Asia Pacific Geographic Information System (GIS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

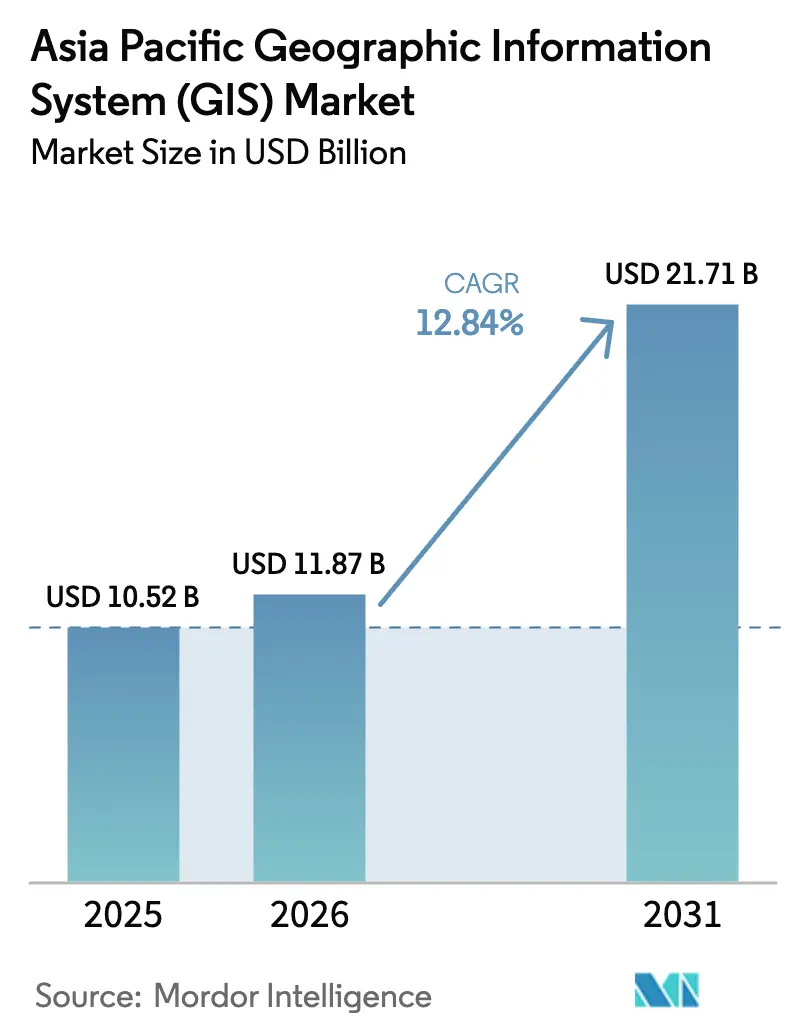

| Base Year Market Size (2025) | USD 10.52 Billion |

| Market Size (2026) | USD 11.87 Billion |

| Market Size (2031) | USD 21.71 Billion |

| Growth Rate (2026 - 2031) | 12.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Geographic Information System (GIS) Market Analysis by Mordor Intelligence

The Asia Pacific Geographic Information System Market size is expected to grow from USD 10.52 billion in 2025 to USD 11.87 billion in 2026 and is forecast to reach USD 21.71 billion by 2031 at 12.84% CAGR over 2026-2031. Robust public spending on smart-city infrastructure, accelerating 5G coverage, and the rise of hyper-granular spatial analytics make geospatial data a core layer of regional digital transformation. Converging investments in digital twins, microsatellite imagery, and IoT-enabled asset tracking are widening the addressable base for spatial intelligence across government, utilities, mining, and logistics. Cloud-native tools that blend real-time sensor feeds with AI-driven analytics are lowering entry barriers for small and mid-sized enterprises, while data-sovereignty rules are nudging larger buyers toward hybrid deployments. Moderate competitive intensity persists as long-time leaders defend ecosystem advantages, even as cost-effective Chinese and Southeast Asian vendors chip away at price-sensitive segments.

Key Report Takeaways

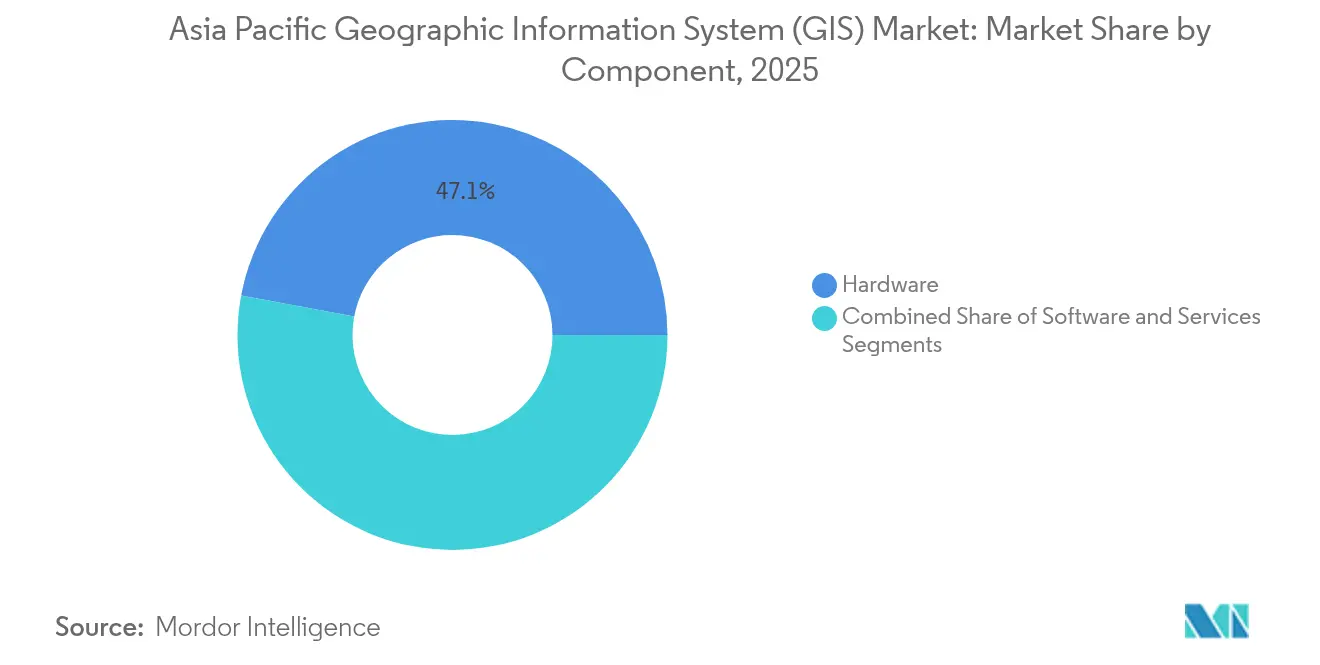

- By component, hardware led with 47.05% of the Asia-Pacific geographic information system market share in 2025; software is forecast to expand at a 14.82% CAGR through 2031.

- By deployment mode, cloud captured 49.85% share of the Asia-Pacific geographic information system market size in 2025, while hybrid architectures are growing fastest at 14.45% CAGR to 2031.

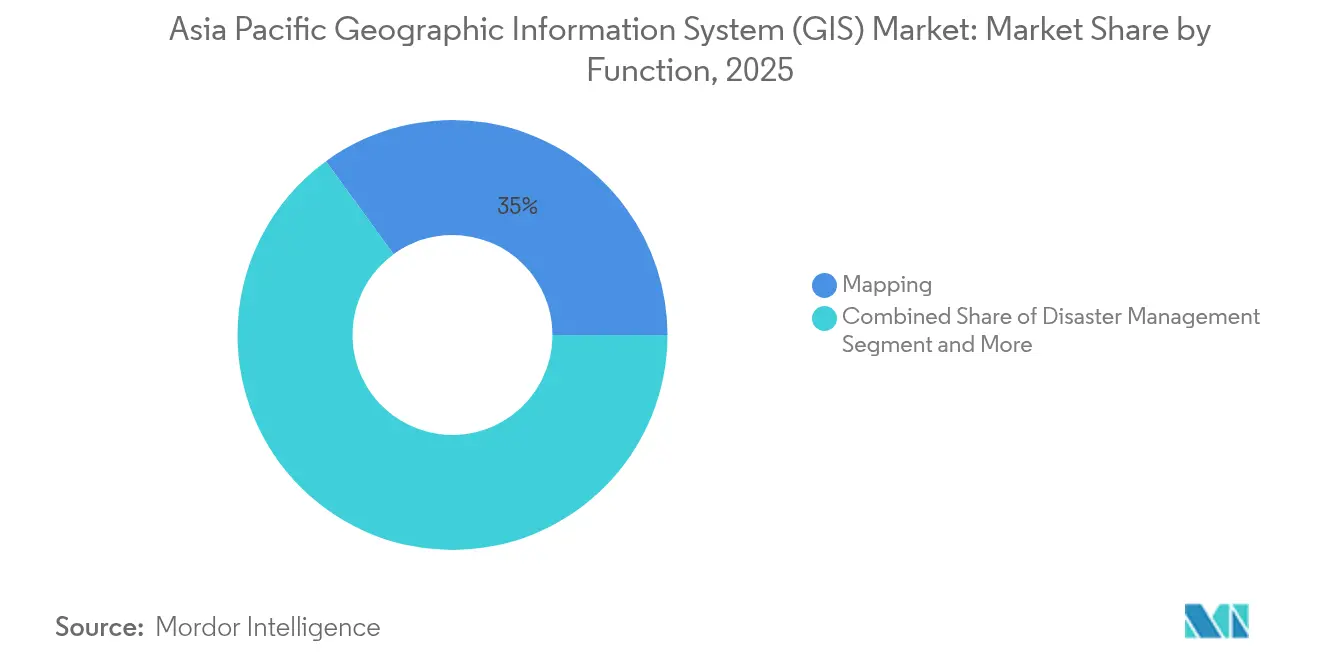

- By function, mapping accounted for a 35.02% share of the Asia-Pacific geographic information system market size in 2025; asset tracking and telematics are advancing at a 14.74% CAGR.

- By end-user industry, government and defence held 28.35% of the Asia-Pacific geographic information system market share in 2025; transportation and logistics records the highest projected CAGR at 14.56% through 2031.

- By country, China commanded 34.20% of the Asia-Pacific geographic information system market share in 2025, while India is set to grow at a 15.12% CAGR.

- Esri, Trimble, Hexagon, and HERE Technologies collectively accounted for a majority of enterprise-class deployments in 2024, with emerging Chinese disruptors increasing price pressure in mid-tier deals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Geographic Information System (GIS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-granular GIS adoption in smart-city programmes | +2.8% | China, India, Singapore, South Korea | Medium term (2-4 years) |

| Cloud-native GIS platforms integrated with IoT networks | +2.3% | Japan, Australia | Short term (≤ 2 years) |

| Government-funded national geospatial data infrastructures | +2.1% | India, Indonesia, Malaysia, Thailand | Long term (≥ 4 years) |

| 5G roll-out enabling real-time mobile GIS analytics | +1.9% | South Korea, China, Japan, Australia | Medium term (2-4 years) |

| Proliferation of microsatellite imagery providers in APAC | +1.6% | Australia, Japan, Southeast Asia | Long term (≥ 4 years) |

| Local-language GIS interfaces for SME digitisation | +1.4% | Indonesia, Malaysia, Thailand, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyper-granular GIS adoption in smart-city programmes

Megacities are moving beyond block-level maps to centimetre-level digital twins that capture every curb, utility conduit, and façade. Singapore’s Gemma platform has trimmed average bus wait times by using 3D spatial models to re-optimize routes. [1]GovInsider, “Using Maps to Build Smarter Cities,” govinsider.asia Seoul’s TOPIS network similarly aggregates live road and subway data to ease congestion. China now mandates sub-decimetre accuracy for urban planning, a standard that is raising procurement thresholds and spurring demand for lidar-equipped survey drones. Vendors able to fuse high-resolution imagery with predictive analytics are gaining footholds as city planners prioritise preventive maintenance over reactive repairs.

Cloud-native GIS platforms integrated with IoT networks

Thousands of on-site sensors streaming position-tagged data every second require compute elasticity that on-premise stacks cannot match. Japanese contractor Chiyoda visualises worker locations in near real time via cloud-hosted dashboards, improving site safety and productivity. China’s Dahaize coal mine used 5G-linked IoT feeds to raise performance stability by 45%. [2]GSMA, “Smarter Mining,” gsma.com As cross-border operators juggle data-localisation rules, hybrid cloud offerings that keep sensitive layers on-premise while bursting into the public cloud for analytics are rising in popularity.

Government-funded national geospatial data infrastructures

Indonesia’s Ina-Geoportal, Malaysia’s National Digital Cadastral Database, and Thailand’s Yala digital twin illustrate how public funding is standardising data schemas and open APIs. These long-cycle programmes lower integration costs for vendors and let SMEs tap authoritative base layers without investing in costly surveys. Precision requirements—Malaysia targets ±10 cm positional accuracy—are also accelerating upgrades to GNSS receivers and lidar scanners across survey fleets.

5G roll-out enabling real-time mobile GIS analytics

Standalone 5G lets field crews collaborate on live maps rather than waiting for overnight synchronization. South Korea posts average SA download speeds of 729.89 Mbps, while Singapore’s Tuas port shaved latency by 50% for automated guided vehicles. China Mobile’s 5G Sea Network extends coverage 50 km offshore, supporting maritime GIS for fleet management. Vendors optimised for low-latency streaming are edging out rivals reliant on batch data pipelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High licence and training costs for professional GIS suites | -1.8% | Global, particularly affecting SMEs in developing markets | Short term (≤ 2 years) |

| Strict data-sovereignty laws limiting cross-border datasets | -1.5% | China, India, with spillover effects across ASEAN | Long term (≥ 4 years) |

| Fragmented cadastral standards across ASEAN economies | -1.2% | ASEAN member states, particularly Indonesia, Malaysia, Thailand | Medium term (2-4 years) |

| Disaster-induced data-loss risk for on-premise deployments | -0.9% | Japan, Philippines, Indonesia, disaster-prone coastal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High licence and training costs for professional GIS suites

Enterprise-grade platforms often bundle multi-year contracts, premium support, and lengthy certification courses. In Indonesia, GIS training programmes required heavy government subsidies before uptake improved among district offices. Skill premiums for certified analysts inflate payrolls, keeping many small firms on freemium tools with limited analytical depth. Subscription cloud models are easing sticker shock, yet the feature parity gap between free and pro editions remains wide enough to slow mass adoption.

Strict data-sovereignty laws limiting cross-border datasets

China’s regulations bar sensitive spatial layers from leaving the country, and India’s draft data framework is trending in a similar direction. [3]Nikkei Asia, “Data Fortress: Digital Protectionism Embraced by Many in Asia,” asia.nikkei.com A Global Data Alliance survey lists more than 50 discrete localisation rules across the region. Vendors must finance country-specific hosting, cutting into operating margins and complicating multi-market product road maps. For end-users, fragmented data pools reduce the utility of cross-border supply-chain and climate-risk models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware anchors, software accelerates

Hardware held 47.05% of the Asia-Pacific geographic information system market share in 2025, underscoring the ongoing need for GNSS rovers, lidar scanners, and ruggedised field sensors. Demand is strongest in nations upgrading baseline geodetic networks to centimetre accuracy. The Asia-Pacific geographic information system market size derived from hardware is projected to expand steadily but will cede proportionate weight to software subscriptions that post a 14.82% CAGR through 2031. Trimble’s earnings show 75% of revenue now tied to software or subscriptions, a bellwether for incumbents migrating away from one-off equipment sales.

Software’s ascent reflects a preference for OPEX over CAPEX and the attractiveness of instant upgrades. Cloud-delivered analytics suites stitch live sensor feeds with AI models to predict equipment failure or pinpoint energy losses. Services revenue grows in tandem as integrators help agencies cleanse legacy shapefiles and port them into modern spatial databases. Firms balancing equipment supply with SaaS road-maps are best placed to defend their share as procurement shifts toward outcome-based contracts.

By Deployment Mode: Cloud dominance, hybrid momentum

In 2025, cloud accounted for 49.85% of the Asia-Pacific geographic information system market size as organisations migrated from on-premise stacks to elastic infrastructure. Early adopters cite faster rollouts and lighter maintenance as primary draws. Hybrid deployments, however, record the fastest 14.45% CAGR, meeting sovereignty mandates by retaining sensitive layers on-site while pushing heavy analytics to the cloud. The pattern mirrors HERE Technologies’ USD 1 billion AWS deal aimed at streaming AI-ready map data globally.

On-premise deployments continue where air-gapped security is non-negotiable—defence, critical infrastructure, and select mining operations. Yet even these users increasingly bolt cloud micro-services onto the perimeter, for example, to tap machine-learning models or satellite archives. Vendors providing mix-and-match deployment blueprints are widening competitive moats against single-stack rivals.

By Function: Mapping leads, asset tracking surges

Mapping supplied 35.02% of the Asia-Pacific geographic information system market size in 2025, reaffirming its foundational role. Still, asset tracking and telematics advance at a 14.74% CAGR as fleets, ports, and utilities instrument operations with low-cost IoT tags. For instance, ConnectEast shifted from paper plans to live dashboards that flag road defects in minutes rather than weeks.

Spatial analysis and modelling, along with surveying and disaster management, maintain healthy uptake as organisations progress from static charts to predictive layers. Jurong Port’s digital twin monitors berth conditions in real time, improving turnaround scheduling. As 5G ubiquity removes latency ceilings, immersive AR overlays and collaborative field editing are set to cross from pilot to mainstream.

By End-user Industry: Public sector still on top, logistics races ahead

Government and defence captured 28.35% of the Asia-Pacific geographic information system market share in 2025, buoyed by defence modernisation and national mapping mandates. Transportation and logistics, however, are pacing the field with a 14.56% growth run, mirroring e-commerce expansion. Indonesia’s PLN visualised grid vulnerabilities post-earthquake by merging utility schematics with disaster portals, highlighting how public-sector data boosts private-sector resilience.

Utilities, mining, and agriculture add stable demand as precision-driven operations become essential for cost control and sustainability reporting. Australian miners overlay drill-hole logs with hyperspectral imagery to optimise blasting patterns. Healthcare and retail remain nascent but show promise where location analytics intersect with last-mile fulfilment or outbreak tracing.

Geography Analysis

China, with 34.20% of the Asia-Pacific geographic information system market share in 2025, benefits from state-mandated digital twins and wide 5G coverage that extends maritime reach to 50 km offshore. Smart-city blueprints require centimetre-grade cadastral layers, pushing demand for advanced survey hardware and AI-infused analytics. Vendors must host data locally and conform to encryption standards, yet the sheer volume of municipal tenders offsets compliance overheads.

India is the fastest-growing geography at 15.12% CAGR through 2031. National geo-portals, land-parcel digitisation, and rapidly expanding SA 5G networks underpin momentum. Lok-language interfaces widen SME uptake, while cadastral survey apps built on the LADM standard accelerate land-title issuance. Integrated payment-GIS linkages—QR codes mapped to storefront coordinates—illustrate how spatial data meshes with broader digitisation goals.

Japan, Australia, and South Korea form a mature-adopter cluster. Japan perfects disaster-response modules after the 2024 Noto Peninsula quake, layering seismic sensors atop nationwide elevation models. Australia’s miners live-stream drill heads via private 5G, while South Korea’s telecoms deliver 729.89 Mbps SA speeds that let city engineers iterate traffic models in real time. Southeast Asian markets—Indonesia, Malaysia, Thailand, Vietnam—add fresh demand as SME cloud uptake rises and governments fund spatial infrastructure backbones.

Competitive Landscape

The Asia-Pacific geographic information system market is moderately concentrated. Long-time leaders Esri, Trimble, Hexagon, and HERE Technologies leverage global partner networks, proprietary data, and end-to-end stacks to retain enterprise loyalty. Hexagon logged EUR 1,448 million sales in 2024 with recurring revenue up 7%, underscoring the stickiness of multi-module platforms. [4]Hexagon AB, “Year-End Report 2024,” hexagon.com

Strategic investment pivots to AI engines that auto-classify satellite pixels and to real-time cloud services. HERE’s decade-long, USD 1 billion AWS pact aims to shrink map-update cycles from weeks to days, a boon for automakers embracing software-defined vehicles. Planet Labs tilts the imagery supply chain by signing USD 230 million in Asia-Pacific satellite deals that broaden downstream analytics options. Local disruptors—SuperMap in China, NGIS in Australia—gain footholds through competitive pricing and feature sets aligned with regional regulations.

White-space niches are forming in vernacular UIs for SMEs, coastal-resilience analytics for low-lying nations, and AR toolkits for field maintenance. Vendors that package flexible deployment models with region-specific compliance playbooks hold an edge as data-sovereignty regimes proliferate.

Asia Pacific Geographic Information System (GIS) Industry Leaders

Autodesk Inc.

Mappointasia (Thailand) Public Company Limited

Bentley Systems Incorporated

Trimble Inc.

Google LLC (Alphabet Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Saudi Arabia’s Neo Space Group partnered with SuperMap Software to expand geospatial capabilities, with SuperMap opening a local office to accelerate urban-planning innovation.

- January 2025: Planet Labs inked a USD 230 million multi-year Pelican satellite agreement with an Asia-Pacific customer, boosting high-resolution capacity.

- January 2025: HERE Technologies and AWS entered a USD 1 billion, 10-year partnership to deliver AI-powered live-streaming maps.

- January 2025: Maxar Intelligence secured USD 35 million in new imagery tasking from two Asia-Pacific governments.

- January 2025: Maxar renewed four defence contracts totalling more than USD 120 million across Asia and the Middle East.

- September 2024: HERE Technologies was selected by Uber as a global location partner to enhance ride-share mapping.

Asia Pacific Geographic Information System (GIS) Market Report Scope

Geographic Information Systems (GIS) store, analyze, and visualize data for geographic locations on the Earth's surface. GIS is a computer-based tool that investigates spatial patterns, relationships, and trends. GIS better understands data employing a geographic context by connecting geography with data.

The Asia-Pacific GIS market is segmented by country (Australia, Singapore, Indonesia, Malaysia, Bangladesh, and the Rest of Asia-Pacific). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| On-Premise |

| Cloud |

| Hybrid |

| Mapping |

| Spatial Analysis and Modelling |

| Surveying and Positioning |

| Asset Tracking and Telematics |

| Disaster Management |

| Others |

| Government and Defence |

| Utilities and Energy |

| Transportation and Logistics |

| Telecommunications |

| Agriculture and Forestry |

| Mining and Resources |

| Real Estate and Construction |

| Healthcare and Public Safety |

| Retail and Consumer |

| Other End-user Industries |

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Indonesia |

| Malaysia |

| Singapore |

| Thailand |

| Vietnam |

| Philippines |

| Rest of Asia-Pacific |

| By Component | Hardware |

| Software | |

| Services | |

| By Deployment Mode | On-Premise |

| Cloud | |

| Hybrid | |

| By Function | Mapping |

| Spatial Analysis and Modelling | |

| Surveying and Positioning | |

| Asset Tracking and Telematics | |

| Disaster Management | |

| Others | |

| By End-user Industry | Government and Defence |

| Utilities and Energy | |

| Transportation and Logistics | |

| Telecommunications | |

| Agriculture and Forestry | |

| Mining and Resources | |

| Real Estate and Construction | |

| Healthcare and Public Safety | |

| Retail and Consumer | |

| Other End-user Industries | |

| By Country | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the Asia-Pacific geographic information system market?

The market is valued at USD 11.87 billion in 2026 and is forecast to hit USD 21.71 billion by 2031.

Which country holds the largest Asia-Pacific geographic information system market share?

China leads with 34.20% share in 2025, driven by large-scale smart-city and 5G investments.

Which deployment mode is growing fastest?

Hybrid deployment is expanding at a 14.45% CAGR as organisations balance cloud scalability with data-sovereignty compliance.

What segment shows the highest growth by function?

Asset tracking and telematics is advancing at a 14.74% CAGR, fuelled by IoT-enabled fleet and infrastructure monitoring.

Why are SMEs increasingly adopting GIS?

Cloud subscriptions and local-language interfaces are reducing cost and skills barriers, opening the Asia-Pacific geographic information system market to millions of smaller firms.

How will 5G influence GIS applications?

Stand-alone 5G eliminates latency bottlenecks, enabling real-time mobile GIS analytics for field crews, autonomous vehicles, and maritime operations.

Page last updated on: