Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

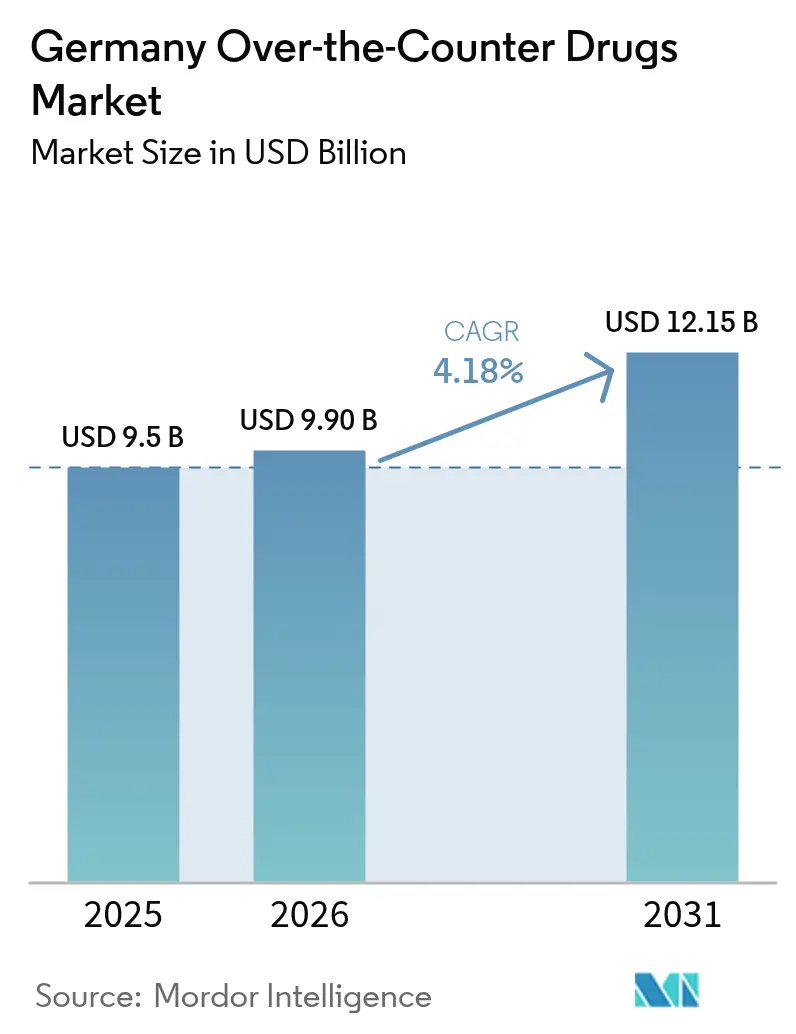

| Base Year Market Size (2025) | USD 9.50 Billion |

| Market Size (2026) | USD 9.9 Billion |

| Market Size (2031) | USD 12.15 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

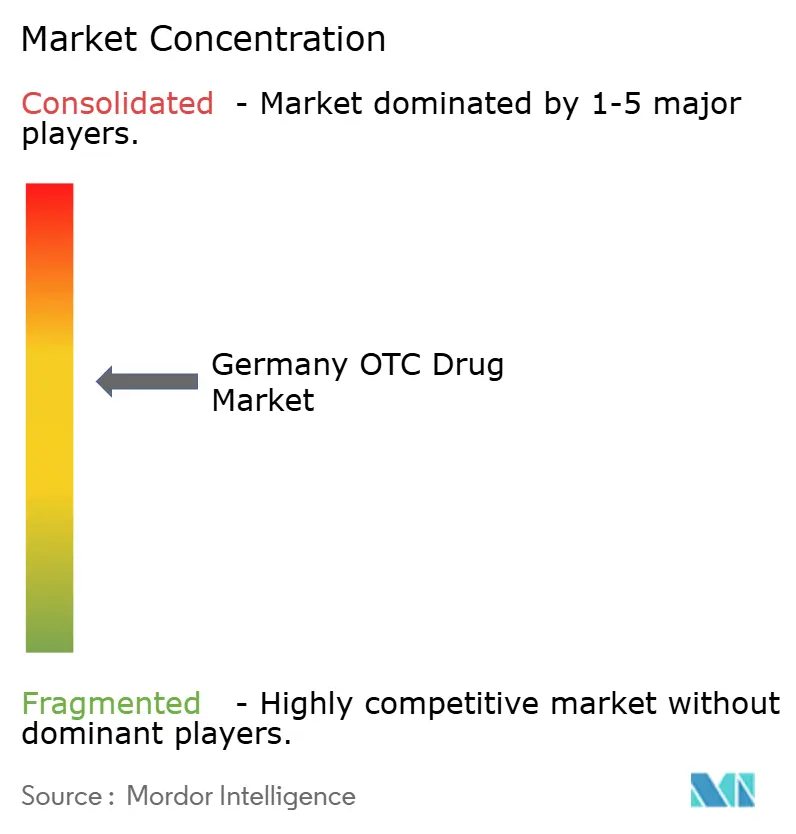

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Over-the-Counter Drugs Market Analysis by Mordor Intelligence

The Germany OTC drug market size was valued at USD 9.50 billion in 2025 and estimated to grow from USD 9.90 billion in 2026 to reach USD 12.15 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031). Digitalization is the headline catalyst: mandatory e-prescriptions introduced in 2024 accelerated online fulfilment, fortified omnichannel retail models, and created new data streams that sharpen product targeting. Alongside this shift, a rapidly ageing population, with 17.3 million citizens 65 years or older, keeps chronic-care self-medication demand high.[1]Bundesministerium für Gesundheit, “E-Rezept: Elektronische Rezepte flächendeckend seit 2024,” bundesgesundheitsministerium.deStreamlined BfArM approval pathways for Rx-to-OTC switches lower time-to-market for well-established actives, while post-pandemic health literacy lifts preventive consumption from episodic use to everyday habit. Manufacturers benefit from the 2025 Medical Research Act, which introduces confidential reimbursement agreements that reward German-based R&D and cushion price pressures. However, 466 listed product shortages, EU serialization costs, and the lowest pharmacy count in four decades add operating friction and threaten rural access.[2]Bundesinstitut für Arzneimittel und Medizinprodukte, “Beschleunigte Zulassung traditioneller Arzneimittel,” bfarm.de

Key Report Takeaways

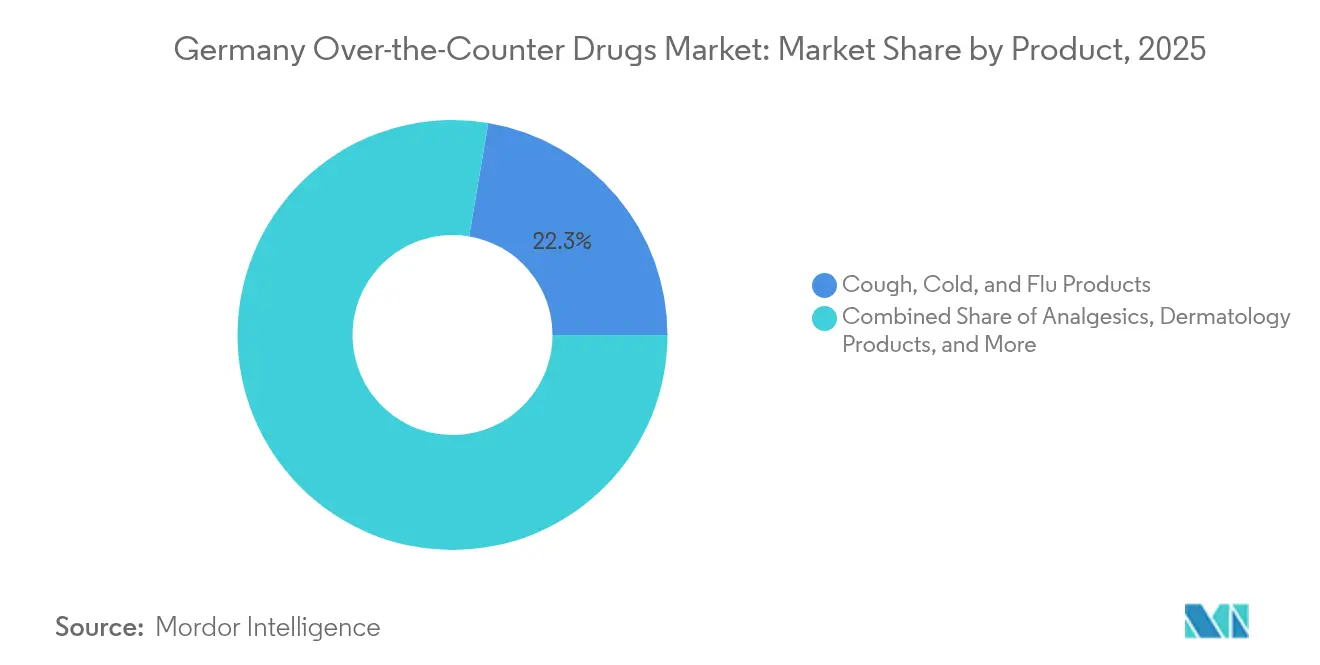

- By product category, Cough, Cold & Flu led with 22.34% revenue share in 2025; Weight-loss/Dietary Products are projected to expand at an 8.78% CAGR to 2031.

- By distribution channel, Retail Pharmacies held 77.40% of the Germany OTC drug market share in 2025, while Online Pharmacies record the fastest growth at 12.40% CAGR through 2031.

- By route of administration, Oral delivery captured 70.10% share of the Germany OTC drug market size in 2025, whereas Nasal delivery is set to grow at 7.08% CAGR between 2026-2031.

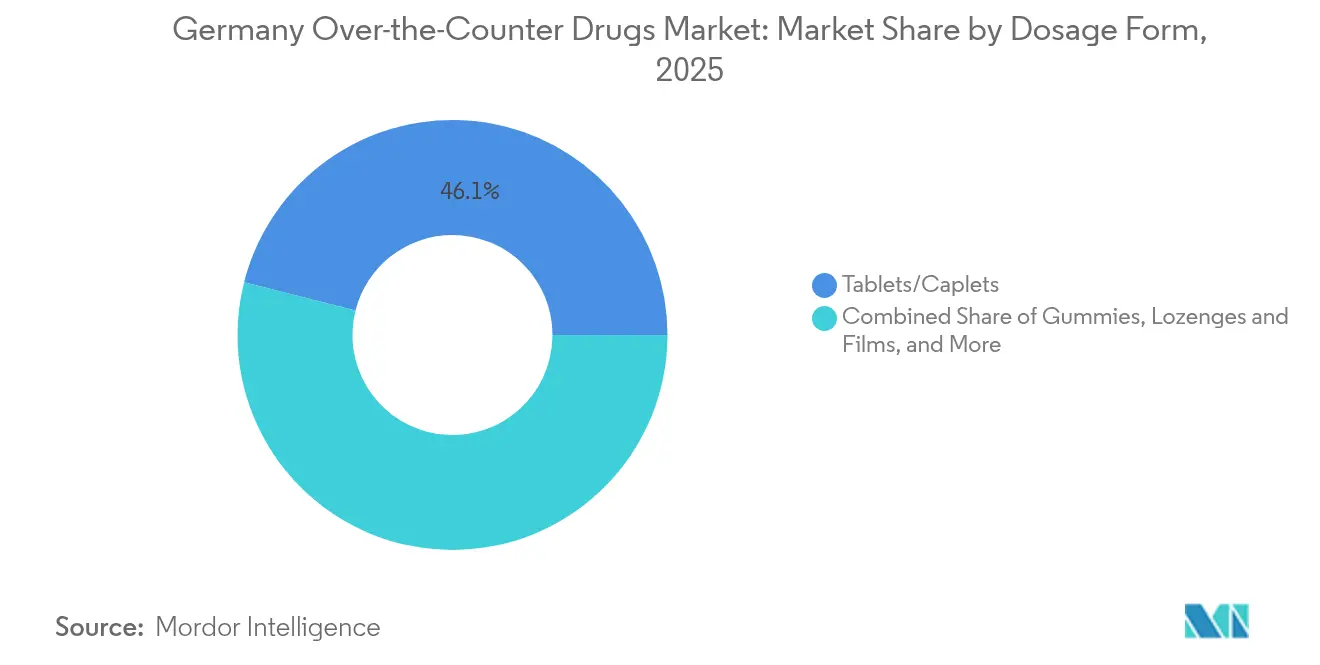

- By dosage form, Tablets & Caplets accounted for 46.05% share of the Germany OTC drug market size in 2025; Liquids & Syrups are forecast to rise at 8.28% CAGR.

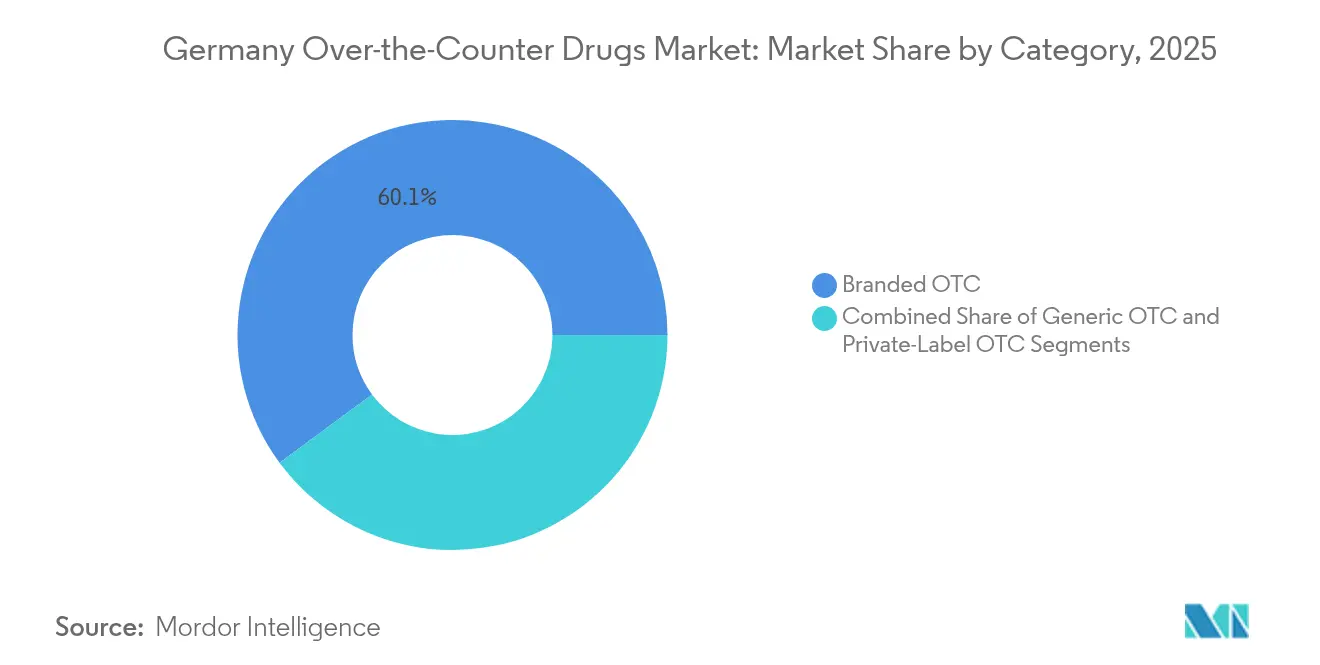

- By category, Branded products commanded 60.12% share in 2025, while Private-label options advance at 7.98% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Over-the-Counter Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing Rx-to-OTC switch acceleration | +0.8% | National; harmonised across EU | Medium term (2-4 years) |

| Rising self-medication & health-literacy levels | +1.2% | National; higher in metropolitan areas | Long term (≥ 4 years) |

| Ageing population driving chronic-care demand | +0.9% | National; pronounced in rural and eastern regions | Long term (≥ 4 years) |

| Favourable EU procedures for well-established actives | +0.5% | EU-wide; Germany primary beneficiary | Medium term (2-4 years) |

| Expansion of e-pharmacies & e-prescriptions | +0.7% | National; early adoption in tech-forward cities | Short term (≤ 2 years) |

| Surge in demand for natural/herbal alternatives | +0.6% | National; Baden-Württemberg leads production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ongoing Rx-to-OTC Switch Acceleration

BfArM’s streamlined protocols now recognise 15 years of safe EU use for traditional herbal medicines instead of the historic 30, cutting approval times nearly in half. The 2025 Medical Research Act supplements this by allowing confidential price negotiations when manufacturers conduct material R&D in Germany, preserving margins even after a switch. Sanofi’s Opella division mirrors industry appetite by gaining FDA clearance for OTC Cialis trials, underscoring global confidence in German regulatory precedents. Wider OTC availability then seeds real-world evidence that supports subsequent switches, reinforcing Germany’s reputation as Europe’s switch test-bed. The virtuous cycle accelerates revenue diversification and expands therapeutic choice for consumers across the Germany OTC drug market.

Rising Self-Medication & Health-Literacy Levels

Electronic patient records became opt-out in January 2025, giving citizens uniform digital access to diagnoses, labs, and prescription data. Visibility of health data fuels informed OTC decisions and has lifted self-medication prevalence to 40.2% of adults. Academic surveys show 47.2% of women and 33.2% of men use OTCs primarily for prevention rather than acute relief. The behavioral shift translates into EUR 21 billion (USD 24 billion) in annual system savings, highlighting policy interest in OTC expansion. Low preventive-care spending, just 3% of the healthcare budget, creates headroom for growth as insurers and employers sponsor self-care programs to curb future chronic-care costs.

Ageing Population Driving Chronic-Care OTC Demand

One in four older Germans practices polypharmacy, blending 3.7 prescription drugs with 1.4 OTCs daily. OTC analgesics achieve 77.2% pain-relief success within 12 weeks among seniors, validating non-prescription pathways. As Germany needs 1.9 million nurses by 2040, OTC modalities ease pressure on professionals and enable home-based management of hypertension, diabetes, and mild cardiovascular conditions. Manufacturers position chronic-care supplements as essential infrastructure, ensuring continuity of care in both urban and underserved rural zones.

Favorable EU Procedures for Well-Established Actives

EMA’s well-established use route now requires only bibliographic safety data for molecules with a 10-year EU track record, slashing dossier complexity. German firms leverage this to expedite launches of herbal expectorants and topical anti-inflammatories that already have robust European safety records. The alignment harmonizes labelling across markets, lowers duplication costs, and lets companies scale evidence-based OTC portfolios in Germany before expanding regionally.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generic Price Erosion from Tender-Based Procurement | -0.70% | Global, particularly pronounced in emerging markets and public healthcare systems | Short term (≤ 2 years) |

| Global Antibiotic Stewardship Restrictions on Broad Use | -0.50% | North America & EU leading, expanding globally through WHO initiatives | Medium term (2-4 years) |

| Poor ROI Despite Pull Incentives Deterring R&D | -0.40% | Global pharmaceutical industry, concentrated in developed markets with high R&D costs | Long term (≥ 4 years) |

| Emerging Non-Antibiotic Modalities (Phage, CRISPR) | -0.30% | North America & EU early adoption, expanding to Asia-Pacific research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Risk of Misdiagnosis and OTC Abuse

After safety concerns linked to Iberogast’s Schöllkraut component, Bayer reformulated the product and added mandatory warnings, signaling stricter post-marketing vigilance. Television audits found common breaches of mandatory risk disclosures, prompting new enforcement guidance and higher fines. PPI sales—2.87 billion tablets sold in a 12-month window—exposed off-label use, leading to guidelines capping therapy at 8 weeks for mild reflux. Collectively, tighter pharmacovigilance and advertising rules raise compliance costs and slow first-to-market strategies inside the Germany OTC drug market.

Stringent Price/Advertising Controls in Germany

The Heilmittelwerbegesetz and Arzneimittelgesetz ban comparative consumer adverts and dictate mandatory wording, limiting creative latitude. Fixed wholesale and pharmacy margins, plus statutory health-insurer discounts, compress OTC profitability. Civil actions and self-regulatory bodies enforce the rules, creating legal uncertainty for aggressive campaigns. Confidential reimbursement agreements under the 2025 Medical Research Act should provide some relief, but only for firms that commit to German-based R&D, raising capital intensity for pipeline development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products: Weight-Loss Surge Challenges Traditional Categories

Cough, Cold & Flu remedies retained a 22.34% slice of the German OTC drug market size in 2025, yet growth is tapering as milder post-pandemic winters shrink symptom incidence. Weight-loss/Dietary Products headline segment momentum with an 8.78% CAGR through 2031, powered by nutraceutical demand representing 4.1% of global supplement sales. Analgesics sustain relevance via caffeine-enhanced ibuprofen that delivers 50% pain reduction within 2 hours for 90% of study participants. Vitamins, Minerals, and Supplements capitalize on immunity awareness, while dermatology lines benefit from the ageing cohort’s skin-health focus. Ophthalmic and sleep-aid niches grow steadily as screen time and stress heighten eye strain and insomnia.

Diverse performance shows how German consumers shift from reactive symptom relief to preventive wellness. Scientific proof points underpin purchasing; herbal adaptogens and sports-nutrition blends succeed only when clinical dossiers substantiate claims. Manufacturers employ staged lifecycles: they start with clinical-grade branded launches and extend into value-priced generics once awareness is built. This approach protects margins while expanding access across income tiers in the German OTC drug market.

By Distribution Channel: Digital Disruption Reshapes Pharmacy Landscape

Retail Pharmacies safeguarded a 77.40% share in 2025, underpinned by counselling services and insurance reimbursement for select OTCs. Pharmacy numbers, however, dipped below 18,000, the weakest count in 40 years, exposing rural gaps. Online Pharmacies are compounding at 12.40% and are set to narrow the channel disparity as e-prescription ease encourages basket bundling. Hospital Pharmacies remain niche, mainly supplying inpatient needs, while Convenience/Grocery outlets capture impulse buys but face legal limits on SKU breadth.

The Germany OTC drug market therefore orbits an omnichannel core. Click-and-collect keeps local chemists relevant, while pure-play e-pharmacies harness AI chatbots for triage and cross-sell. Regulatory debates around cross-border e-scripts could widen competition if neighboring EU sites secure German fulfilment rights, although technical interoperability hurdles persist.

By Dosage Form: Innovation Drives Format Evolution

Tablets & Caplets dominate with 46.05% of the German OTC drug market share in 2025 due to cost-efficient production and dosing familiarity. Liquids & Syrups, the fastest-growing format at 8.28% CAGR, resonate with pediatric and geriatric groups who prefer swallow-free options. Gummies & Chewables attract compliance-challenged users through flavor masking, while Sprays & Drops leverage targeted delivery, such as xylometazoline nasal sprays that achieve over 90% user satisfaction.

Patient-centric design is now a differentiator. Formulators invest in taste, texture, and on-the-go packs to align with busy lifestyles. Innovation must still traverse strict German stability and purity tests, which can slow entry for smaller firms but preserve consumer trust in a competitive Germany OTC drug market.

By Route of Administration: Targeted Delivery Gains Momentum

Oral routes continued to command 70.10% of the German OTC drug market size in 2025, yet Nasal delivery posts the fastest expansion at 7.08% CAGR thanks to rapid-onset decongestants and allergy sprays. Topical formats occupy chronic pain and dermatology spaces; clinical data show diclofenac gel brings significant relief to 77.2% of users within 12 weeks. Rectal/Vaginal routes remain specialized but stable, serving hemorrhoid and women’s health indications.

Demand patterns underscore consumer appetite for quick, localized action. Device innovation—metered nasal pumps, airless topical tubes—improves dosing precision and product shelf-life. These advances sustain price premiums and deter commoditization in the German OTC drug market.

By Category: Private-Label Momentum Challenges Brand Dominance

Branded products still control 60.12% share, yet private-label lines are outpacing at 7.98% CAGR as retailers leverage data to target value-conscious segments. STADA’s EUR 3.73 billion (USD 4.31 billion) consumer-health sales prove that dual-track strategies, premium science brands alongside economical generics, can thrive. Brand switching is fluid; transparent ingredient lists and comparable clinical claims narrow perceived quality gaps. Contract manufacturing alliances allow multinationals to supply retailer brands, capturing volume while defending flagship SKUs.

Private-label success pushes branded players to refresh packaging, expand digital education, and secure patent-backed formulation tweaks. Competitive tension, therefore, raises both innovation tempo and consumer value across the German OTC drug market.

Geography Analysis

Germany anchors the EU’s largest OTC consumption base and is a pivotal phytopharmaceutical manufacturing hub. Baden-Württemberg hosts a dense cluster of herbal-medicine specialists that export clinically validated products worldwide, reinforcing regional specialization and high-skill employment. Eastern regions, however, confront care-access headwinds as pharmacy density thins, prompting public concern over medication counselling and compliance. Online channels partly offset the gap, but bandwidth limitations and older demographics slow digital uptake.

Urban centers such as Munich and Berlin display higher per-capita OTC spending, influenced by education levels and disposable income. Pricing studies in large cities reveal that wealthier districts pay up to 15% more for identical OTC SKUs, reflecting brand orientation and convenience premiums. Federal e-health infrastructure aims to reduce such disparities by standardizing data access and enabling universal e-prescription redemption. Yet, state-level policy differences and reimbursement rules still shape local dynamics.

Germany’s central European location supports export logistics, with manufacturers shipping herbal extracts and finished OTC products to neighboring markets within 48 hours. Cross-border trade is poised to expand once the European Health Data Space enables e-prescription interoperability, although cybersecurity and data-sovereignty issues remain unresolved. Incentives under the Medical Research Act encourage regional governments to court pharma investments, reinforcing Germany’s status as a resilient, innovation-driven OTC stronghold.

Competitive Landscape

Competitive intensity is moderate: multinationals, regional specialists, and digital platforms vie for share without any single player eclipsing the field. Bayer is reorganizing its consumer health unit to accelerate switch candidates and gut-health lines, while Sanofi moves ahead with a EUR 20 billion consumer spin-off to unlock capital efficiency.

Digital disruption reshapes engagement more than molecular innovations. DocMorris and Shop Apotheke deploy telemedicine services, loyalty subscription models, and AI-driven adherence reminders that deepen customer lock-in. Smaller firms find niches in herbal remedies and dosage-form novelties, partnering with contract manufacturers to achieve GMP compliance without heavy capex. EU serialization rules erect cost barriers that favor scale; Germany’s national verification system already coordinates data from roughly 100 drug makers.

White-space opportunities lie in evidence-backed natural alternatives, precision-dosage platforms, and OTC devices that integrate with wearables. Strategic alliances and private-equity backing such as Oakley Capital’s stake in WindStar Medical—illustrate how capital pools into scalable consumer-health platforms. As competition pivots from single SKU success to ecosystem engagement, the German OTC drug market rewards agility, regulatory fluency, and data-driven service innovation.

Germany Over-the-Counter Drugs Industry Leaders

Bayer AG

Sanofi SA

Reckitt Benckiser Group PLC

Haleon Group of Companies

Kenvue Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sanofi steps up preparations to spin off its EUR 20 billion (USD 23 billion) consumer-health division into a standalone OTC company.

- October 2024: Merz Group merges WindStar Medical with Merz Lifecare through a joint holding structure, aiming to strengthen the DACH-region OTC reach.

- June 2024: Gehe AG acquires wholesaler Dr Krey & Vigener GmbH, consolidating regional distribution capacity.

- June 2024: Austria’s competition authority clears a 33.3% Croma-Pharma stake sale to ARGUS Vermögensverwaltung, signalling cross-border interest in aesthetic OTC niches.

- January 2024: Opella secures FDA approval to begin OTC Cialis trials, marking the first PDE-5 inhibitor on an OTC pathway.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Germany's over-the-counter drug market as the yearly value, in US dollars, of non-prescription medicines listed in the BfArM register and dispensed through retail, hospital, or licensed online pharmacies.

Scope exclusion: prescription medicines, unlicensed homeopathic remedies, and medical devices sit outside this boundary.

Segmentation Overview

- By Product Type

- Cough, Cold & Flu Products

- Analgesics

- Dermatology Products

- Gastrointestinal Products

- Vitamins, Minerals & Supplements (VMS)

- Weight-loss / Dietary Products

- Ophthalmic Products

- Sleeping Aids

- Other Product Types

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Convenience / Grocery Stores

- By Dosage Form

- Tablets & Caplets

- Liquids & Syrups

- Gummies & Chewables

- Sprays & Drops

- Topicals & Ointments

- By Route of Administration

- Oral

- Topical

- Nasal

- Ophthalmic

- Rectal / Vaginal

- By Category

- Branded OTC

- Private-label / Store Brands

- Generic OTC

Detailed Research Methodology and Data Validation

Primary Research

We spoke with community pharmacists, online-pharmacy managers, regulatory advisers, and category buyers in Berlin, Munich, Cologne, and rural Saxony. Their views on pack prices, e-prescription uptake, and recent Rx-to-OTC switches enriched and stress-tested desk findings.

Desk Research

Mordor analysts first mapped every OTC SKU in the BfArM Arzneimittel-Informationssystem, then matched those codes with sell-out audits from the German Drug Manufacturers Association. Destatis trade tables, OECD Health Statistics, WHO spending data, and Federal Health Ministry white papers anchored demand and price trends. Company filings, respected press, and D&B Hoovers revenue splits filled channel and margin gaps. These examples illustrate, not exhaust, the sources consulted.

Market-Sizing & Forecasting

A top-down reconstruction blends pharmacy unit sales, import-export values, and penetration-rate demand pools for cough-cold, analgesics, VMS, gastrointestinal, dermatology, and sleep aids. Selective bottom-up checks, average selling price multiplied by sampled volume, align totals. Key variables, including population aged 65+, e-Rx counts, switch approvals, real wages, and online share, feed a multivariate regression that extends figures to 2030. Comparable category margins bridge gaps before final calibration.

Data Validation & Update Cycle

Analysts run variance checks, peer reviews, and anomaly flags, then reconnect with experts if swings persist. The model refreshes every year, with interim updates for major policy or currency shifts, and a pre-publication pass delivers the latest view.

Why Mordor's Germany OTC Drug Baseline Commands Reliability

Published estimates diverge: some include botanicals or vitamin drinks, others lift prices without currency adjustments, and a few ignore online sales.

By limiting scope to BfArM-licensed medicines, indexing prices to pharmacy tills, and revisiting assumptions each year, Mordor Intelligence supplies the balanced benchmark decision-makers trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.5 B (2025) | Mordor Intelligence | - |

| USD 9.8 B (2024) | Regional Consultancy A | Includes botanicals and drinks |

| USD 10.4 B (2024) | Trade Journal B | Uses constant price rise, no FX check |

| USD 7.8 B (2024) | Global Consultancy C | Excludes online sales and switch items |

Taken together, the comparison confirms that Mordor's disciplined scope, clear variables, and yearly refresh yield the most dependable baseline for growth planning.

Key Questions Answered in the Report

What is the current value of the Germany OTC drug market?

The market stands at USD 9.90 billion in 2026 and is projected to hit USD 12.15 billion by 2031.

Which product category is growing the fastest?

Weight-loss and dietary OTC products lead growth with an 8.78% CAGR forecast for 2026-2031.

How has the e-prescription mandate affected distribution?

Mandatory e-prescriptions processed 730 million transactions by April 2025, propelling online pharmacy growth at 12.40% CAGR.

Why are Rx-to-OTC switches important in Germany?

Streamlined BfArM procedures and the 2025 Medical Research Act shorten approval timelines and sustain price realisation for switched products.

What is the main restraint on OTC market expansion?

Stringent German advertising and price-control laws restrict promotional flexibility and compress margins.

Page last updated on: