Europe Barrier Films Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

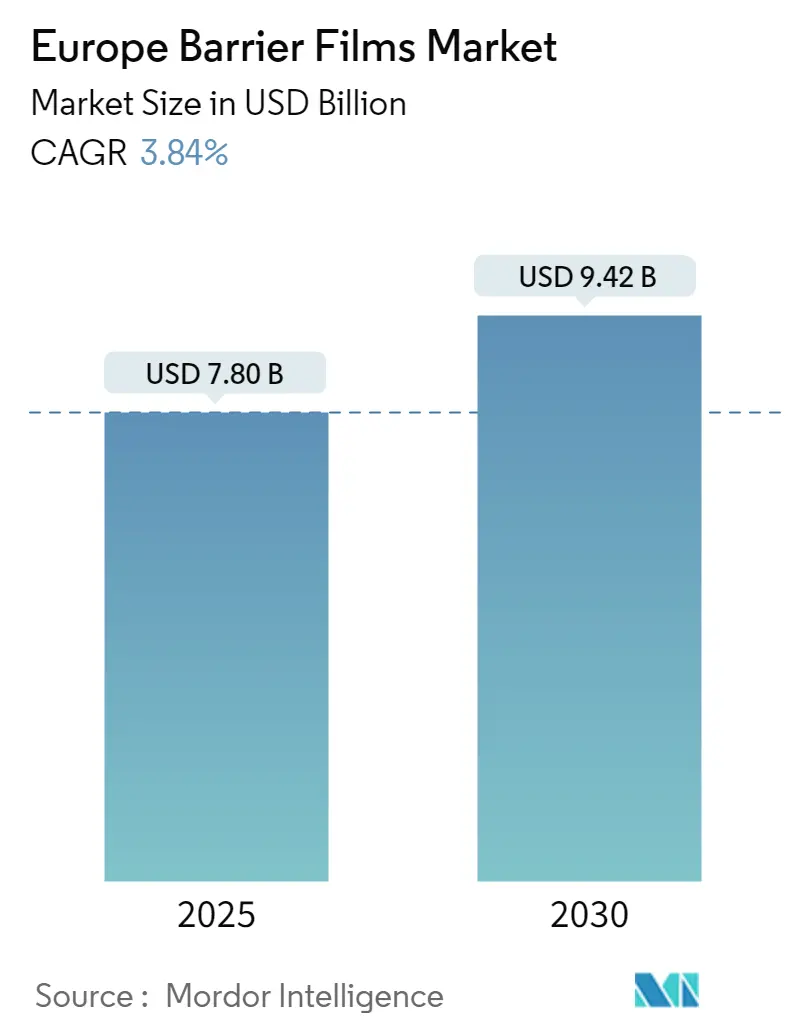

| Market Size (2025) | USD 7.80 Billion |

| Market Size (2030) | USD 9.42 Billion |

| Growth Rate (2025 - 2030) | 3.84% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Barrier Films Market Analysis by Mordor Intelligence

The Europe Barrier Films Market size is worth USD 7.80 Billion in 2025, growing at an 3.84% CAGR and is forecast to hit USD 9.42 Billion by 2030.

The European packaging industry is experiencing significant transformation driven by technological advancements and changing consumer preferences. The German packaging sector, a key indicator of regional market strength, generated revenue of EUR 35 billion in 2022, demonstrating robust growth in the flexible packaging segment. Manufacturing companies across Europe are increasingly investing in advanced processing technologies and innovative materials to enhance barrier properties while reducing material usage. The integration of digital technologies in packaging processes has enabled better quality control and improved production efficiency, particularly in high-barrier film manufacturing.

The beverage packaging sector has emerged as a significant growth driver, with German household spending on non-alcoholic beverages reaching USD 25.61 billion in 2022. This surge in beverage consumption has led to increased demand for high-performance barrier films that ensure product protection and extended shelf life. Manufacturers are responding by developing specialized barrier solutions that combine superior protection capabilities with enhanced sustainability features. The industry is witnessing a shift towards more sophisticated packaging films solutions that address both functional requirements and environmental concerns.

The market is experiencing a notable shift towards technological innovation and sustainability initiatives. In March 2023, Toppan announced the establishment of a new barrier film manufacturing facility in the Czech Republic, aiming to strengthen its European presence and meet growing demand for sustainable packaging solutions. Similarly, Trioworld's February 2023 announcement of expanding its UK stretch film production capabilities demonstrates the industry's commitment to local manufacturing and sustainable practices. These developments reflect the industry's response to increasing demand for high-quality barrier films with enhanced environmental credentials.

The personal care and pharmaceutical sectors are driving significant innovations in barrier film technology. Consumer spending on personal care products in the United Kingdom has shown consistent growth through 2022, indicating strong demand for sophisticated packaging solutions. In March 2023, Parkside introduced a new mono-polymer laminated film that can be integrated into existing UK recycling streams, representing a significant advancement in sustainable packaging technology. This innovation trend is further exemplified by the March 2023 collaboration between Amcor and Nfinite Nanotechnology, focusing on developing enhanced recyclable and biodegradable packaging solutions.

Europe Barrier Films Market Trends and Insights

Replacement of Rigid Packaging Formats

The European packaging industry is witnessing a significant shift from rigid to flexible packaging formats, driven by manufacturers' focus on cost-effectiveness, sustainability, and consumer convenience. Flexible packaging solutions like barrier films offer substantial advantages over traditional rigid packaging, including reduced material usage, lower transportation costs, and improved shelf life for products. According to Statistisches Bundesamt, the German packaging sector earned over EUR 35 billion in revenue in 2022, demonstrating the robust growth of innovative packaging films solutions. The transition is particularly evident in the food and beverage industry, where barrier films are increasingly replacing conventional glass, metal, and rigid plastic containers.

The shift towards flexible barrier films is further accelerated by changing consumer preferences for portable, lightweight, and easy-to-handle packaging formats. Manufacturers are responding to this demand by developing innovative solutions like zip-locks, resealable seals, and convenient carrying options, especially for food products such as bakery, confectionery, and dairy items. This trend is exemplified by recent industry developments, such as Jufico's launch of fully recyclable monomaterial pouches without aluminum for their organic baby food brand FruchtBar, demonstrating the industry's commitment to combining convenience with sustainability. The growing frozen food sector, which generated approximately EUR 19.54 billion in sales in 2022, has also contributed significantly to the adoption of flexible barrier films over rigid packaging formats.

Increasing Biodegradable Barrier Films

The European barrier films market is experiencing a substantial push towards biodegradable solutions, driven by stringent environmental regulations and increasing consumer awareness about sustainable packaging. Major manufacturers are investing heavily in research and development to create innovative, eco-friendly barrier films that maintain the same level of protection and functionality as traditional materials. In March 2023, Toppan demonstrated this commitment by announcing a new facility in the Czech Republic, focusing on developing sustainable and transparent barrier films for the European market, highlighting the industry's shift towards environmentally responsible packaging solutions.

The development of biodegradable barrier films is also supported by technological advancements in material science and manufacturing processes. Companies are increasingly focusing on mono-material solutions and bio-based alternatives that can be easily recycled or composted while maintaining high barrier material properties. For instance, Sealed Air has expanded its recyclable barrier film portfolio with new CRYOVAC Brand Eco BDF films, designed specifically for LDPE mechanical and chemical recycling processes. These innovations include versions made from 100% virgin materials and variants containing 30% Certified Circular Resins (CCR), demonstrating the industry's commitment to circular economy principles. The trend is further reinforced by collaborations between companies, such as TIPA's partnership with Aquapak to develop high-barrier and PVDC-free compostable films, showcasing the industry's collective effort to advance sustainable packaging solutions.

Segment Analysis: By Packaging Product

Bags & Pouches Segment in Europe Barrier Films Market

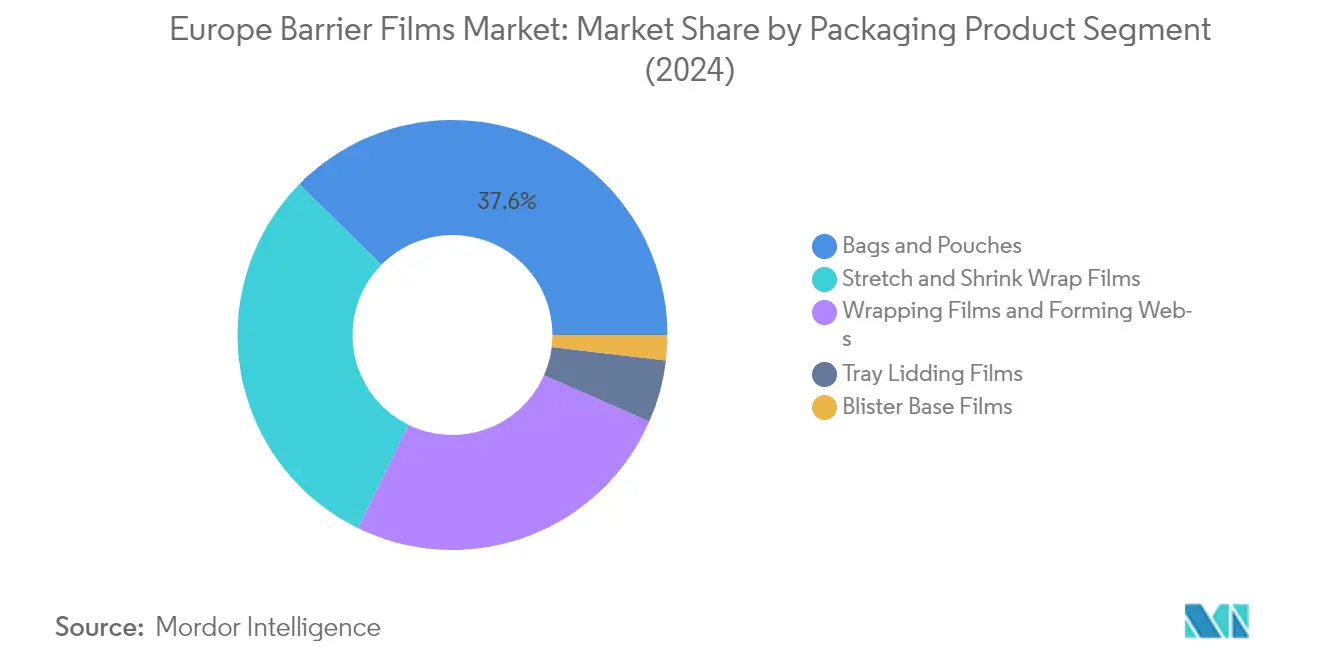

The Bags & Pouches segment continues to dominate the Europe barrier films market, holding approximately 38% market share in 2024. This segment's prominence is driven by its widespread adoption across various industries, particularly in food and beverage packaging applications. The segment's success can be attributed to its versatility in providing high-barrier protection against moisture, oxygen, and other environmental factors while offering convenient features like easy-opening and resealability. Manufacturers are increasingly focusing on developing sustainable solutions in this segment, with many companies introducing recyclable and mono-material options to meet growing environmental concerns. The segment's strong position is further reinforced by the rising demand for flexible packaging solutions that offer extended shelf life for products while maintaining product integrity and safety.

Wrapping Films and Forming Webs Segment in Europe Barrier Films Market

The Wrapping Films and Forming Webs segment is experiencing the fastest growth in the Europe barrier films market, with an expected growth rate of approximately 5% from 2024 to 2029. This robust growth is primarily driven by the increasing demand for flexible, co-extruded films with superior thermoforming qualities and enhanced puncture resistance. The segment's growth is further accelerated by innovations in multilayer barrier films technology, allowing manufacturers to create films with customized barrier properties for specific applications. The rising adoption of these films in the food industry, particularly for packaging fresh produce, meat, and dairy products, continues to drive market expansion. Manufacturers are also focusing on developing sustainable solutions in this segment, with many companies introducing recyclable options that maintain the same level of barrier protection and performance.

Remaining Segments in Barrier Films Market by Packaging Product

The remaining segments, including Stretch and Shrink Wrap Films, Tray Lidding Films, and Blister Base Films, each play crucial roles in serving specific market needs. Stretch and Shrink Wrap Films represent a significant portion of the market, particularly in industrial and logistics applications where product protection during transit is essential. Tray Lidding Films serve the growing demand for convenient, portion-controlled packaging solutions, especially in the ready-meal and processed food sectors. The Blister Base Films segment, while smaller in market share, remains vital for pharmaceutical and medical device packaging, where stringent barrier properties and sterilization capabilities are required. These segments continue to evolve with technological advancements and increasing focus on sustainable solutions.

Segment Analysis: By Material

Polypropylene Segment in Europe Barrier Films Market

The Polypropylene segment has emerged as a dominant force in the Europe barrier films market, holding approximately 24% market share in 2024. This significant market position is attributed to polypropylene's versatility in both Cast Unoriented Polypropylene (CPP) and Biaxially Oriented Polypropylene (BOPP) applications. The material's popularity stems from its cost-effectiveness, excellent clarity, good tensile strength, and high gloss properties. Polypropylene barrier films are particularly favored in food packaging applications due to their superior moisture barrier properties and chemical resistance. The segment's growth is further supported by innovations in mono-material solutions that align with European sustainability regulations and recycling requirements.

Polypropylene Segment in Europe Barrier Films Market - Growth Analysis

The Polypropylene segment is projected to maintain its strong growth trajectory, with an expected growth rate of approximately 5% during the forecast period 2024-2029. This growth is driven by increasing demand for recyclable packaging solutions and the material's superior barrier properties. The segment's expansion is supported by technological advancements in film manufacturing, particularly in developing high-performance BOPP films with enhanced barrier properties. The growth is further bolstered by the increasing adoption of polypropylene films in various applications, including food packaging, pharmaceuticals, and personal care products, due to their excellent moisture barrier properties and cost-effectiveness.

Remaining Segments in Material Segmentation

The other significant materials in the Europe barrier films market include BOPET, Polyethylene, Polyvinyl Chloride, and other materials like EVOH, Polystyrene, and Nylon. BOPET films are valued for their excellent mechanical properties and chemical resistance, making them ideal for food and pharmaceutical packaging. Polyethylene continues to be a crucial material due to its versatility and cost-effectiveness, while PVC finds specific applications in pharmaceutical blister packaging. The remaining materials, including EVOH and Nylon, play vital roles in providing specialized barrier properties for specific applications, contributing to the overall market diversity and meeting various end-user requirements.

Segment Analysis: By End-User Industry

Food and Pet Food Segment in Europe Barrier Films Market

The Food and Pet Food segment dominates the Europe barrier films market, holding approximately 33% market share in 2024, while also maintaining the highest growth trajectory for the forecast period 2024-2029 at around 4% CAGR. This segment's prominence is primarily driven by the increasing demand for extended shelf-life and protection against contamination in food products across Europe. The segment's growth is further bolstered by the rising adoption of flexible packaging solutions in the pet food industry, as manufacturers increasingly opt for barrier films that offer superior protection against moisture, oxygen, and other environmental factors. The implementation of stringent food safety regulations in European countries has also contributed to the segment's dominance, as barrier films help maintain product integrity and comply with packaging standards. Additionally, the growing consumer preference for convenient, lightweight, and sustainable packaging solutions has encouraged food manufacturers to transition from rigid to flexible barrier film packaging formats.

Beverages Segment in Europe Barrier Films Market

The Beverages segment represents a significant portion of the Europe barrier films market, demonstrating strong growth potential driven by increasing demand for innovative packaging solutions in the beverage industry. The segment's growth is supported by the rising consumption of ready-to-drink beverages and the need for packaging solutions that ensure product freshness and extended shelf life. Manufacturers are increasingly adopting barrier films for beverage packaging due to their excellent barrier properties against moisture, oxygen, and other external factors that could compromise product quality. The segment is witnessing significant innovations in sustainable barrier film solutions, particularly for applications in juice packaging, dairy beverages, and non-alcoholic drinks. The growth is further supported by the increasing adoption of pouch formats and flexible packaging solutions in the beverage industry, as these formats offer advantages such as reduced material usage, lower transportation costs, and enhanced shelf appeal.

Remaining Segments in End-User Industry

The remaining segments in the Europe barrier films market include Pharmaceutical and Medical, Personal and Home Care, and Other End-user Industries, each serving distinct market needs. The Pharmaceutical and Medical segment is driven by the stringent requirements for product protection and compliance with healthcare packaging regulations. The Personal and Home Care segment focuses on barrier films that protect against moisture and maintain product efficacy, particularly in cosmetics and household products. Other End-user Industries encompass various applications including electronics, chemicals, and agriculture, where barrier films play crucial roles in product protection and preservation. These segments collectively contribute to the market's diversity and demonstrate the versatility of barrier film applications across different industries, with each segment driven by specific requirements for product protection, regulatory compliance, and consumer convenience.

Europe Barrier Films Market Geography Segment Analysis

Barrier Films Market in Germany

Germany maintains its dominant position in the European barrier films market, commanding approximately 23% of the total market share in 2024. The country's robust packaging industry, particularly in the food and pharmaceutical sectors, continues to drive demand for high-performance barrier films. German manufacturers are increasingly focusing on developing sustainable and recyclable barrier film solutions to align with the country's strict environmental regulations and sustainability goals. The country's strong presence in medical device manufacturing and pharmaceutical production further reinforces its position in the barrier films market. Additionally, Germany's advanced technological infrastructure and research capabilities enable continuous innovation in barrier film development, particularly in areas such as mono-material solutions and bio-based alternatives. The presence of major industry players and their manufacturing facilities in the country also contributes to its market leadership. Furthermore, Germany's central location in Europe makes it a strategic hub for barrier film manufacturing and distribution across the continent.

Barrier Films Market in Italy

Italy emerges as the most dynamic market in the European barrier films sector, projected to grow at approximately 5% annually from 2024 to 2029. The country's barrier films market is experiencing rapid transformation driven by increasing adoption in pharmaceutical packaging and medical device applications. Italian manufacturers are at the forefront of developing innovative barrier film solutions, particularly focusing on sustainable and recyclable options. The country's strong food processing industry, especially in the dairy and meat sectors, continues to fuel demand for high-performance barrier films. Italy's packaging industry is witnessing significant technological advancements, with manufacturers investing in state-of-the-art production facilities. The growing emphasis on extended shelf life for food products and the rising demand for convenient packaging solutions further accelerate market growth. Additionally, Italy's strong export-oriented economy and its position as a major food producer in Europe contribute to the sustained demand for barrier films. The country's focus on research and development in packaging technologies also plays a crucial role in market expansion.

Barrier Films Market in United Kingdom

The United Kingdom maintains its position as a significant player in the European barrier films market, driven by its robust food and beverage industry and growing pharmaceutical sector. The country's focus on sustainable packaging solutions has led to increased investment in recyclable barrier film technologies. British manufacturers are particularly active in developing innovative barrier film solutions for the healthcare and personal care sectors. The UK market is characterized by strong research and development activities, with several companies focusing on creating bio-based and environmentally friendly barrier materials. The country's emphasis on food safety and extended shelf life continues to drive demand for high-performance barrier films. Additionally, the UK's strong e-commerce sector has created new opportunities for barrier film applications in packaging. The market also benefits from the presence of major multinational companies and their manufacturing facilities. Furthermore, the UK's commitment to reducing plastic waste has led to increased innovation in sustainable barrier film solutions.

Barrier Films Market in France

France demonstrates strong market potential in the barrier films sector, supported by its sophisticated packaging industry and growing demand from various end-user segments. The country's focus on environmental sustainability has led to increased adoption of eco-friendly barrier film solutions. French manufacturers are particularly active in developing innovative barrier technologies for the luxury goods and cosmetics sectors, where the country holds a significant market position. The nation's strong food and beverage industry continues to drive demand for high-performance barrier films, especially in applications requiring extended shelf life. French companies are increasingly investing in research and development to create more sustainable packaging solutions. The country's strict regulations regarding food safety and packaging materials have led to the development of advanced barrier film technologies. Additionally, France's position as a major agricultural producer in Europe contributes to the sustained demand for barrier packaging solutions.

Barrier Films Market in Other Countries

The barrier films market in other European countries, including Spain, the Netherlands, Switzerland, and the Nordic countries, shows diverse growth patterns and opportunities. These markets are characterized by varying levels of technological advancement and different regulatory frameworks regarding packaging materials. Countries in Eastern Europe are emerging as potential growth markets, driven by increasing industrialization and growing demand from the food processing sector. The Benelux region demonstrates strong potential due to its strategic location and well-developed logistics infrastructure. Mediterranean countries show increasing demand for barrier films in agricultural and food packaging applications. These markets are also witnessing a gradual shift towards sustainable packaging solutions, influenced by broader European environmental policies. The varying needs of different regional markets have led to the development of specialized barrier film solutions catering to local requirements and preferences. The presence of both established players and emerging manufacturers creates a competitive landscape that drives innovation and market growth across these regions.

Competitive Landscape

Top Companies in Europe Barrier Films Market

The European barrier films market is dominated by established players like Amcor PLC, Mondi Group, Berry Global, Huhtamaki Oyj, and Sealed Air Corporation, who have demonstrated strong capabilities in product innovation and market expansion. These companies are actively investing in research and development to create sustainable flexible packaging solutions, particularly focusing on recyclable and biodegradable barrier films. The industry has witnessed significant technological advancements in multi-layer film development, with companies emphasizing improved barrier material properties while reducing material usage. Market leaders are expanding their manufacturing footprint through strategic facility establishments and modernization initiatives, particularly in key European markets like Germany, Italy, and the UK. There is also a notable trend toward the digitalization of production processes and the integration of smart packaging solutions to meet evolving consumer demands.

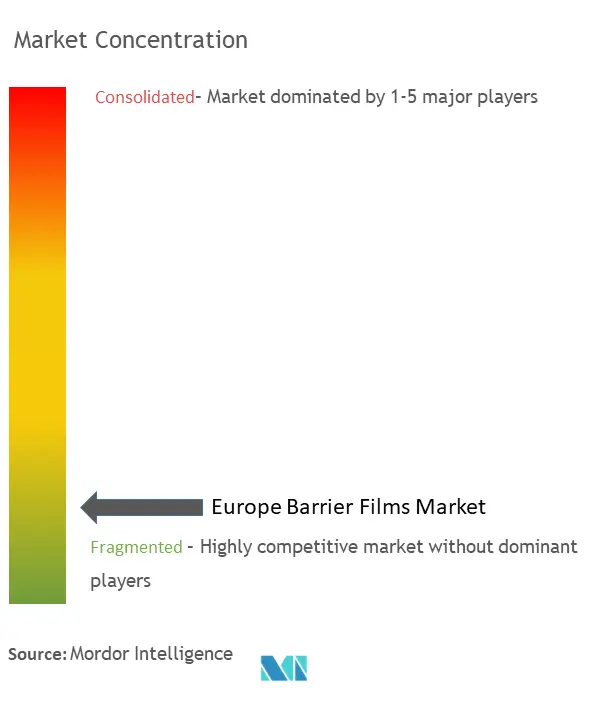

Consolidated Market with Strong Regional Players

The European barrier films market exhibits a moderately consolidated structure, characterized by the presence of both global conglomerates and specialized regional manufacturers. Global players leverage their extensive research capabilities and established distribution networks to maintain market leadership, while regional players capitalize on their local market knowledge and customer relationships. The market has witnessed significant merger and acquisition activities, with larger companies acquiring smaller, specialized manufacturers to expand their product portfolios and geographical presence. Companies like Constantia Flexibles and Wipak have strengthened their positions through strategic acquisitions of local players, particularly in Eastern European markets.

The competitive landscape is further shaped by vertical integration strategies, with several major players controlling multiple stages of the value chain, from raw material procurement to end-product manufacturing. This integration has enabled better cost control and quality assurance, while also providing advantages in terms of supply chain efficiency. The market also features collaborations between film manufacturers and technology providers, particularly in developing sustainable packaging solutions. These partnerships have become increasingly important as companies seek to address environmental concerns and meet stringent regulatory requirements across different European countries.

Innovation and Sustainability Drive Future Success

Success in the European high barrier films market increasingly depends on companies' ability to balance performance requirements with sustainability goals. Market leaders are investing heavily in developing eco-friendly alternatives to traditional packaging films, focusing on recyclable materials and reduced carbon footprint. Companies are also strengthening their positions through enhanced customer service capabilities, including customized solutions and technical support. The ability to provide end-to-end packaging solutions, rather than just barrier films, has become a crucial differentiator in the market. Additionally, manufacturers are focusing on building strong relationships with key end-user industries, particularly in the food and beverage sector, to better understand and address specific packaging requirements.

The market's future competitive dynamics will be significantly influenced by regulatory changes, particularly those related to plastic packaging and recycling requirements. Companies that can quickly adapt to these changes while maintaining product performance will gain competitive advantages. The threat of substitution from alternative packaging materials remains moderate, but companies are addressing this through continuous innovation in barrier properties and cost-effectiveness. Success will also depend on companies' ability to manage raw material costs and maintain pricing flexibility while investing in sustainable solutions. Furthermore, manufacturers are increasingly focusing on developing specialized products for high-growth segments like pharmaceutical packaging and pet food, where barrier properties are crucial.

Europe Barrier Films Industry Leaders

Amcor PLC

Coveris Management Gmbh

Mondi PLC

Berry Global Group

Huhtamaki OYJ

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: Constantia announced that it had acquired the Clean organization Drukpol Flexo. Drukpol Flexo is a well-established player in the Clean, flexible packaging market. This acquisition further enhanced the Gathering's flexo printing capabilities following the acquisitions of Propak and FFP. In addition, it expands the Group's local customer base and increases its cost-competitiveness.

- March 2023: Toppan established a new facility in Most, Czech Republic. Toppan intends to begin mass production at its first European transparent barrier film manufacturing location by the end of 2024. With the opening of the new factory, Toppan will develop a market-leading and global supply capacity for transparent barrier films, with manufacturing bases in Japan, North America (Georgia, the United States), and Europe.

- April 2023: Gualapack Spa announced the acquisition of Print & Packaging Farma, which will help the company grow its portfolio of products and services for pharmaceutical and nutraceutical clients.

Europe Barrier Films Market Report Scope

The market studied defines the revenues generated from various vendors' sales of barrier film packaging. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the barrier film packaging market in terms of drivers and restraints.

The European barrier films market is segmented by packaging products (bags and pouches, stretch and shrink wrap films, tray lidding films, wrapping films and forming webs, and blister base films), by material (polyethylene, BOPET, polypropylene (CPP and BOPP), and polyvinyl chloride), by end-user industry (food and pet food, beverages, pharmaceutical and medical, and personal and home care), by country (United Kingdom, France, Germany, Italy, Spain, and the Rest of Europe). The market sizes and forecasts are provided in terms of value in USD for all the segments.

| Bags and Pouches |

| Stretch and Shrink Wrap Films |

| Tray Lidding Films |

| Wrapping Films and Forming Webs |

| Blister Base Films |

| Polyethylene |

| BOPET |

| Polypropylene (CPP and BOPP) |

| Polyvinyl Chloride |

| Other Material (EVOH, Polystyrene (PS), and Nylon) |

| Food and Pet Food |

| Beverages |

| Pharmaceutical and Medical |

| Personal and Home Care |

| Other End-user Industries |

| United Kingdom |

| France |

| Germany |

| Italy |

| Spain |

| Rest of Europe |

| By Packaging Product | Bags and Pouches |

| Stretch and Shrink Wrap Films | |

| Tray Lidding Films | |

| Wrapping Films and Forming Webs | |

| Blister Base Films | |

| By Material | Polyethylene |

| BOPET | |

| Polypropylene (CPP and BOPP) | |

| Polyvinyl Chloride | |

| Other Material (EVOH, Polystyrene (PS), and Nylon) | |

| By End user Industry | Food and Pet Food |

| Beverages | |

| Pharmaceutical and Medical | |

| Personal and Home Care | |

| Other End-user Industries | |

| By Country | United Kingdom |

| France | |

| Germany | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe Barrier Films Market?

The Europe Barrier Films Market size is worth USD 7.80 billion in 2025, growing at an 3.84% CAGR and is forecast to hit USD 9.42 billion by 2030.

What is the current Europe Barrier Films Market size?

In 2025, the Europe Barrier Films Market size is expected to reach USD 7.80 billion.

What years does this Europe Barrier Films Market cover, and what was the market size in 2024?

In 2024, the Europe Barrier Films Market size was estimated at USD 7.50 billion. The report covers the Europe Barrier Films Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Barrier Films Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: