Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.58 Billion |

| Market Size (2026) | USD 11.03 Billion |

| Market Size (2031) | USD 13.62 Billion |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Switzerland Self-Storage Market Analysis by Mordor Intelligence

Switzerland self-storage market size in 2026 is estimated at USD 11.03 billion, growing from 2025 value of USD 10.58 billion with 2031 projections showing USD 13.62 billion, growing at 4.30% CAGR over 2026-2031. The growth outlook rests on a chronic housing shortage that drives vacancy rates to 1.08% nationally and an extreme 0.46% in Geneva, forcing residents and businesses to externalize possessions.[1]Ramzi Chamat, “Declining Housing Vacancy Rate in Switzerland: Analysis and Outlook,” OAKS GROUP, oaks.ch Alpine geography constrains new construction, yet Switzerland’s safe-haven status keeps capital flowing into real estate, sustaining demand for premium storage space. Businesses accelerate adoption because flexible, small-footprint logistics hubs help them serve cross-border customers under strict Swiss customs rules. Foreign investment in Alpine resorts also fuels large-unit rentals as international buyers secure climate-controlled storage for art, wine and gear. The Switzerland self-storage market therefore benefits simultaneously from residential crowding, corporate supply-chain re-design and the country’s role as a global wealth repository.

Key Report Takeaways

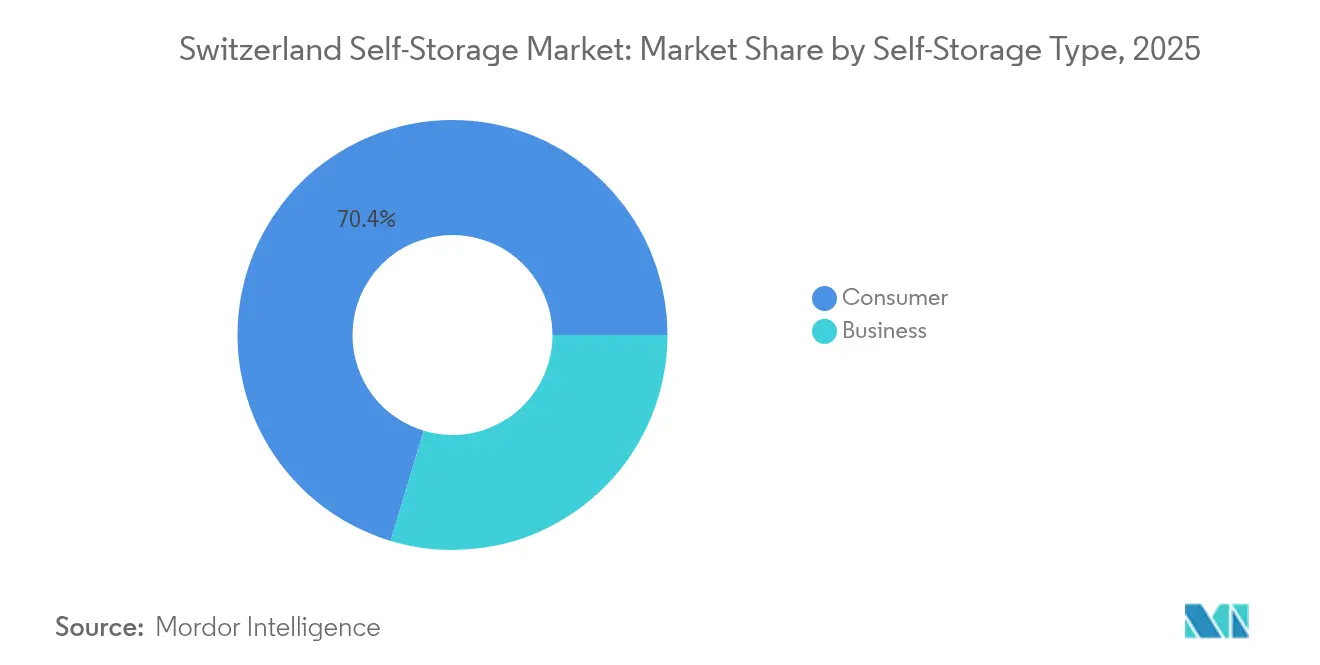

- By self-storage type, consumer applications held 70.35% of the Switzerland self-storage market share in 2025, while the business segment is projected to grow at a 5.90% CAGR through 2031.

- By unit size, 25-50 sq ft small units captured 33.45% of the Switzerland self-storage market share in 2025; units above 200 sq ft are forecast to register a 6.75% CAGR by 2031.

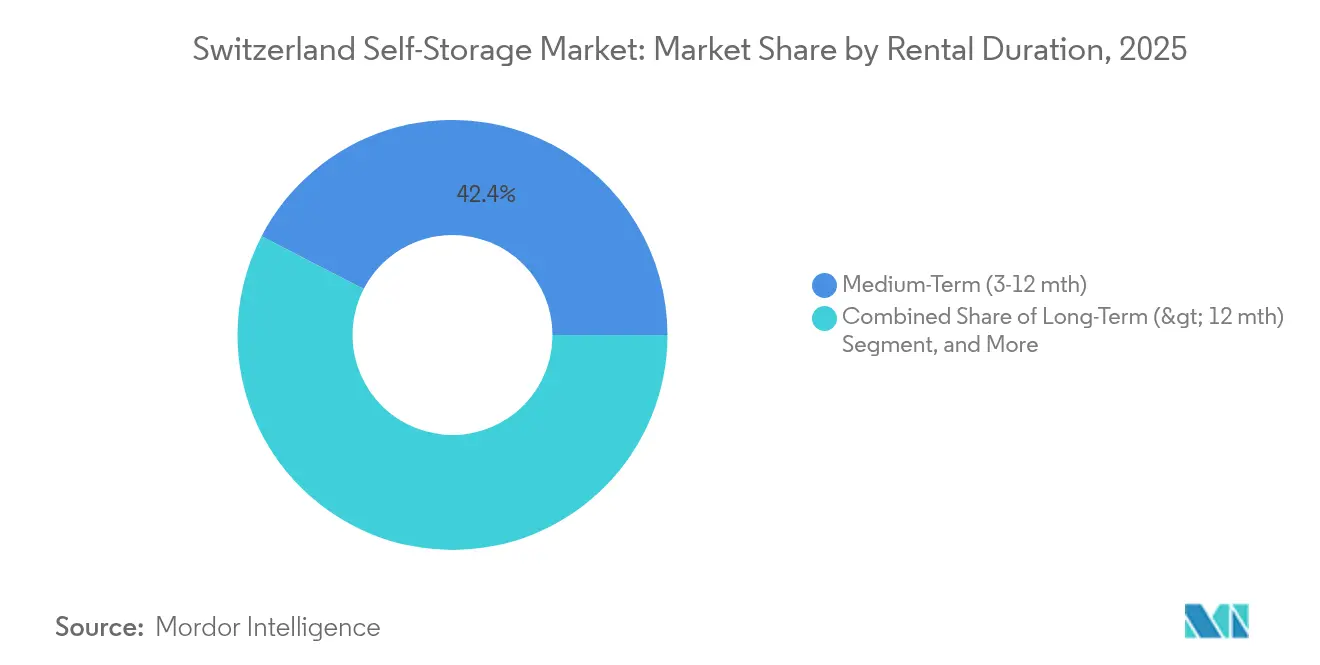

- By rental duration, medium-term contracts of 3-12 months accounted for a 42.40% share of the Switzerland self-storage market size in 2025, whereas short-term rentals below three months will advance 7.05% annually to 2031.

- By application, household and personal goods dominated with 56.20% revenue share in 2025, while micro-fulfillment hubs are set to expand at an 7.55% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Self-Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking Urban Living Space and Rising Rental Prices | +1.2% | National, with acute impact in Geneva, Zurich, Basel | Short term (≤ 2 years) |

| Growing SME and E-commerce Fulfillment Needs | +0.8% | National, concentrated in logistics hubs | Medium term (2-4 years) |

| Aging, Affluent Population Seeking Decluttering Solutions | +0.9% | National, skewed toward urban cantons | Long term (≥ 4 years) |

| Wine and Fine-Art Storage Demand From HNWI | +0.7% | Geneva, Zurich, Zug financial centers | Medium term (2-4 years) |

| Alpine Adventure Gear Lockers for Tourism Operators | +0.5% | Alpine regions, seasonal tourism centers | Medium term (2-4 years) |

| Digital-Nomad Visa Holders Using Storage as "Base-Camp" | +0.4% | Urban centers, tech hubs, co-working spaces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shrinking Urban Living Space and Rising Rental Prices

Vacancy rates of 0.07% in Zurich and 0.46% in Geneva place Switzerland at the global extreme of housing scarcity, turning external storage from convenience into basic infrastructure.[2]“Swiss government proposes measures to curb rising rents,” SWI swissinfo.ch, swissinfo.ch Federal data warn that current conditions mirror the 2014 crunch but now feature near-zero interest rates that inflate property values beyond middle-class budgets.[3]Federal Office for Housing, “Wohnungsmarktindikatoren,” bwo.admin.ch Tenants discover that paying CHF 200 (USD 225) for a locker costs less than upgrading apartments, which encourages stable demand even during economic slowdowns. Developers respond by designing smaller units to meet rent caps, indirectly funneling overflow items into the Switzerland self-storage market. Operators position inner-city micro-facilities close to public transport so residents can access belongings without owning cars, reinforcing network effects that lock in occupancy.

Growing SME and E-Commerce Fulfillment Needs

Swiss SMEs export niche products that require just-in-time inventory near consumer clusters across the Schengen area. Government SME-Portal programs guide firms toward flexible capacity rather than capital-intensive warehouses. Self-storage units therefore double as micro-fulfillment nodes equipped with parcel drop-rooms, barcode access and customs-ready documentation services, easing cross-border trade compliance outlined by the World Bank. As marketplace sellers promise 24-hour delivery, demand shifts toward facilities along the main north–south corridors that link Basel, Zürich and Ticino. The Switzerland self-storage market gains resilience because business customers sign staggered contracts that smooth seasonal swings in consumer occupancy.

Aging, Affluent Population Seeking Decluttering Solutions

Switzerland’s median age surpasses 44 years, and retirees hold high net wealth but relocate into smaller urban flats to access medical and cultural services. Downsizing families place furniture and heirlooms in climate-controlled rooms rather than selling beloved assets. Storage firms respond with concierge pick-up, insurance integration and digital inventories, creating premium tiers that lift average revenue per square foot. Zurich and Geneva municipalities expect senior-led households to rise 18% by 2030, signaling sustained latent demand. The Switzerland self-storage market thus aligns with demographic trends that favor predictable, low-churn cash flows relative to younger, more transient cohorts.

Wine and Fine-Art Storage Demand from HNWI

Swiss stability, discretion and favorable customs zones attract collectors who require bank-grade security combined with private access. Facilities near Geneva’s free-ports or Zurich’s art quarter provide humidity-controlled vaults, biometric entry and independent valuation services. High-net-worth clients often rent rooms exceeding 200 sq ft to consolidate collections that cannot fit in urban condos. Transaction data on Alpine resort homes worth CHF 14.2 million (USD 15.9 million) purchased by Americans in early 2025 underscore the influx of portable wealth. These buyers seek year-round storage for wine, art and ski equipment, supporting the most profitable slice of the Switzerland self-storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity and High Cost of Commercial Real-Estate | -0.6% | National, acute in urban centers | Short term (≤ 2 years) |

| Restrictive Zoning and Building-Code Approvals | -0.4% | Cantonal variations, strictest in heritage areas | Long term (≥ 4 years) |

| Cooperative Housing Providing Communal Storage | -0.3% | Urban cantons, social housing developments | Medium term (2-4 years) |

| Heritage-Building Regulations Limiting Conversions | -0.2% | Historic city centers, protected districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity and High Cost of Commercial Real-Estate

Switzerland’s limited developable land and environmental safeguards tighten supply for every asset class. Real-estate investors channel abundant liquidity into mixed-use projects, bidding up land values that self-storage operators struggle to match. Inner-city parcels often top CHF 5,000 (USD 5,600) per m², forcing operators toward costlier vertical builds or peripheral sites. Financing risk rises because interest-rate shifts directly affect cap-rates, yet storage rents cannot escalate as rapidly as acquisition costs. The imbalance narrows margins and delays new capacity additions, tempering growth within the Switzerland self-storage market.

Restrictive Zoning and Building-Code Approvals

Cantonal zoning boards prioritize residential units to ease housing pressure, relegating storage projects to industrial zones far from customer catchments. Lengthy approval cycles sometimes stretch beyond three years, exposing developers to cost inflation. Heritage preservation laws in Zurich, Bern and Lucerne restrict façade alterations, complicating adaptive-reuse of urban warehouses for storage. Smaller local operators without specialized compliance expertise often exit the pipeline, which gradually tilts the Switzerland self-storage market toward well-capitalized chains able to navigate complex regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Self-Storage Type: Business Segment Drives Future Growth

In 2025 the consumer segment generated 70.35% of revenue, illustrating how tight residential space underpins the Switzerland self-storage market. That dominance will remain, yet business demand is projected to expand at a 5.90% CAGR, creating the market’s most dynamic revenue source. SMEs adopt distributed storage to match cross-border shipping requirements and reduce customs clearance times, benefiting operators that can integrate barcode-based inventory services. Large corporate clients, including pharmaceutical and watchmakers, rent entire floors to stage bonded inventory awaiting European distribution, boosting average lease sizes. Consumer uptake continues to increase but at a slower pace because apartment downsizing has plateaued in some cantons where zoning restrictions curb further footprint reduction. However, pervasive vacancy pressure ensures a baseline customer influx, ensuring the Switzerland self-storage market maintains balanced revenue streams over the forecast horizon.

The Switzerland self-storage industry also witnesses hybrid models where a single facility allocates separate wings for private boxes and palletized commercial stock. Business users value clear service-level agreements, weekend access and data-driven reporting, allowing operators to charge premium rates for reliability. Consumer areas prioritize flexible hours and contactless move-in to minimize staffing costs. This dual-focus strategy extends lifetime value across both segments, especially in urban catchments where land scarcity forces operators to maximize revenue per square foot. As supply-chain digitization accelerates, demand for barcode scanning, real-time CCTV and automated invoicing grows, pulling technology partnerships into the center of competitive differentiation across the Switzerland self-storage market.

By Unit Size: Large Units Capture Premium Demand

Extra-large units above 200 sq ft are set to grow at 6.75% annually as wealthy international clients use Switzerland for treasure-class asset storage. These premium rooms command rents up to 2.5 times standard rates, lifting the Switzerland self-storage market size for the upper-tier segment. Geneva free-port operators report waiting lists for climate-controlled vaults designed for wine, paintings and precious metals, encouraging chains to allocate full mezzanine levels to oversized units. Small lockers of 25-50 sq ft still held a 33.45% Switzerland self-storage market share in 2025, anchoring occupancy and hedging volatility from high-end segments. Mid-range rooms between 51-100 sq ft remain vital during residential relocations, especially in German-speaking cantons where job mobility is highest.

Demand stratification allows operators to practice yield management similar to airlines: premium units gain dynamic pricing during art-fair seasons, while economy lockers offer bundled discounts in low occupancy months. Investors recognise that larger rooms attract lower churn because collectors sign multi-year agreements to consolidate multiple asset classes under one roof. Construction plans increasingly layer modular partitions so operators can reconfigure space quickly as the Switzerland self-storage market evolves. This adaptability mitigates risk when macro-drivers—such as currency moves that affect cross-border art flows—shift unit-size mix unexpectedly.

By Rental Duration: Short-Term Storage Reflects Economic Dynamism

Short-term contracts under three months will post a 7.05% CAGR, underscoring Switzerland’s agile economy. Start-ups, expats and digital nomads take advantage of contactless move-in via mobile app, turning storage into an on-demand utility. Seasonal tourism further boosts under-90-day occupancy for outdoor gear lockers in Alpine cantons. Medium-term rentals spanning 3-12 months maintained a commanding 42.40% share of the Switzerland self-storage market size in 2025, reflecting standard apartment lease turnover cycles. Operators optimise revenue by charging time-based premiums rather than square-foot premiums for customers seeking flexibility.

Long-term agreements exceeding one year remain attractive for retirees and SME archival needs because operators often offer graduated discounts. Yet the trend toward asset-light lifestyles favours shorter commitments, nudging product design toward pro-rated billing, digital identity verification and cross-facility access privileges. This shift compels operators to refine revenue-management algorithms capable of balancing higher churn with price elasticity, keeping overall yields steady across the Switzerland self-storage market.

By Application: Micro-Fulfillment Hubs Lead Innovation

Micro-fulfillment hubs will grow at 7.55% annually as e-commerce firms re-design last-mile logistics to comply with Swiss consumer-protection and customs regimes. Facilities retrofit individual boxes with IoT sensors that capture temperature and humidity, allowing food-grade or cosmetic items to remain within regulatory thresholds during short holding periods. Household and personal goods still dominated with 56.20% market share in 2025, highlighting how living-space scarcity remains the core demand driver. Document archiving experiences steady demand from legal and fiduciary firms obliged to keep hard copies under strict privacy laws, while student storage peaks around university breaks in Lausanne, Basel and Zurich.

Wine and specialty items storage illustrates Switzerland’s premium curve. Collectors insist on 12°C constant environments with vibration control, pushing operators to install redundant HVAC and smart monitoring. These capital-intensive improvements justify lease rates several multiples above standard boxes, contributing disproportionally to profit. Convergence across applications allows operators to convert under-used areas seasonally—for example, shifting student boxes into micro-fulfillment racks during summer—maximising utilisation within the Switzerland self-storage market.

Geography Analysis

Urban cantons constitute the demand epicenter. Geneva’s Lake region posts the greatest per-capita uptake because the vacancy rate of 0.46% forces even affluent tenants to externalize possessions. Zurich follows with a 0.07% vacancy rate, translating into waiting lists for centrally located facilities. Basel leverages its life-sciences cluster to drive specialised cold-chain storage, blending corporate and consumer use within the same footprint. German-speaking cantons bordering Germany house cross-border commuters who store goods in Switzerland to avoid customs delays, sustaining an above-average occupancy profile.

Alpine regions anchor premium demand tied to tourism and luxury real estate. Property purchases in Andermatt illustrate how inbound wealth creates spill-over storage needs for art, sports equipment and seasonal vehicles. Central Switzerland—especially Zug—capitalises on tax advantages that draw commodity traders and crypto firms requiring secure document and hardware storage. Ticino serves as a commercial gateway to Italy, increasing throughput for micro-fulfillment parcels moving south while still adhering to Swiss security expectations. Rural municipalities offer cheaper land that enables large-format builds; digital access panels reduce staffing, allowing these sites to price aggressively and pull overflow demand from urban cores.

Federalism influences growth because cantonal zoning rules vary widely. Bern fast-tracks conversions of redundant military depots into storage, whereas Lausanne imposes strict aesthetic rules on new builds near heritage zones, slowing capacity expansion. Operators that develop multi-cantonal portfolios can balance risk by offsetting regulatory delays in one region with quicker openings elsewhere. Switzerland’s efficient rail and road network connects these distributed assets, ensuring customers accept a short commute in exchange for lower rents, preserving elasticity across the Switzerland self-storage market.

Competitive Landscape

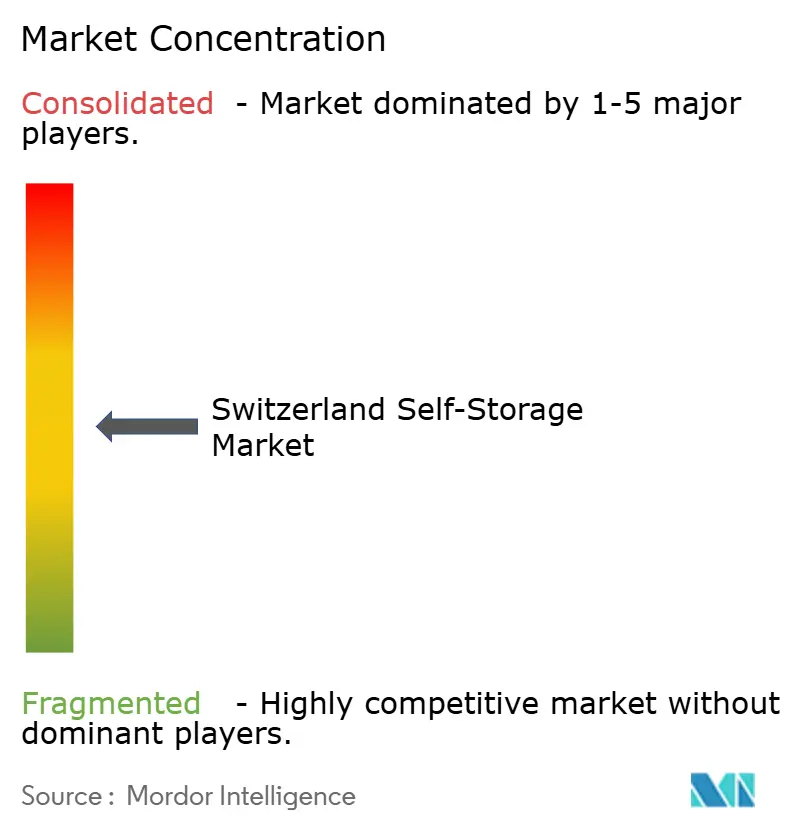

The Switzerland self-storage market features moderate fragmentation with early signs of consolidation. Shurgard leads capacity expansion, adding 405,000 m² by 2026 and recording 10.8% revenue growth in 2024. Its scale affords marketing clout and automated KYC enrollment, capturing affluent urban customers willing to pay for reputational assurance. Zebrabox defends share through personalised services, including white-glove transport for art pieces, while placeB differentiates with fully digital access and dynamic pricing that adjusts every six hours. These models highlight technology adoption as the primary strategic lever.

Local players exploit deep knowledge of cantonal permitting. In heritage-sensitive cities, regional firms win approvals faster by incorporating façade conservation and mixed-use community spaces. Some boutique operators specialise in wine cellaring and partner with insurance underwriters to issue asset-specific coverage at the point of rental. Such micro-niches command outsized margins, balancing the volume advantages enjoyed by multinationals.

Acquisition opportunities remain abundant because a long tail of single-facility owners lacks resources to modernise. Chains with institutional backing pursue roll-ups, standardising operating systems and introducing cross-selling such as moving supplies and last-mile logistics services. Fragmentation coexists with high customer switching costs, so first movers that upgrade IT platforms lock in subscribers. In this context, the Switzerland self-storage market encourages scale yet still rewards specialised value propositions, keeping rivalry robust without tipping into price wars.

Switzerland Self-Storage Industry Leaders

-

Zebrabox AG

-

Casaforte (SMC Self-Storage Management) SA

-

Secur’Storage SA

-

Homebox Switzerland SA

-

MyPlace Self-Storage GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Andermatt Swiss Alps reported CHF 14.2 million (USD 15.9 million) in American property sales, spotlighting cross-border wealth inflows that drive demand for premium storage near resort towns.

- April 2025: The Zurich city council approved a CHF 500 million (USD 560 million) housing taskforce. Storage operators anticipate spill-over demand as new subsidies target micro-apartments that further constrain resident space.

- March 2025: placeB integrated IoT-based door sensors across its network, cutting unplanned downtime by 18% and enhancing reputation among tech-savvy users.

- December 2024: Zebrabox partnered with Swiss Post to pilot parcel-handover lockers inside storage corridors, turning facilities into last-mile nodes for SMEs.

Switzerland Self-Storage Market Report Scope

The self-storage solutions offer value to continue protection from environmental damage and theft by providing cost-effective storage solutions. The study scope of the Switzerland self-storage market tracks down the adoption of different self-storage solutions used by business customers and domestic consumers. The study also focuses on the impact of COVID-19 on the market ecosystem. In the study scope, the existing storage provider landscape also covered, which consists of major players operating in the market.

By Self-Storage Type

| Consumer |

| Business |

By Unit Size (sq ft)

| < 25 (Locker) |

| 25-50 (Small) |

| 51-100 (Medium) |

| 101-200 (Large) |

| > 200 (Extra-Large) |

By Rental Duration

| Short-Term (< 3 mth) |

| Medium-Term (3-12 mth) |

| Long-Term (> 12 mth) |

By Application

| Household and Personal Goods |

| Business Inventory and Equipment |

| Student Storage |

| Document and Records Archiving |

| Wine and Specialty Items |

| Micro-Fulfilment / Last-Mile Hubs |

| By Self-Storage Type | Consumer |

| Business | |

| By Unit Size (sq ft) | < 25 (Locker) |

| 25-50 (Small) | |

| 51-100 (Medium) | |

| 101-200 (Large) | |

| > 200 (Extra-Large) | |

| By Rental Duration | Short-Term (< 3 mth) |

| Medium-Term (3-12 mth) | |

| Long-Term (> 12 mth) | |

| By Application | Household and Personal Goods |

| Business Inventory and Equipment | |

| Student Storage | |

| Document and Records Archiving | |

| Wine and Specialty Items | |

| Micro-Fulfilment / Last-Mile Hubs |

Key Questions Answered in the Report

What is the current size of the Switzerland self-storage market?

The Switzerland self-storage market is worth USD 11.03 billion in 2026.

How fast is the market expected to grow?

Industry revenue is projected to rise at a 4.30% CAGR, reaching USD 13.62 billion by 2031.

Why are Swiss vacancy rates influencing storage demand?

Urban vacancy rates as low as 0.07% in Zurich leave residents without in-home space, forcing them to rent external units.

Which self-storage segment is expanding fastest?

Business applications lead with a 5.90% CAGR, driven by SMEs that need flexible logistics hubs.

Where is geographic demand strongest?

Geneva and Zurich top the list due to extreme housing scarcity, while Alpine resort areas attract premium demand tied to luxury property buyers.

Page last updated on: