Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.62 Billion |

| Market Size (2026) | USD 7.34 Billion |

| Market Size (2031) | USD 11.44 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

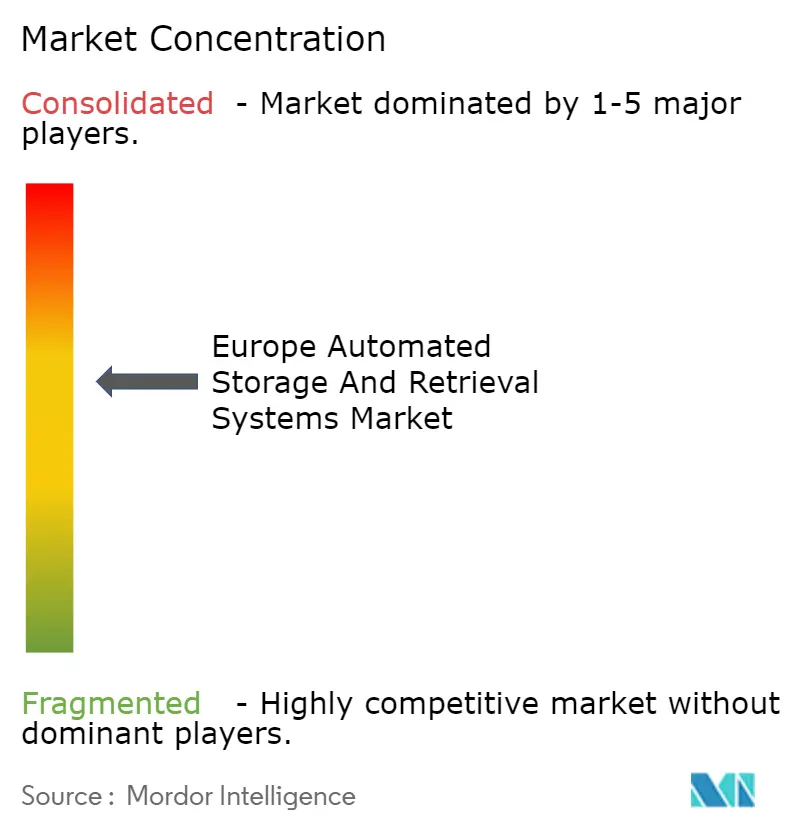

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automated Storage And Retrieval Systems Market Analysis by Mordor Intelligence

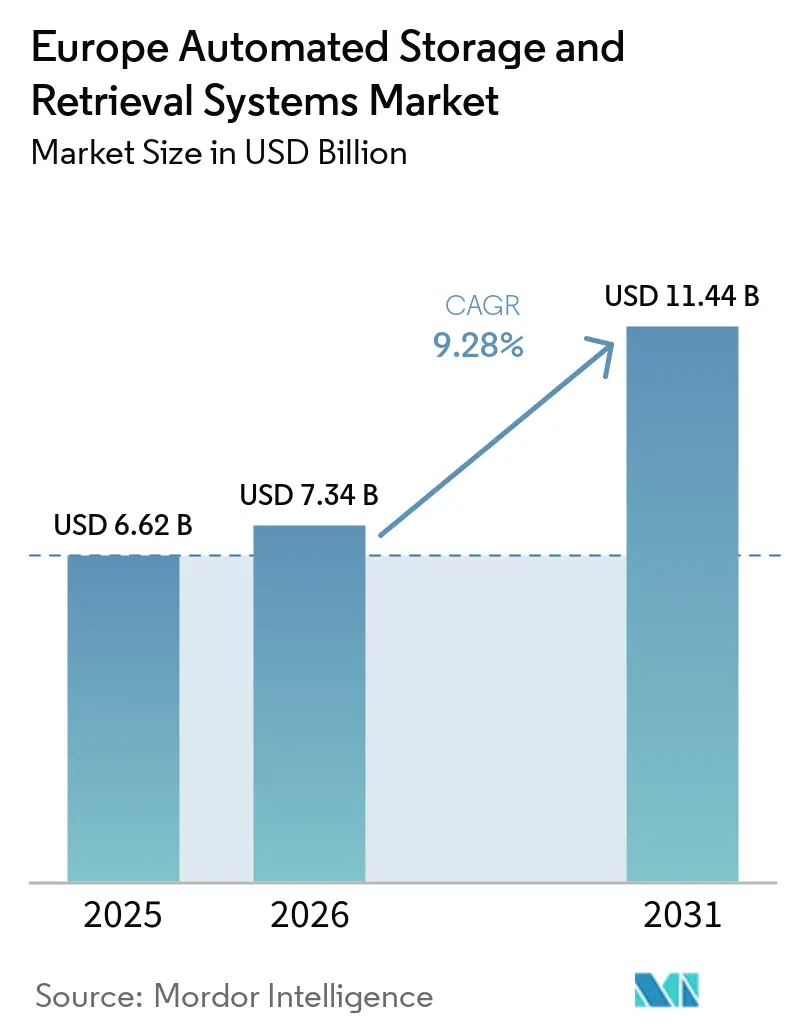

The Europe automated storage and retrieval systems market size is expected to grow from USD 6.62 billion in 2025 to USD 7.34 billion in 2026 and is forecast to reach USD 11.44 billion by 2031 at 9.28% CAGR over 2026-2031. Robust expansion is anchored in e-commerce fulfillment, which compresses order-to-ship windows to under one hour, escalates warehouse wages in high-cost labor markets, and is influenced by European Union regulations that tie energy-efficient automation to Net-Zero targets. Vendors are shifting emphasis from static capacity toward AI-driven throughput optimization, integrating modular shuttles, cube storage grids, and autonomous mobile robots under unified software control. Capital inflows are focusing on micro-fulfillment nodes within urban grocery stores, automotive just-in-time buffers, and pharmaceutical cold-chain hubs, while funding from Horizon Europe and the Digital Europe Program accelerates the diffusion of technology. Competitive intensity is shifting from hardware to software orchestration as integrators strive to demonstrate interoperability across mixed fleets and ensure a rapid return on investment.

Key Report Takeaways

- By product type, unit load ASRS held 35.24% of the Europe automated storage and retrieval systems market share in 2025, while shuttle and bot systems are forecast to expand at a 10.63% CAGR through 2031.

- By load capacity, medium load systems captured a 47.33% share of the Europe automated storage and retrieval systems market size in 2025; light load configurations are projected to advance at a 9.77% CAGR through 2031.

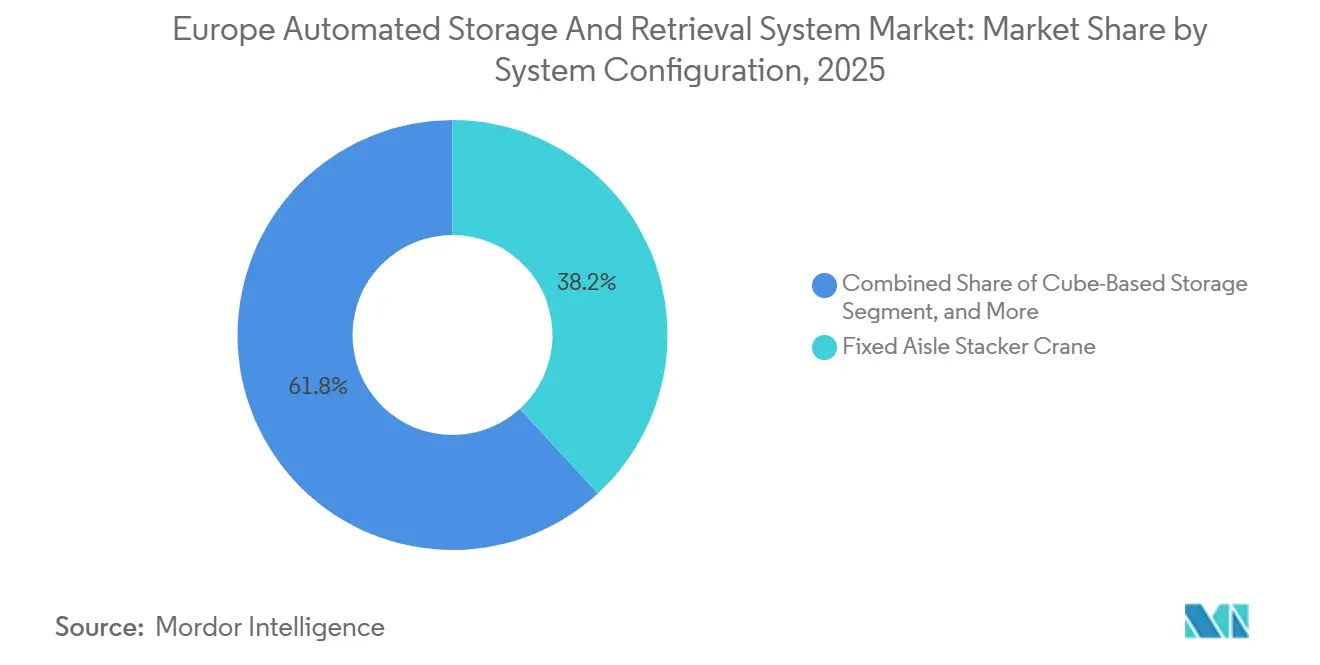

- By system configuration, fixed aisle stacker cranes accounted for 38.19% share in 2025, and cube-based storage architectures are set to grow at a 10.31% CAGR over the forecast period.

- By end-user vertical, retail and e-commerce represented 28.91% of demand in 2025, while micro-fulfillment installations are expected to post a 10.74% CAGR to 2031.

- By geography, Germany led with a 27.49% revenue share in 2025, and Spain is projected to record the highest CAGR of 10.59% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Automated Storage And Retrieval Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking Warehouse Space and Urban Land Costs | +1.8% | Germany, Netherlands, United Kingdom, France (urban logistics hubs) | Medium term (2-4 years) |

| E-commerce Surge Requiring High Throughput Fulfilment | +2.3% | Pan-European, with concentration in Germany, United Kingdom, France, Spain | Short term (≤ 2 years) |

| Rising Labor Shortages and Wage Inflation Across Europe | +1.9% | Germany, Netherlands, Nordic countries, United Kingdom | Medium term (2-4 years) |

| Advancements in AI-Driven Warehouse Execution Software | +1.4% | Germany, France, United Kingdom, Benelux (early adopters) | Long term (≥ 4 years) |

| ESG Mandates Driving Energy-Efficient Warehouse Automation | +1.1% | European Union member states (Net-Zero Industry Act 2024/1735, Ecodesign Regulation 2024/1781) | Long term (≥ 4 years) |

| EU Funding for Industry 4.0 and Digital Logistics Initiatives | +0.7% | All European Union member states and associated countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Surge Requiring High Throughput Fulfillment

Order volumes now demand sub-two-hour delivery in large metropolitan areas, compelling operators to deploy automated storage and retrieval systems capable of 6,000 pallet movements per day. A brownfield retrofit in Rumst, Belgium, achieved this benchmark by operating 20 autonomous shuttles across four levels and reusing existing racking, resulting in EUR 680,000 in capital expenditure savings and a reduction of 680 t of carbon emissions.[1]Movu Robotics, “ODTH and Movu Robotics set new benchmark in warehouse automation,” movu-robotics.com A United Kingdom facility, commissioned in December 2025, employs 200 robots across 3,000 m² to quadruple picking efficiency. Micro-fulfillment modules inserted into grocery backrooms further decentralize inventory and reduce last-mile costs, positioning modular shuttles and cube grids as the preferred architecture.

Rising Labor Shortages and Wage Inflation Across Europe

Logistics wages in Germany and the Netherlands advanced by double digits in 2025, compressing payback periods on automation to under three years. A survey of European operators revealed a 90% adoption rate of AI tools as firms rushed to offset labor shortages. Third-party logistics leaders now operate thousands of autonomous mobile robots across multi-temperature zones, blending collaborative automation with human quality control. The dynamic strengthens demand for shuttle systems that can run 24/7 without shift changeovers while maintaining occupational safety standards.

Shrinking Warehouse Space and Urban Land Costs

Prime land near ports and airports commands escalating rents, pushing distribution centers vertical. A cube-based grid at Oslo Airport lifted storage capacity by 64% within the same 318 m² footprint, cutting fulfillment time from six hours to one hour. In Finland, an 8,000-bin system, fitted into a 2,000 m² building, doubled capacity and allowed the conversion of legacy storage into production space.[2]Vaisala, “Vaisala to build new automated logistics center in Vantaa,” vaisala.com Such density premiums favor cube storage and shuttle elevators, particularly in Germany, the Netherlands, and the United Kingdom, where land scarcity is acute.

Advancements in AI-Driven Warehouse Execution Software

Modern execution platforms allocate tasks across heterogeneous fleets in real time, integrating directly with enterprise resource planning systems through standardized APIs. A Belgian retrofit interconnected shuttles, elevators, and conveyors under a single software layer, while Swiss Post’s Villmergen hub is slated to synchronize 23,000 pallet spaces, 20,000 trays, and 125,000 bins upon launch. Automotive plants utilize cloud scheduling to dynamically reroute automated tugger trains, highlighting software as the primary differentiator in vendor selection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure for SMEs | -1.2% | Pan-European, particularly Central and Eastern Europe and Southern Europe | Short term (≤ 2 years) |

| Integration Complexities with Legacy WMS and ERP | -0.9% | Germany, France, United Kingdom, Italy (mature logistics markets with installed base) | Medium term (2-4 years) |

| Limited Skilled Technicians for Maintenance | -0.6% | Central and Eastern Europe, Southern Europe, United Kingdom | Medium term (2-4 years) |

| Supply-Chain Disruptions Inflating Component Lead Times | -0.5% | Pan-European (semiconductor and programmable logic controller shortages) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for SMEs

Entry-level installations cost EUR 1 million, while high-bay projects can exceed EUR 20 million, excluding civil works. Only 8% of European SMEs had adopted advanced digital tools by 2024, citing financing constraints. While leasing and automation-as-a-service models are available, their presence is largely confined to Western Europe. This limited availability has slowed the adoption of these models by logistics firms in other regions, as they face challenges such as lack of infrastructure, awareness, and tailored solutions to meet their specific operational needs.

Integration Complexities with Legacy WMS and ERP

Brownfield projects must bridge proprietary protocols, often doubling commissioning timelines and adding 20-30% to budgets. One Belgian distributor required custom middleware to connect rail-guided vehicles and shuttle systems with incumbent software, underscoring the engineering burden. Vendors offering pre-built connectors for SAP, Oracle, and Microsoft Dynamics win disproportionate share, while equipment-only suppliers struggle to penetrate retrofit opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shuttle Systems Gain on Modular Scalability

Unit Load ASRS secured 35.24% of Europe Automated Storage and Retrieval Systems market share in 2025, reflecting the dominance of pallet-centric buffers at automotive and general manufacturing plants.[3]Swisslog, “ROCKWOOL partners with Swisslog for automated high-bay warehouse,” swisslog.com The Europe Automated Storage and Retrieval Systems market size tied to Shuttle and Bot Systems is projected to rise at a 10.63% CAGR as omnichannel retailers add robots in small tranches without re-engineering racking, a capability proven by Knapp’s OSR Shuttle Evo, which clears 1,000 bin picks per hour. Cube grids can disrupt space-constrained nodes, such as airport duty-free stores, where an AutoStore installation in Oslo increased capacity by 64% within the same 318 m² footprint.

Second-generation shuttle projects have reduced civil costs by EUR 680,000 and 680 tonnes of carbon at a Belgian brownfield site, while maintaining 6,000 pallet moves per day. Grocers plan similar grids inside backrooms, as shown by Axfood’s Kungsbacka project, to meet click-and-collect demand. Beverage producers favor hybrid layouts that merge pallet shuttles with cranes and conveyors under one SynQ layer, a model Ringnes will adopt from 2026.

By Load Capacity: Light Load Surges with Micro-Fulfillment

Medium-load systems, ranging from 100 kg to 500 kg, captured 47.33% of the European Automated Storage and Retrieval System market share in 2025, driven by pallet flows in automotive and third-party logistics corridors. Light-load units below 100 kg are projected to expand at a 9.77% CAGR as grocers and pharmacies integrate tote grids that fulfill orders in under 30 minutes. Vaisala’s 8,000-bin AutoStore grid, located within a 2,000 m² site, exemplifies the compact design trend. Roche’s Kaiseraugst hub demonstrates that tote automation also thrives in cooled drug warehouses, where 1,500 pallet moves occur daily at temperatures ranging from +2 °C to +8 °C.

Urban retailers require small payload speed, so Light Load modules now command a growing share of the European Automated Storage and Retrieval System market, especially in Spain and France, where click-and-collect volumes surge on weekends. Automotive plants still rely on Medium-Load tugger trains for sequenced parts, blending load classes under a single software stack. Heavy Load lanes remain a niche service, serving beverage kegs at Ringnes’s forthcoming shuttle complex, which will transport 1,000 kg pallets within ambient and chilled zones.

By System Configuration: Cube Storage Disrupts Fixed-Aisle Dominance

Fixed-aisle stacker cranes accounted for 38.19% of 2025 revenue, due to their proven reliability in high-bay warehouses, such as ROCKWOOL’s 35,000-pallet project in Germany. The Europe Automated Storage and Retrieval Systems market size attached to Cube-Based Storage is forecast to climb at a 10.31% CAGR, as the aisle-free grid maximizes every cubic meter, a benefit that enabled Oslo Airport to boost storage density by 64%. Moveable-Aisle cranes still serve archival rooms, while free-roaming shuttles thrive in third-party logistics halls that reconfigure layouts seasonally.

Hybrid complexes are multiplying, mixing cranes, shuttles, and autonomous mobile robots under unified execution software that simulates flows before hardware arrives. Swiss Post will bring 23,000 pallet slots, 20,000 trays, and 125,000 AutoStore bins under one SynQ layer when its expansion goes live. Brussels Airport is installing semi-automatic baggage modules that connect to early-bag storage zones, indicating aviation's interest in mixed fleets. As operators demand openness over proprietary stacks, configuration diversity widens, and the uptake of cube and shuttle solutions accelerates across the region.

By End-User Vertical: Retail and Pharma Drive High-Velocity Demand

Retail and E-commerce accounted for 28.91% of the European Automated Storage and Retrieval System market share in 2025, and micro-fulfillment grids inside stores are on track for a 10.74% CAGR as grocers chase 30-minute pickup windows. Third-party logistics firms follow, with DHL operating 35 AutoStore systems and 2,000 robots to handle surges in consumer goods. Automotive plants such as BMW Regensburg log 10,000 daily tugger-robot trips to meet just-in-time sequencing, underpinning steady crane demand.

Pharmaceutical distributors are accelerating cold-chain automation, exemplified by Roche’s controlled-temperature hub, which processes up to 1,500 pallet moves per day. Food and beverage groups are adopting shuttle systems that straddle ambient and chilled lanes, mirroring the Ringnes brewery blueprint, slated for completion in 2027. Airports expand robotic storage for duty-free and baggage flows, while general manufacturing outfits fit mini-load cranes for component buffers. Each vertical selects hardware that matches order velocity, regulatory burden, and temperature needs, pushing software vendors to integrate heterogeneous fleets at scale.

Geography Analysis

Germany sustained the largest slice of regional revenue at 27.49% in 2025, underpinned by automotive original equipment manufacturers and dense third-party logistics corridors. A 35,000-pallet high-bay warehouse, set to start construction in February 2026, illustrates the continued appetite for large-scale projects. Wage inflation exceeding 10% in logistics roles accelerates adoption, and federal programs subsidize energy-efficient upgrades. Spain, predicted to log a 10.59% CAGR, benefits from greenfield e-commerce hubs such as a 175,000-m² robotized site in Asturias that automates 40,000 m² zones to serve Southern Europe. The United Kingdom aligns automation with post-Brexit supply chain restructuring, as highlighted by a 200-robot facility delivering next-day commitments.

France operates as a continental gateway, yet it grapples with strict labor codes and protracted permitting, which delays some deployments. Italy’s focus centers on food, beverage, and automotive parts, with regional integrators tailoring shuttle platforms to multi-temperature requirements. Central and Eastern Europe leverages nearshoring momentum, erecting buffer storage for component suppliers feeding Western European vehicle plants.

Scandinavian adoption scales despite smaller volumes thanks to acute labor shortages and high wage floors, exemplified by Finnish and Norwegian projects that combine pallet shuttles, conveyors, and AI orchestration. Collectively, these dynamics create a two-speed Europe Automated Storage And Retrieval Systems market: retrofit-heavy Western nodes and greenfield-heavy Southern and Eastern corridors.

Competitive Landscape

The five largest suppliers control near 45% of regional revenue. Hardware incumbents now differentiate themselves through software stacks, digital twin simulation, and reference pilots. A leading vendor’s order intake dipped 7.1% year-over-year in Q3 2024 as customers demanded proof-of-concept demonstrations before capital commitment, highlighting tightening pricing power.

Swisslog couples cube storage with proprietary SynQ software in turnkey packages and recently secured a CHF 40 million (USD 51.5 million) hospital logistics project that fuses high-bay, medium-parts, and bin storage under one platform. Pure-play software entrants capture retrofit opportunities by offering API-rich execution layers that sit atop legacy equipment, as illustrated by a Belgian installation that integrated shuttles with SAP without modifying the incumbent conveyors.

AutoStore’s dense cube grids are favored in airports and pharmaceuticals, delivering a 64% storage gain at Oslo Airport. Regional integrators excel in vertical niches: pharmaceutical cold-chain specialists offer modular refrigerated shuttles, while automotive service providers optimize tugger-train routing inside plants. Vendors increasingly pitch leasing models and per-pick pricing to court SMEs, though financing partners remain sparse in Central and Eastern Europe. Over the forecast horizon, ecosystem openness rather than proprietary hardware will shape share shifts across the European Automated Storage And Retrieval System market.

Europe Automated Storage And Retrieval Systems Industry Leaders

Daifuku Co. Ltd

KION Group AG

SSI Schaefer AG

Knapp AG

Swisslog AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: JD Logistics inaugurated a 200-robot facility in the United Kingdom to serve fashion and electronics retailers with next-day delivery.

- October 2025: Swisslog won a contract from Ringnes to automate Norway’s largest brewery using PowerStore pallet shuttles, automated guided vehicles, and SynQ software, with completion set for H1 2027.

- September 2025: ROCKWOOL partnered with Swisslog to build a 35,000-pallet high-bay warehouse in Germany, breaking ground in Feb 2026.

- August 2025: Movu Robotics and ODTH completed Phase 1 of their Belgian brownfield project, reusing existing racking and avoiding 680 t of CO₂ emissions.

Europe Automated Storage And Retrieval Systems Market Report Scope

The Europe Automated Storage And Retrieval Systems Market Report is Segmented by Product Type (Unit Load ASRS, Mini Load ASRS, Shuttle and Bot Systems, Carousel Systems Horizontal, Carousel Systems Vertical, Vertical Lift Modules, Hybrid Integrated Systems), Load Capacity (Light Load (Below 100 kg), Medium Load (100-500 kg), Heavy Load (Above 500 kg)), System Configuration (Fixed Aisle Stacker Crane, Moveable Aisle Crane, Cube-Based Storage, Free-Roaming Robotic Shuttles, Micro-Fulfilment Modules), End-User Vertical (Airports, Automotive, Retail and E-commerce, Third-Party Logistics Providers, General Manufacturing, Food and Beverage, Pharmaceuticals, Other End-User Verticals), and Geography (United Kingdom, Germany, France, Italy, Spain, Central and Eastern Europe, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Unit Load ASRS |

| Mini Load ASRS |

| Shuttle and Bot Systems |

| Carousel Systems, Horizontal |

| Carousel Systems, Vertical |

| Vertical Lift Modules |

| Hybrid Integrated Systems |

By Load Capacity

| Light Load (Below 100 kg) |

| Medium Load (100-500 kg) |

| Heavy Load (Above 500 kg) |

By System Configuration

| Fixed Aisle Stacker Crane |

| Moveable Aisle Crane |

| Cube-Based Storage |

| Free-Roaming Robotic Shuttles |

| Micro-Fulfilment Modules |

By End-User Vertical

| Airports |

| Automotive |

| Retail and E-commerce |

| Third-Party Logistics Providers |

| General Manufacturing |

| Food and Beverage |

| Pharmaceuticals |

| Other End-User Verticals |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Central and Eastern Europe |

| Rest of Europe |

| By Product Type | Unit Load ASRS |

| Mini Load ASRS | |

| Shuttle and Bot Systems | |

| Carousel Systems, Horizontal | |

| Carousel Systems, Vertical | |

| Vertical Lift Modules | |

| Hybrid Integrated Systems | |

| By Load Capacity | Light Load (Below 100 kg) |

| Medium Load (100-500 kg) | |

| Heavy Load (Above 500 kg) | |

| By System Configuration | Fixed Aisle Stacker Crane |

| Moveable Aisle Crane | |

| Cube-Based Storage | |

| Free-Roaming Robotic Shuttles | |

| Micro-Fulfilment Modules | |

| By End-User Vertical | Airports |

| Automotive | |

| Retail and E-commerce | |

| Third-Party Logistics Providers | |

| General Manufacturing | |

| Food and Beverage | |

| Pharmaceuticals | |

| Other End-User Verticals | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Central and Eastern Europe | |

| Rest of Europe |

Key Questions Answered in the Report

How fast is demand for automated storage and retrieval solutions growing in Europe?

The Europe Automated Storage And Retrieval System market is projected to rise at a 9.28% CAGR between 2026 and 2031, moving from USD 7.34 billion to USD 11.44 billion.

Which countries lead adoption of automated storage and retrieval systems?

Germany accounts for 27.49% of regional revenue thanks to its automotive and logistics clusters, while Spain is the fastest-growing with a 10.59% CAGR through 2031.

What technologies are displacing traditional fixed-aisle cranes?

Modular shuttle systems and cube-based storage grids are expanding rapidly, with Shuttle and Bot Systems forecast to post a 10.63% CAGR and cube architectures a 10.31% CAGR.

Why are Light Load systems gaining traction?

Growth in urban micro-fulfillment and online pharmaceuticals favors tote-handling solutions, driving Light Load configurations to a 9.77% CAGR over the forecast horizon.

What is driving software innovation in European warehouses?

Operators prioritize real-time orchestration across mixed fleets of robots, shuttles, and conveyors, turning AI-driven warehouse execution platforms into the primary differentiator among suppliers.

How does rising labor cost influence investment decisions?

Double-digit wage inflation in logistics roles compresses payback periods on automation to under three years, accelerating capital allocation toward high-throughput solutions that reduce manual dependence.

Page last updated on: