Germany Self Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

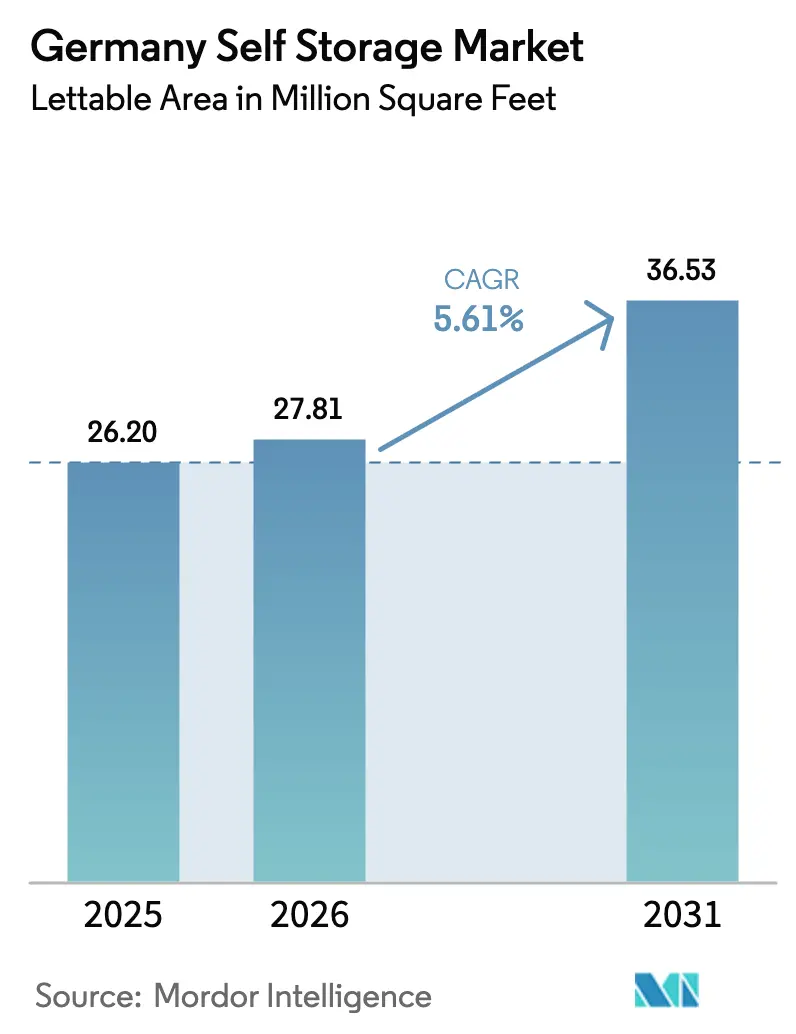

| Base Year Market Size (2025) | 26.20 Million square feet |

| Market Volume (2026) | 27.81 Million square feet |

| Market Volume (2031) | 36.53 Million square feet |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Self Storage Market Analysis by Mordor Intelligence

The Germany self storage market size is expected to increase from 26.2 million square feet in 2025 to 27.81 million square feet in 2026 and reach 36.53 million square feet by 2031, growing at a CAGR of 5.61% over 2026-2031. Shrinking apartment footprints, a rising share of single-person households, and sustained institutional capital inflows are anchoring this growth trajectory. Households in Berlin, Munich, and Hamburg are externalizing possessions to offset the high cost of urban floor space, while small online sellers rely on self-storage bays as micro-fulfillment nodes to shave last-mile delivery costs. Investors view the asset class as a defensive hedge, funding rapid conversions of obsolete industrial stock into multi-level, tech-enabled stores. Facility operators are layering digital access, concierge logistics, and value-added insurance bundles to lift revenue per square foot even as competition intensifies across both primary and secondary cities.

Key Report Takeaways

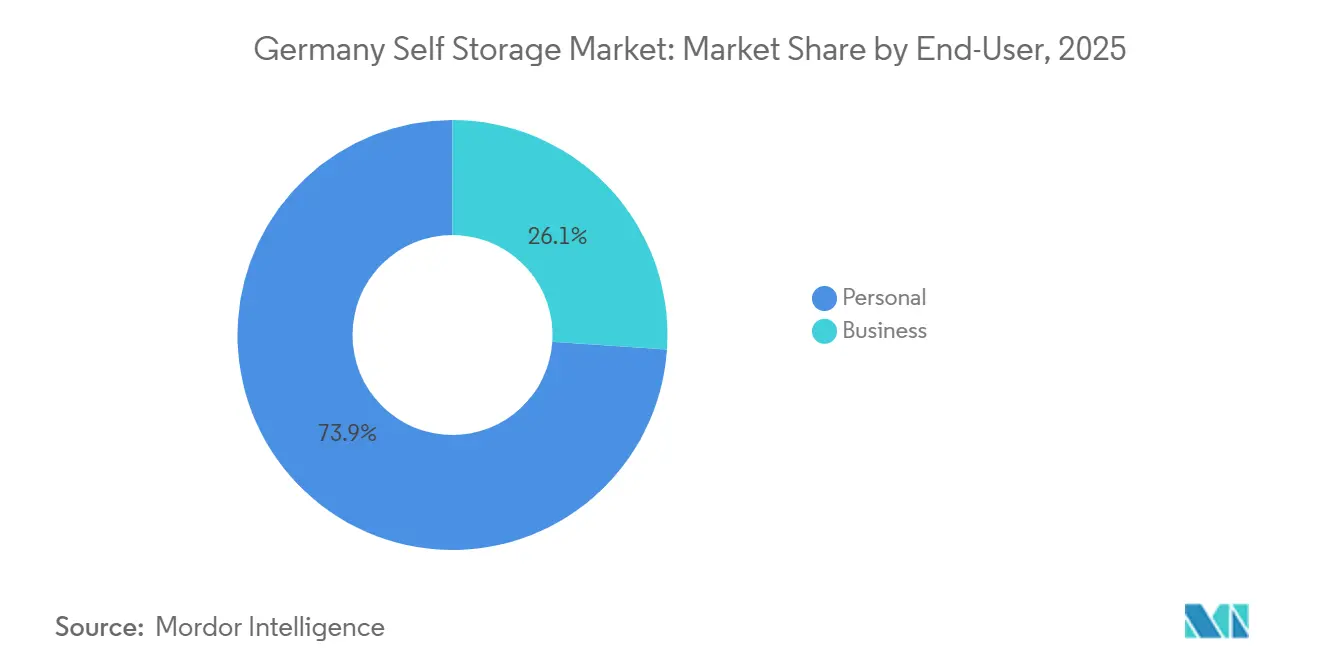

- By end-user, personal renters accounted for 73.92% of Germany self storage market share in 2025, while the business segment is expanding at a 6.37% CAGR through 2031.

- By storage size, small and medium units captured 47.34% share of Germany self storage market size in 2025, whereas large bays above 40 square feet are projected to advance at a 5.84% CAGR through 2031.

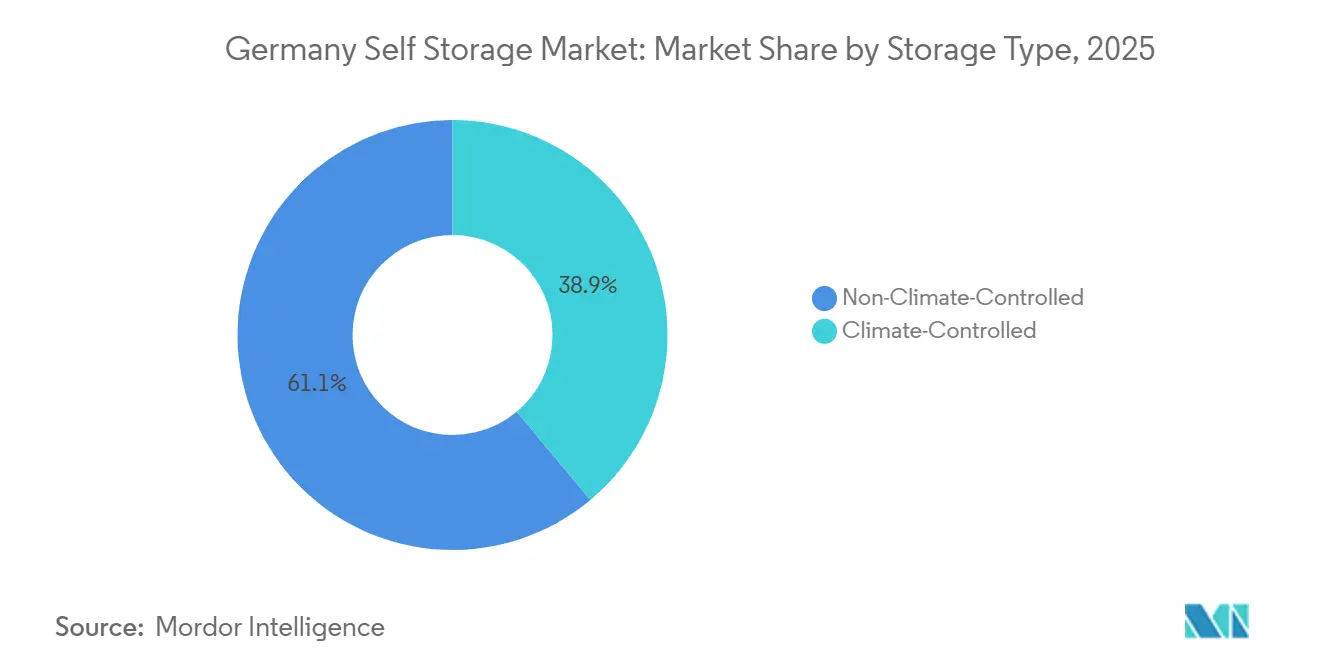

- By storage type, non-climate units represented 61.09% of Germany self storage market size in 2025 and climate-controlled space is accelerating at a 6.01% CAGR over 2026-2031.

- By ownership pattern, owned facilities held 67.13% share of Germany self-storage market size in 2025, yet leased formats are poised to grow at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Self Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and Shrinking Average Dwelling Size | +1.2% | Berlin, Munich, Hamburg, Frankfurt, Cologne | Medium term (2-4 years) |

| Growth in E-Commerce and SME Inventory Requirements | +1.4% | Rhine-Ruhr logistics arc and greater Berlin | Short term (≤ 2 years) |

| Investor Appetite and Institutional Capital Driving Rapid Facility Expansion | +1.1% | Tier-1 metros and select autobahn-linked tier-2 cities | Long term (≥ 4 years) |

| Accelerating Residential Mobility Among Students and Professionals | +0.9% | Major university hubs | Medium term (2-4 years) |

| Corporate Archiving Mandates Boosting Off-Site Document Storage | +0.5% | Financial-legal centers | Long term (≥ 4 years) |

| Smart-Lock and App-Based 24/7 Access Enabling Unmanned Micro-Stores | +0.6% | Emerging tier-2 corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanization and Shrinking Average Dwelling Size

Germany’s sustained urban migration is compressing per-capita living area, triggering a structural hand-off of surplus belongings to external facilities. Single-person households reached 41.9% of total dwellings in 2024, while average new-build apartment sizes fell by roughly 3 square meters during 2020-2024.[1]Federal Statistical Office of Germany, “Living Area and Household Statistics 2024,” DESTATIS.DE Berlin and Munich command rent premiums above EUR 20 (USD 21.4) per square meter, nudging tenants to treat self-storage as an affordable annex.[2]Deutsche Bank Research, “German Real Estate Market Report 2024-2025,” DBRESEARCH.COM Operators are bundling concierge retrieval, digital inventories, and insurance to lock customers into multi-year contracts. Longer dwell durations lift occupancy stability and let owners pass through inflation-linked escalators, a pattern that underpins the resilience of the Germany self-storage market. With room sizes set to tighten further under municipal densification plans, demand visibility on this driver remains high through at least 2030.

Growth in E-Commerce and SME Inventory Requirements

E-commerce penetration hit 15.1% of German retail sales in 2024 and parcel throughput topped 4.3 billion consignments.[3]OECD, “E-Commerce Statistics and Trends 2024,” OECD.ORG, Parcel Perform, “Germany Parcel Delivery Market Analysis 2024,” PARCELPERFORM.COM Small merchants that lack dedicated warehouses are leasing storage bays near autobahn interchanges to stage fast-moving SKUs for next-day dispatch. Rhine-Ruhr operators outfitting units with pallet racking and loading docks command double-digit rent premiums and near-full occupancy, reinforcing the short-cycle growth of the Germany self-storage market. Business tenants’ willingness to pay for operational features helps balance seasonal volatility in personal demand and provides upside for revenue-management systems that price space by hourly access rather than static square footage.

Investor Appetite and Institutional Capital Driving Rapid Facility Expansion

Blackstone’s EUR 100 million (USD 107 million) injection into Lagerbox during 2024 signaled a step-change in private-equity conviction. Shurgard disclosed German net-operating-income margins above 70% in its 2024 report.[4]Shurgard Self-Storage SA, “Annual Report 2024,” SHURGARD.COM Heitman has earmarked more than USD 200 million for European self-storage allocations, with Germany as its single-largest exposure. Institutional liquidity is accelerating brownfield conversions, installing solar PV arrays, and scaling digital access to protect operating margins. While this funding wave intensifies competitive pressure, it also validates the Germany self-storage market as an institutional core-plus real-estate niche, underpinning longer-term capacity build-outs that will shape supply-demand balances well beyond 2031.

Accelerating Residential Mobility Among Students and Professionals

University enrollment reached 2.95 million students in the 2024-2025 academic year, with international cohorts at 14%. Simultaneously, intra-German corporate relocations in knowledge industries rose 8% year-over-year in 2024. Semester transitions and job moves spike short-term bookings, pushing occupancy above 90% in Munich, Berlin, and Heidelberg during peak months. Operators deploy dynamic pricing to smooth seasonality, pushing higher daily rates for three-month leases and offering digital onboarding that cuts administration overhead. Leased models flourish in university towns where capital-light conversions of retail space allow rapid reaction to dorm-vacancy cycles, reinforcing the agile supply posture of the Germany self-storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restrictive Zoning and Lengthy Planning Approvals | -0.8% | Bavaria, Baden-Württemberg, historic cores | Long term (≥ 4 years) |

| Escalating Urban Land and Construction Costs | -0.7% | Berlin, Munich, Hamburg, Frankfurt | Medium term (2-4 years) |

| Intensifying Competition from On-Demand Mobile Storage Start-Ups | -0.4% | Berlin, Hamburg, Cologne | Short term (≤ 2 years) |

| Stricter ESG Retrofit Requirements Inflating CapEx Budgets | -0.5% | Nationwide, 2027-2028 compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Restrictive Zoning and Lengthy Planning Approvals

Germany’s Baugesetzbuch framework excludes self-storage from many mixed-use zones, pushing developers to outlying industrial parcels. In Bavaria, approvals for greenfield facilities stretch 18-24 months due to mandatory impact assessments and community hearings. Heritage overlays in Berlin and Hamburg bar façade changes, stalling adaptive-reuse opportunities. Carrying costs during protracted entitlements erode returns and favor deep-pocketed investors that can warehouse land, hampering the organic scaling pace of the Germany self-storage market. Smaller entrants instead gravitate toward leased conversions where zoning hurdles are lower, but those sites often lack prime visibility and must rely on digital marketing to capture demand.

Escalating Urban Land and Construction Costs

Prime industrial plots near gateway autobahns cost upward of EUR 800 (USD 856) per square meter in Munich and Frankfurt, while 2024 steel and concrete input prices climbed 18% and 14% respectively. Development underwriting now assumes higher stabilized rents to offset cap-rate compression, narrowing the field of feasible projects. Operators adopting modular steel frames shave build cycles by months, and hedge commodity exposure, but most regional players lack procurement scale. Elevated capital intensity slows new-supply additions, supporting sustained occupancy and pricing power yet placing a ceiling on how quickly the Germany self-storage market can absorb latent demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Personal Demand Anchors Market, Business Segment Accelerates

Personal tenants occupied 73.92% of capacity in 2025, underscoring how the Germany self-storage market evolved as a household space-extension solution. Urban renters store seasonal sports gear, archived memorabilia, and heirloom furniture, often treating external units as semi-permanent home annexes. Operators have responded with curated insurance, item-level barcoding, and 24/7 smartphone-based entry, ensuring that personal demand remains a stable revenue pillar despite modest growth. Business users, although currently smaller, are scaling at a 6.37% CAGR, reflecting e-commerce sellers, trades contractors, and professional-services firms archiving client files. Shurgard notes that corporate renters deliver 28% of German revenue while occupying 22% of square footage, highlighting stronger yield potential.

Over the forecast horizon, personal demand growth moderates but remains structurally supported by urban densification and demographic churn. Facility operators segment buildings by floor, dedicating ground-level and drive-up bays to SMEs shipping palletized inventory daily, while upper floors cater to households that access units only a few times per year. This spatial stratification maximizes revenue per square foot and balances peak usage loads, a tactic increasingly critical as the Germany self-storage industry integrates dynamic pricing engines. Business occupants reinforce weekday traffic and raise ancillary-service uptake, such as receipt-handling and parcel dispatch, thereby diversifying income streams beyond pure rent.

By Storage Size: Compact Units Dominate, Large Bays Gain Share

Units below 40 square feet held 47.34% of total inventory in 2025, mirroring tight urban living but also benefiting from high turnover that enables granular repricing. Large bays above 40 square feet enjoy a faster 5.84% CAGR because SMEs need pallet-racked space close to urban delivery corridors. Sensorberg-enabled smart locks now allow unmanned control of oversized units, streamlining access for van drivers and reducing security overhead. Operators retrofit older layouts, removing internal walls to stitch together contiguous zones that appeal to commercial renters with variable inventory volumes.

Larger bays deliver superior absolute monthly rent even though square-foot rates moderate slightly, lifting facility-level NOI where enterprise adoption is rising. Conversely, micro-lockers and double-stacked configurations are flourishing as courier drop-boxes in dense neighborhoods, underlying the versatility of sizing strategies within the Germany self-storage market. Owners leverage modular partitions to pivot between size mixes according to quarterly demand signals captured via IoT occupancy sensors, creating a nimble asset base that can capture both personal downsizing waves and business inventory bursts.

By Storage Type: Non-Climate Units Lead, Climate-Controlled Segment Surges

Non-climate rooms comprised 61.09% of footprint in 2025, favored for durable household items and budget-sensitive customers. Temperature-regulated suites, at 38.91% share, outpace overall growth at 6.01% annually as pharmaceutical distributors, vintage-wine collectors, and electronics retailers seek strict humidity and temperature bands. Germany’s Medicinal Products Act imposes 15 °C-25 °C thresholds on several drug classes, prompting distributors to sign multi-year leases in facilities certified to Good Distribution Practice standards. Electronics merchants, confronting tight working-capital cycles, now buffer seasonal stock in climate-controlled rooms adjoining last-mile hubs near Cologne Bonn Airport, paying double the national median rent.

Operators justify capital-intensive HVAC retrofits by commanding premiums of EUR 20-30 (USD 21.4-32.1) per square meter that enhance paybacks even as ESG rules tighten. Germany’s Building Energy Act forces pre-2025 facilities to upgrade insulation and systems by 2028, but early movers can market energy-efficient credentials and secure sustainability-focused corporate tenants. Consequently, climate capacity will likely breach 45% of the Germany self-storage market size before 2031, moving the asset class closer to U.S. specification standards.

By Ownership Pattern: Owned Models Prevail, Leased Formats Gain Traction

Owned assets represented 67.13% of capacity in 2025, mirroring the preference of REITs and private equity for fee-simple control and inflation-hedged land appreciation. Leased configurations expand at 6.12% annually, unlocking quicker market entries for regional chains that lack deep balance sheets. In Nuremberg and Dresden, landlords agree to 15-year triple-net leases in exchange for tenant-funded capital spend, offering spreads that make up for absence of land upside. Sensor-enabled unmanned tech removes onsite staffing, allowing leased facilities to match per-foot margins of owned counterparts even after rent outflows.

Institutional groups chase trophy sites in Berlin’s industrial belts, bidding up valuations and compressing yields. Smaller players pivot to adaptive-reuse of under-occupied retail stores on the periphery of tier-1 metro areas, sidestepping rezoning bottlenecks. The resulting barbell structure, capital-intensive flagships versus agile leaseholds, gives the Germany self-storage market a diversified ownership tapestry that can accommodate both yield-hungry funds and entrepreneurial newcomers.

Geography Analysis

Germany’s five largest metros, Berlin, Munich, Hamburg, Frankfurt, and Cologne, account for roughly 55-60% of installed capacity, underpinning the primacy of densely inhabited urban corridors. Berlin leads in absolute square footage, propelled by a 3.7 million population and a burgeoning technology scene that feeds both personal and SME demand. Munich commands the sector’s highest effective rents, pricing units 15-20% above national averages, a premium justified by land scarcity and high household purchasing power. Hamburg’s seaport logistics cluster attracts import-export firms that use self-storage to buffer trans-shipment inventory, embedding commercial resilience into the Germany self storage market.

Tier-2 cities such as Leipzig, Hanover, Nuremberg, Dresden, and Stuttgart are the next frontier. Zoning approvals finalize faster, build-cost bases are lower, and facility density remains a fraction of tier-1 levels. Sirius Real Estate reported 88% mean occupancy across its tier-2 assets in 2024, only 4-percentage points under Berlin’s figure, affirming latent depth outside primary metros. Operators deploy smart-lock-enabled unmanned facilities to maintain tight cost structures where walk-in demand lags. Digital-first marketing, including Google-maps integrated booking engines, substitutes for roadside visibility and delivers customer acquisition costs below EUR 50 (USD 53.5) per tenant.

Exurban and rural belts remain thinly penetrated, yet commuter towns circling Frankfurt and Munich are developing micro-needs as dual-income households downsize to energy-efficient apartments. Modular steel-frame boxes erected on vacant parking lots meet these suburban pockets quickly at sub-EUR 400 (USD 428) per square-meter build costs. However, longer lease-up timelines and heavier reliance on digital discovery raise break-even risk. Operators evaluating greenfield expansion therefore triangulate local dwelling size trends, e-commerce parcel density, and competitor storefront counts before committing capital, ensuring new supply aligns tightly with demonstrated regional liquidity.

Competitive Landscape

The top five operators, Shurgard, MyPlace (Lagerbox), HOMEBOX, Pickens, and Space Plus, control an estimated 35-40% of national capacity, reflecting moderate concentration that still leaves plenty of fragmentation. Shurgard’s 54-site German network leverages pan-European scale to negotiate digital advertising and insurance discounts, reinforcing its first-mover edge. MyPlace and Lagerbox, backed by Blackstone, concentrate on flagship locations within A-class logistics rings, fortifying brand visibility and enabling pricing power in Germany self storage market hotspots.

Regional specialists thrive by tailoring service to hyper-local needs, offering staff-assisted moves, multilingual support, and flexible contracts for students. Pickens’ tie-up with Sensorberg reduced on-site staffing by 30% and funneled savings into social-media campaigns targeting millennial renters. HOMEBOX’s Cologne launch showcased climate-controlled high-bay racking that attracts pharmaceutical distributors willing to sign three-year terms at 25% rent premiums.

Mobile-storage entrants disrupt the cost-sensitive consumer tier. By decoupling storage from physical visits, they rent cheaper peripheral warehouses and deploy van fleets for pick-and-drop. CityBox24’s Berlin pilot captured share among gig-economy workers who lack cars, pressuring conventional sites on price. Incumbents retaliate with hybrid models such as drive-up container parking and value-added logistics, amplifying competitive churn. Over the next five years, technology adoption and ability to deliver ancillary services will separate market leaders from laggards, even as consolidation rolls smaller portfolios into institutional platforms.

Germany Self Storage Industry Leaders

Shurgard Self Storage SA

Space Plus Store GmbH

Hertling GmbH and Co. KG

XXLAGER Selfstorage GmbH

Lanzell Spezialtransporte GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Shurgard completed the retrofit of 10 legacy buildings with rooftop solar arrays totaling 2 MW capacity to lower operating expenses and bolster ESG credentials.

- January 2025: Shurgard Self-Storage SA acquired a four-facility portfolio in Rhine-Ruhr, lifting its German footprint to 54 locations.

- November 2024: Blackstone finalized a EUR 100 million (USD 107 million) equity investment in Lagerbox Holding GmbH, earmarked for 12 new stores across Berlin, Munich, Hamburg, and Frankfurt.

- September 2024: HOMEBOX opened a 35,000-square-foot climate-controlled facility in Cologne designed for pharmaceutical and electronics tenants.

Germany Self Storage Market Report Scope

Self-storage facilities give people access to space to rent and store household or business possessions. Rental agreements for storage space, often known as storage units, are month-to-month agreements. Self-storage allows the user much greater control than full-service storage options, which restrict the customers' access to their possessions and depend on the storage provider to maintain and manage them.

The Germany self storage market is defined based on the revenues generated from the services used by various user types. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the number of self-storage facilities, total lettable area, occupancy rate (%), and average rent per square meter, along with major factors impacting the growth of the market in terms of drivers and restraints. The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

The Germany Self-Storage Market Report is Segmented by End-User (Personal, and Business), Storage Size (Small and Medium Units (Less than 40 Sq Ft, Large Units (Above 40 Sq Ft), and More), Storage Type (Climate-Controlled, and Non-Climate-Controlled), Ownership Pattern (Owned, and Leased). The Market Forecasts are Provided in Terms of Volume (Million sq ft).

| Personal |

| Business |

| Small and Medium Units (Less than 40 sq ft) |

| Large Units (Above 40 sq ft) |

| Others (Lockers/Double-Stacked) |

| Climate-Controlled |

| Non-Climate-Controlled |

| Owned |

| Leased |

| By End-User | Personal |

| Business | |

| By Storage Size | Small and Medium Units (Less than 40 sq ft) |

| Large Units (Above 40 sq ft) | |

| Others (Lockers/Double-Stacked) | |

| By Storage Type | Climate-Controlled |

| Non-Climate-Controlled | |

| By Ownership Pattern | Owned |

| Leased |

Key Questions Answered in the Report

How large is the Germany self-storage market in 2026?

It spans 27.81 million square feet in 2026, on a path toward 36.53 million square feet by 2031 at a 5.61% CAGR.

Which customer category dominates Germany's self-storage facilities?

Personal renters lead with 73.92% of capacity, driven by shrinking urban apartments and a high share of single-person households.

What is driving business tenant growth in German self-storage?

Last-mile inventory pressures tied to e-commerce and SME archiving needs are pushing the business segment to a 6.37% CAGR through 2031.

Why are climate-controlled units growing faster than standard space?

Pharmaceuticals, electronics, and wine collections require regulated environments, prompting a 6.01% annual expansion of climate-controlled capacity.

How do zoning regulations affect new self-storage construction in Germany?

Stringent municipal planning rules extend approval timelines to as long as 24 months, raising entry costs and favoring acquisitions over greenfield builds.

Which German cities present the strongest growth opportunities beyond the big five metros?

Leipzig, Nuremberg, Dresden, Hanover, and Stuttgart combine lower land costs with rising urbanization, attracting operators deploying unmanned, tech-enabled stores.

Page last updated on: