Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.05 Billion |

| Market Size (2026) | USD 4.18 Billion |

| Market Size (2031) | USD 4.89 Billion |

| Growth Rate (2026 - 2031) | 3.24% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Pharmaceutical Market Analysis by Mordor Intelligence

The Denmark pharmaceutical market size was valued at USD 4.05 billion in 2025 and estimated to grow from USD 4.18 billion in 2026 to reach USD 4.89 billion by 2031, at a CAGR of 3.24% during the forecast period (2026-2031). Solid domestic demand for chronic-disease therapies, coupled with aggressive export growth, underpins steady top-line expansion in the Denmark pharmaceutical market as value creation shifts toward intellectual-property-driven assets rather than high-volume manufacturing. Novo Nordisk’s outsized valuation amplifies systemic importance, prompting regulators to balance innovation incentives with macro-prudential oversight. Real-world evidence drawn from nationwide e-health infrastructure accelerates time-to-market for advanced therapies, while cross-border collaboration in Medicon Valley sustains a high-density talent pool. Biosimilar capacity investments diversify the Denmark pharmaceutical market’s production base, yet supply-chain dependence on imported active ingredients remains a structural vulnerability.

Key Report Takeaways

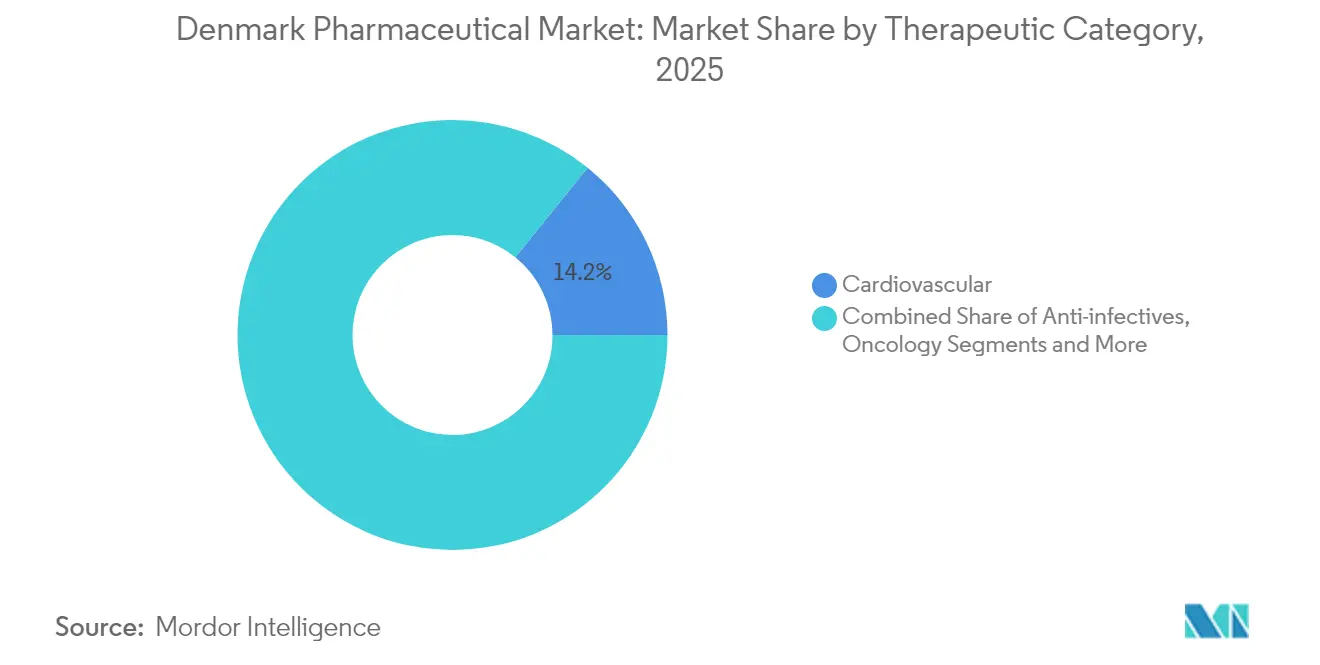

- By therapeutic category, cardiovascular treatments led with 14.18% of the Denmark pharmaceutical market share in 2025; oncology is forecast to expand at a 4.21% CAGR through 2031.

- By drug type, prescription medicines dominated with an 86.05% share of the Denmark pharmaceutical market size in 2025, whereas OTC products are poised to grow at a 3.8% CAGR to 2031.

- By formulation, tablets commanded 51.72% of the Denmark pharmaceutical market size in 2025, while injectables post the fastest 3.94% CAGR outlook.

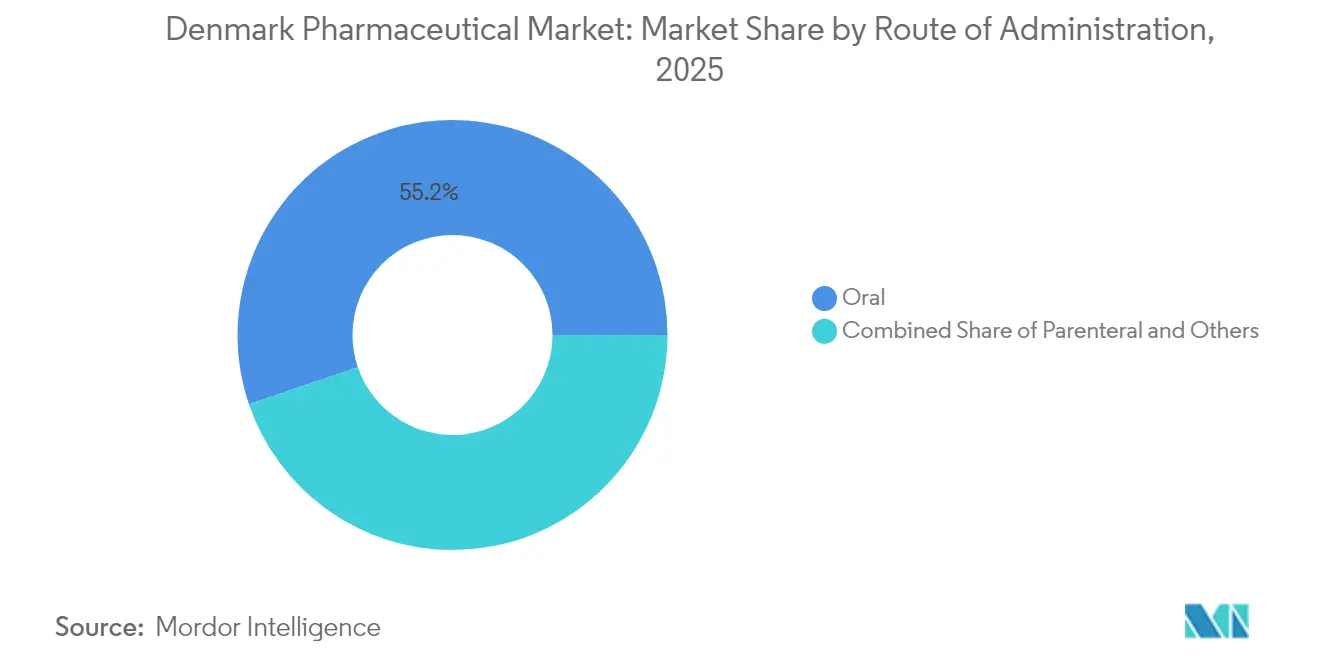

- By route of administration, oral drugs accounted for 55.21% of the Denmark pharmaceutical market share in 2025, but parenteral delivery is advancing at a 3.74% CAGR.

- By distribution channel, hospital pharmacies captured 46.83% revenue share in 2025; online pharmacies are projected to climb at a 4.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark Pharmaceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising R&D investments in biopharmaceuticals | +0.8% | Denmark, spillover to Nordic region | Long term (≥ 4 years) |

| Increasing prevalence of chronic diseases & aging population | +0.6% | National, urban concentration | Medium term (2-4 years) |

| Government incentives for life-science innovation clusters | +0.4% | Medicon Valley, Greater Copenhagen | Medium term (2-4 years) |

| Expansion of biosimilar manufacturing capabilities | +0.5% | National, export focus | Long term (≥ 4 years) |

| Digital health integration for adherence & companion services | +0.3% | National, early system adoption | Short term (≤ 2 years) |

| EU strategy harmonizing EMA fast-track approvals | +0.2% | EU-wide, Denmark first mover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising R&D Investments in Biopharmaceuticals

Sector R&D now absorbs roughly 60% of Denmark’s total research outlays, propelling the Denmark pharmaceutical market toward discovery-led value creation. The Novo Nordisk Foundation funds almost one-quarter of private research, compressing decision cycles but heightening concentration risk [1]Novo Nordisk Foundation, “Annual Impact Report 2023,” novonordiskfonden.dk. A USD 80 billion API capacity program accelerates scale-up, while USD 94 million of venture backing for oral biologics signals investor confidence beyond incumbents. Government life-science policy earmarks DKK 100 million annually to double exports by 2030, cementing long-run growth. Regulatory sandboxes that legitimize real-world data shorten approval timelines for advanced-therapy medicinal products, reinforcing Denmark’s first-mover edge.

Increasing Prevalence of Chronic Diseases & Aging Population

Demographic aging intensifies demand for diabetes, obesity, and cardiovascular drugs, anchoring revenue momentum in the Denmark pharmaceutical market. SELECT trial data broaden GLP-1 indications, spurring uptake across cardiometabolic cohorts. Off-label semaglutide use fell from 33% to 13% between 2022 and 2024 as clinical governance tightened. General-practice spending hit DKK 10.5 billion within a DKK 266 billion health budget, indicating resource strain from chronic care. Nationwide medication registers enable precision epidemiology that feeds drug-development pipelines. Digital prescriptions and patient portals close adherence gaps, generating data loops that further shape product design.

Government Incentives for Life-Science Innovation Clusters

A “red-carpet” licensing scheme cuts approval lead-times, pulling new capacity into the Denmark pharmaceutical market. Medicon Valley Alliance harmonizes Danish-Swedish research, reducing redundancy and amplifying shared infrastructure. Greater Copenhagen’s 40-plus microbiome startups leverage unique biobanks to accelerate clinical validation. A 2025 R&D tax credit lowers effective innovation costs by up to 25%. The Lundbeck Foundation targets strategic Danish ownership positions in five to eight health companies, ensuring patient capital for long-cycle science. Cluster effects now support 153,000 life-science jobs, reinforcing multiplier impacts across adjacent industries.

Expansion of Biosimilar Manufacturing Capabilities

Fermentation expertise and stringent regulators position Denmark as a low-risk choice for biosimilar scale-up, just as key biologics face patent expiry. Xellia’s USD 185 million asset sale to Hikma validates global appetite for Danish production quality. Sandoz booked 9% European growth underpinned by Danish supply nodes. Nordic manufacturers pursue net-zero facilities, differentiating their bids in tenders that now score carbon metrics. Skilled labor supply supports expansion, though wage inflation emerges as Novo Nordisk absorbs technical talent at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of innovative therapies limiting reimbursement | -0.4% | National, EU price spillover | Medium term (2-4 years) |

| Stringent price-cap negotiations with Danish Medicines Council | -0.3% | National | Short term (≤ 2 years) |

| Talent shortage in advanced cell & gene therapy manufacturing | -0.2% | National, biotech hubs | Long term (≥ 4 years) |

| Supply-chain dependence on imported APIs | -0.3% | National, EU linkage | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Innovative Therapies Limiting Reimbursement

GLP-1 drugs consumed 18% of regional drug budgets in 2024, straining payer headroom. A new QALY-based assessment adds transparency but leaves implicit cost-effectiveness thresholds, fueling launch-price uncertainty. Novo Nordisk trimmed Ozempic’s monthly list to USD 125 amid negotiations, illustrating leverage limits even for market leaders. A proposed three-year confidential discount program may delay patient access as details are ironed out. Pediatric reimbursement is 60% from first krone, while adults see zero support until surpassing DKK 1,075, creating equity debates. Cannabis pilot reimbursement caps illustrate selective subsidy expansion rather than broad budget loosening.

Stringent Price-Cap Negotiations with Danish Medicines Council

A 1.5% annual ceiling since 2008 forces real-price erosion, compelling firms to pursue high-value niches. New dispensing permits for unlicensed products ease shortage crises but add bureaucracy that smaller entrants may find prohibitive. Active-substance prescribing under study could accelerate generic uptake, but safety concerns linger. Antitrust scrutiny, highlighted by excessive-pricing findings in oxytocin, underscores aggressive enforcement appetite. Pharmacy Act reforms segregate prescription and retail margins, prompting renegotiation of channel economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Category: Cardiovascular Leadership Drives Stability

Cardiovascular drugs generated the largest slice of the Denmark pharmaceutical market in 2025 at a 14.18% share and will keep its lead as demographics skew older. Oncology contributes the fastest 4.21% CAGR, adding USD 0.1 billion in incremental revenue by 2031. Layered risk screening programs, such as the DANCAVAS trial, heighten early detection, expanding eligible patient pools. M&A momentum, highlighted by Novo Nordisk’s USD 1.112 billion Cardior purchase, shows incumbents reinforcing cardiovascular depth. Anti-infective volume remains relevant via Xellia’s fermentation stronghold, while gastroenterology explores nerve-stimulation modalities that could reset treatment paradigms.

Second-tier categories, including respiratory and anti-diabetes, benefit from digital inhaler monitoring and GLP-1 oral-formulation research, respectively. EMA safety guidance pushes continuous glucose monitors into standard diabetes trials, tightening cardiovascular endpoints and raising data-generating costs. Therapeutic diversification hedges against single-franchise risk inherent in the Denmark pharmaceutical market given Novo Nordisk’s weight.

By Drug Type: Prescription Dominance Faces OTC Momentum

Prescription lines contributed 86.05% of 2025 revenue, reflecting specialist-led care pathways embedded in Denmark’s health system. The Denmark pharmaceutical industry leverages strong payer relationships to secure formulary uptake, yet patent cliffs challenge branded products. OTC products expand 3.8% CAGR on self-medication trends and e-commerce convenience. Active-substance prescribing would further tilt scripts toward generics, eroding brand premiums. Trintellix exclusivity expiry in 2026 pressures Lundbeck to focus on Rexulti lifecycle management. Cannabinoid RX categories mature after the 2026 pilot transition, feeding both prescription and behind-the-counter segments.

By Formulation: Injectable Innovation Outpaces Tablets

Tablets retain 51.72% revenue share due to ease of administration, yet injectables increase at 3.94% CAGR thanks to biologics. Large-volume subcutaneous formats gain traction; a systematic pipeline review identified 182 candidates in late development. Novo Nordisk’s Hillerød expansion underscores device-driven stickiness in chronic therapies. Oral-biologic innovation financed by Orbis could erode parenteral share if bioavailability hurdles fall. Gene-therapy vectors push specialized vial and cold-chain solutions, adding complexity to formulation strategy in the Denmark pharmaceutical market.

By Route of Administration: Oral Preference Meets Parenteral Innovation

Oral products commanded 55.21% share, but parenteral delivery’s 3.74% CAGR aligns with biologics growth. Deal activity such as Novo Nordisk’s USD 2.2 billion obesity-pill partnership illustrates pursuit of oral alternatives to injectables. Transdermal research expands, though regulatory proving remains lengthy. Inhalational routes capture niche respiratory portfolios, aided by integrated digital spirometry that confirms dose compliance. Real-time adherence data feed value-based contract negotiations, deepening payer engagement across administration modes.

By Distribution Channel: Hospital Dominance Faces Digital Disruption

Hospital pharmacies controlled 46.83% of 2025 sales, reflecting centralized specialty dispensing. Online channels will add the most absolute revenue through 2031 as electronic prescriptions integrate with national ID authentication. Pharmacy-act amendments allow hospitals to sell directly to patients, intensifying competition with retail chains. Shared Medication Card interoperability cuts duplication, improving safety and enabling omni-channel fulfillment. Cross-border e-pharmacies within the EEA expand choice yet must still receive physical prescriptions, tempering convenience gains.

Geography Analysis

Pharmaceutical exports reached 24% of Danish goods trade in 2024, though two-thirds of physical output occurs abroad through merchanting, aligning profits with intellectual property domiciled in the Denmark pharmaceutical market . Medicon Valley accounts for over 60% of Scandinavian pharma jobs, leveraging cross-border research synergies and shared infrastructure. Greater Copenhagen’s microbiome specialization attracts capital with deep biobank assets. National e-health integration enables nationwide real-world evidence capture, reinforcing clinical-trial recruitment advantages.

Nordic ministers collaborate on medicine supply to buffer small-market vulnerabilities, including joint tenders for critical drugs. EU presidency periods allow Denmark to imprint patient-centric policy elements into continental legislation, shaping fast-track pathways that benefit its domestic innovators. Export dependence raises trade-policy sensitivity; any shift in U.S. or Chinese procurement could reverberate through Danish GDP given Novo Nordisk’s weight. Supply-neutral merchanting models mitigate tariff exposure but not reputational or regulatory shifts.

Competitive Landscape

Novo Nordisk’s capitalization surpasses Denmark’s GDP, illustrating extraordinary concentration in the Denmark pharmaceutical market. The Danish Competition Authority increases surveillance, evidenced by pricing cases against mid-tier suppliers. Specialty champions such as LEO Pharma, ALK-Abelló, and H. Lundbeck pursue deep therapeutic focus to avoid head-on clashes with the diabetes giant. Ferring scales gene-therapy capabilities through Nordic facilities, while Xellia capitalizes on complex anti-infective fermentation niches [3]Ferring Communications, “Gene Therapy Supply Chain,” ferring.com .

Venture funding supports new entrants; Orbis and Pharmacosmos exemplify start-ups expanding beyond legacy strongholds. Digital-health partnerships emerge as differentiators; AI-enabled discovery shortens target-identification cycles, while adherence apps bundle with high-value injectables.

Strategic expansions include a USD 1.2 billion rare-disease plant in Odense and a USD 400 million quality-control hub, showing Novo Nordisk’s reinvestment alignment with national priorities. Layoffs at LEO Pharma underscore cost-containment amid dermatology competition. Japanese and Indian firms deepen footholds via Danish subsidiaries and acquisitions, enhancing supply-chain diversity.

Denmark Pharmaceutical Industry Leaders

Novo Nordisk A/S

Leo Pharma A/S

H. Lundbeck A/S

Orifarm Group A/S

ALK-Abelló Nordic A / S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2022: Navamedic launches Eroxon® OTC erectile-dysfunction gel in Denmark.

- March 2025: DanCann Pharma secures exclusive rights to Tetra Pharm’s ZYNDIKATE® delivery technology in Denmark.

- December 2024: Novo Nordisk allocates DKK 8.5 billion for a rare-disease manufacturing site in Odense.

- August 2023: Mellozzan (melatonin) debuts in Denmark and Norway via Medice.

Denmark Pharmaceutical Market Report Scope

As per the scope of this report, pharmaceuticals are referred to as prescribed and nonprescription drugs. An individual can buy these medicines with or without a doctor's prescription. The report also covers an in-depth analysis of qualitative and quantitative data. The Danish pharmaceutical market is segmented by ATC/therapeutic class (blood and hematopoietic organs, cardiovascular system, dermatological, gastrointestinal system and metabolism, nervous system, respiratory system, and other classes), drug type (branded and generic), and prescription type (prescription drugs (Rx) and OTC drugs). The report offers the value (USD) for all the above segments.

By Therapeutic Category

| Anti-infectives |

| Cardiovascular |

| Gastrointestinal |

| Anti-diabetic |

| Respiratory |

| Oncology |

| Others |

By Drug Type

| Prescription Drugs | Branded |

| Generics | |

| OTC Drugs |

By Formulation

| Tablets |

| Capsules |

| Injectables |

| Others (Topicals, Patches, etc.) |

By Route of Administration

| Oral |

| Parenteral |

| Others (Inhalational, Transdermal) |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| By Therapeutic Category | Anti-infectives | |

| Cardiovascular | ||

| Gastrointestinal | ||

| Anti-diabetic | ||

| Respiratory | ||

| Oncology | ||

| Others | ||

| By Drug Type | Prescription Drugs | Branded |

| Generics | ||

| OTC Drugs | ||

| By Formulation | Tablets | |

| Capsules | ||

| Injectables | ||

| Others (Topicals, Patches, etc.) | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Others (Inhalational, Transdermal) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

Key Questions Answered in the Report

How big is the Denmark Pharmaceutical Market?

The Denmark Pharmaceutical Market size is expected to reach USD 4.18 billion in 2026 and grow at a CAGR of 3.24% to reach USD 4.89 billion by 2031.

What distribution channels are gaining the most traction through 2031?

Online pharmacies are expected to post a 4.14% CAGR as e-prescriptions integrate with Denmark’s national ID system and consumer uptake accelerates.

Who are the key players in Denmark Pharmaceutical Market?

Novo Nordisk A/S, Leo Pharma A/S, H. Lundbeck A/S, Orifarm Group A/S and ALK-Abelló Nordic A / S are the major companies operating in the Denmark Pharmaceutical Market.

Which therapeutic category contributes the largest share to Danish drug sales?

Cardiovascular treatments hold 14.18% of 2025 sales, driven by an aging population and expanded screening efforts.

Page last updated on: