Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

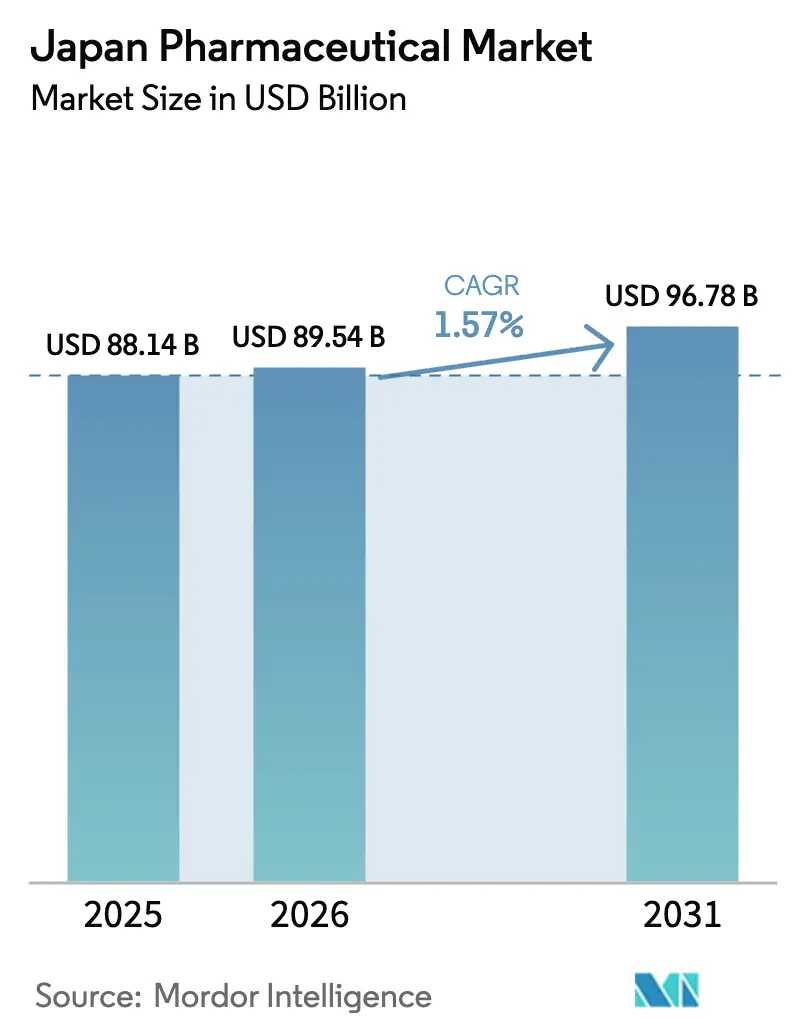

| Base Year Market Size (2025) | USD 88.14 Billion |

| Market Size (2026) | USD 89.54 Billion |

| Market Size (2031) | USD 96.78 Billion |

| Growth Rate (2026 - 2031) | 1.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Pharmaceutical Market Analysis by Mordor Intelligence

The Japan Pharmaceutical Market size is projected to be USD 88.14 billion in 2025, USD 89.54 billion in 2026, and reach USD 96.78 billion by 2031, growing at a CAGR of 1.57% from 2026 to 2031.

Ongoing reforms to drug pricing, rapid regulatory pathways for breakthrough therapies, and a rapidly aging demographic collectively shape a market in transition, with specialty products and self-care categories moving in opposite directions. Oncology’s momentum, robust pipeline replenishment after major patent expiries, and incentives that reward simultaneous global launches underpin premium-priced segments, while biennial price cuts and aggressive generic substitution squeeze commoditized therapies. Digital health adoption is gathering speed as telehealth-enabled prescription fulfillment and reimbursed software therapeutics deepen patient engagement and support volume growth. Foreign innovators leverage the SAKIGAKE framework to approach Japan as a first-wave launch market, adding competitive intensity. At the same time, persistent API import dependence and real-world evidence demands for reimbursement create volatility that firms must navigate.

Key Report Takeaways

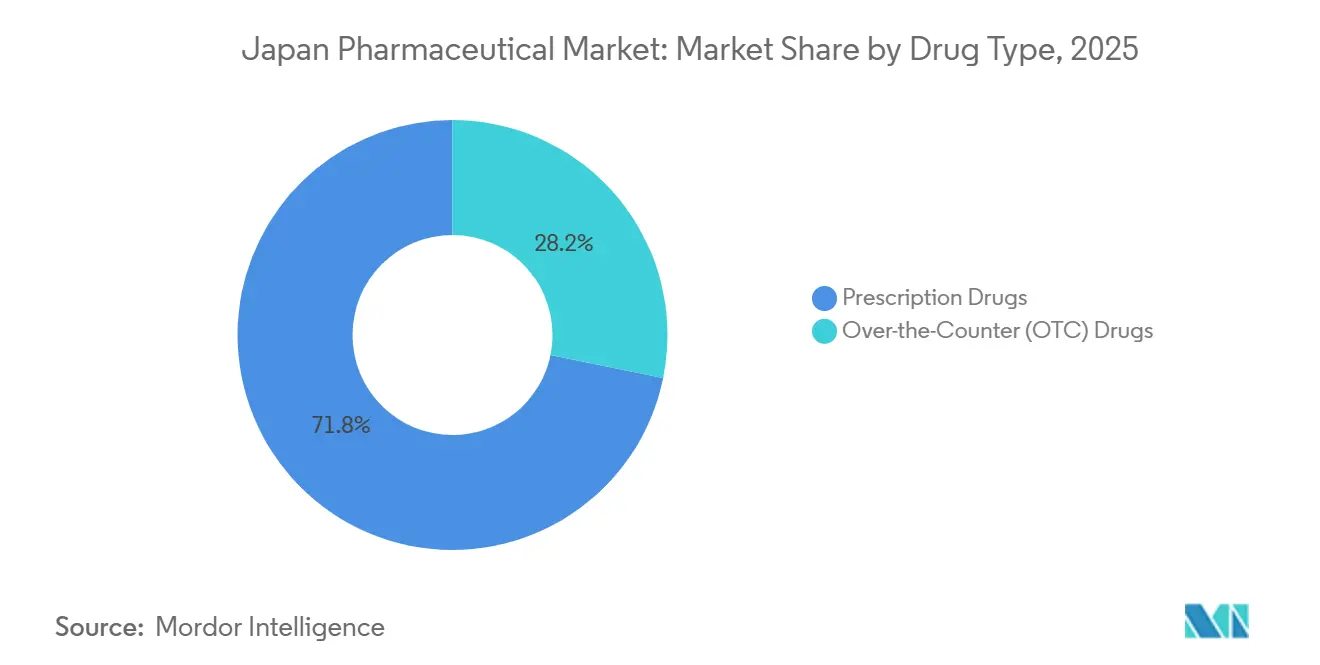

- By drug type, prescription medicines led with 71.78% revenue share in 2025, whereas over-the-counter products are forecast to expand at a 3.93% CAGR to 2031, the fastest within the segmentation.

- By therapeutic area, oncology commanded 18.73% of Japan's pharmaceutical market share in 2025 and is expected to post a 4.19% CAGR through 2031.

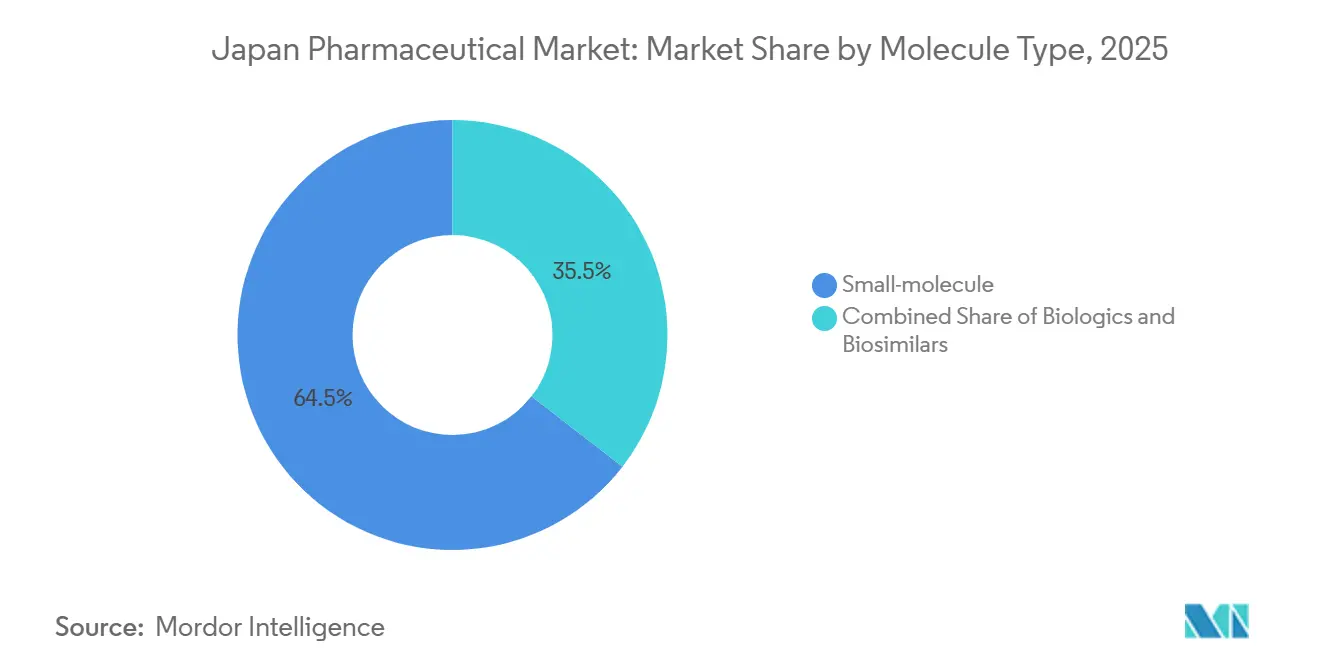

- By molecule, small-molecule agents accounted for 64.48% of the Japanese pharmaceutical market size in 2025, while biologics are projected to grow at a 4.97% CAGR between 2026 and 2031.

- By formulation, oral products captured 55.26% revenue share in 2025; injectables represent the high-growth pocket with a 3.74% CAGR forecast to 2031.

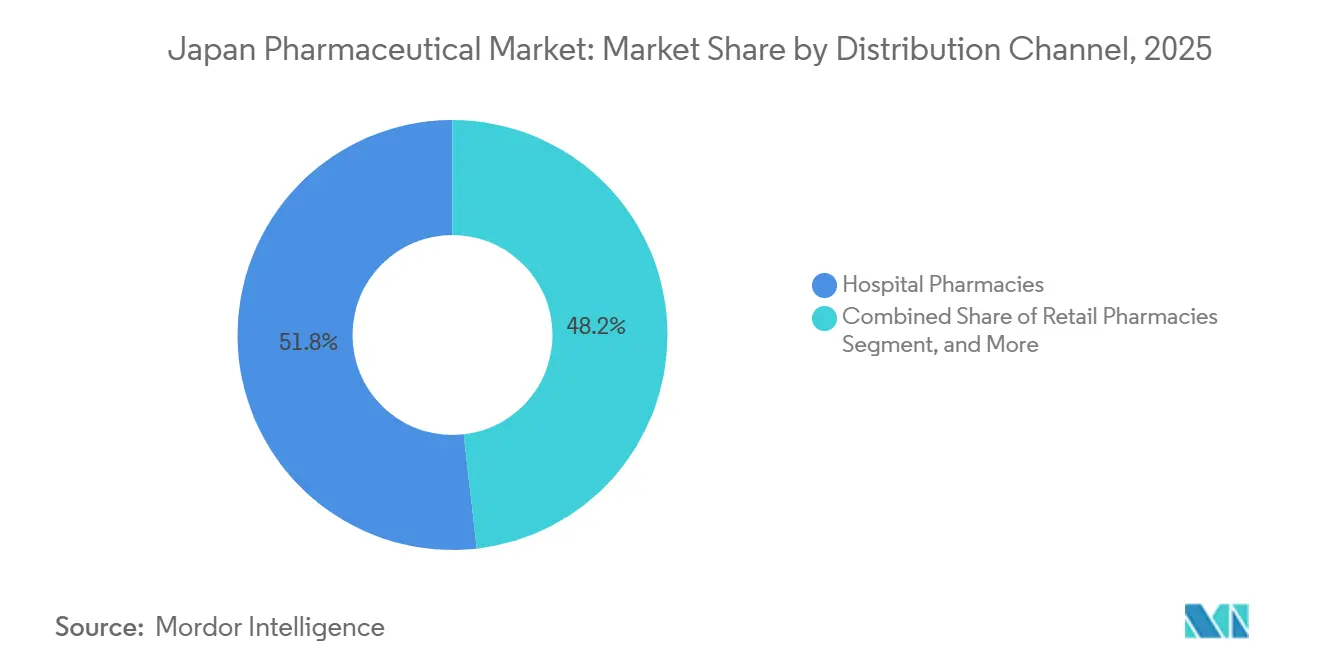

- By distribution, hospital pharmacies retained a 51.84% share in 2025; online and mail-order channels are set to advance at a 4.51% CAGR, outpacing all other routes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Pharmaceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent-Cliff Replenishment Through Specialty Drugs | +0.4% | National, concentrated in Tokyo and Osaka metropolitan areas | Medium term (2-4 years) |

| Fast-Track Regulatory Pathways for Breakthrough Therapies | +0.3% | National, with spillover to PMDA-recognized foreign trial sites | Short term (≤ 2 years) |

| Growing Burden of Oncology & Rare Diseases | +0.3% | National, higher incidence in aging prefectures (Akita, Shimane) | Long term (≥ 4 years) |

| Ageing Population Driving Chronic Therapies | +0.2% | National, acute in rural prefectures with >35% elderly population | Long term (≥ 4 years) |

| MHLW Incentives for Companion Diagnostics Integration | +0.2% | National, early adoption in university hospitals and cancer centers | Medium term (2-4 years) |

| Digital-Health-Enabled Adherence Solutions Boosting Prescriptions | +0.1% | National, pilot programs in Tokyo, Osaka, Fukuoka | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Patent-Cliff Replenishment Through Specialty Drugs

Blockbuster experiences have prompted companies to shift toward higher-value, lower-volume assets that maintain pricing power. Humira biosimilars captured 22% of adalimumab prescriptions within 18 months of their 2024 launch, prompting originators to redirect their research and development efforts to antibody–drug conjugates and rare disease enzymes. Takeda’s USD 2.1 billion biologics complex under construction in Fujisawa illustrates capital redeployment toward niche therapies that can earn a 10% premium under the expanded Premium on Marketability Promotion incentive.[1]Takeda Pharmaceutical Company, “Fujisawa Biologics Facility Investment,” Takeda.com Smaller biotechs partner with domestic distributors to co-file rapid-launch products, thereby compressing the traditional lag in Japan launches. As margins on legacy drugs decline, specialty pipelines become the preferred hedge against pricing attrition.

Fast-Track Regulatory Pathways for Breakthrough Therapies

The SAKIGAKE designation reduced the median approval review time to nine months in 2024, compared to fourteen months under the conventional process.[2]Pharmaceuticals and Medical Devices Agency, “SAKIGAKE Designation and Conditional Approval Framework,” PMDA.go.jp Conditional approvals granted to oncology biologics, such as Chugai’s Polivy, allowed revenue capture while confirmatory trials continued, a competitive lever rarely available in Europe. Multinationals with global data packages, including AstraZeneca’s Enhertu, have captured double-digit market shares within a year of launch. Real-world evidence obligations introduced in 2025 raise compliance costs, but firms with robust pharmacovigilance infrastructure view the requirement as manageable.

Growing Burden of Oncology & Rare Diseases

Japan reported 1.02 million new cancer cases in 2024, and the proportion of citizens aged 65 years or older increased to 28.9% in 2025. Extended life expectancy raises the prevalence of malignancies and genetic disorders that demand high-cost targeted drugs. Rare-disease designations climbed to 87 in 2024 as expanded exclusivity rules drew global developers to file in Tokyo concurrently with Western markets. Kyowa Kirin’s burosumab secured reimbursement within 90 days of approval, validating payers’ willingness to fund ultra-orphan therapies when evidence is compelling.

Ageing Population Driving Chronic Therapies

Chronic conditions affect more than 70% of Japan’s seniors, and the average number of daily prescriptions per elder stands at 6.2, creating adherence challenges. Partnerships, such as Daiichi Sankyo’s 2024 alliance with NTT Data, deploy AI reminder tools across 500 community pharmacies, reducing hospitalizations related to medication errors. Digital therapeutics for diabetes and hypertension became reimbursable under the 2025 revision of long-term care insurance, integrating software into standard treatment pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Drug-Price Revisions & Biennial Cuts | -0.3% | National, acute for high-volume generic manufacturers | Short term (≤ 2 years) |

| Generic Substitution Pressure | -0.2% | National, concentrated in primary-care and retail pharmacy channels | Medium term (2-4 years) |

| Long Approval Timelines for Regenerative Medicines Post-Review | -0.1% | National, affecting university hospitals and specialized centers | Long term (≥ 4 years) |

| Supply-Chain Vulnerabilities for Critical APIs | -0.1% | National, with dependencies on China and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

National Drug-Price Revisions & Biennial Cuts

The April 2024 revision reduced reimbursement for 53% of listed drugs, with an average decrease of 4.8% for brand-name drugs and 7.2% for generic drugs.[3]Ministry of Health, Labour and Welfare, “Drug Pricing System and Biennial Revisions,” MHLW.go.jp Off-year cuts introduced in 2025 targeted high-selling therapies where transaction prices were undershot by at least 2% of the list prices. Sawai’s operating profit fell 9.3% in fiscal 2024, as prices for atorvastatin and amlodipine declined. As value-based pricing expands, products lacking compelling real-world evidence are likely to face deeper erosion, accelerating consolidation.

Generic Substitution Pressure

Generics supplied 80% of prescription volume but only 38% of value in 2024. Government targets call for 85% volume penetration by 2026, yet quality recalls of imported APIs temper uptake in critical-care categories. Biosimilars gained just 18% of the adalimumab market by year-end 2024, due to physician caution and a lack of interchangeability status. To overcome inertia, Nichi-Iko priced its rituximab biosimilar 30% below the reference biologic.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: OTC Gains Amid Prescription Dominance

Prescription medicines accounted for 71.78% of 2025 revenue, yet the over-the-counter segment is expected to advance at a 3.93% CAGR, more than double the CAGR of the Japan pharmaceutical market. The switch of loxoprofen to OTC status in 2024 exemplifies policy efforts to migrate routine pain management from clinics to retail shelves. Self-medication trends among seniors lifted analgesic and gastrointestinal remedy volumes throughout 2025, while e-commerce platforms captured incremental share.

Margin pressure persists for branded prescriptions because biennial revisions tamp profitability. Still, specialty injectables for rheumatoid arthritis and multiple sclerosis remain insulated, sustaining Japan's pharmaceutical market share leadership in prescription lines. Consumer-health divisions invest in influencer-led digital campaigns to grow OTC supplements, reflecting divergent strategies within the same corporate groups.

By Therapeutic Area: Oncology Leads Innovation Pipeline

Oncology represented 18.73% of therapeutic-area revenue in 2025 and is expected to post a 4.19% CAGR through 2031, underscoring its status as the growth engine of the Japanese pharmaceutical market. Enhertu’s JPY 87 billion in domestic sales for fiscal 2024 demonstrates the speed at which innovative products penetrate once reimbursement is secured.

Conversely, cardiovascular drugs advance at only 0.8% CAGR as generics dominate statins and ACE inhibitors. Diabetes therapies experience volume growth but face scrutiny regarding cost-effectiveness. Central nervous system pipelines suffer from high attrition in dementia trials, while respiratory biologics show moderate momentum due to rising urban asthma prevalence. Oncology, therefore, captures investment and launch priority across multinational and domestic portfolios.

By Molecule Type: Biologics Ascend as Small Molecules Plateau

Small molecules maintained a 64.48% share of the Japanese pharmaceutical market in 2025. However, biologics are forecast to expand at a 4.97% CAGR to 2031, tripling the overall market pace. Hemlibra’s JPY 62 billion in sales for 2024 highlights the premium value of biologics.

Biosimilars, although nascent, temper biologic price inflation; however, the lack of interchangeability rulings hinders substitution. New investments, such as Fujifilm’s JPY 100 billion Chiba facility, indicate confidence in sustained demand for biologics. Small molecules face commoditization outside oncology, accelerating portfolio shifts toward complex injectables and hybrid conjugates.

By Formulation: Injectables Gain on Device Innovation

Oral agents held a 55.26% share in 2025, yet injectables will grow at a 3.74% CAGR through 2031, buoyed by home-use auto-injectors. Long-acting psychotropic injections, typified by Abilify Maintena, improved adherence and reduced relapse hospitalizations in 2025, encouraging broader deployment across endocrinology and immunology portfolios.

Device partnerships, such as Ypsomed–Sumitomo’s reusable injector for GLP-1 agonists, extend lifecycle protection and enhance patient convenience. Topical and other niche formulations remain stable but contribute limited value growth.

By Distribution Channel: Online Pharmacies Disrupt Traditional Models

Hospital pharmacies dispensed 51.84% of Japan's pharmaceutical market in 2025, reflecting their control of oncology and infusion therapies, yet online and mail-order outlets are expected to record a 4.51% CAGR, nearly triple the market average. Regulatory clearance for telehealth prescription fulfillment in 2024 enabled Amazon Pharmacy Japan and Rakuten to secure a combined 8% share of the retail prescription market by late 2025.

Brick-and-mortar chains respond by adding clinical services, but same-store volumes fell for leading retailers such as Ain Pharmacies. Hospital outlets remain indispensable for complex biologics, but some infusions are expected to shift to outpatient centers to lower inpatient costs.

Competitive Landscape

The five leading domestic companies, Takeda, Astellas, Daiichi Sankyo, Chugai, and Otsuka, captured higher 2025 revenue, indicating moderate concentration. Multinationals utilize the SAKIGAKE program to launch targeted biologics ahead of their domestic peers, thereby intensifying rivalry. Takeda, Astellas, and Daiichi Sankyo, together, still hold a formidable presence; however, off-patent erosion and generics price controls constrain margin expansion.

Generic producers remain fragmented; the top ten held a 54% volume share in 2025, but falling unit prices have induced merger talks between Sawai and Nichi-Iko to achieve a procurement scale. Technology investment now differentiates leaders: Daiichi Sankyo’s AI-assisted antibody-drug conjugate discovery cut preclinical timelines by 18 months, while Chugai’s PMDA-approved digital pathology platform slashed screening costs. PeptiDream monetized its peptide-discovery engine via 14 partner deals worth USD 340 million in 2025 alone, illustrating value capture without a marketed product.

White-space opportunities lie in prescription digital therapeutics, where CureApp’s first-in-class smoking-cessation software faces limited competition, and regenerative medicines, where stringent post-marketing demands deter smaller challengers but create moats for capitalized incumbents.

Japan Pharmaceutical Industry Leaders

Chugai Pharmaceutical Co., Ltd.

Astellas Pharma Inc.

Takeda Pharmaceutical Co. Ltd.

Otsuka Pharmaceutical Co., Ltd

Daiichi Sankyo Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Daiichi Sankyo and AstraZeneca secured PMDA approval for Enhertu in HER2-low breast cancer, expanding the eligible population by 55% and projecting peak domestic sales of JPY 150 billion.

- May 2025: Shionogi announced the JPY 150–160 billion acquisition of Torii Pharmaceutical and Japan Tobacco’s pharma assets, bolstering its allergy and dermatology franchise while adding U.S. R&D capacity.

- August 2024: Japan Tobacco and Torii Pharmaceutical announced that VTAMA Cream 1% (tapinarof) was listed on the NHI schedule for atopic dermatitis and plaque psoriasis, offering a steroid-free, once-daily topical option under a licensing agreement with Dermavant Sciences.

- July 2024: Chugai obtained exclusive rights to inavolisib, a PI3Kα inhibitor, following positive Phase III results, thereby strengthening its breast cancer portfolio with a breakthrough-designated candidate.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Japan pharmaceutical market as all prescription and non-prescription human drugs sold in the country, valued at ex-factory prices and expressed in USD at the average annual rate. According to Mordor Intelligence, the 2025 baseline is USD 86.3 billion, extending to USD 93 billion by 2030 at a 1.51 % CAGR.

Scope Exclusions: Veterinary medicines, medical devices, bulk APIs traded for export, and traditional Kampo supplements sit outside this scope.

Segmentation Overview

- By Drug Type

- Prescription Drugs

- Over-the-Counter (OTC) Drugs

- By Therapeutic Area

- Oncology

- Cardiovascular

- Anti-diabetic

- Central Nervous System

- Infectious Disease

- Respiratory

- Others

- By Molecule Type

- Small-molecule

- Biologics

- Biosimilars

- By Formulation

- Oral

- Injectable

- Topical

- Other Formulations

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online & Mail-Order Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed hospital pharmacists, generics manufacturers, oncology KOLs, and former PMDA reviewers across Kanto, Kansai, and Kyushu. These conversations clarified real-world generic penetration, discount coefficients applied after the 2025 price revision, and emerging distribution shifts toward online pharmacies, allowing us to stress-test desk assumptions.

Desk Research

We began with authoritative public datasets, including the Ministry of Health, Labor and Welfare (NHI price list, annual drug spend), PMDA approval archives, Statistics Bureau health-care expenditure tables, and Federation of Pharmaceutical Manufacturers of Japan releases, which frame volume, price, and therapy-level trends. Our analysts then layered macro signals from OECD Health Stats, UN Population Division aging curves, and WHO cancer and diabetes registries to capture demand drivers. To refine company-side inputs, we drew selectively on D&B Hoovers for Japanese pharma financials, Questel for recent oncology and biosimilar patents, and Volza shipment records that illustrate import flows of key biologics. Press releases, investor decks, and peer-reviewed journals filled clinical-pipeline and pricing-revision gaps. This list is illustrative; many other credible sources fed into validation.

Market-Sizing & Forecasting

We apply a top-down reconstruction of national drug spending, adjusting NHI reimbursement totals for wholesale and hospital mark-ups to reach ex-factory value, before verifying with sampled bottom-up roll-ups of listed suppliers' Japan revenues and ASP × volume checks in oncology, diabetes, and cardiovascular segments. Key variables include the annual price-cut coefficient, generic uptake rate, treated-patient prevalence for five chronic conditions, biosimilar share, and mail-order channel mix. A multivariate regression, anchored to the aging population trajectory and chronic disease incidence, projects demand; scenario analysis buffers currency swings. Where supplier disclosure is patchy, we gap-fill using moving-average imputation benchmarked to historical unit growth.

Data Validation & Update Cycle

Every model output passes tri-layer checks: variance against government spend, peer ratio benchmarking, and senior analyst review. Reports refresh yearly and trigger mid-cycle updates when policy or epidemiology shifts exceed preset thresholds. Before release, an analyst re-runs the model so clients always receive the latest view.

Why Mordor's Japan Pharmaceutical Baseline Earns Stakeholder Confidence

Published estimates often diverge, as firms choose differing price bases, therapeutic scopes, and refresh cadences.

Key gap drivers include some studies that quote retail-level sales or bundle health-supplement lines; others bake aggressive biologic ASP erosion or freeze currency at a single spot rate, while Mordor rolls a five-year average; a few rely on global company financials without isolating Japan.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 86.3 B (2025) | Mordor Intelligence | - |

| USD 71.5 B (2024) | Global Consultancy A | Retail sales value, narrower therapy list |

| USD 82.27 B (2024) | Industry Analytics B | Uses aggressive ASP cuts, single-year FX |

| USD 95.87 B (2024) | Regional Consultancy C | Includes traditional medicines and distribution margins |

Taken together, the comparison shows that by anchoring to ex-factory prices, disclosing scope, and re-calibrating each year, Mordor delivers a balanced, transparent baseline clients can reuse and audit with confidence.

Key Questions Answered in the Report

How large will Japan’s pharmaceutical market be in 2031?

It is forecast to reach USD 96.78 billion by 2031 on a 1.57% CAGR.

Which therapeutic segment is expanding the fastest?

Oncology leads, supported by a 4.19% CAGR and growing use of antibody–drug conjugates.

What share do biologics hold and how quickly are they growing?

Biologics segment are projected to grow at a 4.97% CAGR through 2031.

How are online pharmacies changing drug distribution?

Regulatory changes in 2024 enabled telehealth prescription fulfilment, allowing online channels to grow at a 4.51% CAGR through 2031.

Why are specialty drugs prioritized by domestic firms?

Patent expiries and biennial price cuts erode margins on mass-market drugs, pushing companies toward high-value assets that earn launch premiums.

What is the key supply-chain risk facing manufacturers?

Over 80% of critical APIs are imported, exposing firms to geopolitical disruptions and quality-control issues.

Page last updated on: