Geographic Information System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

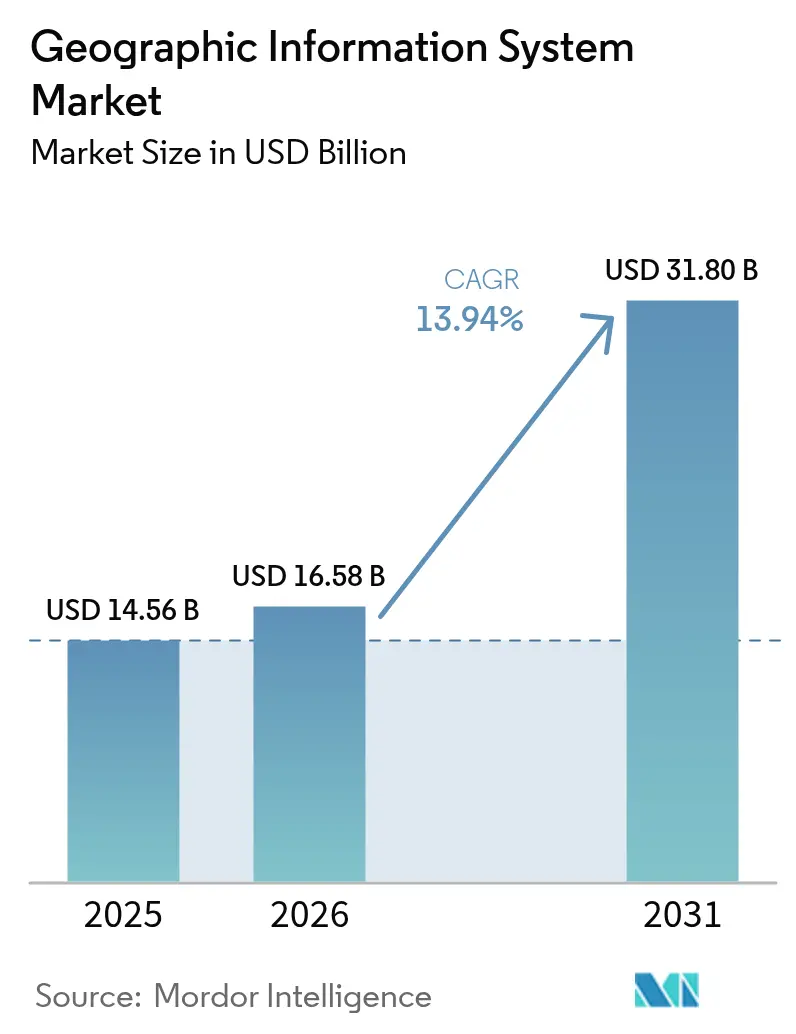

| Market Size (2026) | USD 16.58 Billion |

| Market Size (2031) | USD 31.8 Billion |

| Growth Rate (2026 - 2031) | 13.94% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

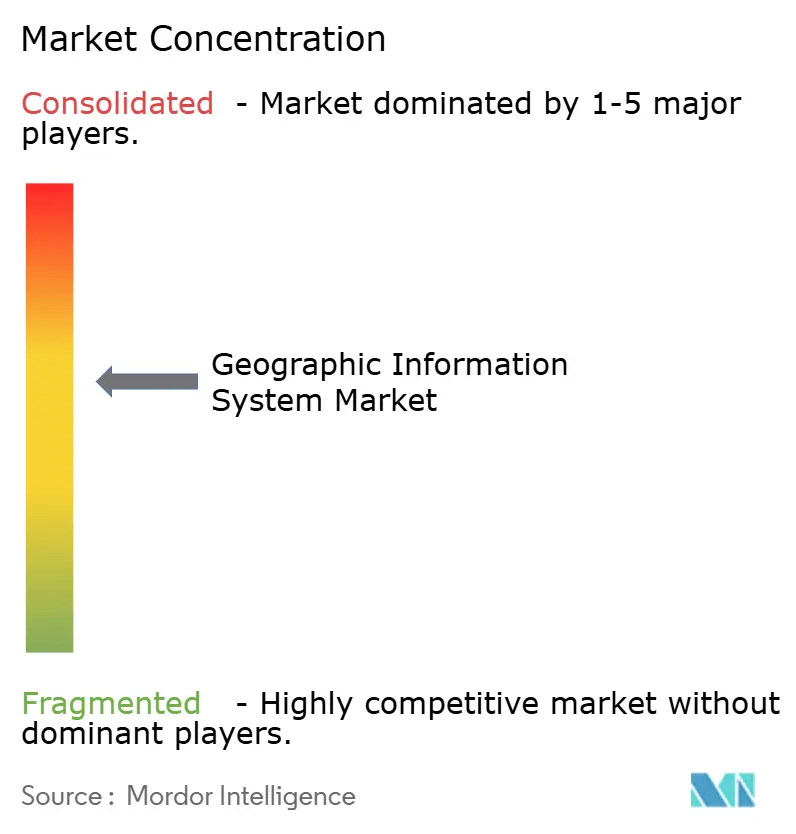

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geographic Information System Market Analysis by Mordor Intelligence

The Geographic Information System market size was valued at USD 14.56 billion in 2025 and estimated to grow from USD 16.58 billion in 2026 to reach USD 31.8 billion by 2031, at a CAGR of 13.94% during the forecast period (2026-2031). Rapid smart-city roll-outs, national open-data mandates, and cloud-native deployments keep demand on an upward slope. Automated feature extraction from sub-30 cm imagery and real-time spatial analytics now reduce decision latency from weeks to minutes, pushing adoption in transportation, oil and gas, and public safety applications. [1]Satellogic, “Pushing Intelligence to the Edge: Satellogic's Vision for AI-Powered Earth Observation,” SATELLOGIC.COM Vendors that bundle AI, edge processing, and managed services continue to gain share as enterprises prioritize scalability and cyber-secure integration with operational networks.

Key Report Takeaways

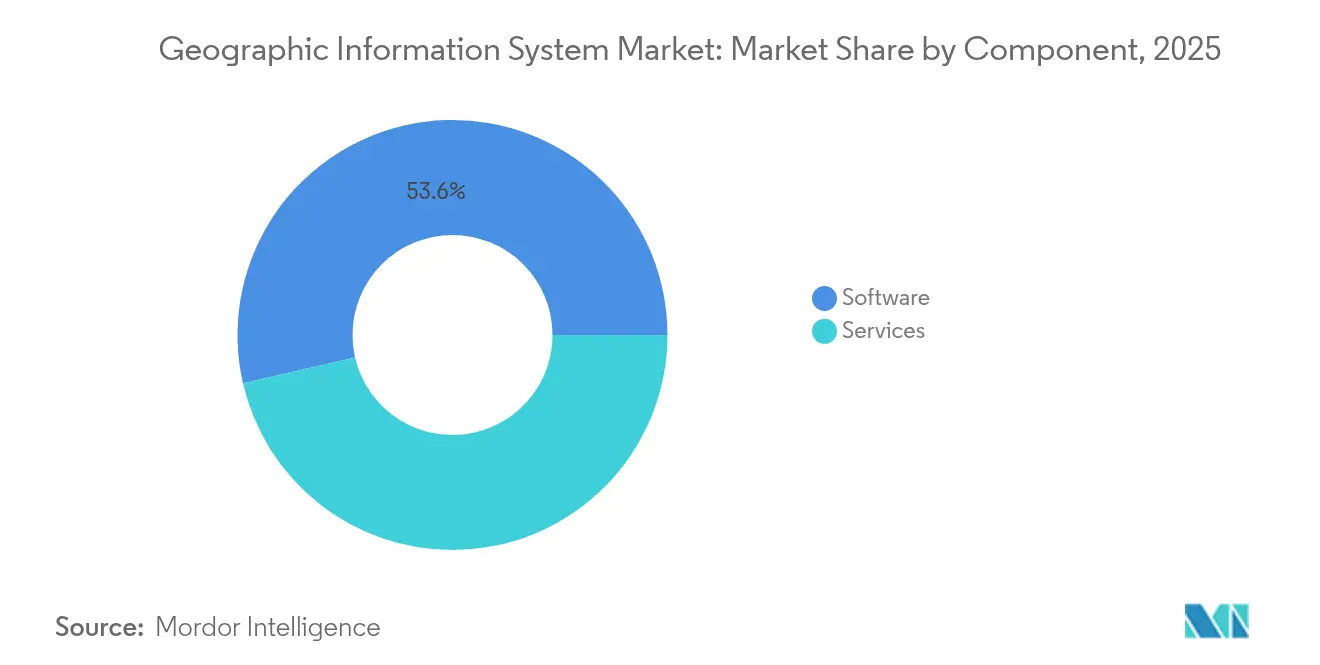

- By component, software commanded 53.60% of the Geographic information system market share in 2025, while services are projected to grow at a 15.45% CAGR through 2031.

- By function, mapping led with a 34.10% share of the Geographic information system market in 2025; geospatial data management and analysis is forecast to post a 15.70% CAGR to 2031.

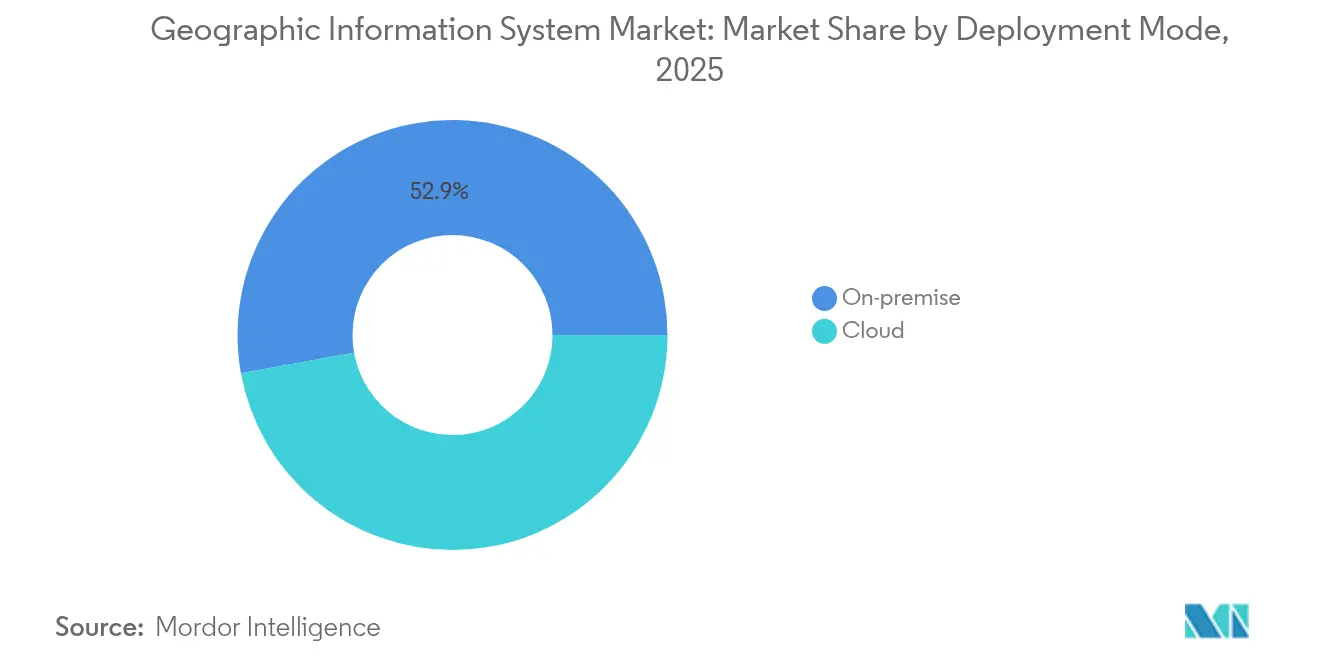

- By deployment mode, on-premise installations held 52.85% of the Geographic information system market size in 2025, whereas cloud deployment is expected to expand at a 16.05% CAGR.

- By end-user industry, transportation and logistics contributed 28.35% of the 2025 spending of the Geographic information system market; oil and gas exhibits the fastest trajectory at a 15.90% CAGR through 2031.

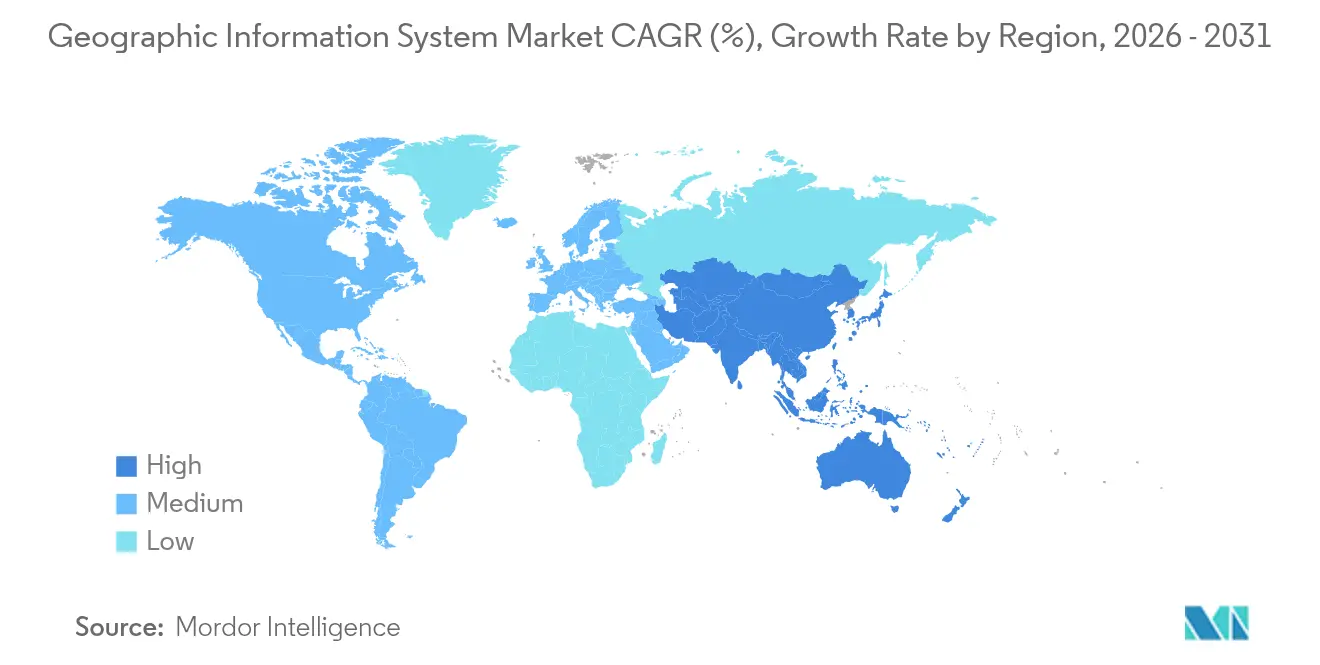

- By geography, North America maintained a 37.80% share in 2025 of the Geographic information system market; Asia-Pacific is set for the highest regional CAGR of 15.95% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Geographic Information System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread smart-city roll-outs require real-time geospatial infrastructure | +3.2% | Global, early gains in APAC and EU | Medium term (2–4 years) |

| Cloud-native GIS lowers TCO and speeds enterprise integration | +2.8% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| Mobile-first field-data-collection platforms expand addressable user base | +2.1% | Global, emerging markets strong | Medium term (2–4 years) |

| AI-powered auto-classification of satellite imagery accelerates analytics | +2.5% | North America, EU, China | Long term (≥ 4 years) |

| Sub-30 cm commercial microsatellite constellations unlock new precision use cases | +1.9% | Global, defense and agriculture focus | Long term (≥ 4 years) |

| National open-data mandates drive adoption | +1.8% | EU core, North America secondary | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Widespread Smart-City Roll-Outs Require Real-Time Geospatial Infrastructure

City agencies are integrating the Geographic information system market platforms with 5G, IoT, and edge compute to orchestrate urban services. Singapore’s Open Digital Platform synchronizes district cooling, waste, and energy through streaming geospatial feeds, improving incident response and infrastructure uptime. [2]Esri, “Esri Collaborates with Google Maps Platform to Offer High-Quality Photorealistic 3D Tiles,” ESRI.COM Los Angeles uses real-time dashboards to route emergency crews, drawing 3.5 million situational-awareness map views during peak events. As municipalities budget for digital twins, vendors that deliver scalable 3D visualization, sensor APIs, and cybersecurity hardening capture a growing portion of public-sector IT spend.

Cloud-Native GIS Lowers TCO and Speeds Enterprise Integration

Bell Canada saved 40-60% in infrastructure outlay by shifting to a cloud-native geospatial data platform, illustrating how containerized micro-services and managed upgrades shorten deployment cycles. ArcGIS Enterprise on Kubernetes and similar offerings align GIS operations with DevOps pipelines, allowing dynamic scaling during disaster events without procurement delays. Push-down analytics in cloud data warehouses eliminate ETL bottlenecks, widening the Geographic information system market addressable base beyond traditional mapping teams.

Mobile-First Field-Data-Collection Platforms Expand Addressable User Base

Smartphone apps now merge GNSS, camera, and lidar sensors into simple survey workflows, cutting field-data costs by up to 70% and boosting accuracy. [3]Trimble Inc., “Trimble Investor Overview – August 2024,” TRIMBLE.COM Augmented-reality overlays help workers visualize buried utilities, preventing excavation mishaps. Offline synchronization protects continuity in remote zones, while 5G uplinks stream high-definition imagery to supervisors, underscoring how the Geographic information system market evolves into frontline operations.

AI-Powered Auto-Classification of Satellite Imagery Accelerates Analytics

Visual-language models now tag ships, roads, and crop stress directly on-orbit, reducing analytic latency from days to minutes. Defense agencies detect illicit construction faster, insurers monitor catastrophe exposure daily, and agribusinesses adjust irrigation in near real time. Service providers monetize API endpoints rather than raw pixels, expanding the Geographic Information System market value creation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy IT integration complexity with OT and SCADA systems | -2.1% | Global, manufacturing and utilities | Short term (≤ 2 years) |

| Persistent data-quality/lineage gaps in crowdsourced layers | -1.8% | Global, all VGI users | Medium term (2–4 years) |

| Rising cloud-egress fees for petabyte-scale imagery archives | -1.3% | North America and EU | Short term (≤ 2 years) |

| Export-control tightening on high-resolution geospatial data | -1.1% | Global, defense and commercial | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy IT Integration Complexity with OT and SCADA Systems

Utilities merging modern GIS with decades-old SCADA confront data-model mismatches, protocol gaps, and new cyber-threat surfaces. Liberty Utilities extended its migration timeline by 18 months due to iterative testing and middleware development. These overruns shift spending toward professional services, slowing software conversions in the Geographic information system market.

Persistent Data-Quality / Lineage Gaps in Crowdsourced Layers

Volunteered geographic information still exhibits uneven accuracy, especially outside urban OECD areas. Peer-reviewed assessments across European cities reveal inconsistent point-of-interest attributes, forcing enterprises to budget extra validation passes. Until automated conflation tools mature, mission-critical users will limit reliance on open contributions, capping growth in certain Geographic information system market niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Propel Digital Transformation

Services revenue in the Geographic information system market rose sharply in 2026, advancing at a 15.45% CAGR as enterprises outsourced cloud migration, AI model tuning, and lifecycle support. Managed-service bundles now cover data-quality audits, security patching, and 24/7 monitoring, shifting spending from capital to operating budgets. Software still accounts for 53.60% of 2025 sales, anchored by the ArcGIS, Hexagon NetWorks, and Trimble Cityworks portfolios. Their continuous update cadence, Esri reinvests roughly 28% of annual turnover into R&D, keeping feature velocity high, while open-API frameworks welcome third-party extensions. Hardware remains essential for GNSS receivers, lidar scanners, and rugged tablets, yet margins compress as more functions migrate into the software layer. The geographic information system market size tied to pure hardware shipments therefore grows more slowly, even as sensor count climbs.

Industry buyers favor vendors that can deliver outcome-oriented service-level agreements; for example, Hexagon’s 2025 decision to divest non-core assets freed capital to bolster subscription support offerings. Training academies, DevOps toolchains, and certified partner networks now form critical selection criteria, signaling a pivot from license counts to customer success metrics across the Geographic information system market.

By Function: Mapping Underpins Insight-Driven Analytics

Mapping held a 34.10% share in 2025, furnishing the spatial context for every downstream workflow. Yet the analytics sub-segment is expanding fastest at 15.70% CAGR, powered by edge inference, foundation models, and data-lakehouse architectures. Enterprises embed predictive geofencing into ERPs, while authorities model urban heat islands through multi-spectral stacks. Surveying remains steady, reinvented through drone photogrammetry that compresses week-long terrain captures into same-day deliverables.

Telematics gains from electric-vehicle routing and cold-chain monitoring, integrating EV-specific range calculations. Location-based services flourish via hyper-personalized retail apps that trigger in-store promotions, though competition from native smartphone OS APIs keeps vendor margins in check. Overall, the Geographic information system market aligns functional roadmaps around holistic data-fabric principles, merging ingestion, cataloging, and AI pipelines under a single governance umbrella.

By Deployment Mode: Cloud Drives Scalability, Hybrid Ensures Control

On-prem clusters still host 52.85% of deployed instances, favored by defense, utilities, and regulators that demand air-gapped architectures. Cloud footprints, however, grow at a 16.05% CAGR as sovereign-cloud frameworks and FedRAMP-equivalent certifications ease compliance barriers.

The geographic information system market size attributable to cloud subscriptions more than doubles between 2026 and 2031. GPU pools, serverless geospatial SQL, and regional edge zones offer elastic performance for compute-intensive terrain analytics. Yet, rising egress fees spur new patterns of object storage tiering, in-cloud AI inference, and on-orbit compression to keep total cost of ownership predictable. Hybrid blueprints enjoy heightened interest; sensitive telemetry is processed at the edge, while non-confidential layers flow to public clouds for collaboration.

By End-User Industry: Oil and Gas Surges as Digital Twins Mature

Transportation and logistics contributed 28.35% of 2025 revenue, deploying GIS for fleet routing, yard management, and cross-border compliance. Oil and gas posts the fastest climb, charting a 15.90% CAGR as producers layer leak-detection models and regulatory reporting onto refineries’ 3D twins. OMV’s deployment demonstrates how continuous spatial audits shrink inspection downtime and bolster ESG transparency.

Government and defense remain stalwarts, expanding intelligence-surveillance-reconnaissance feeds and next-generation 9-1-1 roll-outs. Utilities accelerate grid digitalization, integrating vegetation-risk analytics and outage prediction. Construction, mining, and telecom realize step-changes through lidar-to-BIM pipelines, pit-wall monitoring, and 5G millimeter-wave siting, respectively. Collectively, these verticals illustrate the widening relevance of the Geographic information system market across physical-asset life cycles.

Geography Analysis

North America preserved 37.80% of 2025 spending, thanks to mature cloud infrastructure, robust R&D funding, and agency mandates like the U.S. Geospatial Data Act that standardize interoperability and metadata. Federal programs secure multi-year budgets for wildfire modeling, broadband equity mapping, and critical-infrastructure resilience. Enterprises such as Trimble invest more than USD 660 million annually in innovation, generating patents that reinforce the region’s technological edge. Yet rising cloud-de-storage fees pose cost challenges for petabyte-class imagery analytics, motivating negotiations for localized sovereign clouds.

Asia-Pacific is on track for the highest 15.95% regional CAGR, fuelled by megacity modernization and infrastructure stimulus. Singapore scales 3D underground mapping to mitigate space constraints, while India’s Digital Twin Mission links logistics corridors with unified parcel-level cadasters. Saudi Arabia’s USD 1 billion digital-twin collaboration with Naver underscores Gulf ambitions for smart-city leadership. Regional hurdles include fragmented data-residency rules and varying export controls, yet domestic satellite launches and sovereign cloud zones are mitigating dependencies.

Europe’s growth remains steady, anchored by the INSPIRE directive that democratizes high-value datasets. Open access spawns start-ups specializing in climate-risk scoring and renewable-siting analytics. GDPR influences architecture design, spurring privacy-enhancing computation and in-region processing. South America, the Middle East, and Africa together represent a smaller base but display accelerated adoption in mineral exploration, precision agriculture, and infrastructure security. These markets often leapfrog legacy systems, adopting cloud-native GIS from inception, thereby enlarging the Geographic information system market size through greenfield demand.

Competitive Landscape

Moderate concentration characterizes the Geographic information system market: Esri, Hexagon, Trimble, Bentley Systems, and HERE Technologies collectively capture an estimated 60% of global revenue. Esri fortifies dominance via quarterly feature releases and a 2,000-member partner ecosystem. Hexagon sharpened its focus by divesting USD 90 million in non-core assets and reinvesting in AI-enabled public-safety modules. Trimble fuses hardware and SaaS, converting device telemetry into subscription dashboards that smooth revenue volatility.

Consolidation accelerates: KKR acquired IQGeo for USD 333 million to penetrate telecom network orchestration, [4]KKR, “KKR Completes Acquisition of Geospatial Software Business IQGeo,” KKR.COM while Siemens closed a USD 10 billion deal for Altair, marrying simulation with geospatial digital twins. Meanwhile, HERE and AWS committed USD 1 billion over ten years to embed AI-rich mapping into software-defined vehicles. Start-ups such as Mach9 secured USD 12 million to speed lidar point-cloud processing by 96 times, threatening incumbent workflows.

Competitive levers shift toward AI model libraries, edge-optimized runtimes, and sector-specific solutions. Vendors embed large language models to translate natural-language prompts into spatial queries, broadening user reach beyond GIS specialists. Regulatory licenses for sub-30 cm imagery act as defensive moats, while open-source geocoding and vector-tile engines erode lock-in elsewhere. Ultimately, players able to deliver turnkey, compliance-ready, and cloud-agnostic offerings command premium valuation multiples across the Geographic information system market.

Geographic Information System Industry Leaders

Environmental Systems Research Institute, Inc. (Esri)

Hexagon AB

Trimble Inc.

Autodesk, Inc.

Bentley Systems, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: EarthDaily secured a USD 60 million loan financing to accelerate satellite-constellation expansion, boosting temporal resolution for commercial imagery services.

- August 2025: MDA Space won a USD 1.3 billion contract from EchoStar to build the first 3GPP-compliant low-Earth-orbit 5G network, with options pushing the value to USD 2.5 billion.

- July 2025: Hexagon AB sold non-core business assets in its Safety, Infrastructure & Geospatial unit, divesting revenue streams worth USD 90 million to double down on software subscriptions.

- July 2025: Esri partnered with Google Maps Platform to embed photorealistic 3D tiles covering 2,500 cities into ArcGIS, elevating urban-planning visualization.

- March 2025: Siemens completed the USD 10 billion acquisition of Altair, aligning CAE simulations with geospatial digital-twin workflows.

- January 2025: HERE Technologies inked a 10-year, USD 1 billion alliance with AWS to co-develop AI-powered mapping engines for automotive OEMs.

Global Geographic Information System Market Report Scope

Geographic Information Systems (GIS) store, analyze, and visualize data for geographic positions on the Earth's surface. GIS is a computer-based tool that examines spatial relationships, patterns, and trends. By connecting geography with data, GIS better understands data using a geographic context.

The Geographic Information System market is segmented by component (hardware and software), by function (mapping, surveying, telematics and navigation, location-based services), by end-user (agriculture, utilities, and mining, among others), and by geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| Mapping |

| Surveying |

| Telematics and Navigation |

| Location-based Services |

| Geospatial Data Management and Analysis |

| On-premise |

| Cloud |

| Agriculture |

| Utilities |

| Mining |

| Construction |

| Transportation and Logistics |

| Oil and Gas |

| Government and Defence |

| Telecommunications |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Function | Mapping | ||

| Surveying | |||

| Telematics and Navigation | |||

| Location-based Services | |||

| Geospatial Data Management and Analysis | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

| By End-user Industry | Agriculture | ||

| Utilities | |||

| Mining | |||

| Construction | |||

| Transportation and Logistics | |||

| Oil and Gas | |||

| Government and Defence | |||

| Telecommunications | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big will location-intelligence spending be by 2031?

The Geographic information system market is projected to reach USD 31.8 billion by 2031, nearly doubling 2026 levels at a 13.94% CAGR.

Which component outperforms over the next five years?

Services, thanks to cloud migration and managed-support demand, is forecast to grow at 15.45% CAGR, ahead of software and hardware.

Why does Asia-Pacific post the fastest growth rate?

Government-funded smart-city programs, mega-infrastructure builds, and high mobile-device penetration propel a 15.95% regional CAGR.

What limits adoption in utilities?

Integrating modern GIS with legacy SCADA increases project complexity, imposes cybersecurity requirements, and extends timelines.

How is AI changing geospatial analytics?

On-orbit and cloud inference now classifies satellite imagery in minutes, enabling rapid crop-health, defense, and climate-risk insights.

Which recent deal signals rising consolidation?

KKR’s USD 333 million purchase of IQGeo highlights private-equity interest in telecom-centric geospatial platforms.

Page last updated on: