GCC Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

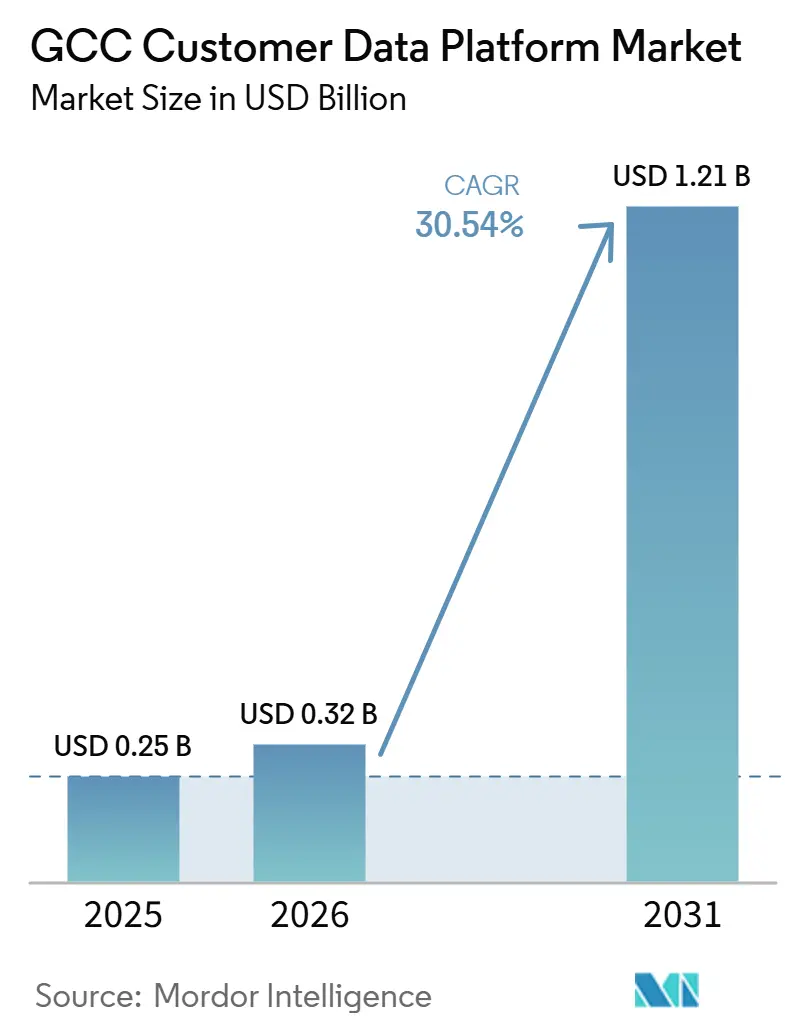

| Base Year Market Size (2025) | USD 0.25 Billion |

| Market Size (2026) | USD 0.32 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 30.54% CAGR |

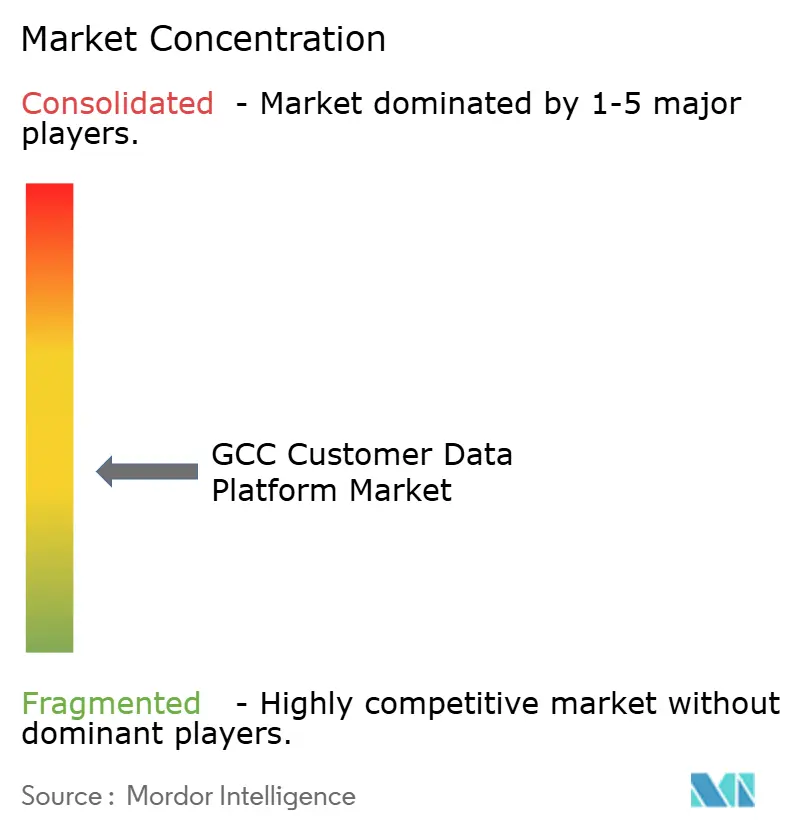

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Customer Data Platform Market Analysis by Mordor Intelligence

The GCC customer data platform market size is expected to increase from USD 0.25 billion in 2025 to USD 0.32 billion in 2026 and reach USD 1.21 billion by 2031, growing at a CAGR of 30.54% over 2026-2031. Growth in the GCC customer data platform market is being supported by retail digitization, mobile-first banking adoption, stronger data governance enforcement, and wider enterprise cloud readiness across the region. Demand is also rising because many enterprises still manage customer data in disconnected CRM, ERP, commerce, and service systems, which limits the value of their existing AI and customer engagement investments. The GCC customer data platform market is also moving through a net-new deployment cycle, where buyers are not replacing mature stacks at scale but instead building governed first-party data layers for the first time. This creates space for platform vendors, cloud partners, and service providers to shorten implementation cycles, support data residency requirements, and improve activation across Arabic- and English-language customer journeys. The main drag on the market remains execution, because integration complexity and the shortage of specialized operating talent can delay time to value even when software demand is strong.

Key Report Takeaways

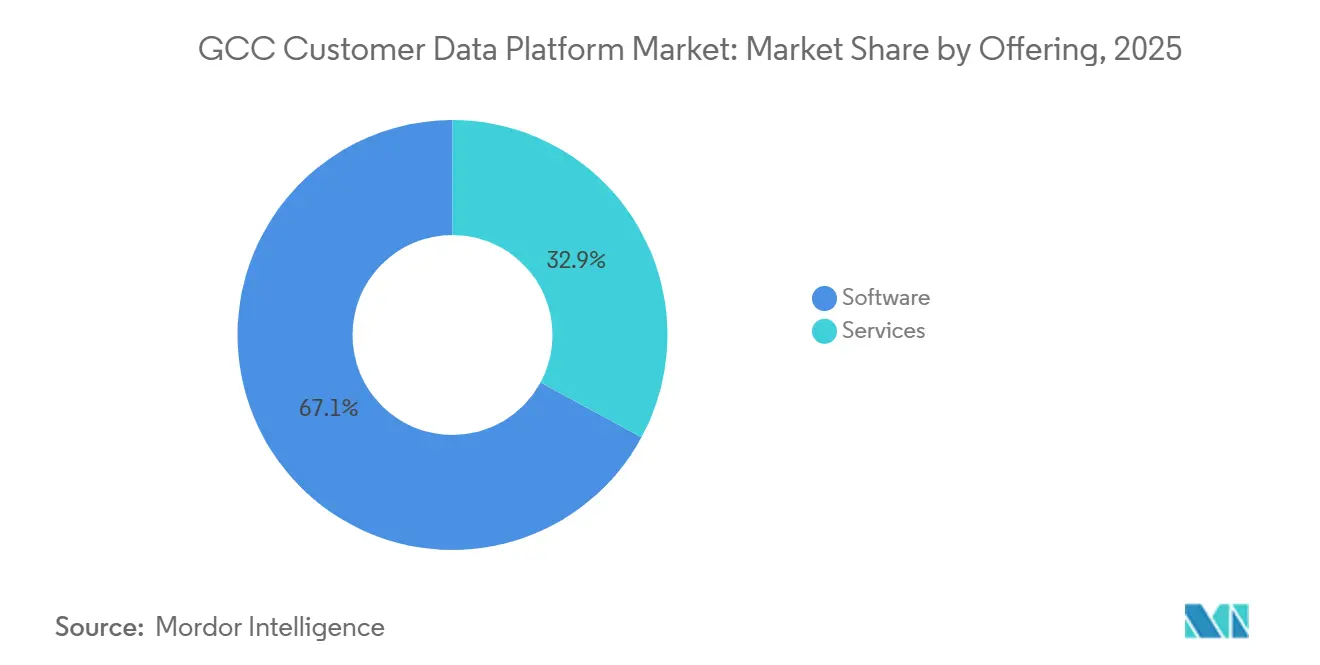

- By offering, software held 67.11% of the GCC customer data platform market revenue in 2025, while services are projected to expand at a 33.72% CAGR through 2031.

- By deployment mode, cloud accounted for 59.18% of the GCC customer data platform market share in 2025 and is projected to advance at a 32.89% CAGR through 2031.

- By organization size, large enterprises captured 70.12% of the GCC customer data platform market revenue in 2025, while SMEs are expected to record the highest CAGR at 33.41% through 2031.

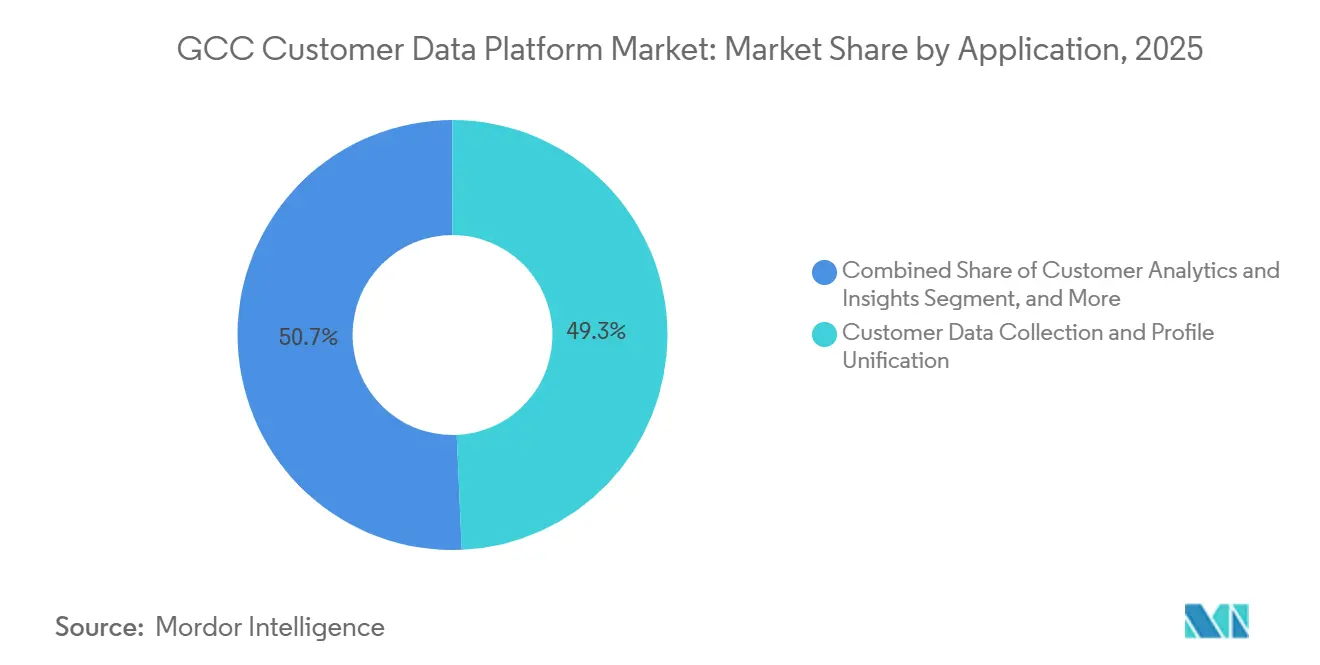

- By application, customer data collection and profile unification represented 49.31% of the GCC customer data platform market revenue in 2025, while audience segmentation and personalization are projected to expand at a 32.56% CAGR through 2031.

- By end-user industry, retail and e-commerce held 28.12% share in 2025, while BFSI is expected to grow fastest at a 31.87% CAGR through 2031.

- By geography, Saudi Arabia accounted for 37.66% share of the GCC customer data platform market size in 2025, while the UAE is projected to expand at a 32.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unified Customer Profiles Across Channels | +5.8% | GCC-wide, with stronger concentration in Saudi Arabia and the UAE | Short term (≤ 2 years) |

| AI-Led Real-Time Personalization in Retail, BFSI, and Telecom | +5.2% | GCC-wide, with stronger use cases in UAE retail and Saudi BFSI | Medium term (2-4 years) |

| Cloud Migration of Customer Engagement and Data Infrastructure | +4.6% | Saudi Arabia and the UAE lead, with Qatar also accelerating | Medium term (2-4 years) |

| Privacy-First MarTech Stack Rebuilds | +4.1% | Saudi Arabia and the UAE | Medium term (2-4 years) |

| First-Party Data Capture After Cookie Deprecation | +3.3% | Broad regional relevance, with greater impact in the UAE and Saudi Arabia | Short term (≤ 2 years) |

| Cross-Border Data Residency and Consent Orchestration Complexity | +2.1% | Saudi Arabia first, with spillover relevance across other GCC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Unified Customer Profiles Across Channels

Enterprises across the GCC customer data platform market are now serving customers through websites, mobile apps, social channels, call centers, messaging platforms, and stores, but many still do not maintain one persistent customer record across those touchpoints. That gap makes personalization harder, slows campaign response rates, and reduces the value of the customer signals already being generated across payments, commerce, service, and loyalty systems. The need is becoming more urgent as digital interaction volumes continue to rise, while brand expectations for continuity and relevance are becoming stricter across retail, banking, and telecom. In the GCC customer data platform market, this pushes CDP spending closer to core operating budgets, because a unified profile is increasingly seen as the base layer for AI activation, consent tracking, and customer journey management. The driver is strongest where enterprises already have broad digital reach and large first-party data flows, which is why the GCC customer data platform market continues to see early intensity in Saudi Arabia and the UAE.

AI-Powered Real-Time Personalization in Retail, BFSI, and Telecom

The GCC customer data platform market is also being boosted by the shift from batch marketing workflows to real-time decisioning, where offers, service prompts, and audience actions must respond instantly to live customer behavior. That shift matters because older CRM and campaign tools were not built to unify event data fast enough for always-on activation across commerce, payments, service, and media channels. Telecom transformation programs in the region are moving in the same direction, with customer-facing systems being rebuilt around omnichannel visibility and next-best-action logic rather than delayed reporting cycles. In the GCC customer data platform market, this expansion of demand extends beyond marketing teams, as real-time customer context is now relevant for service operations, digital sales, retention, and customer experience programs at enterprise scale. The result is a stronger business case for CDP deployments that can connect data ingestion, identity resolution, segmentation, and activation without long manual handoffs.

Cloud Migration of Customer Engagement and Data Infrastructure

The GCC customer data platform market is benefiting from enterprise cloud migration, as most modern CDP architectures perform best when data collection, identity processing, analytics, and activation are designed for cloud-native environments. This matters because cloud migration not only reduces infrastructure friction, but it also encourages buyers to rethink how customer data flows across ERP, commerce, service, and marketing systems. Large modernization programs in the region are reinforcing that pattern, as companies rebuilding their core enterprise systems are also creating the technical conditions for unified customer data layers to follow. In the GCC customer data platform market, cloud readiness also weakens the older argument for keeping fragmented customer records inside isolated business tools, because sovereign and in-country hosting options have improved. As a result, cloud migration is not just a supporting trend; it is directly reshaping procurement timing, deployment design, and the scale of potential activation use cases.

Privacy-First MarTech Stack Rebuilds Across GCC Enterprises

The GCC customer data platform market is being shaped by a privacy-first rebuild of marketing and customer engagement stacks, especially where enterprises now need stronger consent governance, clearer data lineage, and tighter control over data movement. Saudi Arabia’s Personal Data Protection Law has moved from a policy concern to an operating requirement, increasing demand for governed profile management, consent handling, and compliant activation workflows.[1]Saudi Data and AI Authority, “Personal Data Protection Law and Implementing Regulations,” Saudi Data and AI Authority, dgp.sdaia.gov.sa The UAE’s personal data protection framework is driving a similar response, particularly among enterprises that manage sensitive customer records and need clearer controls over collection, storage, and processing. Vendor strategy is aligning with this shift, as shown by Salesforce’s USD 500 million investment in Saudi Arabia, which included local infrastructure commitments and a compliance-led architecture approach for the Kingdom. In the GCC customer data platform market, this means procurement is increasingly supported not only by marketing use cases, but also by IT, legal, governance, and risk priorities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy CRM, ERP, and Data Warehouses | -4.2% | GCC-wide, most acute in Saudi Arabia and the UAE | Medium term (2-4 years) |

| Limited Internal CDP Talent and Operating Maturity | -3.6% | GCC-wide, with sharper pressure in Oman, Kuwait, and Bahrain | Medium term (2-4 years) |

| Compliance Sensitivity Around Data Localization and Customer Consent | -3.1% | Saudi Arabia first, with spillover into other regulated markets | Long term (≥ 4 years) |

| High Implementation and Change Management Burden for Mid-Sized Buyers | -2.4% | GCC-wide, with concentration in Saudi Arabia and the UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity With Legacy CRM, ERP, and Data Warehouses

The largest delivery obstacle in the GCC customer data platform market remains integration, because many buyers still run tightly coupled legacy estates that were not built for real-time identity stitching or event-based data exchange. That problem becomes more severe when profile creation depends on data from ERP, CRM, commerce, service, loyalty, analytics, and middleware systems that each use different models, update cycles, and governance rules. Survey evidence on ERP modernization shows that integration strain remains common, especially when organizations lack centralized integration capabilities and lose consistency across critical system connections. In the GCC customer data platform market, multi-country operations add another layer of difficulty because enterprises often have to align customer data handling across several jurisdictions while still preserving local system requirements. When that work is underestimated, implementation timelines expand, service costs rise, and the commercial benefits of activation use cases are pushed further out.

Limited Internal CDP Talent and Operating Maturity

The GCC customer data platform market also faces a talent constraint, as identity resolution, audience design, consent operations, and real-time customer activation require a mix of technical and commercial skills that many organizations still lack in-house. This shortfall matters after software goes live, because value depends on disciplined data stewardship, strong use-case prioritization, and regular optimization rather than on installation alone. The region is responding with formal upskilling initiatives, including Salesforce’s commitment to train 30,000 Saudi citizens in AI-related skills under its Saudi Arabia investment program. Even so, the operating bench remains deeper in Riyadh and Dubai than in several smaller GCC markets, which means outside partners still carry a large share of implementation, orchestration, and support work. In the GCC customer data platform market, this tends to widen the gap between software purchase and realized business outcomes, especially during the first year of deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Growth is Changing How Buyers Define Value

Software accounted for 67.11% of revenue in 2025, indicating that the GCC customer data platform market initially expanded through foundational platform purchases by large enterprises seeking to secure core data unification and activation capabilities before fully redesigning operating processes. That lead remained important because large retail groups, banks, and telecom operators needed enterprise-grade platforms that could integrate high data volumes, support governance controls, and connect with existing digital engagement stacks. Services, however, are projected to expand at a 33.72% CAGR through 2031, making them the fastest-growing segment of the GCC customer data platform market as buyers seek help with deployment, integration, orchestration, and ongoing activation. This shift reflects a practical reality, because many organizations are willing to buy software, but fewer can move quickly without outside support across data modeling, use-case rollout, consent design, and cross-functional governance. The balance between software and services, therefore, says less about weak platform demand and more about the market’s stage of execution maturity.

That pattern also suggests a change in what enterprise buyers now consider a successful purchase inside the GCC customer data platform market. Early adoption favored license-led buying, where the priority was platform access and internal capability building, but the next phase is increasingly tied to measurable delivery outcomes and faster use-case launch. In the customer data platform industry, this often marks the point at which managed services attachments rise, as buyers seek to reduce internal bottlenecks without slowing deployment. It also means vendors that pair platform breadth with stronger delivery frameworks can gain an advantage, especially when projects span identity resolution, consent control, campaign activation, and customer analytics in parallel. The stronger outlook for services, therefore, reflects a broader shift from capability acquisition to operational execution in the GCC customer data platform market.

By Deployment Mode: Cloud Leadership is Strengthening Under Sovereignty Rules

Cloud accounted for 59.18% of revenue in 2025 and is projected to post a 32.89% CAGR through 2031, confirming that cloud is both the leading and fastest-growing deployment approach in the GCC customer data platform market. This position reflects improved regional cloud infrastructure, stronger acceptance of hosted enterprise software, and the growing mismatch between modern CDP requirements and older on-premises-first operating models. Buyers increasingly want scalable ingestion, flexible identity processing, and easier activation across multiple customer touchpoints, and those needs are better aligned with cloud-based architectures. At the same time, cloud adoption in the GCC customer data platform market is not a simple public cloud story, because many buyers still need clear sovereignty safeguards, in-country controls, and tighter governance around sensitive customer records. That is why cloud dominance is intensifying even as deployment design is becoming more selective and regulated.

On-premises environments still matter, but they now tend to remain in place where existing institutional controls are difficult to unwind quickly, particularly in highly regulated settings with long system lifecycles. Hybrid deployment is therefore acting as a transition model for enterprises that want to connect legacy stores of customer data with newer activation layers without forcing a full redesign at once. In the customer data platform industry, this usually signals that the market is moving from infrastructure debate toward architecture optimization, where the issue is not whether cloud will lead, but which cloud pattern best fits local control needs. The GCC customer data platform market is following that path, with sovereignty-aware cloud design becoming a practical differentiator rather than a secondary technical detail. This makes deployment mode a strategic buying choice tied to compliance, integration complexity, and future AI readiness, not simply a hosting decision.

By Organization Size: SME Demand is Expanding the Addressable Base

Large enterprises accounted for 70.12% of revenue in 2025, indicating that the GCC customer data platform market has been led to date by organizations with deeper data estates, larger digital budgets, and a stronger ability to absorb integration and change management costs. These buyers were the first to justify enterprise-grade CDP deployment because they already managed high interaction volumes across retail, financial services, telecom, and diversified service portfolios. SMEs, however, are forecast to grow at a 33.41% CAGR through 2031, which marks an important broadening of demand beyond the traditional large-account base. This rise suggests that the GCC customer data platform market is entering a more accessible phase, where pricing, packaging, and implementation models are beginning to suit companies previously excluded by complexity or contract size. The change is especially meaningful in a region where SMEs play a major role in non-oil activities and in digital commerce.

The SME opportunity is not uniform, because the most attractive buyers are those already operating multiple digital channels and collecting usable first-party customer data through commerce, service, and loyalty interactions. That is why demand is likely to build first in digitally active SME clusters, particularly in retail, food service, consumer-facing services, and online business models. Vendor actions are also helping reduce entry barriers by offering simplified AI-enabled packages and lower setup friction, improving feasibility for smaller organizations.[2]Salesforce, “Salesforce Invests $500M in Saudi Arabia,” Salesforce, salesforce.com In the GCC customer data platform market, this expanding SME base matters because it diversifies the revenue pool and reduces long-term dependence on a relatively limited set of very large enterprise accounts. It also creates room for lighter deployment models, managed activation services, and more modular platforms that can scale with business maturity rather than requiring full enterprise architecture from day 1.

By Application: Profile Unification Still Leads, While Personalization Gains Speed

Customer data collection and profile unification accounted for 49.31% of the application segment in 2025, indicating that foundational data work remained the largest use case in the GCC customer data platform market. Enterprises continued to prioritize identity stitching, record consolidation, and persistent customer views because these functions are necessary before any meaningful cross-channel activation can happen. Audience segmentation and personalization are projected to grow at a 32.56% CAGR through 2031, indicating that buyers are now moving more quickly from foundational setup to live commercial use cases. In practical terms, the GCC customer data platform market is no longer focused solely on building a single customer record; it is increasingly focused on using that record for relevance, timing, suppression, and journey control across channels. This transition indicates that many organizations are progressing from data assembly to data activation faster than earlier regional adoption patterns suggested.

Other applications are also becoming more important as deployments mature and teams gain confidence in using governed data outside the first implementation phase. Campaign orchestration and customer analytics sit in the middle of that progression, because they depend on the same profile foundation but require broader organizational coordination to convert insight into repeatable action. Consent and preference management remains smaller today, yet it carries notable upside as privacy obligations become more deeply embedded in day-to-day operations across the GCC customer data platform market. That makes application development more sequential than fragmented, with unification first, activation second, and governance-rich optimization following close behind. The segment, therefore, shows a market that is still building its base while also beginning to capture more immediate commercial returns from it.

By End-User Industry: Retail Drives Volume, While BFSI Sets the Growth Pace

Retail and e-commerce accounted for 28.12% of revenue in 2025, making the sector the largest end-user segment in the GCC customer data platform market, as it combines high transaction frequency, broad customer reach, and clear returns from personalization. Retailers typically manage dense streams of browsing, payment, basket, store, loyalty, and service data, which creates a strong business case for profile unification and coordinated activation. BFSI is projected to expand at a 31.87% CAGR through 2031, making financial institutions the fastest-growing vertical in the GCC customer data platform market as digital banking, remote onboarding, and mobile service models intensify the need for governed customer context. This growth is being supported by the shift away from branch-led engagement toward continuous digital interaction, where timely personalization and more coherent customer journeys matter across acquisition, servicing, and retention. The vertical split, therefore, shows one segment leading on scale and another leading on acceleration.

Healthcare, telecom, and public-sector use cases follow a different pattern because their customer data environments are often more regulated, more operationally sensitive, and slower to move through procurement. That does not reduce their relevance, because these sectors hold rich identity-linked data and have strong long-term reasons to improve orchestration, service continuity, and governed engagement. Telecom is especially important in the GCC customer data platform market because operators hold deterministic subscriber data that can support highly accurate customer views across channels and services. Government-related adoption is still earlier, but digital citizen service programs are starting to align with the same underlying need for more consistent records and better journey management. The end-user mix therefore reinforces that the GCC customer data platform market is expanding first where commercial returns are fastest, while regulated sectors build a slower but durable second wave.

Geography Analysis

Saudi Arabia accounted for 37.66% of revenue in 2025, giving it the largest position in the GCC customer data platform market and confirming its role as the region’s primary center for enterprise-scale adoption. That lead reflects the Kingdom’s large enterprise base, its broad digital economy agenda, and the stronger operating effect of data governance requirements that now shape how customer information can be managed and activated. The GCC customer data platform market in Saudi Arabia is also supported by large sector opportunities in retail, BFSI, telecom, healthcare, and public services, where digital modernization programs are already in motion. Salesforce’s Saudi Arabia investment further underlines the country’s strategic importance, because global vendors are pairing market development with local infrastructure and skills commitments rather than treating compliance as a secondary issue. Saudi Arabia, therefore, leads not only because it is large, but also because policy, enterprise demand, and vendor strategy are more closely aligned than in most neighboring markets.

The UAE is projected to record a 32.12% CAGR through 2031, making it the fastest-growing geography in the GCC customer data platform market. Its strength comes from a mature digital commerce base, a strong fintech ecosystem, a high concentration of regional headquarters, and a faster pace of enterprise software adoption in customer-facing sectors. The UAE also benefits from established hosted infrastructure options and a regulatory environment that is pushing enterprises to manage personal data more deliberately across collection, storage, and usage practices.[3]Government of the United Arab Emirates, “Federal Decree by Law No. 45 of 2021 Concerning the Protection of Personal Data,” UAE Legislation Portal, uaelegislation.gov.ae Geographically, the UAE combined forecast growth of 32.12% with a high-value demand profile, while Saudi Arabia held 37.66% of the GCC customer data platform market share in 2025. That combination means the GCC customer data platform market is anchored by Saudi scale and accelerated by UAE speed.

Qatar, Kuwait, Oman, and Bahrain together form a smaller but steadily expanding part of the GCC customer data platform market. Demand in these markets is supported by financial services digitization, retail modernization, and national digital economy programs, even though project sizes are smaller and partner capacity is thinner than in Riyadh or Dubai. Their common challenge is not a lack of use cases, but a narrower pool of specialist implementation resources, which can slow deployment even when enterprise intent is clear. This gives the larger GCC hubs an ecosystem advantage, as many regional service partners, cloud specialists, and enterprise software teams remain concentrated there. Over time, the GCC customer data platform market across these smaller countries is likely to deepen as infrastructure, skills, and proven deployment models spread more evenly across the region.

Competitive Landscape

The GCC customer data platform market is moderately fragmented, with global enterprise software vendors holding a strong position in large-account procurement, while specialist platforms and regional entrants continue to prevent tight concentration across the full buyer base. Large enterprises often favor broad suites because they want CDP functions connected with CRM, commerce, analytics, and service environments rather than purchased as stand-alone tools. At the same time, the GCC customer data platform market still leaves room for smaller and more specialized providers that can offer faster deployment, more flexible architecture, or stronger localization for Arabic-language and compliance-sensitive use cases. This is why competitive intensity is strongest in the upper enterprise tier, while the mid-market remains more open to packaging innovation and services-led differentiation. The field is therefore not defined by a single vendor race, but by several parallel contests around infrastructure fit, delivery speed, localization, and ecosystem reach.

Salesforce has taken one of the clearest strategic positions in the GCC customer data platform market through its USD 500 million investment in Saudi Arabia, which linked market expansion with local compliance infrastructure, regional presence, and large-scale talent development. Oracle has also strengthened its standing by positioning its customer data capabilities within a broader enterprise application environment, appealing to buyers who want account, customer, service, and operational data connected through a single stack.[4]Oracle, “Oracle Named a Leader in the Gartner Magic Quadrant for Customer Data Platforms,” Oracle, oracle.com Another important competitive pattern is the rise of sovereignty-aware architecture, because vendors that can align platform delivery with local hosting, governance, and customer data control requirements are winning earlier consideration. In practice, the GCC customer data platform market now rewards companies that can answer compliance, integration, and operational questions before they start feature-level comparisons.

A second competitive layer is forming around implementation and orchestration capacity rather than software alone. Enterprise buyers increasingly want providers that can reduce deployment friction, connect legacy estates, and move from unified data to active use cases without long delays, which increases the value of strong partner ecosystems and technical delivery depth. Programs like the e& transformation led with Netcracker show how customer experience modernization and data unification are becoming more closely linked in the region’s enterprise environment. The GCC customer data platform market, therefore, remains open to both large-suite vendors and narrower specialists, but the winners are likely to be those that combine compliant infrastructure, practical deployment capabilities, and stronger localization to regional customer engagement patterns. That competitive structure supports steady rivalry without contradicting the market’s still-early adoption stage across several segments and geographies.

GCC Customer Data Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

Twilio Inc.

SAP SE

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Salesforce made Agentforce integration available across Salesforce Suites in the GCC, bringing enterprise-grade AI capabilities to SME customers at no additional cost, directly addressing the affordability barrier that had historically excluded sub-enterprise buyers from AI-powered CDP use cases across the Gulf region.

- April 2026: Oracle was named a Leader in the 2026 Gartner Magic Quadrant for Customer Data Platforms, with Oracle Fusion Cloud Unity Data Platform evaluated based on its ability to unify customer, account, and B2B commercial data from ERP, supply chain, and service sources in a single platform, a capability set aligned with GCC enterprise requirements.

- February 2025: Salesforce announced a USD 500 million investment in Saudi Arabia, unveiled at LEAP 2025, encompassing the Hyperforce deployment on AWS infrastructure to support local data residency compliance, a new regional headquarters in Riyadh, and a commitment to upskill 30,000 Saudi citizens in AI, including a partnership with Princess Nourah University.

- October 2025: Al-Futtaim and IBM completed a landmark SAP S/4HANA migration for Al-Futtaim Automotive to Microsoft Azure through RISE with SAP, described as one of the largest SAP transformations in the region. The unified digital core positions the division to introduce AI-powered customer engagement services and establishes the data infrastructure prerequisites for CDP integration.

GCC Customer Data Platform Market Report Scope

The GCC Customer Data Platform Market comprises platforms that aggregate and unify customer data across touchpoints to provide organizations with a comprehensive, actionable view of their customers. These solutions support audience segmentation, personalization, customer journey orchestration, analytics, and regulatory compliance across the Gulf Cooperation Council (GCC) countries. Increasing investments in customer experience technologies, digital commerce, and data-driven marketing initiatives drive the market. CDPs enable enterprises to improve customer engagement, marketing effectiveness, and revenue generation through centralized customer intelligence.

The GCC Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the GCC customer data platform market size through 2031?

The GCC customer data platform market size is projected to rise from USD 0.25 billion in 2025 to USD 0.32 billion in 2026 and reach USD 1.21 billion by 2031, at a 30.54% CAGR over 2026-2031.

Which country leads customer data platform demand in the GCC?

Saudi Arabia led with 37.66% share in 2025, supported by strong enterprise demand, digital economy investment, and tighter data governance enforcement.

Which GCC country is growing fastest for customer data platforms?

The UAE is projected to record the fastest growth, with a 32.12% CAGR through 2031, driven by strong digital commerce, fintech activity, and enterprise software adoption.

Which end-user sector is creating the largest revenue base?

Retail and e-commerce held the largest end-user share at 28.12% in 2025 because of high transaction frequency, rich customer data flows, and strong returns from personalization.

Which application area is expanding fastest across deployments?

Audience segmentation and personalization is the fastest-growing application, with a 32.56% CAGR through 2031, as enterprises move from profile building into real-time activation.

What is the main obstacle slowing enterprise rollout?

Integration with legacy CRM, ERP, and data warehouse systems remains the biggest restraint, because it lengthens implementation timelines, raises services costs, and delays business value realization.

Page last updated on: