India Plasma Fractionation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.77 Billion |

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

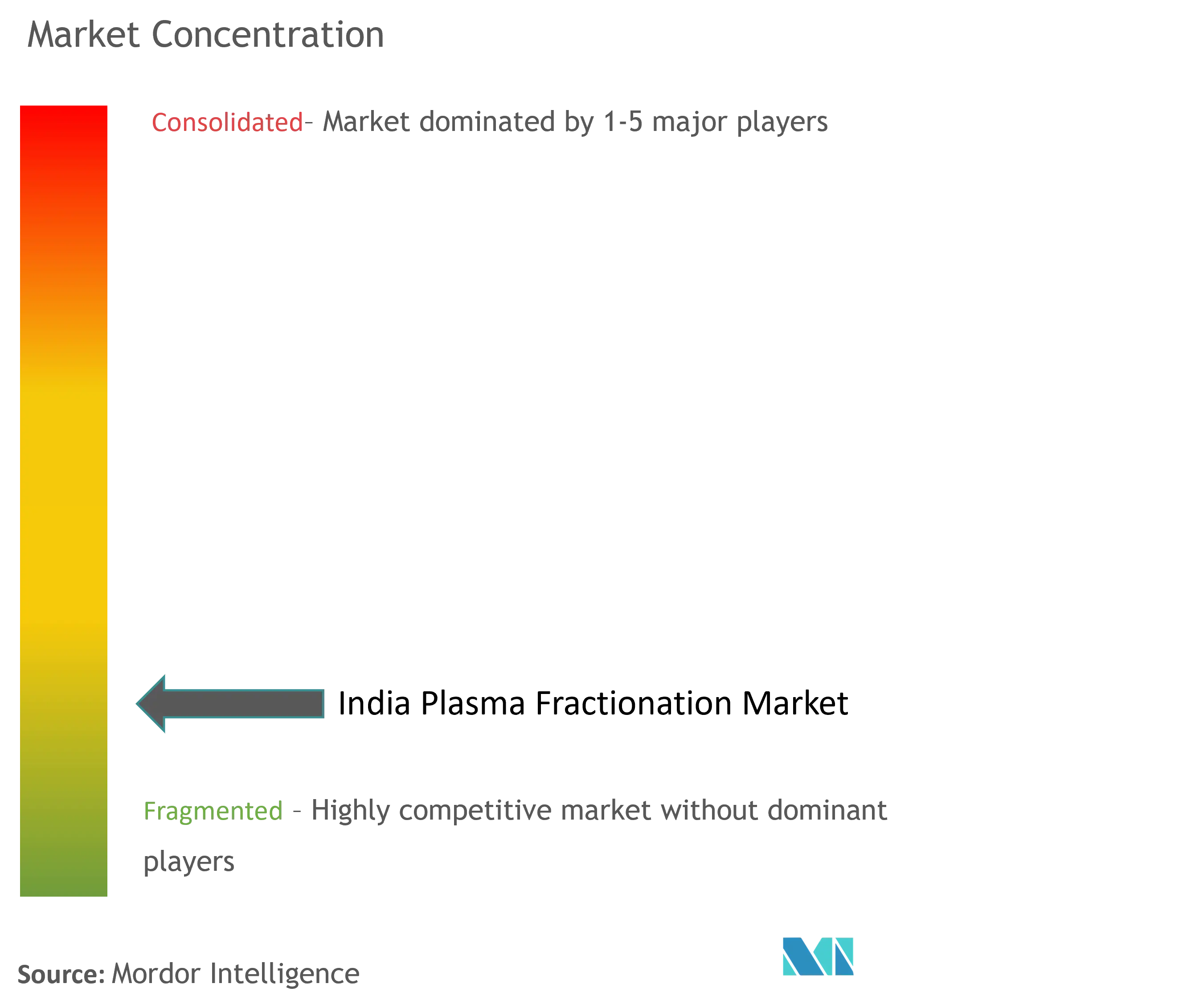

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Plasma Fractionation Market Analysis by Mordor Intelligence

India plasma fractionation market size in 2026 is estimated at USD 1.88 billion, growing from 2025 value of USD 1.77 billion with 2031 projections showing USD 2.56 billion, growing at 6.31% CAGR over 2026-2031. Demand growth rides on the widening diagnosis of primary immunodeficiency disorders, a steady rise in albumin use for critical-care burn management, and the government’s Production Linked Incentive (PLI) scheme, which reimburses incremental domestic biologics output and attracts fresh capital into fractionation parks. Manufacturers are pivoting from the legacy Cohn–Oncley precipitation process toward high-throughput chromatography skids that boost immunoglobulin yield and cut buffer consumption, thereby lowering per-liter conversion cost and aligning with National List of Essential Medicines (NLEM) price ceilings. Post-COVID capital upgrades in public blood banks now provide a larger and safer domestic plasma pool, reducing import exposure while improving long-term supply resilience. Competitive intensity continues to rise as global players secure technology partnerships and Indian firms draw private-equity funding to scale specialty fractions aimed at underserved orphan indications.

Key Report Takeaways

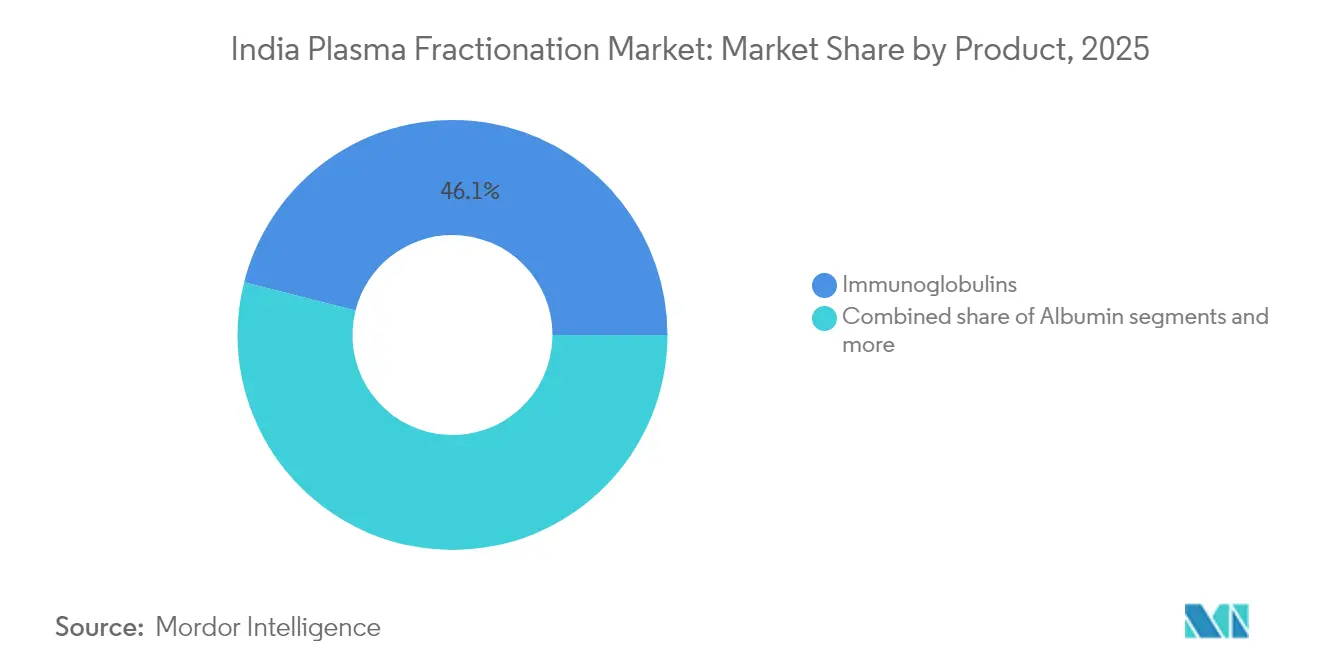

- By product category, immunoglobulins led with a 46.05% revenue share in 2025; hyper-immune and other fractions are projected to expand at a 7.02% CAGR through 2031.

- By application, immunology accounted for 38.10% of the India plasma fractionation market share in 2025, while neurology is advancing at a 7.39% CAGR through 2031.

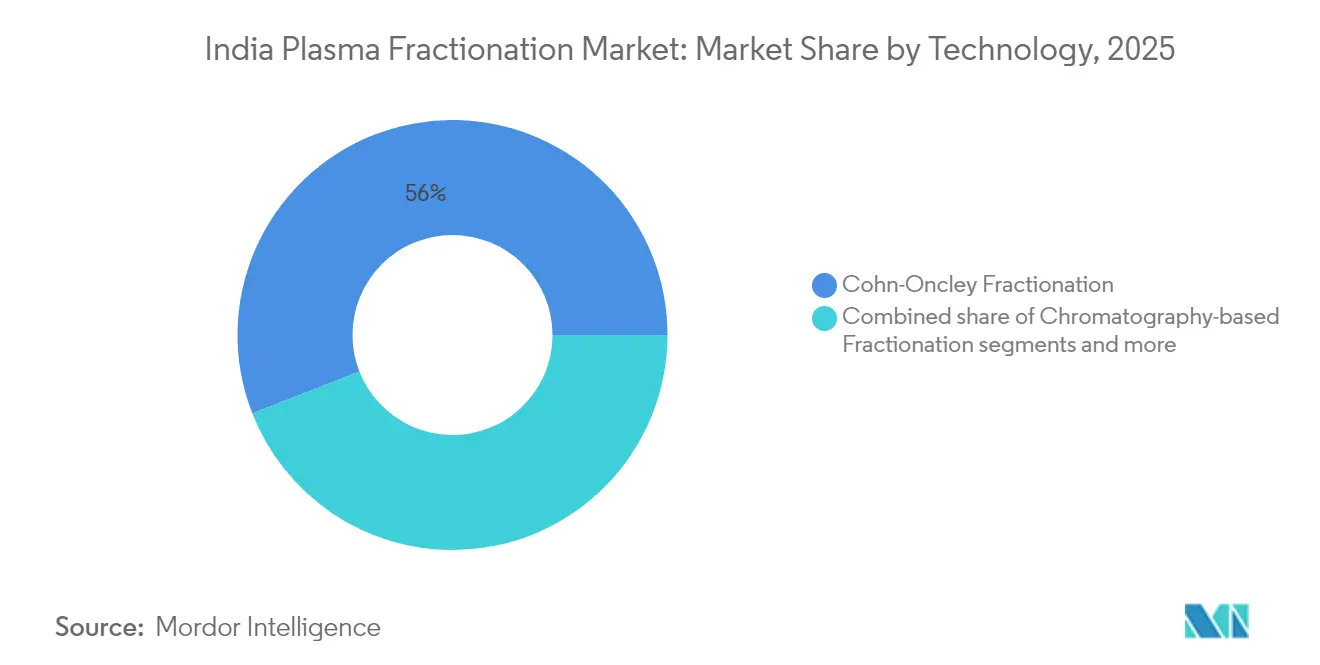

- By technology, Cohn–Oncley fractionation commanded 55.95% of the India plasma fractionation market size in 2025; chromatography-based fractionation is expected to grow at an 8.22% CAGR to 2031.

- By end user, hospitals held 53.25% of the India plasma fractionation market share in 2025, whereas specialty clinics record the highest anticipated CAGR at 7.78% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on plasma fractionation market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Plasma Fractionation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of primary immunodeficiency disorders | +1.2% | National, with higher incidence in urban centers | Medium term (2-4 years) |

| Expansion of public blood-collection infrastructure post-COVID-19 | +0.8% | National, with focus on tier-2 cities | Short term (≤ 2 years) |

| Rising demand for albumin in critical-care burn management | +0.6% | National, concentrated in metro hospitals | Medium term (2-4 years) |

| Government incentives for domestic biologics manufacturing under PLI scheme | +1.5% | National, with manufacturing hubs in Gujarat, Maharashtra | Long term (≥ 4 years) |

| Integration of next-gen chromatography skids lowering per-liter cost | +0.9% | National, early adoption in private facilities | Medium term (2-4 years) |

| Emergence of hospital-based plasma collection centres in tier-2 cities | +0.7% | Regional, focused on tier-2 urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing prevalence of primary immunodeficiency disorders

Specialised immunology units in Delhi, Mumbai and Bengaluru increasingly deploy flow-cytometry and next-generation sequencing panels able to detect X-linked agammaglobulinemia and common variable immunodeficiency in early childhood, swelling the cohort of patients who require lifelong intravenous immunoglobulin therapy. Greater clinical awareness, wider reimbursement under Ayushman Bharat and structured care pathways published by the Indian Society for Primary Immune Deficiency shorten diagnosis-to-treatment timelines, producing a structural lift in immunoglobulin volume. Manufacturers responded by introducing 10% concentration formulations that reduce infusion time per patient visit, freeing hospital chair capacity and nudging monthly throughput upward. Rising therapeutic adherence further locks in annuity-style demand for high-margin products within the India plasma fractionation market. The scale of unmet need remains sizeable because only a fraction of potential patients are yet diagnosed, implying a multi-year contribution to overall market growth.

Expansion of public blood-collection infrastructure post-COVID-19

India’s rapid pandemic response left a legacy of upgraded transfusion facilities, including convalescent plasma banks equipped with pathogen-reduction technology that have since been repurposed for routine fractionation supply. The e-RaktKosh portal now matches donors with district hospitals, reduces wastage and raises traceability standards, while refrigerated vans funded through the National Health Mission improve first-mile cold-chain integrity in tier-2 cities. Capacity at 1,75,338 Ayushman Arogya Mandirs enhances grass-roots community engagement, encouraging voluntary plasma donation drives that target youth cohorts through social-media campaigns. Early data show a 12% year-on-year uptick in voluntary donors across select states, translating to higher domestic raw-plasma availability and lowering reliance on imported source material. The effect is to stabilise supply for fractionators and to buffer the India plasma fractionation market against global plasma-trade disruptions.

Rising demand for albumin in critical-care burn management

Urban tertiary hospitals are standardising albumin infusion protocols after local randomised trials demonstrated a 30% reduction in intra-operative crystalloid volume and vasopressor requirements when 20% human albumin is used during major oncologic surgery. Dedicated burn units in Chennai and Ahmedabad prescribe albumin earlier in resuscitation to manage capillary leak, driving higher daily dose usage per bed. Domestic producer Reliance Life Sciences sells double-pasteurised AlbuRel vials that meet WHO virus safety benchmarks, helping hospitals replace costlier imports. Meanwhile, the Union Budget earmarks funds for new critical-care blocks under the Pradhan Mantri–Ayushman Bharat Health Infrastructure Mission, signalling long-term capacity expansion. These intertwined factors lift albumin consumption and amplify its contribution to overall revenue growth for the India plasma fractionation market.

Government incentives for domestic biologics manufacturing under PLI scheme

The PLI scheme offers cash-back incentives on incremental sales of plasma products and has cleared 764 project applications, committing INR 1.61 lakh crore and creating more than 11.5 lakh jobs across pharmaceutical verticals. Within this framework, 32 critical bulk API projects are already commercial, delivering ethanol, glycine and chromatography resins that previously depended on imports. The Ministry of Chemicals and Fertilizers has also inaugurated 27 bulk-drug parks that share effluent treatment and solvent recovery assets, lowering fixed operating costs for plasma processors. By coupling fiscal incentives with infrastructure, the policy improves unit economics, spurs capacity build-out and fosters technology partnerships that import advanced fractionation know-how into Indian plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low plasma donation rate per 1,000 population | -1.8% | National, more acute in rural areas | Long term (≥ 4 years) |

| Price controls under National List of Essential Medicines (NLEM) | -0.9% | National, affecting all healthcare providers | Medium term (2-4 years) |

| Inter-state logistical bottlenecks for cold-chain transport | -0.6% | National, particularly affecting remote regions | Short term (≤ 2 years) |

| Dependency on imported fractionated intermediates | -1.1% | National, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low plasma donation rate per 1,000 population

India collects just 11 million blood units annually for a population surpassing 1.4 billion, reflecting donation density below 0.8 units per 1,000 people[1]Source: Nature Communications, “Therapies From Industrial Plasma Waste,” nature.com —far short of the WHO’s 10-unit benchmark. Geospatial studies of eight northern states reveal vast “blood deserts,” where 61% of residents have no timely access to transfusion services, forcing hospitals to rely on replacement donors or purchase imported plasma at premium cost. Cultural misconceptions, scant awareness campaigns and long travel times to donation centres impede voluntarism in rural belts. Although the National Blood Policy promotes 100% voluntary donation, underfunded district programmes struggle to move beyond sporadic drives. As fractionators elevate capacity, supply tightness keeps raw-plasma procurement costs high and acts as a structural drag on the India plasma fractionation market growth trajectory.

Price controls under National List of Essential Medicines (NLEM)

The National Pharmaceutical Pricing Authority froze prices for 651 essential formulations in 2024 after wholesale inflation eased, leaving ceiling prices for albumin, immunoglobulin and coagulation factors unchanged. Stable prices safeguard patient affordability but compress manufacturer margins as electricity, labour and single-use consumable costs rise. Larger firms mitigate pressure via higher process yields and economies of scale, yet smaller plants equipped with dated precipitation lines face thin profitability that discourages expansion investment. Unless price caps are coupled with differential reimbursement or input-cost pass-through mechanisms, constrained earnings will limit innovation spending and moderate the India plasma fractionation market’s supply-side response.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Immunoglobulins anchor market scale while hyper-immune fractions accelerate

Immunoglobulins retained a commanding 46.05% share of 2025 revenue within the India plasma fractionation market, cemented by their role in chronic therapy for primary immunodeficiencies and acute immunomodulation protocols for Guillain–Barré syndrome. Monthly offtake at tertiary hospitals jumped as clinicians switched to 10% IVIG formulations that cut chair time and raise bed utilisation efficiency. Albumin, the second-largest product, rides on expanded burn-care capacity and more aggressive fluid-resuscitation protocols in cancer surgery. Factor concentrates cater to haemophilia A and B, yet growth is slower because recombinant alternatives, including gene therapy pipelines, begin nibbling at volume.

Hyper-immune and other niche fractions, though still modest in value terms, post the fastest 7.02% CAGR as processors exploit industrial plasma waste to isolate ceruloplasmin for aceruloplasminemia or anti-D immunoglobulin for Rh prophylaxis. Research collaborations with national institutes explore fibrinogen-rich cryo-precipitate derivatives for topical wound-healing sprays, broadening therapeutic horizons. Domestic processors thus court specialist demand pockets that face limited foreign competition, creating fresh revenue streams and improving overall plasma-utilisation yield in the India plasma fractionation market.

By Application: Neurology outpaces traditional immunology indications

Immunology remains the anchor application, absorbing 38.10% of 2025 consumption as more patients with hypogammaglobulinemia gain diagnosis and reimbursement coverage. Yet neurology now advances at a 7.39% CAGR—the fastest among segments—on the back of accumulating evidence for IVIG efficacy in chronic inflammatory demyelinating polyneuropathy and paediatric autoimmune neuropsychiatric disorders. Neuro-immunology clinics report higher per-patient dosage intensity, often spanning five-day loading regimens and ongoing maintenance cycles.

Hematology applications hold steady as national haemophilia treatment centres broaden factor infusion coverage, though recombinant entrants temper volume acceleration. Critical-care and trauma units provide a stable baseline for albumin demand, while dermatology and ophthalmology explore off-label plasma protein use. AI-driven diagnostic algorithms flag atypical immune profiles from electronic medical records, nudging clinicians toward earlier immunoglobulin consideration and thereby widening the patient funnel for the India plasma fractionation market.

By Technology: Chromatography wins investment priority over legacy precipitation

Legacy Cohn–Oncley precipitation still handles 55.95% of 2025 production because older plants are fully depreciated, require modest upkeep and deliver predictable output. Their disadvantages—lower protein yield and heavy ethanol consumption—become evident under price-ceiling regimes. Consequently, new entrants and upgrade projects increasingly favour chromatography-based fractionation, which expands at an 8.22% CAGR. Twin-column continuous systems recover more IgG per litre, produce purer albumin and leave less residual solvent, improving sustainability profiles that appeal to ESG-minded investors.

Hybrid flowsheets intermix ethanol precipitation for bulk separation and ion-exchange chromatography for polishing, balancing capex and performance. Emerging single-use technologies replace stainless-steel piping with disposable flow-paths, cutting cleaning validation downtime and enabling rapid product switches. Facilities employing these modules achieve turnaround gains of up to 25% and energy savings that buffer against utility tariff hikes. Adoption of continuous-flow precipitation units that integrate inline buffer adjustment further reduces footprint and cements the technology shift shaping the future cost curve for the India plasma fractionation market.

By End User: Specialty clinics command fastest growth as care decentralises

Hospitals accounted for 53.25% of 2025 purchases owing to their central role in treating complex immune and bleeding disorders. Large public tertiary centres in metros still consume the bulk of high-dose IVIG courses required for paediatric immunodeficiency patients. However, specialty clinics—particularly stand-alone immunology and haemophilia centres set up in tier-2 cities—log the highest 7.78% CAGR. Investors back these focused facilities for their operational efficiency and closer patient engagement models.

Academic and research institutes purchase plasma proteins for clinical trials evaluating dosing algorithms and pandemic-preparedness stockpiles. Home-care providers, while nascent, increasingly administer subcutaneous immunoglobulin under nursing supervision, lightening hospital load and improving patient convenience. The embedding of plasma-collection suites within specialty clinics enables vertical integration, allowing centres to source local donor plasma and administer derived therapies on the same premises. This combined service model tightens supply-demand synchrony and demonstrates innovative delivery pathways inside the India plasma fractionation market.

Geography Analysis

Metropolitan corridors remain the consumption core for the India plasma fractionation market, with Mumbai, Delhi and Chennai collectively accounting for nearly half of national immunoglobulin throughput. Mumbai’s cluster benefits from proximity to port infrastructure, easing export logistics for fractionators eager to serve neighbouring South-Asian markets. Delhi’s AIIMS campus operates India’s busiest immunology clinic, anchoring demand for high-dose IVIG regimens. Chennai’s large burn-care hospital network sustains robust albumin offtake, while the city’s mega blood bank supplies surplus plasma to southern processors.

Tier-2 cities—Lucknow, Nagpur, Coimbatore and Jaipur—are emerging as secondary demand hubs. Government-funded AIIMS branches, combined with Ayushman Bharat insurance coverage, expand access to advanced therapies. Hospital-based plasma collection centres in these cities narrow the distance between donor and processor, lowering spoilage and logistics cost. State public-private partnerships are piloting mobile apheresis vans to reach rural donors, aiming to lift voluntary donation ratios from 17% to 40% by 2028.

Manufacturing capacity clusters around Gujarat’s bulk-drug park, Maharashtra’s biologics corridor and Andhra Pradesh’s Visakhapatnam biotech zone. These parks provide shared effluent treatment, solvent recovery and cold-storage warehouses, reducing capex for new entrants and encouraging technology transfer tie-ups with European skid builders. Foreign direct investment worth USD 1.5 billion flowed into healthcare logistics in 2024, earmarked for multi-modal warehousing that supports plasma transport along the Delhi–Mumbai Industrial Corridor. Implementation of the National Logistics Policy, which targets logistics cost parity with global benchmarks by 2030, will further smooth inter-state movement and enlarge the effective catchment for fractionators. Collectively these geographic dynamics underpin a broadening footprint and help the India plasma fractionation market achieve nationwide reach.

Competitive Landscape

The India plasma fractionation market presents moderate concentration. Global stalwarts CSL Behring, Takeda and Kedrion leverage proprietary viral-clearance and chromatography platforms to supply premium immunoglobulin brands, often priced at a 10-15% premium over domestic alternatives. CSL Behring’s deployment of the Rika plasma-collection system, which yields 10% more plasma per donor, feeds into its regional purification line in Chennai, reinforcing scale advantage.

Domestic firms Reliance Life Sciences, Bharat Serums & Vaccines and PlasmaGen BioSciences compete on local market knowledge and lower labour cost. Mankind Pharma’s 2025 acquisition of Bharat Serums for INR 13,768 crore consolidates women’s-health biologics with plasma-derived lines and enhances distribution reach to 1,000-plus wholesalers nationwide. Reliance Life Sciences invests in depth-filtration and single-use chromatography modules that raise albumin yield, while PlasmaGen channels private-equity capital into a greenfield hyper-immune fraction plant in Bengaluru.

Entry barriers include hefty GMP validation cost, a two-year timeline for CDSCO marketing authorisation and tight cold-chain prerequisites. However, niche opportunities persist in contract fractionation services for neighbouring South-Asian countries lacking local capacity. Smaller Indian firms aim at specialised fractions—anti-D, VWF concentrate—where global majors pay limited attention. Intellectual-property constraints are modest because fractionation know-how rests more on tacit process expertise than patented inventions, allowing fast learning curves for motivated domestic entrants.

India Plasma Fractionation Industry Leaders

PlasmaGen BioSciences Pvt. Ltd.

Reliance Industries Limited (Reliance Life Sciences)

Intas Pharmaceuticals Ltd

Taj Pharmaceuticals Limited

Virchow Biotech Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Government launched the BIO-E3 biotechnology policy targeting a USD 300 billion sector by 2030, with precision-biotherapeutic incentives covering plasma products

- March 2024: The Government inaugurated 27 greenfield bulk-drug park projects and 13 medical-device plants under the pharmaceutical PLI scheme.

India Plasma Fractionation Market Report Scope

As per the scope of the report, plasma fractionation is defined as the general process of separating the various components of blood plasma obtained via blood fractionation. Plasma contains multiple proteins, including immunoglobulins, albumin, and coagulation proteins.

The Indian plasma fractionation market is segmented by product, application, and end user. By product, the market is segmented into immunoglobulins, platelets and coagulation factor concentrates, albumin, and other products. By application, the market is segmented into neurology, immunology, hematology, and other applications. By end user, the market is segmented into hospitals and clinics, clinical research laboratories, and other end users. The other end users include academia and research institutes. The report offers market size and forecasts in value (USD) for the above segments.

| Immunoglobulins |

| Albumin |

| Coagulation Factors (FVIII, FIX, FVII, etc.) |

| Hyper-immune & Other Fractions |

| Immunology |

| Hematology |

| Neurology |

| Critical Care & Trauma |

| Others |

| Hospitals |

| Specialty Clinics |

| Academic & Research Institutes |

| Others |

| Cohn–Oncley Fractionation |

| Chromatography-based Fractionation |

| Hybrid & Continuous Processes |

| Emerging Single-use Technologies |

| by Product (Value) | Immunoglobulins |

| Albumin | |

| Coagulation Factors (FVIII, FIX, FVII, etc.) | |

| Hyper-immune & Other Fractions | |

| By Application (Value) | Immunology |

| Hematology | |

| Neurology | |

| Critical Care & Trauma | |

| Others | |

| By End User (Value) | Hospitals |

| Specialty Clinics | |

| Academic & Research Institutes | |

| Others | |

| By Technology (Value) | Cohn–Oncley Fractionation |

| Chromatography-based Fractionation | |

| Hybrid & Continuous Processes | |

| Emerging Single-use Technologies |

Key Questions Answered in the Report

How big is the India Plasma Fractionation Market?

The India Plasma Fractionation Market size is expected to reach USD 1.88 billion in 2026 and grow at a CAGR of 6.31% to reach USD 2.56 billion by 2031.

What is the current India Plasma Fractionation Market size?

In 2026, the India Plasma Fractionation Market size is expected to reach USD 1.88 billion.

Who are the key players in India Plasma Fractionation Market?

PlasmaGen BioSciences Pvt. Ltd., Reliance Industries Limited (Reliance Life Sciences), Intas Pharmaceuticals Ltd, Taj Pharmaceuticals Limited and Virchow Biotech Private Limited are the major companies operating in the India Plasma Fractionation Market.

What years does this India Plasma Fractionation Market cover, and what was the market size in 2025?

In 2025, the India Plasma Fractionation Market size was estimated at USD 1.88 billion. The report covers the India Plasma Fractionation Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India Plasma Fractionation Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: