United States Agricultural Sprayers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

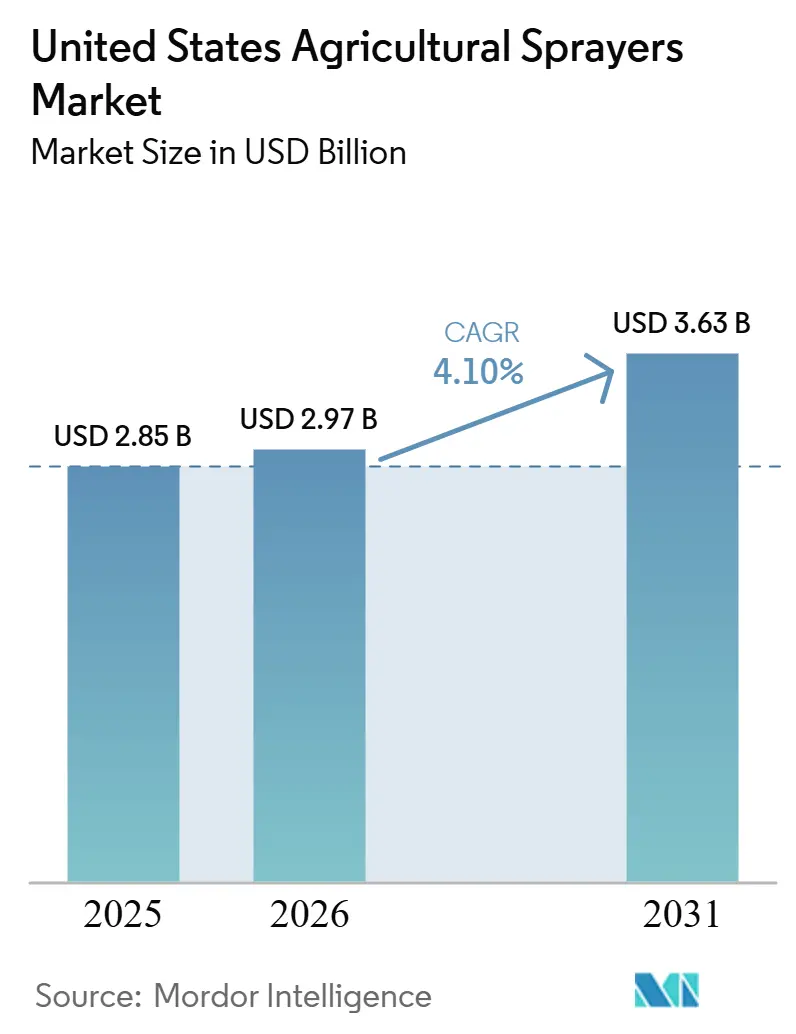

| Base Year Market Size (2025) | USD 2.85 Billion |

| Market Size (2026) | USD 2.97 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

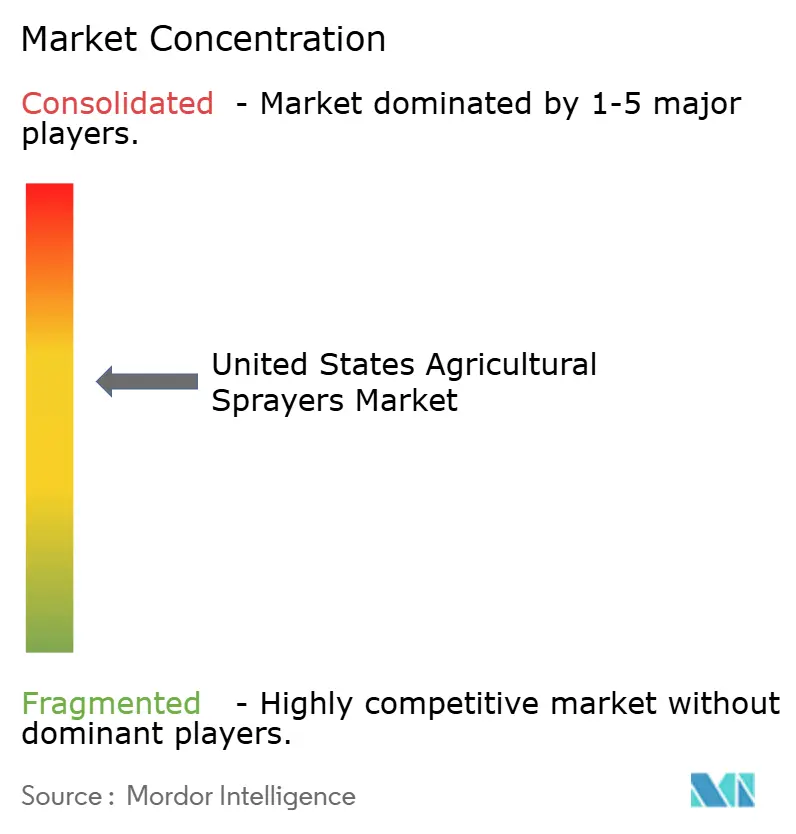

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Agricultural Sprayers Market Analysis by Mordor Intelligence

The United States agricultural sprayers market size was valued at USD 2.85 billion in 2025 and is estimated to grow from USD 2.97 billion in 2026 to reach USD 3.63 billion by 2031, at a CAGR of 4.10% during the forecast period (2026-2031). The market remains supported by a stable row-crop base, sustaining core spraying demand despite increasingly selective farm purchasing decisions. Market growth is transitioning from replacement demand to technology-driven investments, particularly in precision software, retrofit kits, and application systems designed to enhance compliance documentation and minimize chemical usage. Labor shortages are further driving the adoption of higher-throughput and operator-light equipment. The increased reliance on the H-2A Temporary Agricultural Program, due to limited domestic labor availability, has made automation economically advantageous for growers across various crop systems. Additionally, Environmental Protection Agency (EPA) regulations are intensifying the focus on drift control, nozzle management, and application recordkeeping, influencing equipment purchasing decisions. As a result, while demand in the United States agricultural sprayers industry continues to stem from broad-acre agriculture, value growth is increasingly linked to precision technologies, autonomous functionalities, and upgrade opportunities within the existing equipment fleet.

Key Report Takeaways

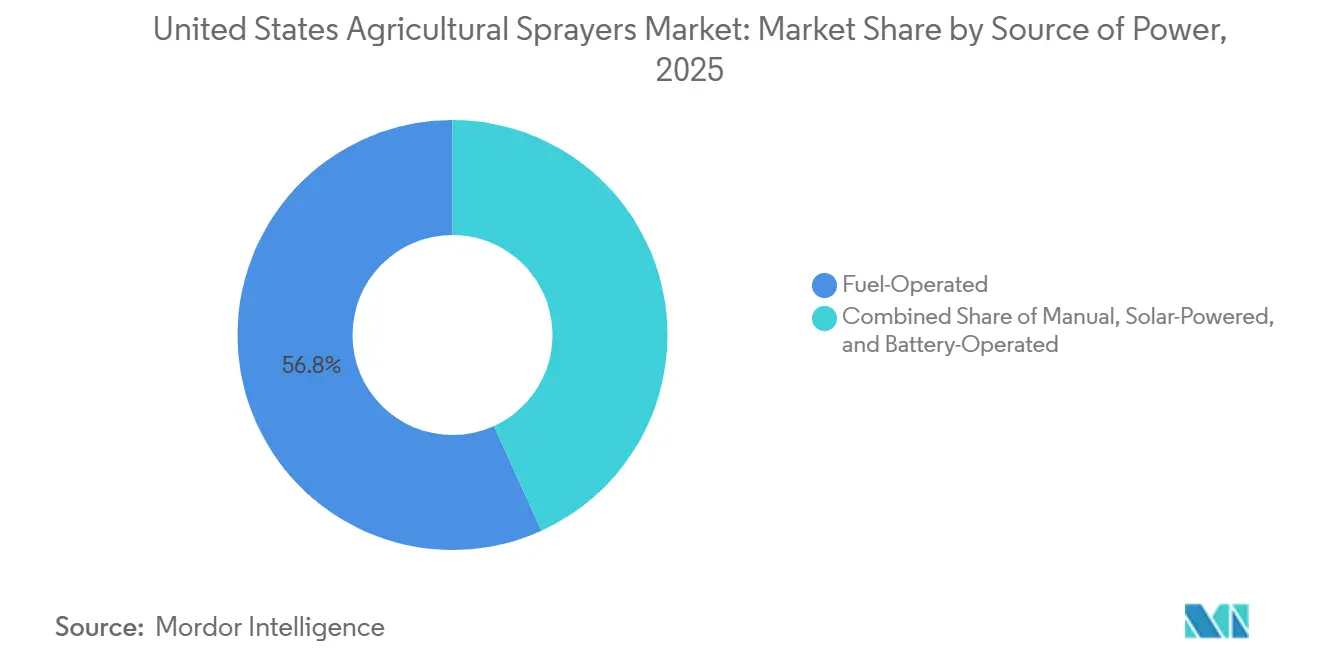

- By source of power, fuel-operated sprayers held 56.8% of revenue in 2025, while battery-operated sprayers are projected to expand at a 17.9% CAGR through 2031.

- By product type, self-propelled sprayers accounted for 55.0% of the United States agricultural sprayers market size in 2025, while unmanned aerial vehicle sprayers are forecast to grow at a 20.2% CAGR through 2031.

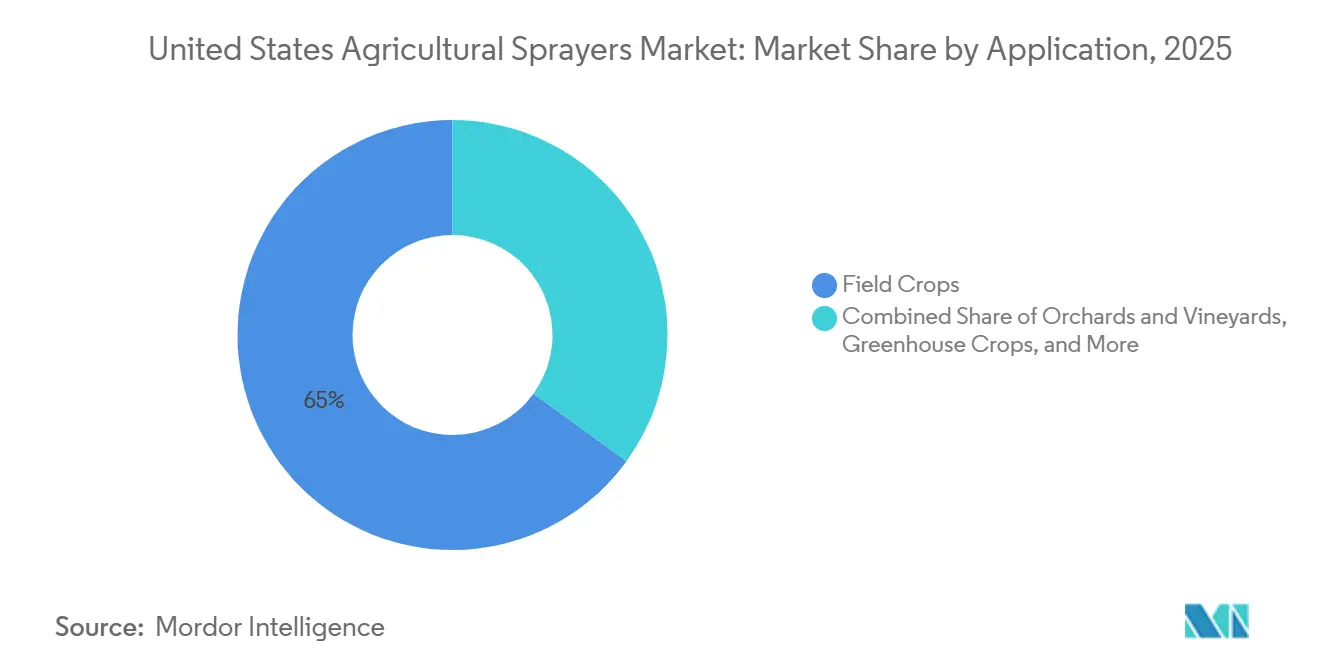

- By application, field crops captured 65.0% of the United States agricultural sprayers market share in 2025, while orchards and vineyards are projected to grow at a 5.8% CAGR through 2031.

- By spray volume capacity, high-volume sprayers accounted for 49.0% of the United States agricultural sprayers market in 2025, while ultra-low-volume sprayers are the fastest-growing sub-segment, with a 7.5% CAGR through 2031.

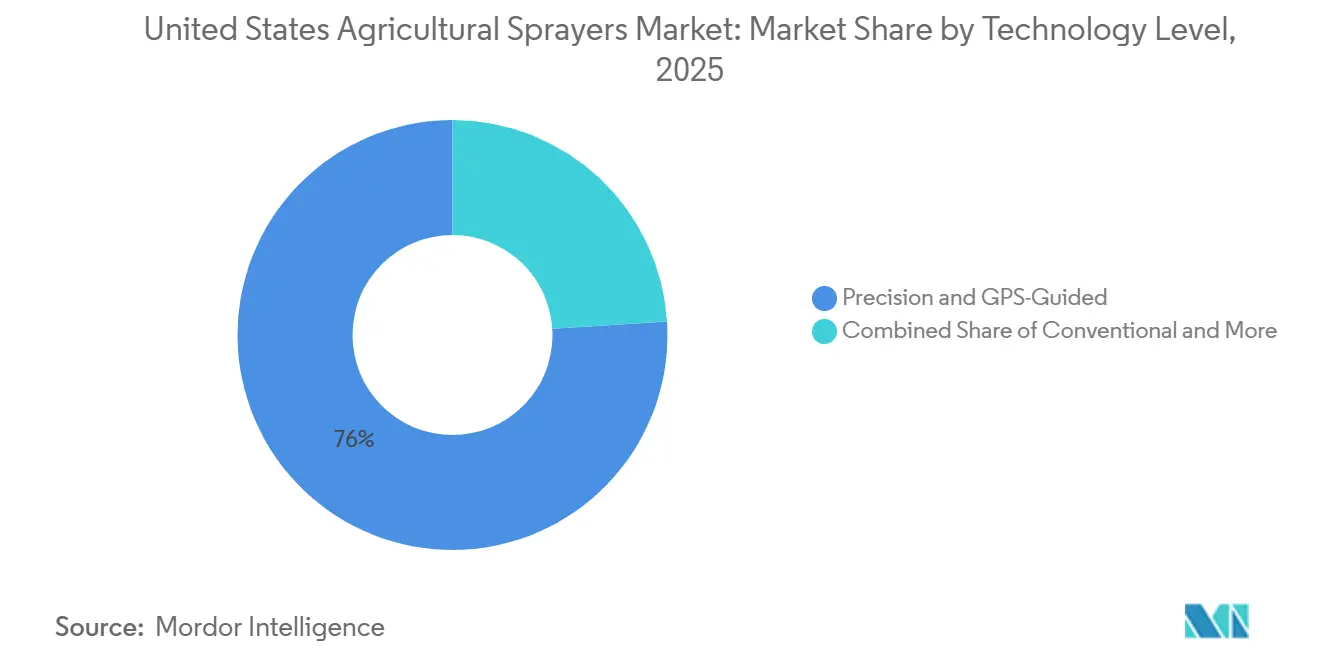

- By technology level, precision and GPS-guided sprayers held the largest share of 76.0% in 2025, while artificial intelligence-enabled and autonomous systems are expanding the fastest through 2031 with a CAGR of 9.8%.

- By pump mechanism, centrifugal pumps held 46.0% share of the United States agricultural sprayers market share in 2025, while diaphragm pumps are projected to grow at a 9.5% CAGR through 2031.

- Deere and Company, CNH Industrial N.V., AGCO Corporation, EXEL Industries, and Equipment Technologies, Inc. held a significant combined share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Agricultural Sprayers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Broad-acre corn and soybean spray intensity | +1.2% | National, with highest intensity in Iowa, Illinois, Indiana, Minnesota, and Nebraska | Long term (≥ 4 years) |

| Precision input savings and selective spraying ROI | +0.8% | National, strongest in the Corn Belt and Delta row-crop regions | Medium term (2-4 years) |

| Farm labor scarcity and operator productivity needs | +0.6% | National, with acute pressure in California, Florida, and Pacific Northwest specialty-crop corridors | Medium term (2-4 years) |

| EPA mitigation and drift-control compliance | +0.4% | National, with stronger impact in areas near endangered-species habitats | Short term (≤ 2 years) |

| Orchard and vineyard autonomy adoption | +0.4% | California Central Valley, Pacific Northwest, and New York wine-grape belt | Medium term (2-4 years) |

| Retrofit economics for installed sprayer fleets | +0.3% | National, especially in Corn Belt dealer territories with dense installed bases | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Broad-Acre Corn and Soybean Spray Intensity

The United States agricultural sprayers market still depends heavily on the scale and intensity of corn and soybean production. A broad and active row-crop base continues to support spraying demand, with corn covering around 33.8 million hectares and soybean cultivation reaching about 35.1 million hectares across major farming states[1]Source: FAOSTAT, “Crop Production Data,” FAOSTAT, faostat.fao.org. That acreage base supports repeated in-season applications, and the equipment used in those windows often operates near full utilization during peak periods. The real demand signal is not acreage alone, because many farms still run multiple passes through a season as weed pressure and crop protection schedules require. That raises wear on booms, pumps, controls, and guidance systems, which supports both replacement demand and upgrade demand. Resistance management adds to this pattern because problem weeds increase the need for better timing and better application quality. Consequently, the market maintains a stable demand for large-tank self-propelled and trailed machines, even during periods of reduced grower confidence.

Precision Input Savings and Selective Spraying Return on Investment (ROI)

Selective spraying has become one of the clearest value drivers in the United States agricultural sprayers market. John Deere reported that growers used See and Spray technology across more than 5 million acres in 2025, with average savings of nearly 50% on non-residual herbicide costs and 31 million gallons of herbicide mix avoided during the season[2]Source: John Deere, “See and Spray Technology Across Five Million Acres in 2025,” Deere, deere.com. Those savings change the purchase decision because growers can now tie equipment upgrades to direct operating cost reductions rather than relying solely on labor savings or yield protection. Precision systems also help maintain performance on irregular field boundaries and mixed-pressure weed environments where blanket application is less efficient. The benefit is growing because label restrictions are becoming stricter and more documentation-heavy. EPA’s dicamba framework underscores the importance of drift-reduction agents and application discipline, making nozzle-level control and boom automation even more valuable in daily field practice. As a result, the market is rewarding machines and retrofits that can deliver both measurable input savings and cleaner compliance records.

Farm Labor Scarcity and Operator Productivity Needs

Labor scarcity is pushing growers toward equipment that can cover more area with fewer workers in the United States agricultural sprayers industry. The American Farm Bureau Federation has highlighted a significant gap between the demand for agricultural labor and the availability of domestic workers, reinforcing the need for more efficient and automated spraying solutions. This gap matters because spraying is time sensitive, and delays during narrow weather windows can reduce the value of every other input on the farm. Larger self-propelled sprayers help by extending the acreage covered per shift, while autonomous orchard units and remote supervision systems reduce the number of people needed in repetitive routes. Specialty crops feel the pressure even more because labor dependency is higher and the cost per missed operation is greater. That is why autonomous spraying is moving faster in orchards, vineyards, and high-value produce than in many row-crop settings. The market is therefore benefiting from a structural labor imbalance unlikely to ease soon.

Environmental Protection Agency (EPA) Mitigation and Drift-Control Compliance

EPA compliance is turning application hardware into a practical requirement in the agricultural sprayers market. The Herbicide Strategy and the mitigation menu now require applicators near listed-species habitats to choose and document drift-reduction measures, a task that is easier to manage with modern controls than with manual methods. This favors sprayers with boom-height control, section control, telematics, and application logging. It also supports demand for nozzles, pump systems, and recordkeeping tools that can show how the application was made. Suppliers below the Original Equipment Manufacturer (OEM) layer benefit as much as full-machine manufacturers do because compliance depends on the entire delivery system. Recent efforts to modernize spray drift modeling highlight a broader shift toward precision-driven regulatory practices. In practical terms, the market is seeing compliance shift from a paperwork issue to an equipment specification issue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront machine and technology cost | -1.0% | National, most acute in smaller operations in the Midwest and mid-South | Long term (≥ 4 years) |

| Commodity-margin volatility delaying replacement cycles | -0.8% | National, concentrated in the corn and soybean belt | Medium term (2-4 years) |

| Tariff-driven component and steel cost inflation | -0.7% | National, with proportionally higher impact on domestically manufactured machines | Short term (≤ 2 years) |

| Battery runtime and charging constraints | -0.2% | National, most limiting in remote row-crop geographies with limited charging infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Machine and Technology Cost

High purchase costs remain a significant barrier to faster adoption in the United States agricultural sprayers market. Precision-equipped self-propelled machines often carry an additional cost compared to baseline configurations, which many mid-sized operations find challenging to afford, particularly when farm income is under pressure. This challenge is most pronounced among farms in acreage bands that could benefit substantially from selective spraying but face tighter financial constraints. The cost issue is further compounded by the expense of advanced technologies, such as sensing systems, machine vision, and software subscriptions, which increase the overall cost of ownership. A survey indicated that machine vision weed detection was implemented on only a small percentage of dealer-tracked custom acres, despite higher dealer intent to adopt the technology. This indicates that price resistance remains a significant factor at the farm level. While subscription models and retrofit kits help lower the initial cost barrier, they do not eliminate it. As a result, the market continues to experience a slower adoption rate in cases where the potential return on investment is strong, but the upfront capital requirement remains prohibitive.

Commodity-Margin Volatility Delaying Replacement Cycles

Commodity price pressures are lengthening replacement cycles in the United States agricultural sprayers market. When farm margins narrow, growers tend to delay significant equipment purchases, prioritizing maintenance or specific repairs instead. This approach reduces short-term new unit sales, even as equipment usage remains high. A cyclical decline in agricultural spraying activity has further encouraged cautious spending among farmers. In the United States, a similar pattern is evident, with large row-crop operators initially postponing replacements and later making concentrated purchases. This suggests that demand does not vanish but becomes harder to predict in terms of timing. As a result, the United States agricultural sprayer industry faces revenue risks when prolonged periods of low commodity prices defer fleet renewal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Power: Electrification Creating Two-Speed Market Dynamics

Fuel-operated sprayers held 56.8% of revenue in 2025, which kept them as the largest power source in the United States agricultural sprayers market. Their lead comes from the basic needs of large-acre row-crop farming, where long range, high tank capacity, and uninterrupted operating windows matter more than fuel savings. Large self-propelled units in the Corn Belt still depend on diesel power because they must sustain coverage across large fields without stopping for recharge. Manual and solar-powered systems remain in place, but they serve much narrower roles on small holdings, in greenhouse settings, and in specialty use cases.

Battery-operated systems are projected to be the fastest-growing power source, advancing at a 17.9% CAGR through 2031 in the United States agricultural sprayers industry. Growth is strongest in Unmanned Aerial Vehicle (UAV) sprayers and in greenhouse or orchard robots, where short routes and lower noise levels make electrification practical. The emergence of smart battery-powered backpack sprayers highlights how suppliers are developing a premium battery segment even within handheld equipment. Even so, large-acre electrification still faces a hard limit because cycle time and charging constraints do not align with the tight spray windows common in row crops. The United States agricultural sprayers industry is therefore moving toward a split model where battery growth is strong in smaller and more precise formats, while fuel-powered machines remain the operating backbone for farm-scale field spraying.

By Product Type: Self-Propelled Strength and UAV Disruption

Self-propelled sprayers accounted for 55.0% of product-type revenue in 2025, giving them the leading position in the United States agricultural sprayers market. Their scale advantage reflects the country’s bias toward high-clearance, large-tank machines that can move quickly across broad-acre farms during narrow spray windows. The segment remains central in the Midwest and Plains, where farmers prioritize acres covered per day, consistent field speed, and compatibility with precision systems.

UAV sprayers are the fastest-growing product segment, with a 20.2% CAGR through 2031 in the United States agricultural sprayers market. Their growth is attributed to their effectiveness in hard-to-access terrain, specialty crops, and targeted spot-treatment applications, where conventional equipment proves less efficient. However, recent regulatory measures targeting foreign-manufactured drones have created uncertainty in supplier dynamics, particularly due to the significant presence of certain global brands in the United States market. This development presents opportunities for domestic manufacturers and alternative suppliers but also introduces risks to this rapidly evolving segment. In contrast, tractor-mounted, trailed, and handheld sprayers remain essential, catering to more stable and cost-sensitive applications compared to the dynamic UAV category.

By Application: Field Crops Holding Scale While Orchards and Vineyards Pull Technology

Field crops represented 65.0% of application demand in 2025, which gave them the largest role in the United States agricultural sprayers industry. Corn, soybeans, wheat, and cotton create a large installed base because dealer networks, custom application fleets, and agronomy support are all built around row-crop geographies. This application base keeps demand broad even when individual farm purchasing cycles fluctuate. EPA drift-control and recordkeeping rules are also affecting this segment because compliance standards now shape sprayer specifications more directly than before[3]Source: U.S. Environmental Protection Agency, “Strategy to Protect Endangered Species From Herbicides,” epa.gov.

Orchards and vineyards are the fastest-growing application category, with a 5.8% CAGR through 2031. Their growth reflects strong labor pressure, high per-acre crop value, and a better economic fit for autonomous equipment. Greenhouse crops, turf, and gardening remain smaller, but they are important for battery systems and precise, low-volume delivery formats. The market is therefore seeing steady volume remain with field crops while premium technology adoption moves faster in specialty agriculture.

By Spray Volume Capacity: High Volume in Broad Acres and Ultra-Low Volume in Precision Niches

High-volume sprayers accounted for 49.0% of the United States agricultural sprayers market share in 2025, maintaining their position as the largest spray volume category . These systems align with the operational needs of large row-crop farms by minimizing refill stops and enhancing field efficiency during peak spraying periods. Tanks with capacities ranging from 800 to 1,250 gallons cater to farms seeking extended operating cycles with fewer interruptions. Meanwhile, low-volume systems continue to play a significant role in specialty crops and mid-scale operations where full high-volume capacity is not required.

Ultra-low-volume systems represent the fastest-growing segment, with a 7.5% CAGR between 2026 and 2031, despite a smaller demand base than high-volume machines. This growth is driven by advancements in spot-spraying and drone technologies that apply chemicals only where necessary. For instance, Verdant Robotics expanded the commercial availability of its SharpShooter system in May 2025, reporting up to a 96% reduction in chemical inputs for specialty-crop applications[4]Source: Verdant Robotics, “Verdant Robotics Expands Commercial Availability,” verdantrobotics.com. This trend is particularly pronounced in vegetables, fruits, and other high-value crops, where input savings can be clearly quantified on a per-acre basis. Consequently, the market is delivering value across the spectrum, with high-volume systems addressing large-scale operations and ultra-low-volume platforms focusing on precision applications.

By Technology Level: Precision and GPS-Guided Systems as the Base, Artificial Intelligence-Enabled and Autonomous Segment as the Growth Layer

Precision and GPS-guided systems are the largest technology category, accounting for a 76% of the United States agricultural sprayers market size in 2025. This adoption indicates that precision application is no longer limited to large-scale operators but is becoming a standard feature in many professional spraying fleets. While conventional systems are still used in older or smaller fleets, the market has increasingly shifted toward guidance systems, section control, and variable-rate capabilities.

AI-enabled and autonomous systems are the fastest-growing tier in the United States agricultural sprayers market, with a CAGR of 9.8% during the forecast period (2026-2031). Leading OEMs are introducing advanced sensing and application platforms that enable real-time detection and targeted spraying, reflecting a shift toward machine-led detection and response rather than basic guidance support. At the same time, regulatory pressure is increasing the importance of logged and controlled applications, while the addressable crop base continues to widen, making AI-driven features more relevant across a broader range of agricultural use.

By Pump Mechanism: Centrifugal Pumps Lead Volume While Diaphragm Pumps Gain Growth

Centrifugal pumps held 46.0% share in 2025 and remained the main pump type in the United States agricultural sprayers market. Their position comes from high-flow performance, lower maintenance, and a strong fit with large-tank self-propelled sprayers in row-crop use. Piston pumps still serve specific high-pressure applications, especially in orchard mist systems and other targeted spray tasks. The installed base of broad-acre equipment continues to favor centrifugal systems because they match the speed and volume needs of large field operations.

Diaphragm pumps are the fastest-growing pump category, with a 9.5% CAGR through 2031 in the United States agricultural sprayers industry. Their growth is closely tied to UAV sprayers and spot-spray platforms where smaller chemical volumes and variable operating pressures are common. Innovations in pump and nozzle-control systems highlight how fluid delivery is increasingly merging with precision application logic. This shift is important because performance is no longer judged only by flow, but also by how effectively the system integrates with smart controls, resulting in a market where centrifugal pumps still hold the largest installed base while diaphragm designs gain traction in emerging precision-driven formats.

Geography Analysis

The United States agricultural sprayers market operates on a national scale, with demand intensity varying significantly by region. The Midwest remains the largest demand center, driven by the region's extensive corn and soybean acreage, large farm sizes, and a dense dealer network. States such as Iowa, Illinois, Indiana, Minnesota, and their neighbors host the highest concentration of self-propelled, high-volume, fuel-operated sprayers. Farms in this area often span large acreages, ensuring high equipment utilization during narrow spraying windows. Retrofit demand is particularly prominent in this region, as many fleets already possess the chassis and hydraulic capacity for precision upgrades but lack advanced sensing and application technologies.

The Great Plains region follows a similar broad-acre logic, with an additional emphasis on wheat-driven spray demand in states like Kansas, Nebraska, and the Dakotas. These states continue to support large-field equipment and require high-throughput operations. Across both the Midwest and the Great Plains, the market favors original equipment manufacturers (OEMs) with robust dealer networks, comprehensive parts coverage, and reliable in-season service. Companies such as Deere and Company, CNH Industrial N.V., and AGCO Corporation benefit from this structure, as uptime is as critical as pricing in large-acre spraying operations. These regions are also pivotal for the next wave of retrofit adoption, with dealer-tracked acres already showing significant precision control adoption and a growing pipeline for machine vision enhancements.

The Pacific Coast and other specialty-crop regions, while smaller in terms of unit volume, exert a significant influence on premium technology demand within the market. California leads this trend due to labor shortages, high-value crops, and fixed orchard layouts, which make autonomous and AI-guided spraying more justifiable. The Southeast and Delta regions add a smaller but strategically important layer to the market, driven by crops such as citrus, cotton, peanuts, and soybeans. Challenges like herbicide resistance, canopy treatment requirements, and UAV use cases are accelerating the adoption of specialized systems in these areas. While these regions do not match the Midwest in terms of installed volume, they contribute significantly to the fastest-growing market segments and premium pricing trends through the forecast period.

Competitive Landscape

The United States agricultural sprayers market is moderately concentrated. Deere and Company, CNH Industrial N.V., AGCO Corporation, EXEL Industries, and Equipment Technologies, Inc. together held a significant market share in 2025, which gave the leading group clear scale advantages in product reach, dealer support, and installed fleet access. Even so, competition below the top tier is fragmented because autonomy providers, retrofit specialists, and AI application companies are building positions that did not exist in the same form a few years ago. This mix gives the United States agricultural sprayers market both a stable OEM core and a more fluid technology layer.

The main competitive pattern is the move to integrate sensing, control, and application logic directly into machine platforms. John Deere rolled out See and Spray Gen 2 for its MY27 sprayers, expanding crop compatibility and pushing selective spraying deeper into mainstream equipment lines. It also strengthened its specialty-crop autonomy position by fully acquiring GUSS Automation in August 2025[5]Source: Purdue University survey via Global Ag Tech Initiative, “The 2025 CropLife Purdue Precision Adoption Survey,” globalagtechinitiative.com . These moves show that the market is no longer competing only on horsepower, tank size, or boom width.

A second layer of competition is forming around the cross-OEM precision application stack, particularly in nozzle-control and pulse-width modulation systems that can operate across multiple equipment platforms. This is significant because farms can now adopt precision capabilities through retrofit solutions without replacing entire machines. At the same time, newer entrants are adding pressure with per-acre or targeted specialty-crop models that lower the upfront cost of adoption. As a result, the market is being shaped by both large equipment manufacturers and the growing influence of independent application-technology providers.

United States Agricultural Sprayers Industry Leaders

Deere and Company

CNH Industrial N.V.

AGCO Corporation

EXEL Industries

Equipment Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Ecorobotix announced a USD 50 million investment to manufacture its ARA Ultra-High Precision Sprayer in Lyons, Kansas. This initiative will create 80 jobs in the United States and establish the company's first manufacturing presence in North America.

- March 2026: Nordson Corporation acquired CapstanAG Systems, Inc., strengthening its presence in the United States agricultural sprayers market by enhancing precision spraying capabilities. CapstanAG’s PinPoint III PWM system, compatible with major OEM platforms, improves spray accuracy and efficiency. This drives higher adoption of advanced sprayer technologies among farmers.

- January 2026: Deere and Company introduced See and Spray Gen 2 sprayers, which expanded precision spraying to more crops and doubled the addressable market. The addition of variable-rate technology and dual-tank configuration improves efficiency and supports herbicide-resistance management in a single pass.

United States Agricultural Sprayers Market Report Scope

Agricultural sprayers are equipment used to apply liquid substances such as pesticides, herbicides, fertilizers, and water to crops in a controlled manner. They play a critical role in crop protection, nutrient management, and irrigation. These sprayers are available in various types, ranging from manual handheld devices to advanced tractor-mounted and automated systems. Their design ensures efficient coverage, minimizing waste and enhancing agricultural productivity.

The United States Agricultural Sprayers Market is Segmented by Power Source (Manual, Battery-Operated, Solar-Powered, and Fuel-Operated), Product Type (Handheld, Tractor-Mounted, Trailed, Self-Propelled, and Unmanned Aerial Vehicle Sprayers), Application (Field Crops, Orchards and Vineyards, Greenhouse Crops, and Turf and Gardening), Spray Volume Capacity (Ultra-Low Volume, Low Volume, and High Volume), Technology Level (Conventional, Precision and GPS-Guided, and Artificial Intelligence-Enabled and Autonomous), and Pump Mechanism (Diaphragm Pumps, Piston Pumps, and Centrifugal Pumps). The Report Offers the Market Size and Forecasts in Terms of Value (USD).

| Manual |

| Battery-Operated |

| Solar-Powered |

| Fuel-Operated |

| Handheld |

| Tractor-Mounted |

| Trailed |

| Self-Propelled |

| Unmanned Aerial Vehicle Sprayers |

| Field Crops |

| Orchards and Vineyards |

| Greenhouse Crops |

| Turf and Gardening |

| Ultra-Low Volume |

| Low Volume |

| High Volume |

| Conventional |

| Precision and GPS-Guided |

| Artificial Intelligence-Enabled and Autonomous |

| Diaphragm Pumps |

| Piston Pumps |

| Centrifugal Pumps |

| By Source of Power | Manual |

| Battery-Operated | |

| Solar-Powered | |

| Fuel-Operated | |

| By Product Type | Handheld |

| Tractor-Mounted | |

| Trailed | |

| Self-Propelled | |

| Unmanned Aerial Vehicle Sprayers | |

| By Application | Field Crops |

| Orchards and Vineyards | |

| Greenhouse Crops | |

| Turf and Gardening | |

| By Spray Volume Capacity | Ultra-Low Volume |

| Low Volume | |

| High Volume | |

| By Technology Level | Conventional |

| Precision and GPS-Guided | |

| Artificial Intelligence-Enabled and Autonomous | |

| By Pump Mechanism | Diaphragm Pumps |

| Piston Pumps | |

| Centrifugal Pumps |

Key Questions Answered in the Report

Which product category leads demand in 2025?

Self-propelled sprayers lead demand with a 55.0% share in 2025 because large-acre United States farms still depend on high-clearance, high-capacity machines.

Which product category is growing the fastest through 2031?

The UAV sprayers category is the fastest-growing product segment at a 20.2% CAGR through 2031.

Why are precision and AI systems gaining ground so quickly?

Growers are responding to herbicide savings, tighter compliance needs, and labor scarcity. John Deere reported nearly 50% savings on non-residual herbicide costs across more than 5 million acres in 2025.

Which application area still drives most equipment demand?

Field crops remain the main demand base with 65.0% of application demand in 2025, supported by corn, soybean, wheat, and cotton acreage.

What is the 2026 value of the United States agricultural sprayers space?

It is estimated at USD 2.97 billion in 2026 and is forecast to reach USD 3.63 billion by 2031 at a 4.10% CAGR.

Page last updated on: