Germany Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

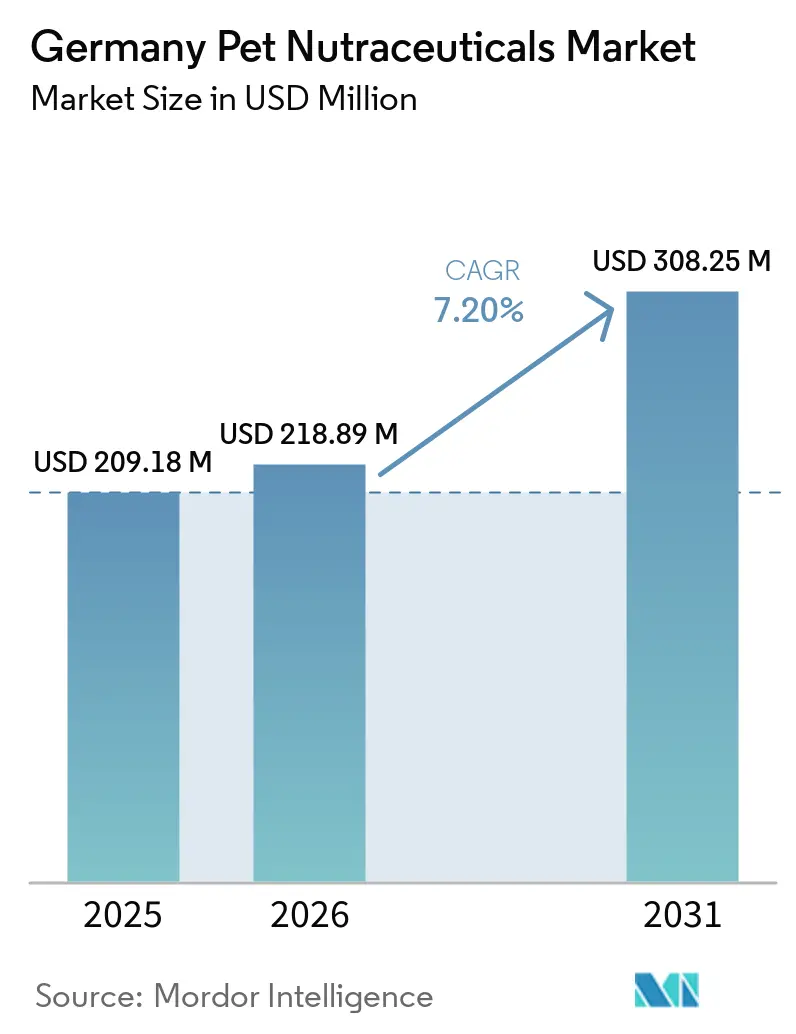

| Base Year Market Size (2025) | USD 209.18 Million |

| Market Size (2026) | USD 218.89 Million |

| Market Size (2031) | USD 308.25 Million |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

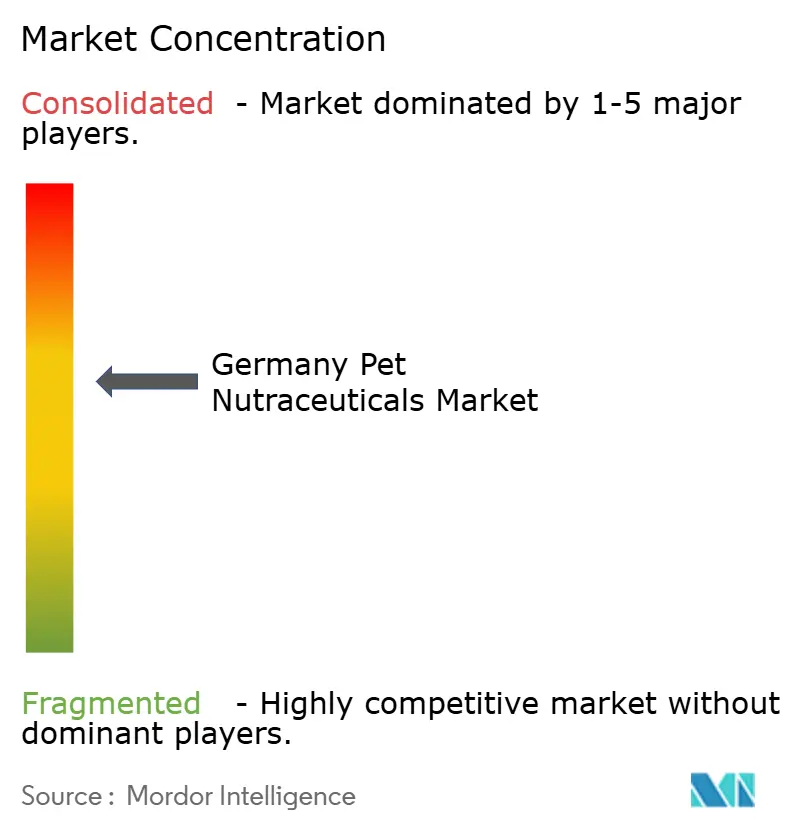

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Pet Nutraceuticals Market Analysis by Mordor Intelligence

The Germany pet nutraceuticals market size is projected to increase from USD 209.18 million in 2025 to USD 218.89 million in 2026 and reach USD 308.25 million by 2031, growing at a CAGR of 7.2% over 2026-2031. As per Industrieverband Heimtierbedarf (IVH) data, The Germany pet nutraceuticals market is expanding from a stable base of companion animal ownership, with 33.4 million pets recorded in Germany in 2025 and pets present in 43% of households, which keeps demand broad even when discretionary categories soften[1]Source: Industrieverband Heimtierbedarf and Zentralverband der Heimtierbranche, “The German Pet Market 2025, Structure and Sales Data,” zzf.de. This pattern is reinforced by the fact that Germany’s broader pet accessories segment declined by 4.6% in 2025, while functional pet health products continued to hold buyer attention, showing that owners are treating preventive nutrition as a more necessary spend than many nonessential pet items. Veterinary acceptance is also becoming more important in the Germany pet nutraceuticals market because buyers increasingly look for products linked to digestive health, mobility, skin condition, and behavior support that carry a clearer health rationale. At the same time, the category is moving into a more disciplined phase as regulatory compliance, ingredient quality, and traceable supply become more central to brand selection and channel access.

Key Report Takeaways

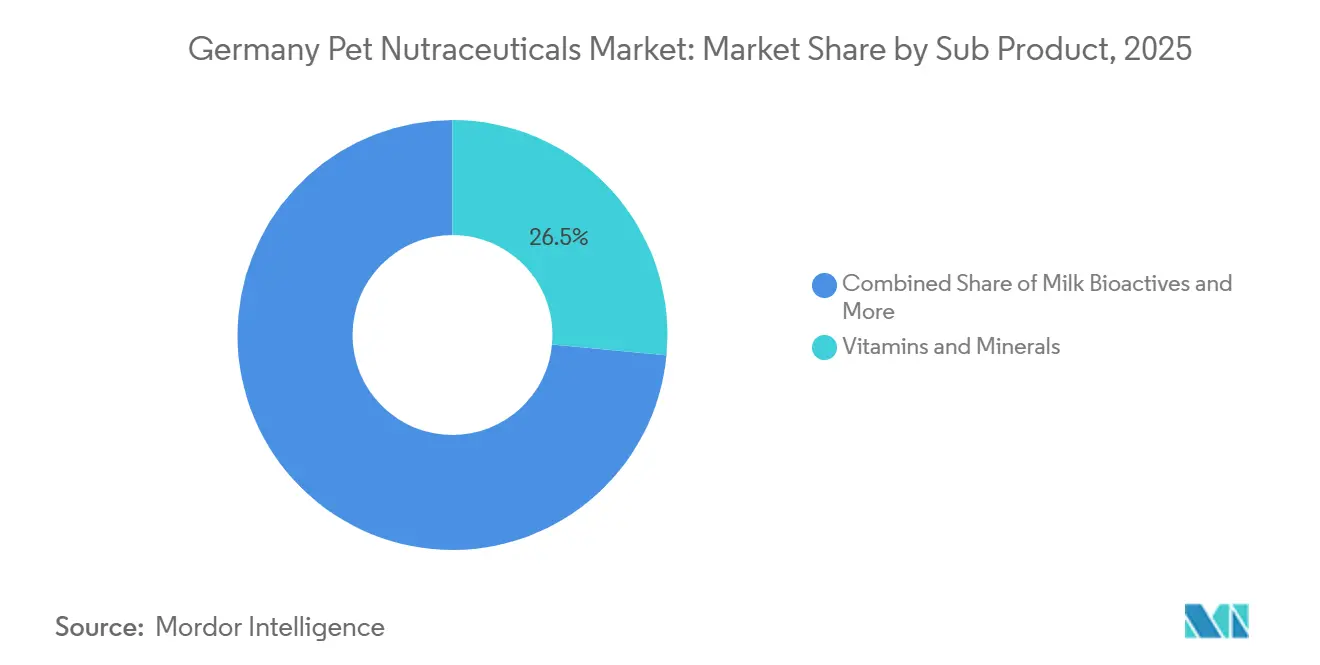

- By sub product, vitamins and minerals led with 26.5% of the Germany pet nutraceuticals market share in 2025, and this segment is also projected to record the fastest 7.7% CAGR through 2026 to 2031.

- By pet type, dogs held the largest 51.1% share in 2025, and are set to expand at the fastest projected CAGR of 7.5% through 2026 to 2031.

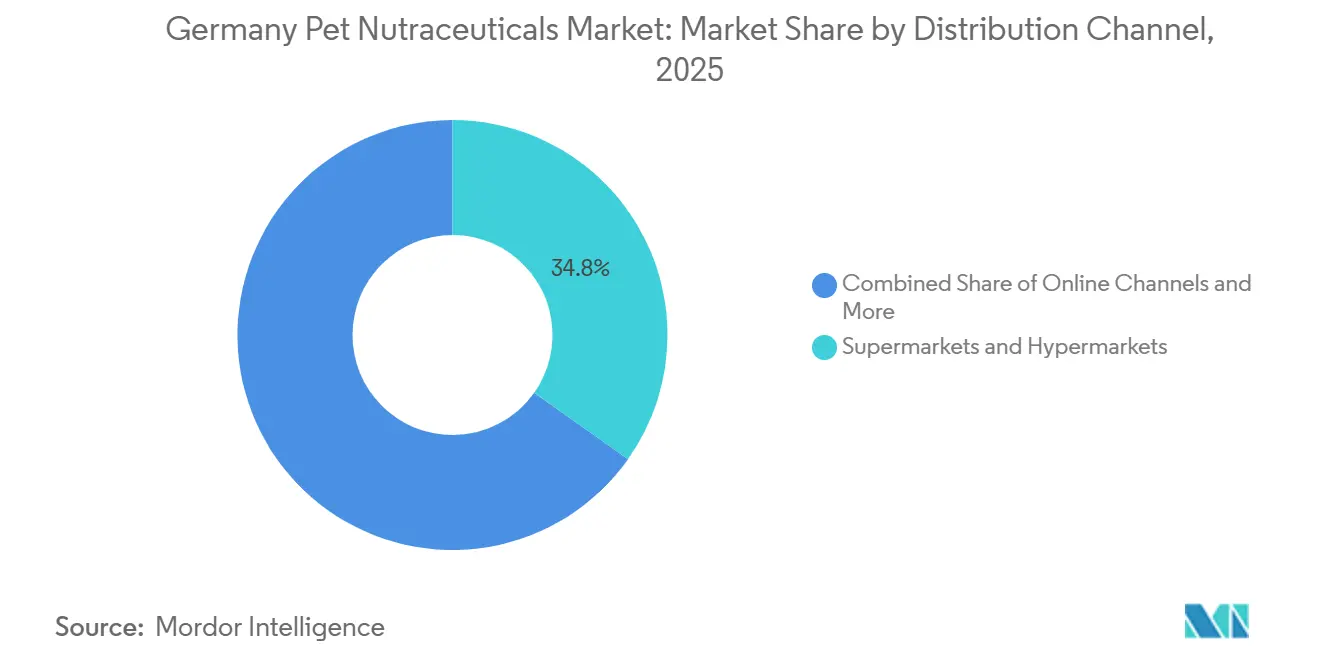

- By distribution channel, supermarkets and hypermarkets accounted for 34.8% of the Germany pet nutraceuticals market size in 2025, while the online channel is forecast to grow at the fastest 7.8% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization and preventive wellness spending | +1.9% | National, with strongest uptake in Munich, Hamburg, and Berlin | Short term (≤ 2 years) |

| Rising veterinary endorsement of condition-specific supplements | +1.5% | National, disproportionately in Bavaria and North Rhine-Westphalia veterinary networks | Medium term (2-4 years) |

| Premiumization of dog and cat care routines | +1.2% | National, with early concentration in major metropolitan areas | Medium term (2-4 years) |

| E-commerce reorder behavior and subscription purchases | +1.0% | National, highest penetration in Hamburg, Berlin, and Munich | Short term (≤ 2 years) |

| Multipet household cross-selling of health products | +0.5% | National, concentrated in 3-or-more-person households | Medium term (2-4 years) |

| Evidence-based formulations for mobility, digestive, and skin health | +0.7% | Global sourcing with primary commercial implementation in Germany and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization and Preventive Wellness Spending

The Germany pet nutraceuticals market is benefiting from a steady shift in owner behavior toward preventive care rather than waiting for visible illness. According to the reports of Industrieverband Heimtierbedarf and Zentralverband der Heimtierbranche, in 2025, 43% of German households owned at least one pet, and 67% of families with children kept a pet, indicating a large, emotionally engaged base for daily wellness products. The same dataset also showed that 13% of households kept at least 2 different pet types, supporting repeat buying across multiple animals within the same home. That broad ownership pattern matters because preventive products are most likely to scale when demand does not depend on a narrow disease event or a single clinical trigger. It also explains why mainstream categories such as vitamins, digestive support, and coat health are holding attention in the Germany pet nutraceuticals market even when other pet-related purchases become more selective. As owners make pet care decisions more like family wellness planning, products with simple daily use and clear purpose are gaining the strongest traction.

Rising Veterinary Endorsement of Condition-Specific Supplements

Veterinary support is becoming a stronger commercial filter in the Germany pet nutraceuticals market, especially for products tied to mobility, skin condition, and gastrointestinal balance. Omega-3 fatty acids from fish oil have one of the strongest evidence bases for orthopedic support in dogs, providing practitioners with a clearer reference point when discussing supplement use with owners. This matters in Germany because products that enter the veterinary channel with a defined use case often move more smoothly into specialty retail and premium online listings afterward. The pattern favors companies that can support claims with clinical logic, dosing clarity, and traceable ingredient systems rather than broad wellness language alone. It also raises the bar for smaller entrants, since veterinarian-backed products are more likely to build trust across the Germany pet nutraceuticals market than generic formulations that look interchangeable on the shelf. Over time, this strengthens brands that invest early in practitioner relationships and scientific communication.

Premiumization of Dog and Cat Care Routines

Premiumization is reshaping the Germany pet nutraceuticals market because owners are moving from basic multibenefit formulas toward more targeted products with clearer use cases. The category is no longer defined only by broad nutritional support, as more brands are focusing on digestive support, joint care, behavioral balance, and skin or coat function through specific formats and ingredients. This shift aligns with the wider move in companion animal care toward products that resemble structured wellness routines rather than occasional add-ons. It also rewards manufacturers with stronger formulation capability, especially in delivery systems that protect sensitive actives such as probiotics and omega-3 ingredients during production and storage. In practical terms, premiumization is making the Germany pet nutraceuticals market less about shelf abundance and more about evidence, palatability, and repeat adherence. That creates more room for companies that can defend pricing through quality and clinical relevance, while limiting the appeal of lower-grade formulations with weaker differentiation.

E-Commerce Reorder Behavior and Subscription Purchases

The Germany pet nutraceuticals market is also gaining support from digital reorder behavior, because supplements that are used daily fit naturally into subscription and replenishment models. Once a product becomes part of a feeding or care routine, online repeat purchase reduces the need for a new buying decision each month and helps brands stabilize demand. This is especially relevant for vitamins, digestive products, and condition-specific supplements that owners intend to use over long periods. Online growth also helps premium products reach households that may not find the same depth of assortment in physical grocery retail. As a result, digital channels do more than widen reach in the Germany pet nutraceuticals market, they also improve continuity of use and reduce the drop-off that can happen when owners have to search again in store. The strongest benefit goes to brands that combine clear product education, easy reordering, and a format that fits regular administration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and claims compliance burden | -1.0% | National, with European Union-wide spillover and compliance influence | Medium term (2-4 years) |

| Price sensitivity for long-term preventive use | -0.8% | National, most pronounced in East Germany and lower-income urban areas | Short term (≤ 2 years) |

| Ingredient supply volatility for specialty inputs | -0.6% | Global sourcing networks, with direct impact on German nutraceutical formulators | Long term (≥ 4 years) |

| Consumer skepticism from inconsistent product efficacy | -0.4% | National, amplified through online review ecosystems and high-context consumer behavior | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory and Claims Compliance Burden

The Germany pet nutraceuticals market operates under a strict regulatory setting, and that raises cost and timing pressure for companies that want to expand quickly. Germany’s Federal Office of Consumer Protection and Food Safety, or Bundesamt für Verbraucherschutz und Lebensmittelsicherheit, plays a central role in oversight of veterinary medicine and related compliance functions, making regulatory readiness a practical requirement rather than a back-office task. European Union feed additive rules add another layer, because product positioning and ingredient use must align with a wider regional framework rather than a single national interpretation. This does not stop growth in the Germany pet nutraceuticals market, but it does favor larger companies with dedicated regulatory teams and more experience in evidence-backed claims. The result is a category where speed to shelf is less important than compliance discipline and documentation quality.

Price Sensitivity for Long-Term Preventive Use

Price sensitivity remains a real brake on the Germany pet nutraceuticals market because the value of preventive use often unfolds slowly, while the cost is immediate and recurring. This challenge is strongest in categories linked to aging, mobility, and daily maintenance, where owners may not see a dramatic before-and-after change in a short period. The issue becomes more visible in households with tighter spending capacity, especially when supplements compete with essential pet food, veterinary visits, and routine care products. Germany’s pet ownership base includes a significant share of single-person households, which can lower the willingness to sustain multiple preventive products over the long term. For the Germany pet nutraceuticals market, that means long-term growth depends not only on product availability but also on clearer communication of outcomes, better adherence support, and product formats that feel worth repeating month after month. Brands that cannot make benefits easy to understand are more exposed when consumers start trimming nonessential spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Vitamins and Minerals Anchor Broad Demand

Vitamins and minerals held 26.5% of the Germany pet nutraceuticals market share in 2025, and the same segment is also projected to post the fastest 7.7% CAGR through 2026 to 2031. That rare combination of largest and fastest status reflects how widely micronutrient products can be used across immunity, bone support, coat quality, and early cognitive support without needing a narrow condition-specific diagnosis. In the Germany pet nutraceuticals market, that flexibility makes the segment relevant across life stages and across both veterinary recommendations and self-directed owner purchases. It also keeps the category visible across multiple channels because the value proposition is easy to explain and repeat.

The market opportunity for milk bioactives, proteins, and peptides is expanding as product developers and pet owners increasingly seek specialized nutritional solutions beyond standard vitamins. Milk-derived bioactives are becoming more significant in early-life and recovery-focused applications, as they align with feeding strategies tailored to younger animals and households that prioritize life-stage-specific pet care over addressing occasional symptoms. Proteins and peptides are also benefiting from this trend, with companies like Kemin Industries, Inc., providing protein solutions designed to support immune and digestive health in premium pet nutrition formulations. Other nutraceuticals, such as botanical extracts and mobility blends, remain more fragmented. However, their positioning is improving as research on stress, behavior, and joint health continues to grow.

By Pets: Dogs Lead Share And Drive Faster Expansion

Dogs accounted for 51.1% of segment demand in 2025, making them the largest pet type in the Germany pet nutraceuticals market. Additionally, dogs represent the fastest-growing segment, with a 7.5% CAGR projected from 2026 to 2031. This growth reflects a consumer base increasingly willing to invest in products that support mobility, metabolism, skin health, and activity over time. The Germany pet nutraceuticals market is thus characterized by dog-driven premium growth, providing manufacturers with opportunities to develop higher-value programs focused on dog health management. The market potential for other pets remains smaller but offers targeted growth opportunities in areas where species-specific products are underserved in mass retail. Small mammals, ornamental birds, rabbits, and reptiles rely more on specialty channels and informed purchasing decisions because their nutritional requirements are less standardized in mainstream retail environments. As a result, this segment is commercially smaller but less competitive, particularly for products with clear species-specific positioning.

According to the Industrieverband Heimtierbedarf and the Zentralverband der Heimtierbranche, Germany had 15.7 million cats in 2025, with many multi-cat households. This increases unit volume when owners adopt a supplement routine applicable across the household. The cat segment drives strong demand for digestive support, general vitamins, and other daily products suited for routine care. Additionally, the growing awareness among pet owners about the benefits of supplements and routine care products further supports the market's expansion. Multi-cat households, in particular, offer manufacturers an opportunity to offer value packs and tailored solutions to meet the needs of multiple pets within a single household.

By Distribution Channel: Grocery Reach Leads While Digital Reorder Accelerates

Supermarkets and Hypermarkets accounted for 34.8% of channel demand in 2025, making them the largest route to purchase in the Germany pet nutraceuticals market because they fit routine household shopping behavior. Their lead also reflects the convenience advantage, as supplements can be purchased alongside regular pet food and weekly grocery items rather than requiring a separate trip. This channel works especially well for widely understood categories such as multivitamins and other basic functional products that do not require much explanation at the point of sale. In the Germany pet nutraceuticals market size structure, grocery-led distribution supports base volume and keeps entry-level products visible to a broad owner group. The online channel, however, is the fastest-growing, with a 7.8% CAGR through 2026 to 2031, indicating that repeat-use products benefit from digital replenishment and a deeper assortment.

The market opportunity for specialty stores and other direct channels is rising because higher-value products often require more explanation, stronger trust cues, or closer alignment with veterinary guidance. Specialty stores remain important for premium formulations, where ingredient origin, clinical support, and staff explanations influence purchase decisions. Other channels, including direct-to-consumer platforms and veterinary practice dispensing, are also gaining relevance as companies try to control product education and gather feedback that can support future formulation work. This matters in the Germany pet nutraceuticals market because products that require longer use often perform better when brands can explain purpose, dosing, and projected benefits clearly.

Geography Analysis

Bavaria and North Rhine-Westphalia were the largest regional demand centers in the Germany pet nutraceuticals market because they combine dense pet ownership, strong purchasing power, and well-developed veterinary and specialty retail networks. Bavaria benefits from a premium consumer base around Munich that is more receptive to targeted products linked to mobility, skin health, digestive support, and veterinarian-guided care. North Rhine-Westphalia adds scale through its large population and dense urban areas, such as Cologne and Düsseldorf. The region also matters operationally because its logistics infrastructure supports the efficient movement of shelf-stable and temperature-sensitive pet health products across western and northern Germany. Together, these two states help set the commercial tone for the Germany pet nutraceuticals market by concentrating both premium demand and distribution efficiency.

Hamburg and Berlin play a different role in the Germany pet nutraceuticals market because they function more as innovation and early adoption centers than as broad volume hubs. Their higher concentration of younger, smaller, and digitally engaged households supports demand for premium online-first products and newer categories such as microbiome support or behavior-oriented supplements. Germany’s pet base includes a significant share of animals in single-person households, and that demographic is more visible in large cities where convenience, delivery, and product education matter more in the purchase journey. Hamburg also has practical importance as a port-linked gateway for imported specialty ingredients, especially for marine-derived components used in omega-3 formulations. Berlin supports premium demand through a dense veterinary network and a consumer base that is open to products positioned around preventive care and functional nutrition.

Baden-Württemberg and Lower Saxony form the next important layer of the Germany pet nutraceuticals market because each supports growth through a different strength. Baden-Württemberg benefits from higher household incomes and a consumer profile that is comfortable with subscription-based and direct-to-consumer buying models. Lower Saxony matters because it is linked to veterinary research and academic work around companion animal nutrition, which supports a market that increasingly values substantiated claims and professional confidence. Eastern states such as Saxony, Thuringia, and Brandenburg currently spend less per pet, but they remain relevant as a medium-term expansion zone as income patterns and premium pet care behavior continue to converge. This means the Germany pet nutraceuticals market is not driven by one uniform national pattern, but by a layered regional structure where western and southern states lead current value, city-states shape early product adoption, and eastern regions provide future headroom.

Competitive Landscape

The Germany pet nutraceuticals market is moderately fragmented, with competition spread across animal health companies, ingredient specialists, and consumer pet nutrition brands rather than controlled by one dominant leader. Mars, Incorporated, Nestle S.A. (Purina), Zoetis Inc., Virbac SA, and Vetoquinol S.A. appear relevant to the competitive field described in the draft. The first group brings veterinary credibility, broad product portfolios, and distribution power, while the second group shapes the market through ingredient platforms, formulation capability, and technical support. This split matters because the Germany pet nutraceuticals market is increasingly won through both brand trust and upstream control over active ingredients, stability, and claim support. Companies that can connect those two layers are better placed to defend premium pricing and secure preferred access to veterinary, specialty, and digital channels.

Recent moves show that competition is intensifying at the formulation and infrastructure level, not only at the finished-product shelf. DSM-Firmenich AG announced in February 2026 that it would divest its Animal Nutrition and Health business to CVC Capital Partners for an enterprise value of EUR 2.2 billion (USD 2.4 billion), a move that could reshape sourcing decisions for mid-tier manufacturers that rely on vitamins, premixes, and specialty actives in the Germany pet nutraceuticals market. In April 2026, DSM-Firmenich AG also launched Veramaris O3 Max Pure, giving pet food and supplement makers a microalgal alternative that can replace fish oil without altering the targeted EPA-to-DHA profile[2]Source: DSM-Firmenich AG, “dsm-firmenich Launches Veramaris O3 Max Pure, a Seamless Fish Oil Replacement at Petfood Forum 2026,” dsm-firmenich.com. Elanco Animal Health Incorporated entered the over-the-counter supplement space in February 2025 with Pet Protect, using veterinarian-formulated positioning and the National Animal Supplement Council quality seal to extend clinical trust into retail wellness products[3]Source: Elanco Animal Health Incorporated, “Elanco Launches Pet Protect From the Makers of Advantage, Veterinarian-Formulated Supplements for Complete Pet Wellness,” Elanco Investor Relations, investor.elanco.com. These moves show that the Germany pet nutraceuticals market is becoming more competitive through science-backed ingredient control, adjacent category expansion, and stronger use of veterinary credibility.

White space remains visible in senior cat care, behavior support for urban dogs, and sustainable omega-3 alternatives, all of which align with the needs described in the draft. Senior cats are especially important because Germany has a large cat population, and multi-cat households can support repeat purchases across multiple animals. Behavioral support also has room to grow as scientific discussion around the gut-brain axis becomes more visible in companion animal health literature. The Germany pet nutraceuticals market therefore remains open to innovation, but the best openings sit in niches where clinical logic, premium willingness, and product adherence can come together. That is why the next phase of competition is likely to favor precise positioning over broad category expansion.

Germany Pet Nutraceuticals Industry Leaders

Mars, Incorporated

Nestle S.A. (Purina)

Virbac SA

Zoetis Inc.

Vetoquinol S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: German food-tech startup MicroHarvest announced the launch of 15 low-carbon, waste-upcycled microbial-protein pet food products across Europe by Q2 2026. This expansion addresses the growing demand for sustainable, gut-healthy, and hypoallergenic products in the German pet nutraceuticals market.

- April 2026: DSM-Firmenich AG introduced Veramaris O3 Max Pure at the Petfood Forum 2026, the first microalgal oil with a natural 3:2 EPA: DHA omega-3 ratio, produced through closed-system fermentation. This contaminant-free, non-GMO ingredient enables pet food brands in Germany and Europe to replace fish oil without compromising formulation integrity or label health claims.

- February 2026: DSM-Firmenich AG announced the sale of its Animal Nutrition and Health (ANH) business to CVC Capital Partners for EUR 2.2 billion (USD 2.42 billion), retaining a 20% equity stake. The ANH division will split into the Solutions Company (premixes, precision services) and the Essential Products Company (vitamins, carotenoids), with a long-term vitamins supply agreement supporting pet food and nutraceutical applications, including in Germany.

Germany Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are functional nutritional products formulated for pets that provide health benefits beyond basic nutrition, supporting specific functions such as joint health, digestion, immunity, skin and coat condition, and overall wellness. They typically include omega-3 fatty acids, probiotics, vitamins, minerals, proteins, peptides, and bioactive compounds.

The Germany Pet Nutraceuticals Market Report is Segmented by Sub Product (Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals, and Other Nutraceuticals), by Pets (Cats, Dogs, and Other Pets), and by Distribution Channel (Convenience Stores, Online Channel, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals | |

| Pets | Cats |

| Dogs | |

| Other Pets | |

| Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the current outlook for pet nutraceuticals in Germany?

The Germany pet nutraceuticals market is valued at USD 218.89 million in 2026 and is forecast to reach USD 308.25 million by 2031 at a 7.2% CAGR through 2026 to 2031.

Which sub product category leads demand in Germany?

Vitamins and minerals is the largest sub product segment with a 26.5% share in 2025, and it is also the fastest-growing segment with 7.7% CAGR through 2026 to 2031.

Which pet category leads the market in Germany?

Dogs held the largest pet-type share at 51.1% in 2025.

Which sales channel is expanding the fastest?

The online Cannel is the fastest-growing distribution route with a 7.8% CAGR through 2026 to 2031, supported by repeat purchase behavior and subscription-friendly product use.

What is the biggest challenge for brands selling supplements for pets in Germany?

Regulatory compliance is a major constraint because Germany applies strict labeling, feed, and veterinary oversight, which raises time-to-market and documentation requirements.

Where are the best growth openings for companies?

Senior cat products, behavior support for urban dogs, and sustainable omega-3 alternatives stand out because they fit Germany's pet demographics, premium demand, and evidence-focused buying behavior.

Page last updated on: