Industrial Workwear Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 19.38 Billion |

| Market Size (2030) | USD 24.66 Billion |

| Growth Rate (2025 - 2030) | 4.93% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Industrial Workwear Market Analysis by Mordor Intelligence

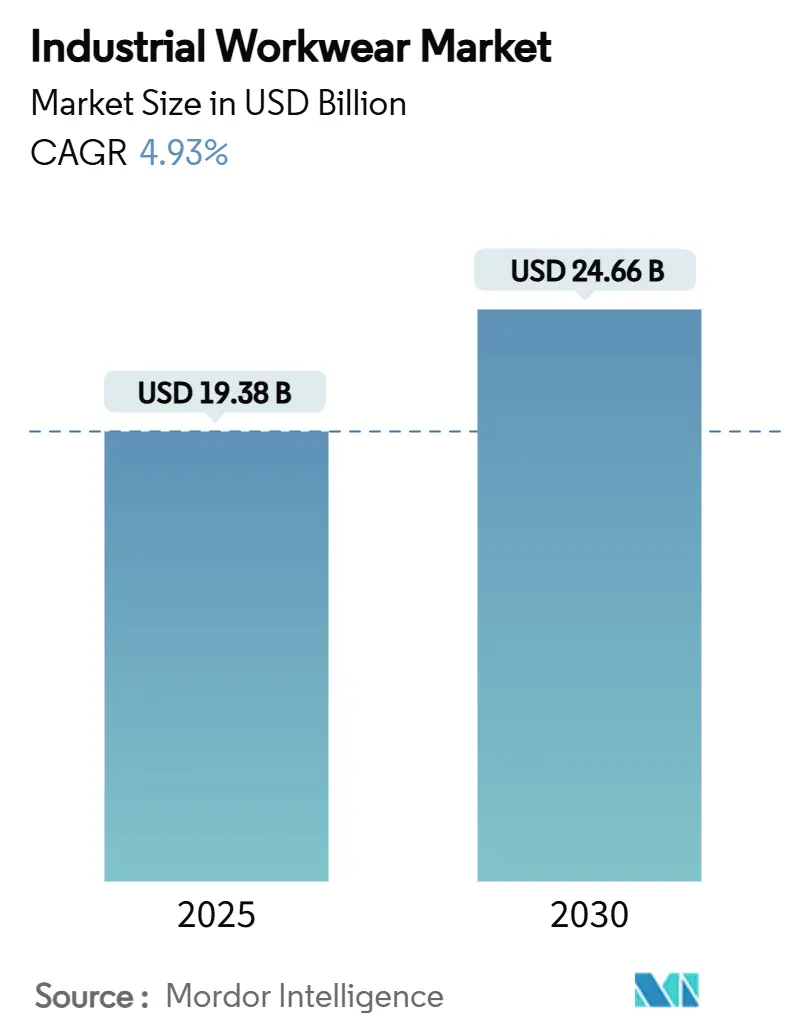

The industrial workwear market size stands at USD 19.38 billion in 2025 and is projected to reach USD 24.66 billion by 2030, registering a CAGR of 4.93% during the forecast period. OSHA's January 2025 mandate on personal protective equipment (PPE) fit has intensified regulatory scrutiny, prompting quicker replacement cycles and a surge in demand for designs catering to diverse body types[1]Source: United States Department of Labor," Department of Labor finalizes rule on proper fit requirements for personal protective equipment in construction", www.dol.gov. This mandate underscores the importance of ensuring PPE provides adequate protection and comfort, addressing safety concerns across a wide range of industries. Employers, aiming to mitigate litigation risks and improve workplace safety standards, are prioritizing injury-prevention initiatives. This focus has driven the adoption of advanced flame-resistant and high-visibility apparel, particularly those incorporating ergonomic features that enhance worker comfort, mobility, and overall safety during extended use. Additionally, the digitization of procurement processes is channeling incremental growth toward e-commerce platforms, which offer convenience, extensive product catalogs, and competitive pricing. Despite this shift, brick-and-mortar distributors remain relevant by leveraging their ability to maintain local inventory, provide immediate product availability, and offer personalized support tailored to specific customer requirements, ensuring they continue to meet the needs of their client base effectively.

Key Report Takeaways

- By product type, protective workwear led with 64.86% of 2024 revenue, while general workwear is forecast to expand at a 5.64% CAGR through 2030.

- By gender, male workers held 78.48% of the 2024 demand; the female segment is projected to grow at a 5.83% CAGR between 2025-2030 .

- By distribution channel, offline retail stores captured 82.44% of 2024 sales, whereas online channels are set to advance at a 5.54% CAGR to 2030.

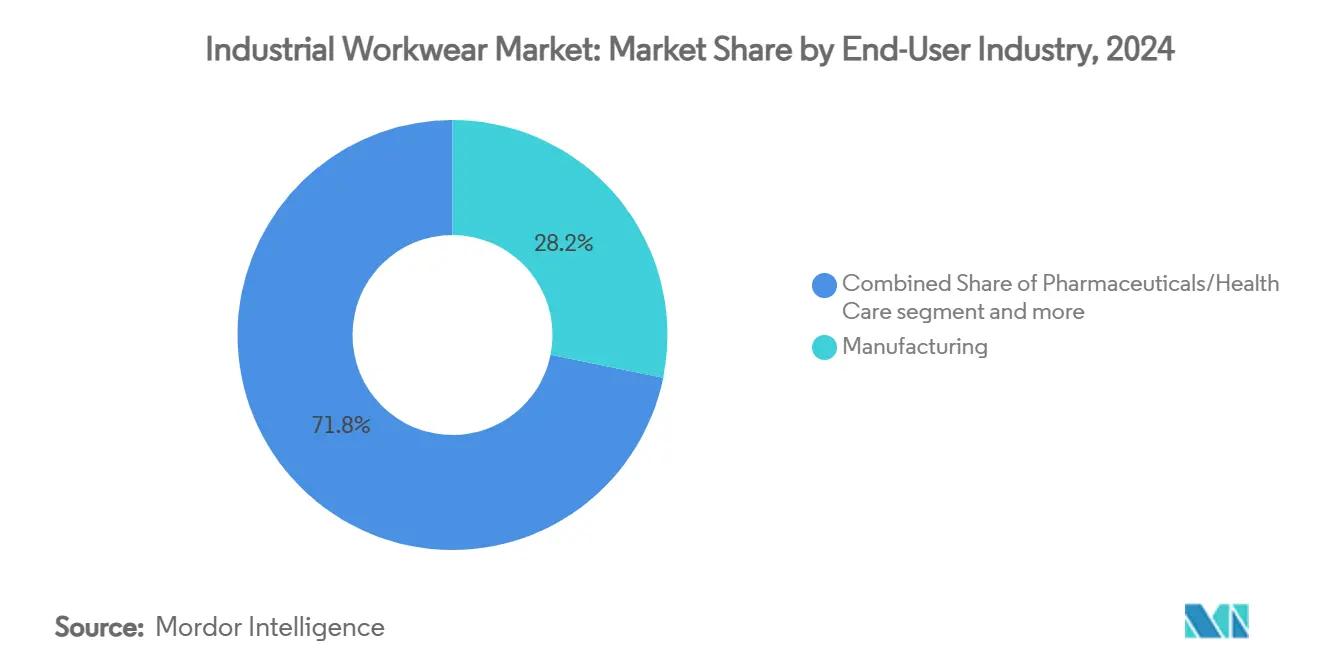

- By end-user, manufacturing accounted for 28.18% share of the 2024 industrial workwear market size, while pharmaceuticals and healthcare are pacing at a 5.47% CAGR through 2030.

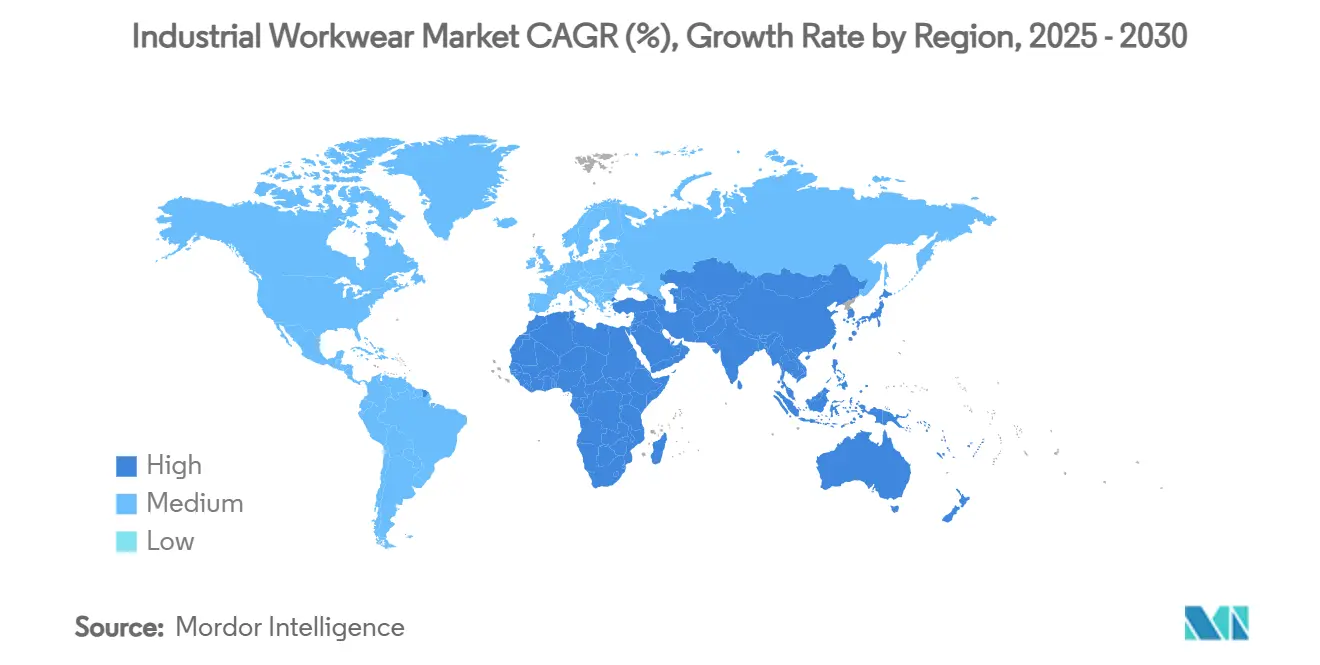

- By geography, Asia-Pacific commanded 39.68% of 2024 industrial workwear market share; the Middle East and Africa is projected to record the fastest regional CAGR of 6.24% over 2025-2030.

Global Industrial Workwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent workplace-safety regulations | +1.2% | Global, with strongest impact in North America and EU | Medium term (2-4 years) |

| Expansion of manufacturing and construction sectors | +1.0% | Asia-Pacific core, spill-over to MEA and North America | Long term (≥ 4 years) |

| Growing employer liability awareness | +0.8% | Global, particularly developed markets | Short term (≤ 2 years) |

| Rising demand for FR and high-visibility apparel | +0.7% | North America, EU, and industrial-heavy Asia-Pacific regions | Medium term (2-4 years) |

| Integration of IoT sensors into workwear | +0.5% | Developed markets initially, expanding to emerging economies | Long term (≥ 4 years) |

| Sustainability-driven demand for recycled fabrics | +0.3% | EU leading, followed by North America and select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent workplace-safety regulations

U.S. construction firms must now provide properly fitting PPE, as mandated by OSHA's 2025 revision. This move ends the era of one-size-fits-all procurement and expands the market for ergonomic designs, addressing the need for enhanced worker safety and comfort. In tandem, proposals aimed at preventing heat-related illnesses stipulate the provision of cooling gear when heat indices surpass 80 °F. This adds a seasonal surge in demand for breathable, moisture-wicking garments, particularly in regions prone to high temperatures. Across the globe in Kenya, a new Occupational Safety and Health Authority is set to enforce standards, responding to 6,979 recorded incidents in 2023. This initiative highlights the growing emphasis on workplace safety in emerging markets. Meanwhile, the UAE not only mandates that employers provide protective clothing but also prohibits outdoor work during peak heat hours. This has led to a heightened demand for UV-resistant and cooling fabrics, reflecting the region's proactive approach to mitigating heat-related risks. Together, these global policies are steering employers to allocate budgets towards compliant, gender-specific uniforms, ensuring better protection for a diverse workforce while aligning with evolving regulatory frameworks.

Expansion of manufacturing and construction sectors

Between 2023 and 2033, the U.S. construction sector is set to add approximately 380,100 jobs, marking a 4.7% growth. A significant portion of these jobs will be linked to the burgeoning fields of renewable energy infrastructure and data center expansions. Since 2021, spending on manufacturing construction has more than doubled, a surge largely attributed to the CHIPS Act's USD 50 billion semiconductor incentive[2]Source: United States Department of Commerce,"Manufacturing Booms Thanks to Biden-Harris Administration Investments", www.commerce.gov. This uptick in manufacturing has spurred a heightened demand for specialized items like clean-room coveralls and electrostatic-dissipative garments. Across Asia, governments are actively promoting shifts towards advanced manufacturing. For instance, India's Production Incentive Scheme is championing research and methodology in technical textiles, while Indonesia's "Making Indonesia 4.0" initiative is steering the nation towards high-value production lines that necessitate advanced personal protective equipment (PPE). In Canada, the construction sector, which currently employs 1.6 million individuals, anticipates a steady 1.5% annual labor growth through 2033. This growth trajectory is poised to further amplify North America's appetite for protective apparel. Such global expansions in capacity underscore a resilient upward trend in the industrial workwear market, even amidst broader economic slowdowns.

Growing employer liability awareness

As litigation costs rise, boards are increasingly viewing worker safety as both a financial and ethical imperative. U.S. construction accidents are costing companies an estimated USD 11.5 billion annually, a figure that could be reduced with targeted PPE programs. Carhartt's AI-driven ergonomics initiative has successfully halved recordable incidents across several plants, showcasing the tangible ROI of tailoring apparel for specific movements. This demonstrates how integrating technology into PPE design can directly impact workplace safety and operational costs. In the Gulf, studies linking extreme heat exposure to kidney failure are leading regulators to tighten oversight, boosting sales of cooling vests and phase-change garments. These garments are designed to regulate body temperature, ensuring worker safety in harsh climates while reducing health-related risks. In the UAE, regulations mandating employers to report injuries and compensate victims bolster the argument for premium protective solutions that mitigate claim exposures. Such regulations not only protect workers but also incentivize businesses to invest in advanced PPE to avoid financial and reputational damages. This trend positions advanced PPE not just as an optional expense, but as a vital asset in risk mitigation.

Rising demand for FR and high-visibility apparel

In November 2024, OSHA mandated updates for high-visibility clothing, emphasizing fluorescent colors and ANSI-rated retro-reflective trims. This regulatory change has prompted a swift replacement of older vests and jackets across industries to ensure compliance with the updated safety standards. Meanwhile, in South Africa, labor unions, reacting to rising fatal accident rates in hazardous work environments, are advocating for increased adoption of globally certified flame-resistant (FR) apparel[3]Source: International Trade Administration,"South Africa National Occupational Safety Sector", www.trade.gov. This demand is particularly pronounced in sectors like mining and heavy construction, where workers face elevated risks. DuPont’s Tyvek® 500 HP garment, crafted for harness compatibility, exemplifies a growing trend in multi-hazard protection. This innovative product integrates chemical, fall, and visibility safeguards into a single SKU, addressing multiple safety concerns simultaneously. In parallel, oil and gas, along with chemical companies, are expanding their contract specifications to include arc-flash-rated materials with moisture management capabilities. These enhanced requirements are driving up average order values as companies prioritize worker safety and regulatory compliance. Lakeland Industries’ Fire Services division reported a staggering 226% revenue surge in Q4 2025, highlighting the strong and growing demand for next-generation FR solutions. This growth reflects a broader industry shift toward advanced protective apparel that meets evolving safety standards and addresses the complex needs of high-risk work environments.

Restraint Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices | -0.9% | Global, with strongest impact in price-sensitive markets | Short term (≤ 2 years) |

| Proliferation of low-cost unbranded products | -0.6% | Emerging markets and price-competitive segments | Medium term (2-4 years) |

| Cyclical cap-ex in heavy industries | -0.4% | Industrial-heavy regions, particularly during economic downturns | Medium term (2-4 years) |

| Data-privacy pushback against smart workwear | -0.2% | Developed markets with strict privacy regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile raw-material prices

Over the last cycle, cotton prices fluctuated between USD 0.60 and nearly USD 2.00 per pound. This significant price volatility forced apparel makers, like garment supplier Topeco, to either absorb the cost spikes or raise their prices, with Topeco implementing a 20% retail price increase in 2024 to offset rising input costs. Sustainability regulations, including the U.S. Cotton Trust Protocol and the upcoming phase-outs of PFAS, are further intensifying margin pressures by narrowing the pool of acceptable materials and increasing compliance costs. While polyester and viscose serve as substitutes, they offer only limited relief due to performance compromises in key areas such as breathability and flame resistance, which are critical for certain applications. As mandates for recycled yarns gain traction globally, mills are compelled to invest in costly mechanical and chemical recycling lines to meet regulatory requirements. These added expenses inevitably get passed on to finished goods pricing, potentially limiting order volumes, especially in price-sensitive contracts, as buyers may seek alternative suppliers or materials to manage costs.

Proliferation of low-cost unbranded products

Online marketplaces empower small-scale manufacturers to sidestep traditional distributors. This shift has led to an influx of price-centric SKUs, complicating procurement decisions, especially in emerging economies where cost sensitivity is high. While budget-friendly items may catch the eye, OSHA's fit requirement challenges the prevalent one-size-fits-all approach found in unbranded catalogs, as these products often fail to meet safety and compliance standards. As a result, premium brands are urged to emphasize the total cost of ownership in their messaging. This includes highlighting benefits like extended service life, compliance assurances, and enhanced worker productivity, which can justify the higher upfront costs. To combat commoditization and safeguard margins, the marketing narrative is increasingly centered on tangible safety outcomes, such as reduced workplace injuries and improved operational efficiency, which resonate strongly with procurement decision-makers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protective Wear Dominates but Everyday Garments Accelerate

In 2024, protective wear commands a dominant 64.86% share of the industrial workwear market, driven by stringent global safety regulations. These regulations mandate the use of flame-resistant, chemical-resistant, and high-visibility garments in hazardous work environments. Continuous updates to safety specifications fuel ongoing retrofits and replacements in sectors like heavy manufacturing, energy, and infrastructure. Innovations, including stretch panels, gender-specific sizing, and sensor pockets, align with OSHA’s emphasis on fit and comfort, all while upholding safety standards. Furthermore, tech-enabled fabrics that monitor ambient temperatures or detect toxic gases are entering pilot phases. This suggests a future where personal protective equipment (PPE) evolves into a sophisticated platform for safety data collection and analytics. Such a blend of compliance and innovation solidifies protective wear's position as the largest and most critical segment in industrial workwear. Its resilience is largely attributed to its essential role in fulfilling mandatory safety needs, a non-negotiable aspect for employers globally.

On the other hand, the general workwear segment, holding a smaller 35.14% market share, is set to outpace the overall industrial workwear market with a robust projected growth rate of 5.64% CAGR through 2030. This surge is driven by the rising prominence of service-oriented roles in factories, logistics centers, and support functions. In these settings, comfort, style, and employee brand engagement have taken center stage. Today's general workwear boasts advanced features like moisture management, odor control, and stain resistance—traits once exclusive to premium sportswear. As competition for skilled workers intensifies, employers leverage these enhanced uniforms not just for brand perception but also to uplift employee morale. The lines between traditional workwear categories are increasingly blurred; for instance, stretch ripstop fabrics now meld durability and abrasion resistance with all-day comfort. This evolution mirrors a workforce's growing preference for multifunctional garments. By catering to a more diverse and service-oriented industrial workforce, this dynamic, innovation-driven segment is carving out its identity as a pivotal growth area.

By Gender: Inclusive Design Unlocks Untapped Demand

In 2024, male workers dominated industrial workwear purchases, accounting for 78.48% of the market. This trend mirrors traditional labor patterns in sectors like construction, mining, and heavy manufacturing, where male workers have long been the majority. Growth in this segment is tempered, as replacement rates align closely with mandated inspection and safety cycles, curbing the pace of demand. To stimulate repeat purchases and foster enduring customer relationships, manufacturers are prioritizing durability enhancements and rolling out extended warranty programs. In a bid to bolster brand loyalty amidst rising market competition, they're also adopting digital fitting applications that accurately gauge body dimensions, aiming to curtail return rates. Despite the tempered growth, this segment's substantial size and consistent replacement needs solidify its status as the cornerstone of industrial workwear consumption.

On the other hand, while females made up a smaller 21.52% of purchases in 2024, this segment is set to outpace others with a projected 5.83% CAGR through 2030. Heightened regulatory scrutiny on the fit and ergonomics of female-specific personal protective equipment (PPE), underscored by OSHA’s fit mandates and EU gender-inclusion guidelines, is prompting employers to seek out separate SKUs tailored for women. As awareness grows regarding health issues stemming from ill-fitting garments, buyers are increasingly valuing features like proper grading, bust darts, and designs accommodating maternity needs. Brands that offer a broad spectrum of sizes, from petite to plus, and include gender-neutral options, are gaining traction by meeting these demands. This momentum is especially pronounced as more women step into skilled trades and supervisory positions, driving fresh procurement cycles. With a heightened focus on fit, comfort, and inclusivity, the female segment emerges as a dynamic growth frontier in the industrial workwear landscape.

By End-User Industry: Manufacturing Holds Scale, Healthcare Surges

In 2024, the manufacturing sector leads the industrial workwear market, accounting for 28.18% of its total size. This dominance stems from vast factory operations and intricate risk scenarios, underscoring the need for diverse personal protective equipment (PPE) for both production and maintenance teams. Even with the rise of automation, the demand for industrial apparel remains strong. Robotics technicians and maintenance engineers continue to confront significant risks, including arc-flash incidents and chemical splashes. The manufacturing segment enjoys the advantage of long-term master supply agreements, ensuring bulk purchases and paving the way for product line extensions. These extensions include specialized items, such as anti-static smocks for electronics assembly. Such agreements not only guarantee manufacturers a consistent revenue stream but also deepen customer ties through ongoing product innovation and customization. These elements firmly establish manufacturing as the bedrock of industrial workwear consumption.

Meanwhile, the pharmaceuticals and healthcare sector, while smaller in 2024, emerges as the fastest-growing end-use category, boasting a projected CAGR of 5.47% through 2030. This segment's growth is propelled by the specialized demands of biologics manufacturing, cell therapy suites, and the production of high-potency active pharmaceutical ingredients (APIs). These processes necessitate sterility-assured coveralls and premium protective garments. Recent strategic maneuvers, like Ansell’s acquisition of Kimberly-Clark’s PPE unit with a focus on clean-room applications, underscore the influx of capital into these lucrative niche markets. Furthermore, bolstered by post-pandemic budgets for infection control, there's a sustained demand for disposable isolation gowns and reusable barrier garments. These are crafted from fabrics compatible with sterilization. The segment's growth is not just a result of stringent regulatory mandates but also a heightened awareness of contamination control, marking pharmaceuticals and healthcare as a pivotal growth area in the industrial workwear landscape.

By Distribution Channel: E-Commerce Gains but Physical Networks Retain Dominance

In 2024, industrial workwear saw a dominant 82.44% market share captured by offline retail and distributor outlets. This strong presence underscores the enduring importance of physical interactions, such as touch-and-try fitting sessions, fabric feel assessments, and on-site embroidery services, all of which are challenging to replicate in the online realm. Safety managers, for instance, often prefer face-to-face consultations to ensure adherence to ANSI or EN safety standards, utilizing vendor sizing kits for accurate garment fitting. Moreover, these offline channels provide essential services like quick repairs and loaner fleets, significantly reducing production downtime from accidental damages. The immediacy and tailored support from these outlets solidify their vital role in the industrial workwear supply chain. The trust and hands-on expertise found in physical locations continue to nurture strong loyalty among industrial procurement teams.

On the other hand, while online platforms held a smaller slice of the market in 2024, they're set to emerge as the fastest-growing segment, boasting a projected CAGR of 5.54% through 2030. This surge is driven by the rise of B2B digitization and the inclinations of millennial procurement managers, who lean towards self-service portals for their convenience. Cutting-edge technologies, including high-definition product imagery, augmented reality try-ons, and tailored customer purchasing portals, are refining replenishment processes, especially for firms overseeing multiple plants. The growth is further bolstered by hybrid fulfillment models, enabling online orders to be delivered via regional service centers that manage customizations and quality checks. Consequently, brands are recognizing the necessity of omni-channel fluency to sustain market share and optimize distribution costs. The online channel's growth signifies a pivotal shift in the procurement and customization of industrial workwear in our digitally-driven world.

Geography Analysis

In 2024, the Asia-Pacific region commanded a dominant 39.68% share of the global industrial workwear market, underscoring its pivotal role in worldwide manufacturing and construction. As China, India, and Vietnam unveil new semiconductor, electric-vehicle, and renewable-energy facilities, they're simultaneously onboarding tens of thousands of workers requiring personal protective equipment (PPE). Government stimulus packages, emphasizing local content, are not only boosting the adoption of domestically produced protective garments but also diversifying the supply chain. However, this move complicates the convergence of quality standards. Original Equipment Manufacturers (OEMs) in the region are still adhering to Western certification standards, leading to enhancements in lab testing and traceability systems. Additionally, trade agreements like RCEP are streamlining exports of finished workwear within Asia.

Meanwhile, the Middle East and Africa are on track to be the fastest-growing regions, with projections of a 6.24% CAGR through 2030. Major infrastructure projects, from Saudi Arabia’s ambitious NEOM city to Egypt’s high-speed rail, are spurring a heightened demand for PPE, especially for multinational joint ventures navigating the region's challenging climates. As national oil companies bolster petrochemical clusters, there's a surging need for specialized multi-hazard flame-resistant coveralls, adept at shielding against both flash fires and chemical splashes. Governments are ramping up labor-law enforcement; for instance, the UAE mandates heat-exposure breaks and employer-provided cooling gear, consequently elevating average selling prices. In Kenya, the proposed Safety Authority exemplifies how emerging economies are establishing compliance watchdogs, funded by fees, that require third-party certified garments for project tender eligibility.

North America and Europe, while mature, are witnessing steady growth, fueled by ongoing regulatory updates and technological advancements. OSHA's fit mandate is prompting the replacement of outdated stock, and the EU's Green Deal is championing circular-economy models, promoting longer garment lifespans and enhanced repair services. Both regions are at the forefront of adopting IoT-embedded garments, which monitor biometric data for real-time hazard assessments, consequently driving up average unit costs. South America is experiencing moderate growth, closely linked to the commodity cycle. Yet, political instability and currency fluctuations introduce unpredictability in procurement timing. This regional diversity presents a rich tapestry of opportunities for both global and local suppliers, urging them to customize certifications, fabrics, and distribution strategies to meet varied climate and compliance demands.

Competitive Landscape

The industrial workwear market is moderately fragmented, with no single vendor holding dominant pricing power. Global players like VF Corporation, Honeywell (before its divestiture), and 3M utilize multi-brand portfolios to cater to a diverse customer base. In contrast, regional specialists focus on climate-specific fabrics and speedier customization. Brands are increasingly turning to vertical integration—spanning from yarn spinning to the embroidery of finished garments—as a strategy to counter raw-material volatility. This approach not only safeguards their margins but also enables them to provide shorter lead times to distributors. Furthermore, investments in proprietary fabric blends and the integration of smart wear set established players apart from their low-cost counterparts.

In 2024-2025, merger and acquisition activities saw a notable uptick. Honeywell's USD 1.325 billion divestiture from PPE saw 20 factories and 17 distribution centers transition to Protective Industrial Products (PIP). This move effectively doubled PIP's global footprint. Ansell's acquisition of Kimberly-Clark's PPE assets for USD 640 million bolstered its lineup with Kimtech™ clean-room coveralls, deepening its foothold in the burgeoning pharmaceutical sector. In a strategic move, Kontoor Brands' USD 900 million agreement to acquire Helly Hansen infuses outdoor heritage into its denim-centric portfolio, paving the way for cross-selling opportunities to industrial clients seeking weatherproof garments.

Technology investments are taking center stage: DuPont's Tyvek® 500 HP showcases a shift towards multi-risk convergence products by embedding harness compatibility into its chemical-protective suits. Lakeland Industries celebrated a record Q4 2025 sales figure of USD 46.6 million, buoyed by a staggering 226% surge in revenue from Fire Services. This highlights the potential for niche, high-hazard lines to outpace the broader industrial workwear market. These strategic maneuvers underscore a competitive landscape where specialization, smart fabric integration, and channel diversification are paramount as vendors position themselves for the upcoming procurement cycle.

Industrial Workwear Industry Leaders

-

Carhartt Inc.

-

VF Corporation

-

Cintas Corporation

-

Honeywell International

-

3M Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ALD Engineering & Construction rolled out a program to upgrade workwear and personal protective equipment (PPE). As a key feature of this initiative, the company is replacing outdated canvas suits for welders with advanced gear crafted from the innovative flame-resistant WelderSafe fabric. This specialized material, tailored for welding applications, boasts certifications from international standards ISO 11612 and ISO 11611.

- May 2025: Thorogood Workwear unveiled a new limited-edition collection, proudly made in the USA. Most items in this lineup feature a DWR (Durable Water Repellent) coating, ensuring enhanced protection against the elements. Designed with tradespeople in mind, each piece utilizes premium materials such as Cordura® ripstop canvas, moisture-wicking linings, and boasts triple-needle reinforced stitching for exceptional durability.

- February 2025: Kontoor Brands sealed a deal to acquire Helly Hansen for an estimated USD 900 million. This move diversifies Kontoor's portfolio, extending its reach beyond denim into the outdoor and workwear sectors. Projections indicate the acquisition could yield over USD 680 million in revenue and an adjusted EBITDA of USD 80 million for 2025, bolstering Kontoor's foothold in the expanding workwear market.

- July 2024: Ansell Limited finalized its acquisition of Kimberly-Clark's Personal Protective Equipment business for a substantial USD 640 million. This strategic move not only broadens Ansell's portfolio with the addition of Kimtech™ and KleenGuard™ brands but also amplifies its capabilities in cleanroom applications and scientific markets. Furthermore, the acquisition brings onboard The RightCycle™ Program, promoting sustainable PPE waste disposal, and APEX™ cleanroom management solutions, strategically positioning Ansell for growth in the lucrative pharmaceutical and laboratory sectors.

Global Industrial Workwear Market Report Scope

| General Workwear |

| Protective Workwear |

| Male |

| Female |

| Oil and Gas |

| Manufacturing |

| Construction |

| Mining |

| Chemicals |

| Pharmaceuticals/Health Care |

| Others |

| Offline Channels |

| Online Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | General Workwear | |

| Protective Workwear | ||

| By Gender | Male | |

| Female | ||

| By End-User Industry | Oil and Gas | |

| Manufacturing | ||

| Construction | ||

| Mining | ||

| Chemicals | ||

| Pharmaceuticals/Health Care | ||

| Others | ||

| By Distribution Channel | Offline Channels | |

| Online Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global industrial workwear market in 2025?

The industrial workwear market size is valued at USD 19.38 billion in 2025 and is projected to reach USD 24.66 billion by 2030.

Which region leads current demand for industrial workwear?

Asia-Pacific accounts for 39.68% of 2024 sales due to its vast manufacturing base and ongoing infrastructure expansion.

What is driving the fastest growth segment in industrial workwear?

Inclusive PPE tailored for female workers is growing at a 5.83% CAGR as regulations now require proper fit for all employees.

Which industry vertical is expected to outpace overall market growth?

Pharmaceuticals and healthcare are forecast to advance at a 5.47% CAGR on the back of clean-room expansion and stricter contamination control norms.

Page last updated on: