Parmesan Cheese Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

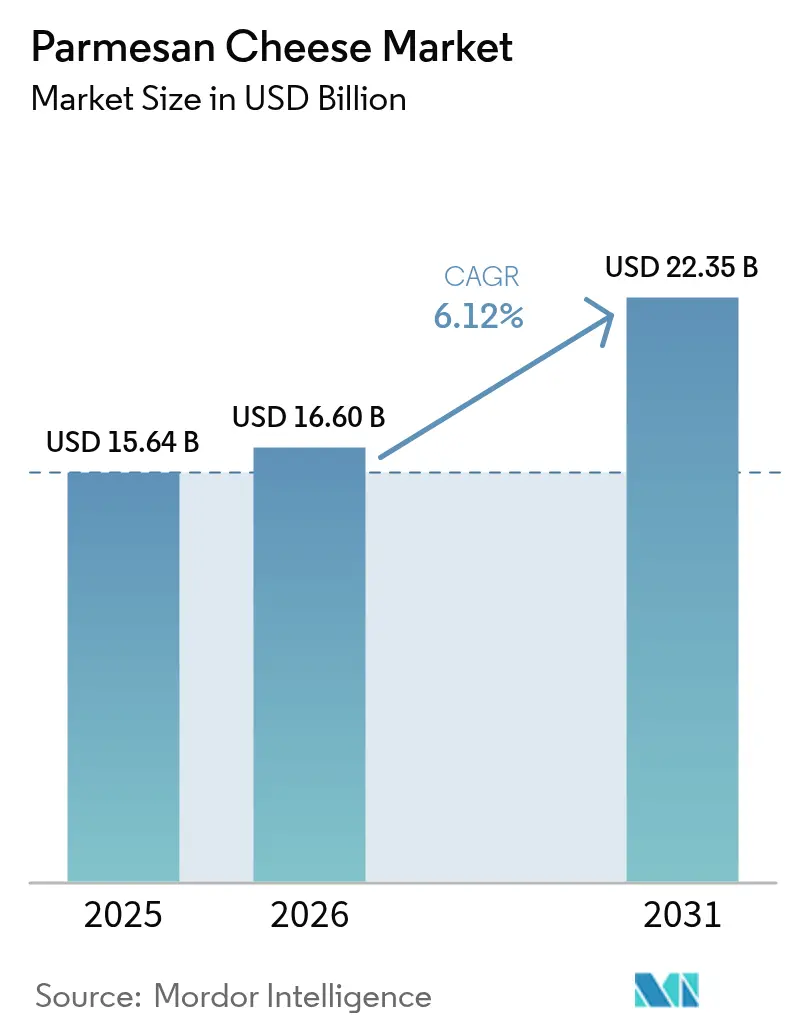

| Market Size (2026) | USD 16.6 Billion |

| Market Size (2031) | USD 22.35 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

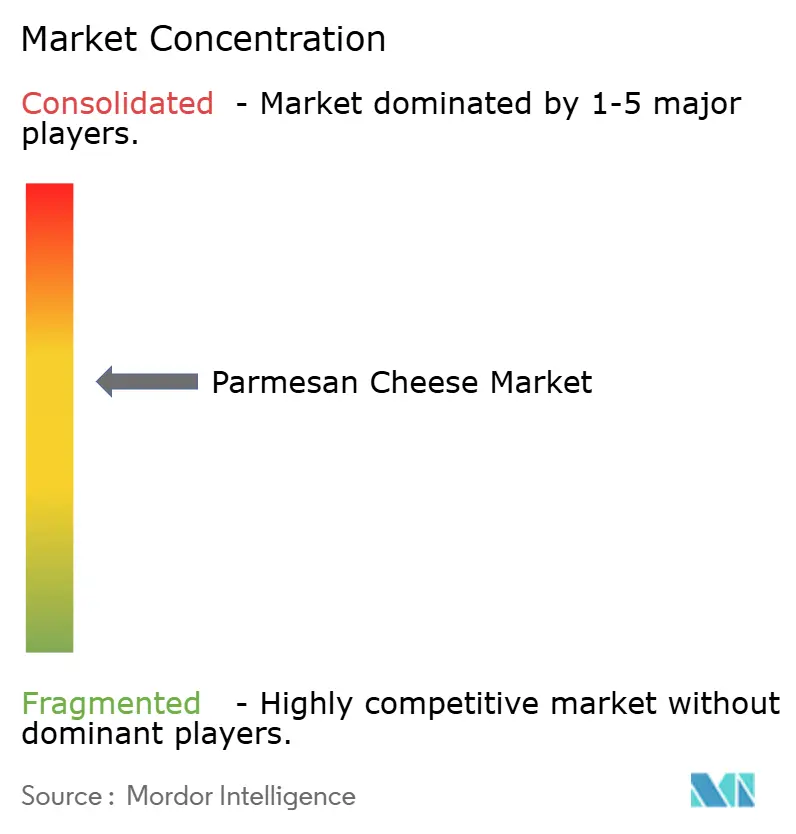

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Parmesan Cheese Market Analysis by Mordor Intelligence

The Parmesan cheese market size was valued at USD 15.64 billion in 2025 and estimated to grow from USD 16.6 billion in 2026 to reach USD 22.35 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). This growth is bolstered by tightening PDO regulations, a surge in plant-based innovations, and an uptick in demand from quick-service restaurants (QSRs) in emerging markets. Multinational processors are expanding production, driven by a consistent consumer appetite for protein-rich foods and international QSR chains localizing their menus. In the Asia-Pacific, rising disposable incomes and urban lifestyle shifts are turning occasional Parmesan buyers into regulars. Investments in technology, like AI-driven yield optimization, are boosting cost efficiencies. Meanwhile, the EU's stringent measures against counterfeit labeling safeguard the price premiums of authentic PDO cheese. Overall, a sustained demand for genuine flavors, convenient formats, and clean-label products positions the Parmesan cheese market for steady double-digit value growth in major urban centers throughout the forecast period.

Key Report Takeaways

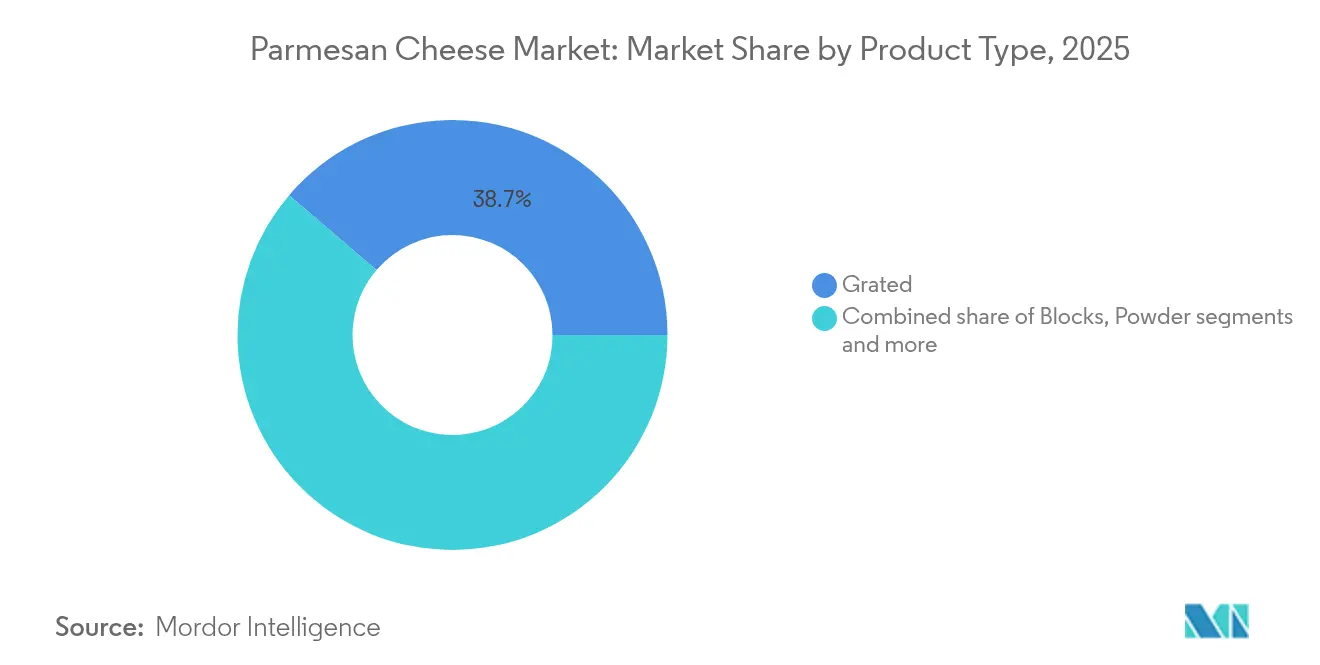

- By product type, grated formats led with 38.74% of the Parmesan cheese market share in 2025, while shredded variants are projected to expand at a 4.86% CAGR to 2031.

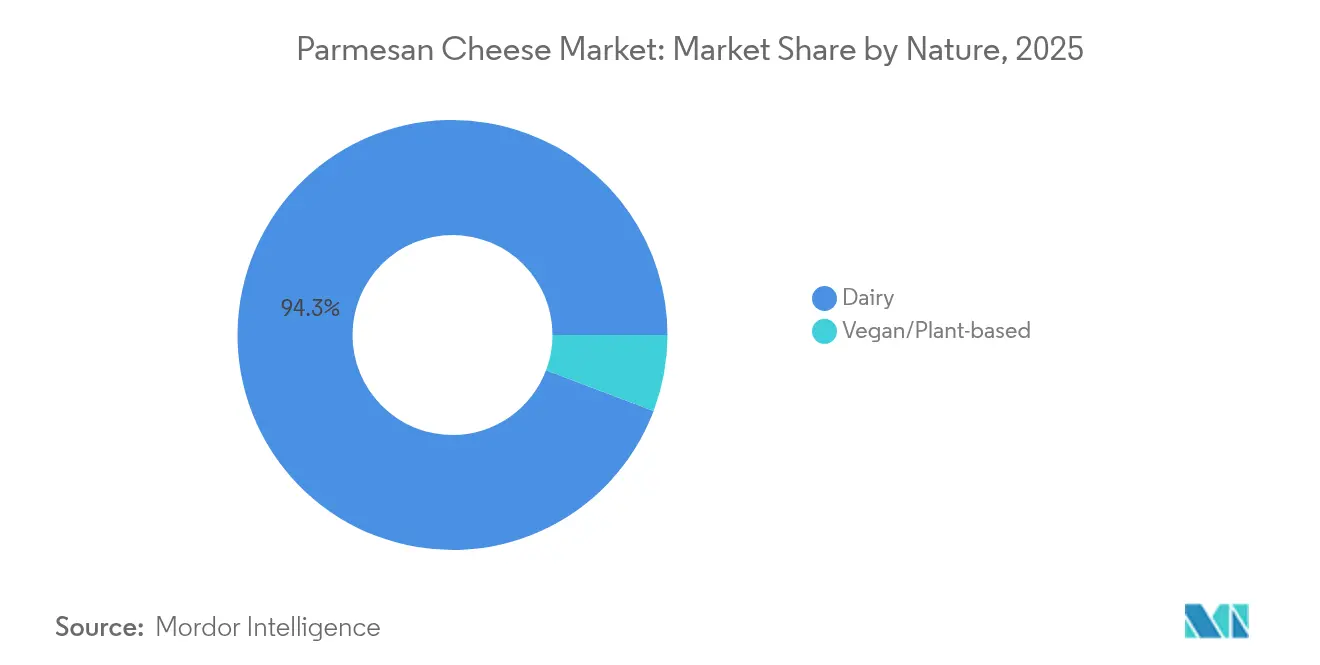

- By nature, dairy products retained 94.25% share of the Parmesan cheese market size in 2025, while vegan and plant-based alternatives are advancing at a 5.12% CAGR through 2031.

- By distribution channel, off-trade outlets captured 56.35% revenue in 2025; on-trade channels are growing at 5.73% annually to 2031.

- By geography, Europe contributed 54.90% of 2025 revenue, whereas Asia-Pacific is pacing a 4.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Parmesan Cheese Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for protein-rich and nutrient-dense foods | +1.2% | Global, with pronounced uptake in North America and Europe | Medium term (2-4 years) |

| High global demand for authentic PDO cheeses | +1.5% | Europe core, expanding to North America and Asia-Pacific premium segments | Long term (≥ 4 years) |

| Increased incorporation of Parmesan cheese into fast food and convenience food | +1.0% | Global, led by North America and Asia-Pacific QSR expansion | Short term (≤ 2 years) |

| Increasing demand for premium, organic, and artisanal cheese varieties | +0.9% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Innovations in plant-based and vegan Parmesan alternatives | +0.8% | North America and Europe, with early adoption in Australia | Short term (≤ 2 years) |

| Growing popularity and awareness of Italian cuisine worldwide | +1.1% | Global, strongest in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for protein-rich and nutrient-dense foods

Health-conscious consumers are increasingly prioritizing nutrient density over caloric intake, driving the shift toward protein fortification in dairy portfolios. Parmesan cheese has become a preferred option for those seeking nutrient-rich choices. For instance, in March 2024, the Consumer Affairs Agency revealed that 12.2% of Japanese consumers selected health foods labeled as "foods with nutrient function claims" (FNFC)[1]Source: Consumer Affairs Agency, "Consumer Survey on Food Labeling", caa.go.jp. The USDA's Dietary Guidelines for Americans 2020-2025, reaffirmed in 2024, recommend three daily servings of dairy for adults. This makes hard cheeses like Parmesan, which provides 10 grams of protein per ounce, an ideal option to meet these dietary recommendations. This aligns with the World Health Organization's 2024 emphasis on nutrient-dense foods to address micronutrient deficiencies in aging populations. Parmesan's 18-month aging process enhances its protein and calcium content while reducing lactose, making it appealing to consumers with digestive sensitivities. In North America, where meal customization drives revenue growth, foodservice operators are leveraging this trend by incorporating Parmesan into protein bowls and as a salad topper.

High global demand for authentic PDO cheeses

Parmigiano-Reggiano's Protected Designation of Origin status, regulated by the Consorzio del Formaggio Parmigiano-Reggiano and supported by EU Regulation 2024/1143, restricts production to five Italian provinces. This requirement for traditional methods creates a scarcity that maintains its price premiums. Germany is a key market for Italian PDO cheese exports in terms of both volume and value. In 2024, exports exceeded EUR 820 million, reflecting a 10% increase compared to the previous year. This growth continued into the first half of 2025, with exports reaching EUR 445 million, a 12% rise from the same period in 2024[2]Source: European Food Agency, "Italian PDO cheeses: double-digit sales growth in Germany", efanews.eu. The Consorzio's traceability system, which provides unique identification codes for each cheese wheel, supports premium positioning in specialty retail and fine dining. This provenance authentication justifies a 30-50% price premium over non-PDO alternatives. Consequently, the market is diverging: PDO producers are achieving margin growth, while non-PDO manufacturers focus on competing through volume and convenience formats.

Increased incorporation of parmesan cheese into fast food and convenience food

Quick-service restaurant chains are increasingly embedding Parmesan cheese into their core menu items to differentiate themselves and increase average customer spending. This rising trend of Parmesan cheese usage in quick-service restaurants (QSRs) is significantly driving market growth. In 2024, the International Franchise Association reported that the U.S. had 199,931 QSR franchise establishments, reflecting the growing demand for Parmesan cheese[3]Source: International Franchise Association, " 2025 Franchising Economic Outlook, franchise.org. Domino's Pizza has launched items like Parmesan Bread Bites and Parmesan Bread Twists, leveraging the cheese's umami flavor to enhance their snack offerings. Similarly, Pizza Hut has introduced Parmesan-crusted pizza variants, targeting millennials and Gen Z consumers who prioritize bold flavors. These innovations are particularly impactful in the Asia-Pacific region, where Western QSRs are rapidly expanding. China's growing middle class and Japan's convenience-store culture are driving demand for pre-portioned, shelf-stable Parmesan products. Additionally, the shift toward Parmesan is evident in North American casual dining, where chains are adding Parmesan-crusted proteins and pasta bowls to capitalize on higher-margin entree sales.

Increasing demand for premium, organic, and artisanal cheese varieties

As consumers increasingly align their purchasing decisions with values such as sustainability and animal welfare, the sales of organic and artisanal Parmesan cheeses are surpassing those of conventional options. In 2024, the USDA's National Organic Program reported sustained growth in organic dairy production, with organic cheese benefiting significantly from its ability to command premium pricing and achieve broader distribution through natural-channel retailers. Artisanal producers, including BelGioioso Cheese and Organic Valley, are distinguishing themselves in the market by focusing on small-batch aging processes, utilizing heirloom milk sources, and maintaining transparent supply chains. These companies have expanded their aged Parmesan product lines (SKUs) to address the increasing demand from specialty grocers and farm-to-table restaurants. This trend is particularly prominent in North America and Europe, where consumers are willing to pay a premium for products that offer traceability and authentic craft narratives. Additionally, the trend is beginning to emerge in urban markets across the Asia-Pacific region, driven by rising disposable incomes and a growing interest in premium, sustainably produced food products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Milk-price volatility squeezing small dairies | -0.7% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Counterfeit "Parmesan" eroding PDO price premium | -0.5% | Global, most severe in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing vegan-cheese substitution in Western markets | -0.4% | North America and Europe, emerging in Australia | Medium term (2-4 years) |

| Strict geographic and quality regulations | -0.3% | Europe core, spillover to export markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Milk-price volatility squeezing small dairies

In 2024, raw milk prices experienced notable volatility, primarily driven by escalating feed costs, persistent labor shortages, and the USDA's amendments to the Federal Milk Marketing Orders in December 2024. These amendments revised Class III pricing formulas, which significantly compressed profit margins for small and mid-sized dairies. The FAO Dairy Price Index remained elevated through 2025, underscoring a constrained global milk supply coupled with strong demand from cheese and powder processors. Small dairies, which lack the benefits of scale economies and forward-hedging mechanisms, are under increasing margin pressure. This financial strain hampers their ability to invest in modernizing aging infrastructure and implementing quality improvements necessary for producing premium Parmesan cheese. As a result, the market is becoming increasingly polarized. Larger players are leveraging vertical integration to achieve cost efficiencies, while smaller artisanal producers face challenges in maintaining consistent production levels. This disparity could potentially restrict the availability of differentiated, small-batch Parmesan, further emphasizing the divide within the market.

Counterfeit "Parmesan" eroding PDO price premium

Italian-sounding products, such as cheeses labeled "Parmesan" without PDO certification, generate substantial sales, surpassing authentic Italian products. This trend weakens brand equity and creates consumer confusion. In June 2024, the European Union implemented Regulation 2024/1143, enhancing enforcement mechanisms and expanding geographical indication protections. However, implementation gaps remain in non-EU markets, particularly in North America and the Asia-Pacific region. The Consorzio del Formaggio Parmigiano-Reggiano has increased legal actions and consumer education efforts. Despite these measures, counterfeit products persist due to their lower prices and well-established distribution networks. This scenario reduces the premium authentic Parmigiano-Reggiano can achieve, compressing margins for PDO producers and discouraging investments in traditional aging and quality practices. The issue is most significant in North America, where "Parmesan" is commonly used as a generic term, and in the Asia-Pacific region, where geographical indication regulations are still developing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Convenience Formats Drive Grated Dominance

Grated Parmesan captured 38.74% of product-type volume in 2025, highlighting a growing preference for ready-to-use formats in both retail and foodservice. Pre-grated cheese removes preparation steps, catering to busy consumers and enabling quick-service restaurants to streamline portion control and reduce labor costs. Shredded Parmesan is projected to grow at an annual rate of 4.86% through 2031, driven by its popularity in fast-casual chains and meal-kit services that value its melt consistency and visual appeal. In contrast, Blocks, favored by culinary enthusiasts and fine-dining establishments for their fresh-grated flavor, hold a stable but slower-growing market share due to their requirement for specialized equipment and higher per-unit costs.

Powder formats, popular among snack manufacturers and industrial food processors for seasoning blends and dry mixes, represent a niche segment. Companies such as Kerry Group and All American Foods lead this category, utilizing spray-drying technology to improve shelf life and reduce shipping weight. In September 2024, Armored Fresh secured a patent for grated plant-based cheese technology, signaling potential disruption in the traditional dairy market. The company introduced Grated Parmesan and Grated Kimchi Parmesan in November 2024, targeting flexitarian consumers seeking dairy-free options with familiar textures. Regulatory oversight for grated and shredded products falls under FDA standards of identity, which regulate moisture content and anti-caking agents. While these standards ensure consistent quality, they also limit formulation flexibility.

By Nature: Dairy Retains Share as Plant-Based Gains Momentum

In 2025, dairy-based Parmesan commanded a dominant 94.25% market share, bolstered by traditional production methods, well-established supply chains, and consumer familiarity with its aged-cheese flavor profile. This segment enjoys the benefits of PDO protections and adheres to the stringent quality standards set by the Consorzio del Formaggio Parmigiano-Reggiano, which mandates a minimum aging of 12 months and confines production to select provinces in Italy. Meanwhile, vegan and plant-based Parmesan alternatives are on a growth trajectory, expanding at an annual rate of 5.12% through 2031. This surge is fueled by active patent filings, a broader retail presence, and continuous ingredient innovation. Highlighting the industry's shift, Saputo's acquisition of Bute Island Foods for CAD 187 million signals a recognition among established players: plant-based offerings have transitioned from niche to a pivotal element of portfolio diversification.

In August 2024, SimplyV debuted its almond-based product, ParmVegan, on Ocado in the UK, aiming at flexitarian and vegan consumers who desire familiar flavors sans dairy. While these innovations predominantly emerge from North America and Europe, regions with entrenched vegan dietary patterns, they're also making inroads in Australia and urban markets across the Asia-Pacific. In response, dairy producers are rolling out organic and lactose-free products to cater to health-conscious consumers who aren't entirely plant-based. A case in point is Arla's strategic acquisition of Yeo Valley's organic business.

By Distribution Channel: Off-Trade Leads, On-Trade Accelerates

In 2025, off-trade channels, including supermarkets, hypermarkets, convenience stores, specialty outlets, and online platforms, accounted for 56.35% of Parmesan sales. This reflects a growing consumer preference for preparing meals at home and the convenience of pre-packaged formats. Supermarkets and hypermarkets dominate this segment, offering extensive SKU assortments and promotional pricing that drive sales volume. Online retail is expanding rapidly, supported by advancements in cold-chain logistics and subscription models that encourage repeat purchases. Specialty retailers, such as Murray's Cheese, are leveraging e-commerce to target affluent consumers seeking artisanal and PDO-certified products. On-trade channels, comprising restaurants, cafes, and foodservice operators, are projected to grow at an annual rate of 5.73% through 2031, driven by Parmesan's increasing use in quick-service and casual-dining menus.

For example, Domino's Pizza has introduced Parmesan Bread Bites, while Pizza Hut has launched a Parmesan-crusted pizza, demonstrating how on-trade operators are incorporating the cheese into signature dishes to increase check averages and differentiate themselves in the market. In Japan and South Korea, convenience stores are offering single-serve Parmesan packets, catering to on-the-go consumers and aligning with urbanization and snacking trends. Specialty stores, including cheese boutiques and gourmet grocers, are curating PDO-certified and artisanal selections, commanding premium prices and appealing to consumers who value provenance and craftsmanship. The distinction between off-trade volume and on-trade value is shaping distribution strategies: mass-market brands are focusing on supermarket penetration and promotional efforts, while premium producers are building partnerships with foodservice operators and specialty channels to achieve higher per-unit margins.

Geography Analysis

In 2025, Europe accounted for 54.90% of the global Parmesan revenue, driven by Italy's PDO production system and well-established consumption patterns across the region. Italian cheese exports increased, supported by rising demand in North America and the Asia-Pacific, as noted by Federalimentare in 2024. The European Union's Regulation 2024/1143, effective from June 2024, enhanced the enforcement of geographical indications. This measure protects PDO producers from counterfeit competition but also raises compliance costs for non-PDO manufacturers. Germany, France, and the UK are key consumption markets, with both PDO and non-PDO variants performing well in retail and foodservice channels. Reflecting strategic market moves, Lactalis's USD 55 million expansion of its Tulare, California facility in 2024 highlights the company's efforts to meet North American demand while maintaining its European production capacity.

Asia-Pacific is expected to grow at an annual rate of 4.92% through 2031, the fastest among all regions, driven by increasing cheese imports and the growing popularity of Western cuisine in Japan, China, and India. In China, the expanding middle class and rapid urbanization are boosting demand for Western ingredients, including Parmesan, across retail and quick-service restaurant channels. India's cheese market, though smaller in scale, is growing due to domestic production expansions and relaxed import regulations. South Korea and Thailand are also witnessing rising consumption, supported by the growth of convenience stores and culinary tourism. However, the region's growth is limited by price sensitivity and a lack of familiarity with aged-cheese flavors. To address these challenges, suppliers are introducing smaller pack sizes and blended formats to balance affordability and taste.

North America and Latin America exhibit contrasting trends. The U.S. and Canada are mature markets with established Parmesan consumption in retail and foodservice, but the organic and plant-based segments are expanding rapidly. In Mexico, the cheese market benefits from domestic production and proximity to U.S. supply chains, with Parmesan gaining traction in urban areas. In Brazil and Argentina, Italian culinary influence is driving Parmesan adoption, although growth is constrained by import tariffs and currency volatility. In the Middle East and Africa, the UAE and Saudi Arabia are emerging as key re-export hubs and consumption markets, supported by expatriate populations and tourism. However, price sensitivity and limited cold-chain infrastructure remain significant barriers to wider market penetration.

Competitive Landscape

The Parmesan cheese market is moderately consolidated, with a few multinational dairy giants, Lactalis Group, Saputo Inc, The Kraft Heinz Company, Arla Foods amba, and Fonterra Co-operative Group Limited, holding significant production capacity and distribution networks. At the same time, regional players like BelGioioso, Organic Valley, and Italian dairies associated with Consorzio maintain a premium position through PDO certification and artisanal branding. The industry's consolidation is gaining momentum, as evidenced by Lactalis's EUR 430 million acquisition of Ambrosi, which brought expertise in Parmigiano-Reggiano and Grana Padano under its umbrella. Additionally, technological advancements are reshaping competition: in 2024, AI-driven dairy processing achieved a 10% increase in throughput, a 65% reduction in quality variability, and a 35% decrease in maintenance costs, helping established players defend their market share against smaller competitors.

In the Parmesan cheese sector, companies are actively acquiring shares and developing innovative products to attract a larger consumer base. Firms are making significant investments, collaborating with others, or acquiring companies to strengthen their market positions. While these strategies have proven beneficial for many, not all players are equally aggressive; some companies are refraining from major strategic developments. Mergers and acquisitions in the market are primarily aimed at expanding into new segments, enhancing product portfolios, and maximizing revenue.

Startups like Armored Fresh and NewMoo are identifying opportunities in the plant-based and precision-fermentation segments, securing patents and venture funding to bypass traditional dairy infrastructure. Armored Fresh's September 2024 patent for grated plant-based cheese technology, followed by its November 2024 launch of Grated Parmesan and Grated Kimchi Parmesan, highlights that convenience formats are no longer exclusive to traditional dairy players. Strategic trends reveal a divide: large processors focus on scale, automation, and portfolio diversification, while premium and plant-based specialists emphasize provenance, sustainability, and niche retail partnerships to achieve higher margins.

Parmesan Cheese Industry Leaders

-

Saputo Inc.

-

The Kraft Heinz Company

-

Arla Foods amba

-

Fonterra Co-operative Group Limited

-

Lactalis Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Panacheeza, a producer of cashew-based Parmesan, has expanded its distribution to 56 Whole Foods Market stores across the United States. This development highlights the increasing mainstream retail acceptance of plant-based cheese alternatives.

- November 2024: Armored Fresh launched two new products: Grated Parmesan and Grated Kimchi Parmesan. These plant-based offerings are designed for flexitarian consumers seeking convenient, dairy-free options.

- August 2024: SimplyV introduced ParmVegan, an almond-based Parmesan alternative, on Ocado in the United Kingdom. Designed for vegan and flexitarian consumers, the product delivers familiar cheese flavors without dairy. By adopting an online-first distribution approach, SimplyV leverages Ocado's cold-chain logistics and subscription model.

Global Parmesan Cheese Market Report Scope

| Blocks |

| Grated |

| Powder |

| Shredded |

| Dairy |

| Vegan/Plant-based |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Blocks | |

| Grated | ||

| Powder | ||

| Shredded | ||

| By Nature | Dairy | |

| Vegan/Plant-based | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Parmesan cheese market?

The global Parmesan cheese market is valued at USD 16.6 billion in 2026.

How fast is the sector expected to grow?

The market is forecast to expand at a 6.12% CAGR between 2026 and 2031.

Which region offers the strongest growth outlook?

Asia-Pacific is projected to advance at a 4.92% CAGR through 2031 as Western food adoption rises.

What product type commands the largest share?

Grated Parmesan holds 38.74% of 2025 volume because consumers favor ready-to-use formats.

Page last updated on: