Market Overview

| Study Period | 2021 - 2031 |

|---|---|

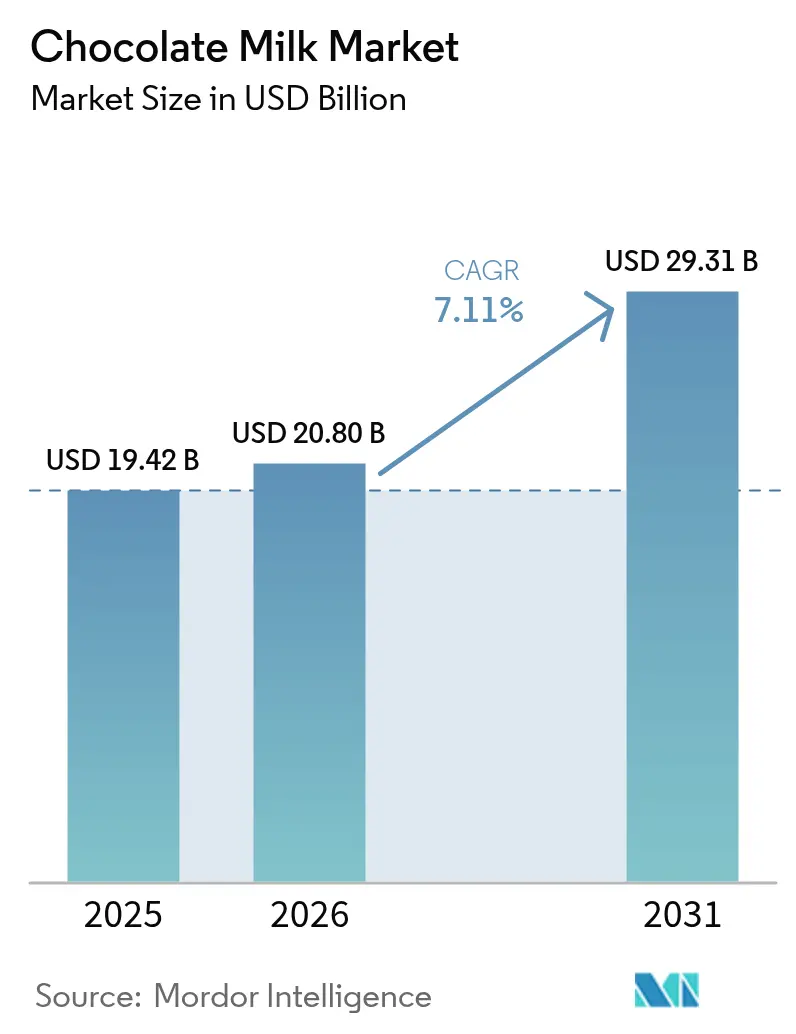

| Market Size (2026) | USD 20.8 Billion |

| Market Size (2031) | USD 29.31 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

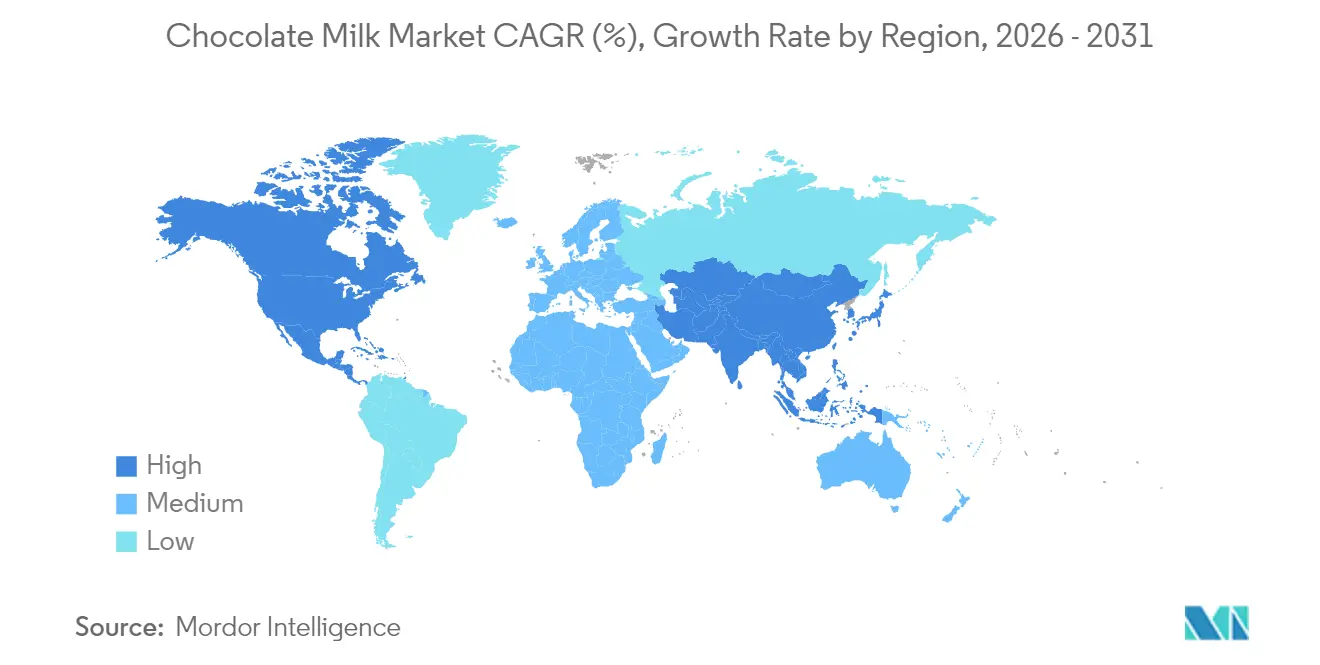

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chocolate Milk Market Analysis by Mordor Intelligence

The chocolate milk market size is expected to grow from USD 19.42 billion in 2025 to USD 20.8 billion in 2026 and is forecast to reach USD 29.31 billion by 2031 at 7.11% CAGR over 2026-2031. Once seen as a children's treat, chocolate milk is now gaining traction among adults, especially as a post-workout recovery drink. Brands like Fairlife, owned by Coca-Cola, are emphasizing their high-protein benefits. While dairy-based chocolate milk continues to dominate, due to robust production networks, plant-based alternatives from companies like Oatly and Ripple are carving out a niche. These options cater to vegans and those with lactose intolerance, all while championing sustainability. Packaging innovations are also making waves: Nestlé’s Nesquik is opting for aseptic cartons to ensure a longer shelf life, whereas regional brands are introducing smaller pouches, perfect for on-the-go snacking or school lunches. Supermarkets still lead in distribution, but cafés are catching up, showcasing premium chocolate milk formats. Starbucks, for instance, has introduced seasonal chocolate beverages, broadening the drink's appeal beyond just home consumption. In response to wellness trends and heightened scrutiny on sugar content, companies are pivoting. Danone, for example, has rolled out protein-enriched chocolate milk lines, focusing on reduced sugar and fortified variants. These trends underscore a significant evolution in chocolate milk's role in daily life, blending indulgence with health and innovation.

Key Report Takeaways

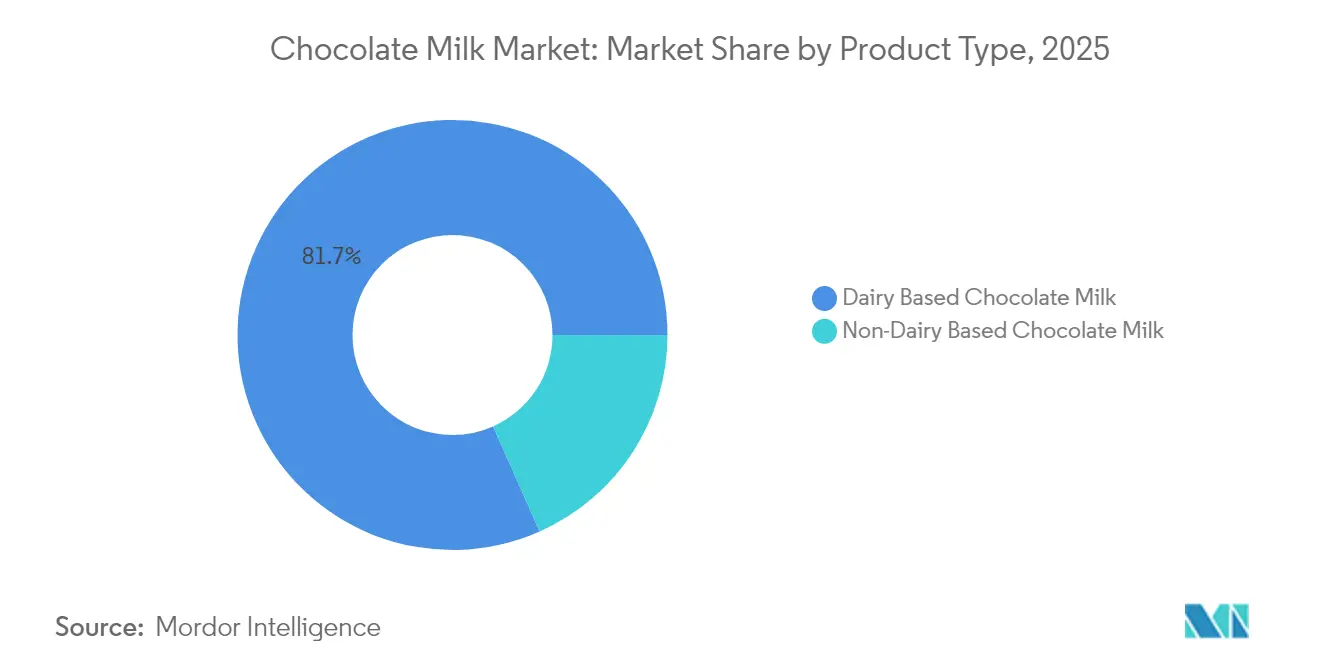

- By product type, dairy-based beverages accounted for 81.65% of the chocolate milk market share in 2025, while plant-based alternatives are projected to post a 7.76% CAGR through 2031.

- By flavor, milk and white chocolate commanded 63.05% of the chocolate milk market share in 2025; dark chocolate variants are on track to grow at an 8.42% CAGR between 2026 and 2031.

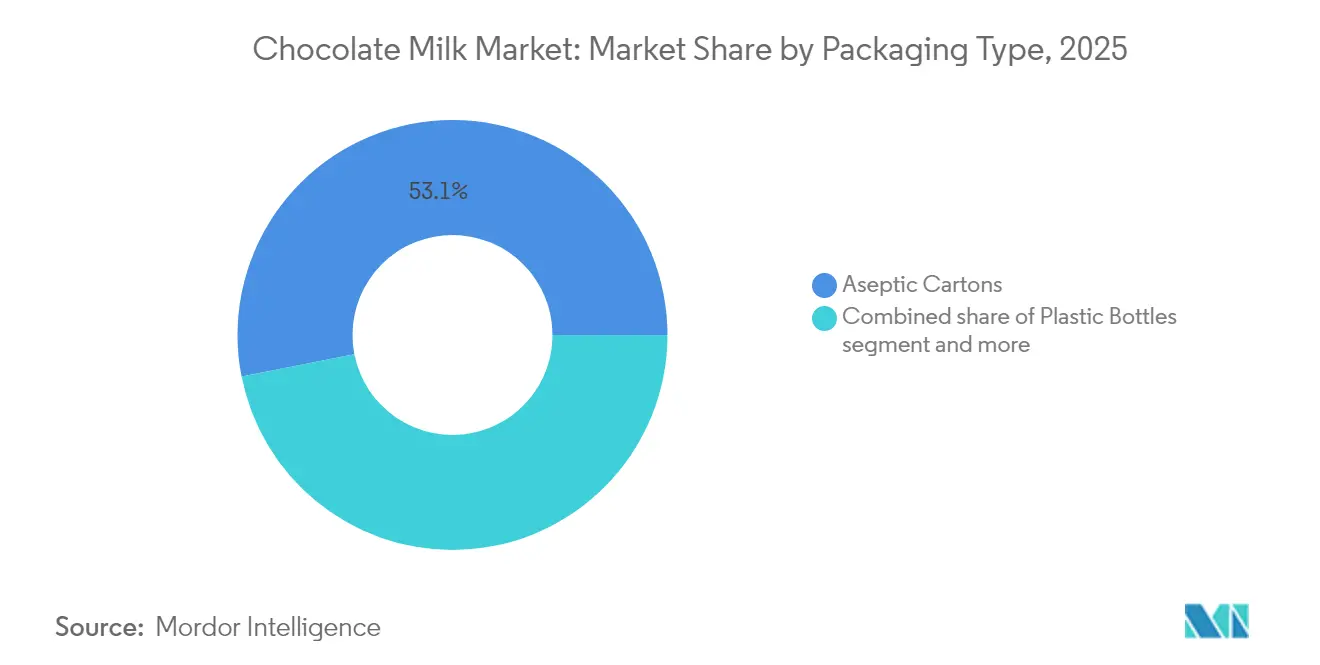

- By packaging, aseptic cartons held 53.10% revenue share in 2025; flexible pouches are advancing at an 8.31% CAGR to 2031.

- By distribution channel, retail outlets controlled 64.05% of the chocolate milk market size in 2025, whereas HORECA is forecast to expand at an 8.05% CAGR through 2031.

- By geography, North America led with 37.10% revenue share in 2025, while Asia-Pacific is registering the highest projected CAGR at 7.66% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chocolate Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Ready-to-Drink Beverages | +1.2% | Global, Asia-Pacific leading | Medium term (2-4 years) |

| Innovation in Low-Sugar and Organic Products | +1.0% | North America and Europe core markets | Long term (≥ 4 years) |

| Expansion of Modern Retail Channels | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Increased Promotional and Marketing Efforts | +0.8% | Global | Short term (≤ 2 years) |

| Partnerships and Influencer Sponsorships | +0.7% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Demand for Chocolate-Based Shakes in Foodservice | +0.6% | Global, North America leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Ready-to-Drink Beverages

As consumers increasingly prioritize convenience without sacrificing taste or functionality, the demand for ready-to-drink beverages surges, propelling the chocolate milk market forward. With single-serve, shelf-stable packaging, chocolate milk has emerged as a go-to option for those on the move. Nestlé's 2024 expansion of its Nesquik RTD line, featuring resealable bottles aimed at both children and young adults, underscores this trend. Health-conscious formats bolster this momentum; for instance, Fairlife markets its protein-rich chocolate milk drinks as post-workout recovery solutions, positioning them as a nutritious alternative to conventional sports beverages. Oatly, a plant-based innovator, is seizing the opportunity with its 2024 launch of chocolate oat milk in ready-to-drink cartons, targeting new retail channels and appealing to those desiring portable, sustainable options. Foodservice outlets, too, are joining the fray, with Starbucks introducing limited-time chocolate ready-to-drink options to their grab-and-go beverage menus. Danone's investment in expanding chilled RTD chocolate milk under its Horizon Organic brand underscores the alignment of premium organic formats with consumer trust in clean-label beverages. Convenience stores and online platforms are not left behind; rapid delivery apps in Asia are promoting RTD chocolate milk multipacks as quick indulgence buys. A global labor force expansion bolsters this surge in demand. The International Labour Organization highlights that by 2025, the employed population will have reached 3.6 billion, a significant jump[1]Source: International Labour Organization, “Employment by Sex and Age,” ilo.org. This growth signals a rise in working consumers with increasingly busy routines, leading them to favor ready-to-drink formats like chocolate milk to seamlessly fit into their modern, on-the-go lifestyles.

Innovation in Low-Sugar and Organic Products

Health-conscious consumers are increasingly turning to low-sugar and organic chocolate milk, seeking indulgent flavors without the burden of excessive sugar or artificial additives. According to the International Food Information Council, 66% of Americans in 2024 reported efforts to limit their sugar intake, a rise from 61% in 2023. This growing trend is directly shaping purchase decisions in the chocolate milk segment. In response, brands are crafting functional formulations that prioritize both taste and wellness [2]Source: International Food Information Council,“2024 Food & Health Survey,” ific.org. In 2024, Horizon Organic bolstered its chocolate milk lineup with a low-sugar organic variant, spotlighting grass-fed milk and clean-label ingredients, appealing to parents seeking healthier choices for their kids. Meanwhile, Fairlife rolled out a plant-based chocolate protein milk with reduced sugar, catering to adults who blend indulgence with fitness aspirations. Retailers are amplifying this trend, dedicating chilled sections to organic and reduced-sugar products, enhancing their visibility and convenience. Furthermore, cafés and quick-service outlets are now serving organic and low-sugar chocolate drinks, catering to urban professionals who favor beverages that complement their wellness routines. These innovations are broadening the consumer base and enticing even the most skeptical buyers, solidifying chocolate milk's status as a functional yet indulgent ready-to-drink beverage.

Increased Promotional and Marketing Efforts by Key Players

In 2024, the National Dairy Council's school-based initiative made hot chocolate milk a daily choice for kids. Horizon Organic's "This Milk Means Business" campaign, emphasizing indulgent taste and organic sourcing, targeted health-conscious parents. Byrne Dairy promoted its reduced-sugar chocolate milk through school outreach and retail promotions, blending innovation with visibility. These strategies align with consumer behavior data: the International Food Information Council found that 85% of Americans prioritize taste in food and beverage purchases, making campaigns emphasizing chocolate milk's indulgence particularly potent. Concurrently, 76% of consumers consider price and 62% prioritize healthfulness, indicating a strong appeal for promotions that merge affordability with wellness claims, such as organic or reduced-sugar positioning. Moreover, 54% of consumers engaged with food and nutrition content on social media in 2024, a rise from 42% in 2023, highlighting the growing influence of digital storytelling and influencers in boosting chocolate milk's visibility [3]Source: International Food Information Council,“2024 Food & Health Survey,” ific.org. Collectively, these marketing endeavors are not merely raising awareness but are actively transforming chocolate milk's image from a nostalgic treat to a functional, everyday beverage.

Rising Demand for Chocolate-Based Shakes and Gourmet Flavors in Foodservice

Driven by a surge in demand for chocolate-based shakes and gourmet flavors, foodservice channels are breathing new life into the chocolate milk market. Cafés, QSRs, and upscale restaurants are now prominently featuring indulgent chocolate milkshakes, malted drinks, and flavored lattes, elevating chocolate milk from a mere household staple to a sought-after ingredient in the foodservice realm. In 2024, Starbucks and regional café chains rolled out limited-edition chocolate milkshakes and chocolate cold brews, seamlessly weaving flavored milk into their premium offerings. Fast-food giants like Shake Shack and Dairy Queen joined the fray, introducing seasonal chocolate milkshake flavors, amplifying trials, and solidifying chocolate milk’s indulgent image. This trend resonates with younger consumers, who are on the lookout for beverages that blend nostalgia with a modern twist, gravitating towards gourmet flavors like dark chocolate, salted caramel, and mocha. Retailers and dairy brands are seizing this opportunity, collaborating with foodservice partners to co-develop chocolate milk SKUs, bridging the gap between in-store purchases and dining out. By championing chocolate milk as both a refreshing beverage and a pivotal ingredient in gourmet creations, the trend is broadening its appeal across various consumption occasions, propelling consistent market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns about Childhood Obesity and Diabetes | -0.8% | Global, North America and Europe most affected | Long term (≥ 4 years) |

| Regulatory Pressures on Sugar and Health Labeling | -0.6% | North America and Europe core, expanding globally | Medium term (2-4 years) |

| Sourcing Challenges for Pure Cocoa | -0.5% | Global supply-chain impact | Short term (≤ 2 years) |

| Penetration of Alternative Functional Beverages | -0.4% | Global, varying intensity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Concerns about Childhood Obesity and Diabetes

Amid rising health concerns, especially regarding childhood obesity and diabetes, chocolate milk consumption faces mounting scrutiny. Parents and caregivers are now more vigilant about sugar content in beverages, leading many to limit or even avoid chocolate milk for children, both at home and in schools. Data from the Centers for Disease Control and Prevention (CDC) in 2024 highlights the issue: roughly 21.1% of U.S. children and adolescents aged 2–19 grapple with obesity, a significant jump from 13.9% in 2000 [4]Source: Centers for Disease Control and Prevention, “Childhood Obesity Facts,” cdc.gov. Furthermore, the rate of severe obesity has doubled, climbing from 3.6% to 7.0%. In response to these concerning statistics, policymakers and school authorities are stepping in, enacting regulations that curtail flavored milk offerings. While retailers and foodservice providers are pivoting, either by reformulating their products or championing low-sugar alternatives, traditional chocolate milk sales are still feeling the pinch. Health-conscious families are increasingly gravitating towards unsweetened or plant-based options. Consumer behavior data underscore this shift: parents are now prioritizing sugar content, calorie counts, and added nutrients over mere taste when making purchases. As a result, these health concerns are dampening both trial and consumption frequency, especially among younger audiences, leading to a deceleration in growth for conventional chocolate milk formulations.

Strong Market Penetration for Other Alternative Beverages

As energy drinks and functional beverages gain traction, the chocolate milk market feels the heat. Today's consumers are on the lookout for drinks that offer tangible health benefits, be it energy, hydration, or mental clarity. This shift in preference makes functional drinks more enticing than traditional chocolate milk. In 2024, brands such as Red Bull and Monster rolled out functional energy drinks, honing in on mental alertness, stamina, and hydration. Young adults and fitness enthusiasts, a demographic that once leaned towards chocolate milk. In response, retailers and foodservice operators are carving out dedicated shelf space and menu slots for these trendy beverages. This move not only boosts the visibility of functional drinks but also sidelines chocolate milk, limiting its trial opportunities. The growing demand for functional beverages highlights a significant change in consumer behavior, driven by health-conscious and performance-oriented lifestyles. This trend poses a challenge for chocolate milk brands, as they must adapt to remain competitive. While functional drinks capitalize on their perceived benefits, chocolate milk brands need to emphasize their nutritional value and versatility. The market's evolution suggests that innovation and strategic positioning will be critical for chocolate milk to sustain its relevance. The surge in functional drinks underscores a larger trend: consumers are increasingly goal-oriented in their beverage choices. In a bid to stay relevant, chocolate milk brands are rolling out innovative formulations. Examples include Shamrock Farms’ protein-enriched chocolate milk and TruMoo’s lactose-free variant with reduced sugar, both tailored to meet the evolving health and performance-centric market demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plant-Based Innovation Accelerates

In 2025, dairy-based products dominated the chocolate milk market, commanding an 81.65% share. This segment holds the advantages of established supply chains, cost efficiencies, and a strong bond with consumers. Brands like TruMoo Chocolate Milk, with its emphasis on real milk and natural flavors, cater to families prioritizing both taste and nutrition. Meanwhile, Shamrock Farms Chocolate Milk, touting its classic taste and nutrient-rich profile, has cultivated loyalty among both children and adults, underscoring the dairy segment's robustness against rising alternatives.

Non-dairy chocolate milk is the market's fastest-growing segment, projected to expand at a CAGR of 7.76% through 2031, driven by a consumer shift towards plant-based, lactose-free choices. Leading the charge, Silk Soy Chocolate Milk's soy-based variants are favored for their high protein content. Oatly Chocolate Milk, with its creamy texture and sustainability focus, is rapidly gaining popularity. Targeting the premium market, Almond Breeze Chocolate Milk offers indulgent flavors and fortification with calcium and other nutrients. Meanwhile, niche players are emerging with innovative options like pea protein and hemp-based chocolate drinks, emphasizing taste, texture, and functional benefits to appeal to health-conscious and environmentally aware consumers.

By Flavor: Dark Chocolate Premiumization Trend

In 2025, milk chocolate continues to dominate the chocolate milk landscape, commanding the largest market share. Its universally appealing sweetness has cemented its status as a favorite among children and families, the primary consumers. Brands such as TruMoo Classic Milk Chocolate and Nesquik Milk Chocolate capitalize on their well-known flavors, bolstered by nutrient-rich, low-sugar, and protein-enhanced formulations to foster brand loyalty. Fairlife Milk Chocolate stands out with its high-protein, lactose-free offerings, while Horizon Organic Milk Chocolate caters to health-conscious families by spotlighting organic ingredients and clean-label formulations. Meanwhile, white chocolate variants, though occupying a smaller niche, prefers consistent demand in premium and specialty markets. Often used as bases for seasonal or limited-edition flavors, they play a pivotal role in brand differentiation and consumer trials.

Dark chocolate variants are on a rapid ascent, projected to grow at a CAGR of 8.42% through 2031. This surge is largely attributed to consumer perceptions linking dark chocolate with health benefits and its premium market positioning. While the segment prefers associations with antioxidants and a lower sugar profile, brands must navigate sweetening carefully to ensure taste. Innovatively, brands are rolling out both functional and indulgent dark chocolate variants: Luker Chocolate’s Caramel Dark Chocolate Milk caters to refined tastes, Organic Valley Dark Chocolate Milk champions organic and low-sugar attributes, and Silk Dark Chocolate Soy Milk targets health-conscious adults with its plant-based, high-protein appeal. These diverse offerings underscore a broader trend: a blend of adult indulgence, premiumization, and a focus on functional nutrition. This strategy enables chocolate milk brands to tap into both the traditional family market and the burgeoning niche segments driven by wellness and refined taste preferences.

By Packaging: Sustainability Drives Flexible Growth

In 2025, aseptic cartons continue to dominate the chocolate milk packaging landscape, commanding the 53.10% market share. Their appeal lies in their shelf stability, convenience, and premium market positioning, making them the go-to choice for retailers and consumers alike. Notable brands, including TruMoo Classic Milk Chocolate and Fairlife Milk Chocolate, alongside India's Amul Kool Chocolate Milk and Britannia NutriChoice Chocolate Milk, are leveraging aseptic cartons. These cartons not only promise an extended shelf life but also house nutrient-rich formulations. Furthermore, innovations like Tetra Pak’s Evero Aseptic cartons and their bottle-shaped designs not only uphold product quality but also resonate with environmentally conscious consumers, solidifying the carton’s dominant market stance.

Flexible pouches and sachets are rapidly gaining traction, emerging as the fastest-growing packaging segment with a projected CAGR of 8.31% through 2031. Their rise is attributed to trends emphasizing portability, convenience, and sustainability. Brands such as Silk Milk Chocolate, Soy Milk, and Fairlife Milk Chocolate, along with India's Epigamia Chocolate Milk Pouches, Raw Pressery Chocolate Milk, and Gowardhan Chocolate Milk, are tapping into this trend. They've rolled out spouted pouches, catering to the demands of on-the-go consumers and single-serve occasions. On the innovation front, companies like Gualapack and Cheer Pack are crafting specialized spouted pouches tailored for liquid dairy products. Meanwhile, Stonyfield is leading the charge with its all-PE recyclable spouted pouches, underscoring a commitment to eco-friendly and technically sound solutions. While other formats like plastic bottles, glass bottles, and metal cans still cater to niche demands, be it single-serve convenience, a premium feel, or durability in sports nutrition, the global and Indian consumer landscape is unmistakably leaning towards lightweight, portable, and sustainable choices.

By Distribution Channel: HORECA Expansion Opportunity

In 2025, retail channels command a significant 64.05% share of the chocolate milk market, a testament to ingrained consumer habits and widespread availability. While traditional supermarkets and hypermarkets remain pivotal, online platforms and convenience stores are swiftly broadening their presence. Brands such as Amul Kool, Epigamia, and Britannia are rolling out ready-to-drink chocolate milk in cartons and pouches, emphasizing a blend of taste, nutrition, and convenience. Meanwhile, Slate Milk is pioneering a direct-to-consumer approach, utilizing subscription services to connect directly with health-conscious consumers in search of premium chocolate milk. Additionally, convenience stores and vending machines bolster single-serve purchases, catering to impulse buyers and amplifying market penetration.

HORECA channels are witnessing the most rapid growth, projected to expand at a CAGR of 8.05% through 2031. Foodservice operators are increasingly tapping into chocolate milk's versatility, using it not just as a beverage but also as an ingredient in specialty dishes. From complementing children's meals to crafting indulgent drinks and desserts for adults, the applications are diverse. On a global scale, Nestlé Professional is championing chocolate milk in schools and cafeterias, while Indian chains like Cafe Coffee Day, Barista, and Domino’s are incorporating it into kids’ combos, premium drinks, and desserts. This trend underscores the potential for chocolate milk to transcend its retail roots, with tailored SKUs, packaging, and marketing strategies propelling its growth across diverse channels.

Geography Analysis

In 2025, North America commands 37.10% market share, bolstered by its robust dairy infrastructure, proactive school nutrition initiatives, and a deep-rooted consumer affinity for chocolate milk, both as a recovery drink and a household staple. Trends like premiumization and functional enhancements are spurring innovation. Brands such as Fairlife Milk Chocolate and TruMoo Classic Milk Chocolate are now offering options that are high in protein, lactose-free, and enriched with nutrients, catering to both children and adults. The region's mature market, coupled with regulatory emphasis on sugar content in schools, steers product development towards enhanced taste, nutrition, and convenience.

Asia-Pacific emerges as the fastest-growing region, boasting a CAGR of 7.66% through 2031. Rising disposable incomes, urbanization, and a growing penchant for Western-style packaged beverages among the youth drive this growth. Nations like China, Indonesia, and India are at the forefront of this expansion. FrieslandCampina is bolstering local dairy infrastructure, while Japan's Meiji Milk Chocolate rolls out premium chocolate-flavored milk. In India, Amul Kool Chocolate Milk and Britannia NutriChoice Chocolate Milk are strategically targeting children and families. Such moves underscore the impact of strategic investments and tailored offerings in propelling market growth.

Regions like the Middle East, Africa, Europe, and South America are witnessing steady, albeit moderate, growth. In the Middle East, Almarai and Sadafco dominate the chocolate-flavored milk scene, serving both retail and foodservice sectors. Europe is leaning towards organic and clean-label chocolate milk, with sugar regulations influencing product reformulation. Meanwhile, in South America, local brands like Itambé and Piracanjuba are making strides in Brazil and Argentina, tapping into the rising middle-class demand for chocolate milk and packaged beverages. These regions, while growing at a slower pace, are shaped by their unique infrastructure, regulatory landscapes, and consumer preferences.

Competitive Landscape

In the global chocolate milk arena, multinational dairy behemoths and regional contenders vie for dominance, employing targeted marketing and distinct product offerings. Brands such as Fairlife Milk Chocolate, TruMoo Classic Milk Chocolate, and Amul Kool Chocolate Milk carve out their niches by spotlighting functional advantages. These include high-protein content, lactose-free options, and added nutrients tailored for children. Marketing strategies frequently underscore a blend of indulgence and wellness, aiming at families, school initiatives, and health-conscious adults. To captivate specific consumer segments and bolster brand loyalty, companies roll out premium and limited-edition flavors, seasonal packaging, and partnerships with foodservice chains and cafes.

Leading brands harness cutting-edge processing and packaging technologies to uphold product quality and stay relevant in the market. Techniques like ultra-filtration and protein concentration empower brands such as Fairlife and Britannia NutriChoice Chocolate Milk to boost protein content while controlling lactose levels. This strategy caters to both indulgent and functional consumption moments. Innovations in packaging, from aseptic cartons and spouted pouches to eco-friendly materials, not only guarantee shelf stability and convenience but also champion sustainability. Brands like Epigamia Chocolate Milk Pouches and Stonyfield are setting the gold standard in eco-conscious design.

Strategic maneuvers are the order of the day as companies aim to bolster their market stance and seize growth prospects. Giants like Nestlé and Danone are making inroads into emerging markets, establishing local production units and forging partnerships. In contrast, regional players like Almarai in the Middle East and Itambé in South America are capitalizing on their domestic distribution channels for deeper market penetration. Through mergers, co-branding, and alliances with HORECA channels and online retailers, brands are amplifying their visibility, especially for premium or functional chocolate milk offerings. Addressing shifting consumer tastes, brands are exploring white-space strategies, introducing adult-centric indulgent products and hybrid formulations infused with probiotics or collagen, underscoring their commitment to long-term competitive edge.

Chocolate Milk Industry Leaders

Nestlé S.A.

Danone S.A.

The Coca-Cola Company

Dairy Farmers of America, Inc.

Horizon Organic Dairy, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Mars Wrigley partnered with Fire Brands to launch SNICKERS, TWIX, and MILKY WAY ready-to-drink shakes, aiming at adults seeking indulgent protein beverages.

- July 2024: FrieslandCampina expanded its Yazoo-flavoured milk range by introducing a new limited-edition chocolate orange flavor. The new Choc-Orange variant combines the Yazoo brand's signature chocolate milk with citrus notes and aims to 'entice' new shoppers into the category.

- January 2024: Dairy Farmers of America debuted TruMoo Zero and Milk50, zero-sugar lines fortified with extra protein, responding to school and retail sugar targets.

Global Chocolate Milk Market Report Scope

Chocolate milk is sweetened chocolate-flavored milk. Chocolate milk is made by mixing chocolate syrup with milk.

The Chocolate Milk Market is segmented by type, distribution channel, and geography. By type, the market is segmented into dairy and non-dairy-based chocolate milk. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East, and Africa. For each segment, market sizing and forecast is based on value (USD million).

Product Type

| Dairy Based Chocolate Milk |

| Non-Dairy Based Chocolate Milk |

By Flavor

| Dark Chocolate |

| Milk and White Chocolate |

Packaging

| Aseptic Cartons |

| Plastic Bottles |

| Flexible Pouches and Sachets |

| Glass Bottles |

Distribution Channel

| HORECA | |

| Retail | Supermarket/Hypermarket |

| Online Retail Channel | |

| Convenience/Grocery Stores | |

| Other Distribution Channel |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Dairy Based Chocolate Milk | |

| Non-Dairy Based Chocolate Milk | ||

| By Flavor | Dark Chocolate | |

| Milk and White Chocolate | ||

| Packaging | Aseptic Cartons | |

| Plastic Bottles | ||

| Flexible Pouches and Sachets | ||

| Glass Bottles | ||

| Distribution Channel | HORECA | |

| Retail | Supermarket/Hypermarket | |

| Online Retail Channel | ||

| Convenience/Grocery Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the chocolate milk market?

The chocolate milk market size is USD 20.8 billion in 2026.

How fast will chocolate milk sales grow through 2031?

Sales are projected to rise at a 7.11% CAGR, reaching USD 29.31 billion by 2031.

Which region shows the strongest growth potential for chocolate milk?

Asia-Pacific is the fastest-growing geography with a 7.66% CAGR forecast.

Are plant-based chocolate milks gaining traction?

Yes, non-dairy alternatives register a 7.76% CAGR, outpacing overall category growth.

Page last updated on: