Tissue Paper Converting Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

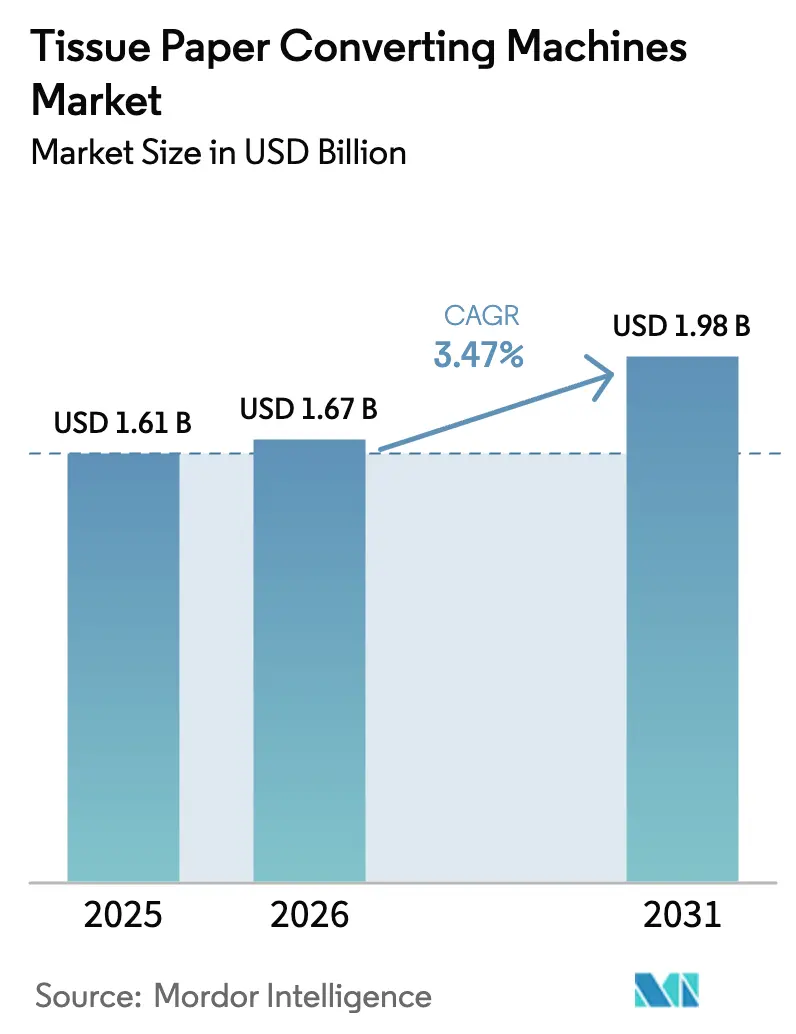

| Market Size (2026) | USD 1.67 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 3.47% CAGR |

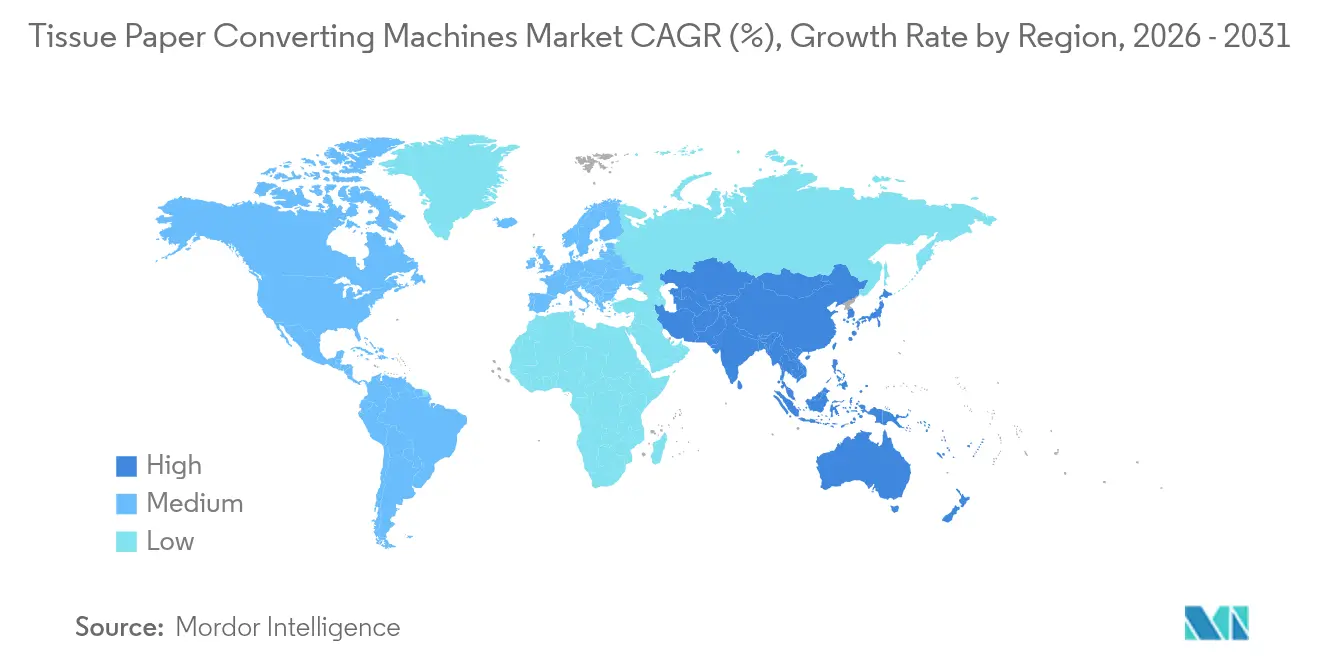

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tissue Paper Converting Machines Market Analysis by Mordor Intelligence

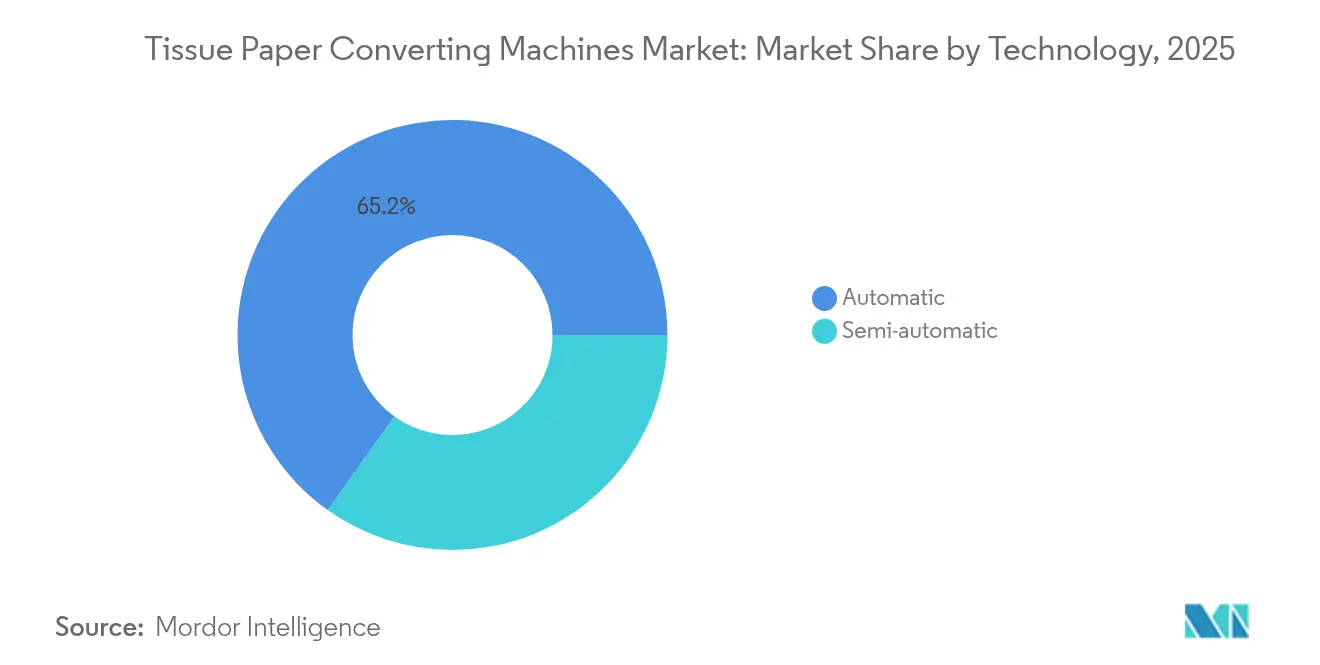

Tissue paper converting machines market size in 2026 is estimated at USD 1.67 billion, growing from 2025 value of USD 1.61 billion with 2031 projections showing USD 1.98 billion, growing at 3.47% CAGR over 2026-2031. Consistent consumption of tissue products, steady equipment replacement cycles, and rising factory automation keep demand on a clear upward path. Automatic technology already accounts for 65.67% of global installations, reflecting an industry‐wide shift toward unmanned, data-driven production lines. Sustainability targets further accelerate upgrades as converters adopt energy-efficient dryers, induction-heated Yankee cylinders, and low-waste embossing units. Digital transformation rounds out the growth narrative; predictive-maintenance platforms and digital-twin models now inform purchasing decisions as much as mechanical design.

Key markets show different but complementary trajectories. North America held 40.56% share in 2024, anchored by large-scale modern mills and strong brand loyalty. Asia-Pacific delivers the fastest rise at 6.78% CAGR to 2030 as hygiene awareness and converting capacity expand across China, India, and Southeast Asia. Machine-type preferences also shift: toilet-roll lines still lead with 45.34% share, yet kitchen-roll systems advance at 7.29% CAGR on the back of premium kitchen-towel demand. High-speed lines of at least 800 m/min already command 52.34% share and grow 5.49% a year as converters chase lower unit costs.

Key Report Takeaways

- By technology, automatic lines captured 65.15% of tissue paper converting machines market share in 2025 while expanding at a 4.66% CAGR through 2031.

- By machine type, toilet-roll equipment led with 44.92% revenue share in 2025; kitchen-roll systems are forecast to move ahead at a 7.12% CAGR to 2031.

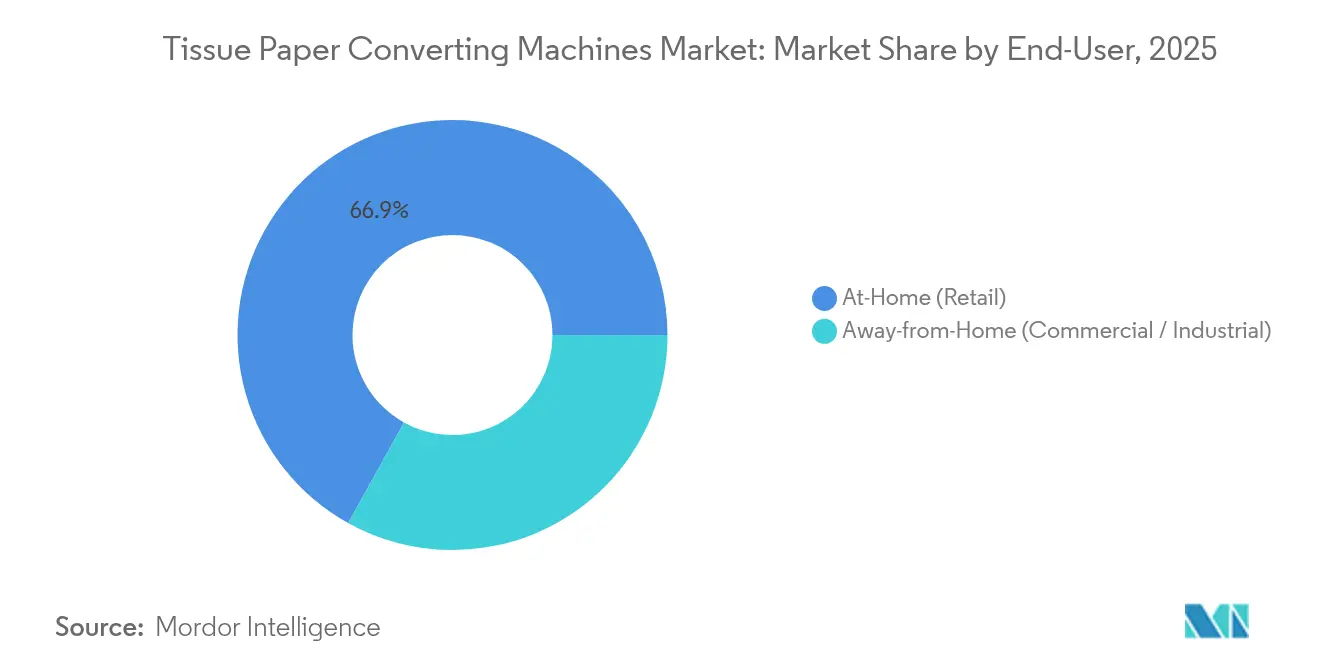

- By end-use, the At-Home segment accounted for 66.93% of the tissue paper converting machines market size in 2025, whereas Away-from-Home demand shows the fastest growth at 4.28% through 2031.

- By production speed, high-speed lines (≥800 m/min) held 51.78% share of the tissue paper converting machines market size in 2025 and will lift output at a 5.41% CAGR to 2031.

- By geography, North America dominated with 40.12% share in 2025, yet Asia-Pacific registers the highest 6.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tissue Paper Converting Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global tissue consumption and hygiene awareness | +0.8% | Global, with accelerated adoption in Asia-Pacific and MEA | Medium term (2-4 years) |

| Growing trend of automation in tissue converting | +1.2% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Sustainability-oriented innovations in converting tech | +0.6% | Europe leading, North America following, Asia-Pacific emerging | Long term (≥ 4 years) |

| Digital-twin and IoT boosting OEE | +0.4% | Developed markets initially, global rollout by 2028 | Medium term (2-4 years) |

| Surge in private-label AfH short-run demand | +0.3% | North America and Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Tissue Consumption and Hygiene Awareness

Sustained post-pandemic hygiene priorities keep tissue volumes on an upward curve. Institutional buyers now request premium converting lines that can handle softer substrates, deeper embossing, and rapid changeovers for differentiated branding.[1]Simon Matthis, “Toscotec Launches New Concept Machine for a More Sustainable Structured Tissue,” Pulpaper News, pulpapernews.com New energy-efficient machines such as Toscotec’s INGENIA cut energy use by 35% yet maintain through-air-dried quality, a combination that unlocks both cost and environmental gains. Commercial kitchens and food-service chains fuel steady orders for kitchen-roll formats with higher absorbency standards, pushing converters toward multi-emboss units and in-line ply bonding. Product mix complexity encourages factories to add flexible unwind stands and programmable knife systems, enabling them to shift between retail and institutional SKUs without long downtime. This sustained demand backdrop undergirds the tissue paper converting machines market and encourages continued equipment modernisation despite moderate headline growth.

Growing Trend of Automation in Tissue Converting

Automation now shapes competitive advantage. Automatic systems already represent two-thirds of installed capacity and grow faster than the broader tissue paper converting machines market. TAPPI’s Tissue 101 and Tissue 202 courses highlight the sector’s commitment to up-skilling operators for such lines.[2]TAPPI, “Registration Now Open: Essential In-Person Tissue Training Courses,” tappi.org BW Converting’s MIAC 2024 showcase introduced high-speed interfolders and coreless rewinding modules, proving that automation opens new product avenues. Fully integrated drives, servo knife positions, and automatic roll-handling robots shorten changeovers and trim labor costs while improving safety. Factories without such technology risk falling behind on cost, quality, and delivery reliability, prompting a replacement wave that keeps the tissue paper converting machines market expansion intact.

Sustainability-Oriented Innovations in Converting Tech

Regulators tighten energy rules and brand owners pledge Scope 3 emission cuts. Equipment builders have responded with electric induction Yankee dryers that eliminate direct fossil fuel use and lower dryer shell temperatures, thereby improving safety. Valmet’s Advantage QRT technology demonstrates 45% energy reduction while preserving softness and bulk.[3] Valmet, “Valmet and Körber Joint Venture Advances Digital Offering,” valmet.com Upcoming efficiency standards for electric motors from 2027 will reinforce demand for such upgrades. Early adopters secure lower operating costs and favorable ESG profiles, spurring peers to accelerate investment and sustaining healthy order books for the tissue paper converting machines market.

Digital-Twin and IoT Boosting OEE

Data frameworks now accompany most capital orders. Valmet’s 2024 acquisition of FactoryPal embeds AI analytics into everyday production decisions, helping mills cut unplanned downtime and lift overall equipment effectiveness. ANDRITZ’s Metris platform lets operators model line performance virtually, tweak recipe settings, and then deploy the optimal code to the machine. Remote dashboards reset the operating baseline toward predictive rather than reactive maintenance. Converters extract greater capacity from existing assets, thereby justifying incremental digital retrofits alongside major mechanical rebuilds. This use of digital twins grows in tandem with the tissue paper converting machines market as new lines ship with edge-ready sensors and secure cloud gateways as standard.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for greenfield converting plants | -0.5% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Volatile pulp and energy prices | -0.3% | Global, with regional variations in energy costs | Short term (≤ 2 years) |

| Shortage of skilled operators for advanced lines | -0.4% | Developed markets primarily, spreading to Asia-Pacific | Medium term (2-4 years) |

| Stricter noise and energy rules on machinery | -0.2% | Europe leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for Greenfield Converting Plants

A new integrated mill demands hundreds of millions of dollars. First Quality Tissue recently earmarked USD 984 million for two Thru-Air-Dried lines plus converting halls in Ohio. Even for established firms, such sums dictate lengthy payback horizons. Smaller companies often forgo large-scale builds and instead upgrade existing lines, which tempers incremental capacity growth in the tissue paper converting machines market. Interest-rate swings further complicate investment timing, especially in emerging regions where credit costs stay elevated.

Volatile Pulp and Energy Prices

Fluctuations in pulp and power prices compress converter margins and can delay machinery orders. Norske Skog’s multibillion-krone pulp project underscores the industry’s drive to secure raw-material self-sufficiency and insulation from price swings. Energy-intensive converting lines face the same volatility; high grid prices make a compelling case for energy-saving drives but can postpone full-line replacements until cost pressures ease, dampening near-term machinery shipments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Automatic Lines Redefine Operations

Automatic lines hold 65.15% of tissue paper converting machines market share in 2025 and expand at a 4.66% CAGR through 2031. These smart systems integrate servo drives, robotic roll handling, and camera-based defect detection. Their superior throughput and lower labor-to-output ratio lift factory productivity, helping purchasers offset higher sticker prices over the asset life. Semi-automatic units remain relevant to niche converters needing flexibility at modest capex, especially in developing economies where wage structures still favor manual intervention.

Advanced automation also provides the foundation for digital overlays. FactoryPal, now majority-owned by Valmet, feeds real-time data from automatic lines into AI models that propose set-point changes for uptime improvement. As more converters upgrade, the tissue paper converting machines market size for fully automatic solutions is projected to expand steadily, reinforcing the technology’s dominant status.

By Machine Type: Kitchen-Roll Systems Accelerate

Toilet-roll lines remain the volume backbone, accounting for 44.92% of the tissue paper converting machines market size in 2025. Yet kitchen-roll lines post the strongest 7.12% CAGR, reflecting consumer preference for thicker kitchen towels and heightened cleaning routines in food-service outlets. Embossing-pattern flexibility and ply bonding quality now influence purchase decisions more than raw speed, spurring OEMs to offer rapid-change print and emboss cassettes.

Folded-tissue and paper-napkin lines serve institutional catering, airlines, and hospitality. Although these segments grow slower, quick pack count changeovers and inline folding accuracy retain importance. OEMs developing multi-format platforms attract buyers aiming to amortise capex across diversified product portfolios, strengthening competition inside the tissue paper converting machines market.

By End-Use Sector: Commercial Demand Gains Pace

Retail At-Home consumption supplies 66.93% of total sales. Growth is steady but less dynamic than in prior years as penetration nears parity in developed economies. In contrast, Away-from-Home demand advances at a 4.28% CAGR. Institutional customers need dispensable hand towels, jumbo rolls, and logo-printed napkins delivered in smaller, more frequent batches. Converters therefore invest in modular unwind decks, automatic tail gluing, and integrated packers that cater to varying sheet counts without long stops.

This segmental divergence means factories often configure hybrid layouts: high-speed toilet tissue assets for core retail volumes and flexible finishing cells for AfH custom jobs. Such hybridisation adds floor-space efficiency and helps maintain balanced utilisation, supporting sustainable growth of the tissue paper converting machines market.

By Production Speed: High-Speed Lines Dominate

Lines rated at ≥800 m/min command 51.78% share of installations and post a 5.41% CAGR. They drive margin optimisation through higher throughput per shift and better energy per tonne metrics when paired with low-friction drivetrains. Toscotec’s INGENIA reaches 2,000 m/min while cutting energy consumption by one-third, an illustration of technology catching efficiency and speed in one design.

Medium-speed and low-speed lines retain roles where product complexity outweighs volume, for example in multi-ply facial tissues with complex lotions or scents. A two-tier machinery strategy allows converters to respond flexibly to market swings and supports the overall resilience of the tissue paper converting machines market.

Geography Analysis

North America led the tissue paper converting machines market with 40.12% share in 2025. Recent commitments such as Kimberly-Clark’s USD 2 billion multiyear upgrade program and First Quality Tissue’s nearly USD 1 billion Thru-Air-Dried expansion illustrate continuous reinvestment in advanced assets. Retrofit activity also remains robust as mills pursue energy savings and digital dashboards to counter tight labor pools. Mature demand limits headline growth but underpins a reliable service and upgrade market for OEMs.

Asia-Pacific represents the principal growth engine with a forecast 6.63% CAGR to 2031. China’s converters scale quickly, ordering European high-speed lines to raise domestic quality standards. Regional suppliers such as Baosuo and Dalian Mach provide cost-efficient alternatives, intensifying competition and broadening equipment access. Rising middle-class incomes raise per-capita tissue use, while government hygiene campaigns spur institutional consumption. These factors together promise the strongest absolute gains for the tissue paper converting machines market across all regions.

Europe balances technology leadership with strict sustainability codes. Italian brands OMET, Maflex, and Körber Tissue keep market clout by coupling mechanical performance with noise and energy compliance. Valmet’s joint venture with Körber on digital services signals further innovation clustering in Europe. Although demand volumes rise modestly, premium equipment pricing and high aftermarket spend make Europe strategically important for technology diffusion across the global tissue paper converting machines market.

Competitive Landscape

The sector shows moderate concentration. Top European OEMs—Valmet, OMET, Körber Tissue, Toscotec, and A.Celli—combine long pedigrees with deep application expertise. Their portfolios span high-speed rewinders, embossing units, and turnkey stock-preparation systems. Asian entrants such as Baosuo, Jin Sung Ent, and Dalian Mach gain share in mid-speed and semi-automatic categories by leveraging cost advantages and shorter lead times, especially within domestic Asia-Pacific orders.

Strategic differentiation now revolves around digital readiness and sustainability credentials. Valmet’s FactoryPal acquisition embeds AI into production optimisation, a service model rather than pure hardware sale. Toscotec’s electric Steel Yankee Dryer points to process breakthroughs that reduce carbon intensity while elevating safety. Joint ventures, tech swaps, and licensing deals accelerate innovation dissemination and keep competitive dynamics fluid.

Service contracts, spare-parts logistics, and operator training increasingly shape long-term customer allegiance. OEMs with globe-spanning service hubs secure renewal orders and recurring revenue streams, fortifying their positions in the tissue paper converting machines market. Market consolidation remains possible as capital intensity rises and smaller factories seek partners for next-generation lines.

Tissue Paper Converting Machines Industry Leaders

C.G. Bretting Manufacturing Company, Inc.

Valmet Oyj

9.Septembar Tissue Converting

Serv-o-Tec GmbH

SDF Schnitt-Druck-Falz Spezialmaschinen GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Valmet secured a major paper machine rebuild for Sylvamo in North America.

- February 2025: First Quality Tissue selected Defiance, Ohio, for its new ultra-premium towel and tissue complex featuring two Thru-Air-Dried lines.

- January 2025: Kimberly-Clark pledged more than USD 2 billion to expand US manufacturing and automate distribution.

- October 2024: Valmet and Kruger Products started up an Advantage DCT 200 TS tissue machine in Quebec.

Global Tissue Paper Converting Machines Market Report Scope

The study tracks the revenue generated from the sales of tissue paper converting machines offered by the vendors operating in the market. The scope of the study includes the cost of integrated service and consumables offered with the purchase of the machine, and it excludes the after-sales service cost. The study provides market estimates and forecasts in terms of revenue (USD) for key segments. The market study factors are based on the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The tissue paper converting machines market is segmented by technology (automatic and semi-automatic), machine type (toilet roll converting lines, kitchen roll converting lines, folded tissue-converting lines, paper napkin converting lines, and standalone systems), and geography (North America [United States and Canada], Europe [Germany, France, Italy, United Kingdom, and Rest of Europe], Asia-Pacific [Japan, India, China, Indonesia, and Rest of Asia-Pacific], Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period.

| Automatic |

| Semi-automatic |

| Toilet-Roll Converting Lines |

| Kitchen-Roll Converting Lines |

| Folded-Tissue Converting Lines |

| Paper-Napkin Converting Lines |

| Stand-alone Systems |

| At-Home (Retail) |

| Away-from-Home (Commercial / Industrial) |

| High-speed Lines (greater than 800 m/min) |

| Medium-speed Lines (400-799 m/min) |

| Low-speed Lines (less than 400 m/min) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | Automatic | ||

| Semi-automatic | |||

| By Machine Type | Toilet-Roll Converting Lines | ||

| Kitchen-Roll Converting Lines | |||

| Folded-Tissue Converting Lines | |||

| Paper-Napkin Converting Lines | |||

| Stand-alone Systems | |||

| By End-Use Sector | At-Home (Retail) | ||

| Away-from-Home (Commercial / Industrial) | |||

| By Production Speed | High-speed Lines (greater than 800 m/min) | ||

| Medium-speed Lines (400-799 m/min) | |||

| Low-speed Lines (less than 400 m/min) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the tissue paper converting machines market?

The tissue paper converting machines market size reached USD 1.67 billion in 2026 and is forecast to reach USD 1.98 billion by 2031.

Which technology segment leads the market?

Automatic tissue paper converting lines held 65.15% of global installations in 2025 and are growing at a 4.66% CAGR.

Why are kitchen-roll lines growing faster than toilet-roll lines?

Kitchen-roll equipment benefits from higher household cleaning standards and expanding food-service demand, resulting in a 7.12% CAGR through 2031 while toilet-roll lines grow more slowly.

Which region is expanding the fastest?

Asia-Pacific records the highest 6.63% CAGR on expanding capacity, rising hygiene awareness, and investment in modern high-speed equipment.

Page last updated on: