Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

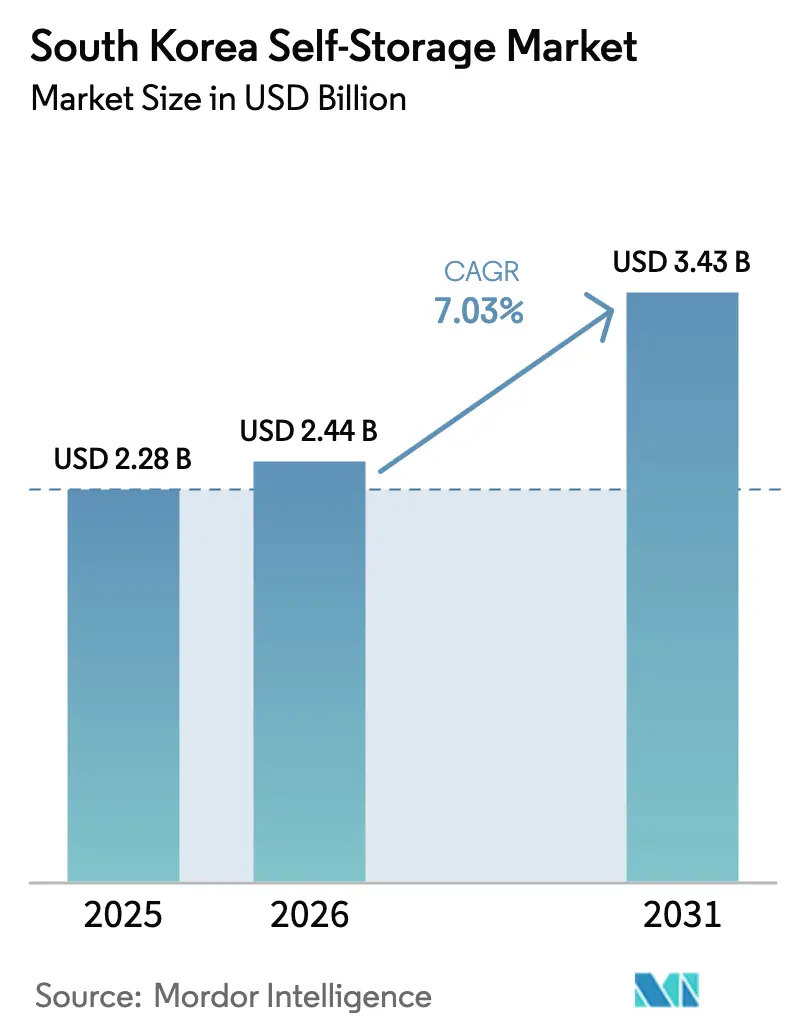

| Base Year Market Size (2025) | USD 2.28 Billion |

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

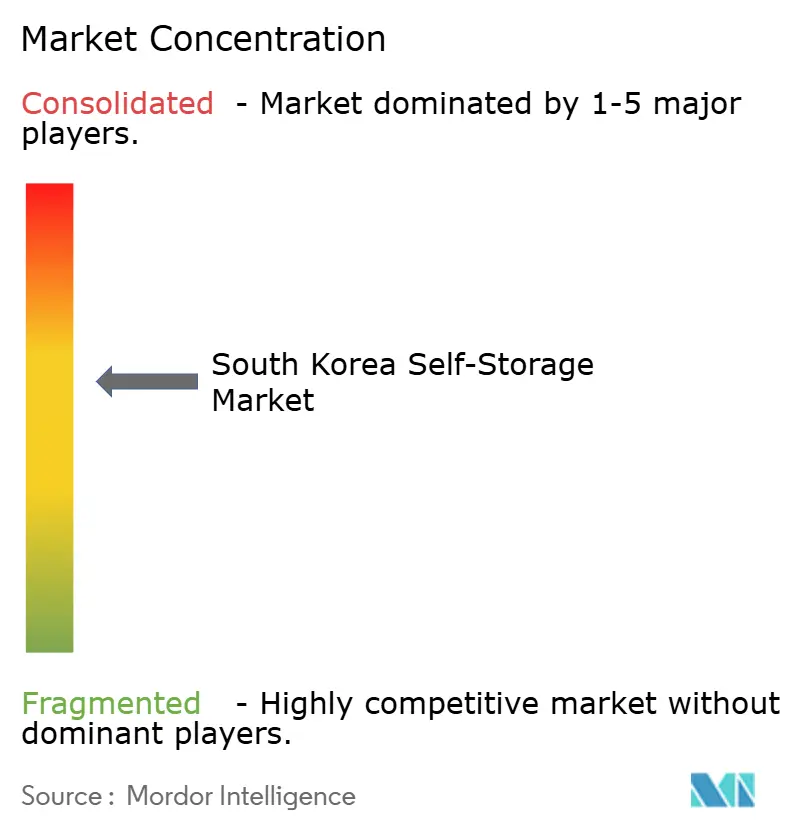

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Self-Storage Market Analysis by Mordor Intelligence

The South Korea self-storage market size is expected to grow from USD 2.28 billion in 2025 to USD 2.44 billion in 2026 and is forecast to reach USD 3.43 billion by 2031 at 7.03% CAGR over 2026-2031. Demand aligns with rapid urban densification, mounting space constraints, and the shift toward single-person households, which already account for more than one-third of residences in the country. Operators are broadening footprints to secondary metros while upgrading facilities with automation to lift utilization and tap high-margin premium services. At the same time, small and mid-sized e-commerce sellers are adopting flexible storage as a cost-efficient alternative to long-term warehousing contracts. Consolidation has begun as well-capitalized incumbents secure prime city locations and invest in digital platforms, raising barriers for late entrants. Regulatory compliance and fire-safety capital outlays temper new builds, but they also provide durable moats for established providers.

Key Report Takeaways

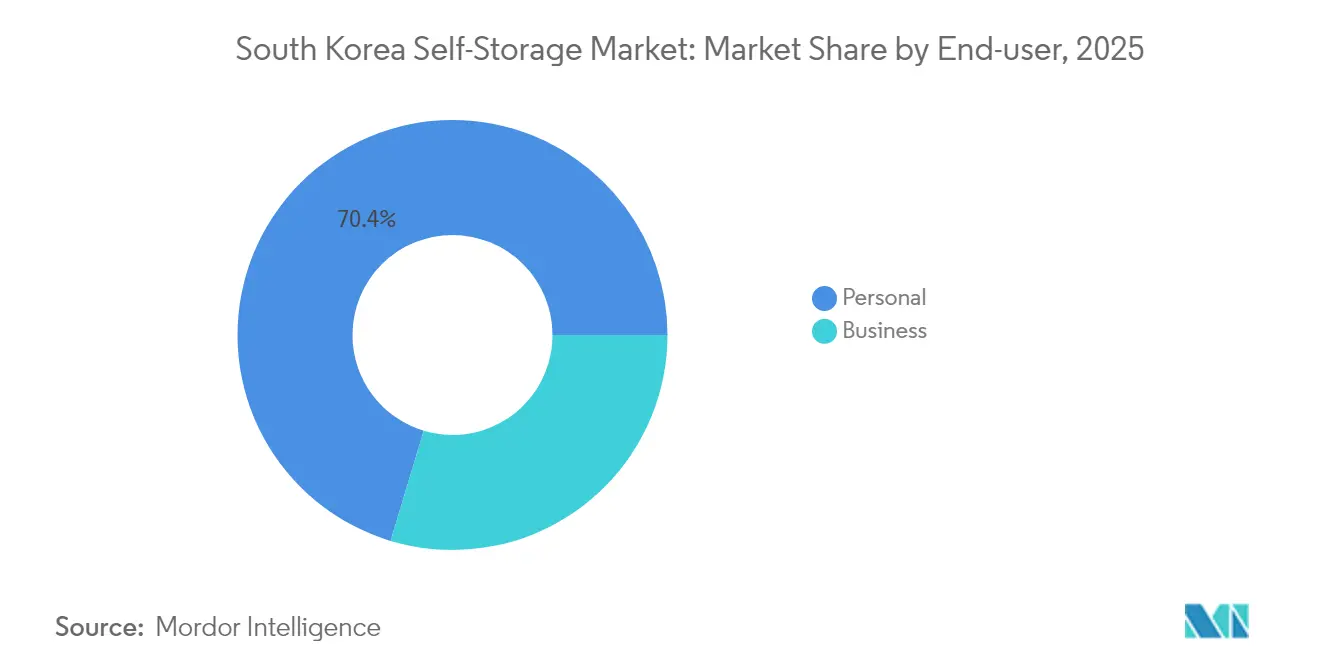

- By end-user, personal users held 70.35% of South Korea self-storage market share in 2025, whereas the business segment is expanding at a 8.75% CAGR through 2031.

- By storage unit size, small units (1–3 m²) led with 41.30% share of the South Korea self-storage market size in 2025, while the XXS/XS category (<1 m²) is growing at a 10.05% CAGR.

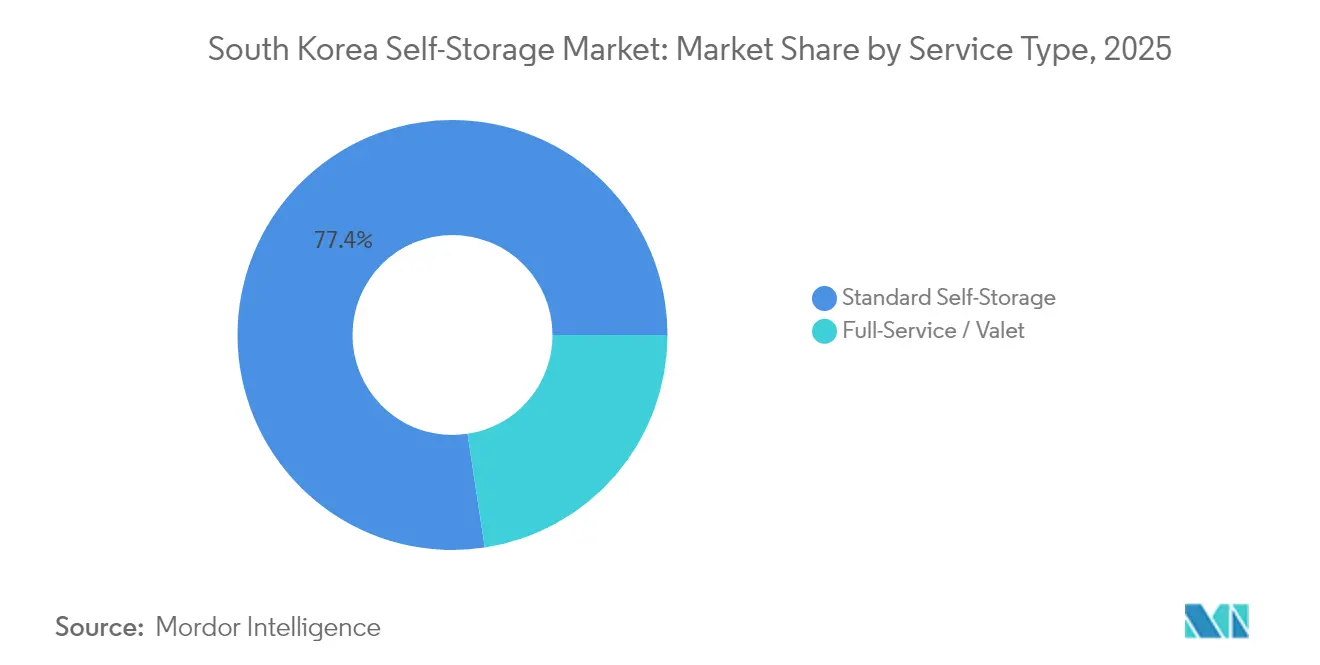

- By service type, standard self-storage commanded 77.40% revenue share in 2025; full-service valet offerings are forecast to post an 7.82% CAGR to 2031.

- By application, household goods and seasonal items accounted for 39.60% share of the South Korea self-storage market size in 2025; e-commerce inventory storage is advancing at a 9.35% CAGR.

- By region, Seoul-city captured 53.60% of South Korea self-storage market share in 2025, while Busan-Ulsan-Gyeongnam is the fastest-growing cluster at an 8.08% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Self-Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization & shrinking average floor space | +2.1% | Seoul Capital Area; spillover to Busan-Ulsan-Gyeongnam | Medium term (2-4 years) |

| Rising housing prices & jeonse deposit squeeze | +1.8% | Seoul-city core; extending to Gyeonggi-do suburbs | Short term (≤ 2 years) |

| E-commerce micro-fulfillment demand | +1.4% | National; focus on Seoul and Busan logistics corridors | Long term (≥ 4 years) |

| Live-commerce broadcasters’ inventory spikes | +0.9% | Seoul Capital Area; emerging in Daegu-Gyeongbuk | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanization & Shrinking Average Floor Space

South Korea’s metropolitan build-up continues to outpace residential floor-space additions, creating a durable storage gap. Single-person households are projected to edge toward 40% of total households by mid-century, a demographic that tends to maximize every square meter of living area. Developers are prioritizing unit count over floor space per dwelling, intensifying the need for external “closet” capacity. Leading operator Mini Warehouse Darak reports utilization above 90% at more than 100 Seoul-area locations, underscoring tight supply.[1]Mini Warehouse Darak, "Mini Warehouse Attic’, Darak, dalock.kr The runway is unlikely to diminish in the medium term because zoning policies still favor residential and commercial projects over storage-specific permits

Rising Housing Prices & Jeonse Deposit Squeeze

Record jeonse deposits now exceed USD 500,000 in Seoul’s premium districts, pushing families into smaller apartments and driving demand for supplemental storage. The financial strain is immediate: tenants downsize to meet deposit requirements yet retain furniture that no longer fits at home. Storage facilities profit from both the initial move-in spike and prolonged retention, as households defer larger home upgrades until deposits ease. Government housing programs that deliver smaller subsidized units inadvertently amplify off-site storage needs.

E-commerce Micro-fulfillment Demand

Mobile purchases already represent 74% of South Korea’s online sales, and food alone makes up 30% of total e-commerce value.[2]U.S. Department of Agriculture, "South Korea Food Ecommerce Market", USDA, apps.fas.usda.gov Tier-one players such as Coupang are pouring USD 2.24 billion into fulfillment hubs, but small and medium sellers rely on pay-as-you-go self-storage to keep last-mile inventory close to customers.[3]Yoon Young-sil, "Coupang to Invest 3 Trillion Won for Logistics Infra Expansion", Business Korea, businesskorea.co.krFacilities equipped with 24-hour access and app-based stock tracking are positioning themselves as micro-fulfillment partners, unlocking premium pricing and longer tenancy.

Live-commerce Broadcasters’ Inventory Spikes

Live-commerce—a blend of streaming and retail—requires broadcasters to hold diverse product samples that turn over rapidly. Studios in Seoul’s Gangnam and Hongdae districts frequently rent short-term storage during promotional events, producing episodic, high-margin demand. Operators are responding by offering photo booths, packing stations, and lightning-fast pickup protocols that align with broadcast schedules, thereby monetizing a niche yet growing user base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of suitable urban real-estate plots | -1.3% | Seoul Capital Area; acute in CBD zones | Long term (≥ 4 years) |

| High conversion cap-ex & fire-protection standards | -0.8% | National; strongest in dense metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Suitable Urban Real-estate Plots

Competing land uses in central Seoul command valuations that often surpass the breakeven threshold for storage facilities. Zoning legislation rarely carves out dedicated provisions for self-storage, forcing bidders to match prices paid by offices or residential developers. The result is a defensive moat for incumbents, yet it suppresses organic capacity growth and channels future projects toward less convenient outskirts.

High Conversion Cap-ex & Fire-protection Standards

Multi-story conversions must comply with warehouse-grade sprinkler and detection systems, lifting project costs by as much as 30%. Academic safety reviews highlight the need for specialized suppression in rack-type environments.[4]Choi, Ki-Ok, and Don-Mook Choi, "A Study on Improvement of Installation Provision for Fire Detection and Suppression System in Rack-Type Warehouse.", j-kosham.or.kr.Smaller entrants struggle to raise the upfront capital, tilting the market toward operators with deeper balance sheets or listed-entity backing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Personal Dominance Masks Business Acceleration

Personal users accounted for 70.35% of revenue in 2025, reflecting deep consumer adoption of the South Korea self-storage market. Households leverage units to offset limited apartment closets during seasonal wardrobe changes and frequent moves. Utilization spikes at quarter-ends when leases renew and during public holidays when families reorganize living areas.

The business segment, though smaller, is set to record a 8.75% CAGR through 2031 as SMEs and start-ups embrace flexible inventory solutions. Entrepreneurs view the South Korea self-storage industry as a variable-cost extension of their supply chains, sidestepping multiyear warehouse leases. Hybrid use is rising, with sole proprietors storing both personal goods and e-commerce stock in the same facility, blurring traditional boundaries.

By Storage Unit Size: Micro-storage Disrupts Traditional Sizing

Small units (1–3 m²) maintained a 41.30% share in 2025, yet the sub-1 m² band is growing at 10.05% annually, outpacing all other sizes in the South Korea self-storage market. Millennials prefer these micro-lockers for sports gear or seasonal décor, prioritizing proximity over volume.

Operators are re-engineering floorplates with denser vertical layouts and automated retrieval, squeezing more rentable lockers into fixed footprints. This shift improves yield per square meter and aligns with evolving urban lifestyles that favor renting over owning bulky items.

By Service Type: Valet Services Challenge Standard Model

Standard access solutions still dominate with 77.40% share in 2025, benefiting from lower price points and customer familiarity. The South Korea self-storage market size for valet services, however, is expected to grow at an 7.82% CAGR as time-poor professionals outsource pickup and delivery.

Digital platforms enable remote inventory visibility and app-driven scheduling, narrowing the convenience gap between standard and valet tiers. Economies of scope arise when providers layer paid transport on top of core rent, boosting revenue per user without proportionate capital outlay.

By Application: E-commerce Inventory Transforms Storage Purpose

Household goods and seasonal items held 39.60% revenue in 2025, anchoring the traditional demand base. E-commerce inventory storage is now the fastest climber at a 9.35% CAGR, underscoring Korea’s digital commerce maturity.

Facilities have begun offering barcode-based stock management, climate-controlled zones for perishables, and same-day courier hand-offs. These add-ons elevate stickiness and justify premium rents, propelling the South Korea self-storage market size allocated to commercial items.

Geography Analysis

Seoul Capital Area remains the nucleus of demand thanks to unparalleled population density and elevated commercial activity. Self-storage fills structural space gaps in apartments that rank among the smallest, globally, on a per-capita basis. Suburban Gyeonggi-do supports spill-over demand as commuters seek larger homes while retaining city jobs, generating peak rental activity during bi-annual moving seasons.

Busan-Ulsan-Gyeongnam’s 8.08% CAGR reflects port-driven commerce and infrastructure upgrades that include new fulfillment centers and industrial parks. Strategic logistics investments by national players spur auxiliary storage demand among SME merchants and third-party sellers. The region’s favorable land costs permit larger footprints, enabling operators to experiment with automated systems that raise throughput.

Mid-tier metros—Daegu-Gyeongbuk, Daejeon-Chungcheong, and Gwangju-Jeolla—show steady adoption as urbanization spreads beyond the capital corridor. Lower real-estate barriers allow facility developers to secure centrally located plots, offering convenience levels once exclusive to Seoul. These geographies present expansion corridors for chains targeting first-to-scale advantage.

Competitive Landscape

Industry structure is moderately fragmented, yet consolidation is accelerating as capitalized incumbents expand networks and integrate technology. Second Syndrome, the market’s largest pure-play operator, plans a KOSDAQ listing to finance service upgrades and international forays. IAMBOX Korea quadrupled its branch count to 50 within a year by combining mobile-first booking with in-house logistics, demonstrating how digital capabilities translate into rapid scale.

Strategic differentiation has shifted from price to value-added amenities such as climate control, IoT security, and coworking lounges. Global best practices flow into the market as members engage with the Self Storage Association Asia, lifting operational standards and customer expectations. Smaller independents face rising customer-acquisition costs and compliance burdens, nudging them toward mergers or franchise partnerships.

Automation partnerships also mark a competitive frontier. CJ Logistics’ installation of 140 AutoStore robots in Incheon showcases the synergy between automated retrieval and quick-turn e-commerce fulfillment. Forward-looking storage chains are evaluating similar systems to enhance throughput and reduce labor intensity, signaling a technology arms race.

South Korea Self-Storage Industry Leaders

-

Extra Space Asia

-

Boxful Korea

-

StoreHub Korea Co., Ltd.

-

QubizKorea Co.,Ltd (Q Storage)

-

Self Box

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Second Syndrome disclosed its intention to list on Korean Securities Dealers Automated Quotations (KOSDAQ), aiming to use proceeds for service enhancement, business diversification, and exploratory expansion into the UK and Japan markets.

- May 2025: Area Link became a platinum sponsor of Self Storage Expo Asia 2025, reinforcing Korea’s integration into the wider Asian storage ecosystem.

- April 2025: IAMBOX Korea expanded from 12 to 50 branches within 12 months and set a 100-location target, underscoring its technology-driven growth plan.

- January 2025: AutoStore deployed 140 robots at CJ Logistics’ Incheon Global Distribution Center to support 24/7 e-commerce fulfillment, highlighting automation’s role in future storage models.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea self-storage market as the yearly revenue generated from purpose-built facilities that rent secure, individual units between 1 m2 and 20 m2 to personal and business customers under renewable month-to-month or longer contracts. All facility formats, manned or unmanned, climate-controlled or standard, are tracked.

Scope Exclusion: Temporary parcel lockers used for fewer than seventy-two hours, cold-chain warehouses, and bonded third-party logistics space are not included.

Segmentation Overview

-

By End-user

- Personal

- Business

-

By Storage Unit Size

- XXS/XS (<1 m²)

- Small (1–3 m²)

- Medium (3–6 m²)

- Large (>6 m²)

-

By Service Type

- Standard Self-Storage

- Full-Service / Valet

-

By Application

- Household Goods and Seasonal Items

- Furniture and Appliances

- Documents and Archives

- E-commerce and Micro-fulfilment Inventory

- Others (Sports, Hobby, Wine)

-

By Region

-

Seoul Capital Area

- Seoul-city

- Gyeonggi-do

- Busan-Ulsan-Gyeongnam

-

Non-Capital Metro

- Daegu-Gyeongbuk

- Daejeon-Chungcheong

- Gwangju-Jeolla

- Gangwon

- Jeju

-

Seoul Capital Area

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with facility owners in Seoul, Busan, and Daejeon, spoke with prop-tech investors, and surveyed frequent renters to validate occupancy, average selling prices, and expansion intent across customer cohorts.

Desk Research

We mapped the facility universe using open data from the Ministry of Land, Infrastructure and Transport, KOSIS urban housing statistics, Korea Customs Service HS-code flows for prefabricated storage modules, and newsletters from the Korea Self-Storage Forum. Company filings gathered through D&B Hoovers, transaction news from Dow Jones Factiva, and patent trails mined in Questel supplied revenue ranges, pipeline details, and technology signals that enrich our demand model. Many additional public and subscription sources supported data collection; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down model converts household counts, small-business registrations, and e-commerce parcel volume into a demand pool, which is then filtered through observed unit penetration and average tariff levels to derive the baseline. Supplier roll-ups of operating square meters and sampled ASP multiplied by utilized units provide a bottom-up check before alignment. Key variables, prime retail rent movements, household formation, average unit occupancy, facility completions, and climate-controlled share shifts, feed a multivariate regression with ARIMA error correction that underpins the forecast, while scenario analysis stress-tests vacancy and tariff swings.

Data Validation & Update Cycle

Outputs face variance checks against taxation filings, occupancy disclosures, and regional rental trackers. Senior reviewers resolve anomalies, and Mordor refreshes the model annually, issuing interim revisions after material market events so clients receive the most current view.

Why Mordor's South Korea Self-Storage Baseline Stands Firm

Published estimates often differ because each publisher selects distinct service mixes, geographic cuts, and refresh cadences, which move the needle in meaningful ways.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.28 B (2025) | Mordor Intelligence | - |

| USD 1.21 B (2024) | Global Consultancy A | Focus on Seoul only and excludes valet services; relies on global share allocation |

| USD 1.50 B (2024) | Industry Journal B | Omits climate-controlled premium; models growth solely from historic occupancy without facility pipeline data |

| USD 2.25 B (2024) | Regional Consultancy C | Uses single average tariff, no unit-size stratification; converts revenue with a fixed 2023 KRW-USD rate |

The comparison shows that Mordor's layered scope, live price sampling, and disciplined yearly refresh deliver a balanced, transparent baseline that decision-makers can retrace and trust.

Key Questions Answered in the Report

What is the current size of the South Korea self-storage market?

The market generated USD 2.44 billion in 2026 and is forecast to reach USD 3.43 billion by 2031, growing at a 7.03% CAGR.

Which user segment dominates demand?

Personal users held 70.35% revenue share in 2025, reflecting widespread household adoption for managing space constraints.

Why is Busan-Ulsan-Gyeongnam the fastest-growing region?

Port logistics expansion, diversified manufacturing, and government decentralization initiatives are driving an 8.08% CAGR in that corridor.

How are e-commerce trends influencing facility design?

Operators are adding barcode-based inventory tools, climate zones, and same-day courier interfaces to serve small merchants needing micro-fulfillment capabilities.

What barriers deter new market entrants?

High urban land costs, stringent fire-safety retrofits, and the capital required for digital platforms collectively elevate entry thresholds.

Are valet storage services gaining traction?

Yes, full-service valet offerings are projected to grow at a 7.82% CAGR as busy professionals prioritize convenience over traditional do-it-yourself access.

Page last updated on: