Geomechanics Software And Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

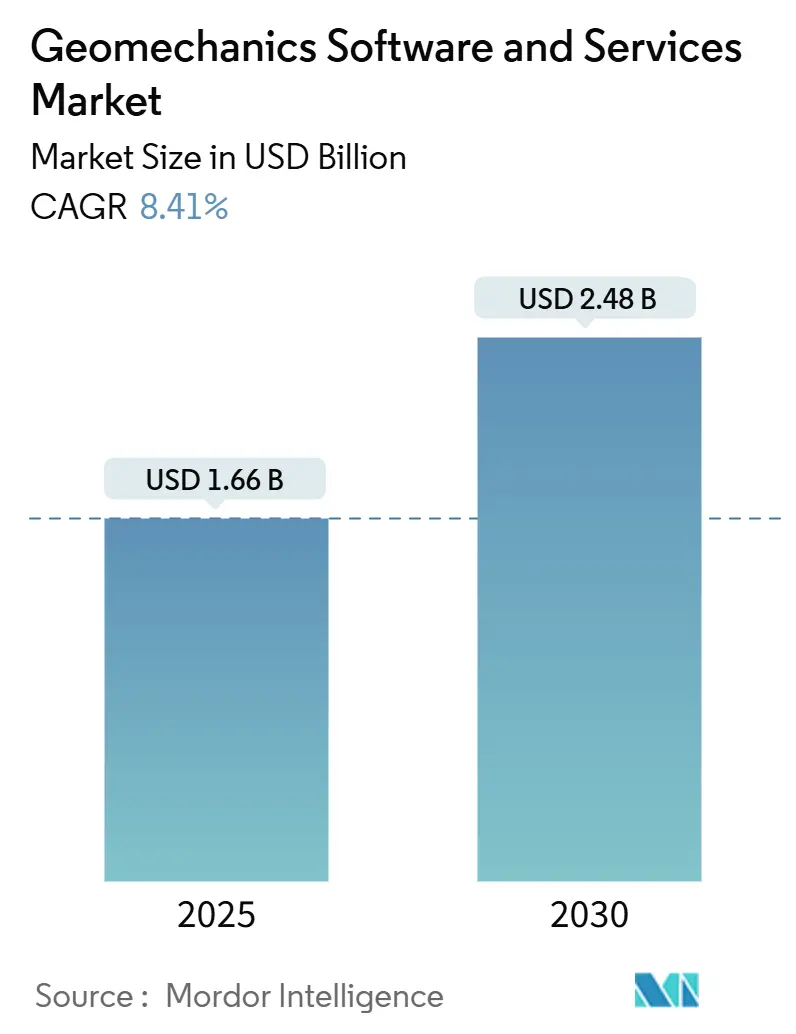

| Market Size (2025) | USD 1.66 Billion |

| Market Size (2030) | USD 2.48 Billion |

| Growth Rate (2025 - 2030) | 8.41% CAGR |

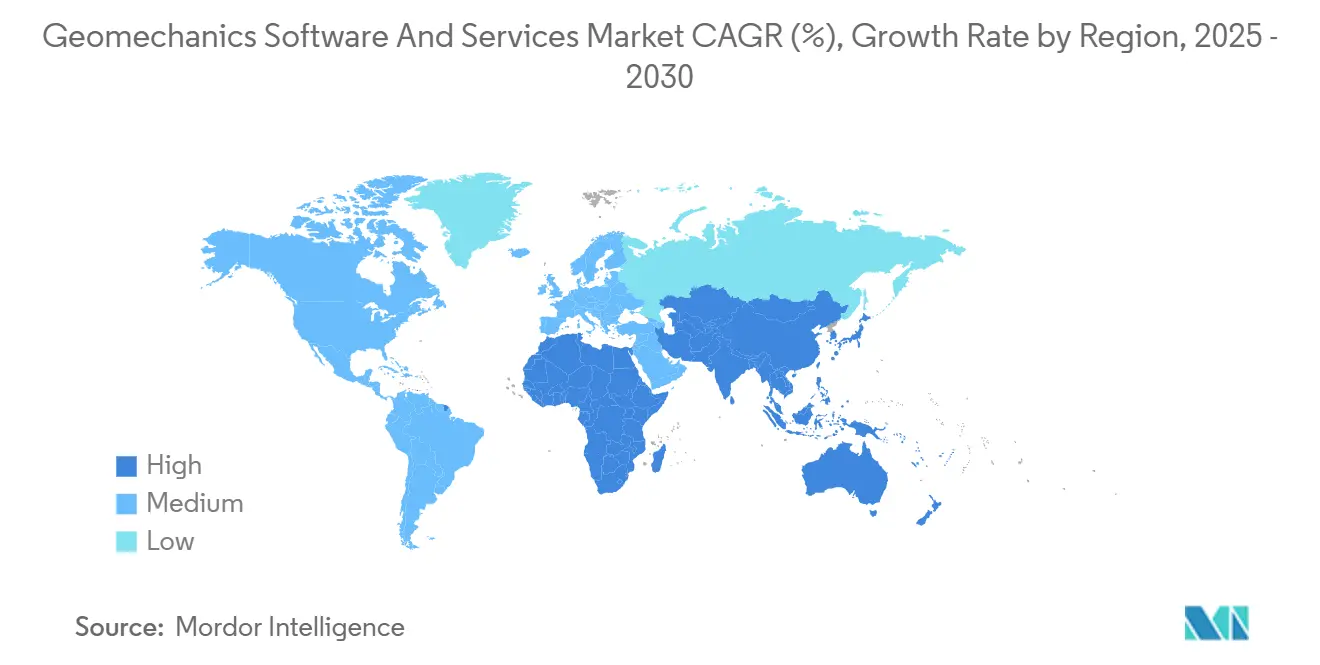

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geomechanics Software And Services Market Analysis by Mordor Intelligence

The geomechanics software and services market size is USD 1.66 billion in 2025 and is forecast to reach USD 2.48 billion by 2030, advancing at an 8.41% CAGR. Robust investment in data-driven subsurface modeling, rising unconventional drilling, and tighter well-integrity mandates underpin this growth trajectory. Operators now favor real-time geomechanics workflows that shorten drilling cycles, cut non-productive time, and safeguard wellbore stability. Services are gaining ground as companies look for turnkey technical support rather than stand-alone tools, while cloud-native platforms unlock collaborative modeling across global teams. North America keeps its revenue lead on the back of shale activity, yet Asia-Pacific represents the fastest-expanding opportunity thanks to mining, infrastructure, and emerging hydrogen-storage projects. Competitive dynamics remain moderately fragmented, prompting platform consolidation and deeper artificial-intelligence integration.

Key Report Takeaways

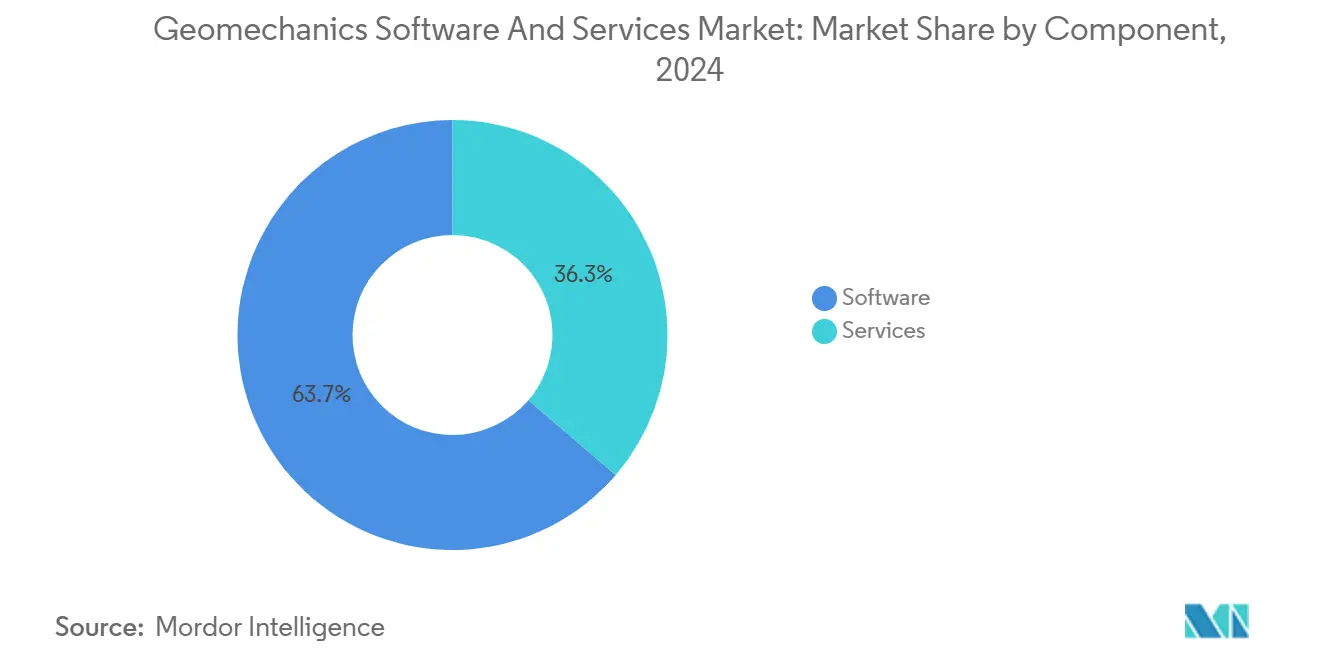

- By component, software held a 63.71% share of the geomechanics software and services market in 2024, whereas services are projected to post a 10.14% CAGR through 2030.

- By deployment mode, on-premise installations commanded 69.42% of the geomechanics software and services market share in 2024, while cloud solutions are expected to grow at a 9.84% CAGR to 2030.

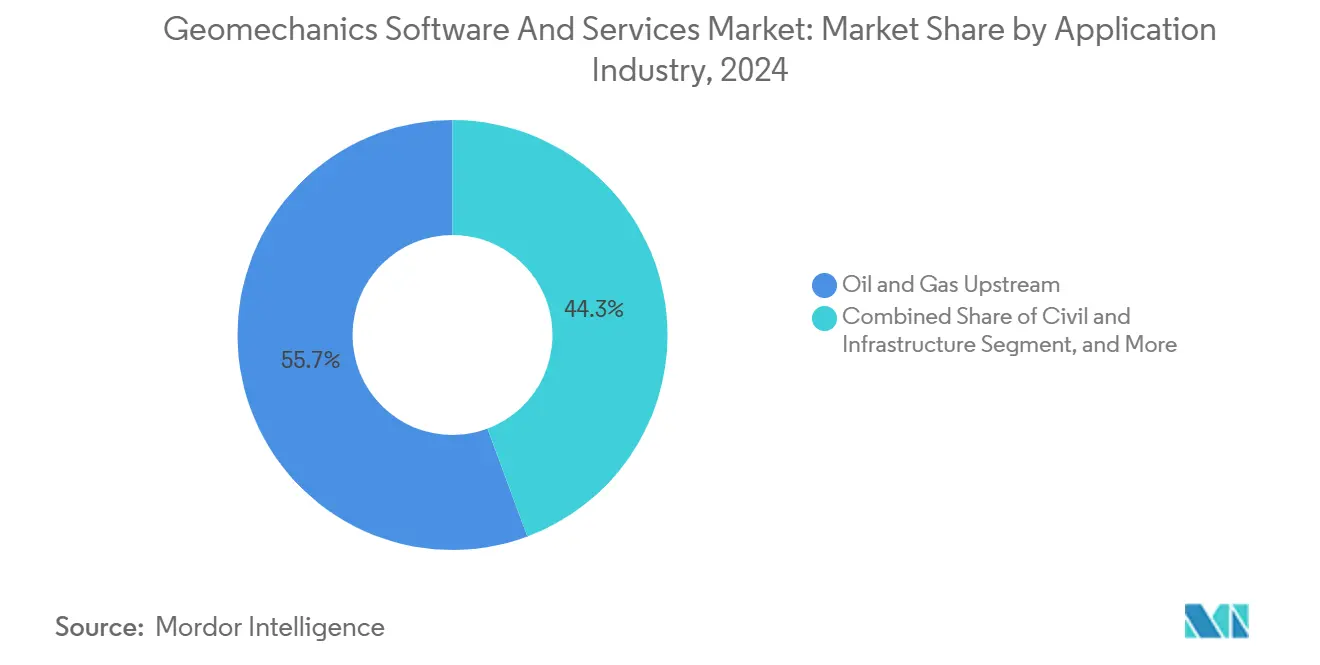

- By application industry, upstream oil and gas represented 55.67% of the geomechanics software and services market size in 2024; nuclear waste disposal is on track for an 8.68% CAGR between 2025 and 2030.

- By software type, stand-alone packages accounted for 57.32% of the 2024 market size, yet integrated platforms are forecast to expand at a 10.23% CAGR through 2030.

- By geography, North America led with 39.62% of the total 2024 revenue, whereas Asia-Pacific is poised for an 8.57% CAGR out to 2030.

Global Geomechanics Software And Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of real-time geomechanics workflows in unconventional plays | +2.1% | North America, with expansion to Argentina Vaca Muerta, Middle East unconventionals | Medium term (2-4 years) |

| Increasing drilling non-productive-time (NPT) costs driving software spend | +1.8% | Global, concentrated in high-cost offshore and unconventional plays | Short term (≤ 2 years) |

| Regulatory push for well-integrity modelling (methane-leak rules) | +1.4% | North America and EU, expanding to Asia-Pacific jurisdictions | Long term (≥ 4 years) |

| Cloud-native geomechanics platforms unlocking collaborative subsurface modelling | +1.2% | Global, led by North America and Europe adoption | Medium term (2-4 years) |

| AI-enabled rock-property prediction reducing core-lab expenditure | +0.9% | Global, early adoption in North America and Middle East | Medium term (2-4 years) |

| Niche: demand for geomechanics in underground hydrogen storage feasibility | +0.3% | Europe, Australia, with pilot projects in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of real-time geomechanics workflows in unconventional plays

Real-time geomechanics integration lets drilling teams adjust mud weights, bit trajectories, and casing programs while the bit is turning. Permian operators reported 15-25% cuts in non-productive time after adding continuous pore-pressure and fracture-gradient monitoring to their rig data streams. [1]SPE Journal, “Real-Time Geomechanics Integration in Unconventional Plays,” onepetro.org EOG Resources captured a 12% boost in drilling efficiency and an 18% drop in wellbore instability incidents across its 2024 Delaware Basin campaign. YPF replicated this success in Argentina’s Vaca Muerta, where real-time model updates proved critical for navigating complex stress regimes. These field results confirm why unconventional producers treat geomechanics software as a strategic lever for cost control and faster well delivery.

Increasing drilling non-productive-time costs driving software spend

Deepwater NPT events cost USD 500,000–2 million per day, and 30-40% of those events stem from geomechanics-related issues such as stuck pipe or lost circulation. [2]Journal of Petroleum Science and Engineering, “Drilling Optimization Through Advanced Geomechanics,” sciencedirect.com Petrobras avoided USD 45 million in 2024 by applying advanced modeling across pre-salt wells, turning simulation insights into adjusted drilling parameters that prevented salt-related failures. Because a single dodged event offsets annual licensing fees, investment cases for geomechanics platforms now pass executive scrutiny even during capital-discipline cycles.

Regulatory push for well-integrity modeling

The U.S. Environmental Protection Agency’s methane-reduction rule obliges operators to present geomechanical validation when applying for well permits, and similar language is appearing in European industrial-emission directives. [3]Federal Register, “Oil and Natural Gas Sector Climate Review,” federalregister.gov Chevron’s Gorgon CCS project uses finite-element stress modeling to verify CO₂ plume containment, setting a precedent that other storage projects must meet. Compliance deadlines extend over the next decade, securing a long runway of software demand tied directly to regulatory reporting.

Cloud-native geomechanics platforms unlocking collaborative modeling

Digital workspaces such as Schlumberger’s DecisionSpace 365 process multi-petabyte data volumes, allowing geoscientists, drilling engineers, and completion teams to iterate on shared models without latency. Global operators deploying these platforms cut model-building time by 40-60% and elevate decision quality because insights from one discipline become instantly visible to others. Shell’s Gulf of Mexico campaign used cloud-enabled geomechanics to avert three potential wellbore-stability incidents in 2024, proving the operational upside of remote collaboration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High licence and training costs for advanced finite-element solvers | -1.6% | Global, particularly affecting smaller operators and emerging markets | Short term (≤ 2 years) |

| Scarcity of geo-data science talent lengthening deployment cycles | -1.3% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Data-sovereignty concerns slowing cloud migration in MENA and Russia | -0.8% | MENA, Russia, China, with spillover effects in Asia-Pacific | Long term (≥ 4 years) |

| Under-reported: lack of unified standards for model interoperability | -0.5% | Global, affecting multi-vendor software environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High license and training costs for advanced finite-element solvers

Enterprise-level geomechanics suites cost USD 22,000 per perpetual seat, while annual subscriptions approach USD 16,000, and certified training adds another USD 5,000–15,000 per engineer. These expenses strain budgets for independents running fewer than 20 wells a year. Without volume programs to spread overhead, smaller firms postpone adoption, slowing total-addressable-market expansion in price-sensitive regions.

Scarcity of geo-data-science talent lengthening deployment cycles

Only about 65% of open geo-data-science roles are filled, and unfilled positions push project timelines 3–6 months beyond plan. ConocoPhillips experienced an eight-month delay in rolling out AI-assisted geomechanics across Eagle Ford wells, even after offering 25% salary premiums. Limited talent availability constrains how fast operators can scale platform capabilities, capping near-term revenue realization for vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Despite Software Dominance

Software accounted for USD 1.06 billion and 63.71% of the geomechanics software and services market in 2024, yet services are projected to grow at a 10.14% CAGR through 2030. The geomechanics software and services market size attributed to services could therefore add more than USD 300 million over the forecast horizon. Operators increasingly outsource finite-element modeling, real-time monitoring, and drilling-optimization support because the required expertise is scarce internally. Halliburton’s integrated services bundles, which couple DecisionSpace licenses with on-rig engineering assistance, earn 40% higher revenue per client compared with license-only contracts.

Service growth depends on complex, unconventional, and deepwater wells where turnkey support delivers immediate value. Hourly rates of USD 200–500 for senior geomechanics consultants are acceptable when a single avoided stuck-pipe incident saves USD 1 million. Vendors are therefore investing in global service centers, multilingual support, and rotational field teams that can mobilize quickly. This strategic pivot positions services as a recurring revenue engine that stabilizes cash flow between major software releases. Over time, bundled models could narrow the software-only share of the geomechanics software and services market to near-parity with services, even as absolute license sales continue rising.

By Deployment Mode: Cloud Migration Accelerates Despite On-Premise Dominance

On-premise solutions held 69.42% of 2024 revenue, but cloud deployments are forecast to show a 9.84% CAGR through 2030 as digital work practices take hold. The geomechanics software and services market share for cloud will expand fastest in companies with distributed engineering hubs. Schlumberger’s DELFI environment already processes 500 terabytes monthly for finite-element analysis, enabling cross-time-zone collaboration that on-premise clusters cannot match.

Hybrid architectures are emerging as a middle ground: sensitive data remains in local servers while compute-intensive workloads burst to the cloud. ISO 27001 certifications and sovereign-cloud variants address data-residency policies in jurisdictions such as the Middle East and China, easing regulatory friction. Capital-efficiency arguments further encourage cloud adoption because operators avoid up-front hardware outlays and scale compute on demand. Over the forecast window, the percentage of new projects launched in pure on-premise environments will decline each year, even though base-installed clusters ensure that absolute on-premise revenue stays material.

By Application Industry: Nuclear Waste Disposal Emerges as Growth Leader

Upstream oil and gas captured 55.67% of 2024 revenue, confirming its historical weight in the geomechanics software and services market. Yet nuclear waste disposal is on track for the highest CAGR at 8.68%, reflecting aggressive repository timelines in Finland, Germany, and the United States. Germany’s Asse II remediation and Finland’s Onkalo deep-geological disposal both demand multidecadal rock-mechanics modeling that far exceeds typical reservoir timeframes.

Governments set aside multi-billion-dollar budgets for long-term safety cases, making software spend a small but essential line item. Each repository stage—site characterization, license application, construction, and closure-requires iterative model updates, locking in decades of services revenue. Mining and civil infrastructure remain steady contributors, driven by slope stability and tunnel design. Continuous adoption across these sectors balances cyclical swings in oil and gas, creating a diversified demand base that shields vendors from energy-price volatility.

By Software Type: Integrated Platforms Gain Momentum

Stand-alone tools captured 57.32% of 2024 sales, but integrated suites are forecast to grow at a 10.23% CAGR. Integrated environments combine rock-mechanics solvers, reservoir simulators, drilling planners, and visualization modules behind a single interface, eliminating file-transfer friction and duplicate data storage. Equinor reports a 45% drop in model-build time after unifying geomechanics, reservoir, and well-planning tools on a single platform.

The geomechanics software and services market size attached to integrated platforms rises in parallel with cloud adoption because web-native architectures simplify module coupling. Bentley’s PLAXIS suite shows how vendors merge civil and subsurface workflows, letting users perform foundation analysis and finite-element geomechanics inside one project file. Over the forecast period, licensing revenue from stand-alone packages will still grow with new-user additions, yet incremental wallet share belongs to platform vendors that deliver measurable productivity gains.

Geography Analysis

North America led with 39.62% of global revenue in 2024 on the strength of shale drilling and methane-emission rules that formalize well-integrity modeling. Operators allocate larger digital budgets to optimize horizontal wells, and service companies maintain regional centers that supply on-site geomechanics specialists within days. The United States also hosts many platform developers, giving local users early access to beta features and technical support.

Asia-Pacific is forecast to be the fastest-growing region at an 8.57% CAGR as mining, tunneling, and infrastructure projects proliferate. Australia deploys real-time slope-stability modeling to protect billion-dollar iron-ore pits, while China integrates geotechnical simulation into high-speed-rail tunnel design. The combination of government-sponsored megaprojects and a widening pool of trained engineers catalyzes demand. National data-security rules encourage hybrid deployments, but this constraint slows adoption less than the efficiency gains lure users.

Europe secures steady growth through nuclear-waste programs and carbon-capture initiatives that require long-term rock-integrity proof. Finland’s repository reached the construction stage in 2025, triggering sustained consulting and software work. North Sea operators continue to champion digital twins, extending geomechanics into late-life reservoir monitoring. Middle East and Africa’s uptake remains tied to giant carbonate reservoirs and early-stage hydrogen-storage pilots, while Latin America gains momentum as Argentina’s Vaca Muerta matures and Brazil’s pre-salt wells push modeling boundaries.

Competitive Landscape

The geomechanics software and services market features a moderate level of fragmentation because no supplier exceeds a 15% revenue share. Schlumberger, Halliburton, and Baker Hughes leverage field-service footprints to cross-sell software and consultancy, whereas Rocscience, Itasca, and Ikon Science compete on specialized solvers and niche domain expertise. Differentiation increasingly hinges on artificial-intelligence pipelines that automate rock-property prediction and real-time drilling guidance.

Platform consolidation shapes recent strategy. Carina’s February 2025 buyout of Ikon Science bundled machine-learning rock-physics with classical geomechanics, signaling that comprehensive subsurface characterization will drive the next competitive wave. Bentley’s 2024 Seequent purchase filled gaps in mining and environmental workflows, while Weatherford partnered with AIQ to co-develop automated parameter-tuning engines. These moves illustrate how vendors chase end-to-end ecosystems that lock users into recurring SaaS fees.

Pricing dynamics remain disciplined because corporate buyers negotiate global master agreements. Vendors, therefore, focus on value-added modules—cloud accelerators, digital-twin connectors, and security certifications—to defend margins. Field-validated case studies that quantify NPT savings or regulatory-compliance wins accelerate sales cycles, especially among smaller operators wary of six-figure license commitments. Over the forecast window, expect joint ventures between software specialists and drilling-contractor groups seeking to embed geomechanics directly at the rig site.

Geomechanics Software And Services Industry Leaders

Schlumberger N.V.

Halliburton Company

Baker Hughes Company

Ikon Science Limited

GeoMechanics Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Carina acquired Ikon Science for an undisclosed amount, combining AI-driven rock-property prediction with advanced geomechanics modeling.

- January 2025: ADNOC, Schlumberger, and Patterson-UTI formed a joint venture for unconventional drilling in Abu Dhabi that embeds real-time geomechanics workflows.

- December 2034: Baker Hughes won a USD 500 million contract with Petrobras for digital well-construction services that include pre-salt geomechanics optimization.

- November 2024: Halliburton launched the SmartDigital platform, integrating machine learning with real-time drilling data to predict wellbore stability.

Global Geomechanics Software And Services Market Report Scope

| Software |

| Services |

| On-premise |

| Cloud-based |

| Hybrid |

| Oil and Gas Upstream |

| Mining |

| Civil and Infrastructure |

| Nuclear Waste Disposal |

| Other Application Industry |

| Stand-alone |

| Integrated Platform |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | On-premise | ||

| Cloud-based | |||

| Hybrid | |||

| By Application Industry | Oil and Gas Upstream | ||

| Mining | |||

| Civil and Infrastructure | |||

| Nuclear Waste Disposal | |||

| Other Application Industry | |||

| By Software Type | Stand-alone | ||

| Integrated Platform | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the 2025 value of the geomechanics software and services market?

The market is valued at USD 1.66 billion in 2025.

How fast is the market expected to grow?

It is forecast to post an 8.41% CAGR from 2025 to 2030.

Which component is expanding quickest?

Services are on track for a 10.14% CAGR through 2030 due to turnkey solution demand.

Why are cloud deployments gaining popularity?

Cloud platforms enable real-time collaboration and scalable compute, propelling a 9.84% CAGR despite data-sovereignty hurdles.

Which application segment shows the highest growth?

Nuclear waste disposal leads with an 8.68% CAGR because repository projects need advanced geomechanical validation.

Which region offers the fastest growth opportunity?

Asia-Pacific is projected to expand at an 8.57% CAGR thanks to mining, infrastructure, and digital-modeling uptake.

Page last updated on: