Italy Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

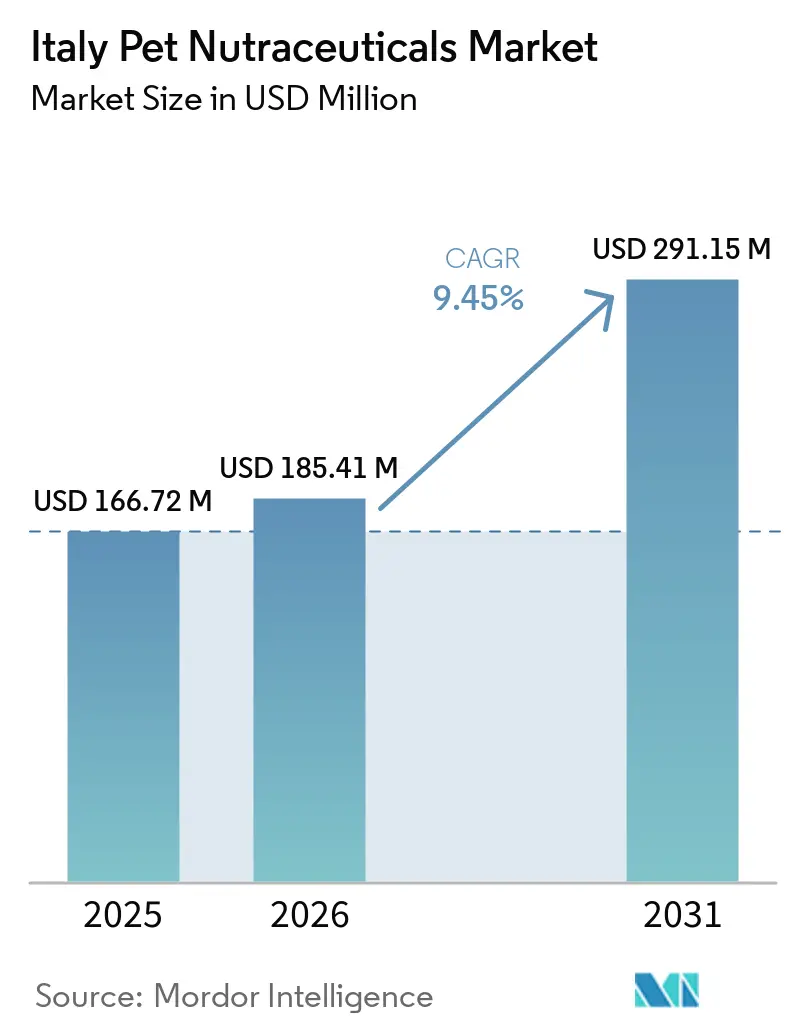

| Base Year Market Size (2025) | USD 166.72 Million |

| Market Size (2026) | USD 185.41 Million |

| Market Size (2031) | USD 291.15 Million |

| Growth Rate (2026 - 2031) | 9.45% CAGR |

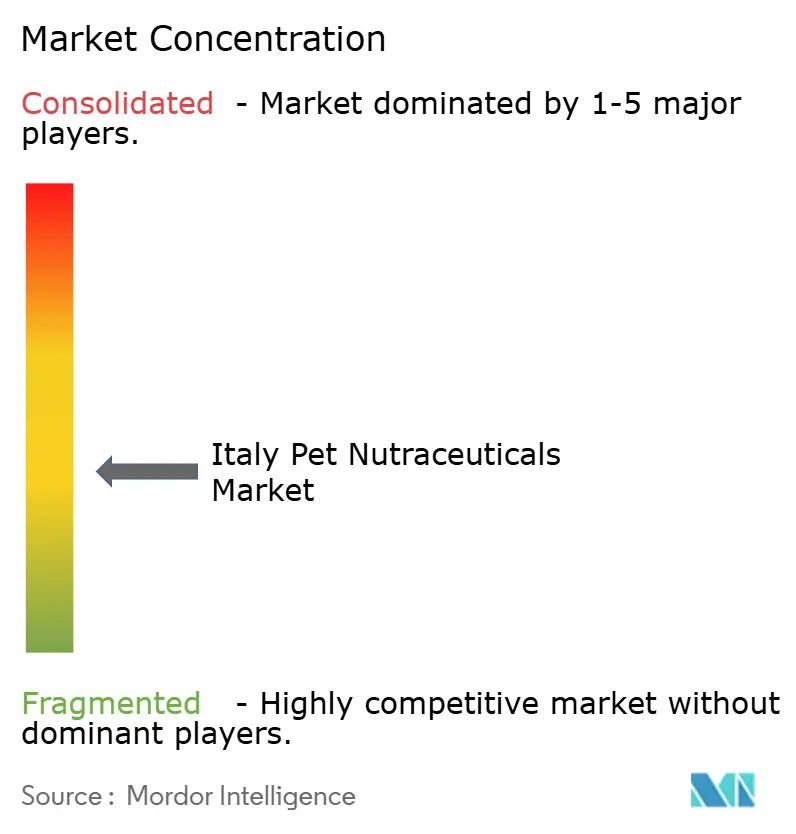

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Pet Nutraceuticals Market Analysis by Mordor Intelligence

The Italy pet nutraceuticals market size is estimated to increase from USD 166.72 million in 2025 and USD 185.41 million in 2026 to USD 291.15 million by 2031, growing at a CAGR of 9.45% during 2026-2031. The market is supported by a large companion animal base of 36.5 million animals[1]FEDIAF, 2025 Facts & Figures: FEDIAF, 2025, europeanpetfood.org, which keeps the addressable demand pool broad nationwide. Demand is also strengthened by high supplement adoption, with nearly half of dog owners already buying functional products in tablet, powder, or paste formats. Northern Italy remains the strongest base for specialist veterinary recommendations and premium repeat buying, while Southern Italy is providing the market with a faster path to online customer acquisition. Clinical support for probiotics, mobility formulas, and gut health products is improving product credibility and helping brands maintain premium price points in veterinary and specialty channels. Growth in the Italy pet nutraceuticals market still faces pressure from compliance with claims requirements, swings in ingredient costs for marine and probiotic inputs, and stronger retailer private-label activity in price-led channels.

Key Report Takeaways

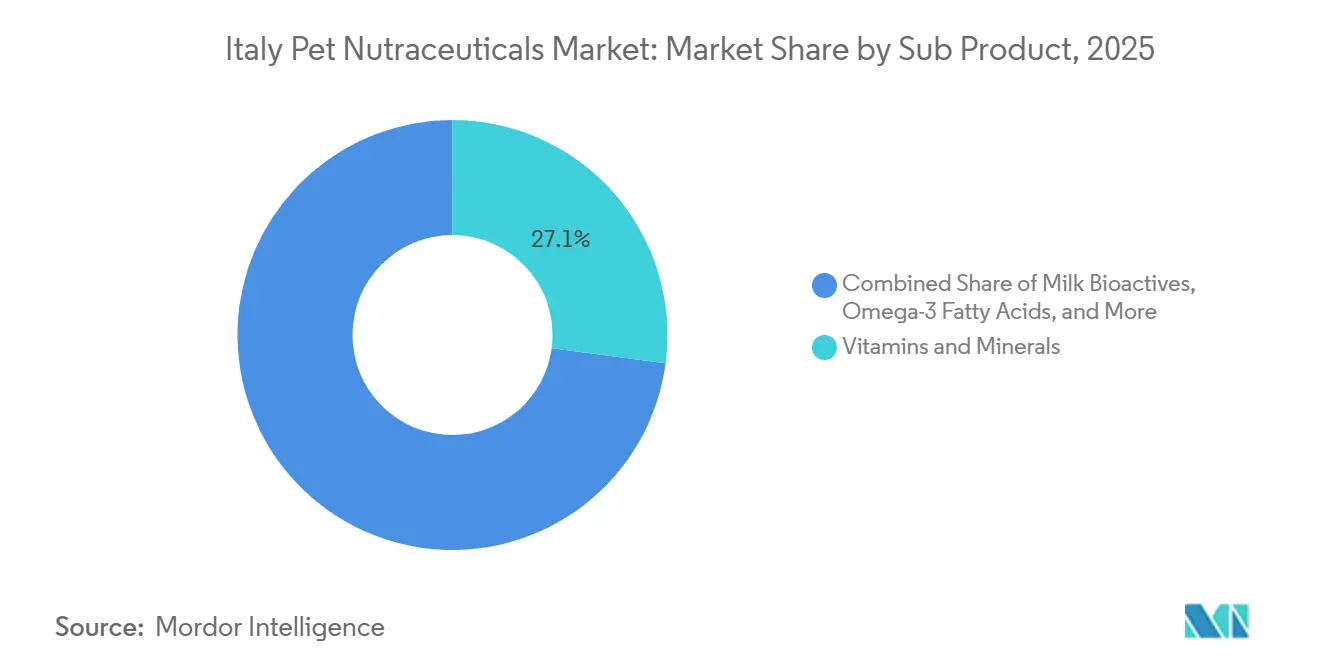

- By sub-product, vitamins and minerals accounted for 27.1% of the Italy pet nutraceuticals market size in 2025, while probiotics are anticipated to expand at a 10.8% CAGR between 2026 and 2031.

- By pets, dogs held 63.1% of the Italy pet nutraceuticals market share in 2025, while cats recorded the fastest projected CAGR at 9.9% between 2026 and 2031.

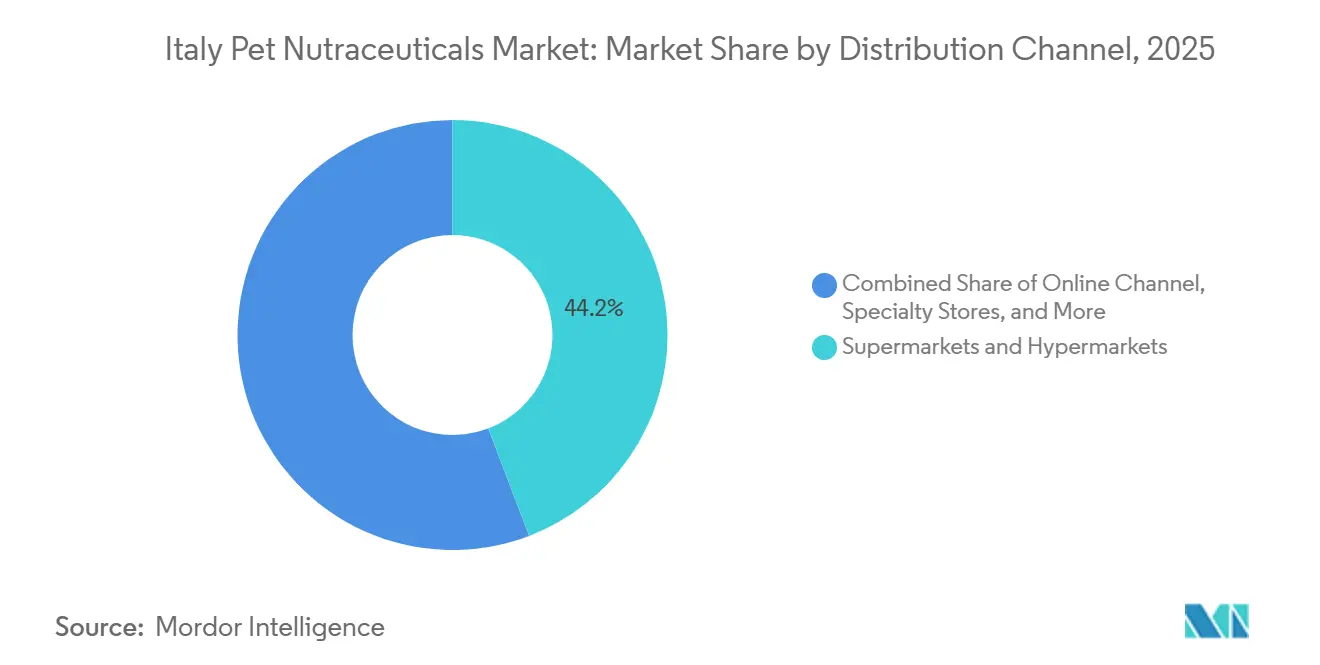

- By distribution channel, supermarkets and hypermarkets accounted for 44.2% of the Italy pet nutraceuticals market size in 2025, while the online channel is projected to advance at an 11.2% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Premiumization of Pet Health Spending | +1.90% | Italy wide, with highest intensity in Milan, Turin, and Bologna | Short term (≤ 2 years) |

| Preventive Veterinary Supplement Adoption | +1.60% | Italy wide, with strongest clinic density in Lombardy, Lazio, and Campania | Short term (≤ 2 years) |

| E-Commerce-Assisted Trial of Functional Pet Formats | +1.40% | Italy wide, with fastest uptake in Southern Italy | Medium term (2-4 years) |

| Aging Companion Animal Demand for Mobility and Gut-Health Products | +1.60% | Italy wide, with stronger repeat buying in Northern urban households | Medium term (2-4 years) |

| Microbiome-Driven Product Differentiation in Veterinary Channels | +0.80% | Europe wide, with Italy as a high value execution market | Long term (≥ 4 years) |

| Sustainable Ingredient Sourcing as a Shelf-Access Advantage | +0.70% | Europe wide, with early preference in Italian specialty retail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Premiumization of Pet Health Spending

Italian pet owners are moving beyond basic care and are spending more on products linked to preventive wellness, which directly supports the Italy pet nutraceuticals market. The adoption rate is already broad, with nearly half of dog owners purchasing functional supplements, indicating that these products are no longer limited to a niche urban audience[5]La Stampa, “Cani e gatti nelle famiglie italiane: Assalco Zoomark 2026,” lastampa.it. This buying pattern aligns with a broader shift toward higher-value pet healthcare choices, where owners seek support for digestion, mobility, immunity, and daily condition management rather than just occasional treatment. Premium demand is strongest in Milan, Turin, and Bologna, where household income and access to specialist clinics make repeat supplement use more consistent. That pattern benefits categories with stronger clinical or ingredient storytelling, since owners in premium cohorts tend to pay more for products that look specific and credible. It also gives specialty stores and veterinary channels more room to defend premium pricing than mass retail formats usually can. As a result, premiumization is not only raising average selling prices but also widening the commercial space for differentiated formulas across the Italy pet nutraceuticals market.

Preventive Veterinary Supplement Adoption

Veterinary recommendations remain one of the strongest purchase triggers in the Italian pet nutraceuticals market, as owners tend to stick with products introduced in a clinic setting. Retail monitoring by GS1 Italy indicated robust sales of vitamins-labeled and prebiotics-related pet products in 2025[2]Riccardo, “Does Your Dog Read Labels Better Than You Do?” Encanto Nutraceutical, 2025, encanto.it, underscoring the growing consumer preference for health-oriented pet nutraceutical solutions. Products recommended by veterinarians usually retain stronger customer loyalty because the purchase is tied to a health plan rather than shelf comparison alone. This matters most in joint support, probiotics, omega-3 fatty acids, and digestive health, where clinical explanation plays a larger role in repeat buying. Northern urban areas have a denser clinic network, which gives brands stronger access to prescriptive influence and better follow-through on longer supplement regimens. Companies that invest in veterinary education, clinical data, and targeted practice outreach are, therefore, better placed to protect premium positions than brands that rely mainly on grocery visibility. This channel effect keeps preventive supplementation a durable demand driver rather than a short-lived retail trend in the Italy pet nutraceuticals market.

E-Commerce-Assisted Trial of Functional Pet Formats

Digital retail is making it easier for consumers to try complex supplement formats, thereby widening access across the Italian pet nutraceuticals market. The Italian pet category saw sustained growth in online sales, reinforcing e-commerce's role as a key channel for discovering and purchasing pet nutraceutical products. That matters because probiotics, postbiotics, milk bioactives, and mobility blends often need more explanation than physical shelves can provide. Online platforms solve part of that problem through richer product pages, reviews, subscriptions, and recommendation tools that simplify first purchase decisions. They also lower entry barriers for brands that do not yet have national shelf coverage, which is especially relevant in Southern Italy, where digital adoption is rising faster than specialist store density. Zooplus and Arcaplanet ranking among Italy's top 100 e-commerce companies shows that pet care is already operating at a digital scale rather than in an early testing phase. This keeps online trials and auto-replenishment as a strong medium-term growth driver for the Italy pet nutraceuticals market.

Aging Companion Animal Demand for Mobility and Gut-Health Products

An aging companion animal base is raising demand for repeat-use products in mobility and digestive support across the Italy pet nutraceuticals market. Italian National Institute of Statistics data published in December 2025 showed that pet-owning households continued to rise between 2020 and 2024, which means a large cohort of animals acquired during that period is moving into life stages with higher support needs. Studies by the Animal Science and Technology College have shown meaningful benefits from synbiotic supplementation and from mobility formulas containing eggshell membrane, hyaluronic acid, krill-derived omega-3, and Boswellia serrata[3]Source: H. Shen, Y. Zhao, S. Zhang et al., “Synbiotic Supplementation Mitigates Antibiotic-Associated Diarrhea by Enhancing Gut Microbiota Composition and Intestinal Barrier Function in a Canine Model,” Probiotics and Antimicrobial Proteins, springer.com. These findings matter commercially because they give veterinarians and premium retailers a firmer scientific basis for recommending longer use cycles. Older dogs drive a large share of mobility purchases, while digestive support spans both dogs and cats and benefits from easier everyday positioning. Because these needs are recurrent rather than seasonal, aging pet demographics support steadier repurchase patterns than many wellness categories do. This makes senior health demand one of the clearest structural supports for sustained growth in the Italy pet nutraceuticals market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Nutraceutical Claims and Label Compliance Burden | -0.90% | Italy and European Union wide, with an added Italy specific notification layer | Short term (≤ 2 years) |

| Ingredient Cost Volatility in Marine, Probiotic, and Specialty Inputs | -0.80% | Global supply chain, with direct margin impact on Italian importers | Medium term (2-4 years) |

| Price Sensitivity in Mass Retail and Private Label Substitution | -0.70% | Italy wide, strongest in Supermarkets and Hypermarkets | Short term (≤ 2 years) |

| Formulation Complexity in Balancing Palatability and Efficacy | -0.50% | Italy wide, with species and breed level intake differences | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Nutraceutical Claims and Label Compliance Burden

Regulatory compliance remains a significant barrier to the Italy pet nutraceuticals market, as supplement claims and labeling must comply with both European Union rules and Italy-specific practices. Products entering Italy must comply with feed additive and complementary feed rules, which makes wording on health support, usage, and ingredient presentation more sensitive than in standard consumer goods categories. A product statement that is commercially usable in another European market may still need relabeling or reformulation before it fits Italian expectations, which adds time and cost for cross-border launches. Large multinational groups can spread those costs across broader portfolios, but smaller challengers often cannot do so as efficiently. This difference slows the entry of innovations and can narrow the number of premium launches that reach veterinary or specialty shelves each year. Compliance pressure also favors companies that already have internal regulatory teams and documented ingredient dossiers, making the market harder for smaller domestic or digital-first entrants. For that reason, claim fragmentation acts as a commercial restraint on speed, margin, and scale across the Italy pet nutraceuticals market.

Ingredient Cost Volatility in Marine, Probiotic, and Specialty Inputs

Input cost volatility is a persistent challenge in the Italy pet nutraceuticals market because several high-demand products depend on ingredients with unstable supply and pricing. Marine omega-3 fatty acids, probiotic cultures, and milk bioactive ingredients are exposed to supply, processing, and transport pressures that can move faster than retail prices[4]Source: R. M. Heilmann et al., “The Effects of Omega-3 Supplementation on the Omega-3 Index and Quality of Life and Pain Scores in Dogs,” PubMed Central, pmc.ncbi.nlm.nih.gov. That is difficult for many Italian buyers because local importers and smaller manufacturers usually do not have the same purchasing scale or hedging capacity as global suppliers. The problem is sharper in proven categories such as omega-3 support, where scientific validation keeps demand firm even when ingredient margins tighten. When costs rise too quickly, retailers often respond by pushing simpler private label alternatives or limiting price increases on branded items. That can reduce space for science-led products whose value depends on more expensive and better-documented actives. As a result, ingredient volatility affects both profitability and premium product mix in the Italy pet nutraceuticals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Vitamins Anchor the Base While Probiotics Set the Growth Pace

Vitamins and minerals held 27.1% of Italy's pet nutraceuticals market share in 2025, making them the largest sub-product group because they combine high awareness, routine use, and wide distribution across grocery, specialty, and veterinary channels. Omega-3 fatty acids, proteins, and peptides followed as the next most commercially relevant groups, supported by stronger use in mobility, skin, and digestive support. Milk bioactives and other nutraceuticals remain on a smaller scale, but they are gaining attention as owners seek more targeted health positioning.

Probiotics are anticipated to record the fastest CAGR at 10.8% between 2026 and 2031, helped by growing veterinary acceptance and a stronger body of peer-reviewed evidence in both dogs and cats. Omega-3 fatty acids and proteins and peptides are also well-positioned for healthy growth because they align with joint care, inflammation support, and condition-specific management. Milk Bioactives are still at an earlier stage, but new science and more specialist positioning should gradually widen their relevance. The category mix shows that volume still sits in familiar formulations, while future growth is moving toward more evidence-based, biologically differentiated products in the Italy pet nutraceuticals market.

By Pets: Dogs Hold the Largest Base While Cats Offer the Stronger Upside

Dogs accounted for 63.1% of the Italy pet nutraceuticals market size in 2025, supported by higher supplement spend per animal and heavier use in mobility, digestive, and general wellness routines. Dogs also benefit from stronger clinic engagement, which raises veterinary recommendation rates and lifts premium product use. Cats formed the second-largest value segment, while other pets remained smaller because product depth and owner awareness are still more limited outside the core dog and cat base.

Cats are anticipated to post the fastest CAGR at 9.9% between 2026 and 2031, backed by a population of 10.2 million as of 2025, according to FEDIAF, and a significant supplement adoption. Dogs will keep growing as senior care and chronic condition support expand, but the feline range still has more whitespace in joint care, cognitive support, and metabolic wellness. Other pets should advance from a smaller base as specialist awareness improves, especially in households with birds and small mammals. That pattern leaves cats as the clearest underdeveloped opportunity set within the Italy pet nutraceuticals market.

By Distribution Channel: Grocery Leads Reach While Online Sales Expand Faster

Supermarkets and hypermarkets accounted for 44.2% of distribution in 2025, giving them the largest channel position in the Italy pet nutraceuticals market, as they offer a broad reach and strong visibility for routine supplement categories. Specialty stores ranked next and remained important for premium formulas that benefit from staff guidance and more thorough product explanations. Convenience stores and other channels were smaller, serving limited top-up and urgent purchase needs rather than broader regimen-based use.

The online channel is anticipated to grow at the fastest 11.2% CAGR through 2031, as subscriptions, education-led listings, and national reach reduce barriers for newer or more complex products. Specialty stores should also continue to expand, as premium buyers often want greater confidence in ingredients and usage before they commit to repeat purchases. Supermarkets and hypermarkets will remain central to scale, but their growth will be more constrained by private label pressure and easier price comparison. This means channel expansion in the Italy pet nutraceuticals market is likely to shift toward formats that combine access, advice, and replenishment efficiency.

Geography Analysis

Italy has a broad demand base, with 54.5% of households owning at least 1 pet and a total companion animal population of 36.5 million in 2025, according to FEDIAF. This gives the market strong depth across both everyday wellness products and more targeted clinic-recommended formulas. Italian owners also show a favorable attitude toward preventive care, making it easier to sustain supplement use over time than in markets where purchases remain mainly episodic.

Northern Italy remains the strongest commercial base for the Italy pet nutraceuticals market because Lombardy, Piedmont, Veneto, and Emilia-Romagna combine higher income, denser veterinary networks, and deeper specialty retail coverage. That mix supports stronger premium spending and more stable repeat buying for probiotics, joint formulas, and omega-3 products. Lombardy also matters as a manufacturing and formulation base for local suppliers working with natural and Mediterranean ingredients. Central Italy, led by Rome, bridges strong clinical activity with a growing online buying habit, which helps both established and new brands. Southern Italy has lower specialty density, but it is recording faster pet e-commerce adoption, which makes online-first expansion more practical there.

Domestic manufacturing gives the Italy pet nutraceuticals market an added local layer that is less common in many European countries. Companies such as Candioli Pharma and NBF Lanes Srl benefit from local formulation credibility and veterinary relationships, which are valuable in a category where trust affects repeat use. Italy also benefits from European Union ingredient access and scientific validation pathways, which helps domestic producers source and position more specialized actives. These regional and structural features support continued expansion in the Italy pet nutraceuticals market, even though pricing and regulatory pressure vary by channel and region.

Competitive Landscape

The Italy pet nutraceuticals market remains moderately fragmented, with the leading group including Mars, Incorporated, Nestlé S.A., Vetoquinol, ADM, and Virbac holding meaningful positions without closing off room for specialists and local challengers. Mars, Incorporated and Nestlé S.A. benefit from broad animal health and nutrition relationships, which help them move adjacent wellness products through retail and professional channels. Vetoquinol and Virbac compete more directly through clinically positioned portfolios and deep veterinary access, both of which are important in a category where trust and compliance matter. ADM plays a different role by supplying ingredient systems and turnkey wellness solutions that help formulators build science-led products for the Italian market. This creates a layered competitive structure where finished-brand strength and upstream ingredient capability both matter.

Several recent strategic moves show how competition is developing in the Italy pet nutraceuticals market. ADM launched PRIOME Joint Health in March 2026 and had already introduced seven turnkey wellness formulas for the European, Middle Eastern, and African regions in 2024, strengthening its science-led ingredient platform. Virbac strengthened its feline health position through the Thyronorm acquisition and widening its relevance in cat-focused care. Swedencare AB used a limited Amazon and Zooplus launch before moving to a broader European rollout of NaturVet in 2026, showing a digital-first route into Italy. H&H Group also expanded Zesty Paws into Italy through European online channels during Fiscal Year 2025, which confirms that cross-border premium supplement brands still see open room in the market.

White space remains strongest in feline-specific formulas, veterinary-exclusive products with locally relevant evidence, and premium lines built around traceable ingredients. Italian companies such as Candioli Pharma and NBF Lanes Srl remain important because domestic production, good manufacturing practice positioning, and veterinary trust still carry weight in specialist channels. The market is therefore competitive, but it is not closed, and newer entrants can still build position if they combine evidence, channel fit, and palatability well. That balance between large multinational scale and specialist opportunity should keep competition active across the Italy pet nutraceuticals market over the forecast period.

Italy Pet Nutraceuticals Industry Leaders

Mars, Incorporated

ADM

Vetoquinol

Virbac

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Swedencare AB commenced a full-scale European rollout of NaturVet by Swedencare, presenting an updated brand identity and reformulated products, directly supporting the brand's commercial readiness for Italian veterinary and specialty retail channels.

- December 2025: Virbac acquired the feline hyperthyroidism treatment Thyronorm/Felanorm from Norbrook Laboratories in a transaction valued at approximately USD 130 million. This acquisition enhanced Virbac's companion animal health portfolio by incorporating a prominent specialty product for chronic feline endocrine disorders, further bolstering its feline-specific health and nutrition offerings in European markets, including Italy.

- March 2025: Swedencare AB acquired Summit Vet, a veterinary pharmaceuticals company, to enhance its access to the veterinary channel in Europe. Summit Vet directly supported NaturVet's expansion into veterinary distribution networks, including the Italian market.

Italy Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are bioactive products derived from nutritional, natural, or functional ingredients that are administered to companion animals to support health, wellness, and disease management beyond basic nutritional requirements. The Italy pet nutraceuticals market is segmented by sub-product (milk bioactives, omega-3 fatty acids, probiotics, proteins and peptides, vitamins and minerals, and other nutraceuticals), by pets (dogs, cats, and other pets), and by distribution Channel (online channel, specialty stores, supermarkets and hypermarkets, convenience stores, and other distribution channels). The market forecasts are provided in terms of value (USD) and volume (Metric Tons).

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Nutraceuticals |

| Dogs |

| Cats |

| Other Pets |

| Online Channel |

| Specialty Stores |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Other Distribution Channels |

| By Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals | |

| By Pets | Dogs |

| Cats | |

| Other Pets | |

| By Distribution Channel | Online Channel |

| Specialty Stores | |

| Supermarkets and Hypermarkets | |

| Convenience Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the size of the Italy pet nutraceuticals space in 2026?

The Italy pet nutraceuticals market stands at USD 185.41 million in 2026.

Which sub product is expanding the fastest in Italy?

Probiotics are advancing at the fastest pace, with a projected 10.8% CAGR through 2031, supported by stronger veterinary acceptance and growing clinical evidence.

Which pet category generates the most revenue?

Dogs remain the largest value contributor, accounted for 63.1% of market share in 2025 because of higher spending per animal and greater use in mobility and digestive support.

Which sales channel is growing the quickest?

The online channel is growing the fastest at an 11.2% CAGR between 2026 and 2031, helped by subscriptions, richer product education, and easier access across regions with lower specialty store density.

Page last updated on: