Russia Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

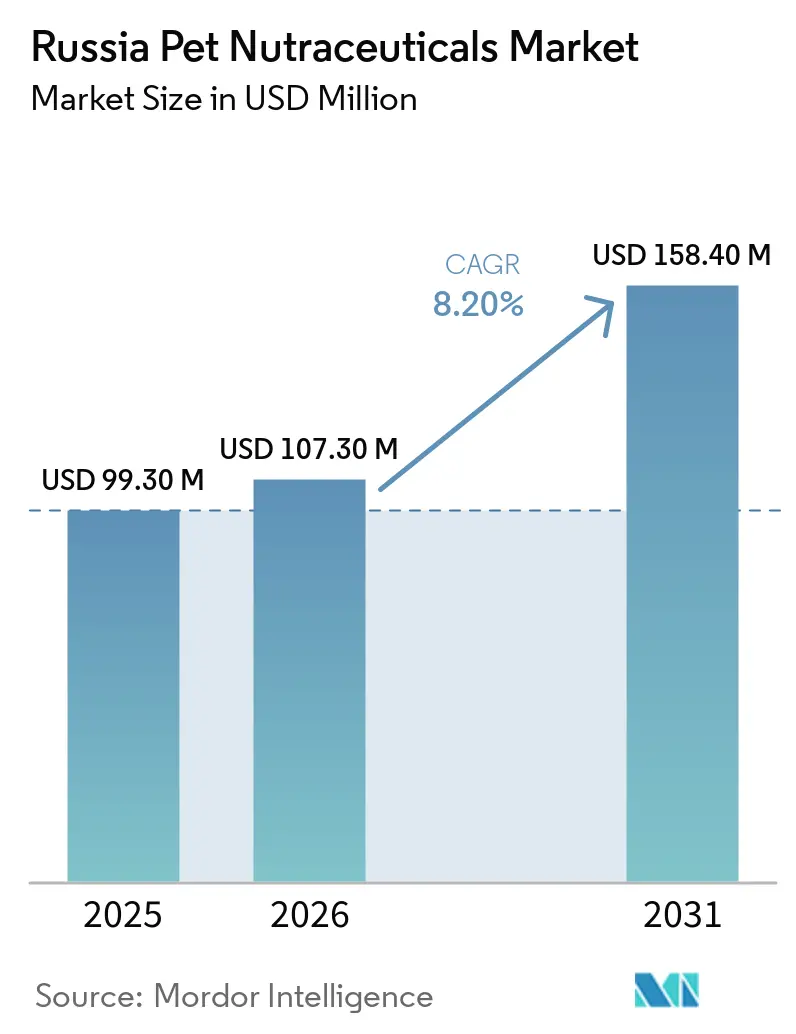

| Base Year Market Size (2025) | USD 99.30 Million |

| Market Size (2026) | USD 107.30 Million |

| Market Size (2031) | USD 158.40 Million |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Pet Nutraceuticals Market Analysis by Mordor Intelligence

The Russia pet nutraceuticals market size was valued at USD 99.30 million in 2025 and is estimated to grow from USD 107.30 million in 2026 to reach USD 158.40 million by 2031, at a CAGR of 8.20% during the forecast period (2026-2031). Growth in the Russian pet nutraceuticals market is influenced by factors such as pet humanization, increased veterinary involvement in preventive care, and the growing adoption of online purchasing and replenishment models. Additionally, the supply side of the market is evolving, with domestic brands gaining prominence and import substitution reshaping competitive dynamics across various supplement categories. However, the Russian pet nutraceuticals market faces challenges outside major cities, where premium pricing and limited product awareness hinder adoption. Furthermore, the market remains heavily reliant on specialized ingredients, making it vulnerable to supply chain disruptions and input cost pressures, despite improvements in local manufacturing.

Key Report Takeaways

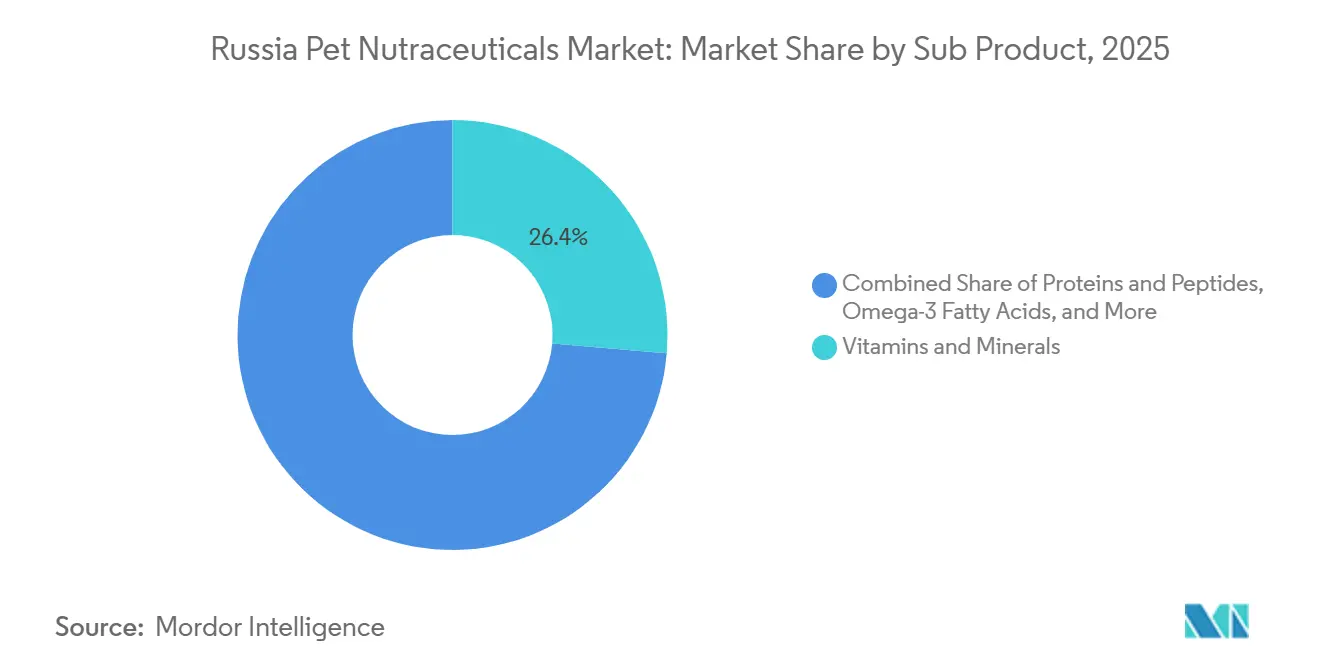

- By sub product, vitamins and minerals held 26.4% of the Russia pet nutraceuticals market share in 2025, and this segment is also projected to grow at a 7.9% CAGR through 2031.

- By pets, dogs accounted for 52.1% of the Russia pet nutraceuticals market size in 2025, while cats are forecast to record the highest CAGR of 8.5% through 2031.

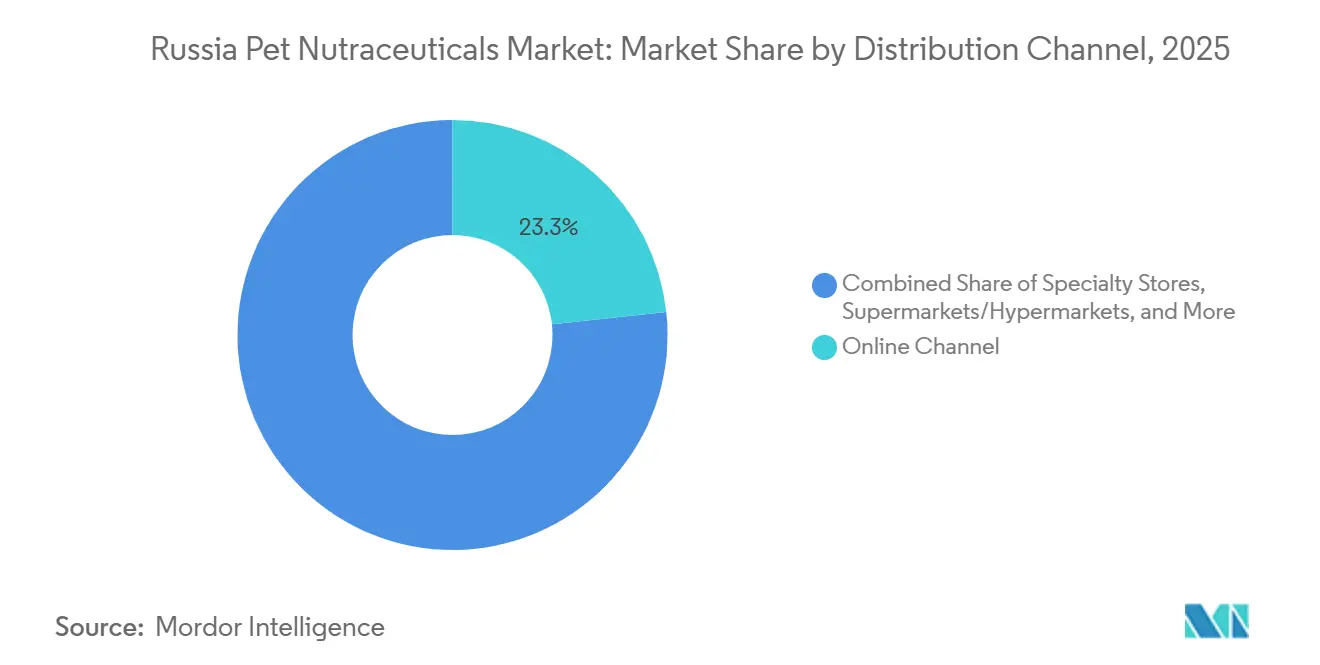

- By distribution channel, the online channel held 23.3% market share in 2025 and is forecast to remain the fastest-growing channel at a 9.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet Humanization and Premiumization in Companion Animal Care | +2.5% | Russia, strongest in Moscow, Saint Petersburg, and major urban centers | Short term (≤ 2 years) |

| Veterinary-Led Preventive Nutrition Adoption | +1.5% | Russia, nationwide, with stronger penetration in clinic-dense urban areas | Medium term (2-4 years) |

| Online Replenishment and Subscription Readiness | +1.0% | Russia, led by Moscow and Saint Petersburg, with growing reach into secondary cities | Short term (≤ 2 years) |

| Aging Pet Population and Geriatric Mobility Support Demand | +1.2% | Russia | Medium term (2-4 years) |

| Localization of Functional Inputs and Packaging | +0.8% | Russia, national, with investment centered in major production clusters | Long term (≥ 4 years) |

| Clinic-Driven Demand for Science-Backed Formulations | +0.5% | Russia, strongest in urban veterinary networks and telemedicine-linked channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization and Premiumization in Companion Animal Care

The Russia pet nutraceuticals market is experiencing growth driven by a more personalized and health-conscious approach to pet ownership, particularly in major Russian cities. According to ZOOINFORM, functional pet food accounted for 34.9% of cat food sales value in 2025, an increase from 33.3% in 2024[1]Source: ZooInform, “Russia's Pet Products Market Reached ₽590 Billion in 2025,” ZooInform, zooinform.ru. This indicates that health-focused spending continues to grow, even as lower-priced categories gain volume. Urban pet owners are increasingly scrutinizing ingredient lists, clinical evidence, and product purposes before purchasing supplements, thereby influencing the product mix in the Russian pet nutraceuticals market. This demand trend is most evident among consumers who already purchase premium pet food, regularly consult veterinarians, and prefer condition-specific products over general supplements. While the humanization of pets in Russia remains concentrated within a smaller, affluent urban demographic compared to Western Europe, this group significantly impacts category trends and pricing. This is driving the market toward formulations targeting immunity, digestion, coat quality, and long-term health maintenance. This shift is prompting companies to emphasize clearer scientific backing, simpler claims, and more targeted product positioning to build trust among premium consumers.

Veterinary-Led Preventive Nutrition Adoption

Veterinarians are the most trusted source for product discovery in the Russian pet nutraceuticals market, particularly for supplements that require detailed explanations and consistent use. According to ZOOINFORM RNC Pharma, sales of animal nutraceuticals through veterinary clinics surpassed RUB 44.5 billion (USD 0.5 billion) across measured categories in 2024. The pharmaceutical-adjacent nutraceutical segment grew 16.9% during the first 11 months of 2025, indicating sustained demand driven by veterinary clinics. A veterinary recommendation often shifts a purchase from discretionary spending to an essential component of ongoing pet care for many owners. This shift increases repeat purchase rates and enables better price realization compared to retail-only discovery. Purina’s FortiFlora, holding a 13% share of the Russian supplement market, demonstrates how strong veterinary placement can directly contribute to brand leadership. Consequently, the Russian pet nutraceuticals market is anticipated to remain closely linked to veterinary education, professional endorsements, and clinic access as preventive care becomes more commonplace.

Online Replenishment and Subscription Readiness

The Russia pet nutraceuticals market is transitioning to online platforms at a faster rate compared to many other pet-related categories, as supplements align well with repeat and convenience-based purchasing behaviors. According to ZOOINFORM and RNC Pharma, E-commerce accounted for 44.1% of the market's monetary volume from January to September 2025, up 5.6% from the previous year. Online spending through platforms such as Wildberries, Ozon, and Yandex. Market grew by 24% during the same period, while offline retail revenue declined by 2%. Subscription and auto-replenishment tools have become increasingly significant, helping minimize skipped purchases during inflationary periods and simplifying the maintenance of daily-use products. This is particularly important for items like vitamins, omega-3 capsules, and probiotic powders, where missed refills can disrupt the usage cycle. Additionally, the online model enhances accessibility for consumers in secondary cities, where specialist store assortments and veterinary retail networks may be limited. Consequently, the Russia pet nutraceuticals market is leveraging digital channels not only to drive sales growth but also to expand geographically and ensure greater category continuity.

Aging Pet Population and Geriatric Mobility Support Demand

The Russia pet nutraceuticals market is experiencing growth driven by the increasing importance of age-related care. Pets adopted between 2019 and 2021 will reach life stages in 2025 where products addressing joint support, digestive health, immune support, and healthy aging are increasingly relevant. This trend supports consistent spending, as older dogs and cats typically require more frequent health management than younger animals. According to RNC Pharma, Dogs play a significant role in this market, accounting for 52.15% of the by-pets segment in 2025, and continue to drive demand for joint and immunity-focused formulations. Cats are also gaining importance, with owners investing more in preventive indoor care, particularly for urinary health, coat maintenance, and weight management. This aging demographic is crucial for the Russia pet nutraceuticals market, as it encourages the adoption of premium, repeat-purchase products rather than one-time trials. Additionally, it highlights the value of clinically supported formulations, as owners of older pets are more inclined to follow targeted preventive care recommendations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Price Sensitivity Outside Major Urban Centers | -1.2% | Russia, strongest in secondary and tertiary cities | Short term (≤ 2 years) |

| Regulatory Friction for Functional Claims and Novel Ingredients | -0.8% | Russia, national, under EAEU EAEU (Eurasian Economic Union) and Rosselkhoznadzor-related frameworks | Medium term (2-4 years) |

| Limited Mass-Market Awareness of Nutraceutical Benefits | -0.6% | Russia, nationwide, especially outside major urban centers | Long term (≥ 4 years) |

| Import Dependence for Specialty Inputs and Packaging Components | -0.5% | Russia, national, with greater exposure in advanced functional categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Price Sensitivity Outside Major Urban Centers

Premium affordability remains a significant constraint on the Russian pet nutraceuticals market, particularly outside Moscow and Saint Petersburg. According to ZooInform's 2025 report, hard discounters experienced 20.2% growth in value and 15.4% growth in volume, indicating that many pet owners are still opting for lower-cost options in the broader market. This trend poses a challenge for nutraceuticals, as they are priced higher than standard supplements and everyday pet care products. In secondary and tertiary cities, while many buyers acknowledge basic pet care needs, they are less inclined to pay for products with functional differentiation. Although the Russian pet nutraceuticals market continues to grow, this dynamic limits the buyer base able to sustain premium price points. Revenue generation is thus concentrated within a smaller, urban-affluent demographic, making the market more vulnerable to fluctuations in city-level household spending. Unless the price gap narrows, broader national penetration will remain below the category's potential.

Regulatory Friction for Functional Claims and Novel Ingredients

Regulatory requirements increase the time, cost, and complexity of launching products for companies aiming to scale in the Russian pet nutraceuticals market. Functional claims and specialized ingredients require documentation and registration in compliance with EAEU (Eurasian Economic Union) regulations and oversight by Rosselkhoznadzor. This regulatory burden is more manageable for well-established suppliers but can hinder smaller entrants lacking local regulatory expertise. Additionally, the post-2022 supply environment has made testing, certification, and compliance processes more stringent for certain product lines. Domestic efforts to develop new bioactive compounds continue to rely heavily on imports in the functional segment, creating overlapping challenges in compliance and sourcing. While the Russian pet nutraceuticals market is not entirely restricted by regulations, the additional time required to commercialize advanced formulations slows market entry. This dynamic tends to benefit brands with existing registrations, enabling them to navigate the approval process more efficiently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Vitamins and Minerals Lead While More Specialized Categories Continue to Grow

Vitamins and minerals accounted for 26.4% of the Russia pet nutraceuticals market share in 2025, making them the largest subcategory. They are also projected to grow fastest, with a CAGR of 7.9% through 2031, indicating strong performance across both current market share and future growth potential. This segment's broad relevance across various life stages, health conditions, and breed sizes gives it a larger addressable market than more specialized functional niches. Domestic brands such as VEDA with My Totem, ECOPROM with Unitabs, and FARMAKS with Omega Neo are particularly prominent in this category, as familiarity and accessibility are significant factors in everyday supplementation. Notably, VEDA experienced a 44% growth in natural unit sales during the first three quarters of 2025, demonstrating the growing traction of domestic brands in this segment.

Probiotics and omega-3 fatty acids represent the sub-product groups with the strongest clinical expansion narratives in the Russia pet nutraceuticals market. In 2025, Purina’s FortiFlora captured 13% of the measured supplement market, highlighting the strong demand for gut health solutions, particularly when supported by veterinary recommendations. Omega-3 products are also gaining traction as clinical evidence for their benefits in skin, coat, and joint care continues to grow. In contrast, proteins, peptides, and milk bioactives remain less developed, partly due to limited local availability compared to more established international markets. Additionally, other pet nutraceuticals, including herbal and botanical options, are expanding their presence as companies seek differentiation in an increasingly competitive core segment.

By Pets: Dogs Hold the Largest Share While Cats Offer the Faster Growth Path

Dogs accounted for 52.1% of the pets segment in 2025, securing the largest size in the Russia pet nutraceuticals market. This dominance reflects higher spending per pet in categories such as joint support, digestive care, skin health, and immune maintenance. The dog segment also benefits from a well-established retail and veterinary infrastructure, facilitating product discovery and repeat purchases. Cats are projected to grow at a CAGR of 8.5% through 2031, making them the fastest-growing pet type in the Russia pet nutraceuticals market. This growth is driven by Russia’s substantial cat population and increased spending on preventive indoor care products addressing urinary, coat, and weight-related needs.

The other pets segment, while smaller, contributes to demand from urban households that keep birds, reptiles, and small mammals. A notable trend within the Russia pet nutraceuticals market is the rise of condition-specific cat products from domestic suppliers. According to RNC Pharma’s 2025 retail data, APICENNA’s Stop-Cystit and Hepatovet formulations are growing faster than the average market, indicating increased demand for targeted feline solutions. This suggests that products supporting feline urinary, hepatic, renal, and healthy-aging needs will remain a focus for product development during the forecast period. As more cats transition into mid-life health management stages, the use of preventive supplements is anticipated to become a regular part of spending patterns in this segment.

By Distribution Channel: E-commerce is Growing While Clinics Retain Premium Influence

The online channel accounted for 23.3% of the market in 2025, making it the largest distribution segment in the Russia pet nutraceuticals market. It is also projected to grow at a CAGR of 9.3% through 2031, indicating both current dominance and the fastest future growth. This trend suggests a structural shift rather than a temporary increase, as online platforms offer the convenience of discovery, comparison, and refill options in one place. While specialty stores remain relevant for premium product discovery, their role is gradually diminishing as consumers increasingly prefer marketplaces that provide reviews, pricing transparency, and subscription services. Supermarkets/Hypermarkets are less effective in this category, as shelf presence alone does not adequately convey the purpose or benefits of more complex functional products.

Convenience stores play a minor role in this market, as supplement purchases typically require comparison, planning, and a clear understanding of their use. Veterinary clinics and pharmacies continue to hold a significant position in the distribution of premium therapeutic and preventive products, where professional guidance is highly valued. Additionally, Rosselkhoznadzor-linked oversight enhances the perceived credibility of products dispensed through clinics for many consumers. The most notable channel shift is the increasing integration of veterinary guidance with digital fulfillment, including telehealth consultations, prescription-linked delivery, and direct manufacturer outreach. This convergence is anticipated to influence access, customer loyalty, and premium product adoption in the Russia pet nutraceuticals market during the forecast period.

Geography Analysis

The Russia pet nutraceuticals market has a unique structure influenced by import substitution, growth in domestic brands, and concentrated demand for premium products. According to RNC Pharma, Functional and health-oriented nutrition categories continued to gain market share, even as overall market growth slowed from 17.7% in 2024 to 15.8% in 2025. Pet food production in Russia increased by 57% between 2021 and 2025, with the country achieving its first 100,000 metric tons export milestone in 2025, highlighting the strengthening of local production capabilities[2]Source: Sergei Dankvert, “Russia in 2025 Exports 100,000 Tonnes of Pet Food for the First Time,” Interfax, interfax.ru.

Within Russia, demand for premium pet supplements remains concentrated in Moscow and Saint Petersburg, where factors such as higher veterinary density, dual-income households, and advanced subscription e-commerce platforms are more prevalent. These cities continue to influence the pricing and product mix of the Russia pet nutraceuticals market, even as the category's reach expands nationally. Secondary cities in the Central, Volga, and Siberian federal districts are emerging as new demand centers, driven by reduced access barriers enabled by online platforms. Future incremental volume growth is anticipated to come more from mid-tier cities than from further penetration in already mature urban centers.

Europe and Asia play a role in the Russia pet nutraceuticals market primarily through ingredient supply, regulatory benchmarks, and adjacent trade dynamics, rather than direct demand. The Eurasian Economic Union (EAEU) framework connects Russia with Kazakhstan, Belarus, Armenia, and Kyrgyzstan under a unified claims and compliance environment for pet food and supplement products. This framework supports regional export ambitions as Russian producers enhance local capabilities and product readiness. However, the primary geographic trend remains the uneven distribution of premium pet health spending, which is expanding from the two largest cities to a broader, more price-sensitive urban base across the country.

Competitive Landscape

The Russia pet nutraceuticals market was moderately concentrated in 2025, dominated by the top five players, including Mars, Incorporated, Nestlé S.A. (Purina), Virbac, Vafo Group, and Colgate-Palmolive (Hills Pet Nutrition). These leading companies benefit from strong veterinary access, established branding, and product familiarity. Meanwhile, the tier below the top players remains more dynamic, with over 30 new brands entering the Russian supplement market in the past three years.

Domestic suppliers are gaining prominence in the Russia pet nutraceuticals market, particularly in areas where local availability and competitive pricing outweigh the appeal of imported brands. For instance, VEDA achieved 44% growth in natural units during the first three quarters of 2025, demonstrating the rapid scalability of local brands. Other domestic players, such as APICENNA and FARMAKS, are also contributing to this trend, especially in condition-specific and everyday supplement categories. This shift signifies more than a short-term substitution, as streamlined local supply chains and faster adaptability are reshaping competition below the multinational leaders. Consequently, the market is becoming more balanced between established clinical brands and increasingly capable domestic challengers.

Leading companies are defending their market positions through science-backed product development and professional engagement rather than relying solely on brand visibility. Nestlé S.A. (Purina) launched AdvantEDGE for global market including Russia in April 2026, focusing on microbiome-targeted nutrition through prebiotics, probiotics, and postbiotics[3]Source: Nestle Purina, “Purina Pro Plan Launches AdvantEDGE Line,” Purina News Center, newscenter.purina.com. Mars Incorporated's Royal Canin renewed its multi-year partnership with the University of Tennessee Veterinary Obesity Center in March 2026, reinforcing its commitment to clinical research to provide improved products in Russia. In 2025,Virbac expanded its specialty companion animal portfolio with the introduction of Thyronorm and Vikaly, strengthening its presence in condition-specific nutrition and care. These initiatives reflect a market where credibility, clinical relevance, and supply chain reliability remain critical to sustaining long-term competitive strength.

Russia Pet Nutraceuticals Industry Leaders

Mars Incorporated

Nestlé S.A. (Purina)

Virbac

VAFO Group

Colgate-Palmolive (Hills Pet Nutrition)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Purina Pro Plan introduced the AdvantEDGE line in the global market, including Russia, a probiotic-based nutrition range for adult and senior dogs and cats. This product line features a triple-action blend of prebiotics, probiotics, and postbiotics designed to support digestive and immune health, addressing the increasing clinical demand for microbiome-focused nutrition.

- April 2026: VAFO Group launched a redesigned global brand identity and refined product portfolio for Carnilove, its premium pet food brand inspired by natural animal diets.

- March 2026: Royal Canin renewed its multi-year agreement with the University of Tennessee Veterinary Obesity Center, continuing a clinical research partnership on feline and canine obesity prevention and treatment. This agreement helps in producing products for the global market, including Russia.

Russia Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are non-drug substances produced from food or natural extracts. Administered orally, they bridge the gap between nutrition and medicine, offering health benefits like preventing disease or supporting normal body functions

The Russia Pet Nutraceuticals Market Report is segmented by sub product (Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals, and Other Nutraceuticals) by pets (Cats, Dogs, and Other Pets), and by distribution channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and Other Channels). The market forecasts are provided in terms of value in USD.

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Pet Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets and Hypermarkets |

| Veterinary Clinics and Pharmacies |

| By Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Pet Nutraceuticals | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets and Hypermarkets | |

| Veterinary Clinics and Pharmacies |

Key Questions Answered in the Report

What is the forecast value of Russia pet nutraceuticals by 2031?

The Russia pet nutraceuticals market is projected to reach USD 158.4 million by 2031 from USD 107.3 million in 2026, at an 8.2% CAGR.

Which sub product category leads demand in Russia?

Vitamins and minerals led with 26.4% share in 2025 and are also forecast to grow at a 7.9% CAGR through 2031.

Which pet type creates the largest and fastest growth opportunities?

Dogs held the largest 2025 share at 52.1%, while cats are estimated to grow the fastest at an 8.5% CAGR.

Why is online retail so important for pet supplements in Russia?

The online channel held 23.3% share in 2025 and is forecast to grow at 9.3% CAGR, helped by subscriptions, comparison tools, and wider reach beyond the largest cities.

What are the main risks affecting future expansion?

Premium price sensitivity outside major cities, regulatory friction, lower mass-market awareness, and dependence on imported specialty inputs remain the main constraints.

Page last updated on: