Reporter Gene Assay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

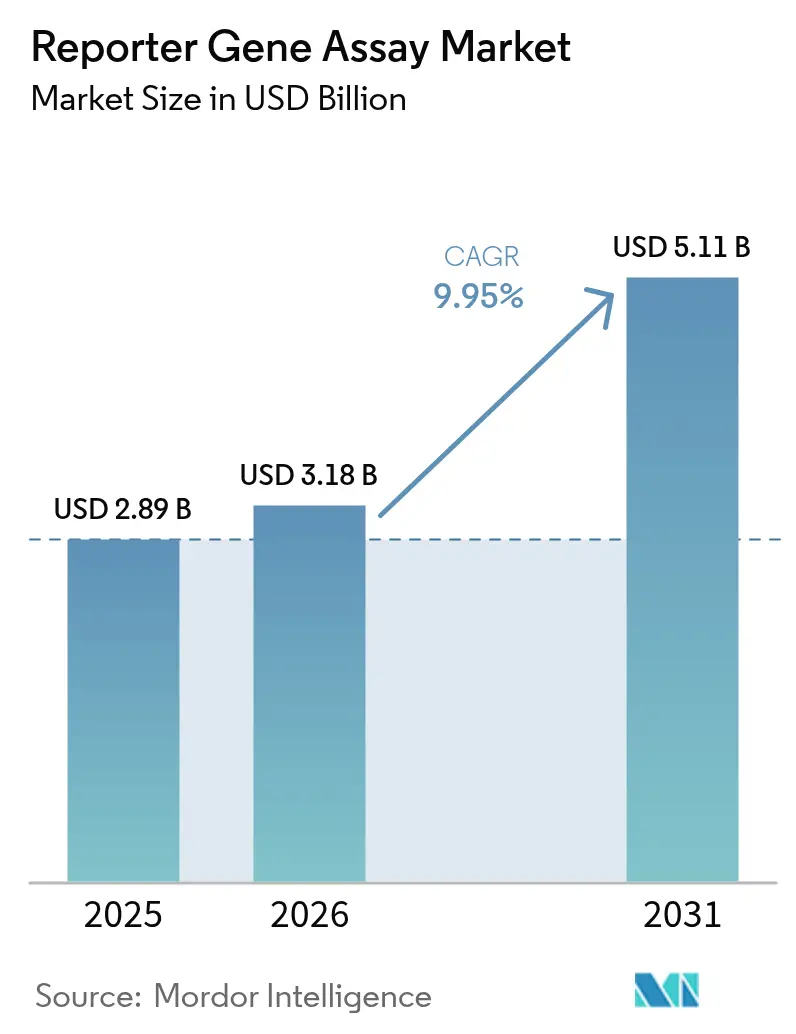

| Market Size (2026) | USD 3.18 Billion |

| Market Size (2031) | USD 5.11 Billion |

| Growth Rate (2026 - 2031) | 9.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reporter Gene Assay Market Analysis by Mordor Intelligence

The reporter gene assay market size is expected to grow from USD 2.89 billion in 2025 to USD 3.18 billion in 2026 and is forecast to reach USD 5.11 billion by 2031 at 9.95% CAGR over 2026-2031. Robust demand stems from higher life-sciences R&D budgets, broader adoption of precision-medicine programs, and the migration of assays onto AI-enabled high-throughput platforms that shorten discovery timelines. Growth is further reinforced by the expanding pipeline of cell- and gene-therapy candidates that rely on sensitive functional-genomics readouts for potency and safety testing. The reporter gene assay market also benefits from rising outsourcing to CRO and CRDMO partners that bundle assay development with manufacturing, thereby lowering total project costs and accelerating scale-up. Despite the upbeat outlook, capital-investment hurdles and heterogeneous regulatory frameworks around genetically modified constructs weigh on near-term uptake, especially for smaller institutes.

Key Report Takeaways

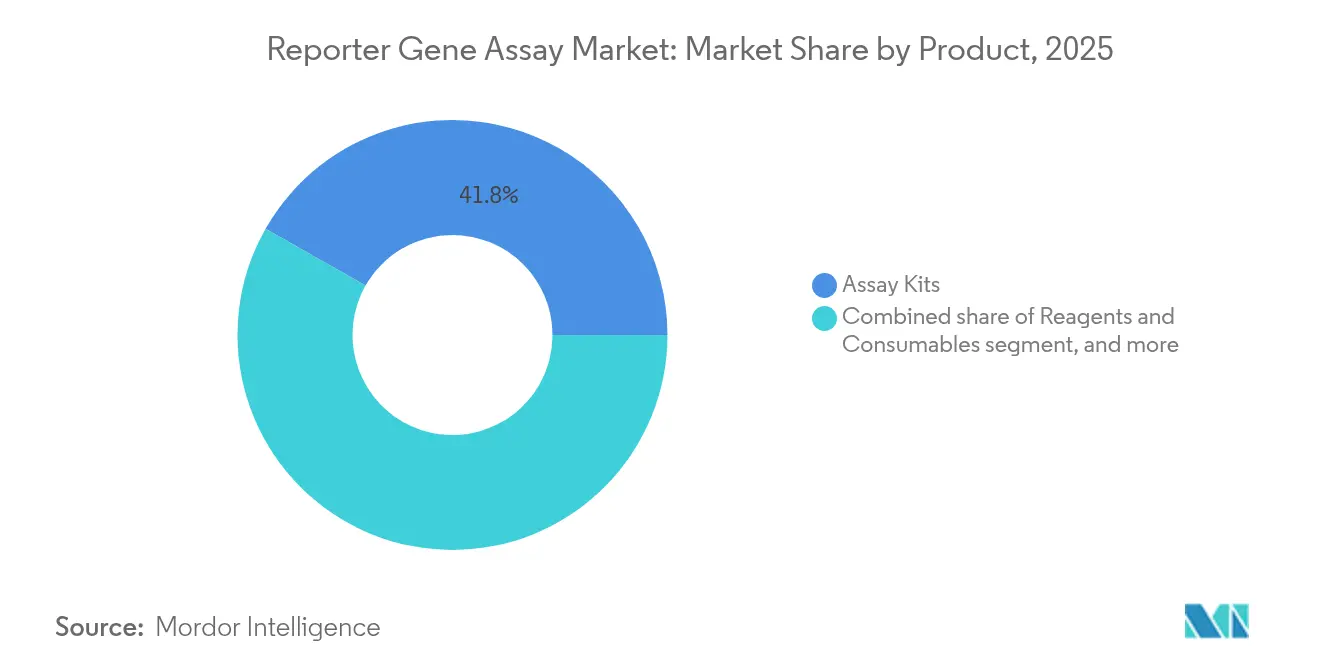

- By product, Assay Kits captured 41.78% of reporter gene assay market share in 2025 and Instruments & Software is projected to expand at a 12.27% CAGR through 2031.

- By application, Gene Regulation Studies held 37.02% of the reporter gene assay market size in 2025, while Cell Signaling Pathways is forecast to grow at 13.29% CAGR to 2031.

- By detection method, Luminescence commanded 70.85% share of the reporter gene assay market size in 2025; Bioluminescent Imaging In-vivo is advancing at a 12.5% CAGR through 2031.

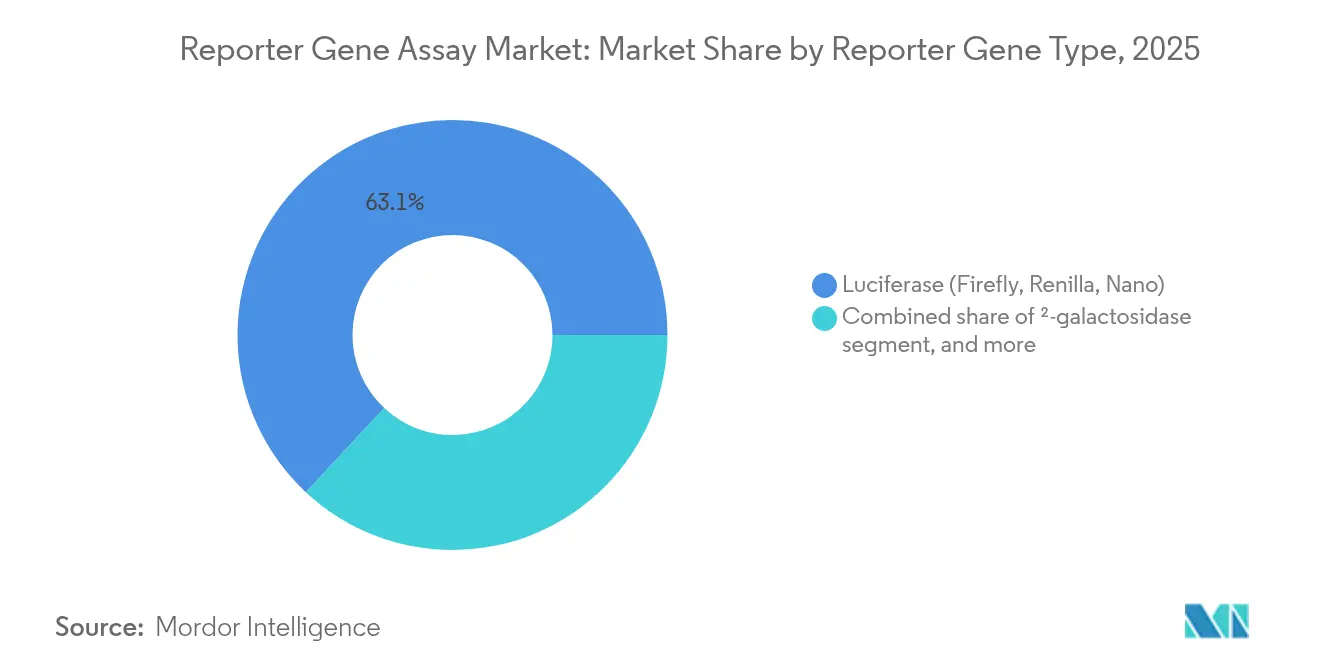

- By reporter gene type, Luciferase systems accounted for 63.05% of the reporter gene assay market share in 2025, whereas GFP/RFP & Variants are set to post a 12.61% CAGR during 2026-2031.

- By end user, Pharma & Biotech Companies represented 48.02% of the reporter gene assay market size in 2025, and CROs & CDMOs are rising fastest at 13.18% CAGR.

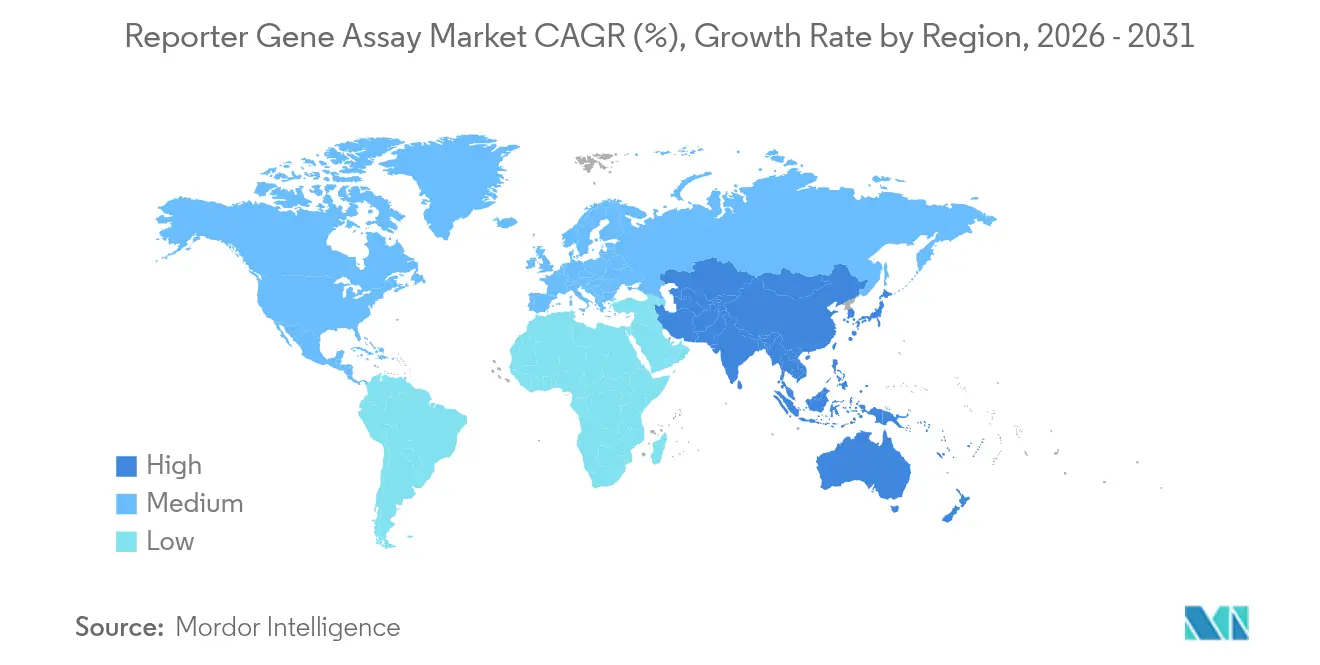

- By geography, North America led with 41.96% revenue share in 2025; Asia-Pacific is projected to register the highest 11.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Reporter Gene Assay Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing investment in life-sciences R&D | +2.8% | Global, concentrated in North America & EU | Long term (≥ 4 years) |

| Expanding applications of reporter gene assays in drug discovery & development | +2.1% | Global, with spill-over from APAC to MEA | Medium term (2-4 years) |

| Rising demand for personalized medicine and gene & cell therapies | +1.9% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Technological advances in high-throughput screening platforms | +1.7% | Global, early adoption in North America | Short term (≤ 2 years) |

| Increasing prevalence of chronic & genetic diseases requiring functional genomics | +1.2% | Global, higher impact in aging populations | Long term (≥ 4 years) |

| Supportive government funding and academia–industry collaborations | +0.8% | APAC core, significant in China & India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Investment in Life-Sciences Research and Development

Record-high corporate and public R&D budgets continue to widen the installed base of advanced reporter systems. Pharmaceutical companies alone spent USD 288 billion in 2024, lifting demand for assays that streamline target validation and mechanism-of-action studies. Strategic acquisitions funnel additional capital toward next-generation constructs that deliver higher sensitivity and automation compatibility. Long-range forecasts show global R&D outlays could surpass USD 340 billion by 2030, anchoring stable multiyear order pipelines for reagents, kits, and integrated platforms. As budgets scale, the reporter gene assay market gains resilience against cyclical funding dips. This sustained spending posture underpins stronger vendor pricing power and fuels continuous innovation cycles.

Expanding Applications in Drug Discovery and Development

Reporter-based readouts have evolved beyond transcriptional-control screens into sophisticated, cellular-pathway interrogation tools. Optogenetic platforms now permit light-induced activation of integrated-stress responses, enabling compound libraries to be triaged for pathway-specific modulators with minimal cytotoxicity. Automated patch-clamp instruments coupled with reporter constructs accelerate ion-channel drug discovery by delivering real-time functional data at single-cell resolution. Machine-learning analytics embedded in screening workflows cut false-positive rates and sharpen structure-activity relationship insights. The reporter gene assay market therefore becomes indispensable to lead-optimization campaigns that demand high fidelity and throughput. Elevating functional-screen success rates shortens attrition in late-stage pipelines, yielding better capital efficiency for sponsors.

Rising Demand for Personalized Medicine and Gene & Cell Therapies

Cell- and gene-therapy pipelines are scaling exponentially, with annualized growth exceeding 36% through 2030, requiring precise in-vivo monitoring of therapeutic constructs. Reporter assays allow direct visualization of gene-editing activity, transgene expression, and engineered-cell homing. The clinical clearance of CRISPR-based treatments such as CASGEVY, which achieved 96.7% crisis-free status in sickle-cell patients, illustrates the high stakes tied to functional readouts. Multimodal reporter platforms that merge bioluminescence, impedance, and fluorescence give clinicians quantitative dashboards for real-time therapy stewardship. Consequently, the reporter gene assay market will see expanding adoption within clinical-manufacturing quality-control regimes as advanced therapies commercialize.

Technological Advancements in High-Throughput Screening Platforms

Integration of AI, microfluidics, and 3D cell culture has ushered in a new era of screening density and data richness. Systems such as HCS-3DX perform automated 3D high-content screening at single-cell granularity, resolving heterogeneity that masks therapeutic windows[1]Wei Z. et al., “HCS-3DX Enables 3D High-Content Screening,” biorxiv.org. De novo-designed bioluminescent proteins with tunable emission spectra are being inserted into multiplex assays, enabling parallel tracking of several pathways inside the same well. Firefly-inspired biosensors now scan 700-compound libraries for orphan GPCR activators pertinent to Alzheimer’s disease. By compressing run-times and enhancing analytic depth, these innovations reinforce the competitive edge of high-throughput adopters and propel additional capital formation in the reporter gene assay market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operational costs of advanced assay instrumentation | -1.8% | Global, stronger impact in emerging markets | Short term (≤ 2 years) |

| Stringent regulatory and biosafety requirements for genetically modified assays | -1.2% | North America & EU, expanding globally | Medium term (2-4 years) |

| Intellectual property and licensing barriers for reporter gene technologies | -1.0% | Global, pronounced in regions with dense CRISPR patent filings | Medium term (2-4 years) |

| Technical challenges related to assay sensitivity, standardization, and reproducibility | -0.9% | Global, affecting cross-lab studies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Operational Costs of Advanced Assay Instrumentation

Fully automated reporter systems often exceed USD 1 million, making procurement difficult for smaller institutes and labs. Annual service contracts can add another 15-20% of equipment cost, stretching operational budgets. Although streamlined platforms such as the Aptegra genetic-stability assay cut testing time by 66% and reduce expenses by 43%, capex remains a gating factor for many users. Emerging secretory-horseradish-peroxidase constructs that deliver nine-fold cost savings versus classical luciferase help to democratize access, but switching assays requires method-validation resources that are themselves expensive. Until price points align with mid-tier-lab economics, diffusion of advanced hardware could lag behind technology readiness, moderating near-term expansion of the reporter gene assay market.

Stringent Regulatory and Biosafety Requirements for Genetically Modified Assays

Revised FDA genome-editing guidance mandates exhaustive analytical and biodistribution profiling for every modified construct, lengthening development timelines[2]U.S. Food & Drug Administration, “Human Genome Editing: Guidance for Industry,” federalregister.gov. ICH Q5A(R2) viral-safety updates further expand documentation burdens, compelling assay developers to conduct multi-tier viral contamination checks. Environmental-risk assessments for gene-therapy vectors add parallel approval layers that differ by jurisdiction, complicating multi-site clinical programs. NIH recombinant-DNA guidelines impose institutional biosafety-committee oversight and contain a host of containment prerequisites updated in 2024. Collectively these frameworks, though vital for public safety, elevate compliance costs and slow the rate at which innovative reporters reach market, thereby placing a drag on the overall reporter gene assay market trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Automated Platforms Accelerate Adoption

Assay Kits delivered 41.78% of 2025 revenue, underscoring their indispensability as recurring consumables across academic and industrial labs. Reagent demand scales directly with experiment volume, and bulk purchasing agreements further entrench kit penetration in core workflows. Instruments & Software, however, are projected to expand at 12.27% CAGR as laboratories transition toward fully integrated solutions that consolidate liquid handling, detection, and data analytics. The reporter gene assay market size for integrated instrumentation is growing in sync with efforts to counter reproducibility challenges by embedding QC checkpoints and algorithmic error detection. Vendors increasingly bundle proprietary analysis suites that automate endpoint interpretation, driving total cost of ownership lower over multiyear use cycles.

Reagents & Consumables remain critical for specialty protocols such as dual-luciferase normalization, maintaining steady demand even as kit formats evolve toward ready-to-use multiplex configurations. Services & Custom Assay Development gain momentum because many sponsors lack in-house capacity to design bespoke reporters for novel targets. CROs combine bioinformatics pipelines with wet-lab resources to shorten assay-development sprints, strengthening their value proposition within the reporter gene assay industry. Overall, product diversification, recurrent-revenue channels, and platform convergence together reinforce the growth engine of this market segment.

By Application: Pathway Mapping Gains Traction

Gene regulation studies accounted for 37.02% of 2025 revenue, reflecting the enduring relevance of promoter- and enhancer-driven luciferase screens in foundational molecular biology. Oncology-oriented assays leverage similar constructs to track transcriptional-reprogramming responses to targeted therapies, aligning with precision-oncology roadmaps. Drug-Discovery/HTS screens integrate reporter readouts to triage hits by functional potency in large-compound libraries, cementing an essential role for high-throughput formats within pharmaceutical research. Other emerging areas such as neuroscience exploit calcium-sensitive reporters to visualize neuronal-circuit dynamics.

Cell signaling pathways are expected to post a 13.29% CAGR as new biosensors reveal spatiotemporal signaling cascades with single-cell granularity. For instance, CCR2 ligand-sensing constructs allow real-time chemokine-gradient mapping in live tissues, which advances inflammation and oncology research. The reporter gene assay market share captured by pathway-centric applications will widen as multiplex biosensors merge with CRISPR-based perturbation libraries. Far-red calcium indicators now penetrate thick tissues without phototoxicity, permitting chronic imaging in preclinical disease models. These innovations situate pathway analysis at the next frontier of functional genomics, driving continued adoption across translational-research teams.

By Detection Method: Imaging Revolution Enhances Versatility

Luminescence methods dominated 70.85% of 2025 sales due to unmatched signal-to-noise ratios and the convenience of glow-type substrates that facilitate kinetic assays. Fluorescence detection remains entrenched in multiplex campaigns where spatial resolution is paramount, aided by continuous expansion of fluorescent-protein color palettes. Colorimetric/Absorbance readouts retain niche utility for low-resource settings and education.

Bioluminescent Imaging In-vivo will deliver 12.5% CAGR, outpacing other detection modes. Artificial-luciferase variants with improved thermostability now support longitudinal tumor-burden tracking in small-animal models without high background noise. Comparative data indicate GFP detection needs only 100 ms exposure versus 30 s for luciferase, yet the latter’s superior dynamic range still governs deep-tissue applications. Continuous emission color shifting observed in Amydetes vivianii luciferase extends functional use to pH-dependent cellular-microenvironment monitoring. Consequently, the reporter gene assay market size attributed to in-vivo imaging modules will climb steadily as life-science teams broaden usage beyond oncology into regenerative medicine and infectious-disease surveillance.

By Reporter Gene Type: Fluorescent Proteins Narrow the Gap

Luciferase systems held 63.05% of 2025 revenue, underwritten by firefly, Renilla, and NanoLuc variants that respectively optimize brightness, dual-reporter normalization, and ultra-small mass for viral-vector packaging. β-galactosidase continues serving colorimetric beta-gal screens in educational labs, whereas SEAP/Gaussia reporters satisfy secretion assays that obviate cell lysis.

GFP/RFP & Variants are forecast to record a 12.61% CAGR as engineering breakthroughs such as SNAP-tag2 yield 100-fold faster labeling and five-fold brighter emissions. The current fluorescent palette encompasses 20 colors, enabling simultaneous lineage tracing of multiple cell populations in organoid models. New probes such as far-red GECO indicators extend imaging penetration depth in vivo, supporting neuroscience and cardiology research that demand minimal light scattering. High-sensitivity temperature reporters like gMELT add physiological-parameter tracking to gene-expression assays, signaling greater functional diversity ahead. Collectively these advances should erode luciferase’s volume premium, though the reporter gene assay market will likely maintain dual-technology coexistence.

By End User: Outsourcing Momentum Reshapes Demand Patterns

Pharma & Biotech Companies generated 48.02% of 2025 revenue by deploying reporters across the entire discovery-to-clinical continuum. Academic laboratories remain pivotal incubators for tool innovation and training ground for new assay methodologies. Clinical and diagnostic facilities adopt specialized reporter constructs for gene-therapy potency assays and rare-disease diagnostics.

CROs & CDMOs will grow at 13.18% CAGR, enlarging the reporter gene assay market size allocated to outsourced testing. Integrated CRDMO models bundle discovery assays, process development, and GMP manufacturing, offering a one-stop-shop value proposition attractive to lean biotech sponsors. The global contract-manufacturing sector could exceed USD 200 billion by 2032, validating scale-economy drivers that justify capital expenditures on high-end reporter equipment. Recent transactions, such as Agilent’s USD 925 million acquisition of BIOVECTRA, illustrate strategic alignment between assay technology providers and advanced biologics manufacturing capacity. Outsourcing therefore stands as a durable growth catalyst for the reporter gene assay market.

Geography Analysis

North America captured 41.96% of 2025 revenue on the back of the world’s deepest R&D funding pools, well-defined regulatory pathways, and the highest concentration of biopharmaceutical headquarters. The United States anchors this dominance through sustained National Institutes of Health appropriations and venture-capital ecosystems that continually spin out platform companies. Canada adds momentum via targeted incentives for genomic medicine and expanding GMP manufacturing clusters, while Mexico’s growing generics-production base sources reporters for lot-release testing. Despite stringent oversight, FDA clarity accelerates commercialization cycles for innovative reporter configurations, providing a policy advantage that supports consistent growth within the reporter gene assay market.

Asia-Pacific is expected to clock an 11.2% CAGR, outpacing all other regions. China remains the centerpiece, channeling multibillion-dollar life-sciences grants into oncology and regenerative medicine programs that standardize reporter assays as potency markers. Japan’s healthcare focus on aging-population needs spurs adoption of reporter-enabled biomarker panels in neurodegeneration research. India’s rapidly scaling CRO sector leverages competitive labor costs to pull in discovery workloads that require high-throughput reporter screening. South Korea’s emphasis on biologics manufacturing quality spurs demand for rapid lot-release assays that rely on secreted reporters. Cross-border partnerships with multinational pharmas accelerate technology transfer, tightening APAC’s integration into the global reporter gene assay market.

Europe delivers steady though slower gains, supported by entrenched pharmaceutical manufacturing and strong academic consortia. Germany tops regional usage thanks to high per-capita R&D spend and advanced precision-medicine initiatives. The United Kingdom, despite regulatory divergence post-Brexit, maintains assay-development vitality through its Golden Triangle universities. France, Italy, and Spain increasingly outsource manufacturing, creating incremental assay demand for process analytics. Intellectual-property debates around new genomic techniques and field trials for gene-edited crops introduce some uncertainty, yet EMA guidance on advanced therapy products provides predictable pathways for clinical reporter deployment. Consequently, Europe’s role in the reporter gene assay market will remain pivotal for standards harmonization and technology validation.

Competitive Landscape

The reporter gene assay market features moderate fragmentation, with Thermo Fisher Scientific, PerkinElmer, and Merck KGaA leading on breadth of integrated solutions and global distribution reach. These incumbents continually refresh product suites by layering AI-driven analytics over established luciferase and fluorescent platforms. Mid-sized innovators focus on niche specializations such as optogenetic reporters and secreted-enzyme systems that slash assay cost. Patent-thicket complexity—over 11,000 CRISPR-related filings—creates defensive-licensing strategies that favor players with robust intellectual-property counsel.

Technology partnerships have intensified: Bio-Techne now co-markets USP reference standards bundled with its Maurice platform, furnishing turnkey CMC analytical packages. MilliporeSigma’s Aptegra assay showcases how consolidation of multiple genetic-stability tests into one run wins share by shrinking timelines and budgets. Artificial-intelligence entrants like GenBio AI simulate in-silico organism responses and export suggested reporter constructs, potentially stripping months out of assay-design cycles. The net effect is a fight for solution-level differentiation wherein data-analysis prowess and regulatory-compliance tooling weigh as heavily as reagent performance.

Emerging white-space segments include de novo-designed, color-shiftable bioluminescent proteins that operate without exogenous substrates, which could displace luciferase in long-term imaging protocols. Companies that integrate microfluidics with 3D culture and reporters hold an edge in modeling human-tissue responses. Overall, competitive success hinges on deep domain expertise across chemistry, optics, and informatics, coupled with flexible licensing models that mitigate IP-gridlock threats within the reporter gene assay market.

Reporter Gene Assay Industry Leaders

PerkinElmer, Inc

Merck KGaA

Bio-Rad Laboratories, Inc

Promega Corporation

Thermo Fisher Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Chugai Pharmaceutical, SoftBank, and SB Intuitions began a generative-AI joint-research program to accelerate clinical-development timelines by deploying large-language models for protocol optimization.

- July 2024: Agilent Technologies agreed to acquire BIOVECTRA for USD 925 million, gaining sterile fill-finish and mRNA capabilities that complement its gRNA manufacturing expertise.

- April 2024: MilliporeSigma introduced the Aptegra CHO genetic-stability assay, an all-in-one test that consolidates five legacy assays, trimming turnaround by 66%.

- September 2024: QIAGEN added 100 validated digital-PCR assays to its QIAcuity platform, targeting cancer, inherited disorders, and infectious-disease surveillance.

- August 2024: QIAGEN deepened collaboration with AstraZeneca to co-develop companion diagnostics on the QIAstat-Dx system for chronic-disease genotyping.

- June 2024: Bio-Techne signed a distribution pact with U.S. Pharmacopeia to package monoclonal-antibody and rAAV reference standards with its Maurice analyzer.

Global Reporter Gene Assay Market Report Scope

As per the scope of this report, the reporter gene assists in recognizing a specific gene that has required expression or not in organisms. These reporter genes are also used as markers in the screening of transformed cells for research in gene expression and other processes. The Reporter Gene Assay Market is by Product (Assay Kits and Reagents), Application (Gene Regulation, Cell signaling pathways, and Others), and Geography ( North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values in USD million for the above segments.

| Assay Kits |

| Reagents & Consumables |

| Instruments & Software |

| Services & Custom Assay Development |

| Gene Regulation Studies |

| Cell Signaling Pathways |

| Drug-Discovery / HTS |

| Oncology / Tumor Biology |

| Other Applications |

| Luminescence |

| Fluorescence |

| Colorimetric / Absorbance |

| Bioluminescent Imaging In-vivo |

| Luciferase (Firefly, Renilla, Nano) |

| ?-galactosidase |

| GFP / RFP & Variants |

| SEAP / Gaussia |

| Pharma & Biotech Companies |

| Academic & Research Institutes |

| CROs & CDMOs |

| Clinical & Diagnostic Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Assay Kits | |

| Reagents & Consumables | ||

| Instruments & Software | ||

| Services & Custom Assay Development | ||

| By Application | Gene Regulation Studies | |

| Cell Signaling Pathways | ||

| Drug-Discovery / HTS | ||

| Oncology / Tumor Biology | ||

| Other Applications | ||

| By Detection Method | Luminescence | |

| Fluorescence | ||

| Colorimetric / Absorbance | ||

| Bioluminescent Imaging In-vivo | ||

| By Reporter Gene Type | Luciferase (Firefly, Renilla, Nano) | |

| ?-galactosidase | ||

| GFP / RFP & Variants | ||

| SEAP / Gaussia | ||

| By End User | Pharma & Biotech Companies | |

| Academic & Research Institutes | ||

| CROs & CDMOs | ||

| Clinical & Diagnostic Labs | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of reporter gene assays?

Global revenue stood at USD 3.18 billion in 2026 and is projected to reach USD 5.11 billion by 2031, reflecting a 9.95% CAGR.

Which product category generates the most revenue in reporter gene assays?

Assay Kits contributed 41.78% of global 2025 revenue, benefiting from their recurring-consumable nature.

Which application area is expanding fastest within reporter gene assays?

Cell Signaling Pathways are projected to grow at a 13.29% CAGR through 2031, outpacing all other applications.

Which detection technology holds the largest share in reporter gene assays?

Luminescence platforms dominated with 70.85% share in 2025 due to their superior sensitivity and dynamic range.

Which region is expected to grow quickest for reporter gene assays?

Asia-Pacific is forecast to post the fastest 11.2% CAGR between 2026 and 2031, driven by strong cell- and gene-therapy investment.

How is outsourcing to CROs and CDMOs influencing uptake of reporter gene assays?

Greater reliance on integrated service providersÑgrowing at 13.18% CAGRÑboosts demand for advanced, high-throughput reporter assays that shorten development timelines.

Page last updated on: