Loratadine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

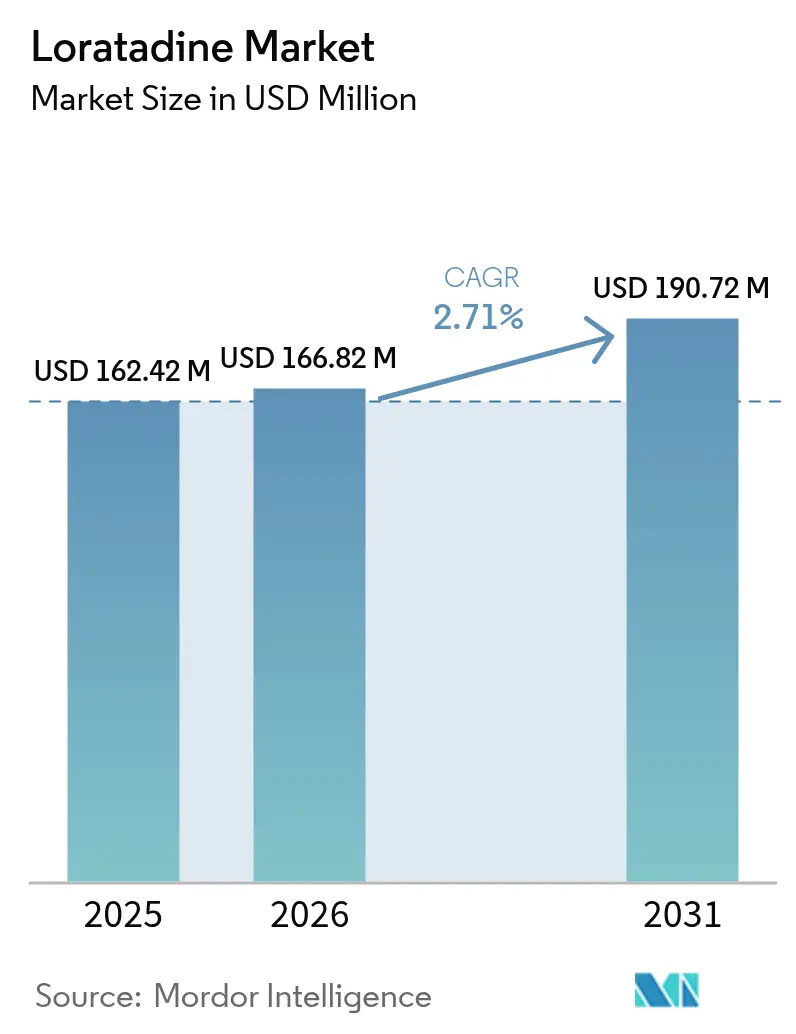

| Market Size (2026) | USD 166.82 Million |

| Market Size (2031) | USD 190.72 Million |

| Growth Rate (2026 - 2031) | 2.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Loratadine Market Analysis by Mordor Intelligence

loratadine market size in 2026 is estimated at USD 166.82 million, growing from 2025 value of USD 162.42 million with 2031 projections showing USD 190.72 million, growing at 2.71% CAGR over 2026-2031. Modest expansion occurs despite the steady climb in allergy cases worldwide, because intensifying generic competition squeezes prices and margins across key retail and e-pharmacy channels. The market draws support from non-sedating profiles that encourage patient adherence, regulatory moves that widen over-the-counter (OTC) access, and rapid digitalization of medicine distribution. Competitive pressures nevertheless remain pronounced as next-generation antihistamines gain clinical favor, forcing legacy brands to defend share with combination formulations, extended-release technologies, and aggressive pricing. Robust supply-chain diversification, spanning certified API plants in India, China, and the United States, adds resilience yet also intensifies commoditization, reinforcing the mature character of the global loratadine market.

Key Report Takeaways

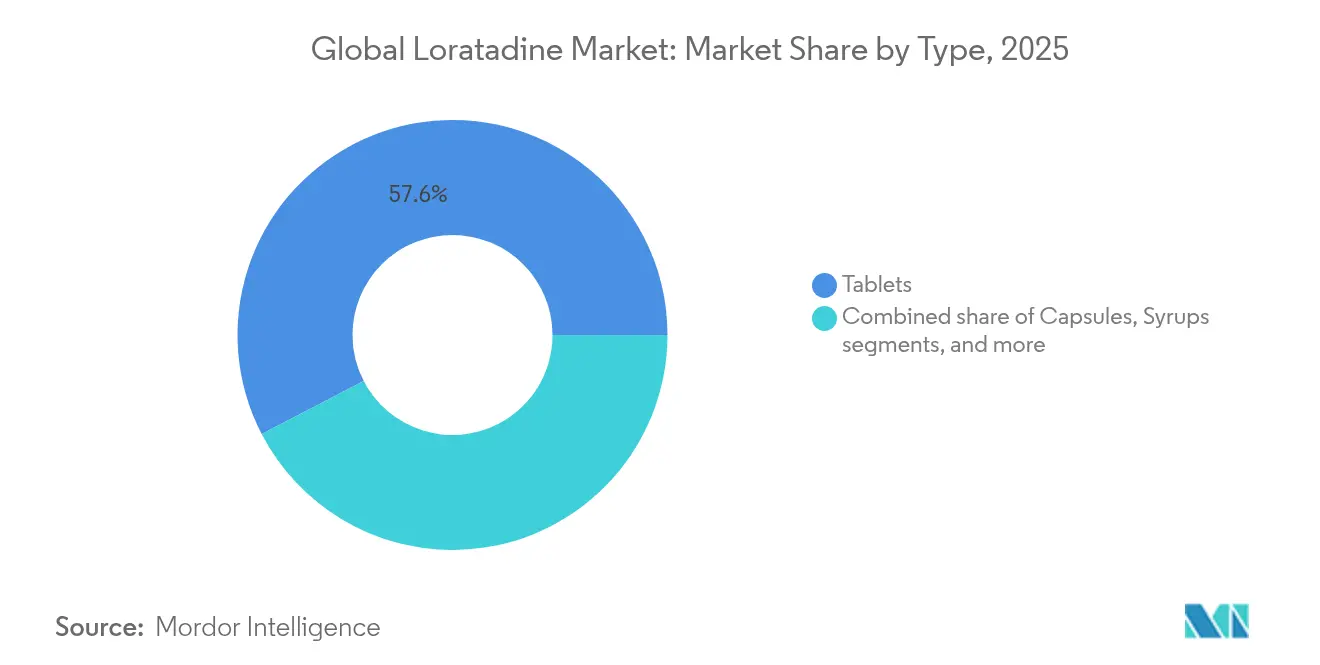

- By formulation, tablets accounted for 57.62% of the loratadine market size in 2025, while extended-release combinations advance at a 4.38% CAGR to 2031.

- By distribution channel, retail pharmacies generated 44.88% revenue in 2025, whereas online pharmacies climb at a 5.46% CAGR during the forecast window..

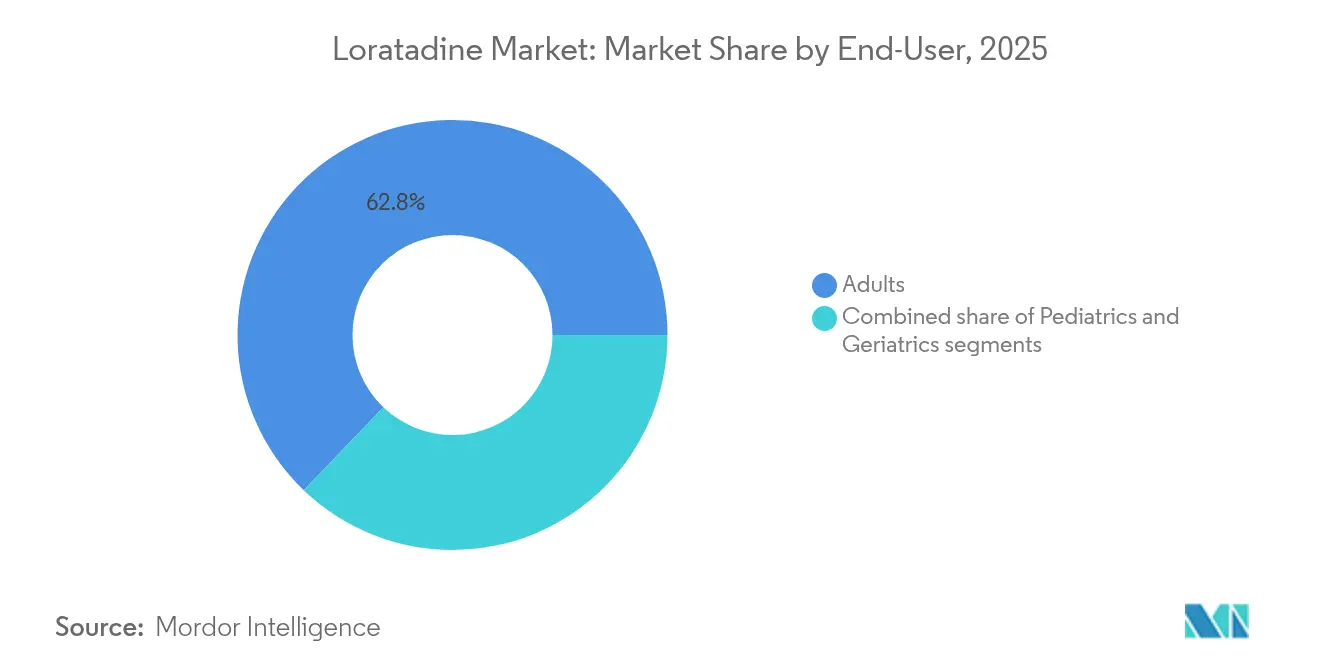

- By end-user, adults comprised 62.84% of demand in 2025, yet pediatric use expands at a 5.12% CAGR supported by favorable safety data

- By formulation class, single-ingredient products retained 65.83% share in 2025, but loratadine-montelukast fixed-dose combinations are projected to grow at 4.63% CAGR to 2031.

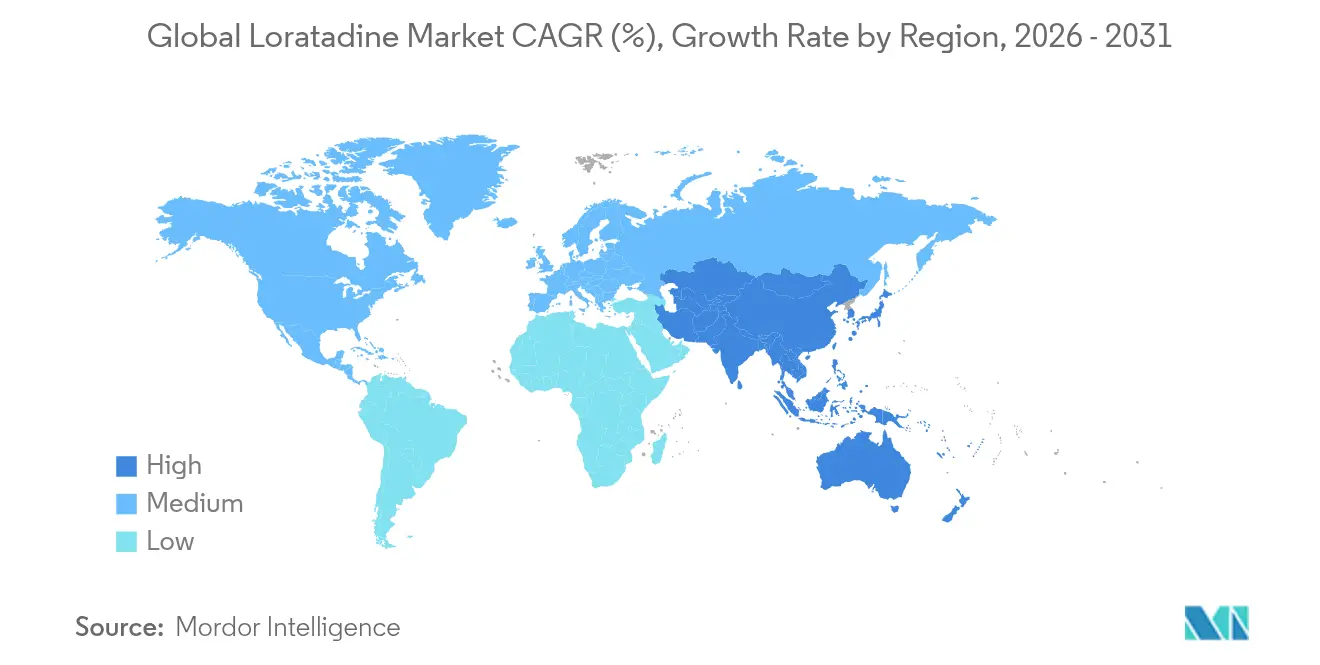

- By geography, North America held 41.98% loratadine market share in 2025 and Asia-Pacific is set to post the fastest 3.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Loratadine Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Allergy Prevalence | +0.8% | Global; highest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Increasing Over-The-Counter Accessibility | +0.6% | Global; pronounced in emerging markets | Medium term (2-4 years) |

| Expansion of E-Pharmacy Distribution Channels | +0.4% | North America & EU; expanding to Asia-Pacific | Short term (≤ 2 years) |

| Advancements in Fixed-Dose Combinations | +0.5% | North America & EU; selective Asia-Pacific markets | Long term (≥ 4 years) |

| Growing Preference for Non-Sedating Agents | +0.3% | Global | Medium term (2-4 years) |

| Diversification of API Supply | +0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Allergy Prevalence

Growing urbanization, environmental shifts, and lifestyle changes are pushing allergy incidence upward, widening the patient base for the loratadine market[1]Annals of Allergy, Asthma & Immunology, “Guidelines for allergic rhinitis management,” annallergy.org. Demand concentrates in emerging Asia-Pacific economies where rapid industrialization correlates with higher airborne allergen loads. Clinical guidelines still list loratadine as a first-line treatment for intermittent allergic rhinitis, offering a broadly accessible remedy. Expanded use in pediatric cohorts, backed by electrocardiographic safety studies, further enlarges the addressable pool. Yet heightened awareness also drives clinicians to evaluate newer molecules with perceived efficacy advantages, tempering automatic reliance on traditional antihistamines.

Increasing Over-The-Counter Accessibility

The January 2025 FDA final rule on Additional Conditions for Nonprescription Use (ACNU) formalized a streamlined path for select OTC drugs, lowering clinical entry barriers for mature antihistamines such as loratadine. Greater OTC availability aligns with payer efforts to reduce primary-care visits by encouraging self-care for uncomplicated allergy episodes. In emerging markets, relaxed prescription requirements noticeably uplift volumes, especially among price-sensitive consumers who value pharmacist guidance. Cheaper generics, however, intensify shelf competition, obliging brands to differentiate via packaging, loyalty programs, and extended-release variants.

Expansion of E-Pharmacy Distribution Channels

E-pharmacy operators combine price transparency with doorstep fulfillment, capturing young, digitally savvy customers and chronic allergy sufferers who favor subscription refills. Artificial-intelligence chatbots recommend dose regimens, while blockchain audits build trust in product provenance. The channel’s 14.42% CAGR through 2026 accelerates loratadine market penetration for combination products that benefit from richer online product descriptions. Regulators still require stringent prescription verification for decongestant blends containing pseudoephedrine, adding cost to platform compliance yet preserving patient safety.

Advancements in Fixed-Dose Combination Therapies

Meta-analyses covering 4,902 participants confirm that loratadine-montelukast dual therapy yields superior relief of congestion and night-time symptoms versus monotherapy[2]Frontiers in Pharmacology, “Meta-analysis of loratadine-montelukast efficacy,” frontiersin.org. Combinations simultaneously target histamine and leukotriene pathways, attracting patients with comorbid asthma. Extended-release layers enable 12-hour and 24-hour dosing, sustaining plasma levels and improving adherence. Regulatory approval demands bioequivalence and stability data, discouraging smaller entrants and enabling premium pricing. Successful launches by Perrigo and Viatris demonstrate that innovation is still possible in a commoditized loratadine market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Competition from Next-Generation Antihistamines | -0.7% | Global; strongest in developed markets | Medium term (2-4 years) |

| Regulatory Stringency on Pseudoephedrine Combinations | -0.3% | North America & EU | Short term (≤ 2 years) |

| Potential Adverse Drug Reactions and Interactions | -0.2% | Global | Long term (≥ 4 years) |

| Pricing Pressure from Generic Saturation | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from Next-Generation Antihistamines

Bilastine and newer non-sedating molecules advertise superior receptor selectivity and minimal drug–drug interaction profiles, winning favor among 88.33% of surveyed Indian specialists[3]International Journal of Innovative Research in Medical Science, “Physician preference for bilastine,” ijirms.in. Desloratadine, marketed as a more potent metabolite, also eats into adult prescriptions. Advanced nasal sprays such as Ryaltris combine corticosteroids and antihistamines, reshaping clinician algorithms. In high-income markets, reimbursement committees increasingly weigh incremental efficacy over cost, eroding legacy positions. Traditional suppliers must respond with value-added formats, aggressive contracting, or bundled patient-support services.

Pricing Pressure from Generic Saturation

Widely available generics price a 10-tablet loratadine blister at roughly USD 11, reflecting a crowded supplier field of more than 70 global API manufacturers. European payers enforce tender systems that reward the lowest bidder, further compressing margins. Inflation adds raw-material cost volatility, while wholesalers negotiate volume-based rebates. Companies counter by shifting focus to fixed-dose blends and private-label contracts with mass-retailers, but the pricing spiral remains a structural constraint on loratadine market profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Extended-Release Drives Innovation

Tablet formulations dominated 57.62% loratadine market share in 2025 as decades of clinical familiarity, low production costs, and widespread generic licenses kept demand elevated. Many consumers view 10 mg tablets as the default self-care option, available across grocery, convenience, and pharmacy outlets. Capsule uptake stays modest because bioequivalence offers little extra benefit relative to higher unit cost. Syrups reserve a niche for children aged 2–5 years, supported by clear pharmacokinetic data. Orally disintegrating tablets appeal to users with dysphagia but face limited retail shelf space.

Extended-release combinations represent the fastest-growing type, printing a 4.38% CAGR through 2031. Loratadine-pseudoephedrine 12-hour tablets, marketed by Perrigo and large retail chains, lengthen symptom coverage and minimize dosing frequency. Behind-the-counter rules for pseudoephedrine elevate pharmacist engagement yet add administrative steps that depress impulse purchases. Manufacturers therefore invest in loratadine market messaging that underlines day-long relief and nasal decongestant synergy, offsetting paperwork friction. Private-label adoption across big-box stores proves consumers will trade branded recognition for price savings once therapeutic parity is accepted.

By Distribution Channel: Digital Transformation Accelerates

Retail pharmacies retained 44.88% revenue in 2025, propped up by walk-in convenience and consumer desire for real-time pharmacist counseling. Brick-and-mortar chains leverage loyalty programs and seasonal allergy-endcap displays to capture episodic shoppers. Hospital pharmacies cater to inpatient allergy management but remain a small slice due to loratadine’s OTC status. Wholesalers like McKesson facilitate logistics, squeezing margins through bulk-purchase agreements.

Online pharmacies, however, are the growth story, advancing at 5.46% CAGR. Subscription models ship monthly refills, locking in repeat orders while providing price predictability. Digital storefronts showcase comparative tables that heighten awareness of combination options, nudging shoppers toward higher-priced extended-release SKUs. Application-programming-interface links with telehealth platforms close the loop from virtual consultation to doorstep delivery. Regulators mandate e-verification for pseudoephedrine sales, but blockchain-backed identity checks increasingly automate compliance. As mobile penetration widens, especially in Southeast Asia, the loratadine market finds a fertile runway for direct-to-consumer scale.

By End-User: Pediatric Safety Drives Growth

Adults generated 62.84% of loratadine market demand in 2025, reflecting elevated exposure to environmental allergens at workplaces and outdoor settings. Working professionals value once-daily dosing that maintains productivity without sedative side effects. The geriatric cohort, although smaller, depends on loratadine’s mild hepatic metabolism and low CNS penetration, critical for polypharmacy regimens.

Children form the fastest-growing group, climbing at 5.12% CAGR. Pediatric use gains momentum after studies reported no clinically relevant ECG changes in patients aged 2–5 years receiving syrup formulations. Caregivers prioritize non-sedation to maintain learning focus, amplifying loratadine’s reputation. Formulators experiment with fruit flavors and sugar-free sweeteners to heighten adherence. Regulatory guidance permitting pediatric OTC purchase in several jurisdictions removes former prescription obstacles, widening household adoption and boosting the loratadine market among young families.

By Formulation: Combination Therapies Lead Innovation

Single-ingredient products captured 65.83% of the loratadine market size in 2025 due to time-tested efficacy, straightforward manufacturing, and aggressive generic competition. Price competition borders on commoditization, with supermarket store brands undercutting national labels. Loratadine-pseudoephedrine blends satisfy sufferers requiring decongestant relief but face pseudoephedrine sales restrictions that hamper volume.

The loratadine-montelukast combination is the innovation vanguard, posting a 4.63% CAGR. Clinical evidence from 23 randomized trials shows marked improvement in total nasal symptom scores compared with antihistamine alone. Dual-mechanism action addresses both histamine-mediated itching and leukotriene-driven inflammation, appealing to patients with overlapping asthma. Development hurdles include stability of two active moieties and comprehensive safety datasets, yet successful approvals secure higher list prices and brand exclusivity windows. Marketing messages emphasize reduced pill burden and holistic airway control, enhancing perceived value in the competitive loratadine market.

Geography Analysis

North America controlled 41.98% loratadine market share in 2025, anchored by robust OTC culture, broad insurance penetration for allergy therapeutics, and active e-commerce adoption. The May 2025 FDA advisory highlighting severe itching after abrupt cessation of cetirizine and levocetirizine presents a notable switch opportunity toward loratadine formulations. Manufacturer promotion centers on non-sedating characteristics and combination SKUs positioned for all-day relief, even as payers encourage generics to curb costs. Telemedicine uptake, rising from 11% to 46% of physician visits, streamlines online prescription renewals and product delivery, fueling digital purchases.

Europe forms a highly regulated but sizeable market where tender rules and reference pricing squeeze margins for mature antihistamines. Several governments weigh automatic indexation to adjust generic prices for inflation, safeguarding supply after pandemic shortages. Physicians follow evidence-based guidelines that still include loratadine as an initial step, yet bilastine gains traction following Health Canada and European approvals. Sustainable pricing mechanisms, including multi-winner tenders, seek to avoid supply disruptions that previously plagued low-margin generics. Manufacturers diversify packaging languages and strengthen pharmacovigilance reporting to satisfy heterogeneous national regulations.

Asia-Pacific is the fastest-growing region, advancing at 3.48% CAGR through 2031. Rising urban pollution and increased pollen counts in megacities elevate allergic rhinitis incidence, particularly in India where prevalence hits 30% of the population. Pharmacies proliferate in both metropolitan centers and second-tier towns; China’s LBX Pharmacy Chain operates more than 15,000 outlets, integrating brick-and-click models to reach rural consumers. Physician surveys in Malaysia reveal strong confidence in non-sedating antihistamines for mild rhinitis, favoring OTC accessibility. Multinational producers compete with well-capitalized domestic generics, prompting collaborative quality audits to reassure regulators after past adulteration scares. The loratadine market benefits from government campaigns that license e-pharmacy pilots, thereby improving access for remote populations.

Regulatory Landscape

Regulation for loratadine is anchored in established quality and labeling requirements for mature OTC antihistamines, including harmonized expectations around pharmacopoeial compliance (for example, USP) and routine post-approval labeling maintenance. In the United States, FDA actions during 2024 included streamlined OTC labeling update processes (including March 2024 guidance on annual-report labeling for established OTC drugs) and continued reliance on product-specific bioequivalence expectations through published pathways such as FDA product-specific guidance (PSG) for loratadine.

Policy changes that enable broader nonprescription use and faster lifecycle management continue to shape go-to-market strategy. The FDA final rule on Additional Conditions for Nonprescription Use (ACNU), finalized in January 2025, formalized a mechanism for select OTC products to be supported by additional conditions. This reinforces the compliance role of labeling, packaging, and controlled use conditions across retail and e-pharmacy channels. At the same time, controls affecting decongestant combinations, notably pseudoephedrine tracking and verification, keep combination SKUs subject to higher compliance and dispensing friction than single-ingredient loratadine, influencing portfolio prioritization by companies active in extended-release combination formats.

Competitive Landscape

Competition remains fragmented: more than 70 API producers hold active capacity, and 25 maintain USDMF registrations, diluting individual pricing power. Perrigo leverages private-label agreements with national retailers, embedding loratadine generics into store-brand allergy aisles. Viatris and Sun Pharmaceutical focus on supply-chain efficiency and global quality harmonization to defend volume amid a 4% year-on-year revenue dip reported in 2024. Smaller firms differentiate via extended-release technology or niche formats such as orally disintegrating tablets.

Regulatory shifts shape strategy. The FDA’s streamlined annual-report labeling guidance, issued March 2024, simplifies updates for established OTC drugs, allowing faster packaging revisions and claim optimization. Conversely, stricter pseudoephedrine tracking rules in the United States and Europe raise compliance costs for combination SKUs, favoring larger entities with sophisticated data systems. Forward-looking firms hedge supply risk by dual-sourcing key intermediates and investing in digital serialization that meets cross-border traceability mandates.

Product innovation continues despite maturity. Perrigo’s extended-release loratadine-D twelve-hour tablet competes directly with branded Claritin-D, carving space through competitive pricing and equivalent efficacy claims. Pipeline development tilts toward fixed-dose combinations that offer multi-pathway symptom relief, while topical antihistamines such as PBZ OTC illustrate adjacent category expansion. As new-generation oral agents penetrate guidelines, legacy players highlight cost-effectiveness and vast post-marketing safety data to sustain formulary positions within the crowded loratadine market.

Loratadine Industry Leaders

Bayer AG

Pfizer Inc.

Sun Pharmaceutical Industries Ltd.

Viatris Inc.

Cadila Pharmaceuticals Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities in the loratadine market are concentrated in value-added OTC formats and channel execution rather than new molecule discovery, given low concentration and pervasive generic saturation across single-ingredient 10 mg tablets. The most visible whitespace sits in fixed-dose combinations (for example, loratadine-montelukast) and extended-release decongestant combinations, where differentiated dosing convenience and symptom coverage support premium positioning, even as they raise regulatory and operational barriers such as bioequivalence and stability requirements and controlled-sale verification for pseudoephedrine. The January 2025 FDA ACNU final rule also provides a concrete framework that can be leveraged to scale nonprescription access with structured conditions, which creates room for brands and private-label suppliers to compete on packaging, claim optimization, and compliant digital workflows.

Geographically, distribution expansion and supply-chain repositioning create practical whitespace. Asia-Pacific is the fastest-growing region in the report scope, supported by rising allergic rhinitis prevalence (including India) and rapid retail footprint scale (for example, China’s LBX Pharmacy Chain operating more than 15,000 outlets), alongside government-backed e-pharmacy pilots. On the supply side, Morepen Laboratories securing China NMPA approval for loratadine API (April 2025) shows how API suppliers are using new-market regulatory access to diversify beyond mature US and European demand. Continued reliance on imported key starting materials in India also underscores the value of dual-sourcing, quality audits, and regional regulatory readiness for uninterrupted OTC availability.

Recent Industry Developments

- July 2026: Bayer Pharmaceuticals and Daiichi Sankyo Healthcare entered a licensing agreement for Claritin EX in Japan, effective July 1, 2026. The deal supports localization of an established OTC allergy brand through a partner with domestic commercial reach, tightening alignment with Japanese retail distribution and consumer engagement.

- April 2026: Juno OTC (a wholly owned subsidiary of LSL Pharma Group) signed a binding term sheet with Instapill Private Limited to supply private-label Loratadine 10 mg rapid dissolve tablets to Canadian retailers. The agreement points to continued expansion of store-brand and differentiated dosage forms in mature OTC categories, where retailer relationships and shelf presence influence volume.

- April 2025: Morepen Laboratories received NMPA approval for its loratadine API in China. This approval broadens export potential and diversifies supply options for loratadine manufacturing in the region.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from loratadine based antihistamine products that are sold for allergy symptom relief across major regions, covering both prescription and over-the-counter routes depending on local rules.

Scope exclusions: We do not count diagnostic allergy testing, physician consultation fees, or non-loratadine antihistamines, even if they are used for similar symptoms.

Segmentation Overview

- By Type

- Tablets

- Capsules

- Syrup

- Orally Disintegrating Tablets

- Extended-Release Combinations

- By Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

- Drug Wholesalers

- By End-User

- Adults

- Pediatrics

- Geriatrics

- By Formulation

- Single-Ingredient Loratadine

- Loratadine + Pseudoephedrine

- Loratadine + Montelukast

- Loratadine + Phenylephrine

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context and anchor inputs that tend to remain stable over time. We referred to public health and drug-regulation sources such as the US FDA, the US CDC, the WHO, and the European Medicines Agency for indications, labeling, and safety notes that influence usage and switching.

On the market side, we also reviewed trade and statistics sources such as UN Comtrade, national customs releases, and published healthcare utilization briefs, then cross-checked them with company annual reports, investor presentations, and reputable press coverage for product availability and channel mix signals. Where needed, subscription databases were used for company financials and intelligence, plus patent databases to understand formulation activity and generic intensity. These sources are not exhaustive, and many other public documents were also used to collect, validate, and clarify specific data points.

Primary Interviews and Surveys

Primary discussions were run with a mix of manufacturers, distributors, pharmacy channel participants, and clinical stakeholders who see demand patterns for allergy therapies. We used these inputs to confirm realistic pricing movement, validate regional splits across APAC, EMEA, and the Americas, and pressure-test assumptions around substitution toward other antihistamines and combination products.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 50% |

| Mid tier: 46% | Functional/Unit leaders: 31% | EMEA: 30% |

| Smaller Players: 16% | Managers: 55% | Americas: 20% |

Market-Sizing & Forecasting

For sizing, we apply a top-down approach by building a treated demand pool from allergy prevalence and care-seeking behavior, then converting it to loratadine consumption using therapy mix and channel access assumptions. We corroborate these totals with selective bottom-up approximations, such as sampled average selling price by dosage form multiplied by implied volume, plus distributor and pharmacy channel checks, before settling the final number.

Key inputs used in the model include allergy prevalence trends (allergic rhinitis and urticaria), over-the-counter availability and switching behavior, average price progression by major dosage forms (tablets, capsules, syrups, and similar), the mix of single-ingredient versus combination formulations, and regional seasonality patterns that shape demand peaks. When specific country splits were thin, we used proxy indicators such as population-weighted allergy rates, then adjusted using interview feedback on local channel penetration.

Forecasting was mainly completed using scenario analysis, since pricing pressure from generics and product substitution can move differently by region. Assumptions for each scenario were reviewed with primary respondents, and the mid case was used as the reported forecast path.

Data Validation & Update Cycle

Outputs were checked through multiple steps, starting with variance reviews against independent signals such as allergy burden direction, channel expansion, and pricing movement observed in public filings and regulatory events. If the model suggested a sharp jump or drop, we rechecked the driver inputs and, where needed, re-contacted experts to confirm whether the change was real or reflected an assumption error.

Before sign-off, the full set of calculations is reviewed by another analyst so obvious inconsistencies are caught early, and regional totals are forced to reconcile to the global number. Reports are refreshed annually, with interim updates when material events occur, such as policy shifts on OTC access or major supply disruptions. Right before delivery, a final data pass is completed so clients receive the latest updated view.

Mordor Intelligence's Loratadine Market Size Compared Against Other Published Estimates

Published numbers for loratadine often do not match because the market gets defined in different ways, and because each publisher makes its own choices on pricing, geography, and what counts as a loratadine product. Differences also come from the base year used, currency conversion timing, and how fast price erosion is assumed in generic-heavy markets.

Some estimates roll diagnostic and broader allergy related spending signals into the narrative, which can push the value up even when loratadine drug revenue itself is stable. In Mordor Intelligence's model, the market is limited to loratadine product revenue by dosage form and channel, and combination formulations are counted only when loratadine is the active drug being sold in that pack.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 162.42 M (2025) | |

| Global Consultancy A | USD 153.40 M (2023) | Uses an earlier base year and a different forecast window, and the scope description is broad, which can apply different price erosion and channel mix assumptions across regions. |

| Industry Publisher B | USD 164.52 M (2025) | Includes a wider set of segmentation lenses and country cuts that can change regional weighting, and it may apply a higher growth expectation for OTC access and demand peaks, which shifts the total. |

Taken together, the spread is mainly explained by what is counted as in-scope loratadine revenue, plus the timing of the base year and the way price changes are carried into the forecast. Our approach stays traceable because the total is built from clear demand indicators and then checked back to practical price and channel assumptions that can be explained and repeated.

Key Questions Answered in the Report

How large is the loratadine market in 2026?

The loratadine market size is USD 166.82 million in 2026, set to climb to USD 190.72 million by 2031 at a 2.71% CAGR.

Which region leads in loratadine sales?

North America commands the largest share at 41.98%, supported by mature OTC culture and wide insurance coverage.

Why are fixed-dose combinations gaining popularity?

Loratadine-montelukast tablets offer dual-pathway relief, producing greater symptom reduction and supporting a 4.63% CAGR segment growth.

What is driving online pharmacy growth for loratadine?

Convenience, subscription refills, and integrated telehealth programs push online channels up at a 5.46% CAGR.

How do next-generation antihistamines affect loratadine demand?

Molecules such as bilastine show higher receptor selectivity, drawing clinician preference and applying negative 0.7% impact on loratadine CAGR.

Are safety concerns limiting pediatric use?

No; clinical evidence shows no significant ECG changes in children aged 2Ð5 years, enabling a 5.12% CAGR in pediatric demand.

Page last updated on: