Cycling Wear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

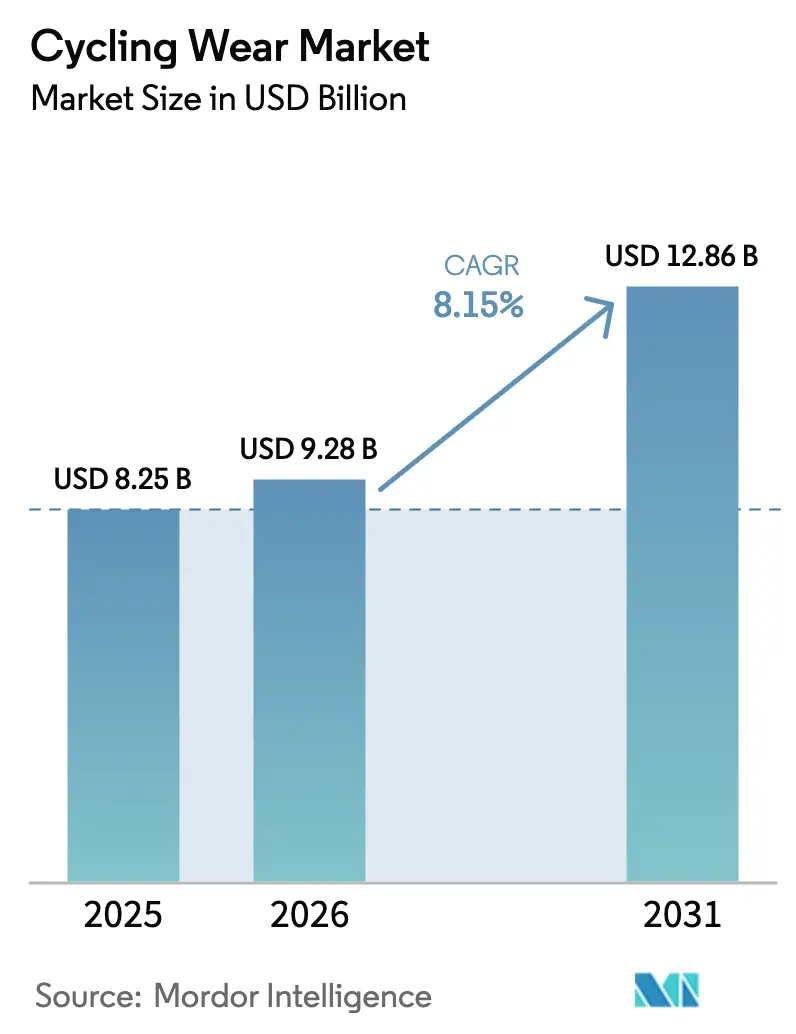

| Market Size (2026) | USD 9.28 Billion |

| Market Size (2031) | USD 12.86 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

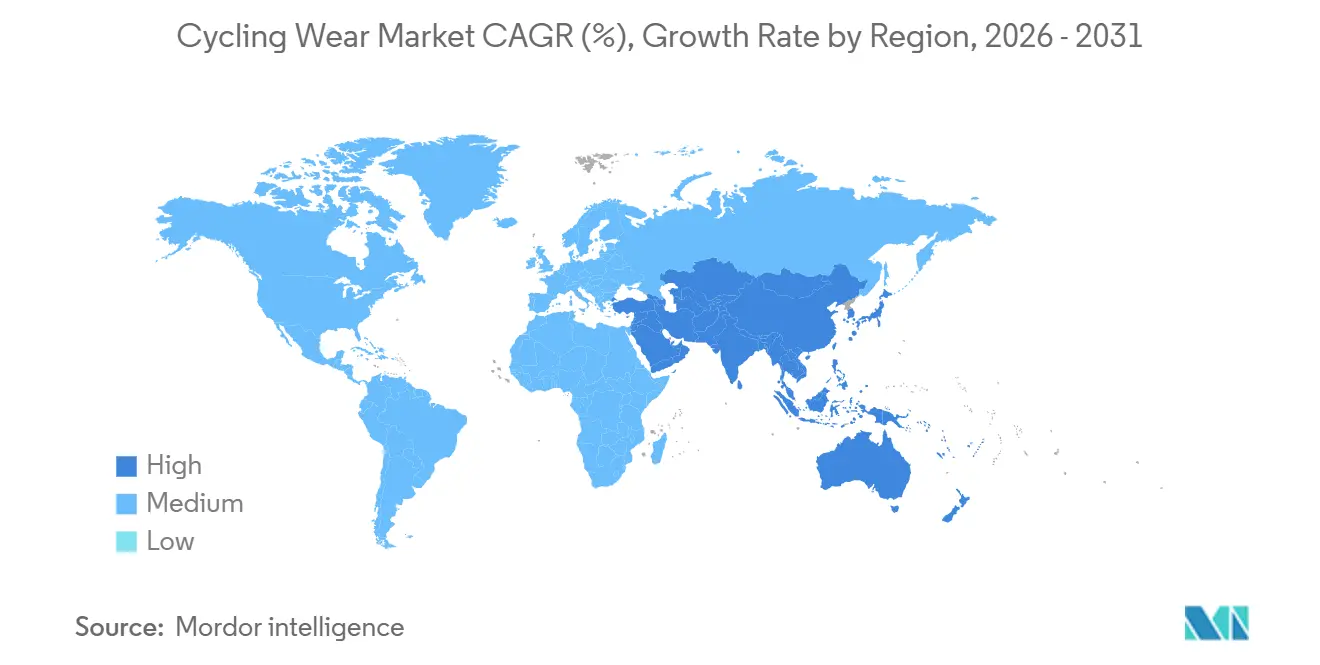

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cycling Wear Market Analysis by Mordor Intelligence

The cycling wear market size is projected to be USD 8.25 billion in 2025, USD 9.28 billion in 2026, and reach USD 12.86 billion by 2031, growing at a CAGR of 8.15% from 2026 to 2031. Functional demand is widening as governments fund commuter-friendly infrastructure, shifting purchases toward weather-resistant apparel that blends performance and everyday utility. Premiumization is accelerating because smart fabrics and lifestyle positioning justify higher prices even while mass-market volumes dominate. Accessories outpace core garments as riders build modular wardrobes around packable, visibility-focused items. Digital channels grow fastest as festival-driven promotions and direct-to-consumer (DTC) models compress decision cycles into brief, high-traffic events. Challenger brands leverage niche cultural marketing to erode incumbent share, especially in women’s and premium lines.

Key Report Takeaways

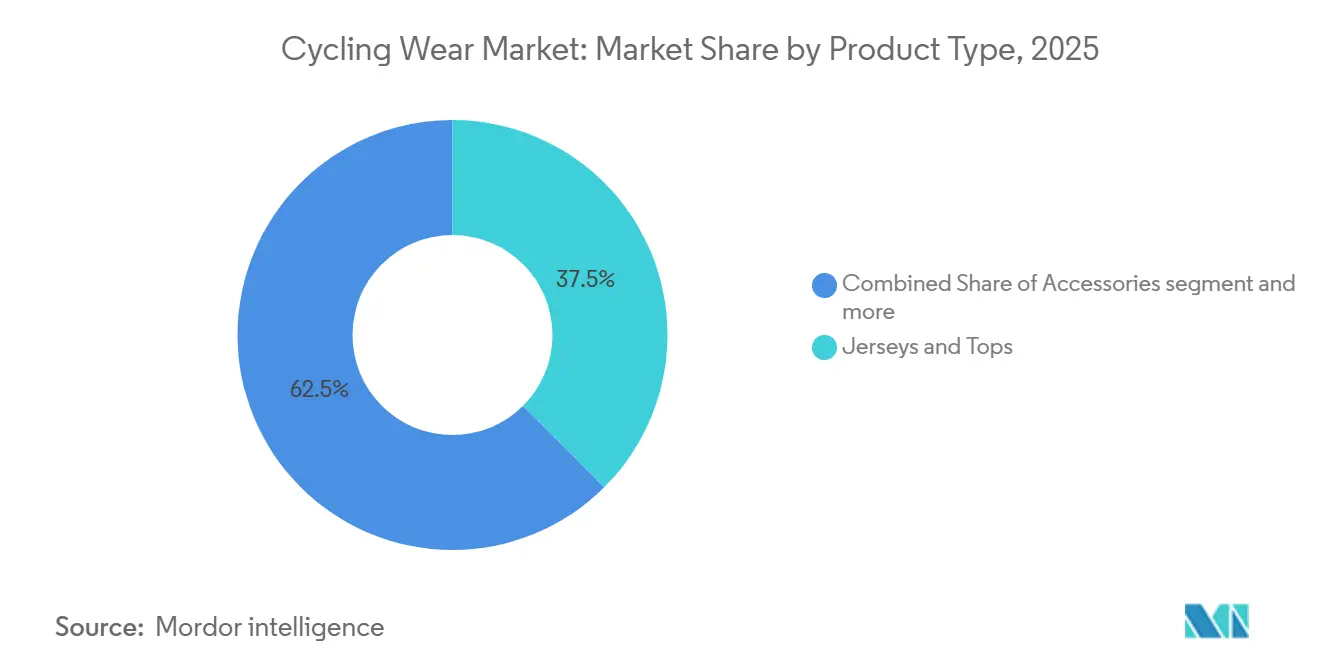

- By product type, jerseys and tops led with 41.28% of the cycling wear market share in 2025. Accessories are forecast to expand at a 9.32% CAGR through 2031.

- By end user, men accounted for 58.33% share of the cycling wear market size in 2025, while the women’s segment is projected to grow at a 9.27% CAGR to 2031.

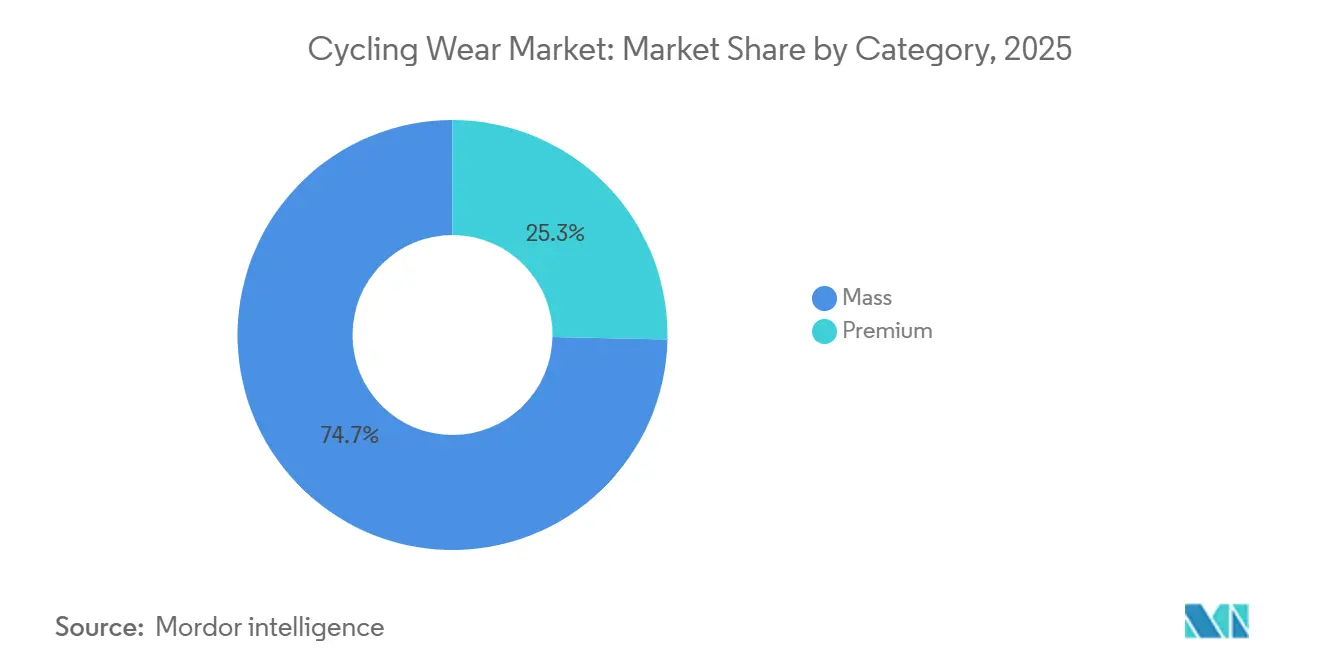

- By category, mass products held 75.42% of the market in 2025, while premium offerings will record a 10.02% CAGR to 2031.

- By distribution, sports and athletic goods stores captured 38.95% share in 2025; online retail channels are advancing at a 10.56% CAGR through 2031.

- By geography, Europe retained 40.21% share in 2025; Asia-Pacific is the fastest-growing region at a 9.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cycling Wear Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health And Fitness Awareness | +1.8% | Global, with stronger influence in North America and Western Europe | Medium term (2-4 years) |

| Growing Popularity Of Cycling For Commuting And Recreation Amid Urban Congestion | +2.1% | Europe, Asia-Pacific urban centers, North American metropolitan areas | Short term (≤ 2 years) |

| Technological Innovations In Materials For Breathability, Lightness, And Smart Features | +1.5% | Global, led by Europe and North America R&D hubs | Long term (≥ 4 years) |

| Expanded Cycling Infrastructure And Government Initiatives Supporting Bike Lanes | +1.9% | Europe, UK, select Asia-Pacific markets (China, India) | Medium term (2-4 years) |

| Increased Sports Participation In Road, Mountain, And Gravel Biking | +1.3% | North America, Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Environmental Concerns Promote Sustainable, Eco-Friendly Cycling Products | +0.9% | Europe, North America, spillover to Asia-Pacific premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Health and Fitness Awareness

As cycling increasingly becomes a badge of identity rather than just a pastime, its appeal is broadening from traditional enthusiasts to wellness oriented consumers. A 2025 McKinsey survey highlighted that 51 to 54% of active consumers, especially millennials and Gen Z, see fitness as integral to their identity. This shift in perception is benefiting cycling wear brands that market their products as essential lifestyle items rather than just functional gear. While the World Health Organization warns of a rise in adult physical inactivity from 31% in 2022 to 35% by 2030, translating to 1.8 billion globally, it is also a golden opportunity for brands. By innovating products and engaging at the grassroots level, they can tap into this vast, currently inactive demographic. Shimano's Trail Born initiative, which allocated USD 10 million over a decade to trail development and made inroads into South America and Asia in 2026, underscores the trend. It is a testament to how component manufacturers are bolstering participation infrastructure, inadvertently boosting apparel demand. To entice these previously inactive consumers, brands need to focus on comfort and versatility in their apparel, rather than just race day performance, especially given the 75.42% mass market share noted in 2025.

Growing Popularity of Cycling for Commuting and Recreation Amid Urban Congestion

Urban mobility policies are shifting cycling from a leisure pursuit to a staple mode of transport, fueling a consistent demand for durable, weather-resistant apparel. In 2024, the European Commission's Declaration on Cycling, endorsed by Member States, emphasizes the establishment of safe cycling networks, the integration of bikes with public transport, and the development of e-bike charging infrastructure. This initiative is bolstered by a substantial commitment of EUR 4.5 billion in EU funds, allocated for the 2021 2027 period. A preliminary study by the EU has pinpointed over 900,000 kilometers of existing cycle paths throughout Europe. However, significant regional disparities highlight an uneven maturity in demand[1]Source: European Commission, “EU Progress on Cycling,” europa.eu. The United Kingdom's Third Cycling and Walking Investment Strategy (CWIS3) aims to boost the number of cycling stages per individual while simultaneously working to reduce cyclist casualties. Active Travel England is set to bolster its technical support starting in 2026. As commuter cycling gains traction, there is a rising preference for versatile apparel that seamlessly transitions from bike rides to office settings. In a notable surge, China's outdoor clothing sales on Douyin skyrocketed by 75.5% year on year from January to October 2024, hitting a remarkable USD 2.4 billion. This uptick underscores the growing allure of functional outdoor wear, particularly cycling commuter apparel, among the digitally savvy consumer base.

Technological Innovations in Materials for Breathability, Lightness, and Smart Features

Advancements in material science are driving the development of apparel capable of harvesting energy, monitoring physiological metrics, and adapting to environmental changes. This progress positions cycling wear at the forefront of the integration between textiles and wearable electronics. In March 2026, researchers from Nantong University and SUNY Stony Brook published findings on core-spun yarns. These yarns, featuring moisture-enabled electric generators, generate 0.75 volts and 0.034 milliamps at 95% relative humidity. This technology enables self-powered breathing pattern recognition and wireless abnormality alerts, as highlighted by Zhang et al. Although the current output is limited, the yarn's architecture allows direct integration into cycling jerseys, enabling continuous physiological monitoring without external batteries. Additionally, TNO, a European organization, filed a patent in 2024 for a modular smart sensing textile[2]Source: TNO, “Smart Sensing Textile Patent EP 4 364 663 A1,” epo.org. This textile incorporates stretchable conductive electrodes made from silver-plated yarns and removable flexible electronics patches. It delivers ECG signal quality comparable to medical-grade gel electrodes while maintaining garment washability.

Expanded Cycling Infrastructure and Government Initiatives Supporting Bike Lanes

Investments in public cycling infrastructure are lowering perceived barriers to adoption, driving increased demand for cycling apparel. The EU's 2025 progress report revealed that Lithuania introduced its first national cycling strategy in 2024. Furthermore, 26 Member States established national cycling contact points, reflecting a coordinated policy effort (European Commission, 2025). In the UK, the CWIS3 consultation proposed statutory objectives to make active travel safer and more accessible. Key performance indicators included an increase in the percentage of individuals achieving 150 minutes of weekly active travel and a reduction in serious injuries or fatalities among pedestrians and cyclists (Department for Transport, GOV.UK, 2025)[3]Source: Department for Transport, “Third Cycling and Walking Investment Strategy,” gov.uk. These indicators tie funding to measurable behavioral changes, encouraging local authorities to prioritize cycling infrastructure that supports daily riders. The density of cycling infrastructure directly influences apparel purchases, as cyclists using protected bike lanes are more likely to ride year-round, requiring seasonal wardrobes instead of single-use kits. The EU's Recovery and Resilience Facility allocated approximately €1.3 billion for cycling projects. Combined with €3.2 billion from EU structural funds, this creates a sustained demand tailwind for the coming years.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Costs Of Advanced Materials Like Carbon Fiber Limit Affordability | -1.2% | Global, most acute in price-sensitive Asia-Pacific and Latin America markets | Short term (≤ 2 years) |

| Supply Chain Disruptions And Inventory Issues Hinder Reliability | -0.9% | Global, with concentrated risk in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Presence of Counterfiet Products | -0.6% | Asia-Pacific, Middle East, emerging e-commerce platforms globally | Medium term (2-4 years) |

| Stricter Micro-Fiber Shedding Regulations | -0.7% | Europe, North America, with future expansion to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Costs of Advanced Materials Like Carbon Fiber Limit Affordability

Premium material costs create a ceiling on mass-market penetration, particularly in price-sensitive geographies where cycling is transitioning from recreation to transport. While carbon fiber is primarily associated with bicycle frames, advanced technical fabrics incorporating graphene, silver-plated yarns, and specialty polymers face similar cost pressures. The reduced graphene oxide yarns described in peer-reviewed sweat lactate monitoring research cost approximately USD 0.03 per meter at lab scale, but commercial-scale production with consistent quality remains unproven. KPMG's China consumer report noted that mid- and high-end outdoor brands saw faster online growth, with one high-end brand achieving CNY 1.228 billion (approximately USD 170 million) turnover in January-October 2024, up 220% year-on-year, suggesting that affluent consumers will pay premiums for performance.

Supply Chain Disruptions and Inventory Issues Hinder Reliability

Geopolitical tensions and concentrated manufacturing footprints expose cycling wear brands to inventory volatility that erodes customer trust and channel relationships. McKinsey's 2025 sporting goods survey found that 84% of executives expressed concern about geopolitical and tariff risks, the highest-ranked macro threat. The EU's 2025 cycling report noted that European bicycle production fell 24% from 12.7 million units in 2022 to 9.7 million in 2023, driven by rising production costs and price competition from non-EU producers benefiting from state subsidies. While this data pertains to bicycles, cycling apparel shares similar supply chain dependencies on Asian textile manufacturing and synthetic fiber production. Brands relying on single-source suppliers for technical fabrics face extended lead times when disruptions occur, forcing retailers to hold excess safety stock or accept stockouts during peak seasons. McKinsey recommended that sporting goods companies diversify supply chains, digitize inventory management, and increase automation to mitigate these risks, strategies equally applicable to cycling wear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accessories Outpace Core Apparel

Accessories are forecast to expand at 9.32% CAGR during 2026-2031, outstripping the growth of jerseys and tops despite the latter's 41.28% share in 2025. This divergence reflects the modular purchasing behavior of commuter cyclists, who invest incrementally in visibility gear, packable rain shells, and thermal layers rather than replacing entire wardrobes. Jerseys and tops remain the largest segment because they are the entry point for new cyclists and require frequent replacement due to wear and perspiration exposure. Bottoms and bib-shorts represent a smaller share but command higher per-unit prices due to chamois padding and compression fabrics, making them a margin-accretive category for brands. Jackets and outerwear serve seasonal and weather-specific needs, with demand concentrated in temperate climates where year-round cycling requires layering systems.

The accessories surge is tied to urban cycling's rise, where riders prioritize packability and multi-functionality over race-day aerodynamics. Shimano's February 2026 launch of RIDESCAPE lens options for road, gravel, and trail riders, featuring darkened lenses to reveal surface texture like potholes and seams, illustrates how accessories are evolving into performance-enhancing tools rather than afterthoughts. Although eyewear falls outside apparel, the design philosophy applies to accessories like gloves with touchscreen-compatible fingertips and caps with integrated LED strips. China's Double 11 festival in 2024 saw cycling goggles sales surge 210% year-on-year on Tmall, confirming that accessories benefit disproportionately from promotional events.

By End User: Women's Segment Closes Gender Gap

Women's cycling wear is projected to grow at 9.27% CAGR through 2031, narrowing the gap with men's 58.33% share recorded in 2025. This acceleration stems from rising female participation in cycling, driven by inclusive infrastructure policies and targeted marketing by brands recognizing women as an underserved demographic. The EU's Declaration on Cycling emphasizes inclusivity and accessibility, with Member States launching tailored programs for women, older adults, and families European Commission, 2025. KPMG's China report noted that women comprised 55.41% of fitness consumers in 2023, indicating that female engagement in active lifestyles is translating into cycling participation. Brands that offer gender-specific fits, extended size ranges, and design aesthetics beyond traditional racing palettes are capturing this growth.

Men's segment retains majority share due to historical participation rates and higher average spending on performance gear, but growth is moderating as the market matures. Children's cycling wear remains a smaller segment, yet it serves as a funnel for long-term brand loyalty if parents introduce cycling early. The UK's CWIS3 targets an increased percentage of children aged 5-10 who usually walk to school, with cycling training programs like Bikeability expanding reach. Children's apparel must balance durability with rapid sizing changes, favoring adjustable designs and value pricing.

By Category: Premium Gains as Performance Expectations Rise

The premium segment is projected to grow at a 10.02% CAGR from 2026 to 2031, nearly twice the growth rate of the mass market. This growth is driven by consumers increasingly distinguishing between basic apparel and performance-enhancing options. In 2025, premium products accounted for a 24.58% market share (derived from the mass market's 75.42%), yet they generated disproportionate revenue due to higher per-unit prices and better margin profiles. McKinsey's analysis of the sporting goods sector highlighted that challenger brands, many operating in premium niches, have gained market share from established players by focusing on visible innovation and cultural marketing. Cycling wear brands such as Rapha and Assos exemplify this approach, positioning their products as luxury performance items rather than standard sportswear. USA Cycling's January 2026 partnership with Rapha, which designates them as the official supplier for the national team kit through 2029 and includes replica merchandise sales, illustrates how premium brands leverage elite associations to justify premium pricing.

Mass-market products maintain a 75.42% share, as commuter and recreational cyclists prioritize functionality and affordability over incremental performance improvements. Decathlon's presence in the TOC underscores the importance of this segment, as the retailer caters to budget-conscious consumers with its private-label offerings. The premium segment's growth is supported by advancements such as smart textiles, bio-based fabrics, and direct-to-consumer models that minimize retail markups. Canyon's December 2025 launch of the CANYON//SRAM zondacrypto 'Luminous' kit, scheduled for Spring 2026 and sold exclusively through Canyon.com and the Canyon App, demonstrates how bicycle manufacturers are expanding into apparel with coordinated bike-and-kit merchandising. This vertical integration enables premium brands to capture full-stack margins while maintaining control over the customer experience.

By Distribution Channels: Online Disrupts Traditional Retail

Online retail channels are set to grow at 10.56% CAGR through 2031, the fastest rate among distribution types, as direct-to-consumer models and festival-driven promotions reshape purchasing behavior. Sports and athletic goods stores held 38.95% share in 2025, anchored by specialty retailers offering fitting services and expert advice, yet this channel faces margin pressure from e-commerce's convenience and broader selection. KPMG's China report documented that cycling outfits and equipment each surged over 100% year-on-year during Double 11 2024 on Tmall, with road bicycles up 300% and cycling goggles up 210%, demonstrating that promotional events concentrate demand into short windows. Brands must develop festival-specific inventory strategies and leverage livestreaming and short-form content marketing on platforms like Douyin to capture these spikes.

Supermarkets and hypermarkets serve entry-level consumers seeking basic cycling wear alongside other sporting goods, but this channel's share is eroding as online platforms offer superior product variety and customer reviews. The 'Others' category includes direct brand stores, cycling clubs, and event-based sales, which provide experiential touchpoints that online channels cannot replicate. Rapha's global clubhouse network exemplifies this hybrid approach, combining retail with community spaces that host group rides and events. McKinsey noted that 81% of surveyed consumers attended in-person fitness classes in the past year, and the global live events ticketing market is projected to exceed USD 150 billion by 2030, indicating that experiential retail remains relevant.

Geography Analysis

Europe commanded 40.21% market share in 2025, underpinned by entrenched cycling cultures in the Netherlands, Belgium, Germany, and the UK, where cycling is embedded in daily transport and recreational routines. The European Commission's Declaration on Cycling and the €4.5 billion investment for 2021-2027 are expanding infrastructure beyond core markets into Southern and Eastern Europe, where cycling adoption lags. Lithuania's adoption of its first national cycling strategy in 2024 signals that emerging European markets are entering growth phases, creating opportunities for brands to establish a presence before competition intensifies. The UK's £616 million CWIS3 allocation for 2026-2030 targets measurable increases in cycling stages per person, directly stimulating apparel demand as new cyclists require starter kits and existing riders upgrade seasonal wardrobes. Germany, the Netherlands, and Sweden benefit from high per-capita cycling rates and premium brand concentration, sustaining Europe's leadership despite slower growth relative to Asia-Pacific.

Asia-Pacific is forecast to expand at 9.98% CAGR during 2026-2031, the fastest regional rate, driven by urbanization, infrastructure investment, and rising middle-class incomes in China, India, and Southeast Asia. China's government issued consumption vouchers and sports-promotion policies in 2024, including financial support for sports consumption via China UnionPay and e-CNY use, creating fiscal tailwinds for cycling participation. India's cycling infrastructure remains underdeveloped compared to China, but urban congestion and environmental awareness are driving two-wheeler adoption, with cycling wear benefiting as a secondary effect. Vietnam and Indonesia represent emerging markets where rising incomes and youth populations favor active lifestyles, yet distribution infrastructure and brand awareness remain barriers.

North America, South America, and the Middle East and Africa collectively represent smaller shares but exhibit heterogeneous growth patterns. North America benefits from established recreational cycling and gravel biking trends, with Shimano's February 2026 partnership with the Canyon x DT Swiss All-Terrain Racing team highlighting the gravel segment's momentum Shimano, 2026. The United States and Canada have fragmented cycling infrastructure, with urban centers like Portland and Vancouver leading adoption while suburban and rural areas lag. South America's cycling wear market is nascent, constrained by economic volatility and limited infrastructure, though Shimano's Trail Born expansion into Brazil and Mexico in 2026 signals growing interest. The Middle East and Africa face infrastructure and climate challenges, with cycling concentrated in cooler months and affluent urban enclaves. The UAE and South Africa lead regional adoption, but market scale remains limited compared to Europe and Asia-Pacific.

Competitive Landscape

Competition remains moderately fragmented. Heritage brands such as Rapha, Assos, and Castelli, which have benefited from decades of feedback from the pro-peloton, continue to drive innovation in high-end fabrics and aerodynamic designs. These brands capitalize on their established reputations and technical expertise to maintain a competitive advantage in the premium segment. At the same time, challenger labels are establishing their presence by leveraging direct-to-consumer logistics, influencer-driven marketing, and specialized offerings, such as cargo bibs for gravel enthusiasts and jerseys designed for Islamic modesty, to capture a larger share of consumer spending. These emerging players focus on meeting specific consumer needs and preferences, enabling them to stand out in a competitive market.

Technology is emerging as a critical differentiator. By collaborating with electronics companies, leading brands are incorporating heart-rate sensors and heating elements into sleek, minimalist designs, enhancing both functionality and consumer appeal. Simultaneously, the proliferation of counterfeits on major online platforms is prompting genuine brands to implement measures like digital watermarks and serialization to safeguard their intellectual property and maintain consumer trust. Furthermore, as brands address microfiber-related mandates, sustainability-focused newcomers skilled in bio-based polymers and closed-loop yarn recovery are finding opportunities to grow. These innovations not only comply with regulatory requirements but also align with the rising consumer demand for environmentally sustainable products.

Brands that diversify their supply chains, such as near-shoring specific SKUs to mitigate fluctuations in polyester prices, are better positioned to remain resilient, while others may struggle. Supply-chain flexibility allows these brands to manage costs more effectively and reduce risks associated with global disruptions. Over the next few years, the cycling wear market may experience a wave of opportunistic mergers and acquisitions, potentially consolidating mid-tier labels that lack proprietary intellectual property. This consolidation could result in a more concentrated market landscape, fostering increased efficiency and the emergence of stronger players with enhanced capabilities to innovate and compete on a global scale.

Cycling Wear Industry Leaders

Rapha Racing Ltd

Assos of Switzerland

Castelli (Manifattura Valcismon)

Pearl Izumi

Specialized Bicycle Components (Apparel)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nimbl introduced a new line of high-performance cycling apparel. Currently undergoing rider testing, these items are set to hit the market soon, exclusively through direct-to-consumer channels.

- May 2025: Santini Cycling teamed up with Pirelli Design to debut a new technical cycling apparel line named Sport Club. The collection features two unisex jerseys: the Ruota, boasting a wheel-shaped silicone detail on its back, crafted from ultra-light, elastic fabric for a sleek, second-skin fit; and the Tape, adorned with stripes reminiscent of 1960s Pirelli posters, made from Polartec® Power Stretch™, complete with lightweight raw-cut sleeves, reflective accents, and a comfort-driven covered zip.

- April 2025: CUORE introduced the Gold Pro Speed Suit, its latest cycling apparel. With meticulous design adjustments, CUORE has optimized the Gold Pro Speed Suit for superior aerodynamics, enabling cyclists to slice through the wind with enhanced efficiency.

- March 2025: MAAP unveiled its latest creation, the Aeon Jersey, utilizing the cutting-edge Polartec Delta fabric. This advanced cooling material boasts a 3D knit structure that efficiently wicks moisture away from the skin, enhancing airflow and minimizing cling for an unparalleled breathable experience.

Global Cycling Wear Market Report Scope

| Jerseys and Tops |

| Bottoms and Bib-shorts |

| Jackets and Outerwear |

| Accessories |

| Men |

| Women |

| Children |

| Mass |

| Premium |

| Sports and Athletic Goods Store |

| Online Retail Channels |

| Supermarkets/Hypermarkets |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Jerseys and Tops | |

| Bottoms and Bib-shorts | ||

| Jackets and Outerwear | ||

| Accessories | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channels | Sports and Athletic Goods Store | |

| Online Retail Channels | ||

| Supermarkets/Hypermarkets | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the cycling wear market be by 2031?

It is forecast to reach USD 12.86 billion by 2031, expanding at an 8.15% CAGR from 2026 to 2031.

Which product category is growing fastest?

Accessories, including gloves, caps, and packable shells, are projected to rise at a 9.32% CAGR through 2031.

Why is Asia-Pacific considered the most dynamic region?

Rising urbanization, government cycling incentives, and digital-festival promotions drive a 9.98% regional CAGR.

What factors support premium cycling apparel growth?

Smart fabrics, direct-to-consumer strategies, and elite team partnerships fuel a 10.02% CAGR for premium products.

Page last updated on: