Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

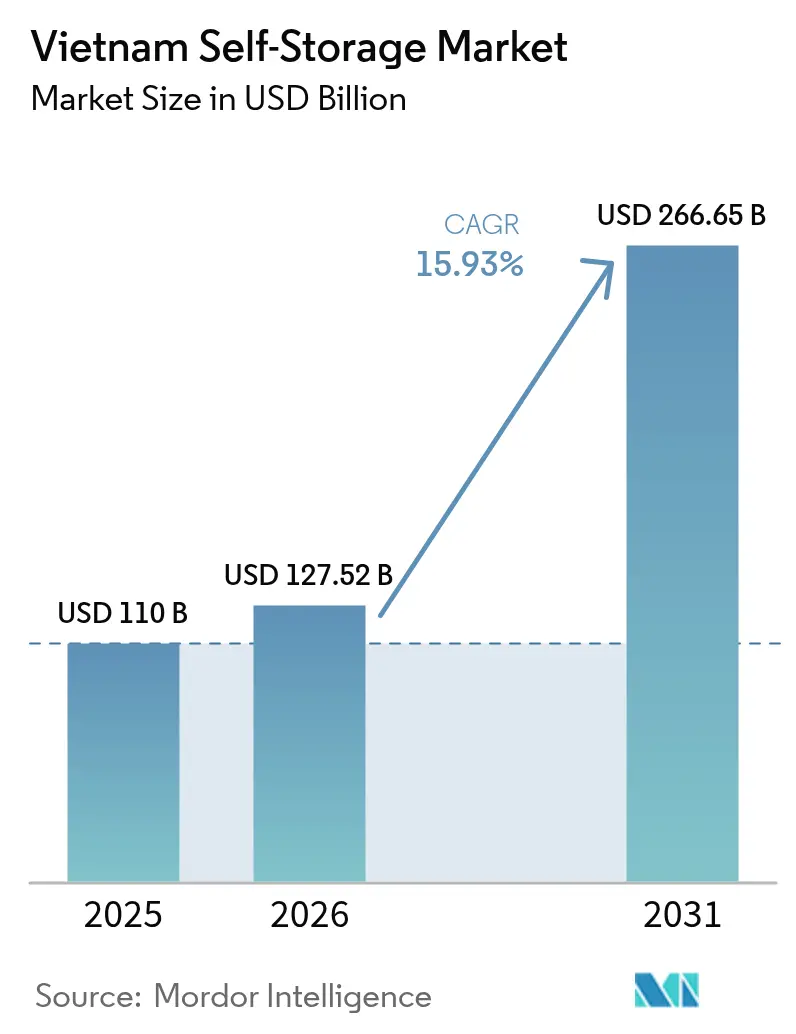

| Base Year Market Size (2025) | USD 110 Billion |

| Market Size (2026) | USD 127.52 Billion |

| Market Size (2031) | USD 266.65 Billion |

| Growth Rate (2026 - 2031) | 15.93% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Self-Storage Market Analysis by Mordor Intelligence

The Vietnam self-storage market size in 2026 is estimated at USD 127.52 million, growing from 2025 value of USD 110 million with 2031 projections showing USD 266.65 million, growing at 15.93% CAGR over 2026-2031. An urban population on track to hit 50% by the end of the decade, skyrocketing e-commerce sales, and shrinking apartment footprints in Ho Chi Minh City and Hanoi are the structural forces that keep demand for off-site space rising. Operators are layering technology into everyday operations, adding on-site inventory systems, and experimenting with valet pickup to widen appeal among city residents and micro-enterprises pressed for space. Land scarcity in downtown districts elevates development costs, yet the Vietnam self-storage market continues to grow as providers shift to multi-story formats and peripheral districts where zoning is easier and rents are lower. Foreign brands entering through joint ventures with local partners are lifting service standards, while first movers expand quickly to lock in strategic locations and high-yield customer clusters.

Key Report Takeaways

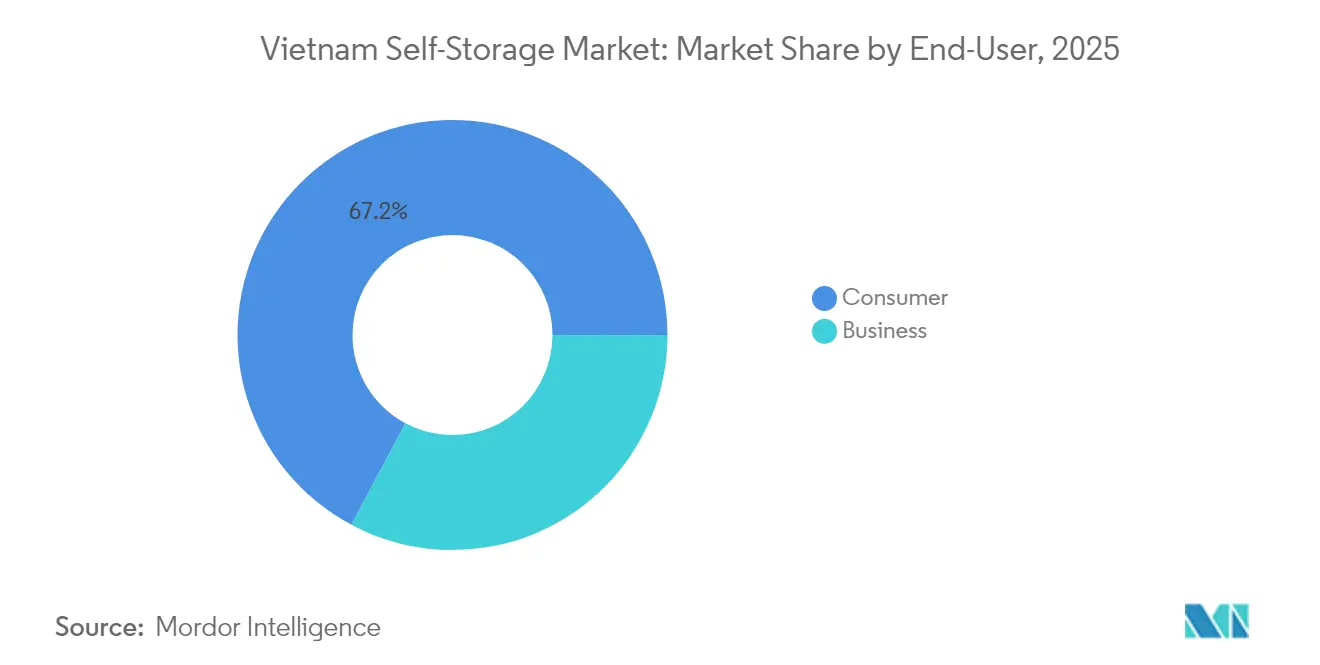

- By end-user, the consumer segment led with 67.20% of Vietnam self-storage market share in 2025; the business segment is projected to expand at an 18.58% CAGR through 2031.

- By facility type, non-climate-controlled units captured 56.40% of Vietnam self-storage market size in 2025, whereas valet/full-service sites are forecast to grow at 22.85% CAGR to 2031.

- By application use, E-commerce micro-fulfillment has emerged as the fastest-growing application segment, 42.60% of the Vietnam self-storage market size in 2025, with explosive online retail growth, which exceeded USD 20 billion in 2023, with a 29% CAGR to 2031.

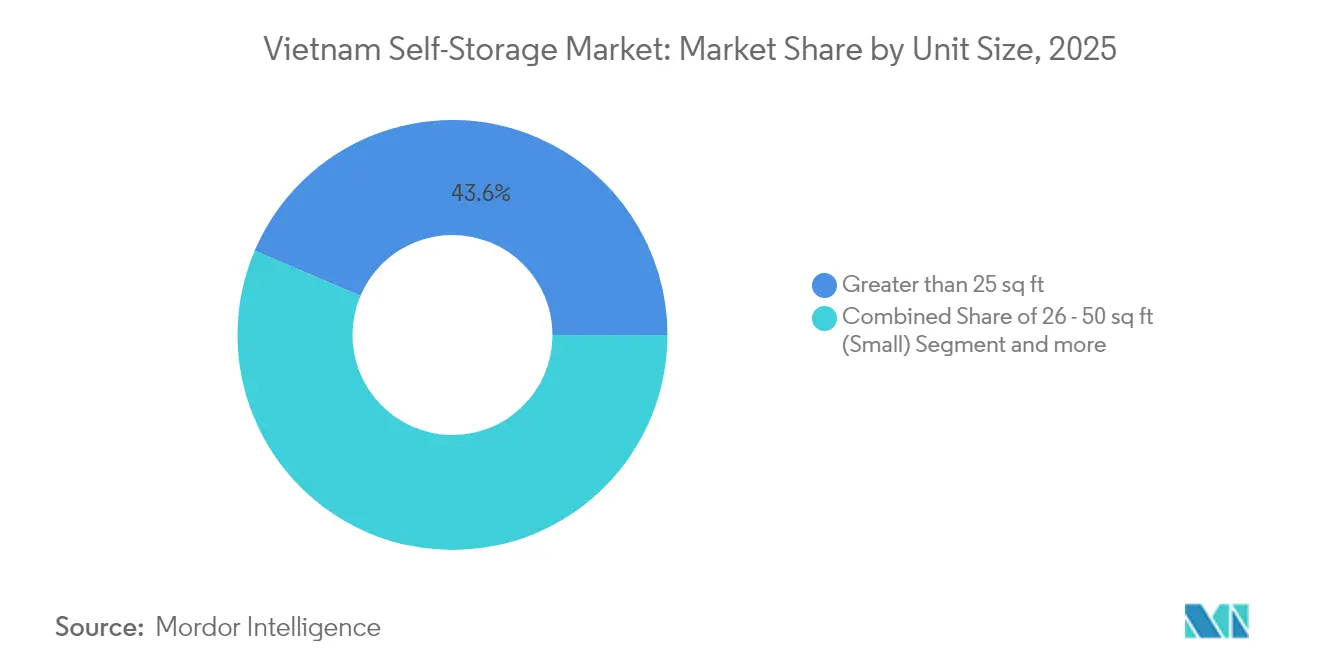

- By unit size, 26–50 sq ft rooms accounted for 43.60% of Vietnam self-storage market size in 2025, yet sub-25 sq ft lockers are on track for a 19.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Self-Storage Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shrinking Urban Living Space in Tier-1 Cities Boosting Off-Site Storage | +4.2% | Ho Chi Minh City, Hanoi, Da Nang | Long term (≥ 4 years) |

| E-commerce SMEs' Need for Micro-Fulfillment Space | +3.8% | National, with concentration in Ho Chi Minh City and Hanoi | Medium term (2-4 years) |

| Expat and Digital-Nomad Influx Driving Short-Term Storage Demand | +2.7% | Ho Chi Minh City, Hanoi, Da Nang, Nha Trang | Short term (≤ 2 years) |

| Home-Renovation and Hybrid-Work Furniture Storage Spike | +1.9% | Urban centers nationwide | Short term (≤ 2 years) |

| Government Push to Formalize Micro-Businesses Requiring Compliant Storage | +2.3% | National | Medium term (2-4 years) |

| Rising Affluent Collectors Seeking Climate-Controlled Units | +1.6% | Ho Chi Minh City, Hanoi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shrinking Urban Living Space Boosting Off-Site Storage

Vietnam’s largest cities see a steady rise in studio and one-bedroom rentals, with 40% of new leases in Ho Chi Minh City fitting that description.[1]Thanh Nguyen, “Urbanization and Forecast Possibilities of Land Use Changes by 2050,” De Gruyter Brill, degruyterbrill.com When coupled with median home prices equal to 32.5 times median household income, residents inevitably look beyond their walls for secure storage. Operators in the Vietnam self-storage market respond by positioning multi-story sites along ring roads where land is cheaper yet still close to dense residential clusters. The long-run nature of urban land compression gives providers the confidence to invest in purpose-built facilities equipped with 24/7 access and remote monitoring. Over the forecast horizon, these sites form a distributed grid that expands in step with city sprawl and contributes materially to the long-term growth of the Vietnam self-storage market.

E-Commerce SMEs’ Need for Micro-Fulfillment Space

With national online retail surpassing USD 20 billion in 2023 and rising roughly 29% each year, small sellers require scalable inventory points near customers.[2]DHL Editorial, “Logistics Trends Shaping SEA in 2025,” DHL Cambodia, dhl.com Flexible leases, pay-as-you-go fees, and embedded barcode tracking make self-storage an attractive middle ground between improvised spare-room stockpiles and full-scale warehousing. Leading operators now bundle cloud-based management dashboards, last-mile courier tie-ups, and secure unloading bays, effectively turning storage corridors into micro-fulfillment nodes. The Vietnam self-storage market benefits because the same square footage can earn higher turnover as goods cycle in and out more rapidly. Demand is densest in Ho Chi Minh City and Hanoi, yet secondary cities begin to emulate this pattern as regional e-commerce logistics mature.

Expat and Digital-Nomad Influx Driving Short-Term Demand

Vietnam’s visa-on-arrival ease, low cost of living, and vibrant tech scenes attract a transient population that values portability.[3]BoxLok Team, “Expats in Vietnam: The Ultimate Guide to Long-Term Storage Solutions,” BoxLok, boxnlok.vn Typical rentals run from 1,000,000 VND to 5,000,000 VND per month depending on climate control and concierge services, and many opt for premium tiers offering English-language support and biometric entry. Short tenure means high churn, so occupancy analytics and automated billing become critical. Providers tap this segment by promoting flexible month-to-month contracts, app-based reservations, and free pickup within city limits. Revenues from this niche spill into larger units as nomads establish longer residencies, supporting the Vietnam self-storage market even in shoulder seasons.

Home-Renovation and Hybrid-Work Furniture Storage Spike

The shift to hybrid work has households repurposing living areas into offices, triggering short bursts of demand when furniture is stored off-site during remodels. Construction supply bottlenecks stretch project timelines, lengthening average stay per unit. Operators see weekday access peaks as contractors collect or return materials, prompting extensions of staffed hours and the rollout of secure loading docks. Though episodic, renovation-related demand lifts the Vietnam self-storage market during periods when consumer move-outs slow, smoothing revenue across the calendar.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarce Central-District Land Elevating Facility Rental Costs | -2.1% | Ho Chi Minh City, Hanoi | Long term (≥ 4 years) |

| Ambiguous Licensing Framework Causing Permitting Delays | -1.8% | National | Medium term (2-4 years) |

| Low Consumer Awareness Beyond Ho Chi Minh City | -1.6% | Secondary cities and provinces | Medium term (2-4 years) |

| FX-Driven Capex Volatility for Imported Modular Units | -0.9% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarce Central-District Land Elevating Facility Costs

Prime sites inside District 1 and District 3 cost multiples of peripheral zones, squeezing feasibility for ground-up builds. Multi-story conversions of obsolete retail and commercial property partially offset land scarcity but carry higher structural retrofit expenses. Many operators pivot to ring-road parcels where entry costs are affordable, then rely on shuttle pickup to maintain customer convenience. These work-arounds keep the Vietnam self-storage market expanding yet shave a few points off potential CAGR, especially for entrants lacking patient capital.

Ambiguous Licensing Framework Causing Permitting Delays

Vietnam lacks a clearly defined self-storage category, so developers must navigate warehouse, retail, and general-service regulations simultaneously. Approval layers vary by district, leading to timeline slippage, escalating interest costs, and non-uniform fire-safety interpretations. While industry associations lobby for standardized rules, seasoned players mitigate risk by pre-consulting with local authorities and phasing projects to secure incremental permits. Regulatory opacity slows velocity but has not derailed the long-range expansion of the Vietnam self-storage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Business Segment Accelerates Through E-Commerce Integration

The consumer segment retained 67.20% of Vietnam self-storage market share in 2025 on the back of rising urban middle-class purchasing power. Shrinking apartments mean families send bulky furniture, seasonal décor, and recreational gear to off-site units, anchoring baseline occupancy. Vietnam self-storage market size attributable to urban residents is expected to advance steadily but at a lower clip than business demand. The business cohort, currently smaller, is expanding at an 18.58% CAGR to 2031, reflecting the surge of SMEs formalizing operations and seeking compliant storage. Operators courting this segment roll out plug-and-play inventory portals, barcode scanning, and temperature-monitored aisles that align with new packaging and EPR rules.

Momentum in the business segment feeds directly into higher revenue per square foot because turnover of parcels is faster than household belongings. Value-added logistics, such as pick-and-pack or last-mile dispatch desks, generate fee layers beyond core rent. Throughout the review period, the Vietnam self-storage industry sees cross-selling of insurance, seasonal surplus space, and late-night access packages as incremental boosters of average unit revenue. Successful facilities locate near arterial transport links to serve both city couriers and residential customers without sacrificing accessibility. This blend of demand cushions occupancy cycles and sustains the long-term trajectory of the Vietnam self-storage market.

By Facility Type: Climate-Control Premium Emerges Amid Tropical Challenges

Non-climate-controlled rooms commanded 56.40% of Vietnam self-storage market size in 2025 because they satisfy the majority of everyday needs at accessible price points. High humidity and temperature swings, however, pose risks to electronics, artwork, and wooden antiques. Wealthier collectors and corporate archives now account for a growing slice of bookings in climate-controlled aisles where humidity remains under 55% and ambient temperature stays below 25 °C. Differentiation strategies involve HEPA-filtered ventilation, remote environmental monitoring, and tiered pricing that encourages upsell. Operators forecast the premium tier to grow faster than the general pool, widening both unit spread and total revenue within the Vietnam self-storage market.

Valet and full-service concepts, on track for 22.85% CAGR, solve last-mile pain points by picking up items directly from customers and storing them in centralized depots. This format is capital-light on storefront space yet demands route-optimization software and multi-temperature vans, capabilities increasingly sourced through tech partnerships. Outdoor containerized storage targets construction firms and event contractors needing oversized or irregular-shape space, often in industrial belts outside the urban ring. Each facility archetype serves a distinct client set, underscoring how the Vietnam self-storage market diversifies to capture multiple layers of demand without diluting its core proposition.

By Unit Size: Micro-Units Capture Digital-Nomad Momentum

Medium-sized rooms of 26–50 sq ft held 43.60% of Vietnam self-storage market size in 2025, striking an ideal cost-to-volume balance for urban households and side-hustle entrepreneurs. Digital nomads and expatriates drive the traction of lockers under 25 sq ft, a niche forecast to grow at 19.76% CAGR through 2031. High turnover and premium service features, such as app-based biometric entry, permit operators to price these micro-units at higher yields per square foot. The Vietnam self-storage market therefore extracts more value from the same footprint by mixing small and mid-sized units inside one building.

Large rooms above 100 sq ft attract corporations storing seasonal inventory and affluent families archiving heirlooms, yet account for a smaller slice of occupancy because land costs discourage low-density layouts. Variable pricing strategies ensure every tier delivers margin, with lockers rented on daily tallies as low as USD 0.21, while larger rooms clear USD 43 each month. Across all sizes, cloud-connected sensors feed real-time occupant data to dashboards, letting managers upsell climate control or extend contracts before expiry. Such operational intelligence is rapidly becoming standard across the Vietnam self-storage market.

By Application Use-Case: E-commerce Fulfillment Transforms Traditional Storage Paradigms

E-commerce micro-fulfillment has emerged as the fastest-growing application segment, driven by Vietnam's explosive online retail growth which exceeded USD 20 billion in 2023 with a 29% annual growth rate, 2024. This application represents a fundamental shift from traditional storage concepts, as businesses transform self-storage units into operational logistics hubs equipped with inventory management systems and integrated with last-mile delivery networks. The segment's expansion is particularly pronounced among SMEs that prefer flexible mini-storage solutions over traditional warehousing, with operators like MyStorage reporting that business clients now form a significant portion of their customer base. Personal household goods currently dominates by volume, encompassing excess furniture, electronics, and personal belongings that urban residents cannot accommodate in increasingly compact living spaces where over 40% of new rentals are studios or serviced apartments.

Business inventory and documents storage is experiencing steady growth as Vietnam's formalization of micro-businesses creates compliance requirements for proper record-keeping and inventory management. The implementation of Extended Producer Responsibility (EPR) regulations effective January 2024 has intensified demand for compliant storage solutions, particularly among businesses handling packaging materials that must meet specific recycling targets Nguyen, 2025. Furniture and renovation storage represents a cyclical but lucrative segment, driven by Vietnam's expanding middle class and their increasing propensity for home improvements as disposable income rises. Seasonal items and sports gear storage, while smaller in volume, commands premium pricing due to the specialized handling requirements and the seasonal nature of demand, particularly for equipment used during Vietnam's distinct wet and dry seasons. The convergence of these application segments is creating opportunities for operators to develop specialized facilities with features tailored to specific use cases, such as climate-controlled units for sensitive business documents or accessible ground-floor units optimized for frequent e-commerce inventory turnover.

Geography Analysis

Southern Vietnam anchors demand momentum, with Ho Chi Minh City generating the highest absolute revenue and housing the densest network of multi-story sites. Peripheral districts such as Thu Duc benefit from new metro lines and ring-road extensions, allowing self-storage operators to tap cost-effective parcels while staying within a 20-minute drive of key residential towers. The Vietnam self-storage market, already clustered along East-West traffic corridors, leverages this infrastructure to roll out valet routes that cover both CBD and suburban pickup windows. Developers in the south emphasize vertical expansion, converting obsolete retail shells into six-floor facilities that extract value from tight footprints.

Northern Vietnam follows a slightly different pattern where mixed-use developments integrate storage levels beneath residential blocks in Hanoi’s emerging urban districts. Tenants appreciate on-premise access, and property developers gain a recurring income stream that stabilizes project cash flow. Vietnamese and Singaporean joint ventures are behind several of these hybrid complexes, giving foreign investors a foothold in the Vietnam self-storage market without direct land purchases. Regulatory acceptance of mixed-use designs accelerates project clears, offsetting licensing ambiguity elsewhere.

Central and coastal provinces, led by Da Nang and Nha Trang, register early-stage adoption with only a handful of modern facilities yet growing tourist and expatriate inflows. Local authorities courting digital-nomad visa programs view self-storage as an essential service amenity, easing planning approvals for small-footprint buildings near coworking hubs. Although current contribution to overall Vietnam self-storage market share remains modest, the blended growth rate outpaces that of tier-1 cities, signaling a long runway once awareness campaigns take root. Improved highway connectivity and flight links into these secondary hubs are forecast to lift unit take-up as transient populations scale.

Competitive Landscape

Vietnam’s self-storage arena features roughly twenty active brands, with no single operator controlling a dominant majority of installed square footage. MyStorage, the local pioneer, reports 98% average occupancy and 50% annual revenue gains, illustrating the upside of first-mover proximity to high-rise condominiums. Extra Space Asia and StorHub import operational templates honed in Singapore and Hong Kong, bringing modular racking, dynamic pricing algorithms, and regional customer databases to capture early adopters looking for international-grade security. Their entry fosters healthy rivalry in the Vietnam self-storage market and sets new benchmarks for climate control and digital booking.

Partnerships and strategic capital infusions accelerate network build-out. BitcoinVN’s stake in MyStorage injects blockchain-based payment rails and real-time asset-tracking, differentiating customer experience and lowering fraud risk. Local firms such as KingKho and Saigon Storage harness home-field knowledge to secure council approvals quickly and adopt flexible lease formats prized by Vietnamese SMEs. They often beat multinational peers to land deals in district-level industrial zones, maintaining a defendable share even as foreign brands scale.

Technology constitutes the critical battleground. Operators deploy AI-driven occupancy forecasts to calibrate discount ladders and margin per square foot, while mobile dashboards alert customers to humidity shifts and overdue bills. Up-selling of insurance, padlock upgrades, and 24-hour concierge access layers revenue without additional footprint. Consolidation is expected once early growth moderates, and well-capitalized players eye bolt-on acquisitions to extend service into secondary cities. Regardless of mergers ahead, customer preferences for digital convenience and transparent pricing will dictate the winners in the Vietnam self-storage market.

Vietnam Self-Storage Industry Leaders

-

MyStorage

-

Saigon Storage

-

TITAN Containers

-

Extra Space Asia Corporate

-

KingKho Mini Storage

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BitcoinVN invested in MyStorage, injecting capital for multi-site expansion and introducing blockchain payment options.

- March 2025: Extra Space Asia and StorHub confirmed new facilities in Ho Chi Minh City and Hanoi, leveraging regional playbooks to fast-track market entry.

- February 2025: EFEX upgraded its fulfillment suite, expanding warehouse infrastructure and rolling out a pay-as-you-go model aligned to the needs of Vietnamese e-commerce sellers.

- July 2024: SPX Express and Frasers Property Vietnam allocated USD 30 million to an automated sorting center in Binh Duong province, a development expected to improve last-mile links for storage firms.

Vietnam Self-Storage Market Report Scope

Self-storage offers value to continue protection from environmental damage and theft by providing cost-effective storage solutions. The study scope of the Vietnam self-storage market tracks down the adoption of different self-storage solutions used by business customers and domestic consumers. The study also focuses on the impact of COVID-19 on the market ecosystem. In the study scope, the existing storage manufacturers landscape also covered, which consists of major players operating in the country market.

By End-User

| Consumer |

| Business |

By Facility Type

| Climate-Controlled Facilities |

| Non-Climate-Controlled Facilities |

| Valet / Full-Service Storage |

| Containerised Outdoor Storage |

By Unit Size

| Greater than 25 sq ft (Locker) |

| 26 – 50 sq ft (Small) |

| 51 – 100 sq ft (Medium) |

| Less than 100 sq ft (Large) |

By Application Use-Case

| Personal Household Goods |

| Seasonal Items and Sports Gear |

| Furniture and Renovation Storage |

| Business Inventory and Documents |

| E-commerce Micro-Fulfillment |

By Geography (City)

| Ho Chi Minh City |

| Hanoi |

| Da Nang and Central Coast |

| South-East Industrial Provinces (Binh Duong, Dong Nai) |

| Other Regions (Can Tho and Mekong, Northern Provinces) |

| By End-User | Consumer |

| Business | |

| By Facility Type | Climate-Controlled Facilities |

| Non-Climate-Controlled Facilities | |

| Valet / Full-Service Storage | |

| Containerised Outdoor Storage | |

| By Unit Size | Greater than 25 sq ft (Locker) |

| 26 – 50 sq ft (Small) | |

| 51 – 100 sq ft (Medium) | |

| Less than 100 sq ft (Large) | |

| By Application Use-Case | Personal Household Goods |

| Seasonal Items and Sports Gear | |

| Furniture and Renovation Storage | |

| Business Inventory and Documents | |

| E-commerce Micro-Fulfillment | |

| By Geography (City) | Ho Chi Minh City |

| Hanoi | |

| Da Nang and Central Coast | |

| South-East Industrial Provinces (Binh Duong, Dong Nai) | |

| Other Regions (Can Tho and Mekong, Northern Provinces) |

Key Questions Answered in the Report

What is the current size of the Vietnam self-storage market in 2026?

The market is valued at USD 127.52 million in 2026 and is projected to grow at a 15.93% CAGR to USD 266.65 million by 2031.

Why are small lockers growing faster than larger units?

Units below 25 sq ft cater to digital nomads and expatriates who need compact, short-term storage; this segment is posting a 19.76% CAGR, the fastest across all size tiers.

How much of the Vietnam self-storage market share does the consumer segment hold?

Consumers accounted for 67.20% of market share in 2025, reflecting widespread space constraints in urban apartments.

What makes valet or full-service storage attractive in Vietnam?

Traffic congestion and limited vehicle ownership in big cities make door-to-door pickup convenient, supporting a 22.85% CAGR for valet/full-service formats.

Are climate-controlled units necessary in a tropical climate?

Yes. High humidity threatens electronics, artwork, and wooden items, prompting affluent collectors and corporate archives to opt for climate-controlled rooms that maintain stable environmental conditions.

What regulatory hurdles do self-storage developers face in Vietnam?

The absence of a dedicated self-storage category forces projects to comply with mixed warehouse and service regulations, leading to longer permitting times and inconsistent local enforcement.

Page last updated on: