Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

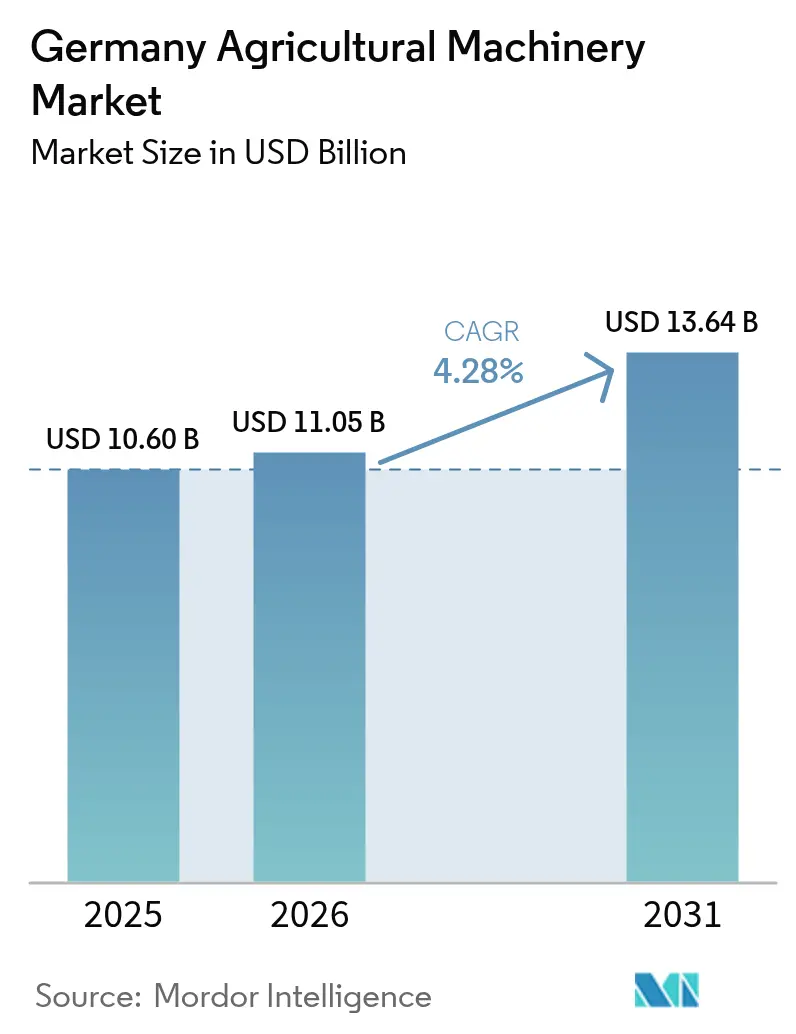

| Base Year Market Size (2025) | USD 10.60 Billion |

| Market Size (2026) | USD 11.05 Billion |

| Market Size (2031) | USD 13.64 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

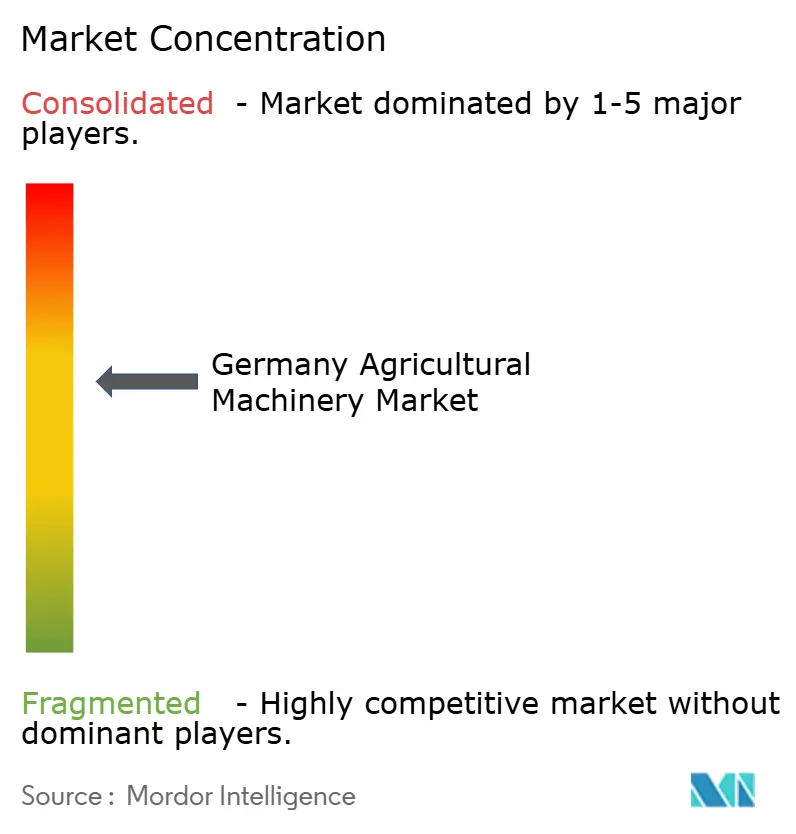

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Agricultural Machinery Market Analysis by Mordor Intelligence

The Germany agricultural machinery market size in 2026 is estimated at USD 11.05 billion, growing from 2025 value of USD 10.6 billion with 2031 projections showing USD 13.64 billion, growing at 4.28% CAGR over 2026-2031. Strong demand for tractors, rapid irrigation system uptake, and sustained subsidy inflows offset reduced equipment registrations and lower farm incomes. Farmers pivot toward precision and autonomous technologies to cope with labor shortages, regulatory emission targets, and climate-driven water stress. Manufacturers scale retrofit kits that embed ISOBUS compliance and smart-connected features, lowering barriers for aging machine fleets. OEMs (Original Equipment Manufacturers) also deploy creative finance models that smooth seasonal cash flows and mitigate high upfront costs. Meanwhile, policy incentives such as EUR 6.2 billion (USD 6.8 billion) in annual CAP transfers keep equipment investment resilient in the Germany agricultural machinery market amid volatile commodity prices.[1]Federal Ministry of Food and Agriculture (Germany) “Main features of the Common Agricultural Policy (CAP) and its implementation in Germany,” bmleh.de

Key Report Takeaways

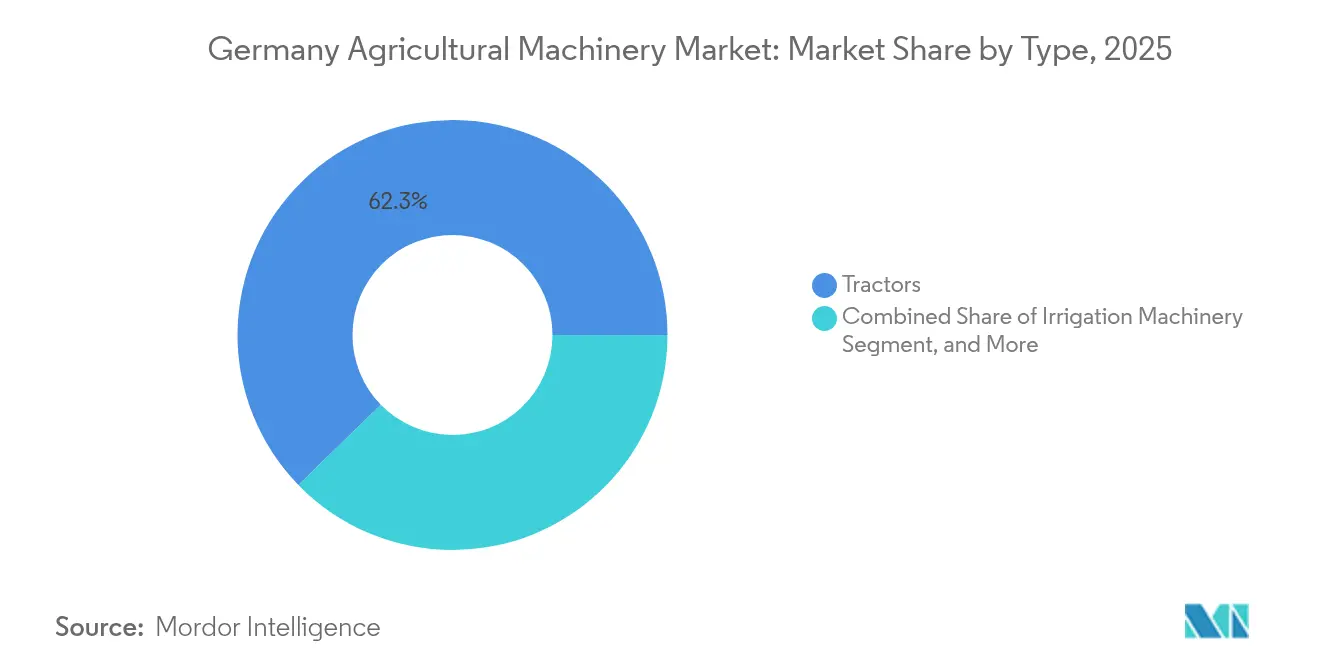

- By type, tractors led with 62.3% of the Germany agricultural machinery market share in 2025, and irrigation machinery shows a 6.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-workforce–driven Labor Scarcity | +1.2% | Rural regions nationwide | Medium term (2-4 years) |

| EU and Federal Subsidies for Precision-Machinery Purchases | +0.8% | Bavaria and Lower Saxony | Short term (≤ 2 years) |

| Rapid Adoption of Smart-connected Implements and ISOBUS Standards | +0.7% | Nationwide | Medium term (2-4 years) |

| Carbon-footprint Regulations Favoring Tier-V and Electric Tractors | +0.5% | Urban-adjacent farms | Long term (≥ 4 years) |

| Autonomous Multi-task Platforms Gaining Pilot Traction | +0.4% | Large-scale operations | Long term (≥ 4 years) |

| Suitable OEM Finance Models | +0.3% | Regions with varied credit access | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing-workforce driven Labor Scarcity

Germany's agricultural sector faces a significant labor shortage due to an aging workforce and limited interest among younger generations. As older farmers retire, hiring gaps widen, prompting a surge in mechanization and automation. Government initiatives support the deployment of mini-robots for targeted field tasks, reducing reliance on manual labor. Plug-and-play interfaces and retrofit kits allow older machinery to integrate with smart implements, making upgrades more accessible. This shift transforms the agricultural machinery market, with increased demand for autonomous solutions and adaptable technologies that maintain productivity across diverse farm sizes and crop types.

EU and Federal Subsidies for Precision-Machinery Purchases

Policy reforms at both the EU and federal levels are increasing investment in precision agriculture technologies across Germany. CAP reforms lift green premium payouts to 130% of the base rate, steering farmers toward precision sprayers and smart irrigation. Gas-oil tax relief of EUR 0.21480 per liter (USD 0.24) cuts running costs for high-tech tractors. State plans such as ILU 2023 add grants for emission-cutting machinery, supporting steady equipment turnover in the Germany agricultural machinery market.[2]Praxis Agrar, “GAP 2025 – Was ist neu?” praxis-agrar.deThis modernization of the agricultural machinery market aligns economic incentives with environmental goals and strengthens Germany's farming infrastructure.

Rapid Adoption of Smart-connected Implements and ISOBUS Standards

Germany's agricultural machinery market is advancing through the integration of smart-connected implements and standardized communication protocols. ISOBUS compliance across new equipment enables seamless data exchange between tractors and tools, simplifying operations and enhancing precision. Innovations in middleware and cloud connectivity enable real-time agronomic decision-making, reducing downtime and improving field efficiency. Manufacturers incorporate these technologies into their product lines, providing farmers with intuitive interfaces and scalable solutions. This digital transformation expands the installed base of precision-ready equipment, establishing Germany's position in smart farming and sustainable agricultural practices.

Carbon-footprint Regulations Favoring Tier-V and Electric Tractors

Stage V diesel limits tighten particulate and NOx thresholds. Fendt’s e100 Vario delivers 4–7 hours of clean operation on a 100 kWh battery, proving viable for municipal and livestock tasks.[3] AGCO, “Fully Electric Tractor: The Fendt e100 Vario,” news.agcocorp.com Weight-optimized harvesters like HOLMER’s Terra Dos 5 cut fuel burn by 20%, aligning with stricter CO₂ targets. These innovations reposition the Germany agricultural machinery market toward low-emission powertrains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Long Payback Period | -0.9% | National, more pronounced in smaller farms | Short term (≤ 2 years) |

| Cybersecurity and Data Ownership Concerns in Digitally Enabled Fleets | -0.6% | National, concentrated in tech-advanced operations | Medium term (2-4 years) |

| Margin Pressure from Falling Commodity Prices and Volatile Energy Costs | -0.7% | National, with regional variations based on crop mix | Short term (≤ 2 years) |

| Regulatory Uncertainty over Pesticide Reduction and Nitrogen Caps | -0.5% | National, with higher impact in intensive crop regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Long Payback Period

The high capital cost of advanced agricultural machinery continues to challenge German farmers, particularly those operating smaller farms. Large combines and precision equipment require substantial investment, and rising financing costs have extended the time needed to recover these expenses. As a result, many farmers are postponing equipment upgrades, which slows overall market turnover and affects manufacturer sales. Smaller farms experience the greatest impact, as they often lack the financial resources to invest in newer technologies. This situation moderates growth in Germany's agricultural machinery market, where cost and return on investment remain significant barriers to modernization.

Cybersecurity and Data Ownership Concerns in Digitally Enabled Fleets

As German agriculture becomes increasingly digitized, cybersecurity and data ownership concerns have emerged as significant challenges. Smart machinery connected through ISOBUS gateways and cloud platforms creates potential vulnerabilities that could expose sensitive farm data. Farmers express concerns about unauthorized access to yield maps, soil profiles, and operational metrics, which they consider valuable intellectual property. The absence of established, industry-specific security standards increases compliance complexity and costs, deterring some producers from implementing digital solutions. These issues slow the adoption of digital technology in the agricultural machinery market, emphasizing the need for enhanced security measures and clear frameworks for data management and ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tractors Lead the Market while Irrigation Machinery Records Fastest Growth

Tractors represent 62.3% of the Germany agricultural machinery market size in 2025, maintaining their dominant position. Despite decreased registration volumes, demand remains robust due to fuel-efficient engines and smart implement compatibility. Farmers are modernizing existing fleets through ISOBUS retrofits and plug-and-play upgrades rather than complete replacements. Electric tractors are gaining adoption in the vegetable farming and municipal services segments. The testing of models like the e100 Vario indicates a gradual transition toward electrification as battery technology advances.

Irrigation machinery demonstrates the highest growth rate at 6.5% CAGR through 2031, driven by climate variability and water-efficient farming requirements. While irrigation adoption remains moderate, increasing drought conditions and changing weather patterns accelerate the uptake of sprinkler and drip systems. Government subsidies and energy tax incentives reduce operational costs, improving access to precision irrigation systems. Climate resilience requirements are transforming irrigation from a supplementary investment to an essential component, influencing Germany's agricultural machinery market dynamics and infrastructure planning.

Geography Analysis

Germany's average farm size enables efficient operational scale and equipment versatility, leading manufacturers to develop modular machinery for diverse farming requirements. Schleswig-Holstein and Mecklenburg-Western Pomerania demonstrate high adoption rates of precision technologies, particularly among mid-sized arable farms. Innovation centers in Lower Saxony, Bavaria, and Saxony-Anhalt foster agricultural robotics and smart machinery development through partnerships with universities and research institutions. While Brandenburg and North Rhine-Westphalia show increased telematics adoption aligned with data-driven farming trends, economic conditions have reduced new equipment investments nationwide.

Lower Saxony dominates Germany's agricultural machinery market due to its concentrated farming and extensive irrigation systems. The state's robust grant programs support regular equipment upgrades, especially for forage and irrigation machinery. Bavaria ranks second, with its varied farming structures creating demand for adaptable utility tractors and harvesters. North Rhine-Westphalia's proximity to major equipment manufacturers makes it an ideal testing location for compact electric machinery designed for urban and semi-urban farming. These regional variations demonstrate how local conditions, livestock concentration, and government support influence equipment selection.

Eastern German states' larger farms create opportunities for autonomous equipment that minimizes soil compaction in extensive fields. Limited availability of equipment dealers creates maintenance challenges for sophisticated digital systems. Regional crop preferences, dominated by maize and winter wheat cultivation, affect machinery requirements. Environmental subsidy programs may influence purchases toward equipment suitable for eco-friendly crops. Regions with significant livestock operations, including Bavaria, Lower Saxony, and North Rhine-Westphalia, maintain consistent demand for forage harvesters, automated feeding equipment, and regulation-compliant manure distribution systems.

Competitive Landscape

The Germany agricultural machinery market share shows a moderate consolidation. Established brands maintain their positions through extensive dealer networks, diverse product portfolios, and strong brand loyalty across farming regions. AGCO Corporation's Fendt brand leads the market, distinguished by its premium engineering and comprehensive precision farming solutions. Fendt's reliability and innovation have established it as a preferred choice among mid- to large-scale German farms, particularly in Bavaria and Lower Saxony. Deere & Company maintains its market position through global manufacturing capabilities and integrated technology platforms.

Kubota Corporation has strengthened its presence in specialty orchards and compact equipment segments, where its machines' maneuverability and efficiency provide advantages. The company's tractors and implements have gained popularity in regions with fragmented landholdings and horticultural operations, including Baden-Württemberg and parts of North Rhine-Westphalia. CLAAS KGaA mbH maintains its position as a significant player in the German machinery sector, particularly in harvesting systems. The company's strength in combine harvesters and forage equipment is enhanced by automation features such as CEMOS, which improves machine performance and reduces operator fatigue. CLAAS's established presence in German agriculture and focus on innovation support its market position.

CNH Industrial N.V. completes the top five with its Case IH and New Holland brands, providing comprehensive solutions for arable and mixed-use farms. The company focuses on telematics, autonomous capabilities, and ISOBUS integration, supporting Germany's transition to precision agriculture. Case IH's high-horsepower tractors serve large-scale operations in eastern states, while New Holland's equipment meets the needs of livestock and mixed farms in the south. CNH's ongoing investment in smart technologies and regional market adaptation maintains its competitive position in this evolving market.

Germany Agricultural Machinery Industry Leaders

Deere & Company

AGCO Corporation

CNH Industrial N.V.

Kubota Corporation

CLAAS KGaA mbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CLAAS KGaA mbH developed the ROLLANT 630 RC round baler, equipped with a 25-knife cutting rotor, MULTIFLOW pick-up, and reinforced drive systems for producing high-density bales. The baler includes ISOBUS control systems, CLAAS connect integration, and improved operator features to enhance forage harvesting efficiency.

- September 2024: AGCO Corporation introduced the Fendt e100 Vario electric tractor, designed for municipal, livestock, and vegetable farming operations. The tractor features zero emissions, quiet operation, a 100 kWh battery, multiple driving modes, and compatibility with standard charging infrastructure, advancing electrification in German agriculture.

Germany Agricultural Machinery Market Report Scope

Agricultural machinery is defined as machinery used in farming and other agricultural activities such as plowing, planting, harvesting, irrigation, mowing etc. The German agricultural Machinery market is Segmented by Type (Tractors, Plowing and Cultivating Machinery, Planting Machinery, Harvesting Machinery, Haying and Forage Machinery, Sprayers, Irrigation Machinery, and Other Types). The report offers the market size in value terms in USD for all the abovementioned segments.

By Type

| Tractors | By Horse-Power | Less than 40 HP |

| 40-100 HP | ||

| 101-150 HP | ||

| Above 150 HP | ||

| By Tractor Type | Compact Utility | |

| Utility | ||

| Row-Crop | ||

| Plowing and Cultivating Machinery | Plows | |

| Harrows | ||

| Cultivators and Tillers | ||

| Others (Ridger, Rotary tillers, etc.) | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Others(Transplanters, Precision Seeders, etc.) | ||

| Harvesting Machinery | Combine Harvesters | |

| Forage Harvesters | ||

| Others (Potato Harvesters, Potato Harvesters, etc.) | ||

| Haying and Forage Machinery | Mowers | |

| Balers | ||

| Others (Rakes, Tedders, etc.) | ||

| Irrigation Machinery | Sprinkler | |

| Drip | ||

| Others (Micro-Sprinklers, Center-Pivot Irrigation, etc.) | ||

| Other Types | ||

| By Type | Tractors | By Horse-Power | Less than 40 HP |

| 40-100 HP | |||

| 101-150 HP | |||

| Above 150 HP | |||

| By Tractor Type | Compact Utility | ||

| Utility | |||

| Row-Crop | |||

| Plowing and Cultivating Machinery | Plows | ||

| Harrows | |||

| Cultivators and Tillers | |||

| Others (Ridger, Rotary tillers, etc.) | |||

| Planting Machinery | Seed Drills | ||

| Planters | |||

| Spreaders | |||

| Others(Transplanters, Precision Seeders, etc.) | |||

| Harvesting Machinery | Combine Harvesters | ||

| Forage Harvesters | |||

| Others (Potato Harvesters, Potato Harvesters, etc.) | |||

| Haying and Forage Machinery | Mowers | ||

| Balers | |||

| Others (Rakes, Tedders, etc.) | |||

| Irrigation Machinery | Sprinkler | ||

| Drip | |||

| Others (Micro-Sprinklers, Center-Pivot Irrigation, etc.) | |||

| Other Types | |||

Key Questions Answered in the Report

How large is the Germany agricultural machinery market in 2026?

The Germany agricultural machinery market size is USD 11.05 billion in 2026 and will reach USD 13.64 billion by 2031.

Which equipment type holds the largest share in German farm machinery sales?

Tractors lead with 62.3% of 2025 revenue, reflecting their central role in field operations.

Which segment is growing the fastest through 2031?

Irrigation machinery is projected to advance at a 6.5% CAGR as drought resilience becomes critical.

How is regulation shaping future tractor purchases?

Stage V emission limits and CAP eco-rules are steering buyers toward electric or low-emission models and precision implements.

Page last updated on: