Juice Concentrates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

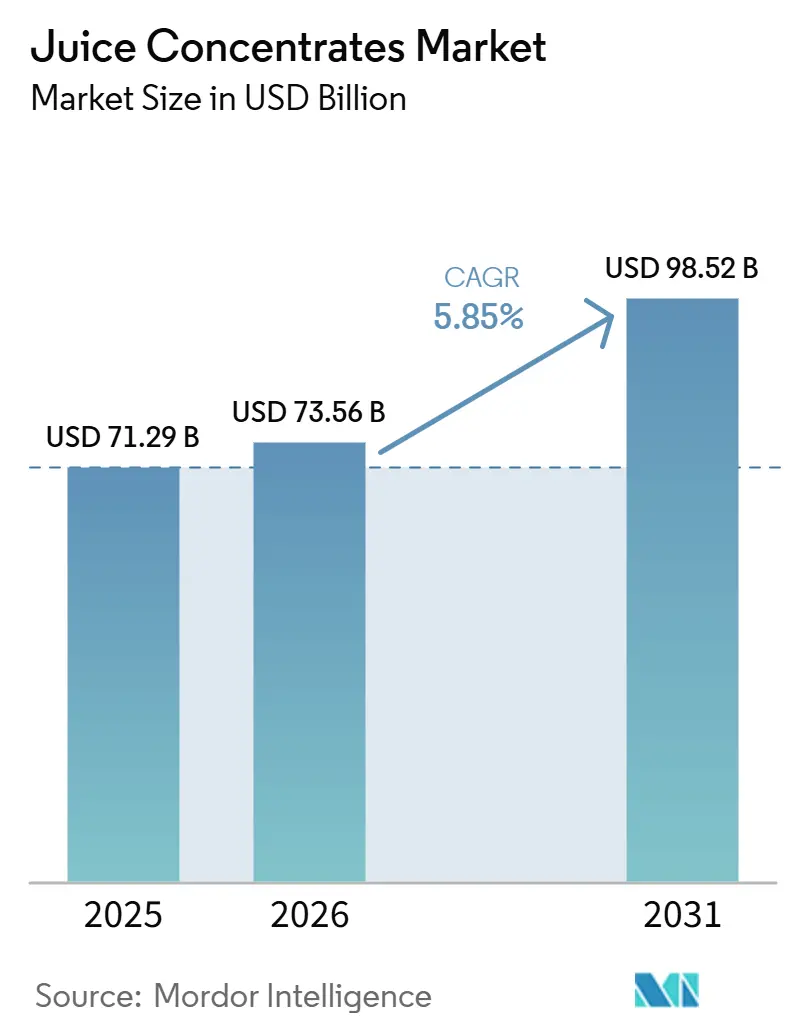

| Market Size (2026) | USD 73.56 Billion |

| Market Size (2031) | USD 98.52 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Juice Concentrates Market Analysis by Mordor Intelligence

The juice concentrates market size is projected to be USD 71.29 billion in 2025, USD 73.56 billion in 2026, and reach USD 98.52 billion by 2031, growing at a CAGR of 5.85% from 2026 to 2031. Concentrates have become the preferred building block for ready-to-drink beverages, bakery fillings, dairy mixes, and plant-based foods because they trim freight costs, extend shelf-life, and deliver consistent flavor. Europe continues to reward suppliers that certify organic and clean-label inputs, while Asia-Pacific’s urban middle class is adopting shelf-stable drinks at a rapid clip. Advances in membrane filtration and spray-drying are improving aroma retention and making lightweight powders viable for long-haul trade. At the same time, large beverage companies are collaborating with concentrate processors to reformulate products in line with sugar-reduction mandates and functional-nutrition trends.

Key Report Takeaways

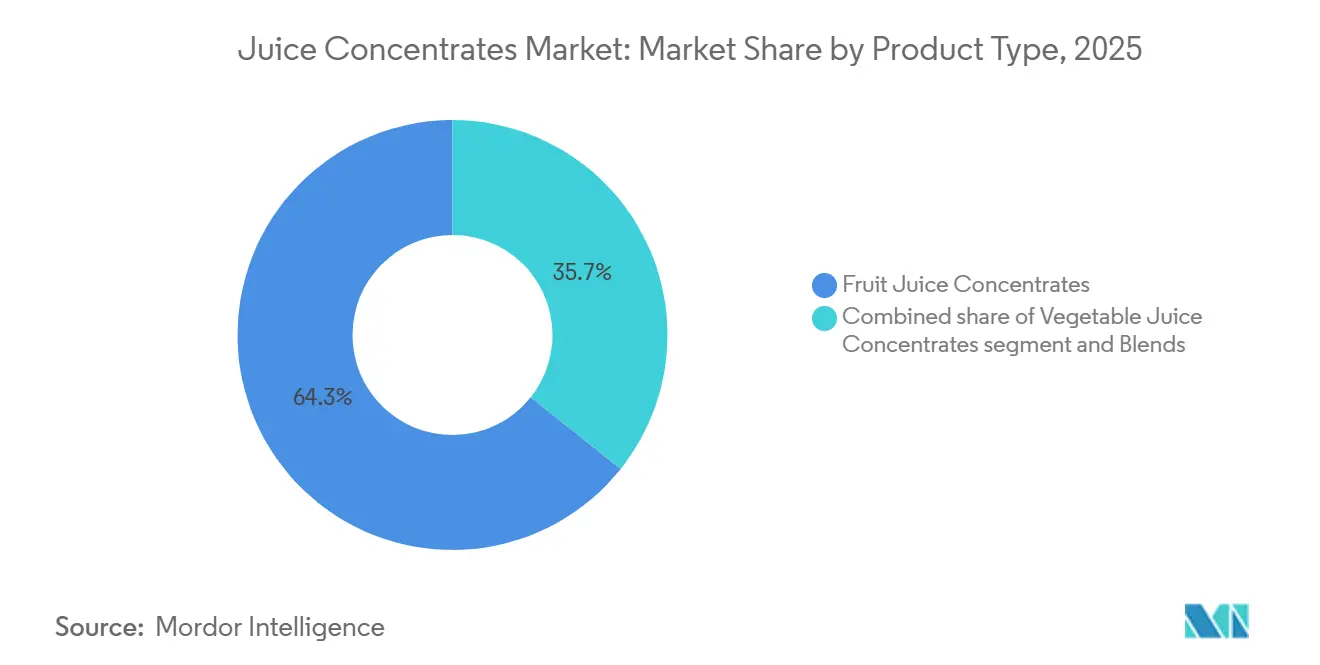

- By type, fruit concentrates led with 64.29% of the fruit and vegetable juice concentrates market share in 2025, while vegetable concentrates are expanding at a 6.65% CAGR through 2031.

- By form, liquid formats retained 71.23% revenue share in 2025; powders are projected to grow at a 7.16% CAGR to 2031.

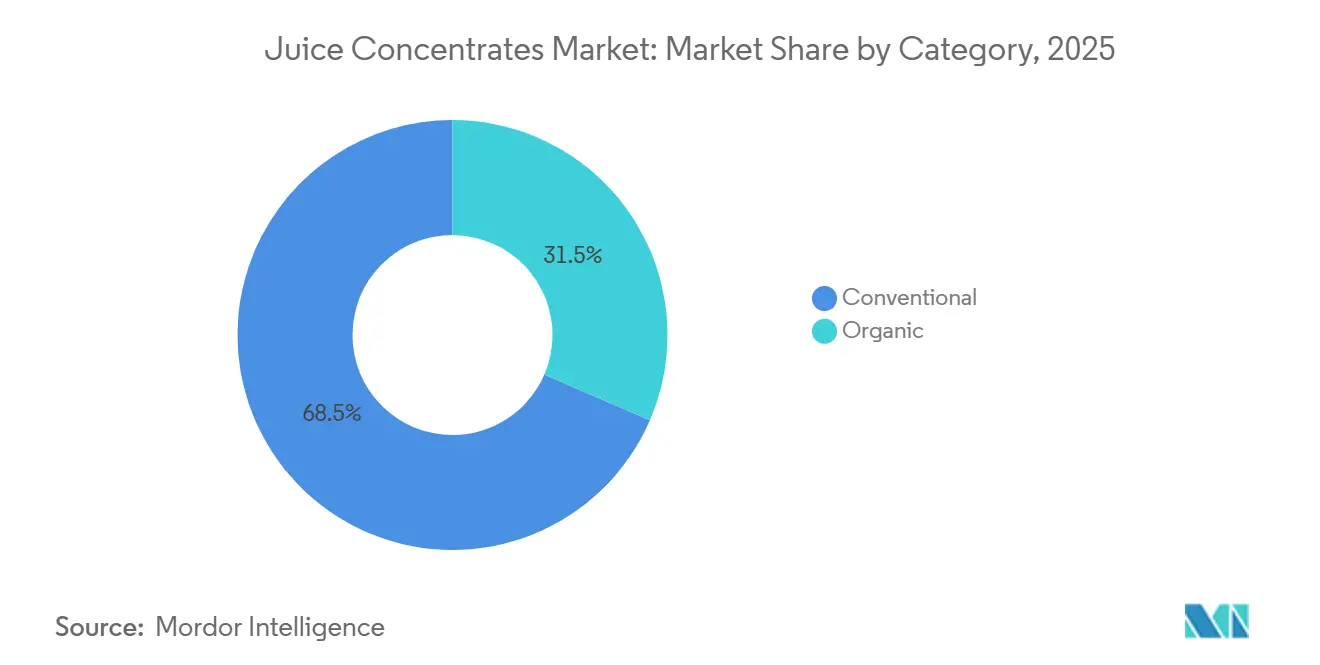

- By category, conventional products accounted for 68.52% of the fruit and vegetable juice concentrates market in 2025, and organic variants are set to grow at a 7.28% CAGR through 2031.

- By application, beverages commanded 32.15% volume in 2025, and bakery and confectionery are advancing at a 6.69% CAGR to 2031.

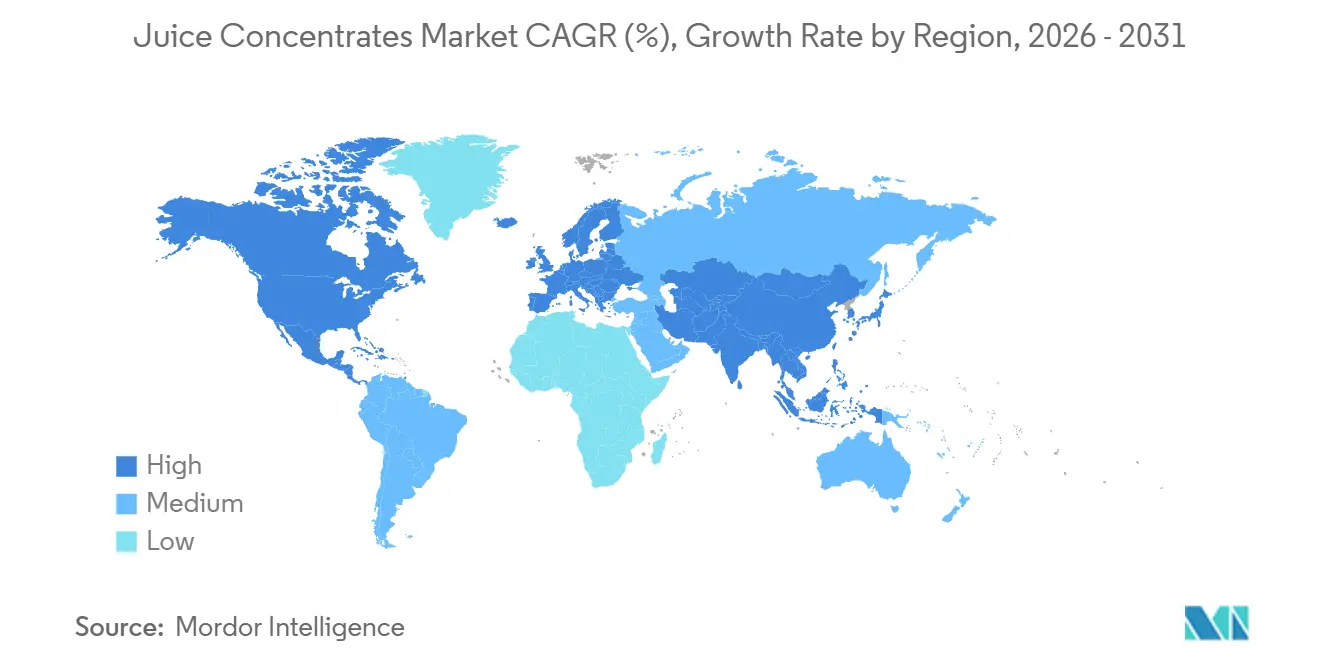

- By geography, Europe secured a 35.84% share in 2025, and Asia-Pacific will record the highest CAGR at 7.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Juice Concentrates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health and Wellness Awareness | +1.2% | Global, with premium segments in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing Demand for Convenience and Ready‑to‑Drink Beverages | +1.0% | Global, led by North America, Asia-Pacific urban centers, Middle East | Short term (≤ 2 years) |

| Expansion of Multi‑Fruit and Exotic‑Fruit Blends | +0.8% | Europe, North America, premium channels in Asia-Pacific | Medium term (2-4 years) |

| Favorable Trends in Natural and Minimally Processed Ingredients | +1.1% | North America, EU, Australia, urban Asia | Medium term (2-4 years) |

| Urbanization and Modern Retail Penetration | +0.9% | Asia-Pacific (China, India, Southeast Asia), Middle East, Latin America | Long term (≥ 4 years) |

| Technological Improvements in Concentration and Processing | +0.7% | Global, with early adoption in North America, EU, advanced Asia-Pacific facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Health and Wellness Awareness

Consumer demand for functional nutrition is driving changes in concentrate formulations, with a focus on blends that provide polyphenols, vitamins, and fiber along with sweetness. Wonder Juice, set to launch in March 2026, will offer organic, cold-pressed concentrates marketed as clean-label alternatives to synthetic vitamin fortification. These products are aimed at health-conscious millennials and Gen Z consumers who are willing to pay a premium for transparency. This trend is also influencing the foodservice sector, where operators are updating breakfast menus and smoothie bars with concentrates certified by USDA Organic or EU Organic standards to meet institutional wellness requirements. The shift is particularly evident in North America and Western Europe, where regulations such as the FDA's updated Nutrition Facts labeling (21 CFR 101) and the EU's Regulation 1169/2011 on food information require manufacturers to disclose added sugars[1]Source: Food and Drug Administration, “21 CFR Part 101 Nutrition Facts Label Final Rule,” fda.gov. This indirectly benefits concentrates with natural fruit sugars over those containing high-fructose corn syrup. Ingredient suppliers are responding by creating concentrates with higher Brix levels and reduced acidity, enabling beverage formulators to lower added sugar content while maintaining flavor. In the medium term, the impact reflects the time lag between product development and widespread consumer adoption, as brands reformulate their portfolios and educate retail buyers on the cost-benefit dynamics of premium concentrates.

Growing Demand for Convenience and Ready-to-Drink Beverages

Urbanization and limited time availability are driving the demand for single-serve, shelf-stable beverages. These beverages, which often use concentrates, provide consistent flavor and cost efficiency. Maison Perrier introduced passion fruit and blackberry RTD sparkling waters in early 2025. By utilizing fruit concentrates, they achieved natural color and taste without artificial additives, securing a position in the premium sparkling segment. In Q3 2025, Sun Cruiser launched low-sugar tropical blends, followed by Daily Dose's introduction of functional RTD shots in late 2025. Both brands incorporated concentrated fruit bases to ensure ambient shelf-life and reduce dependence on cold-chain logistics. These launches signify a significant shift: concentrate suppliers have transitioned from being simple ingredient providers to active partners. They now collaborate with beverage brands to develop sensory profiles, optimizing Brix, acidity, and mouthfeel for specific RTD formats. The short-term impact is evident in the rapid growth of SKUs in convenience retail and e-commerce. In 2025, shelf space for RTD beverages expanded considerably, a trend that continues into 2026. Urban centers in the Asia-Pacific, particularly tier-1 and tier-2 cities in China, along with the growing modern retail sector in the Middle East, are leading the absorption of increased RTD volumes. To meet this demand, concentrate suppliers are establishing regional blending facilities to support just-in-time manufacturing models.

Expansion of Multi-Fruit and Exotic-Fruit Blends

Beverage differentiation increasingly hinges on novel flavor combinations that combine familiar fruits with exotic varieties such as dragon fruit, yuzu, acai, and passionfruit. This trend is most visible in Europe and North America, where private-label and craft beverage brands use multi-fruit concentrates to command premium pricing and shelf differentiation. Wonder Juice's March 2026 launch featured blends of apple, beetroot, and ginger, targeting consumers seeking functional benefits beyond hydration. The commercial logic is compelling: exotic-fruit concentrates typically carry 20% to 40% higher per-kilogram pricing than apple or orange concentrates, yet their inclusion at 5% to 15% of total formulation delivers disproportionate sensory impact and label appeal. Concentrate suppliers are responding by securing long-term offtake agreements with growers in Southeast Asia, South America, and sub-Saharan Africa to stabilize exotic-fruit supply chains that historically suffered from seasonality and quality variability. The medium-term impact reflects the time required to scale exotic-fruit sourcing, establish quality standards, and educate beverage formulators on handling concentrates with unfamiliar pH, Brix, and enzymatic profiles.

Favorable Trends in Natural and Minimally Processed Ingredients

Non-thermal concentration methods that preserve volatile aromatics, anthocyanins, and vitamin C are becoming a priority for buyers, driving changes in concentrate processing. Cornell University's forward osmosis and membrane distillation technology, which concentrates juice without heat, is being tested by mid-sized processors aiming to enhance nutrient retention. Similarly, VeggieWonder's cold-grinding process for vegetable concentrates retains cell-wall integrity and produces cloudy, fiber-rich concentrates, appealing to developers of plant-based smoothies and baby food. These innovations underscore a key industry challenge: traditional thermal evaporation methods (falling-film and rising-film) provide high throughput at a low unit cost but degrade heat-sensitive compounds, whereas membrane technologies like reverse osmosis, ultrafiltration, and microfiltration preserve quality but demand higher capital and energy investments. Over the medium term, adoption is expected to progress gradually as processors assess return on investment. Early adopters in North America, the EU, and advanced Asia-Pacific facilities are leading the way by implementing hybrid systems that combine membrane pre-concentration with short-duration thermal finishing, achieving a balance between quality, cost, and throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating and Volatile Raw-Material Prices | -0.9% | Global, acute in Brazil, Florida, Mediterranean citrus belts | Short term (≤ 2 years) |

| Stringent Food-Safety and Labeling Regulations | -0.5% | North America (FDA), EU (EFSA), Asia-Pacific (FSSAI, China SAMR) | Medium term (2-4 years) |

| Seasonality and Crop-Related Risks | -0.7% | Brazil, Florida, Mediterranean, India, China fruit belts | Short term (≤ 2 years) |

| Rising Preference for Not-From-Concentrate (NFC) and Fresh Juice | -1.5% | Global, particularly Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating and Volatile Raw-Material Prices

Raw-material cost swings compress processor margins and destabilize long-term supply contracts. Brazil's industry-delivered pear orange prices fell 7.69% month-on-month to BRL 34.53 per 40.8-kg box in partial February 2026, while on-tree prices declined 2.87% to BRL 41.40, reflecting the tail end of the 2025/26 crushing season and reduced harvested volumes. Conversely, orange juice concentrate prices swung from record highs of USD 6,000 to USD 7,000 per ton in 2023/24 (driven by Brazilian supply shortfalls) to USD 2,800 to USD 3,500 per ton in 2025/26 as production partially recovered, yet prices remain historically elevated due to persistent Huanglongbing pressure and tight global stocks. This volatility forces beverage manufacturers to hedge via futures contracts or tolling arrangements, adding complexity and working capital requirements. Smaller processors without hedging capabilities face acute margin risk, particularly when multi-month supply contracts lock in fruit costs that subsequently fall, leaving them uncompetitive versus spot buyers. The short-term impact reflects the immediate pass-through of fruit-cost changes to concentrate pricing, with lag effects as annual contracts reset and buyers renegotiate terms.

Stringent Food-Safety and Labeling Regulations

Regulatory compliance costs are rising as authorities tighten standards for contaminants, traceability, and label claims. The FDA's 21 CFR Part 146 mandates specific compositional standards for fruit juices and concentrates, including minimum Brix levels, maximum acidity, and permitted ingredients, while Hazard Analysis and Critical Control Points protocols require documented controls at every processing stage. Codex Alimentarius General Standard for Food Additives (GSFA) sets global benchmarks for preservatives, antioxidants, and color additives in concentrates, with recent updates in 2025 tightening limits on sulfites and benzoates in organic-labeled products. Compliance requires investment in analytical laboratories, third-party audits, and supply-chain traceability systems, with costs disproportionately impacting mid-sized processors who lack the scale to amortize fixed compliance overhead. The medium-term impact reflects the lag between regulatory publication and enforcement, as processors upgrade facilities, retrain staff, and recertify products to meet new standards, with non-compliance risk concentrated in export-oriented producers serving multiple jurisdictions with divergent rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Vegetable Concentrates Gain Traction in Savory Applications

Fruit juice concentrates commanded 64.29% of market value in 2025, anchored by orange, apple, grape, and tropical blends that serve as the backbone for retail juice drinks, nectars, and foodservice beverage programs. Vegetable juice concentrates, though smaller in absolute volume, are forecast to grow at 6.65% CAGR through 2031, driven by reformulation in soups, sauces, baby food, and plant-based beverages where carrot, beetroot, spinach, and tomato concentrates deliver natural color, umami depth, and nutritional density without artificial additives. VeggieWonder's cold-grinding process preserves cell-wall integrity, yielding cloudy, fiber-rich concentrates that appeal to clean-label formulators. Blends, which combine fruit and vegetable concentrates, are capturing share in functional beverage and baby-food categories, where formulators seek to balance sweetness, acidity, and micronutrient profiles in a single ingredient system.

The faster growth of vegetable concentrates reflects a structural shift in how food manufacturers approach color and flavor. Synthetic dyes face increasing regulatory scrutiny under EU Regulation 1333/2008, and consumer backlash against artificial ingredients is prompting reformulation toward vegetable-derived alternatives[2]Source: European Commission, “Regulation (EU) No 1333/2008 on food additives,” europa.eu. Beetroot concentrate, for instance, delivers red hues for yogurt, ice cream and confectionery, while carrot concentrate provides orange tones for bakery glazes and dairy desserts. This substitution is particularly advanced in Europe, where clean-label penetration exceeds 40% in premium grocery channels, and in North America, where Whole Foods Market's quality standards effectively ban synthetic colors in private-label products. Tomato concentrate remains the largest vegetable segment by volume, serving as a base for pasta sauces, soups and ready meals, yet growth is decelerating as the category matures and competition from fresh-pack tomatoes intensifies in short-supply-chain models.

By Form: Powder Concentrates Expand in Export and Ambient Channels

Liquid concentrates held 71.23% of the market value in 2025, favored for their ease of reconstitution, lower processing complexity, and established supply chains that link fruit-growing regions to beverage manufacturing hubs. Powder concentrates, however, are forecast to grow at 7.16% CAGR through 2031, propelled by spray-drying and dehumidified-air drying innovations that reduce moisture content below 3%, extend shelf-life to 18 to 24 months, and cut transport costs by up to 70% versus liquid equivalents. Spray-drying techniques now incorporate carrier agents such as maltodextrin and gum arabic to prevent caking and preserve volatile aromatics, enabling production of free-flowing powders that reconstitute cleanly in cold water. This format is particularly attractive for export-oriented processors in South America, sub-Saharan Africa, and Southeast Asia, where ambient temperatures and limited cold-chain infrastructure favor powder over liquid concentrates that require refrigerated transport and storage.

Powder concentrates are also gaining traction in institutional foodservice and industrial bakery applications, where formulators value the extended shelf-life and dosing precision that powders afford. A bakery producing fruit-filled pastries, for example, can store powder concentrate at ambient temperature for 12 to 18 months and reconstitute batches on demand, reducing waste and working capital tied up in refrigerated inventory. Kerry Group's biotechnology investments, including enzyme systems that enhance natural sweetness and fermentation-derived taste modulators, are enabling powder concentrates with improved sensory profiles that compete with liquid concentrates in premium applications.

By Category: Organic Concentrates Command Premium Pricing Despite Scale Challenges

Conventional concentrates accounted for 68.52% of market value in 2025, benefiting from established supply chains, lower raw-material costs and broader availability across fruit varieties and geographies. Organic concentrates, though smaller in absolute volume, are forecast to grow at 7.28% CAGR through 2031, reflecting sustained premiumization in North America, Western Europe, and urban Asia-Pacific markets where consumers pay 20% to 50% price premiums for USDA Organic, EU Organic, or equivalent certifications. EU organic food and beverage sales reached approximately USD 62.7 billion in 2025, up from EUR 50 billion in 2024, with organic juice and nectar categories growing faster than the overall organic market[3]Source: USDA Foreign Agricultural Service, “Organic Foods and Beverages Annual,” usda.gov. This growth is concentrated in premium grocery chains, natural-food retailers, and e-commerce platforms where shoppers actively seek organic labels and are willing to absorb higher prices.

Organic concentrate supply, however, faces structural constraints. Organic fruit orchards require 3-year transition periods before certification, limiting the speed at which processors can scale organic sourcing. Yields are typically 10% to 30% lower than conventional orchards due to restrictions on synthetic pesticides and fertilizers, elevating per-kilogram fruit costs. Processors must also maintain segregated handling, storage, and processing lines to preserve organic integrity, adding capital and operational complexity. These factors explain why organic concentrates command 25% to 60% price premiums over conventional equivalents, yet the premium is narrowing in mature categories such as organic apple and orange concentrates as supply scales and competition intensify. Emerging organic categories, including exotic fruits and vegetable concentrates, retain wider premiums due to limited supply and niche demand. The medium-term growth outlook reflects the lag between organic orchard plantings and commercial harvest, with acreage expansions in 2024 and 2025 translating to incremental supply in 2027 and beyond.

By Application: Bakery and Confectionery Drive Fastest Growth

In 2025, beverages accounted for 32.15% of concentrate volume, making them the largest application. This includes retail juice drinks, nectars, functional beverages, low-alcohol and non-alcoholic alternatives, and foodservice beverage programs. Bakery and confectionery applications, though smaller in volume, are projected to grow at a 6.69% CAGR through 2031 as manufacturers replace synthetic colors and flavors with fruit and vegetable concentrates to meet clean-label demands. In the bakery, fruit concentrates add natural sweetness, acidity, and moisture retention, while vegetable concentrates like beetroot, carrot, and spinach provide color without artificial dyes. Europe leads this trend due to EU Regulation 1333/2008, which limits synthetic additives, followed by North America, where retailers like Whole Foods Market and Trader Joe's enforce private-label standards banning artificial colors and flavors.

In 2025, dairy and frozen foods utilized a significant share of concentrates. Yogurt, ice cream, and frozen dessert manufacturers used fruit concentrates for flavor, color, and texture while balancing cost and shelf-life. Soups and sauces, though smaller, are strategically important, with tomato, carrot, and beetroot concentrates forming bases for ready meals, pasta sauces, and ethnic dishes. Baby food is the fastest-growing sub-segment, driven by demand for organic, minimally processed ingredients and regulations to reduce added sugars. Carrot, sweet potato, and spinach concentrates are increasingly used in baby food as manufacturers reformulate purees to boost micronutrient density for health-conscious parents. The "Others" category, including nutraceuticals, dietary supplements, and pharmaceuticals, is expanding as suppliers develop high-Brix, low-moisture formats for encapsulation and tablet formulations, offering concentrated fruit and vegetable nutrition in convenient forms.

Geography Analysis

In 2025, Europe held 35.84% of the market value, driven by high per-capita consumption of organic juice blends, clean-label regulations, and a mature retail infrastructure supporting premium pricing. Germany, the UK, France, Italy, and Spain dominated demand, with Germany excelling in organic certification and the UK innovating in low-sugar and functional beverages. The Netherlands, leveraging Rotterdam's port, served as a hub for importing tropical fruit concentrates for re-export across Europe. Sweden and Poland emerged as growth markets due to rising modern retail penetration and consumer preference for natural ingredients. Belgium's confectionery industry fueled demand for fruit concentrates, while Europe's growth remained moderate due to population stagnation and economic challenges.

Asia-Pacific is forecast to grow at a 7.41% CAGR through 2031, driven by urbanization, rising incomes, and modern retail expansion in China, India, Japan, Australia, South Korea, Vietnam, and Indonesia. China embraced innovations in functional and low-sugar beverages, while India's organized retail expanded into smaller cities, boosting demand for juice drinks with mango and guava concentrates. Japan's market focused on premium and functional products, while Australia's clean-label regulations spurred demand for organic concentrates. South Korea's café culture and Vietnam and Indonesia's youthful populations and cold-chain infrastructure supported growth in shelf-stable beverages and processed foods.

North America, led by the U.S., Canada, and Mexico, absorbed significant concentrate volumes in 2025, driven by large-scale beverage manufacturing and export-oriented processing. The U.S. remained the largest market, with stringent FDA regulations and HACCP protocols ensuring quality. Canada faced compliance complexities due to bilingual labeling, while Mexico leveraged USMCA trade terms and lower labor costs to serve North American brands. South America, led by Brazil, Argentina, and Chile, supplied orange and tropical fruit concentrates globally, with Brazil exporting 80% of its production. The Middle East and Africa, including the UAE, Saudi Arabia, and South Africa, saw rapid growth due to urbanization, youth demographics, and modern retail expansion, with multinational suppliers investing in localized production to meet regional demand.

Competitive Landscape

The fruit and vegetable juice concentrates market is moderately fragmented, with a concentration index of 4, signifying that no single player dominates the market. Multinational ingredient leaders such as Archer Daniels Midland Company, Kerry Group, Ingredion Incorporated, Dohler Group, and Symrise AG compete alongside regional processors, vertically integrated citrus cooperatives, and toll manufacturers. These entities cater to niche applications or specific geographic regions. Strategic trends indicate a distinct split: larger players are investing in biotechnology, fermentation-derived taste systems, and membrane concentration technologies to enhance quality and functionality. Meanwhile, mid-sized processors prioritize cost-efficiency, proximity to raw material sources, and flexible tolling arrangements, enabling beverage brands to outsource concentrate production without significant capital investment.

Emerging opportunities include vegetable concentrates for savory applications, organic exotic-fruit blends, and powdered formats designed for export and ambient distribution. Specialty processors are disrupting the market by employing non-thermal concentration methods, such as forward osmosis and membrane distillation, to retain volatile aromatics and nutritional compounds. These methods allow them to secure premium pricing in organic and high-end segments, where buyers value sensory fidelity and clean-label attributes. Technology is increasingly becoming a critical competitive advantage. Kerry Group's fermentation-derived Tastesense™ technologies enable beverage formulators to reduce sugar content by 20% to 40% without compromising taste. Additionally, the company's enzyme systems deliver enhanced natural sweetness from fruit substrates.

In 2024, Dohler Group's acquisition of Premier Juices and the expansion of its Cartersville, Georgia plant highlight a strategy focused on vertical integration. This approach aims to serve North American beverage brands with shorter lead times and customized formulations. Refresco's planned USD 1.1 billion acquisition of SunOpta, expected to close in Q2 2026, reflects ongoing consolidation in the beverage co-packing and private-label sector. In this context, concentrate sourcing and formulation capabilities are becoming strategic assets that support integrated service offerings. For concentrate suppliers serving multinational beverage brands and retail private-label programs, compliance with ISO 22000 (food safety management) and FSSC 22000 (Food Safety System Certification) is now a baseline requirement. However, the fixed costs associated with third-party audits and traceability systems tend to benefit larger, well-capitalized players.

Juice Concentrates Industry Leaders

Archer Daniels Midland (ADM)

AGRANA Beteiligungs-AG

Döhler Group

Kerry Group

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Archer Daniels Midland Company announced a USD 26 million investment in its Erlanger, Kentucky facility to expand flavors and colors capacity, including natural color systems derived from fruit and vegetable concentrates.

- May 2024: Döhler expanded its South African plant in Paarl with new production lines for compounds, emulsions, and flavors in both powdered and liquid forms. The expansion increases the facility's bulk juice concentrate processing capacity, establishing it as a manufacturing hub. This enhancement provides regional customers direct access to Döhler's complete compound portfolio, supporting the food, beverage, and life science and nutrition industries across Southern Africa.

- April 2024: Symrise introduced a prune juice concentrate from its diana food™ portfolio with a minimum sorbitol guarantee at Vitafoods. The Guangdong Provincial Hospital of Traditional Chinese Medicine and the Guangdong University of Technology conducted a clinical trial with Symrise to study the health benefits of this concentrate, involving 38 volunteers with functional constipation.

Global Juice Concentrates Market Report Scope

| Fruit Juice Concentrates |

| vegetable juice Concentrates |

| Blends |

| Liquid |

| Powder |

| Organic |

| Conventional |

| Beverages |

| Bakery and Confectionery |

| Dairy and Frozen Foods |

| Soups and Sauces |

| Baby Food |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Fruit Juice Concentrates | |

| vegetable juice Concentrates | ||

| Blends | ||

| By Form | Liquid | |

| Powder | ||

| By Category | Organic | |

| Conventional | ||

| By Application | Beverages | |

| Bakery and Confectionery | ||

| Dairy and Frozen Foods | ||

| Soups and Sauces | ||

| Baby Food | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global concentrate demand become by 2031?

The fruit and vegetable juice concentrates market size is forecast to reach USD 98.52 billion by 2031 at a 5.85% CAGR.

Which segment is growing the fastest?

Powder concentrates are projected to expand at a 7.16% CAGR, helped by spray-drying investments that cut freight weight and extend shelf-life.

Why are vegetable concentrates gaining share?

Carrot, beet, and spinach concentrates replace synthetic colors and add nutrients to soups, sauces, and baby foods, driving a 6.65% CAGR.

Which region shows the strongest growth outlook?

Asia-Pacific is set to rise at a 7.41% CAGR through 2031 thanks to urbanization and modern retail expansion.

Page last updated on: