Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

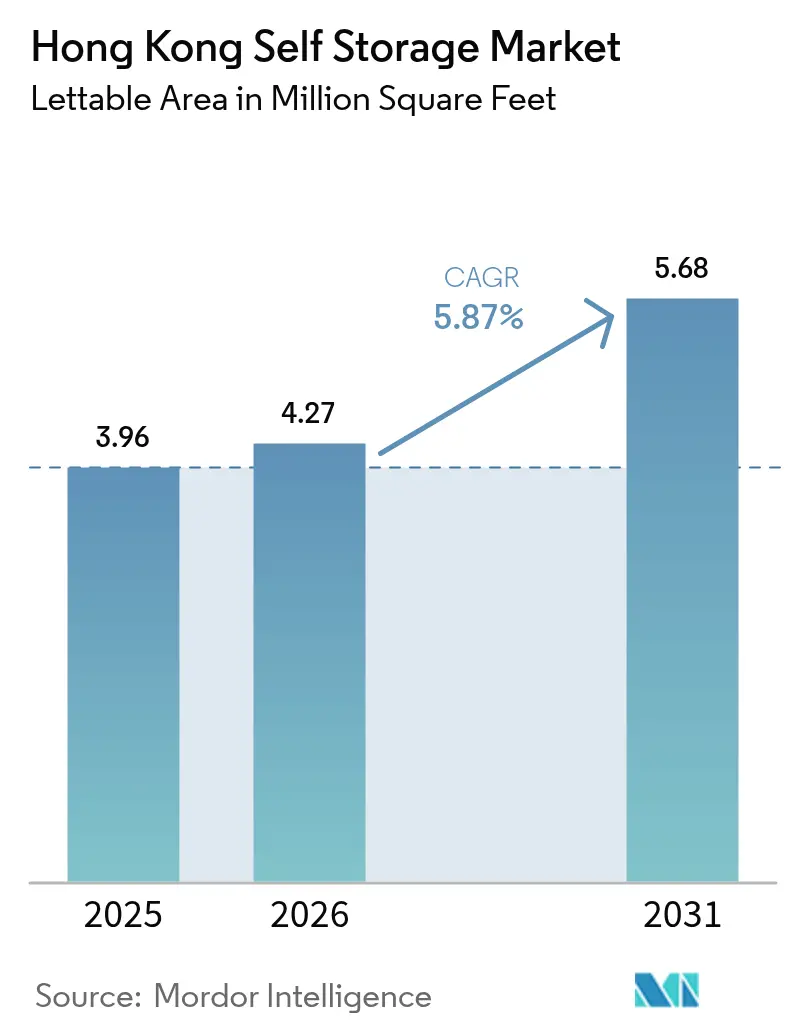

| Base Year Market Size (2025) | 3.96 Million square feet |

| Market Volume (2026) | 4.27 Million square feet |

| Market Volume (2031) | 5.68 Million square feet |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Self Storage Market Analysis by Mordor Intelligence

The Hong Kong self-storage market size is projected to be 3.96 million square feet in 2025, 4.27 million square feet in 2026, and reach 5.68 million square feet by 2031, growing at a CAGR of 5.87% from 2026 to 2031. Demand is underpinned by persistent micro-living, density above 20,000 people per square kilometer, and a widening acceptance of external lockers as a permanent household expense. Operators have raised customer acquisition through smartphone-based access, while landlords convert aging industrial floors into revenue-generating storage as land premiums escalate. Corporate waste-charging laws that took effect in August 2024 have further expanded commercial use cases, encouraging firms to hold materials awaiting redistribution instead of paying disposal fees. Competitive focus has shifted from raw capacity toward proptech, concierge service layers, and climate-controlled amenities that command 30-40% premiums.

Key Report Takeaways

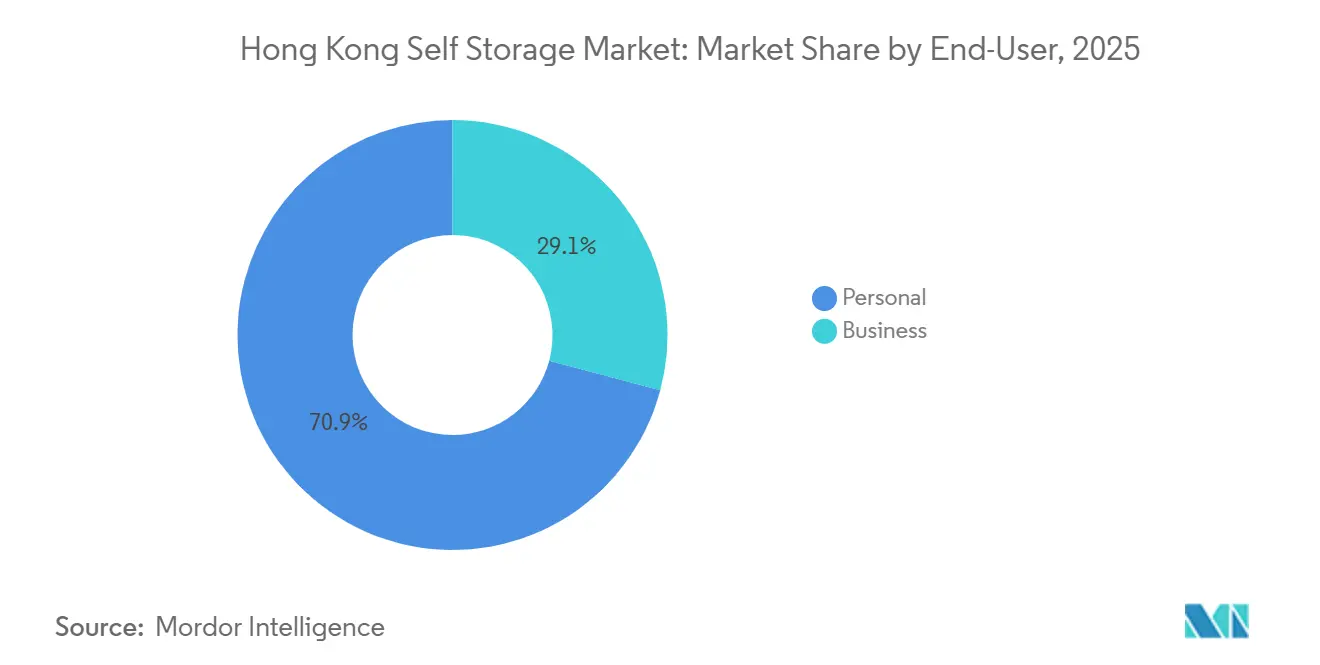

- By end-user, personal contracts held 70.87% of the Hong Kong self storage market in 2025, while business demand is advancing at a 6.68% CAGR through 2031.

- By storage size, units below 40 square feet accounted for 57.09% of the Hong Kong self storage market share in 2025, whereas units above 40 square feet are forecast to be the fastest-growing cohort with a 5.97% CAGR to 2031.

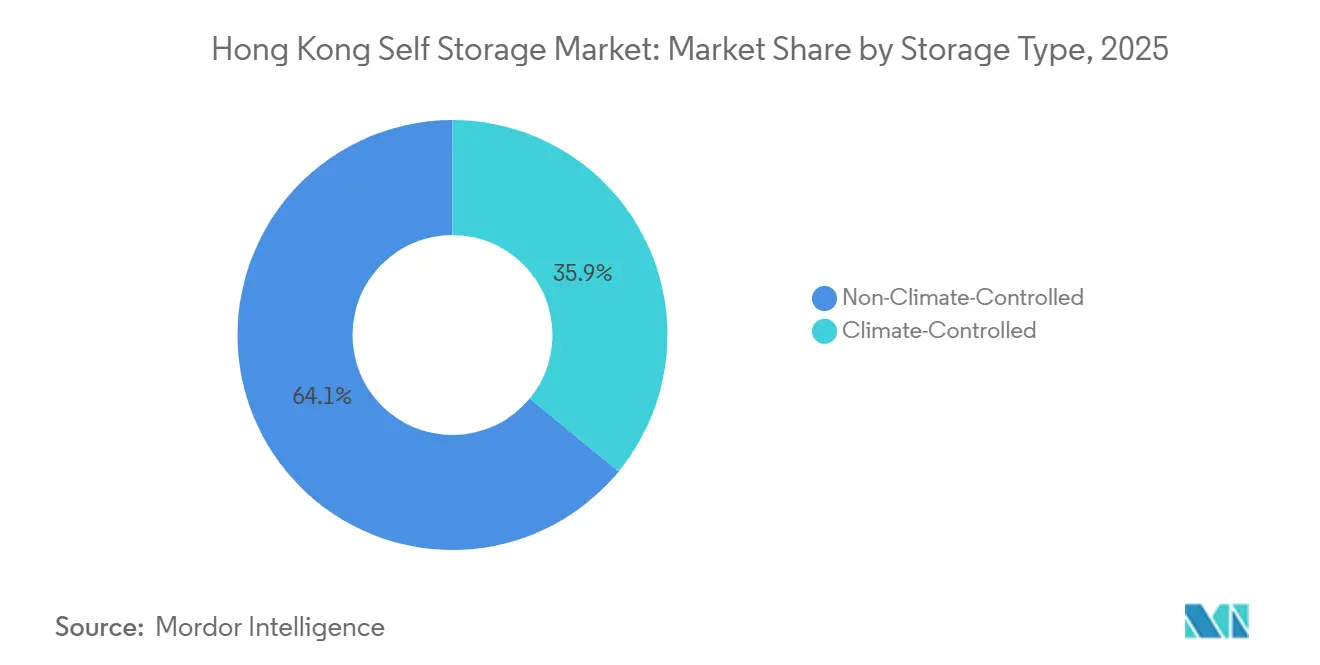

- By storage type, non-climate-controlled space retained 64.06% share in 2025; climate-controlled lockers are expanding at a 6.18% CAGR as wine, art, and pharmaceutical users accept premium tariffs.

- By ownership pattern, owned facilities represented 54.19% capacity in 2025, while leased operations are growing at 6.02% annually as operators favor asset-light entry into high-density districts.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong Kong Self Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Urban Micro-Living Drives External Storage Demand | +1.8% | Hong Kong Island, Kowloon Core Districts | Long Term (≥ 4 Years) |

| Booming E-Commerce Merchants Outsourcing Last-Mile Inventory | +1.5% | New Territories Logistics Corridors, Kwun Tong, Kowloon Bay | Medium Term (2-4 Years) |

| Government-Backed Industrial Revitalization Scheme Releasing Suitable Buildings | +1.2% | Kwun Tong, Kowloon Bay, San Po Kong | Medium Term (2-4 Years) |

| Integration with Proptech and Smart-Locker Networks Enabling Frictionless Access | +0.9% | Territory-Wide, Early Adoption in Central, Causeway Bay | Short Term (≤ 2 Years) |

| Premiumization Trend Toward Climate-Controlled Wine and Art Lockers | +0.6% | Mid-Levels, Peak, Repulse Bay Affluent Zones | Long Term (≥ 4 Years) |

| Corporate ESG Mandates Favor Re-Use Over Disposal, Raising Temporary Storage Need | +0.5% | Quarry Bay, Admiralty Corporate Districts | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Persistent Urban Micro-Living Drives External Storage Demand

Hong Kong’s median apartment of 430 square feet forces households to externalize belongings that would fit indoors in lower-density cities, anchoring the Hong Kong self-storage market even when the real-estate cycle softens.[1]Census and Statistics Department, “Hong Kong Population and Household Statistics,” CENSTATD.GOV.HK Population density beyond 20,000 people per square kilometer lets a single facility capture a larger catchment than peers in most global metros. Remote-work conversion of spare rooms since 2024 has lifted contract duration to 18-24 months, turning storage into a recurring line item rather than a one-off relocation fee.[2]Self Storage Association Asia, “Hong Kong Market Report 2024-2025,” SSAAGLOBAL.COM Operators therefore report occupancy above 80% even amid broader retail rent softness. This hard-wired baseline allows premium pricing and justifies capital expenditure for proptech upgrades that heighten convenience.

Booming E-Commerce Merchants Outsourcing Last-Mile Inventory

Cross-border sellers increasingly view the Hong Kong self-storage market as a micro-fulfillment grid that complements courier partnerships. JD Logistics pushed same-day coverage via multiple 40 square-foot cells in 2025, a model now mirrored by smaller Taobao and Shopify vendors.[3]JD Logistics, “Hong Kong Expansion and Same-Day Delivery Network,” JDL.COM Monthly locker rents of HKD 1,500-3,000 (USD 192-385) undercut multi-year warehouse rates of HKD 15-25 (USD 1.92-3.21) per square foot, providing an immediate working-capital edge. Vacancy in prime warehouses rose to record highs in late 2025, yet storage occupancy held firm, confirming merchants’ preference for flexible, distributed nodes. This interplay supports the 6.68% CAGR projected for business users through 2031.

Government-Backed Industrial Revitalization Scheme Releasing Suitable Buildings

Since the 2018 relaunch, only 23 applications materialized in the Central Business District-2 zone by March 2024, but approvals clustered in Kowloon East now exceed half of all conversions. Land premiums of HKD 40,000-130,000 (USD 5,128-16,667) per square meter filter out under-capitalized players, yet they also assure long tenure for larger operators able to fund fire-safety retrofits.[4]Planning Department, “Town Planning Board Annual Report 2024-2025,” PLAND.GOV.HK Industrial rents in Kowloon East jumped 15-20% from 2024-2025 as self-storage, data centers, and creative studios competed for the same stock. The policy environment therefore accelerates a shift toward institutional backing and professional management across the Hong Kong self-storage market.

Integration With Proptech and Smart-Locker Networks Enabling Frictionless Access

Keyless smartphone entry, NFC locks, IoT humidity monitoring, and dynamic pricing engines now define premium offers. RedBox Storage’s territory-wide rollout in 2024 lifted occupancy 12-15 percentage points above key-and-padlock peers and delivered customer satisfaction above 95%. Kerong’s battery-free NFC locks reduce maintenance downtime. Data-rich platforms allow revenue-management tactics familiar in hospitality, pushing average revenue per square foot 8-10% higher by 2028, cementing technology as a durable differentiator within the Hong Kong self-storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Shortage and Escalating Cost of Compliant Industrial Floorplate | -1.4% | Kowloon East, Tsuen Wan, Cheung Sha Wan | Medium Term (2-4 Years) |

| Stringent Fire-Safety Retrofit Capital Requirements Squeezing ROI | -1.1% | Territory-Wide Older Industrial Stock | Long Term (≥ 4 Years) |

| Cheaper Cross-Border Capacity in Shenzhen Attracting Price-Sensitive Users | -0.7% | New Territories Border Precincts | Medium Term (2-4 Years) |

| Rising Electricity Tariffs Undermine Profitability of Climate-Controlled Units | -0.5% | Territory-Wide Premium Facilities | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Acute Shortage and Escalating Cost of Compliant Industrial Floorplate

Industrial land allocation favors housing and infrastructure, limiting fresh supply and inflating acquisition costs to HKD 40,000-130,000 (USD 5,128-16,667) per square meter. Rents in Kowloon East climbed 15-20% between 2024-2025, reflecting multi-sector bidding for the same buildings. The October 2024 tender in Hung Shui Kiu reserved 30% area for displaced brownfield operators, further shrinking self-storage-ready floorplate. Operators therefore scale via leased conversions rather than outright purchase, but rent escalation still narrows yield for new entrants to the Hong Kong self-storage market.

Stringent Fire-Safety Retrofit Capital Requirements Squeezing ROI

Post-2016 fatalities triggered rigorous enforcement of Cap. 572 and Cap. 502 ordinances, mandating sprinklers, fire-rated partitions, and smoke extraction. Retrofit costs top HKD 1,000 (USD 128) per square foot, slicing net leasable ratios to 40-50%. The SAFE certification program introduced in 2024 adds HKD 50,000-100,000 (USD 6,410-12,821) annual audits, extending payback periods to 8-10 years. Smaller independents exit, leaving the Hong Kong self-storage market increasingly dominated by well-capitalized chains able to amortize compliance overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Commercial Demand Accelerates Amid ESG and E-Commerce Needs

Business tenants are adding units at a 6.68% CAGR through 2031, topping overall growth in the Hong Kong self-storage market. Personal users still occupied 70.87% of capacity in 2025 thanks to micro-flat living, yet corporate adoption is surging as waste-charging laws and last-mile inventory strategies converge. E-commerce sellers exploit flexible month-to-month terms, booking multiple lockers to stage promotions near dense catchments. Average commercial stay lengths have already exceeded 15 months, providing reliable recurring revenue. Personal contracts remain sticky, averaging 18-24 months, reflecting storage’s transition from discretionary to utility-like service.

The Hong Kong self storage market size tied to household clients shows dependable baseline growth from new housing completions that trend smaller. Businesses, however, are now requesting bulk-unit blocks, value-added pallet services, and barcode inventory scans. Operators respond with tiered tariff plans, after-hours courier dock access, and carbon-footprint dashboards aligned to ESG audits. This repositioning widens ARPU while diversifying risk beyond consumer cycles.

By Storage Size: Large Rooms Outpace as Merchants Park Inventory

Units under 40 square feet maintained 57.09% of the Hong Kong self-storage market share in 2025, continuing to serve households seeking seasonal item overflow. The sub-40 cohort’s modest ticket size supports 80%-plus occupancy, particularly on Hong Kong Island where supply is scarce. Large units above 40 square feet are expanding fastest at a 5.97% CAGR, driven by e-commerce bedding, fashion, and electronics merchants situating safety stock minutes from end buyers.

As climate-controlled segments proliferate, some operators convert oversized rooms into dual-zone chambers or double-stacking mezzanines to lift yield per cubic foot. Demand volatility around Singles’ Day and Christmas prompts dynamic allocation, with large-room take-up peaking two months before each retail surge. Household renters upgrade occasionally for renovations or expatriate repatriations, yet the principal use case is now commercial, foreshadowing a tilt in the Hong Kong self-storage market toward bulk logistics functionality.

By Storage Type: Climate Control Moves From Niche to Core Offering

Non-climate stock held 64.06% capacity in 2025, but temperature- and humidity-regulated space is outgrowing the base at 6.18% per year. Wine merchants, art investors, and pharmaceutical reps accept a 30-40% premium to guarantee product integrity. Operators therefore dedicate entire floors to 12-18 °C vaults, installing redundancy chillers and desiccant wheels. Electricity-tariff relief of 2.6% for 2026 only partially cushions elevated utility spend, making granular energy monitoring essential.

The Hong Kong self-storage market size allocated to climate segments is projected to reach 2.0 million square feet by 2031, supported by a deep pool of high-net-worth residents clustering in Peak, Mid-Levels, and Repulse Bay. Technological integrations, including IoT sensors that push alerts to users’ phones, further justify premium rates and elevate customer stickiness above 90%.

By Ownership Pattern: Asset-Light Leases Narrow Gap With Freehold Sites

Freehold installations accounted for 54.19% of floor area in 2025, anchoring operator cost bases where long-term demand is unquestioned. Escalating land premiums, however, prompt a pivot to leased conversions that are scaling at 6.02% annually. Lease tenures generally span three to six years with incremental rent steps of 5% every second year, allowing agile operators to exit underperforming suburbs.

Owned facilities dominate the Hong Kong Island core where vacancy risk is negligible. Leased fleets flourish in Kowloon East, Tsuen Wan, and Yuen Long, sometimes absorbing entire factory floors under management contracts that include revenue-share clauses with the landlord. The model mirrors hospitality’s franchise economics, underscoring how operational expertise, brand, and technology trump bricks-and-mortar ownership in the evolving Hong Kong self storage market.

Geography Analysis

Kowloon East remains the principal supply engine for the Hong Kong self-storage market, hosting over half of revitalization approvals by mid-2025. Aging factories in Kwun Tong, Kowloon Bay, and San Po Kong offer high ceiling heights suitable for mezzanine retrofits, and proximity to dense middle-class estates sustains walk-in traffic. Rents rose 15-20% across these precincts in 2025 as storage, data centers, and creative studios vied for the same floorplate. Although redevelopment activity raises costs, it simultaneously professionalizes assets, aligning them with Cap. 572 fire-safety requirements and widening the investable universe for institutional capital.

Hong Kong Island exhibits an opposite picture: rock-bottom vacancy and limited industrial zoning force operators to lease mixed-use towers at premium rents. The scarcity pushes climate-controlled penetration to its highest levels, with occupancy in Mid-Levels, Peak, and Western District surpassing 90%. Personal renters dominate these branches, and waiting lists persist despite higher tariffs, confirming embedded micro-living pressure.

The New Territories provide latitude for large-unit uptake. Storage clusters in Tsuen Wan, Sha Tin, and Yuen Long capitalize on truck accessibility and lower land premiums, attracting e-commerce firms staging returns and safety stock. The Hung Shui Kiu tender in October 2024 signals incremental supply, but mandated allocation for displaced brownfield tenants curtails fully commercial usage. Border-district facilities also face rate dilution from Shenzhen operators offering lockers at 1 CNY (USD 0.14) daily; yet cross-border customs friction and tight size limits prevent wholesale leakage. Net effect: geography shapes pricing strategy and amenity mix, compelling multi-site operators to tailor formats district by district across the Hong Kong self storage market.

Competitive Landscape

Roughly 420 active facilities render the Hong Kong self-storage market moderately fragmented, with no single brand exceeding a 10% portfolio share. Storefriendly, SC Storage, and Apple Storage headline the ranking by site count, having navigated post-2016 fire-safety crackdowns through heavy retrofit investment. Storefriendly’s HKD 7.8 million (USD 1 million) wine cellar at Lai Chi Kok exemplifies premium diversification. Apple Storage commemorated its 20th anniversary in February 2025 by opening five new outlets and reiterating a target of 180-plus locations by 2028, underlining aggressive network expansion.

RedBox Storage differentiates through deep proptech integration, collecting two Self Storage Awards Asia trophies in 2025 for customer experience and multi-site excellence. Its Red Vault high-security format, launched October 2025, layers biometric entry and reinforced steel rooms at a 40-50% surcharge, courting high-net-worth and corporate document clients. Proptech-driven revenue management, dynamic pricing, and app-based onboarding are raising the performance bar, pressuring legacy independents to upgrade or exit.

White-space opportunities revolve around ESG logistics, distributed fulfillment for cross-border e-commerce, and ultra-premium custody. Few existing operators provide pallet docks, inventory scanning, or ESG reporting dashboards, leaving margin on the table. SAFE certification and strict fire codes now function as de facto barriers, slowing greenfield rollout but boosting brand legitimacy among risk-averse users. The result is a gradual consolidation trajectory as scale, safety compliance, and digital convenience define success in the Hong Kong self-storage market.

Hong Kong Self Storage Industry Leaders

Storefriendly Self Storage Group Limited

SC Storage Group Limited

Tai Yau Storage Group Limited (Apple Storage)

Cube Self Storage Hong Kong Limited

Red Box Storage (Hong Kong) Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CLP Power confirmed its average net tariff reduction of 2.6% to HKD 140.6 (USD 19.9) cents per kilowatt-hour for the year, slightly easing utility pressure on climate-controlled lockers.

- October 2025: RedBox Storage launched the Red Vault premium tier with biometric access and 24/7 video surveillance, charging 40-50% above standard rates.

- September 2025: Storefriendly opened a HKD 7.8 million (USD 1 million) climate-controlled wine cellar comprising 177 units at Lai Chi Kok.

- May 2025: RedBox Storage celebrated its tenth anniversary with a customer-appreciation pop-up that generated 800 new five-star Google reviews.

Hong Kong Self Storage Market Report Scope

Self-storage facilities give people access to space to rent and store any household or business possessions. Rental agreements for storage space, often known as storage units, are month-to-month agreements. Self-storage allows the user much greater control than full-service storage options, which restrict the customer's access to their possessions and dependence on the storage provider to maintain and manage them.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study tracks the number of facilities and total lettable area and summarizes end-users. In addition, the study provides self-storage market trends, along with crucial vendor profiles.

The Hong Kong Self Storage Market Report is Segmented by End-User (Personal, and Business), Storage Size (Small and Medium Units (Less than 40 Sq Ft, Large Units (Above 40 Sq Ft), and More), Storage Type (Climate-Controlled, and Non-Climate-Controlled), Ownership Pattern (Owned, and Leased). The Market Forecasts are Provided in Terms of Volume (Million sq ft).

By End-User

| Personal |

| Business |

By Storage Size

| Small and Medium Units (Less than 40 sq ft) |

| Large Units (Above 40 sq ft) |

| Other Storage Sizes, Lockers/Double-Stacked |

By Storage Type

| Climate-Controlled |

| Non-Climate-Controlled |

By Ownership Pattern

| Owned |

| Leased |

| By End-User | Personal |

| Business | |

| By Storage Size | Small and Medium Units (Less than 40 sq ft) |

| Large Units (Above 40 sq ft) | |

| Other Storage Sizes, Lockers/Double-Stacked | |

| By Storage Type | Climate-Controlled |

| Non-Climate-Controlled | |

| By Ownership Pattern | Owned |

| Leased |

Key Questions Answered in the Report

How large will Hong Kong's self-storage footprint be by 2031?

It is forecast to reach 5.68 million sq ft, reflecting a 5.87% CAGR from 2026.

Which district offers the largest pipeline of conversion opportunities?

Kowloon East, particularly Kwun Tong and Kowloon Bay, holds over half of approved revitalization projects.

What drives corporate uptake of storage units?

E-commerce fulfillment needs and the 2024 waste-charging law that encourages companies to store items pending reuse.

Why are climate-controlled lockers growing faster than standard rooms?

Wine, art, and pharma customers pay 30-40% premiums for stable temperature and humidity, lifting demand at a 6.18% CAGR.

How has regulation shaped market structure since 2016?

Mandatory fire-safety retrofits costing HKD 1,000 per sq ft have forced smaller operators out, consolidating share among capital-rich chains.

What technology features most influence customer choice today?

Keyless smartphone access, IoT monitoring, and dynamic pricing engines are boosting occupancy and revenue across leading facilities.

Page last updated on: