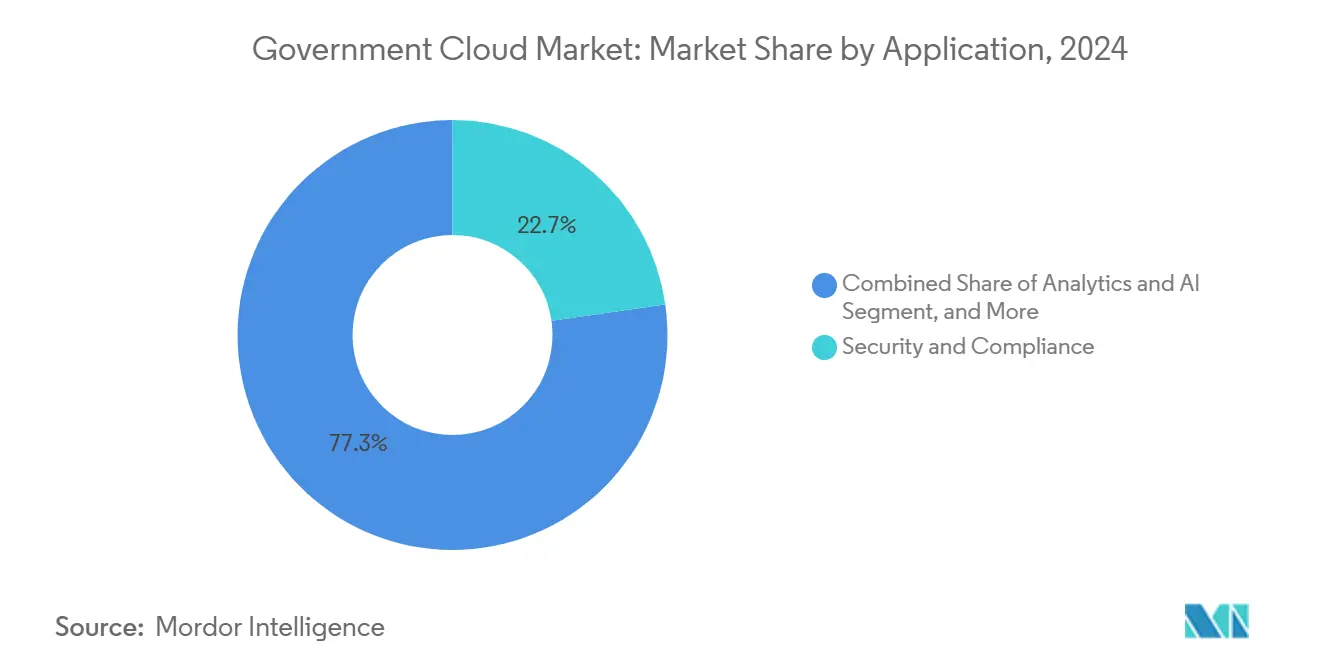

- By application, security and compliance held 22.73% of government cloud market share in 2024, whereas analytics and AI applications are growing at a 17.67% CAGR through 2030.

- By end-user, federal and central agencies accounted for 40.71% of the government cloud market size in 2024; defense and intelligence workloads are poised for an 18.23% CAGR to 2030.

- By geography, North America maintained 39.89% government cloud market share in 2024, while Asia-Pacific is on track for an 18.16% CAGR during the forecast window.

Global Government Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first public-sector modernization programs | +4.2% | Global, with early gains in North America, EU, Singapore | Medium term (2-4 years) |

| Data-sovereignty and localization mandates | +3.8% | EU core, APAC expansion, selective North America | Long term (≥ 4 years) |

| Cost-optimization pressure on government IT budgets | +3.1% | Global, particularly SLED markets | Short term (≤ 2 years) |

| Pandemic-driven remote-work continuity planning | +2.4% | Global, with sustained impact in developed markets | Medium term (2-4 years) |

| Adoption of confidential-computing for classified workloads | +2.0% | North America, EU defense sectors, APAC selective | Long term (≥ 4 years) |

| Inter-agency multi-cloud brokerage platforms | +1.8% | North America federal, EU federated initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-First Public-Sector Modernization Programs

Governments are decommissioning decades-old mainframes in favor of cloud-native stacks that deliver elastic capacity, automated patching, and rapid feature deployment. The U.S. Air Force migrated 1.3 million lines of COBOL to Java on AWS GovCloud and cut annual operating costs from USD 30 million to USD 3 million.[1]Lindsey, Carmen, “Lowered TCO by 90% – COBOL to Java on AWS for the U.S. Air Force,” TSRI, tsri.com Similar code-refactoring projects are under way at the Office of Personnel Management, which has budgeted a two-year plan to infuse AI into legacy benefit-processing systems. These programs mitigate technical debt, improve disaster-recovery postures, and set templates that other ministries can reuse via “Government-as-a-Platform” frameworks. Procurement reforms like FedRAMP High baselines shorten accreditation cycles, enabling agencies to spin-up secure cloud workloads in weeks rather than months. Collectively, these shifts accelerate workload migration from on-premises data centers to sovereign-compliant regions, reinforcing momentum in the government cloud market.

Data-Sovereignty and Localization Mandates

The European Union, Australia, and Singapore now require sensitive workloads to stay within national borders or trusted trade zones. Microsoft’s EU Data Boundary restricts remote access to Europe-based staff, while Oracle’s EU Sovereign Cloud runs isolated regions in Frankfurt and Madrid. Singapore’s Government Commercial Cloud taps dedicated Azure regions to guarantee local residency for citizen data while still drawing on hyperscale innovation. These forced-localization rules create demand for air-gapped or hybrid architectures that blend on-premises security with public-cloud elasticity. Vendors are responding by adding customer-controlled encryption, local support teams, and contractual shields against extra-territorial subpoenas. Sovereignty stipulations thus transform compliance from a cost center into a competitive differentiator inside the government cloud market.

Cost-Optimization Pressure on Government IT Budgets

Roughly 80% of federal IT outlays go toward operating and maintaining legacy systems, leaving limited headroom for innovation. Agencies are therefore prioritizing cloud migrations that promise measurable year-one savings and reduced technical-staff overhead. The Department of Housing and Urban Development’s mainframe migration saved USD 8 million annually while servicing 30,000 users across 100 programs that disburse USD 27 billion each year.[2]U.S. Chamber Staff, “Maximizing Cost Savings: Unleashing the Value of Federal IT Modernization,” uschamber.com State and local entities mirror this pattern, pooling resources into shared cloud procurement vehicles that lower per-capita spend and enable smaller jurisdictions to access enterprise-grade cybersecurity. In the aggregate, budget-driven rationalization continues to underpin the business case for moving workloads to the government cloud market.

Pandemic-Driven Remote-Work Continuity Planning

COVID-19 stress-tested public-sector IT resilience, compelling agencies to adopt cloud-delivered collaboration suites and virtual desktop infrastructures. The 2020 U.S. Census was executed online, saving USD 1.9 billion in field-operations cost while maintaining social-distancing protocols. Lessons learned have institutionalized hybrid-work architectures: 33% of U.S. federal agencies expect to run hybrid multicloud environments within three years, supported by CISA guidance on identity federation.[3]Cybersecurity and Infrastructure Security Agency, “Hybrid Cloud Identity Guidance,” cisa.gov Similar shifts are visible in Canada, the UK, and Japan, where emergency-response agencies now treat cloud scaling as a standard operating procedure. Persistent demand for resilient, anywhere-access services keeps remote-work enablement at the core of the government cloud market’s growth thesis.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and privacy liability concerns | -2.1% | Global, heightened in defense/intelligence sectors | Short term (≤ 2 years) |

| Legacy system and vendor-lock-in integration complexity | -1.8% | North America federal, EU established markets | Medium term (2-4 years) |

| Lengthy FedRAMP/IRAP certification lead-times | -1.5% | North America federal, Australia government | Medium term (2-4 years) |

| Geopolitical sovereignty risk limiting hyperscaler presence | -1.2% | EU core, APAC selective markets, China restrictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Privacy Liability Concerns

High-profile breaches at commercial cloud platforms have prompted regulators to scrutinize supply-chain controls and incident-response readiness. A 2025 review of the Microsoft Exchange Online intrusion underscored how provider misconfigurations can cascade across multiple government tenants, leading to Executive Order 14144 that mandates zero-trust adoption across civilian agencies. The Department of Defense now tracks 152 zero-trust activities across 91 target and 61 advanced implementations, but audit cycles and red-team exercises have lengthened procurement timelines. Classified workloads often require air-gapped regions or on-premises enclaves, which slows migration until sufficient isolation controls are certified. These liability fears subtract momentum from otherwise compelling cost-savings arguments in the government cloud market.

Legacy System and Vendor-Lock-In Integration Complexity

Many mission-critical applications run on code written in COBOL or Assembler more than 50 years ago, with interdependencies that remain poorly documented. The U.S. Government Accountability Office flagged 10 such systems costing USD 337 million annually to maintain, including IRS tax-processing software that still relies on magnetic-tape backups. Migrating these workloads to cloud often demands extensive refactoring, data-schema normalization, and middleware re-platforming, projects that span multiple budget cycles. Agencies also worry that proprietary hyperscaler services will create new switching costs, constraining future procurement optionality. To mitigate lock-in, many insist on open-standard container orchestration and multicloud abstraction layers, but these tools add complexity and can erode some of the operational efficiency gains that initially drove interest in the government cloud market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Balance Sovereignty and Scale

Hybrid cloud accounts for the fastest-growing slice of the government cloud market, expanding at an 18.78% CAGR as agencies fuse on-premises classified enclaves with scalable public-cloud zones for analytics. Public cloud still holds 58.62% government cloud market share in 2024 thanks to its pay-as-you-go economics and FedRAMP-ready service catalogs. Ministries deploy container gateways that broker traffic between air-gapped data centers and external regions, minimizing latency while preserving residency compliance. The U.S. Air Force’s Cloud One program migrated 155 mission-critical systems using such a hybrid blueprint, reducing release cycles from quarterly to daily while keeping secret data on dedicated nodes.[4]Department of Defense, “Cloud One Program Overview,” dod.mil European defense agencies employ similar tactics under the EU Classified Cloud framework, connecting sovereign-cloud regions through encrypted optical links for joint operations. Looking ahead, confidential-container runtimes and quantum-safe key management are expected to deepen hybrid adoption across the government cloud market.

Private cloud remains relevant for agencies that require full hardware isolation or must accommodate bespoke security controls. The Israeli Ministry of Defense’s Nimbus tender illustrates this point, specifying on-shore data centers operated under local law even while permitting burst-out to AWS and Google for non-classified workloads. In emerging economies, restricted bandwidth and higher latency can also tilt deployments toward private or community clouds hosted in national facilities. Yet as hyperscalers roll out sovereign regions that offer local support teams and state-owned data-center shells, the economic gap between private and public deployment models continues to widen.

By Delivery Model: Platform Services Accelerate Modernization Velocity

Software-as-a-Service secured 47.62% of the government cloud market size in 2024 because turnkey applications slash development cycles and shift patching burdens to vendors. Email, case-management, and enterprise-resource-planning suites dominate early migration waves, often bundled under volume-licensing agreements that include FedRAMP High or GDPR compliance add-ons. Platform-as-a-Service, however, is posting an 18.56% CAGR as low-code workbenches enable civil-servant subject-matter experts to build workflows without deep programming skills. The Department of Veterans Affairs scaled its low-code ecosystem from USD 6 million to more than USD 3 billion in contract ceiling value within a single budget cycle, cutting prototype timelines from months to days.

Infrastructure-as-a-Service continues to underpin large-scale data-center exits and disaster-recovery modernization. Agencies copy petabytes of legacy tape archives into object-storage buckets, then layer analytics engines to mine historical patterns for fraud detection and policy impact. Edge-computing variants of IaaS are emerging at battlefield or border-control sites, pushing inference engines closer to sensors to reduce decision latency. Over the forecast period, the composable-infrastructure approach, mixing bare-metal, GPUs, and AI accelerators on-demand, will blur traditional IaaS, PaaS, and SaaS boundaries inside the government cloud market.

By Application: Analytics and AI Fuel Intelligence-Led Governance

Security and compliance workloads retained 22.73% government cloud market share in 2024 because agencies must satisfy regulatory frameworks before migrating citizen data. Tools such as continuous-diagnostics dashboards and automated authority-to-operate pipelines dominate early spend. Once guardrails are in place, ministries pivot to analytics and AI, the fastest-growing segment at a 17.67% CAGR. Federal AI budgets reached USD 5.6 billion for fiscal 2022-2024 and request an additional USD 3.3 billion for 2025, with priority use cases ranging from predictive maintenance to benefits-fraud identification. Cloud-native data fabrics allow agencies to fuse structured and unstructured datasets, unlocking insights that were previously siloed across departmental boundaries.

Server, storage, and disaster-recovery applications remain essential, especially for public-safety agencies that must maintain continuity during hurricanes, wildfires, or geopolitical crises. Content management and collaboration suites surged during pandemic lockdowns and now underpin hybrid-work mandates that span both administrative and field operations. Specialized verticals, such as land-registry digitization or digital-court evidence management, round out the long-tail of application demand, ensuring sustained breadth in the government cloud market.

By End-User: Defense and Intelligence Drive Classified-Cloud Expansion

Federal and central agencies commanded 40.71% of the government cloud market size in 2024, buoyed by multi-year modernization budgets and executive-branch cloud mandates. Defense and intelligence users form the fastest-growing cohort, expanding at an 18.23% CAGR as classified workloads migrate to secret or top-secret regions equipped with secure cross-domain solutions. AWS’s second secret region and Microsoft’s IL6-authorized OpenAI models exemplify this acceleration. Generative AI supports mission tasks such as terrain-image labeling and threat-signal triage while remaining inside national security perimeters.

State and local governments leverage shared-services clouds to digitize tax filings, permitting, and emergency-response coordination. Education ministries employ elastic HPC clusters for genomic research, climate modeling, and distance learning, taking advantage of academic pricing tiers. Public-health agencies combine epidemiological data lakes with AI forecasting to inform vaccination campaigns. As more jurisdictions formalize cloud-first procurement statutes, cumulative demand from these diverse end-users broadens the revenue base of the government cloud market.

Geography Analysis

North America held 39.89% government cloud market share in 2024, fueled by the U.S. federal government’s USD 8.3 billion cloud allocation and the multi-vendor Joint Warfighting Cloud Capability contract that added USD 721 million in awarded task orders during 2025. Mature FedRAMP pipelines, zero-trust mandates, and large-scale framework agreements such as OneGov amplify purchasing power and compress sales cycles. Canadian provinces are adopting similar shared-services agreements, while Mexico’s national digital transformation strategy earmarks cloud as the backbone for universal healthcare records and digital tax collection.

Asia Pacific is the fastest-growing region, expanding at an 18.16% CAGR on the back of sovereign cloud investments and nationwide digital-government roadmaps. Singapore’s Government Commercial Cloud pools agency workloads into isolated Azure regions, and Japan’s My Number initiative links citizen IDs to cloud-hosted benefits portals. Google Cloud is adding regions in New Zealand, Malaysia, and Thailand to address localization statutes and latency concerns. ASEAN member states have pledged USD 110 billion for sovereign AI infrastructure by 2026, further underscoring the strategic weight of the government cloud market in the region.

Europe continues to refine its sovereign-cloud posture, guided by GDPR, the Digital Services Act, and the Gaia-X federated-data project. Microsoft’s EU Data Boundary and Oracle’s EU Sovereign Cloud illustrate hyperscaler adaptation to localized control requirements. The Ukraine conflict has amplified cybersecurity funding, encouraging NATO members to adopt zero-trust reference architectures and cross-border secure networks. Meanwhile, post-Brexit divergence forces UK ministries to reconcile overlapping EU and domestic data-protection laws before committing workloads to pan-European providers.

Competitive Landscape

The government cloud market exhibits moderate concentration, with the top three hyperscalers, AWS, Microsoft, and Google, leveraging dedicated government regions, compliance certifications, and multi-billion-dollar framework contracts to outpace smaller providers. AWS maintains leadership through GovCloud, Secret, and Top Secret partitions; it recently added quantum-networking research via a USD 54.5 million Air Force Research Laboratory contract awarded to IonQ. Microsoft anchors its position with Office 365 Government Community Cloud services and IL6-cleared Azure OpenAI deployments, while Google invests in region expansion to align with data-sovereignty edicts.

Regional telecom operators and systems integrators partner with hyperscalers to provide managed-service overlays, sovereign controls, and industry-specific accelerators. Examples include Orange Business Services’ joint EU sovereign-cloud venture and Telstra’s defense-grade compliance wrapper for Australian workloads. Price competition remains intense for commoditized IaaS, but value migrates upward to platform-native AI, secure-edge services, and multicloud orchestration portals. Vendors that can pre-bundle zero-trust blueprints and offer fixed-price migration toolkits gain a procurement advantage under tightening public-sector budget cycles.

Consolidation is reshaping channel dynamics. GSA’s OneGov elevates OEMs to prime contractors and positions resellers as subcontractors, scaling contract ceilings but shrinking margins for smaller partners. Similar central-buying hubs are emerging in Japan and France, further raising compliance thresholds. Hyperscalers respond by sponsoring accelerator programs that help small and disadvantaged businesses meet security benchmarks and qualify for subcontracting pools, ensuring a diversified supply chain within the government cloud market.

Government Cloud Industry Leaders

CGI Inc.

Cisco Systems, Inc.

Google LLC (Alphabet Inc.)

Dell Technologies Inc.

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AWS launched its second secret cloud region to serve defense and intelligence customers, expanding classified-workload capacity.

- April 2025: Microsoft Azure OpenAI obtained IL6 authorization for U.S. defense operations, enabling AI on classified data.

- March 2025: GSA introduced OneGov, centralizing roughly USD 490 billion in federal procurement under government-wide contracts.

- December 2024: The Defense Logistics Agency has awarded the USD 12 billion JETS 2.0 IDIQ contract for enterprise technology services, including cloud modernization.

Global Government Cloud Market Report Scope

Government cloud market is becoming the next big thing, as vendors provide public, private, or hybrid cloud solutions for managing government data, ensuring security, backing up data, or ensuring compliance. The offerings can be categorized by delivery modes, such as Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), or Software-as-a-Service (SaaS).

The Government Cloud Market can be segmented by Deployment Model (Private Cloud, Public Cloud, Hybrid Cloud), Delivery Mode (IaaS, PaaS, SaaS), Application (Server and Storage, Disaster Recovery/Data Backup, Security and Compliance, Analytics and AI, Content and Collaboration Management, and Other Applications), End-User (Federal and Central Government Agencies, State and Local Government, Defense and Intelligence, Public Safety and First Responders, Education and Research Institutions, and Other End-Users), and Geography (North America, South America, Asia-Pacific, Europe, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Server and Storage |

| Disaster Recovery / Data Backup |

| Security and Compliance |

| Analytics and AI |

| Content and Collaboration Management |

| Other Applications |

| Federal / Central Government Agencies |

| State and Local Government |

| Defense and Intelligence |

| Public-Safety and First Responders |

| Education and Research Institutions |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Delivery Model | Infrastructure-as-a-Service (IaaS) | ||

| Platform-as-a-Service (PaaS) | |||

| Software-as-a-Service (SaaS) | |||

| By Application | Server and Storage | ||

| Disaster Recovery / Data Backup | |||

| Security and Compliance | |||

| Analytics and AI | |||

| Content and Collaboration Management | |||

| Other Applications | |||

| By End-User | Federal / Central Government Agencies | ||

| State and Local Government | |||

| Defense and Intelligence | |||

| Public-Safety and First Responders | |||

| Education and Research Institutions | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the government cloud market in 2025?

It is valued at USD 41.56 billion and is forecast to reach USD 91.62 billion by 2030, growing at a 17.13% CAGR.

Which deployment model is growing fastest for public-sector workloads?

Hybrid cloud leads with an 18.78% CAGR because it balances data sovereignty with public-cloud scalability.

Why are analytics and AI workloads important to public agencies?

They help extract insights from large government datasets, driving the fastest application-level CAGR at 17.67%.

What drives government interest in confidential computing?

Defense and intelligence agencies need hardware-enforced isolation to process classified data in the cloud.

How does OneGov affect cloud procurement?

It centralizes USD 490 billion in annual spend, simplifying vendor selection yet raising entry barriers for smaller providers.

Page last updated on: