GCC Juice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

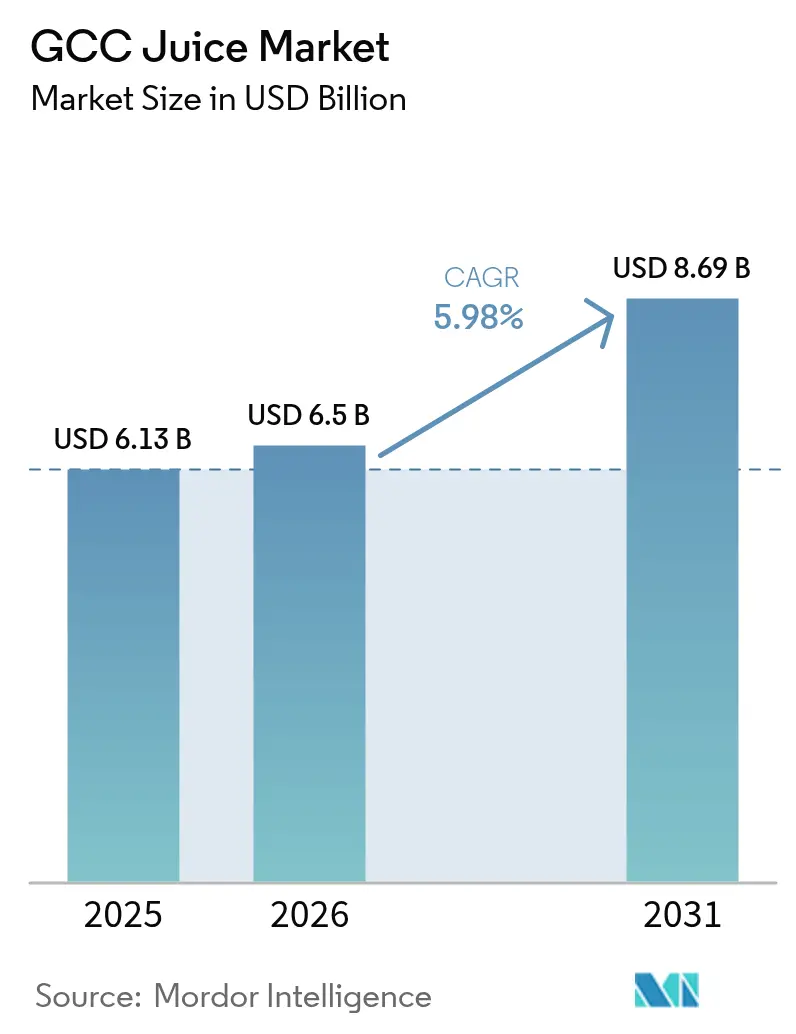

| Base Year Market Size (2025) | USD 6.13 Billion |

| Market Size (2026) | USD 6.5 Billion |

| Market Size (2031) | USD 8.69 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

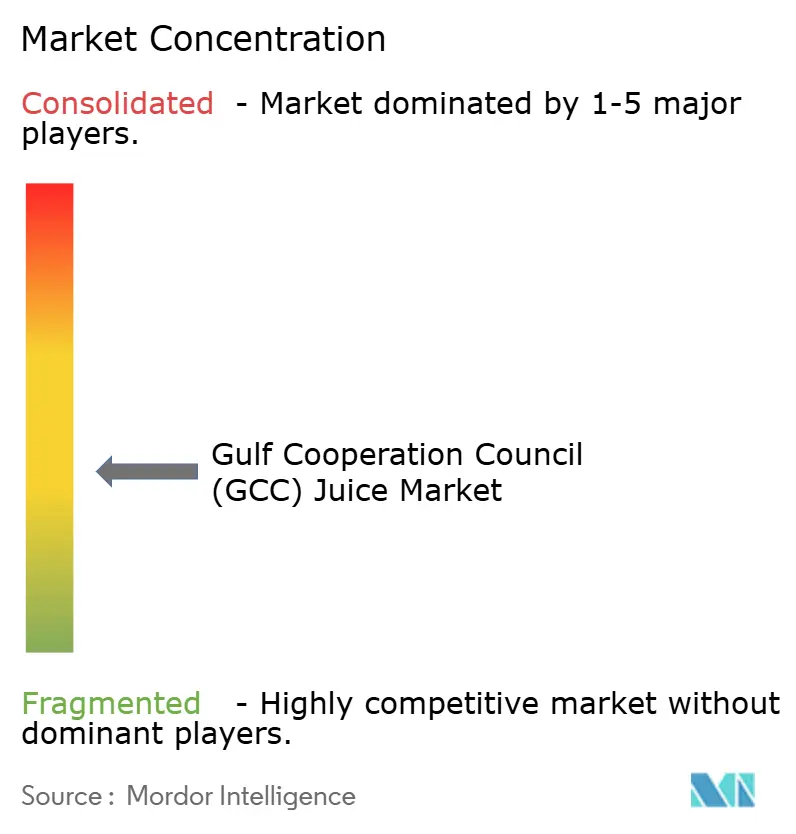

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Juice Market Analysis by Mordor Intelligence

The Gulf Cooperation Council (GCC) juice market size in 2026 is estimated at USD 6.5 billion, growing from 2025 value of USD 6.13 billion with 2031 projections showing USD 8.69 billion, growing at 5.98% CAGR over 2026-2031. This growth is primarily driven by the rising demand for premium juices and functional beverages and the increasing popularity of fortified and natural juices. Saudi Arabia remains the largest market in the region, while the United Arab Emirates is experiencing the fastest growth. The introduction of sugar excise taxes has led manufacturers to reformulate their products. Many companies are now focusing on launching functional, fortified, and natural juice options, particularly in urban retail stores and on-trade outlets. Regulatory measures, such as the 50% excise tax on sugar-sweetened beverages, are pushing manufacturers to expand their non-sugar product portfolios and invest in improving cold chain infrastructure to address the challenges posed by the region's hot climate. The Gulf Cooperation Council juice market is moderately concentrated, but there are signs of increasing competition. In 2024, major players like Almarai and Al Rabie Saudi Foods, along with other diversified beverage companies, continued to hold a significant share of the market.

Key Report Takeaways

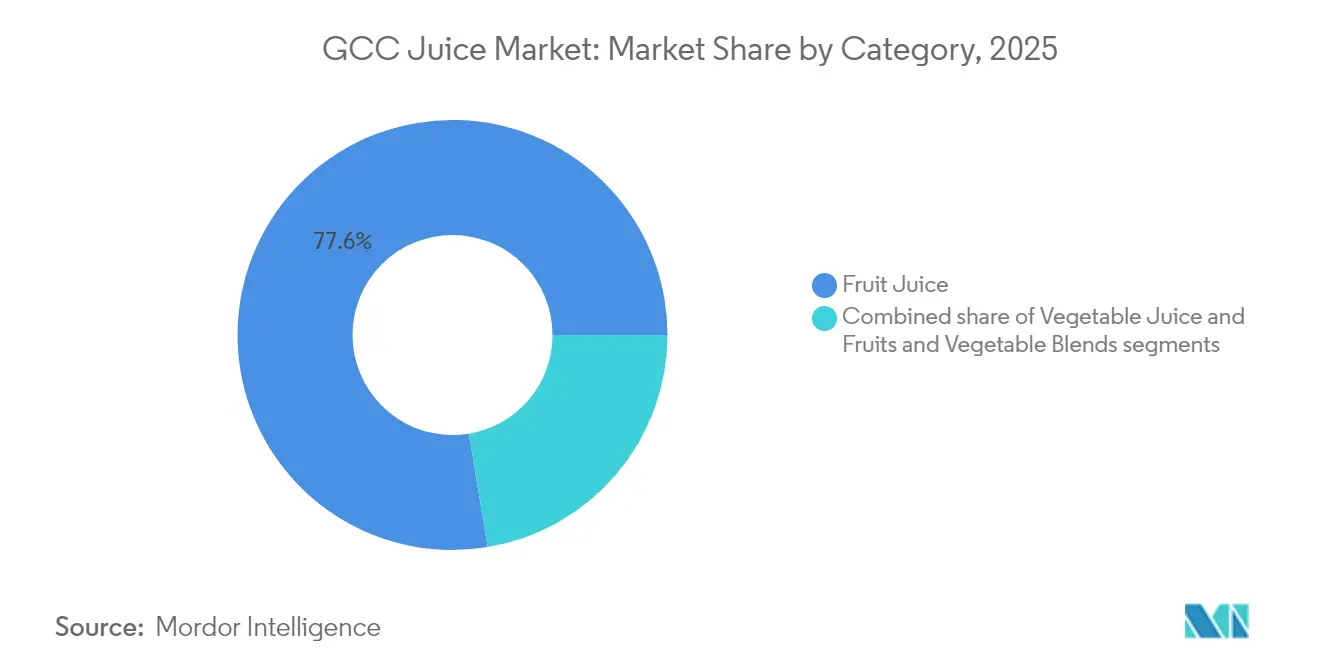

- By product category, fruit juice accounted for 77.62% revenue share in 2025; vegetable juice is projected to rise at a 7.31% CAGR to 2031.

- By type, 100% juice held 51.55% of the Gulf Cooperation Council (GCC) juice market share in 2025, while nectar is projected to grow at a 7.52% CAGR through 2031.

- By packaging, Tetra Pak cartons controlled 54.88% of the Gulf Cooperation Council (GCC) juice market size in 2025; PET bottles are poised for a 6.05% CAGR over 2026-2031.

- By distribution channel, off-trade captured 84.63% of the Gulf Cooperation Council (GCC) juice market share in 2025, yet on-trade is expanding at a 7.12% CAGR between 2026-2031.

- By geography, Saudi Arabia dominated with a 49.15% share in 2025, while the United Arab Emirates is forecast to post the highest 7.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Juice Market Trends and Insights

Drivers Impact Table*

| DRIVERS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Premiumization and demand for functional juices | +1.2 | United Arab Emirates , Saudi Arabia, Qatar | Medium term (2-4 years) |

| Increasing popularity of fortified and functional juices | +0.9 | United Arab Emirates, Saudi Arabia | Medium term (2-4 years) |

| Growing Demand for natural and organic juices | +0.8 | United Arab Emirates, Saudi Arabia, Kuwait | Long term (≥ 4 years) |

| Rising preference for convenient, ready-to-drink (RTD) formats | +0.7 | Saudi Arabia, United Arab Emirates, Oman | Short term (≤ 2 years) |

| Tourism and the HoReCa sector growth | +0.6 | United Arab Emirates, Qatar, Saudi Arabia | Medium term (2-4 years) |

| Health and wellness trends | +0.5 | All Gulf Cooperation Council (GCC) countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing popularity of fortified and functional juices

Urban consumers in cities like Dubai, Abu Dhabi, and Riyadh are increasingly viewing juice as more than just a refreshing drink; it is now seen as a functional wellness product. According to the United Nations Development Programme (UNDP), the urban population in the Gulf Cooperation Council (GCC) region is steadily growing and is expected to reach 54.6 million by 2030 [1]Source: United Nations Development Programme, "Urbanization: regional trends," undp.org. This growing urbanization is driving demand for healthier and more functional beverages. In 2024, there was a noticeable rise in interest in fortified juices enriched with nutrients like vitamin C, zinc, probiotics, and omega-3s, which performed exceptionally well across the region. For instance, Almarai introduced its “Super Juice” range, which includes 100% not-from-concentrate pomegranate and berry juices. These juices are processed using ultra-heat treatment to retain nutrients and are packaged in premium, shelf-stable containers. The company also reported significant growth in its “Better for You” product portfolio during the year.

Tourism and HoReCa sector growth

The tourism and hospitality sector in the Gulf Cooperation Council (GCC) is growing rapidly, creating new opportunities for juice products, especially in the United Arab Emirates and Qatar, where significant investments are being made in tourism infrastructure. For example, Dubai welcomed 8.68 million overnight visitors between January and May 2025, marking a 7% increase compared to the same period in 2024, according to the Dubai Department of Economy and Tourism [2]Source: Dubai Department of Economy and Tourism, "Recipe for success: growth of Dubai’s gastronomy industry in 2024,"dubaidet.gov.ae. The Dubai Gastronomy Industry Report, published in April 2025, highlighted that nearly 1,200 new restaurant licenses were issued in the city, showcasing the sector's remarkable growth [3]Source: Dubai Department of Economy and Tourism, “Dubai Gastronomy Industry Report 2024,” Dubai Gastronomy Industry Report,det.gov.ae . This expansion is driving demand for high-quality juice products that cater to the hospitality industry's focus on premium experiences. Juice manufacturers are responding by creating specialized products and packaging formats designed for food service needs. For example, Barakat Quality Plus in the United Arab Emirates offers freshly squeezed juices in 2-liter and 5-liter foodservice packs specifically tailored for hotels, restaurants, and catering outlets.

Rising preference for convenient, ready-to-drink (RTD) formats

The rapid urbanization and increasingly busy lifestyles in Saudi Arabia and the United Arab Emirates are driving a growing preference for convenient, ready-to-drink (RTD) juice options. These products cater to consumers who are constantly on the move and looking for quick, hassle-free refreshment. According to the International Labour Organization, the United Arab Emirates' employment rate is projected to reach approximately 76.42% in 2024, with a labor force of around 7,076,637 people [4]Source: International Labour Organization, "Country Portal, United Arab Emirates," ilo.org. This highlights the growing number of working individuals who often seek convenient food and beverage solutions. To meet this demand, juice manufacturers are focusing on creating portable and easy-to-use products. For example, in 2024, Almarai launched a 180 ml single-serve juice pack designed for commuters, office workers, and students who need a quick and nutritious drink during their busy schedules, along with better value for money. This shift reflects a broader trend where consumers value both functionality and convenience.

Health and wellness trends

The growing focus on health and wellness in the Gulf Cooperation Council (GCC) region is significantly influencing the juice market, as consumers increasingly look for beverages that offer clear health benefits. This trend is evident across all age groups and income levels, driven by a rising awareness of nutrition and the need to prevent chronic diseases. People are paying closer attention to juice labels, seeking information about vitamin content, antioxidants, and the absence of added sugars or artificial ingredients. To support this shift, regional health authorities have introduced initiatives aimed at reducing sugar consumption and promoting healthier eating habits. For instance, Saudi Arabia’s Ministry of Health actively promotes the Saudi Sugar Reduction Strategy, which aligns with global efforts like the FDI World Dental Federation's Declaration on Sugar [5]Source: Dubai Department of Economy and Tourism, "Tourism Performance Report January - May 2025,"dubaidet.gov.ae. These initiatives encourage manufacturers to create beverages with lower sugar content. In this environment, juice brands that focus on health and wellness, supported by clean labels, certifications, and transparent nutrient information, are gaining a competitive edge and building stronger connections with health-conscious consumers in the Gulf Cooperation Council (GCC).

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High sugar taxes and regulatory challenges | -0.9 | Saudi Arabia, United Arab Emirates, All Gulf Cooperation Council | Short term (≤ 2 years) |

| Increasing prevalence of overweight and obesity among children and adults | -0.7 | Saudi Arabia, United Arab Emirates, Kuwait | Long term(≥ 4 years) |

| Short shelf life of fresh and cold-pressed juices | -0.4 | United Arab Emirates, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Packaging waste and environmental concerns | -0.3 | United Arab Emirates, Saudi Arabia | Long term(≥ 4 years) |

| Source: Mordor Intelligence | |||

High sugar taxes and regulatory challenges

The introduction of high excise taxes on sugar-sweetened beverages in Gulf Cooperation Council (GCC) countries has created significant challenges for juice manufacturers. Both Saudi Arabia and the United Arab Emirates have implemented a 50% excise tax on drinks with added sugars, which includes many juice products. This tax has directly increased retail prices, leading to changes in consumer buying habits. For instance, in Saudi Arabia, soft drink consumption dropped by 19% after the tax was introduced, as reported by a study conducted by Jallouna and Qurban. To adapt, some companies have focused on developing juices with reduced sugar or no added sugar, leveraging their research and development capabilities. However, smaller manufacturers or those with limited resources are struggling with the high costs and complexities of reformulating their products. The World Health Organization (WHO) has highlighted that these tax rates are among the highest in the world, making the Gulf Cooperation Council (GCC) a particularly challenging region for juice producers.

Increasing prevalence of overweight and obesity among children and adults

The increasing rates of overweight and obesity among both children and adults in the Gulf Cooperation Council (GCC) region are putting fruit juice products, especially those with high natural or added sugar content, under more scrutiny from both regulators and consumers. In Saudi Arabia and the United Arab Emirates (UAE), obesity is a growing public health issue. A survey conducted by PMC NCBI NLM on 522 adolescents (aged 11–18) found that, as of January 2025, 13.2% were overweight and 26.1% were obese in Saudi Arabia. This is partly due to government efforts to reduce sugar consumption, including in beverages. While 100% fruit juices provide important nutrients, their natural sugars are being reconsidered by health-conscious consumers. Public health campaigns, like the Saudi Arabia Declaration on Sugar, supported by the Saudi Dental Society and the FDI World Dental Federation, have highlighted sugar-sweetened drinks as contributors to obesity and dental problems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Fruit Maintains Leadership while Vegetables Accelerate

In 2025, the Gulf Cooperation Council (GCC) juice market saw fruit juice dominate, claiming a substantial 77.62% of total revenue. This stronghold can be attributed to consumers' familiarity with the product, a diverse range of flavors, and its prominent presence in both traditional and modern retail formats. Mainstream retailers are actively promoting popular flavors, notably mango and orange, often through multipack deals aimed at family consumption. Leading brands, including Al Rabie and Del Monte, boast extensive portfolios tailored to both value-conscious and brand-loyal consumers. The category's robustness is further enhanced by its adaptability to ambient and long-life packaging formats, which not only ensure cost-efficient storage but also facilitate broad regional distribution.

While vegetable juice currently occupies a smaller niche, it's poised for rapid growth, outpacing its fruit counterpart with a projected CAGR of 7.31%. This momentum is driven by a burgeoning demand for low-sugar and nutrient-rich options, particularly among health-conscious consumers. Responding to this trend, companies like Almarai are introducing blended products, such as beet-carrot juice, prominently showcased in premium outlets and wellness sections. These blends, perceived for their functional benefits like enhanced digestion and antioxidant properties, command a premium price. As retailers allocate more refrigerated shelf space, suppliers who effectively highlight the nutritional advantages and vitamin retention of their vegetable juices stand to gain significantly in this expanding market.

By Type: Nectar Outpaces Conventional Variants

In 2025, the 100% juice category captured 51.55% of the Gulf Cooperation Council (GCC) juice market share, bolstered by its strong reputation as a natural and healthy choice. As consumers increasingly opt for juices devoid of added sugars and artificial ingredients, this segment has surged in popularity across both mainstream and premium retail channels. For example, Almarai’s 100% juice range boasts robust sales in supermarkets throughout Saudi Arabia and the United Arab Emirates, underscoring the trust consumers place in established regional brands. This trend underscores a wider movement towards clean-label, minimally processed beverages, resonating with today's wellness-oriented consumption habits.

Meanwhile, the nectar segment is rapidly gaining traction within the GCC juice market, projected to achieve a strong CAGR of 7.52% starting in 2026. This growth is primarily driven by increasing consumer health awareness and continuous product innovation. Key players, such as Al Rawabi, are introducing cocktail nectar blends featuring tropical flavors like pineapple, mango, and orange, which cater to urban consumers seeking fruit-based refreshment. With its moderate fruit content, nectar is strategically positioned between juice drinks and pure juice, offering a flavorful and convenient option for daily consumption. The demand is particularly robust for premium, organic, and blended nectar formats, distributed through established supermarket chains and expanding online retail platforms.

By Packaging Type: Cartons Retain Scale as PET Rises

In 2025, cartons captured 54.88% of the market share, largely due to their affordability, ease of storage, and extended shelf life at room temperature. These attributes have made cartons the go-to choice for manufacturers and consumers alike in the Gulf Cooperation Council (GCC). Furthermore, the rising adoption of bio-based materials in carton production enhances their eco-friendliness, resonating with the region's sustainability objectives. For instance, in response to the surging demand for eco-friendly packaging, Al Rawabi has rolled out recyclable cartons for its juice lineup. Additionally, in a bid to bolster national sustainability initiatives like Vision 2030, juice producers are teaming up with local municipalities to elevate recycling rates for carton packaging.

PET bottles are witnessing a robust growth trajectory, expanding at a CAGR of 6.05%. Their transparent design, which showcases the product, coupled with a resealable feature, caters perfectly to today's fast-paced lifestyles. The industry is also pivoting towards innovations such as recycled PET (rPET) and tethered caps, ensuring compliance with stringent environmental regulations. Meanwhile, glass packaging, though holding a modest share in the premium segment, is strategically favored by cold-pressed juice brands to exude an aura of quality and luxury. Cans find their niche appeal in sectors like airlines and convenience stores, prized for their compactness and portability. Collectively, these varied packaging formats not only enhance functional convenience but also bolster brand positioning across diverse consumer demographics.

By Distribution Channel: On-Trade Adds Velocity to a Mature Off-Trade Base

In 2025, off-trade channels, such as supermarkets, hypermarkets, and e-commerce platforms, accounted for 84.63% of total juice revenue, buoyed by robust consumer footfall and a diverse range of juice offerings. Quick-commerce apps, including Talabat and Instashop, have spurred off-trade growth in cities like Dubai and Riyadh, delivering orders in under 20 minutes and fueling impulse buys of single-serve juices. Retailers are enhancing shelf placements and bundling strategies to spotlight value packs, while e-commerce platforms utilize search-based targeting to amplify juice promotions. The extensive accessibility and variety in off-trade venues solidify their status as the go-to channel for both daily and bulk juice purchases.

On-trade channels, encompassing hotels and cafés, are rapidly gaining traction, boasting a projected CAGR of 7.12%. Urban centers like Dubai, Doha, and Riyadh are witnessing beverage menu upgrades, with establishments introducing cold-pressed juices and immunity-boosting blends to cater to the premium wellness market. In a nod to the growing emphasis on health and personalization, juice brands are partnering with café chains to craft exclusive ready-to-drink (RTD) flavors. Convenience stores situated at transport hubs and petrol stations are seeing a surge in single-serve juice sales, driven by consumer demand for portability. To capitalize on this trend, manufacturers are rolling out durable, easy-to-carry packaging and introducing limited-time offers and cross-promotions, aiming to boost impulse purchases and trials in urban and travel-centric locales.

Geography Analysis

Saudi Arabia accounted for 49.15% of the juice market volume in 2025, driven by its strong domestic supply chain and widespread modern trade networks. The country's Vision 2030 health initiatives are pushing manufacturers to reduce sugar content in their products. For instance, Almarai’s “Better for You” product line has seen significant growth due to this shift. Retailers in Saudi Arabia continue to prioritize popular 1-liter mango and orange juice products, while also gradually introducing more functional and health-focused juice options to meet changing consumer preferences.

The United Arab Emirates is expected to grow at a CAGR of 7.46%, fueled by its large tourist population, diverse consumer tastes, and advanced logistics infrastructure. Airports and luxury hotels in the United Arab Emirates often test exclusive juice concepts, which, if successful, are later introduced to retail stores. This trend allows the United Arab Emirates to play a key role in shaping regional flavor preferences and driving innovation in the juice market.

Qatar, Kuwait, and Oman collectively contribute a smaller but strategically important share to the Gulf Cooperation Council (GCC) juice market. Qatar benefits from the high purchasing power of its expatriate population, which supports the demand for premium chilled juice products. Kuwait has seen a rise in demand for vitamin-enriched juices targeted at children, reflecting a focus on health and nutrition. Meanwhile, Oman is transitioning from economy cartons to mid-tier PET packaging, supported by the modernization of its supermarket infrastructure. The implementation of consistent sugar-tax policies across all Gulf Cooperation Council (GCC) countries is encouraging manufacturers to adopt uniform labeling and reformulate their products to meet regional standards.

Competitive Landscape

The Gulf Cooperation Council (GCC) juice market is moderately fragmented but is gradually becoming more fragmented. Major players include Almarai, Al Rabie, and other niche brands are gaining traction in premium chilled sections and e-commerce platforms, reducing the market share of the top players. This shift indicates a growing preference for diverse and specialized juice offerings among consumers, leading to increased competition in the market.

Strategic collaborations are becoming a key trend in the competitive landscape. For instance, iPRO’s partnership with Al Rabie in 2025 combines local production capabilities with expertise in functional beverages. Similarly, Almarai’s USD 4.8 billion investment plan over five years focuses on advanced processing technologies and innovative packaging to maintain its position in premium segments. On the other hand, smaller cold-pressed juice brands are leveraging unique selling points like limited-batch production, authenticity through QR codes, and direct-to-consumer sales channels. These strategies help them compete effectively despite their smaller scale.

Technology and sustainability are emerging as critical factors in the market. Gulf Union, for example, uses QR codes on packaging to promote recycling and offer personalized deals, ensuring customer engagement even with lower sales volumes. Larger companies are adopting AI-driven tools for demand forecasting to minimize waste from short-shelf-life products. As regulations around digital traceability and eco-friendly practices become stricter, both large corporations and smaller brands are focusing on proving their sustainability credentials.

GCC Juice Industry Leaders

-

Almarai Company

-

The Coco Cola Company

-

Al Rabie Saudi Foods Co

-

Del Monte Pacific Limited

-

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tetra Pak started a major project with Al Rabie, a top Saudi company in juices, nectar, still drinks (JNSD), and dairy products packaged in cartons, after signing an agreement in November 2024. This three-year deal aims to fully upgrade and digitize Al Rabie’s production facilities in Saudi Arabia.

- February 2025: iPRO Hydrate entered the Saudi Arabian market through a partnership with juice manufacturer Al Rabie. The beverage is available in four flavors: berry mix, citrus blend, mango, and orange and pineapple. While the product will be imported from the UK, it will be co-branded with Al Rabie.

- January 2025: Almarai acquired the Pure Beverages industry for USD 280 million. This acquisition supports Almarai's growth strategy by expanding its beverage portfolio and improving its offerings for consumers.

- June 2024: Boost Juice, the Australian juice and smoothie brand, is expanding its UAE operations with three new locations in Abu Dhabi and Dubai. This expansion follows the successful establishment of three stores in Sharjah through its partnership with Arada, the master franchise agreement (MFA) holder.

GCC Juice Market Report Scope

As per the scope of the report, juice is a beverage created by pressing or extracting the natural liquid in fruits and vegetables. GCC Juice Market is segmented by category, type, packaging type, distribution channel, and geography. Based on category, the market is segmented into fruit juice, vegetable juice and fruit & vegetable blends; by type, the market is segmented into 100% juie, juice drinks (25-99% juice content), concentrates, cold-pressed juice and nectar; by packaging type into tetra pak cartons, PET bottles, glass bottles, cans and others; by distribution channel into on-trade and off-trade; off-trade is further segmented into supermarkets and hypermarkets, convenience/grocery stores, online channels, and other distribution channels (kiosks, vending, specialty stores, warehouse clubs, etc). By Geography, the market is studied for Saudi Arabia, the United Arab Emirates, Qatar, Kuwait and Oman. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Fruit Juice |

| Vegetable Juice |

| Fruit and Vegetable Blends |

| 100% Juice |

| Juice Drinks (25–99% juice content) |

| Nectar |

| Tetra Pak Cartons |

| PET Bottles |

| Glass Bottles |

| Cans |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retailers | |

| Other Off-Trade Channel |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| By Category | Fruit Juice | |

| Vegetable Juice | ||

| Fruit and Vegetable Blends | ||

| By Type | 100% Juice | |

| Juice Drinks (25–99% juice content) | ||

| Nectar | ||

| By Packaging Type | Tetra Pak Cartons | |

| PET Bottles | ||

| Glass Bottles | ||

| Cans | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retailers | ||

| Other Off-Trade Channel | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

Key Questions Answered in the Report

What is the current Gulf Cooperation Council (GCC) juice market size?

The Gulf Cooperation Council (GCC) juice market size is USD 6.5 billion in 2026.

How fast is the Gulf Cooperation Council (GCC) juice market expected to grow?

The market is projected to advance at a 5.98% CAGR, taking the market to USD 8.69 billion by 2031.

Which country holds the largest Gulf Cooperation Council (GCC) juice market share today?

Saudi Arabia leads with 49.15% share of regional sales.

Which segment is growing the fastest within the Gulf Cooperation Council (GCC) juice market?

Nectar show the highest momentum with an 7.52% CAGR forecast for 2026-2031.

Page last updated on: