GHG Protocol Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

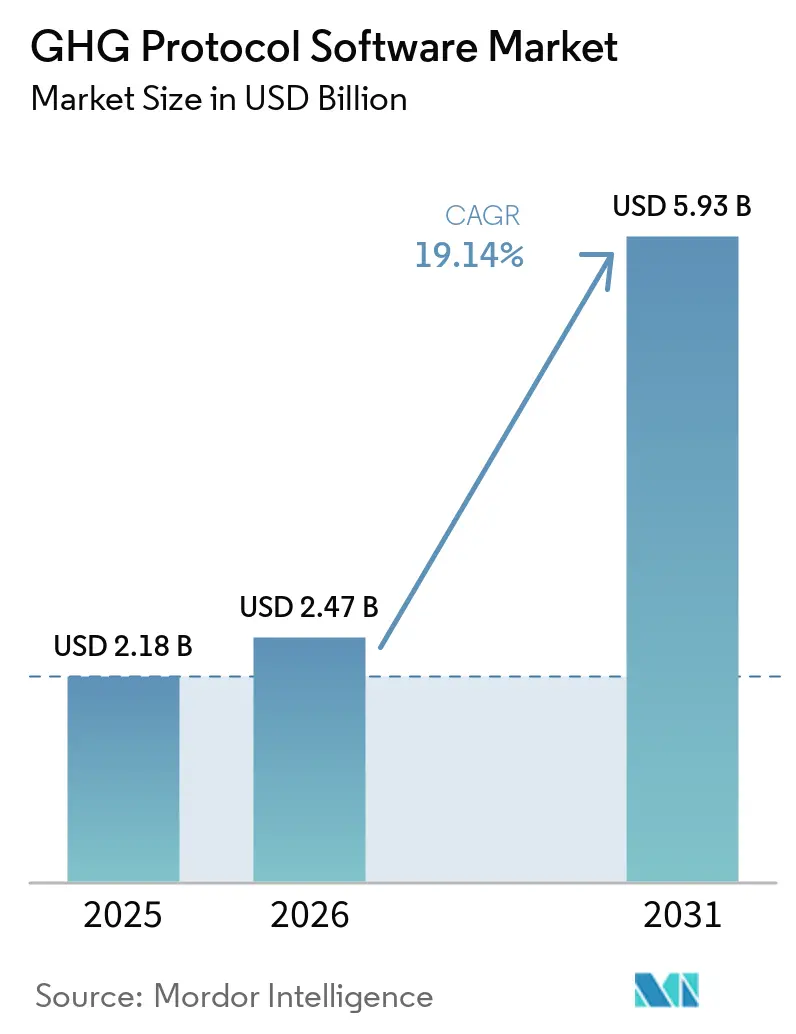

| Market Size (2026) | USD 2.47 Billion |

| Market Size (2031) | USD 5.93 Billion |

| Growth Rate (2026 - 2031) | 19.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GHG Protocol Software Market Analysis by Mordor Intelligence

The GHG Protocol Software Market size is expected to increase from USD 2.18 billion in 2025 to USD 2.47 billion in 2026 and reach USD 5.93 billion by 2031, growing at a CAGR of 19.14% over 2026-2031. Growth is being shaped by a clear shift in how enterprises manage emissions data, with reporting moving out of spreadsheet-based sustainability workflows and into finance, procurement, and operational systems. Mandatory disclosure timelines in Europe and California have shortened buying cycles and turned carbon accounting software from a voluntary reporting tool into core compliance infrastructure. Demand is also rising because finance teams now need audit-ready controls, traceable data lineage, and reporting structures that can stand up to external assurance. Competitive pressure is increasing as ERP vendors embed carbon accounting into financial control environments, which is forcing pure-play providers to broaden their product scope and strengthen assurance capabilities. At the same time, methodology changes tied to the GHG Protocol Scope 3 revision process could slow some purchase decisions among mid-market buyers that are already managing major reporting transitions.

Key Report Takeaways

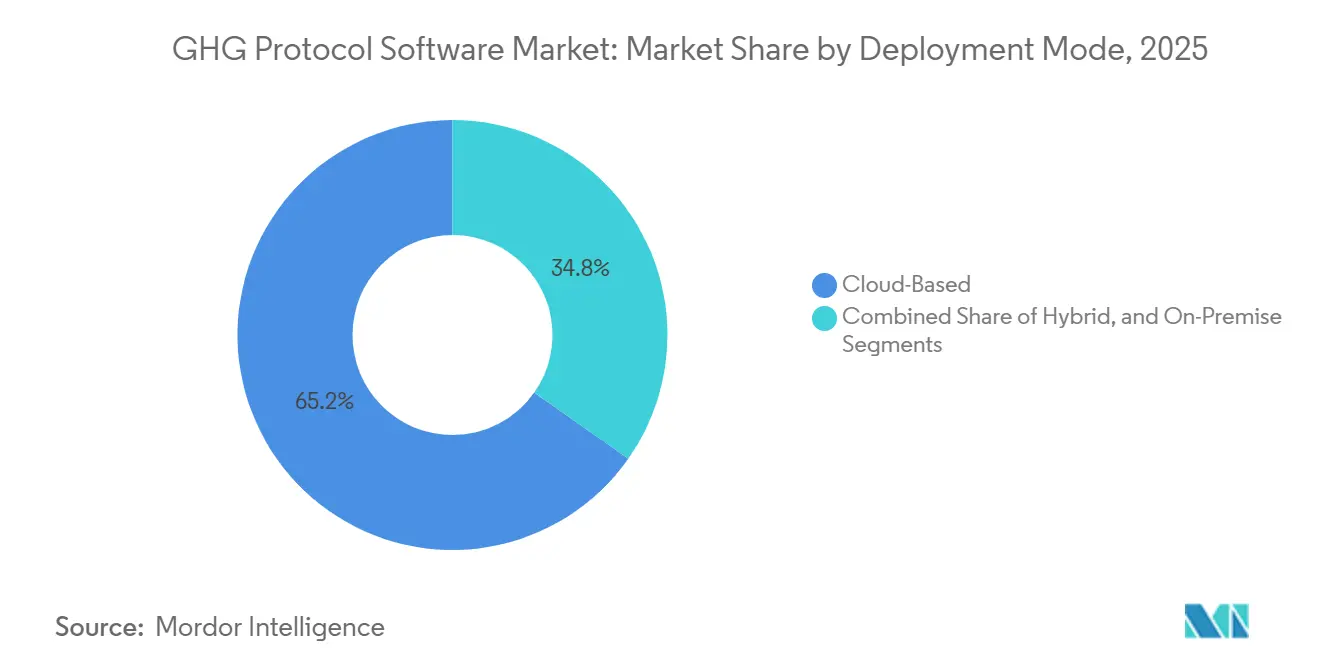

- By deployment mode, cloud-based deployment held 65.23% of the GHG Protocol Software Market share in 2025, while hybrid deployment is projected to expand at a 20.12% CAGR through 2031.

- By enterprise size, large enterprises accounted for 67.12% of revenue in 2025, while SMEs are expected to record the fastest CAGR of 21.34% through 2031.

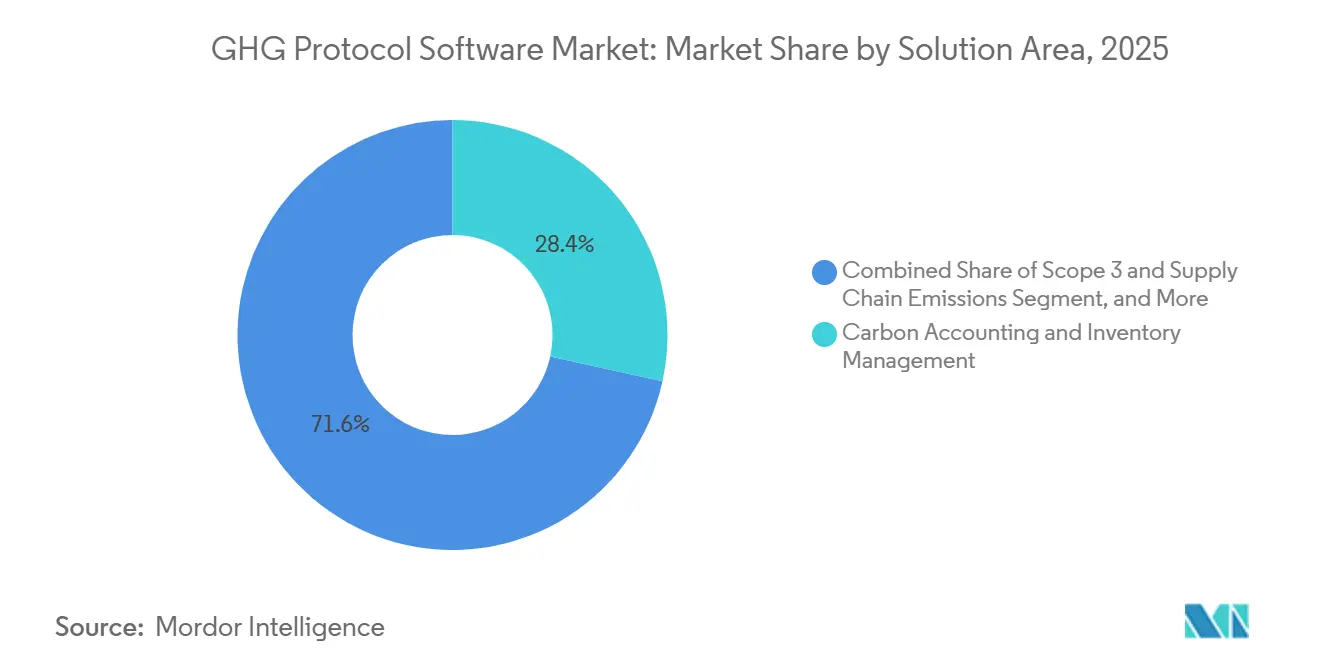

- By solution area, carbon accounting and inventory management represented a 28.45% share in 2025, while Scope 3 and supply chain emissions management is projected to grow at a 24.56% CAGR through 2031.

- By end-user industry, industrial manufacturing held a 26.34% share in 2025, while energy, utilities and resources is expected to expand at a 22.45% CAGR over 2026-2031.

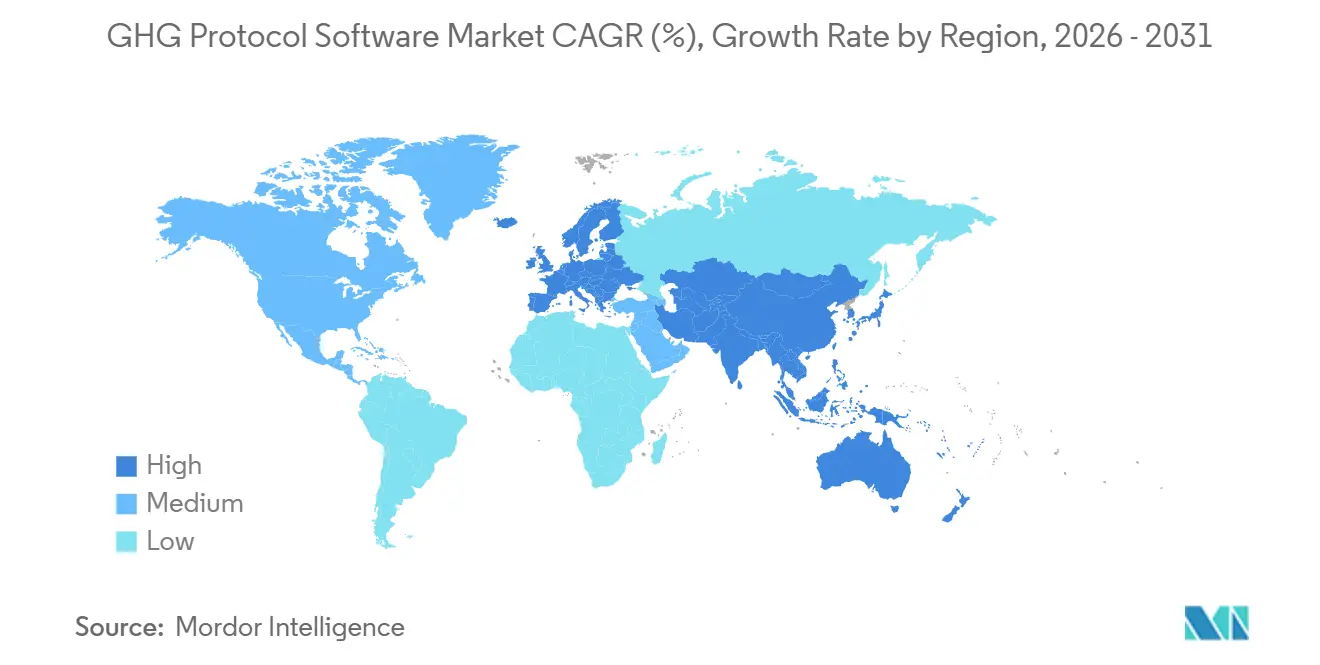

- By geography, North America held 36.12% of the GHG Protocol Software Market size in 2025, while Asia-Pacific is projected to advance at a 26.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GHG Protocol Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Push for Mandatory Scope 1, Scope 2, and Scope 3 Disclosures | +4.5% | Global, concentrated in EU and North America, with phased expansion to Asia-Pacific | Short term (≤ 2 years) |

| GHG Protocol Alignment in CSRD, IFRS S2, and California Compliance Workflows | +3.8% | EU core, North America, California-led, expanding to ISSB-adopting jurisdictions in Asia-Pacific | Short term (≤ 2 years) |

| Audit-Ready Carbon Data Demand Across Finance and Sustainability Teams | +2.9% | Global, highest in markets with third-party assurance mandates, including EU, UK, and Australia | Medium term (2-4 years) |

| AI-Assisted Emissions Factor Mapping and Data Reconciliation | +2.4% | Global, with early concentration in North America and EU technology hubs | Medium term (2-4 years) |

| Shift From Spend-Based Estimates to Primary Supplier Data | +1.8% | Global, especially relevant for complex supply chain geographies in Asia-Pacific, EU, and North America | Medium term (2-4 years) |

| Carbon Ledger Integration With ERP and Financial Controls | +1.3% | Global, concentrated in SAP- and Oracle-heavy enterprise markets in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Mandatory Scope 1, Scope 2, and Scope 3 Disclosures

Mandatory disclosure rules have changed the buyer base for the GHG Protocol Software Market. The EU CSRD took effect from January 1, 2024, and it covers an estimated 50,000 companies, including non-EU groups with substantial EU operations, with ESRS E1 requiring Scope 1, Scope 2, and significant Scope 3 disclosures that directly reference the GHG Protocol Scope 3 Standard.[1]GHG Protocol, “Overview of GHG Protocol Integration in Mandatory Climate Disclosure Rules,” GHG Protocol, ghgprotocol.org California SB 253 added another major trigger: the California Air Resources Board adopted initial implementation language on February 26, 2026, and confirmed filing deadlines for Scope 1 and Scope 2 disclosures for covered entities on August 10, 2026. These rules matter beyond the largest reporters, as large buyers now push emissions data requests down to their suppliers as they work through Scope 3 Category 1 obligations. That spillover is widening adoption in the GHG Protocol Software Market faster than direct regulation alone would suggest, especially for suppliers that need to remain eligible for enterprise procurement programs.

GHG Protocol Alignment in CSRD, IFRS S2, and California Compliance Workflows

The GHG Protocol Software Market is also benefiting from the fact that the same accounting framework is embedded across multiple reporting systems. IFRS S2, issued by the ISSB and effective from January 1, 2024, explicitly requires the use of the GHG Protocol Corporate Standard unless a jurisdiction directs otherwise, and the 2025 amendments did not change that core dependency.[2]IFRS Foundation, “Amendments to IFRS S2, GHG Emissions Disclosures,” IFRS Foundation, ifrs.org The GHG Protocol stated in January 2025 that this dependency is already embedded in rules or adoption plans across a wide range of countries, providing vendors with a durable foundation for product design and customer retention. Interoperability is also tightening, as amended ESRS rules issued in December 2025 moved further toward alignment with IFRS S1 and S2 and reinforced the need for financial-control-style consolidation, which favors standardized platforms over custom methods. That convergence increases the value of a single audit-ready emissions inventory in the GHG Protocol Software Market because a single core dataset can support multiple reporting obligations simultaneously.

Audit-Ready Carbon Data Demand Across Finance and Sustainability Teams

The quality threshold in the GHG Protocol Software Market is rising because climate data now needs to withstand assurance reviews. SAP stated in May 2026 that Green Ledger applies double-entry bookkeeping principles to carbon records and provides transaction-level traceability that mirrors financial postings, demonstrating how carbon accounting is moving toward finance-grade control structures.[3]SAP News Center, “SAP a Leader in IDC MarketScape, Carbon Accounting and Management Applications,” SAP, news.sap.com This shift changes who owns the buying decision because sustainability teams no longer act alone when the output must satisfy audit, finance, and regulatory review. The UCLA Anderson 2026 report found that 38% of companies still did not disclose emissions for any of the 15 Scope 3 categories, suggesting a long runway for platforms to improve controls, documentation, and completeness. As a result, the GHG Protocol Software Market is moving closer to the financial software buying model, where data lineage, control evidence, and system integration carry more weight than basic calculation features.

AI-Assisted Emissions Factor Mapping and Data Reconciliation

Artificial intelligence is becoming a practical efficiency tool in the GHG Protocol Software Market, especially for manual factor matching and data cleanup. Sphera reported in February 2026 that 45% of business leaders had only limited confidence in the accuracy of Scope 3 data, even as 89% planned to expand Scope 3 reporting, which explains why automation is attracting so much attention. Persefoni introduced Analytics Agent in May 2026 to let users query CO2e ledger data with plain-language prompts, while Watershed launched AI agents in April 2026 for data ingestion and emissions analysis workflows. These capabilities matter because they reduce the labor required to expand reporting coverage into harder Scope 3 categories. That makes the GHG Protocol Software Market more accessible to mid-sized organizations that could not previously support large teams for emissions mapping and reconciliation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scope 3 Data Gaps Across Multi-Tier Supply Chains | -2.5% | Global, most acute in Asia-Pacific manufacturing supply chains and multi-tier EU supplier networks | Medium term (2-4 years) |

| Fragmented Reporting Rules Across Jurisdictions | -1.8% | Global, with highest friction in multinational operations spanning EU, US, Asia-Pacific, and Middle East | Medium term (2-4 years) |

| High Implementation and Change-Management Burden for Mid-Market Buyers | -1.2% | North America and Europe mid-market, emerging in Asia-Pacific SME supplier tiers | Short term (≤ 2 years) |

| Assurance, Traceability, and Methodology Switching Complexity | -0.9% | Global, primarily in markets where assurance standards are moving from limited to reasonable | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scope 3 Data Gaps Across Multi-Tier Supply Chains

Scope 3 data collection remains the biggest structural constraint on the GHG Protocol Software Market. Sphera found in February 2026 that 45% of business leaders had only limited confidence in the accuracy of Scope 3 data, even though 89% planned broader reporting, indicating that reporting ambition is still ahead of data quality. EcoVadis stated in April 2026 that it was expanding its Carbon Data Network to improve supplier transparency, reflecting the ongoing difficulty of collecting consistent upstream information across fragmented supply chains. The GHG Protocol Phase 1 Progress Update from March 31, 2026, proposed more explicit disclosure by data quality tier in the revised Scope 3 Standard, and that would require many existing software workflows to be recalibrated. In the near term, that transition burden can slow platform expansion decisions in the GHG Protocol Software Market even though it should increase long-run demand for better supplier data tools.

Fragmented Reporting Rules Across Jurisdictions

The GHG Protocol Software Market also faces friction from uneven reporting rules across major jurisdictions. IFRS S2 remains anchored to the GHG Protocol, but jurisdictional relief provisions and implementation pathways still vary by country, which limits full harmonization for multinational buyers. At the same time, California SB 253 requires Scope 3 reporting from 2027, while the U.S. federal regime took a narrower approach, leaving companies often needing multiple reporting configurations across the same enterprise estate.[4]California Air Resources Board, “California Corporate Greenhouse Gas Reporting and Climate Related Financial Risk Disclosure Programs,” California Air Resources Board, arb.ca.gov The GHG Protocol noted in January 2025 that disclosure frameworks are spreading rapidly across different legal systems, increasing the number of buyers who need cross-framework support rather than single-rule software. This adds cost and extends deployment timelines in the GHG Protocol Software Market, particularly for mid-market organizations that started with basic tools and now need broader configuration depth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Architecture Closes The Audit-Access Gap

Cloud-based deployment held 65.23% of the GHG Protocol Software Market share in 2025, and that lead reflected the appeal of software that can scale across entities and jurisdictions without heavy infrastructure investment. Cloud systems align with the operating model of multinational companies that need faster onboarding for subsidiaries, standardized reporting templates, and easier collaboration among sustainability, finance, and procurement teams. The GHG Protocol Software Market also benefited from multi-tenant platforms' ability to support frequent regulatory updates without requiring lengthy in-house upgrades. That advantage mattered as companies adjusted to the CSRD, California rules, and broader adoption linked to the ISSB. Many buyers also preferred subscription-based deployments because they reduced upfront capital commitments while supporting faster feature expansion.

Hybrid deployment is projected to grow at a 20.12% CAGR through 2031, which makes it the fastest-growing deployment model in the GHG Protocol Software Market. This pattern reflects a practical balance between control and flexibility, especially for companies that want carbon entries governed within finance-grade environments while keeping supplier collaboration and analytics in the cloud. SAP stated in May 2026 that Green Ledger posts carbon data in SAP S/4HANA, using SAP Business Technology Platform for reporting and collaboration, which illustrates why hybrid design is gaining traction. On-premises systems still retain a place in regulated sectors such as energy, utilities, and government, where internal control and data sovereignty requirements remain strict. Even so, the direction of the GHG Protocol Software industry now points toward architectures that combine protected core records with flexible digital interfaces rather than fully isolated environments.

By Enterprise Size: SME Adoption Rises As Supply Chain Pressure Spreads

Large enterprises accounted for 67.12% of revenue in 2025, giving them the leading position in the GHG Protocol Software Market. Their scale, legal exposure, and multi-entity reporting needs made manual processes too limited for the volume of emissions data now required. These buyers also tended to run structured vendor selection programs that favored strong assurance controls, audit documentation, and ERP integration. In practice, large companies use the software not just for disclosure, but also for internal control, consolidation, and supplier engagement. That combination kept them at the center of current spending across the GHG Protocol Software Market.

SMEs are projected to expand at a 21.34% CAGR through 2031, and this shift is being driven as much by customer pressure as by direct regulation. The GHG Protocol Corporate Standard and Scope 3 framework push large enterprises to request supplier data, which effectively brings smaller firms into the reporting chain even when local rules do not directly cover them. A March 2026 framework on SME GHG inventory development noted that digital tools can sharply reduce the effort required to build ISO 14064-aligned records, which supports the case for lower-configuration platforms. Vendors are responding by pairing software with guided onboarding and advisory support, so smaller firms can meet methodology requirements without enterprise-scale internal teams. This is one of the clearest signs that the GHG Protocol Software Market is moving from a large-enterprise niche into a broader supplier-network platform category.

By Solution Area: Scope 3 Modules Become The Main Growth Frontier

Carbon accounting and inventory management accounted for 28.45% of revenue in 2025, making it the largest solution area in the GHG Protocol Software Market. Most organizations still begin with this module because it establishes the core emissions baseline across Scope 1 and Scope 2 and lays the foundation for the reporting structure used by later modules. Its scale also reflects the fact that many buyers are still building reliable organizational boundaries, factor libraries, and recurring data collection processes. In that sense, this segment remains the operational foundation of the GHG Protocol Software Market. It is also where finance-led control expectations are becoming most visible as buyers demand traceability and internal review functionality.

Scope 3 and supply chain emissions management is projected to grow at a 24.56% CAGR through 2031, which makes it the fastest-growing solution area. This growth follows directly from ESRS E1 and the wider push for data across all 15 Scope 3 categories, especially in procurement-heavy businesses. EcoVadis expanded its Carbon Data Network in April 2026 by adding Carbmee, following earlier additions such as Watershed, Sweep, and Normative, indicating that shared supplier-data infrastructure is becoming increasingly important in this part of the GHG Protocol Software Market. ESG reporting and disclosure management is also gaining ground, as companies seek a single reporting layer across CSRD, IFRS S2, CDP, and California filings rather than separate tools. At the same time, decarbonization analytics and assurance modules are moving closer to the core platform as companies increasingly seek planning, evidence, and disclosure in a single workflow.

By End-User Industry: Manufacturing Leads While Energy Gains Speed

Industrial manufacturing accounted for 26.34% of the GHG Protocol Software Market in 2025, making it the largest end-user segment. Manufacturers face concentrated pressure because purchased goods and services often dominate their emissions profile, and product-level data matters in ways that are less common in service sectors. Carbmee stated in June 2026 that its platform supports GHG software workflows tied to corporate emissions management, and that alignment is especially relevant for exporters dealing with both corporate reporting and product-level requirements. In Europe, this is particularly important where CSRD obligations overlap with CBAM-linked product carbon reporting needs. That dual burden helps explain why manufacturing remains the largest commercial base inside the GHG Protocol Software Market.

Energy, utilities, and resources are projected to grow at a 22.45% CAGR through 2031, making it the fastest-growing end-user segment. Buyers in this group need software that supports decarbonization planning, scenario analysis, and links to voluntary carbon market activity, which expands demand beyond basic inventory management. Financial institutions are also becoming strategically important because financed emissions require specialized workflows, and Persefoni highlighted its Investment Positions Manager in 2025 as a product built for that need. Retail, healthcare, government, and logistics users are also broadening adoption because they must gather more auditable upstream and downstream data across product use, transportation, and supplier categories. This spread across verticals shows that the GHG Protocol Software Market is no longer centered on a narrow set of heavy emitters alone.

Geography Analysis

North America held 36.12% of the GHG Protocol Software Market share in 2025, making it the largest regional market. The region benefited from overlapping reporting pressures, as California established a state-level regime explicitly aligned with the GHG Protocol while public companies prepared for broader climate disclosure obligations. The California Air Resources Board confirmed in February 2026 that SB 253 implementation had entered its next phase, reinforcing the shift from voluntary reporting to formal compliance planning. North America also had strong vendor density, with several major software providers headquartered in the United States. That concentration supported faster implementation cycles, stronger integration ecosystems, and more competitive enterprise sales activity.

Europe remained the most developed regulatory environment for the GHG Protocol Software Market, even though it did not lead in regional share in the data provided. The CSRD phase-in created a rolling demand curve from 2024 through 2028, meaning new buyer cohorts continue to enter the market in sequence rather than all at once. Germany stood out because industrial exporters there face both entity-level reporting duties and product carbon reporting needs tied to cross-border trade. Carbmee’s June 2026 positioning on GHG emissions management software reflects how vendors in the DACH market are building products that leverage this overlap between compliance and operational reporting. The broader European opportunity also remains strong in the United Kingdom, France, Italy, Spain, and the Netherlands, where institutional and regulatory pressure continues to reinforce software adoption.

Asia-Pacific is projected to grow at a 26.41% CAGR through 2031, which makes it the fastest-growing regional segment in the GHG Protocol Software Market. This acceleration is being driven by phased adoption of ISSB-linked reporting across Singapore, Japan, Australia, Hong Kong, and Malaysia, which has created a mandatory demand base that was far less established before 2024. China adds another source of demand because enterprise reporting often depends on plant-level emissions monitoring tied to industrial operations. South Korea and India are also becoming more important as listed companies face widening disclosure expectations and alignment with GHG reporting methods. The Middle East and Africa remained earlier-stage markets, but SINAI’s February 2026 partnership with Saudi Arabia’s Regional Voluntary Carbon Market Company showed that government-backed enterprise decarbonization platforms are beginning to build local demand. South America was less prominent in the provided segment data, but global framework adoption and cross-border supply chain reporting are likely to keep it connected to future platform expansion.

Competitive Landscape

The GHG Protocol Software Market remained moderately fragmented in 2026, with competition spread across ERP vendors, pure-play carbon management platforms, supplier data networks, and broader ESG reporting providers. Buying criteria are shifting because customers now place more weight on assurance readiness, platform breadth, and integration with finance systems than on early-mover positioning alone. This is putting pressure on vendors that built narrow-point solutions around a single workflow or disclosure format. It is also changing how customers compare platforms, with total cost of ownership and implementation depth carrying more weight in larger deals.

SAP became a stronger competitive force after making Green Ledger generally available in December 2024 and continuing to position it in 2026 as an ERP-native carbon accounting layer built for financial-grade traceability. That move matters because it gives SAP a clear advantage in accounts that already run SAP S/4HANA and want to keep carbon records close to financial controls. Pure-play vendors are responding by expanding their analytics, supplier collaboration, and workflow automation, rather than competing solely on calculation engines. Persefoni’s October 2025 partnership with Diligent showed one path: combining carbon accounting with governance, risk, and compliance workflows to embed disclosure processes more deeply within enterprise controls. EcoVadis followed a different path by broadening its Carbon Data Network in April 2026, which supported a shared supplier-data layer feeding several software ecosystems.

Consolidation also became more visible across the GHG Protocol Software Market. Green Project Technologies acquired the Emitwise platform in July 2025 to strengthen supply-chain decarbonization capabilities and fold that technology into a unified offering. Diginex closed the acquisition of Plan A in January 2026, combining ESG reporting breadth with AI-based carbon accounting and decarbonization tools. XeleratedFifty then acquired Terrascope in February 2026, preserving its Asia-Pacific focus and supporting further product investment around CBAM and land sector reporting. These deals suggest that scale, geographic coverage, and adjacent workflow depth now matter more than standalone novelty. The clearest open space remains in mid-market implementations, in manufacturing platforms that combine product carbon footprints with corporate inventories, and in localized Asia-Pacific offerings that support multiple language and compliance needs.

GHG Protocol Software Industry Leaders

Persefoni AI, Inc.

Watershed Technology, Inc.

Plan A ESG GmbH

Greenly SAS

Emitwise Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Persefoni AI launched Persefoni Analytics Agent, an agentic AI capability embedded within its platform that allows sustainability teams to query CO2e activity ledger data using plain-language prompts. The feature maintains full audit-trail integrity within Persefoni's existing methodology governance layer, addressing demand from audit-ready disclosure workflows.

- May 2026: SAP was named a Leader in the IDC MarketScape: Worldwide Carbon Accounting and Management Applications 2026, with the IDC assessment recognizing SAP Green Ledger's ERP-native double-entry carbon accounting architecture as a differentiating capability for enterprises requiring financial-grade traceability in GHG Protocol disclosures.

- April 2026: Watershed launched a suite of AI agents designed to automate data ingestion and emissions analysis workflows, alongside the Watershed Sustainability AI Fellowship, an eight-week program running through June 3, 2026, designed to develop AI-driven sustainability use cases with enterprise practitioners. Watershed was also named a Leader in the 2026 IDC MarketScape for Carbon Accounting and Management Applications.

- April 2026: EcoVadis expanded its Carbon Data Network by adding Carbmee as a strategic partner, following earlier additions of Watershed, Sweep, and Normative. Carbmee's AI-native EIS Environmental Intelligence System identifies emissions hotspots at the SKU level, enabling integration of product-level carbon data into buyer-facing Scope 3 Category 1 accounting systems.

Global GHG Protocol Software Market Report Scope

The GHG Protocol Software market comprises digital platforms and solutions that help organizations measure, manage, and report greenhouse gas emissions in compliance with the Greenhouse Gas Protocol standards. These systems provide functionalities such as carbon accounting, ESG reporting and disclosure, Scope 3 and supply chain emissions tracking, decarbonization planning, climate analytics, and assurance and governance.

The GHG Protocol Software market report is segmented by Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Area (Carbon Accounting and Inventory Management, ESG Reporting and Disclosure Management, Scope 3 and Supply Chain Emissions Management, Decarbonization Planning and Climate Analytics, Assurance, Audit and Governance), End-user Industry (Industrial Manufacturing, Energy, Utilities and Resources, BFSI, Retail and Consumer Goods, IT and Telecom, Healthcare and Life Sciences, Government and Public Sector, Transportation and Logistics, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Carbon Accounting and Inventory Management |

| ESG Reporting and Disclosure Management |

| Scope 3 and Supply Chain Emissions Management |

| Decarbonization Planning and Climate Analytics |

| Assurance, Audit and Governance |

| Industrial Manufacturing |

| Energy, Utilities and Resources |

| BFSI |

| Retail and Consumer Goods |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Transportation and Logistics |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Solution Area | Carbon Accounting and Inventory Management | |

| ESG Reporting and Disclosure Management | ||

| Scope 3 and Supply Chain Emissions Management | ||

| Decarbonization Planning and Climate Analytics | ||

| Assurance, Audit and Governance | ||

| By End-user Industry | Industrial Manufacturing | |

| Energy, Utilities and Resources | ||

| BFSI | ||

| Retail and Consumer Goods | ||

| IT and Telecom | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Transportation and Logistics | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the GHG Protocol Software Market?

The GHG Protocol Software Market was valued at USD 2.47 billion in 2026 and is forecast to reach USD 5.93 billion by 2031 at a 19.14% CAGR.

Which deployment model leads software demand for GHG Protocol reporting?

Cloud-based deployment led with a 65.23% share in 2025 because enterprises favored scalable systems that can support multiple reporting entities without large infrastructure costs.

Why are Scope 3 capabilities becoming so important in carbon accounting platforms?

Scope 3 and supply chain emissions management is projected to grow at a 24.56% CAGR through 2031 because companies need deeper supplier data collection and broader coverage across reporting categories.

Which end-user group spends the most on these platforms today?

Industrial manufacturing led with a 26.34% share in 2025 because manufacturers face product-level and corporate-level carbon reporting pressures at the same time.

Which region is growing the fastest for GHG Protocol-aligned software?

Asia-Pacific is the fastest-growing region with a 26.41% CAGR through 2031, supported by phased ISSB-linked disclosure adoption across several major markets.

What is changing vendor competition in this space?

Competition is shifting toward broader platforms with stronger assurance, AI automation, and ERP integration, while acquisitions and partnerships are reducing the room for narrow standalone tools.

Page last updated on: