Self Storage Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 4.48 Billion |

| Growth Rate (2026 - 2031) | 11.02% CAGR |

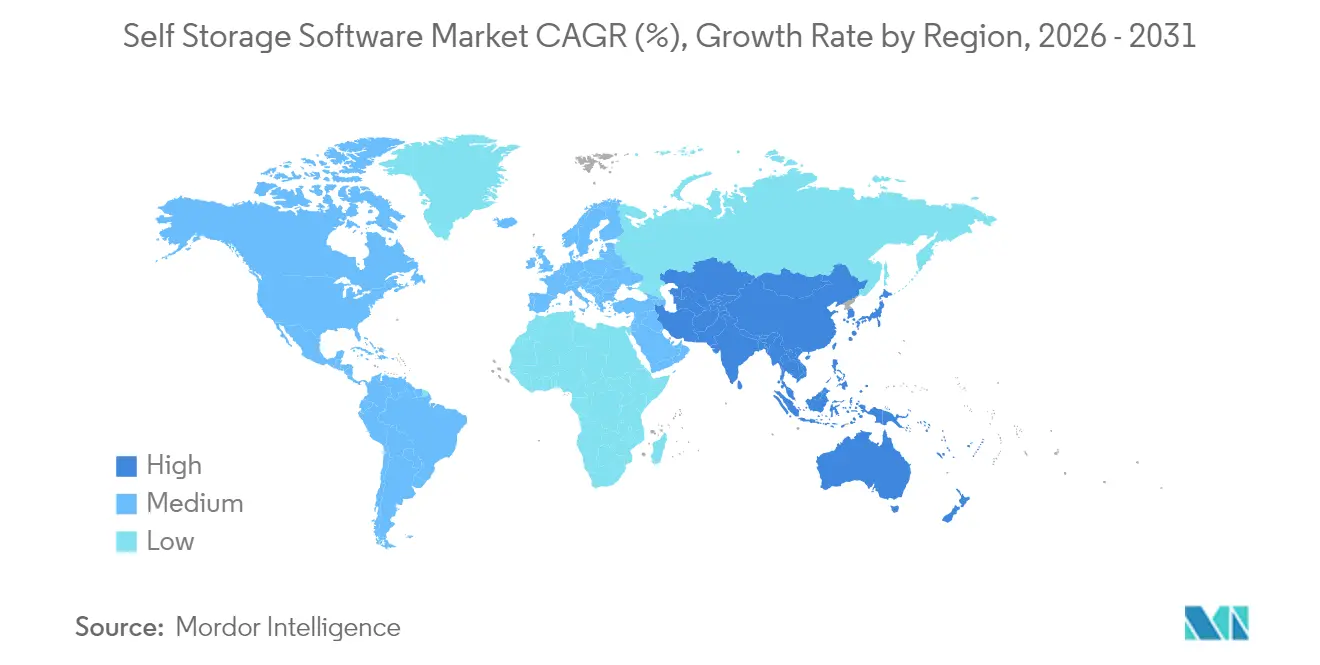

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

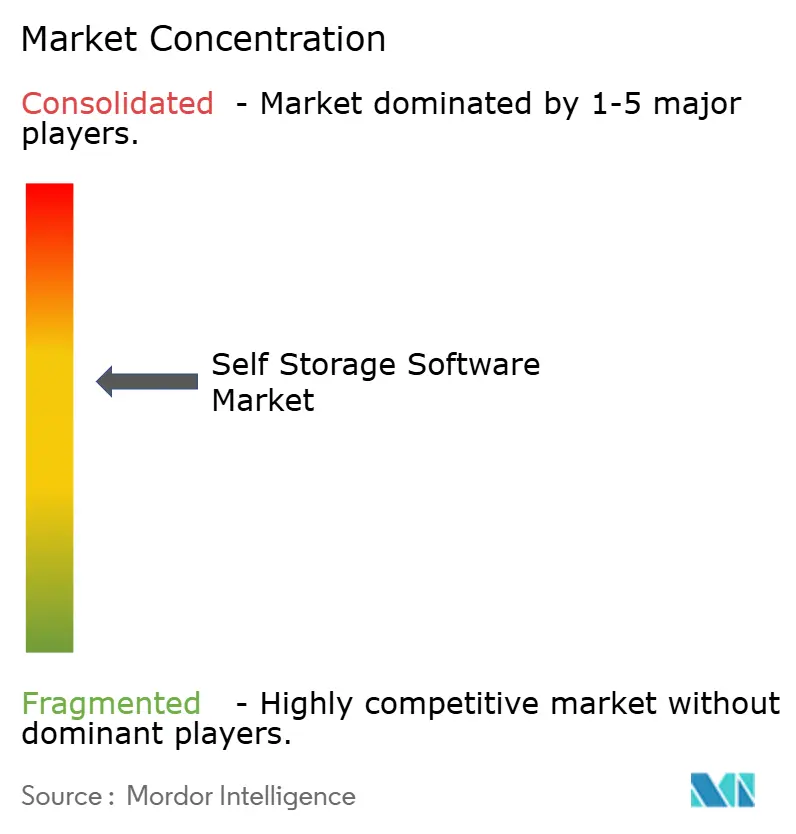

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self Storage Software Market Analysis by Mordor Intelligence

The self-storage software market size is expected to grow from USD 2.39 billion in 2025 to USD 2.65 billion in 2026 and is forecast to reach USD 4.48 billion by 2031 at 11.02% CAGR over 2026-2031. Migration from legacy on-premise tools to cloud-native SaaS platforms is accelerating as facility operators seek real-time reservation management, dynamic pricing, and IoT-enabled access control. Subscription pricing now dominates, enabling operators to align software costs with their monthly rental income while avoiding capital expenditures for perpetual licenses. Cloud deployment has become the default choice, reflecting labor-saving remote management needs and heightened data security expectations. Consolidation among large REITs is creating portfolios that demand enterprise-grade analytics, while third-party management firms are scaling fastest by standardizing software stacks across fragmented ownership bases. Vendors are layering AI-driven yield management and automated marketing modules on top of commoditized facility-management cores to defend margins and deepen customer lock-in across the self-storage software market.

Key Report Takeaways

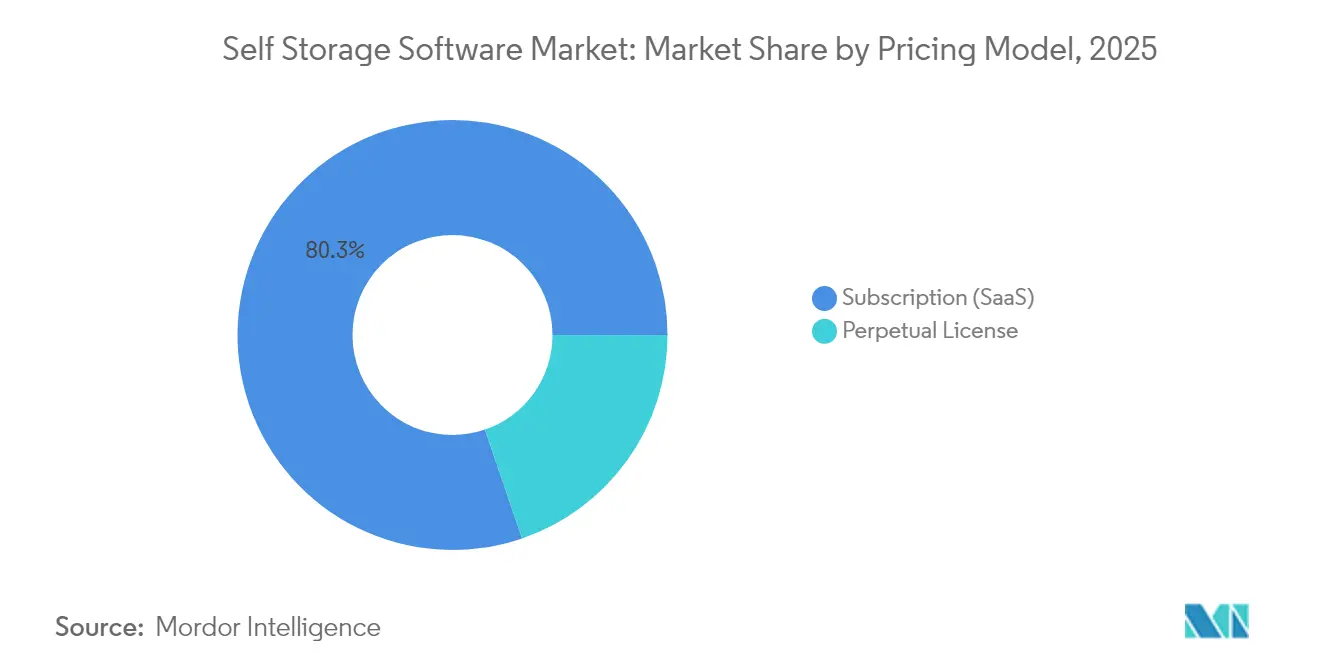

- By pricing model, subscription-based SaaS captured 80.25% of the self-storage software market share in 2025 and is projected to expand at a 12.05% CAGR through 2031.

- By deployment, cloud installations accounted for 70.55% of 2025 implementations within the self-storage software market size and are forecast to grow at a 12.22% CAGR to 2031.

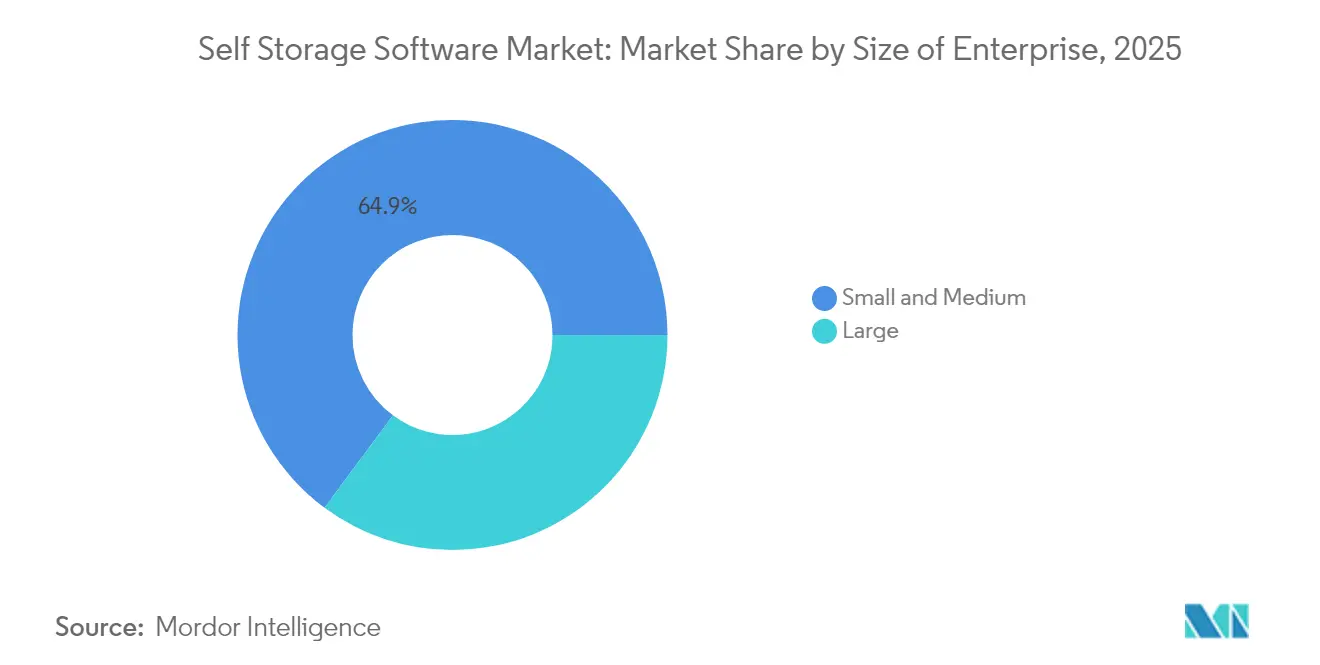

- By size of enterprise, small and medium operators accounted for 64.85% of 2025 revenue, while large operators are growing at a 11.95% CAGR, driven by REIT consolidation waves in the self-storage software market.

- By functionality, facility-management modules led with 42.35% of 2025 revenue, while CRM and marketing automation are the fastest-growing categories at a 13.10% CAGR across the self-storage software market.

- By end-user, self-storage facility owners generated 57.60% of the 2025 demand, whereas third-party management companies are advancing at a 13.45% CAGR through 2031 within the self-storage software market.

- By geography, North America accounted for 37.95% of 2025 revenue, while the Asia Pacific is the fastest-expanding region, with a 13.62% CAGR through 2031 within the self-storage software market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Self Storage Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of cloud-based platforms and mobile applications | +2.8% | Global, with highest adoption in North America and Europe | Medium term (2-4 years) |

| Growing competition among facility operators driving software upgrades | +2.1% | North America and Europe core, spillover to Asia Pacific urban centers | Short term (≤ 2 years) |

| Rising demand for contactless rentals and digital KYC | +1.9% | Global, accelerated in Asia Pacific and Middle East | Short term (≤ 2 years) |

| Integration of IoT-enabled smart locks and sensors | +1.6% | North America and Europe early adopters, Asia Pacific rapid scaling | Medium term (2-4 years) |

| Expansion of third-party management services in fragmented markets | +1.4% | North America fragmented ownership, emerging in Latin America | Long term (≥ 4 years) |

| Adoption of AI-based dynamic pricing and yield management | +1.3% | North America REIT-led, Europe institutional investors, Asia Pacific tier-1 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Emergence of Cloud-Based Platforms and Mobile Applications

Cloud architectures are replacing on-premise systems because they remove server hardware spending and enable instant feature deployments. Stora’s platform processed 70% of U.K. online rentals in 2024, up from 62% in 2023.[1]Stora, “UK Self Storage Industry Insights 2024,” stora.com The Self Storage Manager successfully migrated 1,000 National Storage Affiliates properties in 90 days, demonstrating a rollout speed unattainable under traditional client-server models. SC Navigator consolidated five brands into a single cloud instance in 2025, standardizing dashboards for over 2,000 sites. Offline-capable mobile apps now cache gate credentials and push payment reminders, reducing front-desk calls by an estimated 30%. Augmented-reality wayfinding layers unit locations onto smartphone cameras, improving tenant experience and differentiating providers in the self-storage software market.

Growing Competition Among Facility Operators Driving Software Upgrades

Large REIT acquisitions force independents to upgrade technology or risk tenant churn. Extra Space Storage completed a USD 12 billion Life Storage deal in 2025 and migrated 1,200 stores to its Breeze platform in just 19 days. Public Storage’s USD 2.2 billion acquisition of Simply Self Storage similarly triggered software standardization across newly acquired locations. Third-party managers, such as StorageMart, leverage turnkey SaaS bundles to win contracts from small business owners. Yardi’s February 2025 data showed rental rates stabilizing in top metros after a year of decline, suggesting AI-based pricing is cushioning margins. The technology arms race intensifies demand for analytics-rich platforms across the self-storage software market.

Rising Demand for Contactless Rentals and Digital KYC

The pandemic-era distancing has normalized remote onboarding, which persists for cost savings. Stora integrated Stripe Identity in 2024, cutting tenant verification time to under three minutes. IDprop rolled out biometric checks across Europe in accordance with ISO 27001 compliance. Kiosk-based systems from OpenTech Alliance allow unstaffed operations, extending access beyond office hours. Chelan Boat Storage manages seasonal peaks without extra labor thanks to contactless workflows. Continuous demand for frictionless rentals is solidifying these capabilities as table stakes in the self-storage software market.

Integration of IoT-Enabled Smart Locks and Sensors

Bluetooth and NFC hardware are replacing mechanical locks, enabling instant access revocation for delinquent tenants. Nokē devices enable operators to remotely turn off unpaid units, thereby reducing overlocking costs. Infineon’s NAC1080 chip supports Apple Wallet tap-to-unlock, bolstering consumer convenience.[2]Infineon, “NAC1080 NFC Chip,” infineon.com PTI Security’s StorLogix syncs gate controllers, elevators, and unit locks through open APIs. Wirepas mesh networks link thousands of sensors without cabling, feeding cloud analytics that predict maintenance issues. The resulting data streams unlock autonomous, 24/7 facilities across the self-storage software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonality-driven revenue volatility for software vendors | -0.9% | North America and Europe temperate climates, minimal impact in stable-demand tropics | Short term (≤ 2 years) |

| Escalating cyber-security and data-privacy compliance costs | -1.2% | Europe GDPR-strict, North America CCPA and state-level laws, Asia Pacific emerging frameworks | Medium term (2-4 years) |

| Limited IT budgets of small independent operators | -0.7% | Global small operators, acute in rural North America and emerging Asia Pacific | Long term (≥ 4 years) |

| Complex legacy integrations slowing cloud migration | -0.8% | North America and Europe mature markets with decades-old systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber-Security and Data-Privacy Compliance Costs

GDPR fines are expected to reach EUR 4.5 billion across sectors by 2024, compelling platforms to add encryption and consent-management features that can inflate engineering budgets by up to 20%. CCPA obligations demand opt-out workflows for California residents. PCI DSS 4.0, which has been in effect since March 2025, increases payment-gateway audit costs to USD 50,000-150,000 per annual cycle. ISO 27001 certification has become table-stakes for winning insurance coverage and enterprise contracts. These layered mandates slow feature delivery and compress margins in the self-storage software market.

Seasonality-Driven Revenue Volatility for Software Vendors

Move-in demand peaks from May to August and troughs in winter, causing 30-40% swings in facility occupancy that ripple into usage-based SaaS fees. Yardi’s Q4 2024 survey recorded a 1% year-over-year revenue dip tied to weak winter occupancy.[3]Yardi Systems, “Self Storage Market Intelligence Q4 2024,” yardi.com Vendors must maintain larger cash buffers and offer flexible billing terms, thereby elevating their working-capital needs. Support call volumes surge during summer onboarding spikes, which can inflate service costs. Although commercial tenants add some stability, residential demand drives the core seasonality, restraining growth in the self-storage software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size of Enterprise: Scale Operators Harness Enterprise Analytics

Small and medium-sized enterprises (SMEs) still dominate revenue, accounting for a 64.85% share in 2025, and favor cost-effective SaaS plans that automate basic reservation and billing tasks. Many rely on mobile dashboards for gate monitoring while delaying adoption of AI-pricing add-ons. Broadband gaps and limited IT resources hinder migration, yet rising consumer expectations are nudging independents toward baseline digital capabilities that keep them competitive in the self-storage software market.

Large operators and REITs are expanding at a faster rate than the overall self-storage software market. Extra Space Storage’s rapid expansion drives the segment’s 11.95% CAGR to 1,200 stores and National Storage Affiliates' rollout of 1,000 sites, both of which demonstrate scale efficiencies. These portfolios use centralized dashboards to track occupancy, dynamic pricing, and multi-site maintenance. Synergies, estimated at USD 100 million annually for Extra Space, validate heavy software investments.

By Deployment Model: Cloud Supremacy Redefines Infrastructure

Cloud deliveries accounted for 70.55% of 2025 installations and are projected to rise at a 12.22% CAGR. The self-storage software market size for cloud systems is projected to exceed USD 3.35 billion by 2031, illustrating operator confidence in remote management. High-velocity deployments, such as SC Navigator’s five-brand consolidation, demonstrate downtimes measured in days, not months.

On-premise solutions persist among operators that have amortized legacy licenses and fear connectivity outages. Vendors now offer hybrid modes that cache data locally while syncing to the cloud, easing transition anxiety. Younger owners entering the industry default to cloud subscriptions, accelerating the generational shift in the self-storage software market.

By Pricing Model: Subscription Dominance Reshapes Economics

Subscription SaaS accounts for 80.25% of current revenue and delivers the most predictable cash flows for vendors. Tiered plans start at USD 99 per month for single-site deployments and scale above USD 10,000 for REIT portfolios utilizing AI-driven yield management. Freemium tiers help platforms land small operators and upsell advanced modules over time.

Perpetual licenses remain only where operators prefer full data control or have sunk costs in on-premise servers. QuikStor continues to offer perpetual licenses alongside SaaS, accommodating customers who are wary of recurring fees. Overall, subscription growth is set to outpace perpetual by a 4:1 margin in the self-storage software market.

By Functionality: CRM and Marketing Automation Outpace Core Modules

Facility-management tools led with 42.35% of 2025 revenue, but CRM and marketing automation are the star performers at a 13.10% CAGR. Platforms that embed predictive churn analytics increase tenant retention by 18% and accelerate lease-up times by 22%, according to Storable’s 2025 Tenant Insights report.

Upsell modules, such as tenant insurance, moving supplies, and AI-drafted leases (StoreEase Ease.AI), help vendors capture incremental value per unit. Integration hubs connect payment processors, auction portals, and insurance providers, turning the self-storage software market into an ecosystem characterized by deep third-party connectivity.

By End-User: Third-Party Managers Surge Ahead

Self-storage facility owners generated 57.60% of the 2025 demand, while third-party management firms are projected to show the fastest 13.45% CAGR through 2031. StorageMart and Absolute Storage Management scale standardized software across hundreds of properties, gaining cost advantages that independents cannot match.

REIT mandates accelerate enterprise adoption, concentrating buying power among fewer but larger customers. This raises vendor dependence on a smaller client base, heightening the risk of churn, but also opens doors for high-value, multi-year contracts in the self-storage software market.

Geography Analysis

North America retained 37.95% of global revenue in 2025 as its 50,000+ facilities continue technology refresh cycles mandated by REITs. The self-storage software market size across the region is projected to reach USD 1.71 billion by 2031, driven by AI tools that help stabilize rental rates during periods of demand softness. Cloud migrations accelerate thanks to mature broadband and stringent SOC-2 security requirements.

Asia Pacific is the growth engine with a 13.62% CAGR. Institutional capital backs operators like StorHub, which has spent AUD 110 million (USD 73 million) on Sydney facilities to expand its 7 million-square-foot regional footprint. High urban rents and shrinking apartments in Hong Kong, Singapore, and Tokyo drive demand for micro-storage, compelling operators to prioritize mobile-first reservation apps and biometric access.

Europe’s 9,575 facilities generated EUR 875 million (USD 935 million) in 2024 transactions, a threefold increase from 2023 levels, reflecting rapid consolidation and digital catch-up. FEDESSA found that 69% of operators plan to roll out AI by 2026 to automate pricing and customer service. Shurgard’s Lok’nStore acquisition adds 43 U.K. facilities to its network, promising standardized software upgrades across the locations.

Nascent markets in South America, the Middle East, and Africa exhibit sporadic adoption, primarily driven by urban expatriate segments and corporate document storage. Localization, multi-currency billing, and right-to-left language support are critical to unlocking these regions. Early entrants gain a brand advantage, but fragmented regulations prolong sales cycles across the self-storage software market.

Regulatory Landscape

Regulation affecting self-storage software increasingly centers on tenant-notice, lien enforcement, and digital contracting requirements, pushing platforms to automate state and city-specific workflows. In the United States, California implemented 2026 changes that tighten standards around electronic delivery of lien-related notices and add rental agreement disclosure requirements for leases signed on or after January 1, 2026, which increases the need for configurable templates, audit trails, and proof-of-delivery. New York City advanced rules for self-storage facilities and storage warehouses in 2026 through the Department of Consumer and Worker Protection process, reinforcing tenant-facing notice obligations around fee changes and strengthening the role of automated communications.

Data privacy and payments compliance remain structural constraints on product design and vendor operating costs. A wider set of US state privacy requirements taking effect as 2026 begins, alongside enforcement frameworks such as the California Consumer Privacy Act and European GDPR, increases the need for consent management, retention controls, and secure integrations, particularly where IoT access control and automated identification checks are used. On the payments side, PCI DSS 4.0, in effect since March 2025, continues to raise audit and security requirements for online reservations and recurring billing, supporting demand for compliant payment integrations and security certifications (for example, ISO 27001) across self-storage software stacks.

Value Chain Analysis

The value chain starts with cloud infrastructure and core property management software (PMS) platforms that manage unit inventory, pricing, reservations, billing, and tenant communications, then extends through integrations for identity verification, payments, auctions, insurance, and marketing. Hardware and access-control vendors (smart locks, gate controllers, sensors) feed operational data into the PMS through APIs, which supports contactless rentals and remote facility operations. Implementation and support partners, including third-party management firms and systems integrators, drive multi-site rollouts by standardizing configurations, migrating legacy data, and orchestrating integrations across portfolios.

Distribution and monetization increasingly depend on ecosystem partnerships that connect software to adjacent revenue streams and operational automation. For example, PTI Security (a division of ASSA ABLOY) and Storable introduced real-time integration between StorLogix Cloud and Storable Edge using webhooks, reflecting the shift from batch syncing to event-driven operations that reduce access and delinquency-management latency. Marketplace and channel integrations are also moving closer to the PMS layer, illustrated by QuikStor partnering with Neighbor to sync inventory exposure and customer data into facility-management workflows. Key friction points persist around legacy desktop integrations and the need for reliable connectivity to support IoT-enabled facilities, which keeps open APIs and hybrid or offline modes as important links in the chain.

Competitive Landscape

The market remains moderately fragmented, with no player exceeding 20% share. Storable is building an end-to-end ecosystem, acquiring StorageAuctions.com and updating its brand in March 2025 to extend beyond core management software.[4]Storable, “Acquires StorageAuctions.com,” storable.com Yardi leverages its commercial real estate reach to cross-sell self-storage modules, reinforcing retention through bundled accounting and leasing tools. U-Haul integrates WebSelfStorage with its owned facilities, offering insights that feed product development but raising perceived conflicts for third-party clients.

API-first challengers 6Storage, SC Navigator win share by integrating best-of-breed solutions. StoreEase’s Ease.AI showcases labor-saving, generative AI that drafts leases and recommends unit sizes in real-time. Higher compliance costs under PCI DSS 4.0 and ISO 27001 lift barriers for new entrants, prompting acquisition of compliant codebases rather than greenfield development.

M&A momentum is expected to continue as vendors seek to achieve scale economies and expand their offerings. OpenTech Alliance’s acquisition of two auction portals illustrates a revenue-diversification play that deepens client integration. Overall, vendors differentiate themselves through security certifications, ecosystem depth, and AI capabilities in the self-storage software market.

Self Storage Software Industry Leaders

Storable Group Inc.

Yardi Systems Inc.

Corrigo Incorporated

U-Haul International Inc.

DOMICO Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise consolidation and platform standardization continue to create whitespace for multi-module suites and portfolio-grade analytics, especially for REITs and large operators that need consistent workflows across acquired sites. Public Storage announced an acquisition of National Storage Affiliates in a transaction valued at USD 10.5 billion in Q1 2026, explicitly tying scale synergies to operating-platform leverage, which supports demand for enterprise-ready reporting, centralized pricing controls, and standardized tenant communication tooling. Yardi launched Yardi Storage Manager in January 2026 as an institutional all-in-one platform spanning marketing, leasing, accounting, and operations, reinforcing the opportunity for vendors that can unify formerly separate point solutions while keeping integration flexibility.

AI enablement and API-first architectures are also becoming a commercial differentiator, with a clearer pathway to reduce labor intensity in leasing and customer service. Multiple vendors released AI-forward capabilities in 2026, including 6Storage introducing an AI Sales Agent as part of an integrated growth-and-automation platform, and Storable refreshing Sitelink and Edge with AI-driven business intelligence and automated collections and auction workflows. A distinct integration opportunity is taking shape around making operational data usable by external AI tools: Tenant Inc. opened the Nectar API in July 2026 for direct integration with AI assistants, enabling operators and partners to build custom workflows on top of live facility data. Funding activity further supports product investment headroom, with Cubby raising USD 63 million in a Goldman Sachs-led round in January 2026 to scale its self-storage software platform.

Recent Industry Developments

- March 2026: U-Haul introduced a 1-Year Price Lock Guarantee for new self-storage rentals across more than 2,100 facilities in the United States and Canada. The program increases the focus on pricing and contract-rule automation inside reservation and billing software to enforce guaranteed rates and handle exceptions at scale.

- January 2026: Yardi launched Yardi Storage Manager as an enterprise all-in-one platform integrating marketing, leasing, accounting, procurement, and operations for large self-storage portfolios. The release supports consolidation-driven standardization by offering a single system of record that can replace fragmented point solutions across multi-site operators.

- June 2024: Storable finalized its acquisition of StorageAuctions.com to integrate delinquency and online auction management into its software ecosystem. Folding auction workflows into core operations tightens customer lock-in and expands the monetization surface area beyond facility management and payments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the self-storage software market covers software platforms used by self-storage operators to run day-to-day site operations, including unit and tenant management, reservations, billing, payments, reporting, and links to access control.

Scope exclusions: We exclude general real estate property management tools that are not designed for self-storage workflows, and we also exclude physical security hardware revenue.

Segmentation Overview

- By Size of Enterprise

- Small and Medium

- Large

- By Deployment Model

- PC-based

- Cloud

- By Pricing Model

- Subscription (SaaS)

- Perpetual License

- By Functionality

- Facility Management

- Online Reservations and Payments

- CRM and Marketing Automation

- By End-User

- Self-storage Facility Owners

- Third-party Management Companies

- REITs and Large Operators

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial fact base for demand signals and the operating footprint of self-storage facilities that typically adopt software. Public sources such as the US Census Bureau, the Bureau of Labor Statistics, the Federal Reserve economic data series, and international statistics from groups like the World Bank helped us align macro indicators with storage activity and small business spending.

We also reviewed materials from self-storage and real estate associations (such as membership updates and operating benchmarks), regulatory and procurement notices where relevant, and other open sources such as peer reviewed articles that discuss revenue management and digital adoption in property operations. For company-level context, we used annual reports, earnings call transcripts, investor presentations, and press releases. We supplemented this with paid subscriptions focused on company financials and intelligence, news and financials, and patent databases to validate product direction and module coverage. The desk research sources mentioned here are illustrative only, and many other public documents were also checked to fill gaps and confirm assumptions.

Primary Interviews and Surveys

Primary work focused on aligning what the software actually covers in practice and how pricing is commonly charged (subscription by site, by unit count, or by module). We spoke with a mix of storage operators, third-party facility managers, and software implementation and integration specialists across the main regions so that gaps from desk research could be closed and key assumptions could be stress tested.

What helped most was confirming module attach rates (for online leasing, payments, CRM, and analytics), the cloud versus PC-based mix, and how often operators switch systems. These factors change the revenue pool even when facility counts look stable.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 42% |

| Mid tier: 50% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 14% | Managers: 46% | Americas: 24% |

Market-Sizing & Forecasting

Sizing started with a top-down build where the demand pool is reconstructed from the number of operating storage facilities and sites by region, the share that runs dedicated storage platforms, and the typical spend per site or per unit based on prevailing subscription plans. To keep the logic grounded, we then checked the totals with selective bottom-up approximations, such as sampled operator counts by size band, channel checks on common pricing tiers, and a sanity check using a small roll-up of software revenue signals where they are publicly visible.

Key inputs in the model included cloud adoption rates versus PC-based deployments, module penetration for online reservations and payments, unit occupancy trends that influence transaction volumes, average units per facility (as a proxy for pricing bands), and the pace of multi-site consolidation that often triggers system upgrades. Where direct data was thin for smaller operators, we used conservative adoption assumptions and then adjusted them based on interview feedback and regional consistency checks.

For forecasting, scenario analysis was used with two to three demand paths tied to software adoption, pricing progression for subscription tiers, and the speed of new facility openings. Once these drivers were aligned with expert feedback, the forward view was carried through the model year by year so the growth pattern stays traceable to the same variables used for the base year.

Data Validation & Update Cycle

Validation was done by triangulating model outputs against independent signals, then reviewing any large swings that did not match known market behavior. Checks included variance reviews across regions, comparisons to software spending intensity by operator size, and a lookback test to see whether recent years track expected adoption and pricing changes.

Before sign-off, the work is reviewed in steps so that assumptions, conversions, and growth drivers stay consistent across the full model. Reports are refreshed annually, and if there is a material event such as a major pricing shift, a large acquisition wave, or a clear change in cloud adoption, the key assumptions are rechecked and updated. Right before delivery, we do a final pass to ensure the numbers reflect the latest available information.

Mordor Intelligence's Self Storage Software Market Sizing Compared With Other Published Estimates

Published market sizes for self-storage software can vary even when the topic name looks identical, because the included modules, pricing basis, and base year treatment are not always the same. Differences also show up when some studies mix services and implementation work into the same revenue line, or when they apply aggressive price growth without linking it to operator willingness to pay.

In our cross-check, the main gap drivers were whether PC-based license revenue is treated as recurring, how cloud subscriptions are counted when priced by unit count versus by site, and whether adjacent property management software is blended in. Currency timing also matters because a mid-year exchange rate choice can shift the USD total, and refresh cadence matters because software pricing and cloud mix move quickly. The biggest spread tends to appear when payments processing and non-storage property management suites are included in the revenue pool, which is kept out of scope here and then validated through operator interviews and module attach rates before sign-off in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.39 B (2025) | |

| Global Consultancy A | USD 2.87 B (2025) | This estimate appears to use a broader platform scope that can bundle payments, analytics, and security and access control as a wider suite, which can pull in spend that is not always self-storage specific. It also assumes faster subscription price progression across the forecast window, which lifts the total when normalized to USD. |

| Industry Research Group B | USD 2.50 B (2024) | This number is anchored to a different base year and likely relies on a simplified facility count times average spend method without adjusting enough for cloud versus PC-based mix and module attach rates. When the adoption curve is not revalidated region by region, the total can sit lower or higher depending on the assumed penetration. |

Overall, the spread comes mainly from what is counted as self-storage specific software revenue and from how subscription pricing is annualized across site and unit based plans. When those items are made explicit, the market total becomes easier to replicate and update using the same steps.

Key Questions Answered in the Report

What is the projected value of the self storage software market by 2031?

The market is expected to reach USD 4.48 billion by 2031.

Which pricing model dominates current software deployments?

Subscription-based SaaS accounts for 80.25% of 2025 revenue.

Which region will grow fastest through 2031?

Asia Pacific is forecast to expand at a 13.62% CAGR.

What functionality segment is expanding most rapidly?

CRM and marketing automation is growing at a 13.10% CAGR through 2031.

How are IoT devices influencing facility operations?

Smart locks and sensors enable 24/7 autonomous access, lower labor costs, and reduce delinquency losses.

Why are compliance costs rising for vendors?

Stricter regulations such as GDPR, CCPA, and PCI DSS 4.0 require advanced encryption, audits, and data-residency controls.

Page last updated on: