Cloud Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.48 Billion |

| Market Size (2031) | USD 10.95 Billion |

| Growth Rate (2026 - 2031) | 19.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Monitoring Market Analysis by Mordor Intelligence

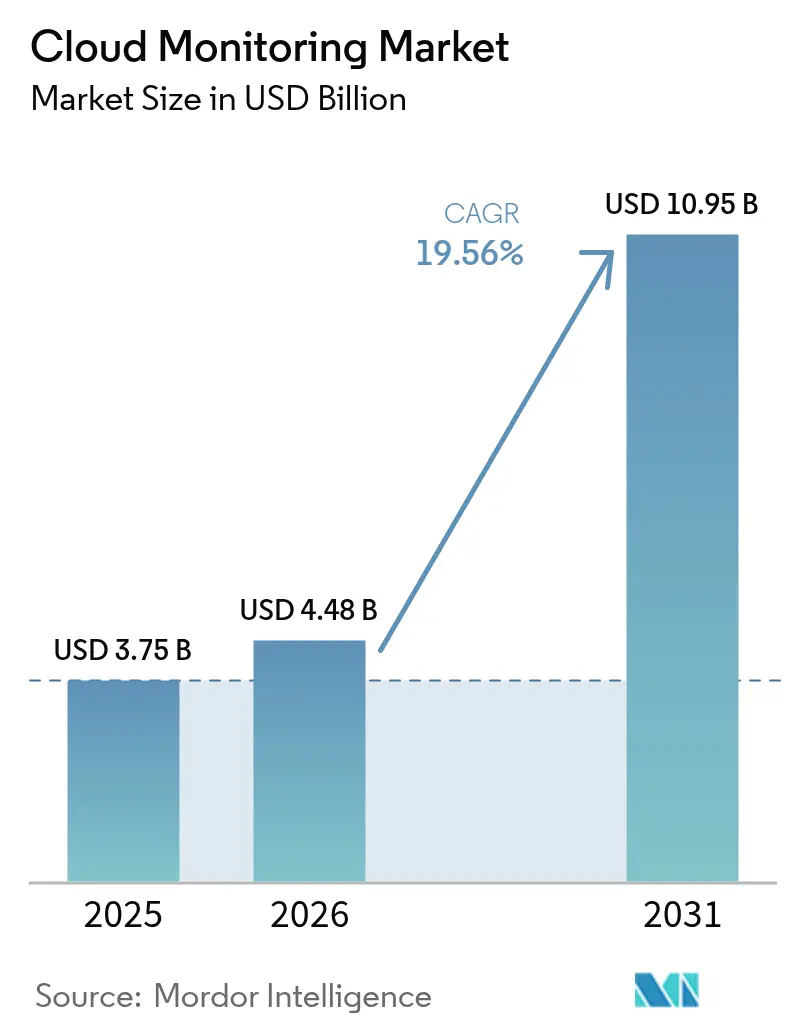

The Cloud Monitoring Market size is expected to grow from USD 3.75 billion in 2025 to USD 4.48 billion in 2026 and is forecast to reach USD 10.95 billion by 2031 at 19.56% CAGR over 2026-2031.

Accelerated multi-cloud adoption, AI workload visibility, FinOps accountability, and data-sovereignty mandates are reshaping vendor roadmaps. Enterprises are replacing point monitoring tools with unified platforms that ingest logs, metrics, traces, user experience, and cost signals in real time. OpenTelemetry’s rapid standardization is lowering integration friction, while AI-driven anomaly detection shortens the mean time to resolution. Spending is shifting from pure infrastructure metrics toward full-stack intelligence that ties technical health to revenue impact. Competitive intensity remains moderate as hyperscale clouds embed native tooling, yet still partner with independent vendors to address hybrid estates.

Key Report Takeaways

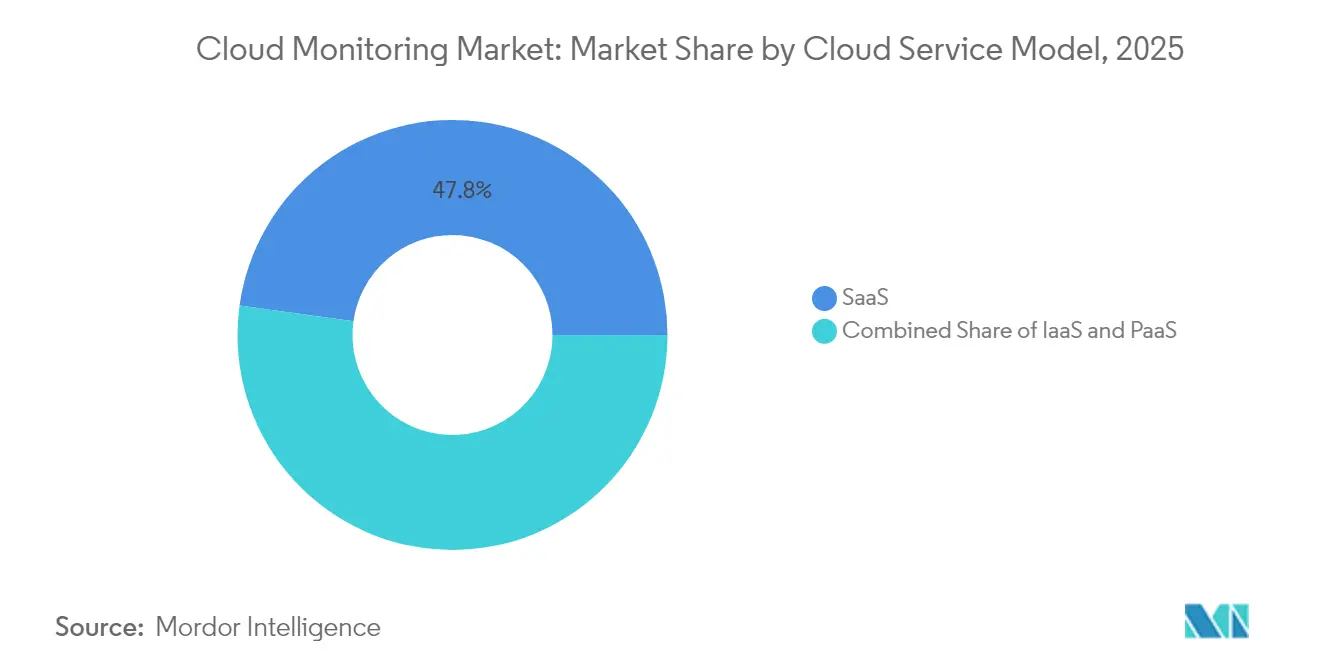

- By cloud service model, SaaS offerings held 47.80% of the cloud observability market share in 2025; PaaS solutions are forecast to grow at 28.45% CAGR to 2031.

- By component, solutions accounted for 61.30% of the cloud observability market size in 2025, while services are expanding at 18.85% CAGR through 2031.

- By deployment mode, public cloud retained 56.40% revenue share in 2025; hybrid and multi-cloud options are set to post a 23.95% CAGR to 2031.

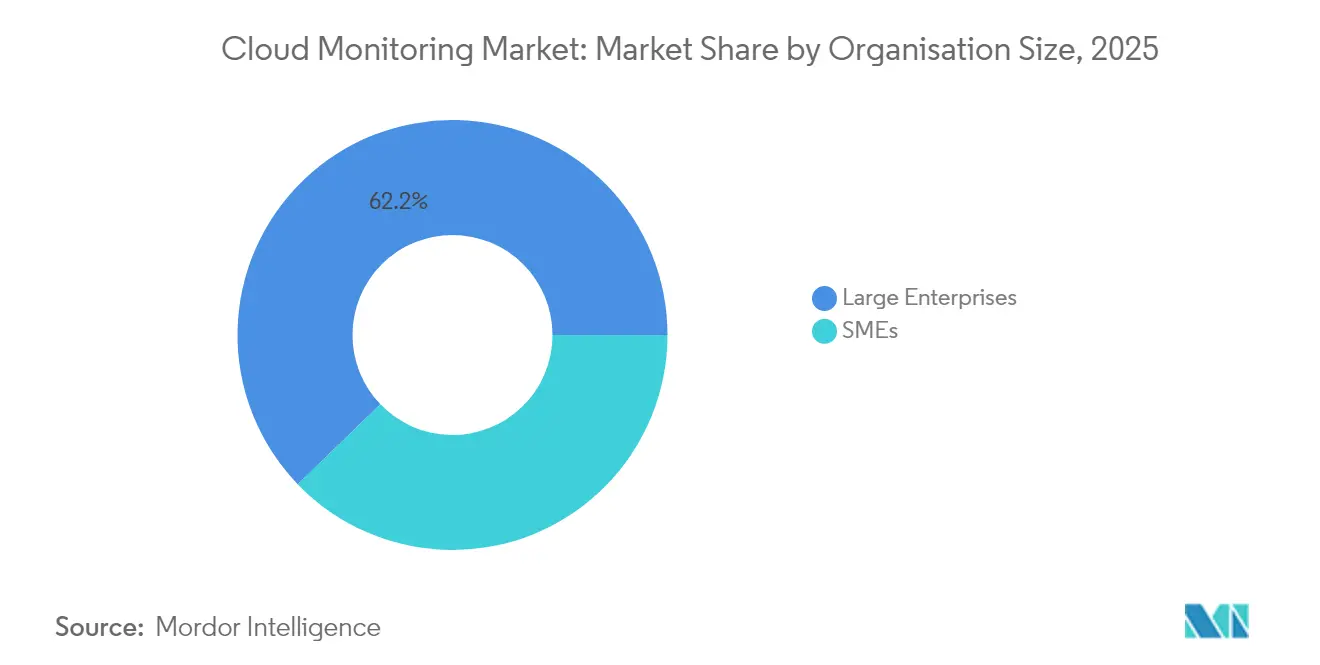

- By organization size, large enterprises contributed 62.20% of 2025 revenue, whereas SMEs are the fastest-growing segment at 18.05% CAGR.

- By end-user industry, IT & telecommunications led with 28.60% share in 2025; retail & e-commerce is projected to climb at 17.25% CAGR to 2031.

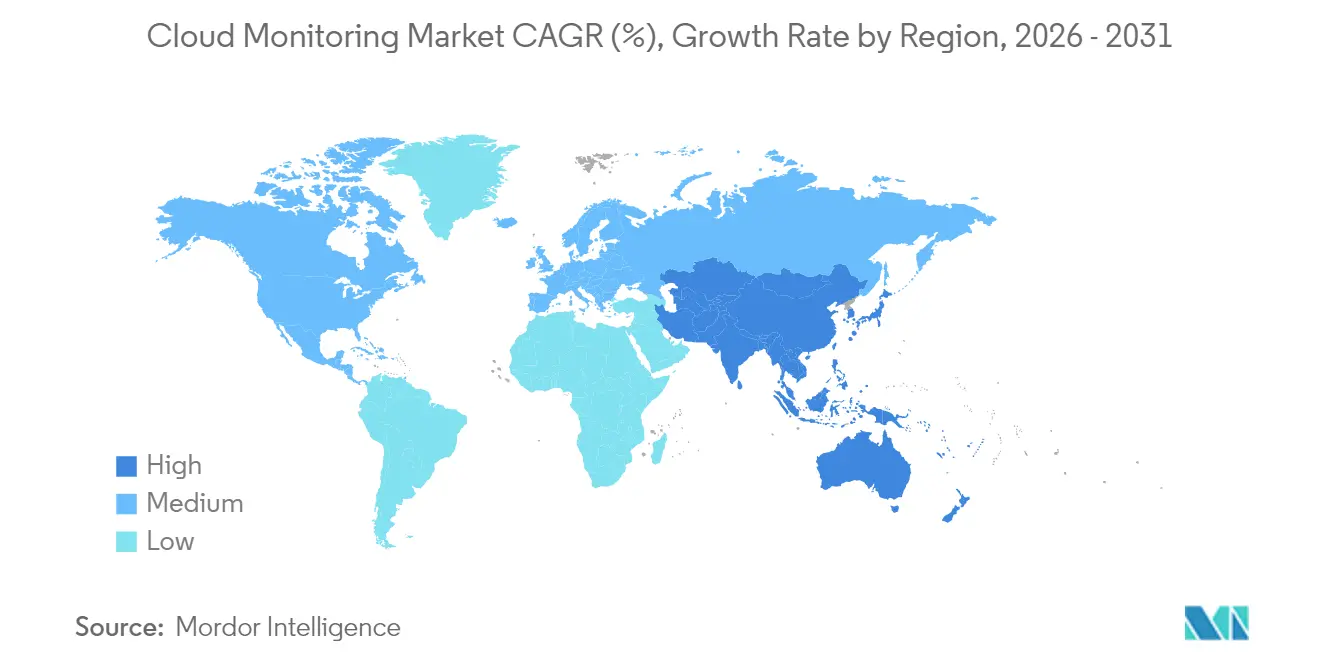

- By region, North America commanded 40.60% revenue in 2025; Asia Pacific is the quickest-expanding geography at 20.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated multi-cloud and hybrid-cloud adoption | +4.20% | Global, with a concentration in North America & Europe | Medium term (2-4 years) |

| DevOps/SRE culture and need for real-time observability | +3.80% | Global, led by North America, is expanding in APAC | Short term (≤ 2 years) |

| AI/ML workload explosion requiring GPU-level monitoring | +3.50% | North America & APAC core, spill-over to Europe | Medium term (2-4 years) |

| FinOps accountability and cost-to-value optimisation pressure | +2.90% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Sustainability dashboards for cloud-carbon reporting | +1.80% | Europe-led, expanding to North America & APAC | Long term (≥ 4 years) |

| Sovereign-cloud and data-localisation mandates | +2.10% | Europe & APAC core, selective adoption in other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Multi-Cloud and Hybrid-Cloud Adoption

Multi-cloud usage crossed a tipping point, with 43% of financial-services firms already distributing workloads across two or more hyperscalers in 2024. Each provider exports unique metrics, so operations teams face telemetry sprawl and blind spots. Unified platforms that normalise data across AWS, Azure, and Google Cloud are therefore replacing single-cloud monitors. Adoption of OpenTelemetry agents rose sharply because vendor-neutral instrumentation eases estate-wide coverage. Organisations also need correlated cost, performance, and compliance views when the same transaction spans on-premises and cloud nodes. These pressures elevate hybrid-cloud observability from optional to indispensable capability, pushing the cloud observability market toward deeper end-to-end context.

DevOps/SRE Culture and Real-Time Observability

Site Reliability Engineering is mainstreamed in large enterprises, cutting mean outage costs that exceed USD 1 million per hour[1]Buddy Brewer, “The Economics of Observability,” New Relic, newrelic.com. Teams now embed golden signals and service-level objectives into CI/CD pipelines so that defects surface before production rollouts. Full-stack insight lowers downtime by 79% versus siloed toolchains. AI-driven anomaly detection augments humans by surfacing precursors to incidents across logs and traces. Faster feedback loops also boost developer productivity, turning observability into a direct business enabler. The cloud observability market, therefore, benefits from budgets shifting left toward engineering teams rather than traditional IT operations.

AI/ML Workload Explosion Requiring GPU-Level Monitoring

Language-model training and real-time inference push GPU clusters to cost hundreds of dollars per hour, demanding granular utilisation metrics. Vendors now expose tensor-core heat, memory bandwidth, and energy draw within the same dashboards that track latency. Datadog’s purchase of Metaplane extended coverage to data-pipeline quality, proving that model accuracy and infrastructure health must be observed together. Edge cases, such as AI agents acting autonomously, need continuous policy-compliance checks. These specialised requirements expand the addressable base for the cloud observability market far beyond classic application performance monitoring.

FinOps Accountability and Cost-to-Value Optimisation Pressure

Observability ingestion can consume 15-25% of cloud spend, so finance leaders demand ROI proof. New platforms apply intelligent sampling and retention tuning to shrink storage without losing critical context. FinOps dashboards now attribute spend down to feature or customer level, enabling charge-back and optimisation decisions. Consumption-based licensing models are replacing host-based pricing that penalized Kubernetes density. This fiscal discipline aligns vendor success with customer savings, enhancing stickiness across all tiers of the cloud observability market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited visibility in containerised, serverless stacks | -2.80% | Global, particularly affecting cloud-native organizations | Short term (≤ 2 years) |

| Rising TCO of full-stack observability platforms | -3.20% | Global, with higher impact in cost-sensitive regions | Medium term (2-4 years) |

| Skills gap for observability engineering | -2.10% | Global, acute in APAC & emerging markets | Long term (≥ 4 years) |

| Hyperscaler API-rate limits, throttling, deep telemetry | -1.90% | Global, affecting high-volume data analytics users | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Visibility in Containerised, Serverless Stacks

Containers may live for seconds, while serverless functions spin up without agents, leaving gaps that legacy monitors cannot fill. Kubernetes adds torrent-level metadata, so brute-force collection inflates storage bills. Distributed tracing that stitches request paths across microservices, combined with eBPF-based low-overhead instrumentation, is emerging as the remedy. OpenTelemetry is pivotal yet still complex to deploy, explaining slower adoption among resource-constrained SMEs. Until turnkey instrumentation matures, observability gaps in ephemeral environments will drag on the cloud observability market CAGR.

Rising TCO of Full-Stack Observability Platforms

Enterprises now store petabytes of telemetry for compliance audits, escalating storage and egress fees that can overtake license costs[2]Martin Mao, “Taming Telemetry Volume at Scale,” Chronosphere, chronosphere.io . Proprietary pricing, often mixing host count and data volume, frustrates budget forecasting. In response, customers adopt open-source back-ends such as ClickHouse or Loki while retaining vendor UI layers or negotiate data tiering that keeps cold logs in cheaper object stores. Vendors are racing to deliver auto-tuning pipelines that drop low-value noise before it ever hits disk. Cost control innovations must keep pace, or some buyers will delay rollouts, capping worst-case revenue upside for the cloud observability market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cloud Service Model: SaaS Dominance Meets PaaS Innovation

SaaS platforms anchored 47.80% of 2025 revenue, underscoring demand for turnkey deployments that remove infrastructure overhead. PaaS solutions shape the fastest lane, growing 28.45% CAGR as users crave deeper code-level insight without managing collectors. IaaS tools retain relevance for hybrid estates that need on-premises collectors close to regulated data. The cloud observability market size for SaaS is forecast to widen by USD 2.92 billion between 2026 and 2031 as lagging industries migrate to managed services.

PaaS momentum reflects platform-engineering teams embedding observability into internal developer portals. Big-tech vendors integrate tracing, chaos testing, and KPI dashboards directly into build pipelines, reducing cognitive load. Combined with OpenTelemetry auto-instrumentation, this synergy accelerates time to value. Consequently, the cloud observability market records almost one-third of net-new bookings from PaaS deals targeting AI model observability and cost analytics.

By Component: Solutions Lead While Services Accelerate

Solution suites captured 61.30% revenue in 2025, covering data lakes, correlation engines, and UX analytics. Services consulting, onboarding, and managed observability grow 18.85% CAGR as enterprises struggle to hire observability engineers. Integrator demand is highest in regulated verticals where instrumentation must map to control frameworks.

Vendor roadmaps now bundle advisory hours, certified training, and quick-start packs that shorten proof-of-value cycles. LogicMonitor’s USD 800 million funding earmarked for services expansion signals how professional expertise becomes a key moat. As frameworks evolve, recurring service contracts will comprise a larger slice of the overall cloud observability market revenue, deepening partner ecosystems.

By Deployment Mode: Public Cloud Leadership with Hybrid Surge

Public-cloud deployments represented 56.40% income in 2025, thanks to latency-free data flow within single VPCs. Hybrid and multi-cloud options, however, record 23.95% CAGR as organisations hedge against lock-in and pursue workload portability. The cloud observability market share for multi-cloud stacks will surpass 30.50% by 2031 if current deal velocity holds.

Data-sovereignty rules in Europe and Asia force some workloads on-premises or in sovereign regions, increasing the need for topology-agnostic visibility. Cisco’s acquisition of Splunk highlights demand for platforms spanning data centres, edge, and clouds. Seamless license portability and federated dashboards now appear on every enterprise RFP, anchoring hybrid appeal.

By Organisation Size: Enterprise Stability Versus SME Dynamism

Enterprises supplied 62.20% of 2025 billings, driven by vast telemetry volume and bespoke analytics. SMEs, empowered by usage-based pricing, deliver 18.05% CAGR as they embed observability on day one of product builds. The cloud observability market size for SMEs is projected to reach USD 2.18 billion by 2031.

Startup developers choose SaaS tiers that auto-scale, shifting budget from headcount to managed tooling. As SMEs mature, they often keep the same vendor, lifting lifetime value. Vendors respond with tiered SKUs and community editions that convert freemium users at low acquisition cost, sustaining segment momentum.

By End-User Industry: IT Leadership with Retail Acceleration

IT and telecom retained a 28.60% share due to complex micro-service estates and stringent SLAs. Retail & e-commerce posts 17.25% CAGR as one-second page delays erode cart revenue. The cloud observability market size for retail could top USD 1.33 billion by 2031 if current digital-commerce growth holds.

In BFSI, real-time fraud analytics and regulatory audit trails drive deep tracing adoption. Healthcare pursues HIPAA-aligned dashboards that encrypt telemetry at rest. Manufacturing links plant-floor sensors to cloud diagnostics for predictive maintenance. Cross-industry expansion underlines the cloud observability market breadth, with vertical modules tailoring terminology and compliance widgets.

Geography Analysis

North America commanded 40.60% of 2025 revenue, reflecting decades-long DevOps maturity and heavy AI investment. Financial institutions cite median outage losses of USD 10.44 million per year, justifying premium tooling. Sovereign-cloud talk is muted, yet privacy laws still nudge data residency features. Growth moderates to low teens after 2027 as replacement cycles saturate, but AI observability upgrades sustain license expansion.

Asia Pacific is the fastest mover at 20.85% CAGR, propelled by cloud-first start-ups and government digital drives. India’s public cloud outlay could reach USD 25.5 billion by 2028. Observability ROI tops 114% in Singapore and Indonesia, showcasing high payoff for downtime reduction. China’s 6.192 trillion-yuan cloud sector, led by Alibaba Cloud’s 43% hold, fuels local-language dashboards and in-country data lakes.

Europe records mid-teens CAGR as GDPR and upcoming AI Act cement data-protection demands. Accenture notes 37% of enterprises investing in sovereign cloud, with 44% planning more within two years. Vendors partner with regional hosts to ensure EU-located logging pipelines. Energy dashboards gain traction as climate reporting merges with performance metrics. These regional nuances collectively propel the cloud observability market toward diverse compliance-aware deployments.

Regulatory Landscape

Compliance requirements for cloud monitoring are increasingly tied to continuous assurance, incident reporting, and evidence quality across sovereign and public cloud deployments. In the United States, FedRAMP released a Public Preview of its Consolidated Rules for 2026 in May 2026, standardizing expectations for cloud service providers through December 31, 2028. The guidance formalizes a shift toward FedRAMP 20x pipelines and collaborative continuous monitoring practices that emphasize monitoring, logging, and machine-consumable security artifacts.

In parallel, NIST published SP 800-172 Rev. 3 in May 2026, strengthening enhanced security requirements for protecting Controlled Unclassified Information in nonfederal systems. That strengthens the compliance focus on monitoring, auditing, and system integrity for vendors serving regulated buyers. In Europe, Commission Implementing Regulation (EU) 2024/2690 (adopted October 17, 2024) under the NIS2 framework increases pressure on cloud providers to operationalize security logging, detection, and incident reporting thresholds, reinforcing demand for monitoring platforms that support auditable retention, alerting governance, and regional data-handling constraints.

Value Chain Analysis

The cloud monitoring value chain starts with instrumentation and telemetry generation (agents, OpenTelemetry collectors, SDKs, eBPF sensors) and extends through data transport and processing (streaming, indexing, time-series and log storage). It then moves into correlation and analytics (AIOps, tracing, root-cause analysis) and user-facing workflows (dashboards, SLOs, incident response integrations). Hyperscalers (AWS, Microsoft Azure, Google Cloud) provide native metrics, logs, and traces, while independent vendors (for example, Datadog, LogicMonitor, Zenoss, IDERA) differentiate through cross-cloud normalization, hybrid coverage, and specialized analytics such as GPU and cost visibility.

Channel partners and services providers (consulting, managed observability, and system integrators) operationalize deployments by integrating monitoring into CI/CD, ITSM, and security operations, and by tuning telemetry pipelines to control cost and retention. Standardization shapes handoffs across the chain: ITU-T Y.3556 (August 2025) defines a framework for microservice monitoring functions, while ISO/IEC TR 23951:2025 (April 2025) and ISO/IEC TR 10822-1:2025 (May 2025) codify practices for cloud SLA metric models and multi-cloud management (including monitoring and reporting). These standards support more consistent SLO reporting and procurement requirements across heterogeneous environments.

Competitive Landscape

The market remains moderately fragmented. Datadog posted USD 762 million Q1 2025 sales, up 25% YoY, while Dynatrace reached USD 1.647 billion ARR, up 16%. Cisco’s USD 28 billion Splunk buyout signals convergence between security and observability, raising entry barriers. Meanwhile, challenger Chronosphere touts cost-efficient time-series ingest built on open-source M3.

Strategic differentiation concentrates on AI workload probes, FinOps metrics, and policy-ready data controls. Datadog’s Metaplane pick-up expands data lineage views critical for model governance. ClickHouse’s HyperDX deal inserts high-speed columnar storage under an OpenTelemetry-native UI. Hyperscalers bundle native monitoring yet still certify third-party partners for hybrid reach, protecting independent vendors.

Patents around distributed sampling and GPU telemetry deepen protective moats. Vendors file for automated anomaly-explanation engines that summarise root cause narratives. Ecosystem partnerships with enterprise resource planning, incident-response chatops, and ticketing systems enhance stickiness. The competitive chessboard will likely tilt toward platform suites that integrate security, cost, and sustainability signals without forcing data egress, reinforcing customer lock-in, yet lowering integration toil.

Cloud Monitoring Industry Leaders

AWS

Broadcom Inc. (CA Technologies)

IDERA Inc.

LogicMonitor Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standardized instrumentation and first-party support for open telemetry formats create whitespace for vendors to simplify adoption, reduce integration friction, and compete on analytics rather than proprietary data collection. OpenTelemetry graduated within CNCF in May 2026, and hyperscalers expanded direct support for OpenTelemetry-driven workflows, including Amazon CloudWatch adding native OpenTelemetry metrics with PromQL querying (June 2026). As enterprises consolidate point tools into unified platforms to manage cost and complexity, differentiation increasingly centers on data portability, governance-ready retention, and cross-cloud correlation that can be implemented without re-instrumenting every service.

AI and agentic operations also expand the monitoring surface area across GPUs, data pipelines, and autonomous agents. This creates opportunities for products that connect infrastructure health to model behavior and business impact. Vendor roadmaps show increased investment in this direction, including Microsoft introducing an Azure Copilot Observability Agent within Azure Monitor (June 2026) and Elastic launching native Prometheus support alongside agentic investigation workflows (June 2026). On the workflow side, Google Cloud previewed SQL-based alerting in Observability Analytics, indicating broader movement toward query-native, self-service observability for engineering and SRE teams that need faster iteration on detection logic and operational reporting.

Recent Industry Developments

- May 2026: LogicMonitor announced a collaboration with IBM and Red Hat to integrate IBM watsonx and Red Hat Ansible Automation Platform into its Edwin AI agent. The partnership links observability insights to automation and AI-assisted operations, supporting faster remediation across hybrid estates that combine on-premises and cloud infrastructure.

- April 2025: Cisco closed its USD 28 billion acquisition of Splunk. This combined security and observability capability under one large platform vendor raises the bar for standalone monitoring providers seeking to prove differentiated value in hybrid and multi-cloud environments.

- December 2024: Oracle released Oracle Enterprise Manager 24ai, adding AI-based impact analysis and tighter integration with OCI Observability and Management. The update strengthens Oracle-centric monitoring for enterprises running mixed OCI and on-premises estates, reinforcing the role of integrated toolchains for governance and operational visibility.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cloud monitoring market is measured as the revenue earned from tools and related services used to track performance, availability, and health of cloud-based infrastructure and applications. We focus on monitoring signals such as uptime, response time, and workload metrics across public, private, and hybrid environments.

Scope exclusions: We exclude broader IT operations work that is not tied to cloud monitoring outcomes, such as general IT helpdesk services and cybersecurity-only tools that do not map to cloud monitoring performance or reliability metrics.

Segmentation Overview

- By Cloud Service Model

- IaaS

- PaaS

- SaaS

- By Component

- Solution

- Services

- By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid/Multi-Cloud

- By Organisation Size

- SMEs

- Large Enterprises

- By End-User Industry

- BFSI

- Retail and e-Commerce

- IT and Telecommunications

- Healthcare and Life Sciences

- Government and Public Sector

- Manufacturing

- Others (Media, Energy, Education)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest Asia Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning the market boundaries and the time series with public indicators that are available consistently across regions. We reviewed sources such as the US Bureau of Economic Analysis (digital economy tables), US Census international trade data, Eurostat ICT usage statistics, OECD digital economy indicators, and the International Telecommunication Union (ITU) connectivity datasets to understand cloud adoption pace and the level of enterprise IT activity.

To ground vendor and customer context, we also used annual reports, SEC filings, earnings call transcripts, and product documentation from software vendors and managed service providers, then checked those with reputable press coverage and association publications related to cloud computing and IT service management. When needed, a paid subscription focused on company financials and news was used to standardize revenue histories, and a patent database was referenced to capture monitoring and observability innovation signals. These examples are not exhaustive, and additional public sources were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to test what buyers actually count as cloud monitoring spend, how budgets split between platform fees and services, and how pricing scales with usage. Topics included the number of monitored hosts and containers, telemetry data ingestion volumes, and retention periods. We spoke with product, engineering, sales, and operations stakeholders across key regions so differences in cloud maturity and procurement patterns could be reflected, and then we rechecked assumptions when responses showed large variance.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 48% |

| Mid tier: 52% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 18% | Managers: 47% | Americas: 20% |

Market-Sizing & Forecasting

Sizing uses a top-down build that starts from cloud software and services spending pools and then narrows them using adoption and usage indicators that map to monitoring demand. In practice, we linked the model to market signals such as public cloud workload growth, the installed base of virtual machines and containers, enterprise DevOps penetration, typical telemetry data volumes (logs, metrics, traces), and the share of environments running hybrid setups, because these variables directly affect monitoring needs and spend intensity.

After forming the first totals, we corroborated them with selective bottom-up checks, including rolling up a sampled set of supplier revenues, validating price bands from channel discussions, and stress-testing implied spend per monitored workload. Where vendor disclosures were incomplete, we used peer benchmarks and applied conservative ranges, then adjusted those ranges after interview feedback. Forecasts were produced using scenario analysis grounded in expert views on cloud migration pace, shifts in pricing model design (consumption versus seat-based), and expected changes in telemetry ingestion and retention behavior.

Data Validation & Update Cycle

Outputs were checked against independent signals to reduce drift from real-world demand, including cloud adoption trends, enterprise IT spending direction, and workload growth measures. When a region or vertical showed an unusual jump, we re-tested the drivers and revisited assumptions through follow-up outreach when needed.

Before sign-off, the model and written assumptions go through multiple analyst reviews focused on unit consistency, year-over-year logic, and currency conversion timing. The report is refreshed annually, and interim updates are made when material events occur, such as sharp pricing changes or major shifts in cloud adoption. Right before delivery, a final review sweep is completed so clients receive the most current view supported by the latest available inputs.

Mordor Intelligence's Cloud Monitoring Market Size Measured Against Other Published Estimates

Published market numbers for cloud monitoring often do not match because each publisher draws the boundary of what counts as monitoring revenue a bit differently, and they also select different base years and currency timing. Differences in whether services are included, how usage-based pricing is treated, and how quickly underlying assumptions are refreshed can also drive noticeable spreads.

The table reflects a split between estimates that stay closer to software platform and related monitoring services, versus estimates that widen into adjacent observability and broader IT operations spending. In Mordor Intelligence's model, the value is counted only when the spend is directly tied to monitoring cloud workloads and performance outcomes rather than broader IT management tool categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.75 B (2025) | |

| Global Consultancy A | USD 2.96 B (2024) | Uses an earlier base year and often applies a narrower inclusion that can exclude portions of monitoring-related services and hybrid monitoring spend, which lowers the captured revenue pool. |

| Industry Publisher B | USD 3.66 B (2025) | Leans on longer forecast horizons and broader functional buckets (for example, folding in adjacent observability or website monitoring categories), and the assumptions are less transparent on usage-based pricing progression and currency timing. |

Overall, the spread is mostly explained by category boundaries, base-year selection, and how usage-linked pricing is converted into annual revenue. By keeping inputs tied to measurable workload and telemetry signals, and then rechecking them through interviews and consistency tests, the resulting estimate is practical to reproduce and easier to audit year by year.

Key Questions Answered in the Report

What is the projected value of the cloud observability market by 2031?

It is forecast to reach USD 10.95 billion by 2031 based on a 19.56% CAGR.

Which region is growing fastest in cloud observability adoption?

Asia Pacific leads with a 20.85% CAGR, spurred by rapid digital-transformation programs and cloud-first start-ups.

Why are PaaS observability tools gaining traction?

They offer deeper code-level insight and quick integration with platform-engineering workflows, expanding at 28.45% CAGR through 2031.

How does FinOps influence observability spending?

FinOps practices demand granular cost attribution, prompting vendors to add usage-based pricing and optimisation dashboards that align monitoring spend with business value.

What is driving vendor consolidation in this market?

The need to unify security, AI workload monitoring, and compliance features pushes larger vendors to acquire niche specialists, exemplified by Cisco’s Splunk and Datadog’s Metaplane deals.

What challenges limit observability in serverless environments?

Ephemeral runtimes and agentless execution create data blind spots, requiring distributed tracing and eBPF instrumentation to maintain end-to-end visibility.

Page last updated on: