Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.35 Billion |

| Market Size (2026) | USD 12.35 Billion |

| Market Size (2031) | USD 18.87 Billion |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Managed Services Market Analysis by Mordor Intelligence

The GCC managed services market size in 2026 is estimated at USD 12.35 billion, growing from 2025 value of USD 11.35 billion with 2031 projections showing USD 18.87 billion, growing at 8.84% CAGR over 2026-2031. Robust national digitization agendas, hyperscale cloud investments exceeding USD 4 billion, and strict data-sovereignty mandates are accelerating the outsourcing of non-core IT functions. Saudi Arabia’s Vision 2030 programs and the UAE’s AI Strategy 2031 account for the bulk of enterprise demand, while sovereign-cloud launches by Microsoft, Oracle, and AWS reinforce the requirement for localized managed-service expertise[1]Saudi Vision 2030, “Leadership Messages,” vision2030.gov.sa. Growing cyber-insurance prerequisites, AI-driven cost-optimization, and environmental, social, and governance (ESG) spending pivots further expand addressable opportunities across the GCC managed services market. Competitive dynamics favor regional telecom operators and cloud-native entrants that can blend local regulatory fluency with advanced automation capabilities.

Key Report Takeaways

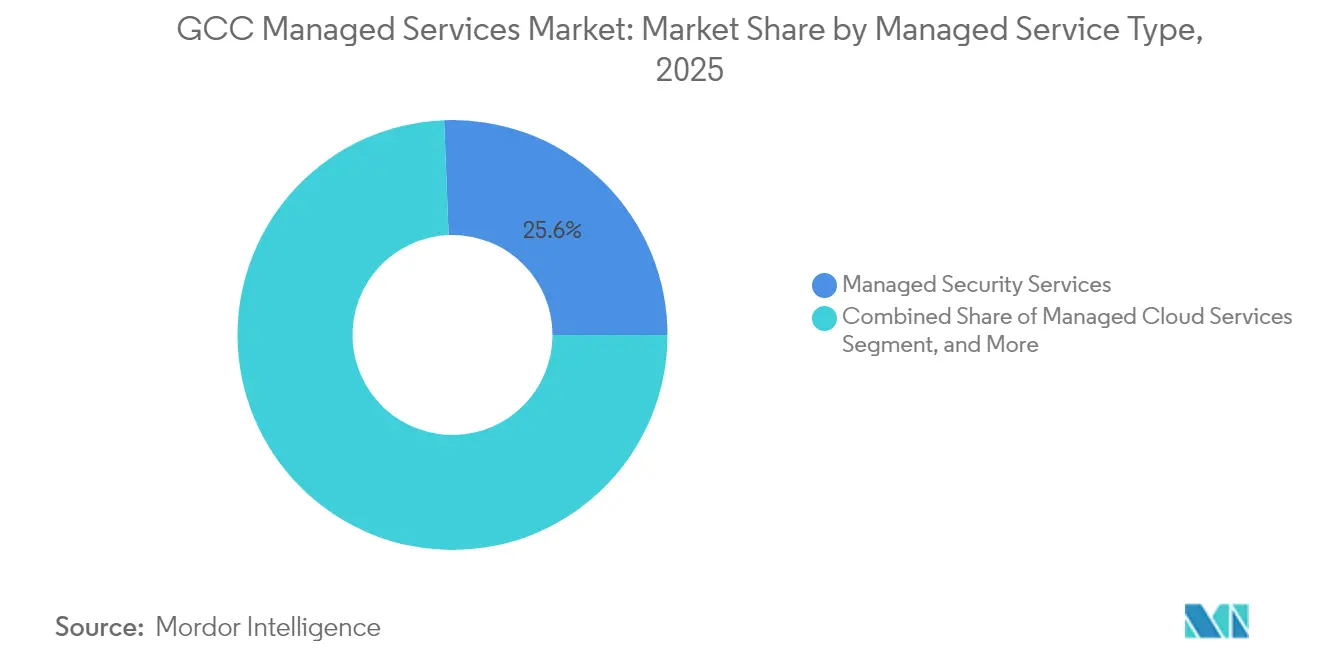

- By managed service type, Managed Security Services held 25.62% of the GCC managed services market share in 2025; Managed Cloud Services are advancing at a 13.65% CAGR through 2031.

- By end-user vertical, BFSI led with 21.45% revenue share in 2025, while Healthcare is forecast to post the fastest 13.36% CAGR to 2031.

- By service delivery model, Remote/Off-site accounted for 43.10% of 2025 revenue; Hybrid delivery is expected to compound at 15.02% CAGR during the forecast horizon.

- By geography, Saudi Arabia dominated with a 43.05% share of the GCC managed services market size in 2025; the UAE is set to record the highest 11.62% CAGR to 2031.

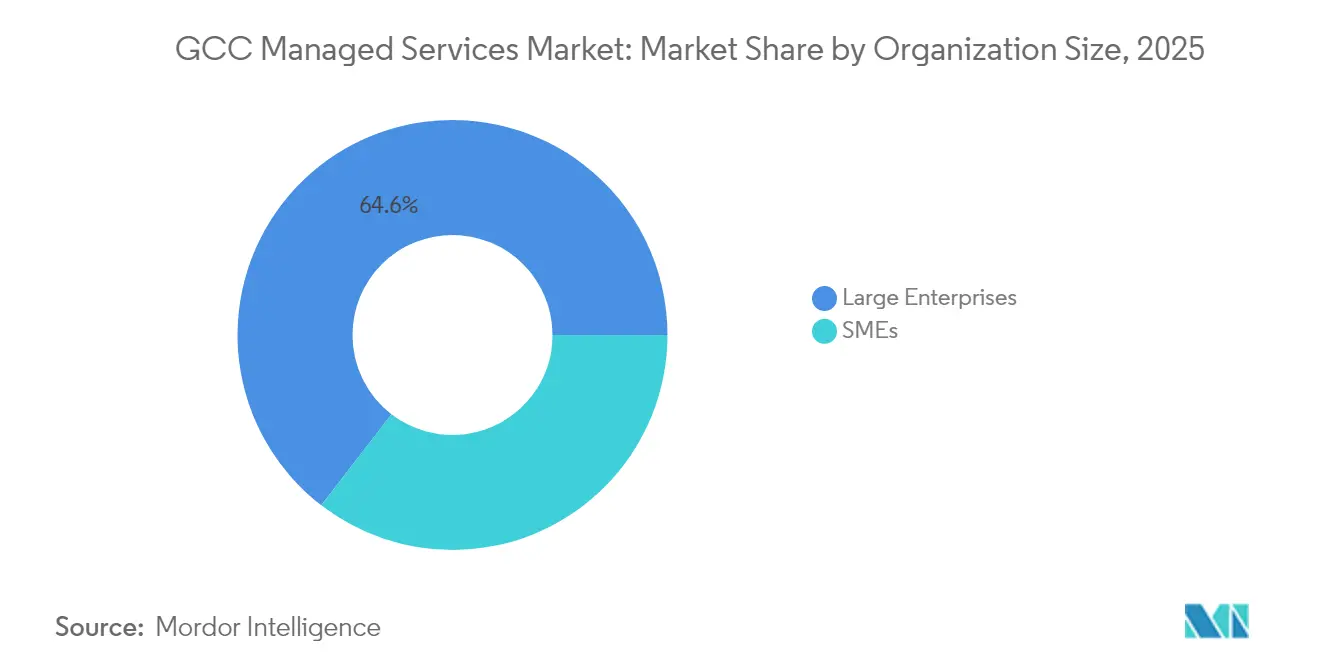

- By organization size, Large Enterprises captured 64.55% of 2025 revenue, but SMEs are projected to expand at 16.21% CAGR on the back of cloud-native offerings.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscale cloud-region launches across GCC | +2.1% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Mandatory in-country data-residency and sovereignty rules | +1.8% | GCC-wide, strongest in Saudi Arabia | Long term (≥ 4 years) |

| Outsourcing push from Vision 2030 and other national agendas | +2.3% | Saudi Arabia, UAE, Kuwait | Long term (≥ 4 years) |

| Rising cyber-insurance requirements driving managed security uptake | +1.4% | GCC-wide, led by UAE and Saudi Arabia | Short term (≤ 2 years) |

| AI-enabled service automation cutting total cost of ownership | +1.2% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| ESG-linked OPEX shifting CAPEX workloads to MSPs | +0.8% | GCC-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in hyperscale cloud-region launches across GCC

Microsoft’s Project MGX targets 14 hyperscale campuses, while Oracle has opened its second Riyadh cloud region under a USD 1.5 billion program. The region’s data-center capacity is on track to surpass 1 GW by 2026, prompting enterprises to seek managed partners for low-latency, AI-ready workloads. A USD 5 billion KKR–Gulf Data Hub venture underscores long-term capital inflows that sustain demand for operations, security, and compliance services[2]KKR, “KKR and Gulf Data Hub Form Strategic Partnership,” kkr.com. As hyperscalers localize infrastructure to satisfy sovereignty mandates, the GCC managed services market must deliver both global-grade tooling and in-country expertise.

Mandatory in-country data-residency and sovereignty rules

Saudi Arabia’s Personal Data Protection Law and the UAE’s banking directives require customer records to remain inside national borders, forcing enterprises to change hosting architectures. Microsoft, Oracle, and AWS have all launched “sovereign cloud” offerings that rely on local partners for monitoring and incident response, because certification schemes differ by state, multi-jurisdiction organizations depend on managed service providers (MSPs) to coordinate audits and maintain continuous compliance across six distinct GCC frameworks. Elevated non-compliance fines in free-zone jurisdictions add urgency to outsource governance workloads.

Outsourcing push from Vision 2030 and other national agendas

Vision 2030 aims to raise private-sector contribution to 65% of Saudi GDP, catalyzing large outsourcing contracts for public-sector IT and cybersecurity. Similar mandates in the UAE’s AI Strategy 2031 target a 50% cost reduction in government operations, creating multi-year MSP engagements for cloud, analytics, and automation. National champions such as Saudi Aramco and stc Group embed managed services clauses in multi-billion-dollar procurement rounds, accelerating vendor consolidation and bolstering recurring revenue streams. The convergence of policy-driven transformation and private-sector efficiency directly lifts the GCC managed services market.

AI-enabled service automation cutting total cost of ownership

Stc Group achieved a 13% drop in energy consumption by embedding AI/ML in its network operations center[3]stc Group, “Annual Report 2024,” stc.com. Enterprises now demand outcome-based contracts in which MSP margins hinge on algorithm-driven productivity gains. The UAE’s 75% enterprise usage rate of generative models sets a regional benchmark that fuels spending on AI-augmented monitoring, self-healing infrastructure, and predictive security analytics. MSPs that industrialize AI workflows capture premium pricing and longer contract tenures within the GCC managed services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortage of Arabic-speaking Tier-3 engineers | -1.5% | GCC-wide, most acute in Saudi Arabia | Long term (≥ 4 years) |

| Government "Saudization/Emiratization" hiring quotas | -1.2% | Saudi Arabia, UAE | Medium term (2-4 years) |

| High energy-pricing volatility for data-center operations | -0.8% | GCC-wide | Short term (≤ 2 years) |

| Fragmented regulatory certifications across GCC states | -0.6% | GCC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent shortage of Arabic-speaking Tier-3 engineers

The GCC faces a critical talent gap in Arabic-speaking technical professionals, with Korn Ferry projecting nearly USD 40 billion in talent shortage costs across the UAE and Saudi Arabia, including USD 2.4 billion in wage premiums for the technology, media, and telecom sectors in Saudi Arabia alone. Saudi Arabia's requirement for 51% of IT organizations to address skills gaps as their primary challenge creates structural constraints on managed services delivery, particularly for complex technical support requiring local language capabilities. The shortage becomes more acute in Tier-3 support roles where cultural understanding and Arabic fluency are essential for effective client interaction, forcing managed service providers to invest heavily in training programs or accept higher operational costs through premium compensation packages. European tech professionals are increasingly attracted to GCC markets, with network engineers earning an average of USD 74,900 in the Middle East compared to USD 31,000 in European markets, but language barriers limit their effectiveness in client-facing roles. Oracle's commitment to train 350,000 people in AI and advanced digital technologies across the Middle East represents industry recognition of the skills gap, but the timeline for developing Arabic-speaking technical expertise extends the constraint's impact. The World Economic Forum's prediction of 945,000 new jobs requiring digital skills in the region by 2025 indicates the scale of talent development needed to address this constraint.

Government “Saudization/Emiratization” hiring quotas

Saudi Arabia raised engineering-sector nationalization to 25% in 2024, while the UAE imposed Emiratization obligations on firms with as few as 20 employees, with penalties nearing USD 26,000 per year for each shortfall. MSPs must redesign staffing models, allocate budget for certification training, and sometimes accept productivity dips to remain compliant. The policy improves local employment but limits providers’ ability to scale rapidly across multiple GCC jurisdictions, tempering the overall growth trajectory of the GCC managed services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Managed Service Type: Security Leads, Cloud Accelerates

Managed Security Services contributed USD 2.91 billion, equal to 25.62% of the GCC managed services market share in 2025, underlining demand for 24/7 threat monitoring and incident response. Rising attack volumes—from 50,000 attempted breaches daily in the UAE alone—drive enterprises to outsource advanced security operations. Managed Cloud Services, while representing a smaller revenue base, are growing at 13.65% CAGR as hyperscale expansions require governance, optimization, and FinOps expertise. The segment benefits from sovereign-cloud rollouts and low-latency AI workload requirements.

Infrastructure, network, and disaster-recovery offerings remain essential for legacy modernization and regulatory compliance. 5G rollouts by e& and stc fuel managed network demand, while national continuity regulations boost uptake of disaster-recovery-as-a-service. Emerging managed IoT and edge compute packages support smart-city projects such as Abu Dhabi’s Aion Sentia, widening the addressable scope. Collectively, these patterns reinforce a diversified revenue mix that protects the GCC managed services market against cyclicality.

By End-user Vertical: BFSI Dominance, Healthcare Surge

The BFSI segment generated USD 2.43 billion, equivalent to 21.45% of the total GCC managed services market size in 2025, reflecting stringent governance standards and real-time transaction-processing needs. Banks contract MSPs for secure core-banking, anti-fraud analytics, and open-banking API management. Healthcare grows fastest at 13.36% CAGR as electronic health records and telemedicine platforms necessitate HIPAA-style data protection alongside AI-enabled diagnostics. Government agencies and energy majors continue to outsource specialized workloads, while retail and manufacturing leverage cloud-native MSPs for omnichannel and supply-chain optimization.

Managed-service penetration remains uneven across verticals, but AI automation and cyber-insurance mandates create cross-sector tailwinds. As sectoral requirements converge on compliance, uptime, and security, providers with verticalized blueprints gain pricing power. These dynamic supports sustained double-digit expansion across the GCC managed services industry.

By Service Delivery Model: Remote Dominance, Hybrid Growth

Remote delivery accounted for 43.10% of 2025 spending, reflecting proven cost efficiency and mature tooling for remote monitoring, patching, and help-desk support. Post-pandemic normalization keeps remote support mainstream, but data-sovereignty and latency needs have elevated adoption of the Hybrid Model, which is projected to grow at 15.02% CAGR through 2031. Hybrid setups couple centralized control planes with on-site presence for critical assets, satisfying compliance without inflating travel overheads.

On-site/Field services remain vital for sensitive industrial control systems, whereas Co-managed arrangements allow in-house IT to supervise strategic assets while offloading routine tasks. MSPs now bundle flexible delivery options, enabling clients to shift workloads among models without contract renegotiation. Such agility embeds switching costs and extends customer lifetime value in the GCC managed services market.

By Organization Size: Enterprise Leadership, SME Acceleration

Large Enterprises captured 64.55% of 2025 revenue, pooling multi-vendor contracts across infrastructure, security, and application management. Complex regulatory obligations, multi-cloud governance, and AI experimentation create long, high-value engagements. SMEs, however, are growing at 16.21% CAGR, taking advantage of standardized, subscription-based bundles that eliminate large capital outlays. Solutions by stc has tailored cloud, voice, and security SKUs for this cohort, expanding its domestic footprint.

As hyperscale platforms democratize advanced capabilities, service catalogs once restricted to enterprises now reach mid-market buyers. MSPs that automate onboarding, billing, and support capture volume-driven growth without proportional headcount increases. This diffusion broadens the GCC-managed services market beyond traditional enterprise segments.

By Deployment Environment: Cloud Transformation Accelerates

Public-cloud workloads dominate new deployments, propelled by Microsoft, Oracle, and AWS regional launches. However, highly regulated entities rely on Private Cloud or on-premise systems, preserving a blended landscape. The fastest expansion is within Hybrid Cloud architectures, where orchestration layers manage data locality, cost policies, and AI workload placement across multiple substrates. G42’s Core42 launch epitomizes the emerging one-stop-shop model that spans cloud, AI, and managed services G42.AI.

Multi-cloud complexity translates into recurring optimization needs, from FinOps to Kubernetes governance. MSPs that master automated policy enforcement and cross-platform observability remain indispensable. Consequently, the GCC managed services market is shifting from pure infrastructure contracts toward holistic, environment-agnostic operating models.

Geography Analysis

Saudi Arabia accounted for 43.05% of 2025 revenue, underpinned by Vision 2030 megaprojects, a dedicated Cloud Computing Special Economic Zone, and stc’s 73% domestic telecom share. Oracle’s USD 1.5 billion commitment and IBM’s USD 200 million investment illustrate the infrastructure depth that sustains managed-services uptake. Public-sector digitization, cybersecurity mandates, and oil-and-gas modernization together support multi-year MSP contracts that anchor the GCC managed services market.

The UAE delivers the fastest 11.62% CAGR, leveraging its hub status for 38-country conglomerates like e& and its regulatory sandboxes for fintech and AI pilots. Abu Dhabi’s USD 2.5 billion Aion Sentia project and G42’s acquisition spree create sustained demand for cloud, security, and AI operations services. Free-zone compliance frameworks require localized MSP capabilities, reinforcing stickiness once vendors meet certification thresholds.

Qatar, Kuwait, Oman, and Bahrain compose the remaining opportunity pool, each characterized by national diversification programs and tailored data-sovereignty statutes. Kuwait’s forthcoming Azure region, Oman’s Kemet Data Center, and Bahrain’s “cloud-first policy” draw MSPs into joint ventures with local investors. Although individual market sizes are smaller, cumulative mid-single-digit CAGR from these states adds incremental lift to the GCC managed services market over the forecast period.

Competitive Landscape

Regional telecom incumbents—stc Group and e&—leverage fiber, 5G, and data-center assets to deliver end-to-end managed portfolios that include security, cloud, and IoT. stc’s USD 2.9 billion IT-services revenue and 22.7% domestic share highlight scale advantages, while e& pairs 38-market geographic reach with strategic AI alliances such as its IBM governance platform. These players invest heavily in sovereign-cloud nodes, satisfying localization rules and erecting entry barriers for foreign competitors.

Global integrators—IBM, Wipro, HPE, and Accenture—counter by localizing delivery centers, forming joint ventures, and acquiring minority stakes in regional specialists. IBM’s new Riyadh innovation hub, Wipro’s Etihad Airways deal, and Accenture’s sovereign-cloud partnership with Google exemplify moves to secure high-profile reference accounts. Multinational credibility combined with regional compliance assets positions these firms to capture complex digital-transformation programs within the GCC managed services market.

Disruptors such as G42’s Core42 and niche AI-native firms enter through specialized offerings—predictive maintenance, smart-city orchestration, or ESG analytics—often achieving double-digit share gains in emerging sub-segments. Competitive intensity therefore hinges on the ability to deliver embedded AI, ensure regulatory conformity, and bundle multi-cloud operations under outcome-based contracts. Providers unable to invest in sovereign infrastructure or Arabic-language talent risk marginalization.

GCC Managed Services Industry Leaders

Etihad Etisalat Co. (Mobily)

AGC Networks (An ESSAR Company)

EITC Group (du)

Saudi Telecom Company

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ADQ and Energy Capital Partners agreed on a USD 25 billion venture to secure low-carbon power for data centers serving AI workloads.

- July 2025: Fujitsu unveiled its Technology and Service Vision 2025, emphasizing AI-enabled cross-industry ecosystems and net-positive outcomes.

- May 2025: Oracle reiterated its USD 1.5 billion Saudi investment to align with economic-prosperity initiatives and expand cloud regions.

- March 2025: Microsoft announced plans for an AI-powered Azure region in Kuwait to accelerate national digital-transformation objectives.

- February 2025: Cognizant entered a three-year alliance with Upsource by Solutions in Saudi Arabia to provide Gen-AI-powered finance automation.

GCC Managed Services Market Report Scope

Managed services are the practice of outsourcing the responsibility for maintaining and anticipating the need for a range of processes and functions, ostensibly for the purpose of improved operations and reduced budgetary expenditures through the reduction of directly employed staff. GCC Managed Services Market is segmented by Type (Managed Infrastructure Services, Managed Hosting Services, Managed Security Services, Managed Cloud Services, Disaster Recovery & Business Continuity Services), End-user Industry (IT & Telecom, BFSI, Oil & Gas, Healthcare, Government), and Country. The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Managed Service Type

| Managed Infrastructure Services |

| Managed Hosting Services |

| Managed Security Services |

| Managed Cloud Services |

| Disaster Recovery and Business Continuity |

| Network and Communication Services |

| End-user Support Services |

| Managed IoT Services |

By End-user Vertical

| IT and Telecom |

| BFSI |

| Oil and Gas |

| Healthcare |

| Government |

| Retail and E-commerce |

| Education |

| Manufacturing |

| Energy and Utilities |

By Service Delivery Model

| Remote / Off-site Managed Services |

| On-site / Field Managed Services |

| Hybrid Model |

| Co-managed Services |

By Organization Size

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

By Deployment Environment

| On-premise |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Managed Service Type | Managed Infrastructure Services |

| Managed Hosting Services | |

| Managed Security Services | |

| Managed Cloud Services | |

| Disaster Recovery and Business Continuity | |

| Network and Communication Services | |

| End-user Support Services | |

| Managed IoT Services | |

| By End-user Vertical | IT and Telecom |

| BFSI | |

| Oil and Gas | |

| Healthcare | |

| Government | |

| Retail and E-commerce | |

| Education | |

| Manufacturing | |

| Energy and Utilities | |

| By Service Delivery Model | Remote / Off-site Managed Services |

| On-site / Field Managed Services | |

| Hybrid Model | |

| Co-managed Services | |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) | |

| By Deployment Environment | On-premise |

| Public Cloud | |

| Private Cloud | |

| Hybrid Cloud | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

How big is the GCC Managed Services Market?

The GCC Managed Services Market size is expected to reach USD 12.35 billion in 2026 and grow at a CAGR of 8.84% to reach USD 18.87 billion by 2031.

What is the current GCC Managed Services Market size?

In 2026, the GCC Managed Services Market size is expected to reach USD 12.35 billion.

Who are the key players in GCC Managed Services Market?

Etihad Etisalat Co. (Mobily), AGC Networks (An ESSAR Company), EITC Group (du), Saudi Telecom Company and IBM Corporation are the major companies operating in the GCC Managed Services Market.

What years does this GCC Managed Services Market cover, and what was the market size in 2025?

In 2025, the GCC Managed Services Market size was estimated at USD 12.35 billion. The report covers the GCC Managed Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the GCC Managed Services Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: