UK Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

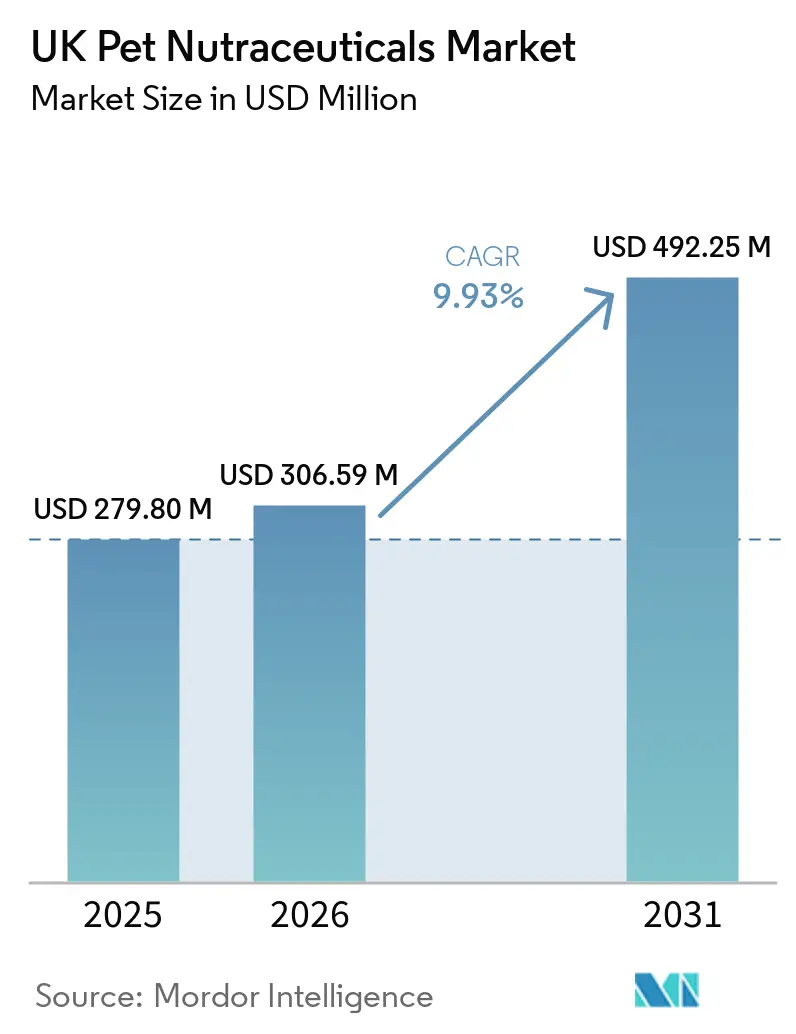

| Base Year Market Size (2025) | USD 279.80 Million |

| Market Size (2026) | USD 306.59 Million |

| Market Size (2031) | USD 492.25 Million |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

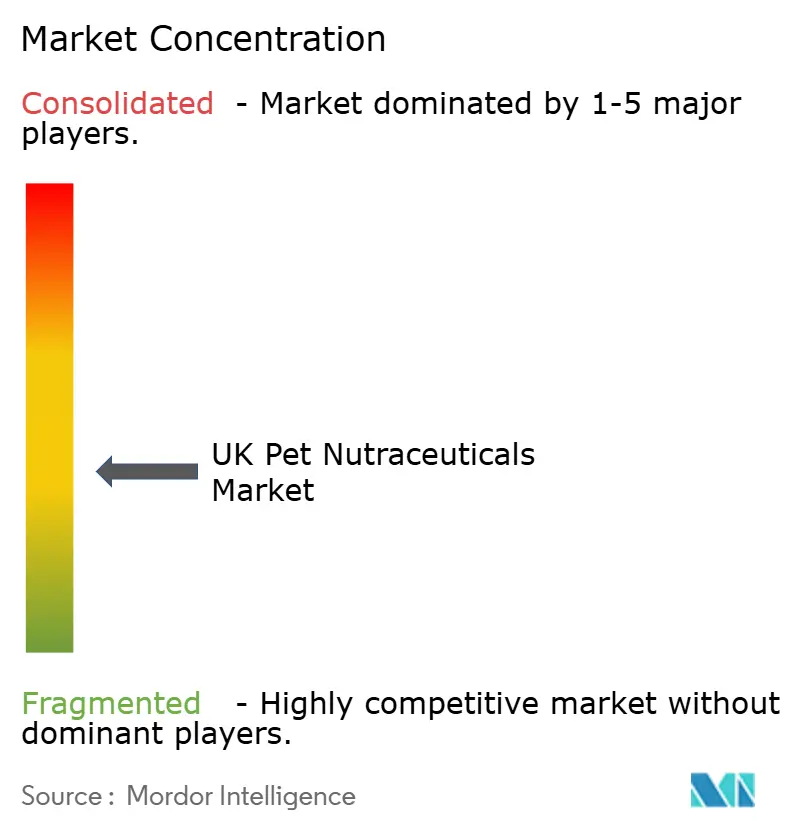

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UK Pet Nutraceuticals Market Analysis by Mordor Intelligence

The UK pet nutraceuticals market size was valued at USD 279.80 million in 2025 and projected to grow from USD 306.59 million in 2026 to reach USD 492.25 million by 2031, at a CAGR of 9.93% during the forecast period (2026-2031). Rising pet humanization, post-Brexit regulatory clarity, and cold-extrusion innovations have shifted supplements from discretionary treats to routine preventative care. Digital retail and subscription programs compress the traditional gap between clinics and consumers, while veterinary endorsements remain the single strongest purchase trigger. Ingredient cost turbulence, especially in marine omega-3 oils, continues to test gross margins, yet corporate investments in data analytics and precision nutrition signal that personalized regimens will anchor the next wave of growth. The market's competitive intensity is moderate, with multinational feed conglomerates benefiting from scale advantages, while specialty competitors focus on differentiation through formulation science.

Key Report Takeaways

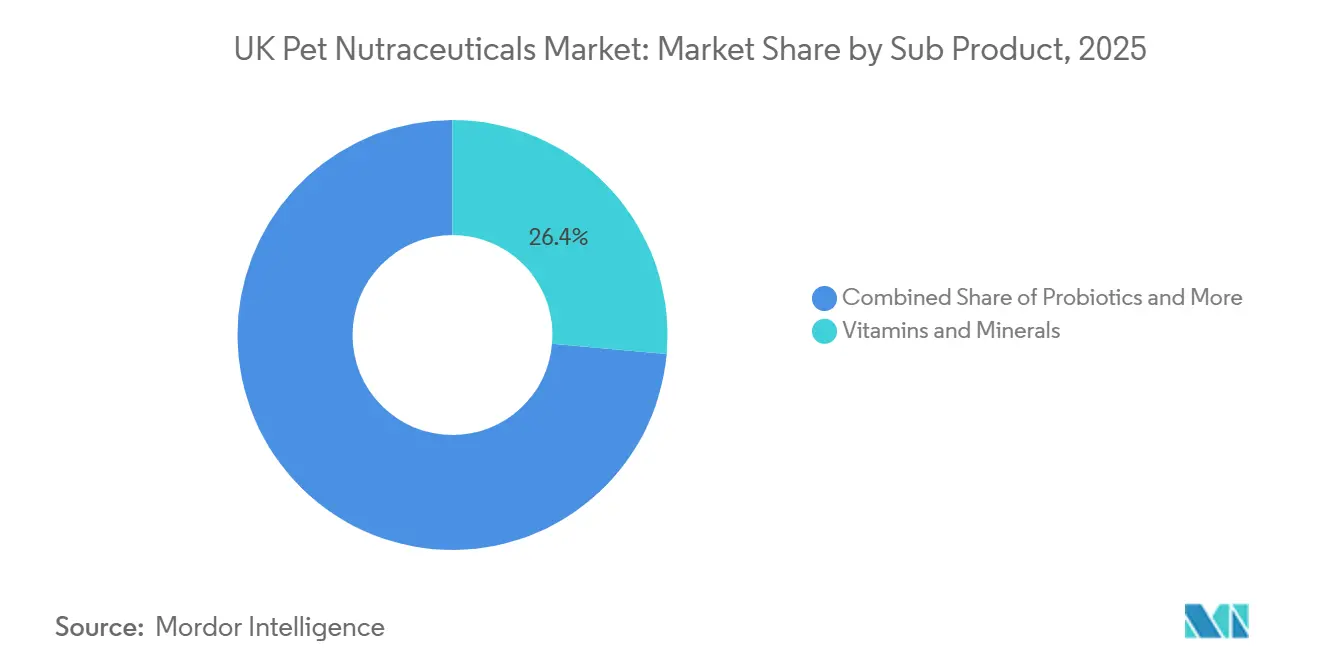

- By sub product, Vitamins and minerals captured 26.4% of the UK pet nutraceuticals market share in 2025 and are advancing at a 10.4% CAGR through 2031, retaining leadership on the strength of clinical validation for organic selenium and carotenoid blends.

- By pets, dogs accounted for 54.3% of demand in 2025, but cats are projected to expand at a 10.6% CAGR through 2026-2031.

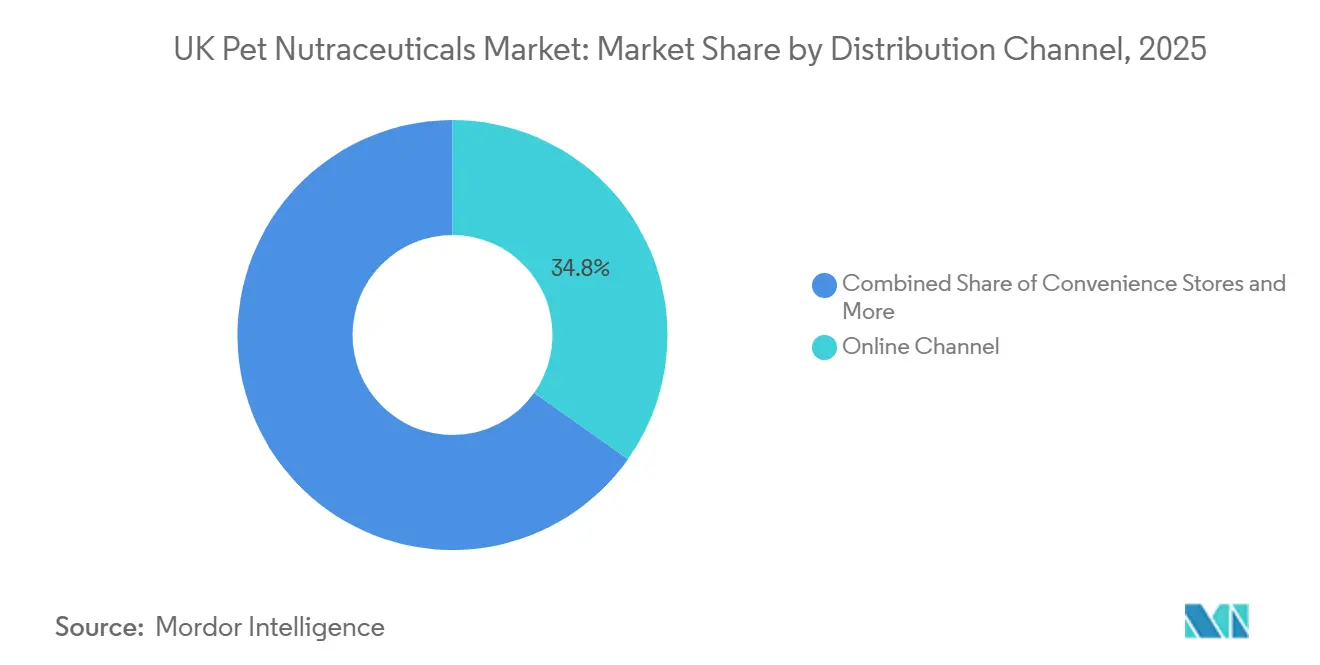

- By distribution channel, the online channel held 34.8% share of the UK pet nutraceuticals market size in 2025, and its 11.2% forecast CAGR to 2031 makes it the fastest-growing distribution route.

- The UK pet nutraceuticals market is moderately concentrated, with leading companies such as Mars, Incorporated, Nestlé Purina PetCare (Nestlé S.A.), Vetoquinol SA (Soparfin SCA), Alltech, Inc., and Virbac SA, collectively accounting for a significant share of the market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet humanization and willingness to pay for premium health products | +1.1% | National, concentrated in Greater London, South East, and other urban centers | Medium term (2-4 years) |

| Growing veterinary recommendations of functional supplements | +0.7% | National, anchored by clinic density in England and Scotland | Short term (≤ 2 years) |

| Regulatory clarity on feed-material registration post-Brexit | +0.9% | National, with spillover into Northern Ireland under Windsor Framework | Medium term (2-4 years) |

| Cold-extrusion technology protecting probiotic viability | +0.7% | National, early manufacturing hubs in East Midlands and Yorkshire | Long term (≥ 4 years) |

| E-commerce and subscription models are expanding access | +1.0% | National, highest penetration in England and Wales | Short term (≤ 2 years) |

| Veterinary clinic data analytics enabling personalized nutraceutical regimens | +0.5% | National, piloted inside corporate clinic chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Willingness to Pay for Premium Health Products

Pet owners increasingly view supplements as essential rather than elective, guided by wellness routines they establish for themselves. Pet care is a thriving industry in the United Kingdom, experiencing consistent year-on-year growth. According to the Office for National Statistics, expenditure on pets and related products reached USD 16.01 billion in 2024, up from USD 11.66 billion in 2021[1]Source: Office for National Statistics, "Consumer spending on pets and related products in the United Kingdom (UK)," ons.gov.uk. Higher disposable income in urban clusters underpins strong demand for immunity and longevity claims. Brands pairing subscription discounts with clear efficacy messaging overcome price sensitivity, locking in recurring revenue. Because this demographic researches ingredients online before purchase, clinically referenced website content outperforms generic lifestyle marketing.

Growing Veterinary Recommendations of Functional Supplements

The majority of pet owners continue to purchase at least one medication directly from veterinary clinics, highlighting the significant role veterinarians play in influencing purchasing decisions. Clinics that integrate supplements into their wellness plans report attach rates exceeding 1/3 of all patients, ensuring a consistent, predictable demand for products such as hip-and-joint supplements, digestive aids, and multivitamins. The publication of randomized clinical trials on bioactive collagen peptides and cyanocobalamin has further strengthened prescribers' confidence in recommending these products. However, professional organizations, including the British Veterinary Association (BVA), are increasingly advocating for more stringent monitoring of adverse events. This push for enhanced surveillance suggests that mandatory post-marketing data collection requirements may soon be implemented to ensure greater safety and efficacy of these products.

Regulatory Clarity on Feed-Material Registration Post-Brexit

The Veterinary Medicines Directorate (VMD) has introduced a practical roadmap to reduce regulatory burdens for well-characterized additives. This roadmap removes the need for renewal obligations and allows manufacturers to submit dossiers supported by peer-reviewed publications. As a result, compounds such as butylated hydroxyanisole and zinc amino-acid chelates can now reach the market in as little as twelve months, compared to the multiple years previously required. Although dual-compliance requirements in Northern Ireland still require additional administrative effort, the streamlined process in Great Britain significantly reduces the primary barriers to innovation costs. This change enables manufacturers to reallocate resources toward clinical validation, thereby fostering a more efficient product development pathway.

E-Commerce and Subscription Models are Expanding Access

E-commerce and subscription models are expanding access to pet nutraceuticals across the United Kingdom by improving convenience, personalization, and recurring delivery for frequently replenished supplements. Preliminary industry estimates indicate that online retail shipment volumes grew at a double-digit rate in late 2025, supported by expansion in pet care subscriptions and automated replenishment services. Algorithm-driven recommendations, automated refills, and price-lock mechanisms are increasing customer retention while helping mitigate cost sensitivity toward premium formulations such as omega-3 oils and probiotics, reinforcing the structural shift toward digital purchasing channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent European Union labeling and health-claim rules | -0.7% | National, amplified in Northern Ireland under Windsor Framework | Medium term (2-4 years) |

| Inflationary raw-material and fish-oil price volatility | -1.1% | National, tied to North Atlantic and Pacific fisheries | Short term (≤ 2 years) |

| Limited clinical evidence for novel botanicals in companion animals | -0.5% | National, impeding herbal formulations | Long term (≥ 4 years) |

| Shelf-life instability in probiotic soft chews | -0.6% | National, particularly in ambient-storage retail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent European Union Labeling and Health-Claim Rules

The retention of Regulation 767/2009 requires that all functional claims be substantiated by comprehensive, costly dossiers submitted to the European Food Safety Authority (EFSA)[2]Source: European Food Safety Authority, "Scientific Opinion on Lactoferrin Safety," efsa.onlinelibrary.wiley.com. This financial burden often deters smaller companies from incorporating botanicals such as turmeric and chamomile into their products, as the expense of registering even a single ingredient can be substantial. Additionally, the mandatory regulatory alignment in Northern Ireland adds further complexity for brands engaged in cross-border shipping, creating additional logistical and compliance challenges. While upcoming reforms by the Food Standards Agency (FSA) are projected to simplify the renewal process for established active ingredients, they are not designed to accelerate the approval of new or innovative compounds. As a result, the development of herbal product pipelines remains constrained, limiting opportunities for innovation in this segment.

Limited Clinical Evidence for Novel Botanicals in Companion Animals

Peer-reviewed evidence supporting the safety and efficacy of veterinary botanicals lags significantly behind that for human applications. Ingredients such as curcumin, green tea catechins, and valerian root are commonly included in product formulations, but dose standardization remains inconsistent. Veterinarians are often reluctant to recommend botanical products due to the lack of robust clinical data, compounded by the British Veterinary Association's concerns regarding underreporting of adverse events. Regulatory bodies like the Veterinary Medicines Directorate (VMD) mandate pharmacovigilance systems for medicated feeds, but over-the-counter nutraceuticals are subject to less stringent oversight, creating a quality assurance gap. Brands that invest in independent clinical trials and publish findings in peer-reviewed journals can enhance their credibility, though the return on such investments is typically realized over a 3 to 5-year horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Vitamins and Minerals Anchor Category Leadership

Vitamins and minerals are the largest sub product, accounting for 26.4% of the UK pet nutraceuticals market size in 2025, and are growing fastest at a 10.4% CAGR through 2026-2031, with organic selenium and carotenoid blends driving double-digit unit growth. Veterinary confidence in micronutrient science underpins the inclusion of multivitamins in clinic wellness plans, creating predictable reorder cycles. Oral cyanocobalamin formats proved bioequivalent to injections, increasing owner acceptance. Dog formulations account for the bulk of revenue due to larger dose requirements per kilogram of body weight.

Omega-3 oils and probiotics follow as significant share contributors but wrestle with cost and stability pressures. Milk bioactives, including lactoferrin and bovine colostrum, have shown potential in canine studies. A 40-week trial reported enhanced fecal immunoglobulin A levels and increased microbiota diversity. High ingredient costs and limited consumer awareness constrain commercial adoption. Proteins and peptides, such as bioactive collagen, have attracted attention for their benefits, with a 12-week study demonstrating improvements in gait and quality of life in 31 dogs. Other nutraceuticals, such as botanicals and joint-support compounds, face challenges due to strict European Union health-claim regulations, which require substantiation dossiers that many herbal ingredients fail to meet.

By Pets: Dogs Demand Dominates while Cats Growth Accelerates

Dogs are the largest animal segment and accounted for 54.3% of the UK pet nutraceuticals market share in 2025, driven by higher body weight and frequent vet visits. In 2024, the United Kingdom's dog population was estimated at 13.5 million, with 36% of households owning a dog. This significant population is a key driver of the growing, premium-focused pet nutraceuticals market. The industry is being propelled by the "pet humanization" trend and pandemic-era adoptions, leading to increased spending on health-focused supplements for mobility and anxiety relief[3]Source: UK Pet Food, "UK Pet Population," ukpetfood.org. Bioactive collagen peptides and large-breed joint formulas swell the average basket size. Corporate clinic packages that bundle canine supplements with diagnostics further cement category stickiness.

Cats, although smaller in absolute terms, will advance faster at a 10.6% CAGR to 2031 as taurine, phosphorus-balanced renal aids, and cobalamin products target species-specific gaps. Oral formats lessen clinic stress for felines, improving compliance. Specialized formulas now include stress-reduction actives and hairball-control prebiotics, broadening application occasions beyond core nutrition.

By Distribution Channel: Online Channel Captures Subscription Loyalty

The online channel is the largest distribution channel, capturing 34.8% of the UK pet nutraceuticals market in 2025 and posting an 11.2% CAGR through 2031. Algorithmic storefronts and automated replenishment services increase customer lifetime value and reduce out-of-stock risk. Veterinary prescription fee caps lower barriers to switching to online chemists, further fueling the channel shift. The online channel's ability to aggregate long-tail SKUs, provide personalized recommendations via algorithms, and secure recurring revenue through subscription models positions it as a key driver of structural growth.

Specialty stores and supermarkets remain relevant due to in-person consultations and impulse purchases, though their growth lags behind that of digital channels. Specialty retailers provide curated product assortments and staff expertise, attracting pet owners who require guidance on complex formulations. Supermarkets and hypermarkets, on the other hand, offer convenience for purchasing commodity supplements like multivitamins. Convenience stores hold a minimal market share due to limited shelf space and lower foot traffic for pet-specific products. Other channels, such as veterinary clinics, continue to play a significant role, as the United Kingdom's pet owners frequently purchase medicines directly from these practices, highlighting the channel's gatekeeping influence.

Geography Analysis

England holds a significant share of the UK pet nutraceuticals market, largely due to its dense populations and higher disposable incomes, particularly in areas such as Greater London and the South East. Urban millennials in these regions are strongly focused on preventive health measures for their pets and are quick to adopt subscription-based programs for convenience and consistency. Additionally, these areas benefit from advanced digital infrastructure, which supports higher online engagement and facilitates one-day shipping services through major fulfillment hubs, further enhancing accessibility and consumer satisfaction.

Scotland and Wales contribute smaller absolute revenue but exhibit robust mid-single-digit volume uplift, propelled by higher rural pet ownership. Veterinary clinic density in regional towns provides repeated touchpoints for supplement counseling. Country-level government initiatives on animal welfare have amplified media visibility for preventative care, indirectly stimulating nutraceutical adoption.

Northern Ireland faces unique dual compliance with European Union regulations, which adds to formulation and labeling complexity. However, its strategic position for cross-border trade into the Republic of Ireland entices suppliers who can navigate both regimes. Growth in the province remains slightly below the national average but offers a staging ground for pan-island launches once dossiers satisfy European Food Safety Authority scrutiny.

Competitive Landscape

The UK pet nutraceuticals market exhibits moderate concentration, with the top companies, including Mars, Incorporated, Nestlé Purina PetCare (Nestlé S.A.), Vetoquinol SA (Soparfin SCA), Alltech, Inc., and Virbac SA, accounting for a significant market share in 2025. The companies leverages integrated portfolios spanning therapeutic diets and medicines, creating systemic switching costs for clinics. Companies embed artificial intelligence into their veterinary practice networks, locking in data-driven supplement protocols. Nestlé Purina PetCare’s forthcoming precision-nutrition research center, slated for 2026, complements its pet food franchise and shores up scientific credentials.

Mid-tier companies such as Elanco Animal Health Incorporated and Archer Daniels Midland Company focus on differentiation through product launches and technological advancements. In February 2025, Elanco Animal Health Incorporated introduced Pet Protect, a new range of veterinarian-formulated, science-backed, and National Animal Supplement Council (NASC) approved supplements for dogs and cats. Drawing on 25 years of expertise with the Advantage brand, this portfolio offers targeted solutions for joint health, skin, digestion, and stress management, distributed through veterinary channels and retail partners. Archer Daniels Midland Company has enhanced product quality through cold-extruded probiotics, ensuring more accurate label claims. DSM-Firmenich AG's 2024 collaboration with NutriLeads on the Benicaros prebiotic highlights the potential of innovative ingredients to establish premium market segments.

Emerging disruptors are utilizing subscription models, first-party data, and personalized nutrition algorithms to bypass traditional retail and veterinary intermediaries. Direct-to-consumer brands are establishing feedback mechanisms to enhance customer compliance and lifetime value. The Veterinary Medicines Regulations 2024 have introduced stricter advertising standards and pharmacovigilance reporting requirements. These changes pose challenges for smaller entrants without in-house regulatory teams but also present opportunities for brands that invest in clinical trials and publish their findings in peer-reviewed journals.

UK Pet Nutraceuticals Industry Leaders

-

Mars, Incorporated

-

Nestlé Purina PetCare (Nestlé S.A.)

-

Alltech, Inc.

-

Vetoquinol SA (Soparfin SCA)

-

Virbac SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Zooomy, a veterinary-developed joint supplement brand, has introduced a new affiliate program tailored for pet professionals such as trainers, behaviorists, and physiotherapists. The program aims to offer a low-barrier revenue opportunity for small pet businesses facing rising operational expenses.

- August 2025: Omni Pet, a United Kingdom-based vegan dog food startup, has launched LeanPaws, a plant-based, drug-free weight-loss supplement for dogs. This product is designed to replicate the effects of the human GLP-1 hormone and was previously referred to as "Pawzempic."

- July 2025: LitPet has introduced a range of premium dog supplements inspired by Traditional Chinese Medicine (TCM) and supported by scientific research. Manufactured in the United Kingdom, the product line includes four powders including Pawsitive Powder for stress management, CardioPlus for heart health, ImmunoPro for immunity support, and Body Balance for overall wellbeing.

- February 2025: Elanco Animal Health Incorporated launched Pet Protect, a range of veterinarian-formulated supplements for dogs and cats. The product is positioned as a science-based supplement line tailored to address pets' varied health needs.

UK Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are bioactive, nutrient-derived compounds, including supplements, herbs, probiotics, and fatty acids, formulated to enhance health, prevent diseases, and support organ function in dogs and cats beyond basic nutrition. These products are commonly used to manage joint health, improve skin and coat condition, and support gut health.

The UK Pet Nutraceuticals Market Report is segmented by sub-product, including milk bioactives, omega-3 fatty acids, probiotics, proteins and peptides, vitamins and minerals, and other nutraceuticals, by pets including cats, dogs, and other pets, and by distribution channel, including convenience stores, online channel, specialty stores, supermarkets and hypermarkets, and more. The market forecasts are provided in terms of value in USD and volume in metric tons.

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms