Isothermal Nucleic Acid Amplification Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

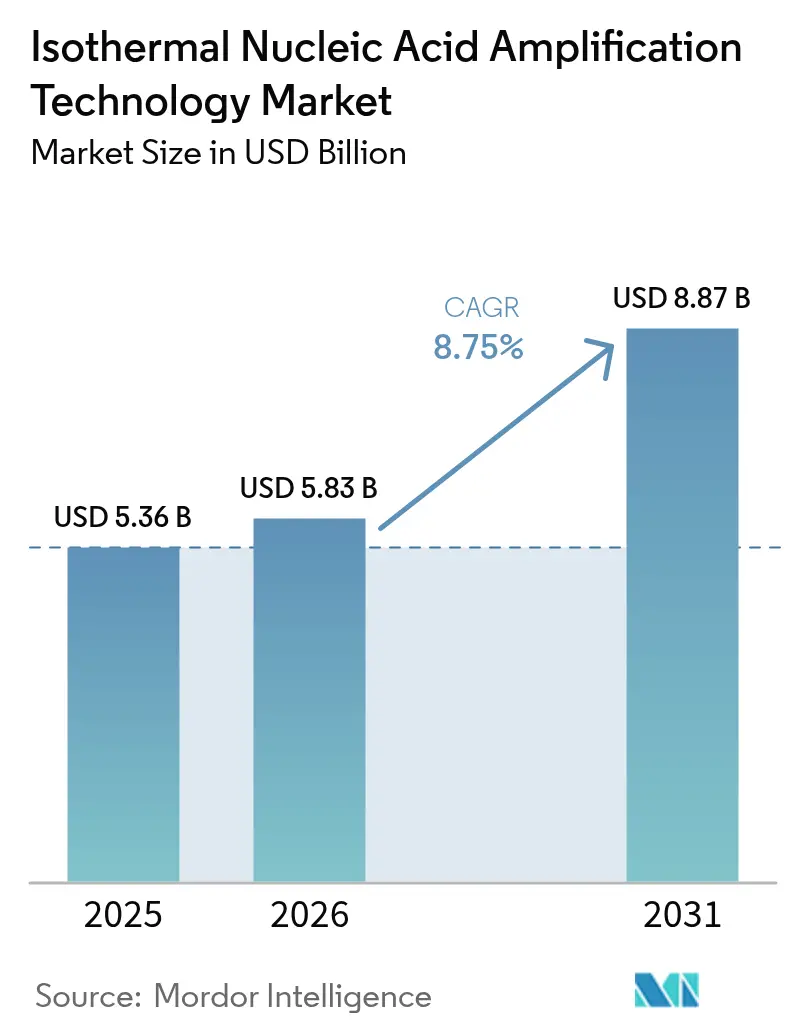

| Market Size (2026) | USD 5.83 Billion |

| Market Size (2031) | USD 8.87 Billion |

| Growth Rate (2026 - 2031) | 8.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Isothermal Nucleic Acid Amplification Technology Market Analysis by Mordor Intelligence

The Isothermal Nucleic Acid Amplification Technology market size is expected to grow from USD 5.36 billion in 2025 to USD 5.83 billion in 2026 and is forecast to reach USD 8.87 billion by 2031 at 8.75% CAGR over 2026-2031.

Growth is fuelled by constant-temperature amplification, which removes the need for bulky thermal cyclers and supports rapid point-of-care testing. Hospitals deploy INAAT platforms in emergency units to cut result turnaround from hours to minutes, while reagent suppliers benefit from steady, high-margin consumable sales. Manufacturers are integrating microfluidics, lyophilised reagents and colourimetric detection that lower per-test costs and broaden use in non-laboratory settings. Asia-Pacific adoption accelerates as streamlined device approvals shorten time-to-market, whereas North America leads on revenue owing to established reimbursement frameworks.

Key Report Takeaways

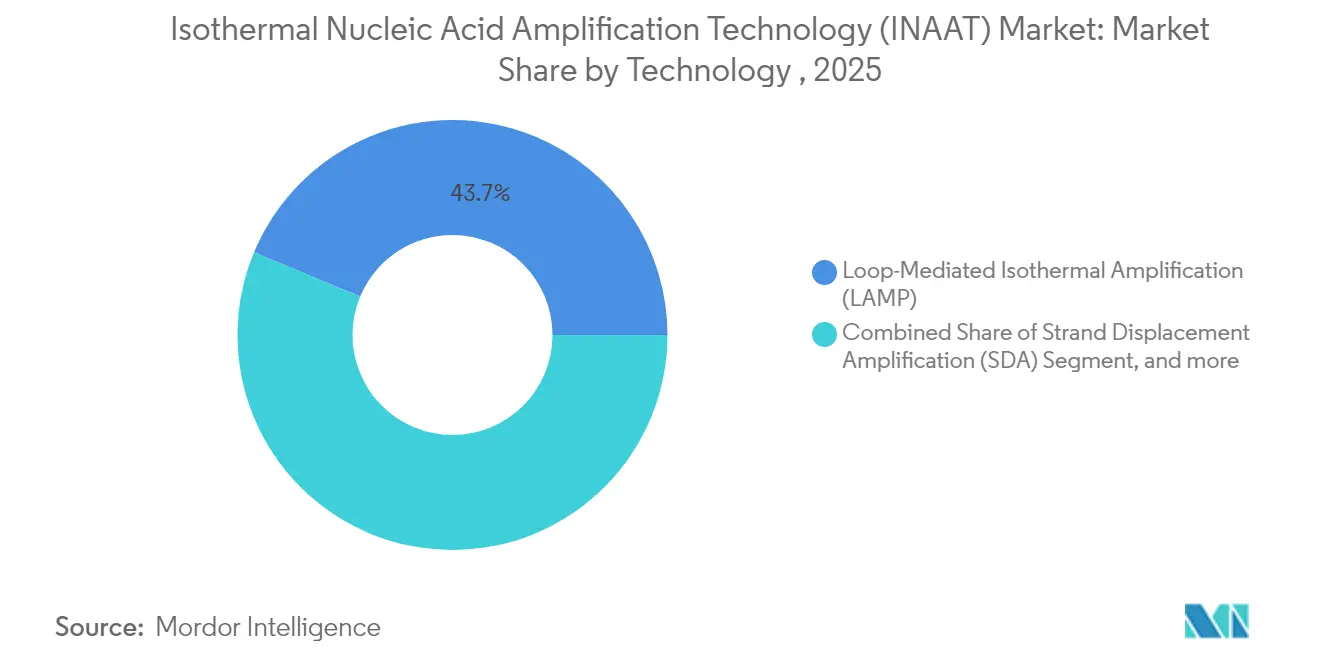

- By technology, Loop-Mediated Isothermal Amplification (LAMP) led with 43.72% revenue share in 2025 and is projected to record a 13.02% CAGR through 2031.

- By product, reagents and consumables accounted for 62.94% of 2025 revenue, while instruments are expected to expand at an 10.98% CAGR to 2031.

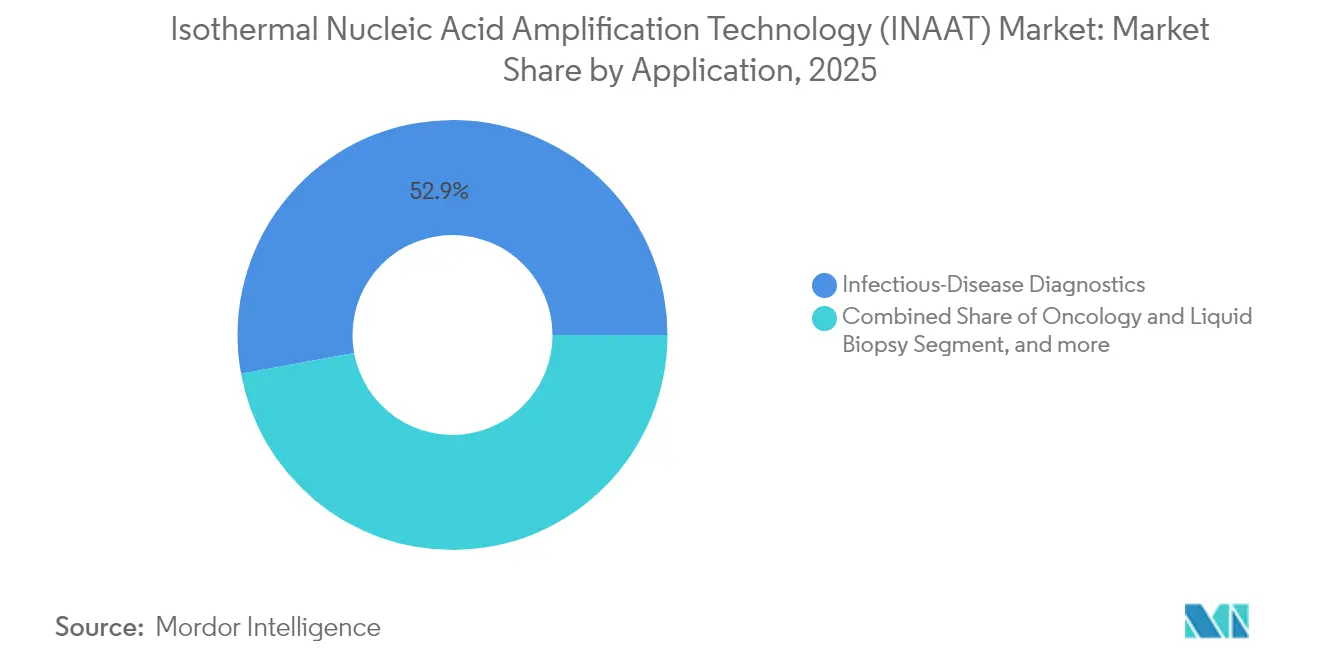

- By application, infectious-disease testing held 52.88% of the Isothermal Nucleic Acid Amplification Technology market share in 2025; oncology and liquid biopsy are forecast to grow at a 15.62% CAGR.

- By end user, hospitals and reference laboratories held 56.12% share in 2025; point-of-care sites are projected to grow at an 11.28% CAGR.

- By region, North America captured 35.12% revenue in 2025, whereas Asia-Pacific is set to log a 15.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Isothermal Nucleic Acid Amplification Technology Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Point-of-Care Infectious-Disease Adoption | +2.1% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Aging Population & Chronic-Disease Burden | +1.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Workflow Shift from PCR to INAAT | +1.5% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Lower Per-Test Cost Economics | +1.3% | Global, accelerated in emerging markets | Short term (≤ 2 years) |

| Microfluidic Battery-Powered Cartridges | +0.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| CRISPR-Enhanced Assay Specificity | +0.7% | Global, led by research institutions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Point-of-care infectious-disease adoption

Emergency departments now rely on INAAT respiratory panels that deliver lab-quality answers in minutes, boosting patient throughput and antibiotic stewardship. FDA clearance of Cepheid’s Xpert HCV in June 2024 allows same-visit hepatitis C diagnosis from a fingertip blood sample, a milestone that removes multi-visit loss to follow-up.[1]U.S. Food and Drug Administration, “FDA Authorizes First Point-of-Care Hepatitis C Test,” fda.gov Result accuracy remains on par with PCR while constant-temperature reactions suit battery-powered, portable devices useful in resource-limited settings.

Aging population & chronic-disease burden

Populations over 65 years demand regular biomarker checks for infections and cancer recurrence. INAAT-based liquid-biopsy systems can detect minimal residual disease with 94.1% sensitivity, enabling home or community clinic monitoring.[2]Nature Communications, “Portable Dragonfly Platform Enables Field Molecular Diagnostics,” nature.com Integration with telemedicine platforms streamlines result review, curbing unnecessary hospital visits and lowering system costs.

Workflow shift from PCR to INAAT

Clinical labs that transition to LAMP report 60% less hands-on time because extraction steps are simplified and reactions run at a single 60-65 °C setting.[3]Frontiers in Cellular and Infection Microbiology, “Automation-Compatible LAMP Workflows Reduce Hands-On Time,” frontiersin.org Lyophilised reagent cups ship at ambient temperature and slot into existing automation lines, keeping throughput high while cutting maintenance needs typical of thermal cyclers.

Lower per-test cost economics

Instrument capital costs fall by roughly 40% when constant-temperature heaters replace multi-zone cyclers. Colourimetric readouts remove expensive optics, pushing high-volume per-test costs below USD 5 for respiratory targets. Room-temperature reagent stability trims 20-30% from cold-chain spend in emerging economies, accelerating deployment.

Restraints Impact Analysis of Isothermal Nucleic Acid Amplification Technology Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition From PCR & DCR Platforms | -1.9% | Global, strongest in established markets | Medium term (2-4 years) |

| Awareness And Reimbursement Gaps | -1.4% | North America & EU primarily | Short term (≤ 2 years) |

| Enzyme-Supply Volatility for Bst Reagents | -0.8% | Global, acute in supply-constrained regions | Short term (≤ 2 years) |

| Stringent CLIA-Waiver / IVDR Evidence Hurdles | -1.1% | North America & EU regulatory domains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition From PCR & DCR Platforms

Established PCR infrastructure represents significant switching costs for laboratories that have invested in thermal cycling platforms, automated sample handling systems, and technician training programs optimized for traditional amplification workflows. Digital PCR platforms further intensify competition by offering absolute quantification capabilities that INAAT currently cannot match, particularly in applications requiring precise viral load monitoring or copy number variation analysis. Laboratory directors cite workflow disruption concerns when evaluating INAAT adoption, as existing quality control procedures, regulatory validations, and staff competencies align with PCR methodologies.

Awareness and Reimbursement Gaps

Healthcare payer recognition of INAAT clinical utility lags behind technology capabilities, creating reimbursement uncertainties that limit adoption in cost-sensitive healthcare environments. Medicare's MolDX program requires extensive clinical evidence demonstrating diagnostic accuracy and patient outcome improvements before establishing coverage policies for novel molecular diagnostic technologies. The evidence generation process typically requires 18-24 months of clinical data collection, during which INAAT developers must fund studies without guaranteed reimbursement outcomes. Physician awareness of INAAT capabilities remains limited outside infectious disease specialties, with many clinicians defaulting to familiar PCR-based testing despite potential advantages in turnaround time and point-of-care deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Isothermal Nucleic Acid Amplification Technology Market Segment Analysis

By Technology:

LAMP Dominance Drives InnovationLAMP captured 43.72% of the Isothermal Nucleic Acid Amplification Technology market in 2025 and is forecast to grow at 13.02% CAGR to 2031. The methodology targets six gene regions, conferring high specificity without thermal cycling. Complementary approaches like HDA and NEAR address low-temperature use cases, while TMA retains value in blood screening where RNA detection matters.

Detection innovation is reshaping the Isothermal Nucleic Acid Amplification Technology market as developers pair LAMP with CRISPR–Cas systems to reach attomolar sensitivity in 30 minutes. Colourimetric lateral-flow strips integrate directly into cartridges, widening adoption in clinics lacking fluorescence readers.

By Product:

Reagent Revenues Fund Instrument InnovationReagents and consumables generated 62.94% of 2025 revenue, providing recurring cash flow that subsidises R&D. Bst polymerase supply resilience remains critical because it underpins most INAAT kits. Instruments are set to expand 10.98% annually as vendors embed microfluidics and one-step extraction, evidenced by iPonatic’s 30-minute cartridge achieving full workflow automation.

Instrument innovation focuses on integration and miniaturization, with manufacturers developing portable platforms that combine sample preparation, amplification, and detection in single-use cartridge formats. The iPonatic system exemplifies this trend, delivering complete nucleic acid testing within 30 minutes using room-temperature extraction and integrated detection capabilities. Microfluidic integration enables precise fluid handling and thermal control while reducing reagent consumption and contamination risks, though manufacturing complexity and cost considerations limit adoption to high-value applications.

By Application:

Oncology Emergence Challenges Infectious-Disease DominanceInfectious-disease testing retained 52.88% revenue in 2025 yet will lose relative share as oncology earns a 15.62% CAGR. The FDA’s 2024 clearance of Geneoscopy’s ColoSense stool-RNA test confirms INAAT’s role in non-invasive cancer screening. Blood centres also rely on TMA to shorten viral-window periods, underscoring broad pathogen focus.

Oncology traction exemplifies the Isothermal Nucleic Acid Amplification Technology market’s capacity to address continuous surveillance, detecting circulating tumour DNA before imaging modalities can confirm relapse. Food-safety and veterinary segments add diversity by exploiting INAAT tolerance for complex matrices, supporting field diagnoses where culture labs are scarce.

By End User:

Point-of-Care Adoption AcceleratesHospitals and reference labs together held 56.12% revenue in 2025, leveraging existing molecular infrastructure. Emergency units use thirty-minute respiratory panels to triage patients quickly, improving bed management. Reference labs add INAAT for STAT testing to differentiate from routine PCR competitors.

Decentralised clinics and urgent-care chains are set to grow at 11.28% CAGR, aided by cartridge-based analyzers that need minimal training. The Dragonfly portable station demonstrated reliable outbreak response in remote regions with no mains power. Academic centres continue to seed breakthroughs that commercial partners scale, reinforcing the innovation cycle across the Isothermal Nucleic Acid Amplification Technology market.

Geography Analysis

North America Isothermal Nucleic Acid Amplification Technology Market

North America leads with 35.12% revenue in 2025, underpinned by FDA pathways such as CLIA waiver rules that bring fifteen-minute respiratory panels into clinics fda.gov. Extensive insurance coverage permits hospitals to adopt INAAT without budget disruption. Research funding and robust venture capital accelerate domestic device launches.

APAC Isothermal Nucleic Acid Amplification Technology Market

Asia-Pacific is the growth engine, forecast at 15.1% CAGR. China’s NMPA shortened review timelines from 24 to 12 months, attracting multinationals to localise production nmpa.gov.cn. Japan’s senior population spurs home-based diagnostics, while India’s public-health programmes source affordable INAAT kits for tuberculosis and dengue surveillance. Local manufacturing dampens currency risk and secures supply during global disruptions.

Europe Isothermal Nucleic Acid Amplification Technology Market

Europe grows steadily as the IVDR harmonises standards, though smaller innovators face higher evidence hurdles for CE marking. Germany and the United Kingdom anchor demand through strong hospital networks and translational research output. Cost-containment policies favour constant-temperature systems that save energy and labour compared with PCR.

Competitive Landscape

The market remains moderately fragmented. Abbott, Roche and Qiagen leverage installed customer networks to cross-sell INAAT cartridges, while pure-play specialists like Meridian Bioscience and Molbio Diagnostics focus on assay breadth. Bio-Rad’s USD 105 million stake in Geneoscopy illustrates the trend of large firms partnering to accelerate oncology assay roll-out.

Acquisitions expand point-of-care capabilities: bioMérieux bought SpinChip Diagnostics in January 2025 for EUR 111 million, adding a 10-minute cardiac marker platform that complements its respiratory test suite. Competitive advantage hinges on regulatory prowess because payers demand robust clinical-utility dossiers before reimbursements flow.

White-space opportunities persist in ultra-rapid field diagnostics and in low-infrastructure regions where constant-temperature assays outperform PCR. Vendors pairing INAAT with CRISPR or AI-enabled result interpretation could secure premium niches before incumbents re-engineer their portfolios.

Isothermal Nucleic Acid Amplification Technology Industry Leaders

Becton Dickinson and Company

BioMerieux SA

Quidel Corporation

Qiagen N.V.

Tecan Genomics Inc.

- *Disclaimer: Major Players sorted in no particular order

Isothermal Nucleic Acid Amplification Technology Market Companies Covered in this Report

- Abbott Laboratories

- Amplifica Labs

- Beckton Dickinson

- bioMérieux

- DiaSorin

- Eiken Chemical Co., Ltd.

- Genomera Inc.

- Hologic

- Lucigen (LGC Biosearch)

- Meridian Bioscience

- Molbio Diagnostics

- New England Biolabs

- OptiGene Ltd.

- QIAGEN

- QuidelOrtho Corp.

- Roche

- Tecan Group

- Thermo Fisher Scientific

- TwistDx Ltd.

- Ustar Biotechnologies

Read Analysis of Isothermal Nucleic Acid Amplification Technology Companies

Recent Industry Developments in Isothermal Nucleic Acid Amplification Technology Market

- January 2025: bioMérieux completed acquisition of SpinChip Diagnostics for EUR 111 million (USD 116 million), gaining access to innovative immunoassay diagnostics platform designed for point-of-care testing with 10-minute result delivery from whole blood samples. The acquisition strengthens bioMérieux's point-of-care portfolio with technology targeting cardiac markers for myocardial infarction diagnosis, with first product launch expected in 2026 following CE marking under IVDR.

- January 2025: Geneoscopy closed USD 105 million Series C funding round led by Bio-Rad Laboratories to support commercialization of ColoSense colorectal cancer screening test and advance inflammatory bowel disease diagnostic pipeline. The investment leverages Bio-Rad's Droplet Digital PCR technology to enhance test sensitivity and specificity while expanding market access through established distribution channels.

- June 2024: FDA granted marketing authorization to Cepheid for Xpert HCV test and GeneXpert Xpress System, establishing first point-of-care hepatitis C RNA test capable of detecting HCV RNA from fingertip blood samples with approximately 60-minute turnaround time. The authorization enables test-and-treat approaches that address multi-step testing barriers resulting in untreated infections.

- May 2024: FDA approved Geneoscopy's ColoSense device for qualitative detection of colorectal neoplasia-associated RNA markers and occult hemoglobin in stool samples, marking first RNA-based stool test for adults aged 45 and older at average risk for colorectal cancer. The approval includes post-market study requirements with 12,500 subject enrollment over 36 months to confirm clinical effectiveness.

Isothermal Nucleic Acid Amplification Technology Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the isothermal nucleic acid amplification technology (INAAT) market as all commercial instruments, reagents, and integrated test kits that amplify DNA or RNA at a constant temperature for clinical, veterinary, food safety, and research diagnostics. The valuation, according to Mordor Intelligence, covers revenue generated from first-sale hardware and consumables across hospitals, reference labs, point-of-care settings, and academic centers in seventeen major countries.

Scope exclusion: ancillary PCR thermocyclers and contract testing revenues are outside this assessment.

Segments Covered in This Report

- By Technology

- Helicase-Dependent Amplification (HDA)

- Nicking Enzyme Amplification Reaction (NEAR)

- Loop-Mediated Isothermal Amplification (LAMP)

- Strand Displacement Amplification (SDA)

- Nucleic Acid Sequence-Based Amplification (NASBA)

- Transcription-Mediated Amplification (TMA)

- Single-Primer Isothermal Amplification (SPIA)

- Other Technologies

- By Product

- Instruments

- Reagents & Consumables

- By Application

- Infectious-Disease Diagnostics

- Oncology and Liquid Biopsy

- Blood-Screening and Transfusion Safety

- Food- & Water-Safety Testing

- Veterinary and Agricultural Diagnostics

- By End-User

- Hospitals & Reference Labs

- Point-of-Care / Decentralised Clinics

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interview product managers at global assay suppliers, procurement leads at hospital chains in North America, Europe, and Asia Pacific, and regional clinical pathology professors. These conversations solidify penetration rates for LAMP, NEAR, and RPA methods, reveal reagent discounting patterns, and test preliminary volume assumptions drawn from desk research.

Desk Research

We screen hundreds of public sources, beginning with peer-reviewed articles in PubMed and CDC Emerging Infectious Diseases, and rolling national infectious disease databases from WHO, ECDC, and China NHC to size potential test volumes. Trade statistics (UN Comtrade code 382200 for diagnostic reagents), patent filings from Questel, and import tariffs published by USITC and Eurostat clarify technology flow and price dispersion. Company 10-Ks, investor decks, and device recall notices add shipment and average selling price color, while D&B Hoovers supplies hard revenue splits for smaller manufacturers. The sources listed are illustrative; many additional references guide data validation and gap filling.

Market-Sizing & Forecasting

A top-down construct begins with infectious disease test volumes and blood screening procedures by country, which are then multiplied by INAAT penetration and weighted average reagent ASPs. Supplier roll-ups and sampled instrument placements provide a bottom-up check that fine tunes totals. Key model inputs include tuberculosis incidence, hepatitis C screening mandates, point-of-care device approvals, reagent ASP erosion, and annual healthcare expenditure growth. Five-year forecasts apply multivariate regression augmented with scenario analysis reviewed by interviewed experts; gaps in bottom-up totals are bridged through calibrated utilization factors.

Data Validation & Update Cycle

Outputs pass three-layer checks covering statistical outliers, year-on-year variance, and cross-source coherence before senior review sign-off. Reports refresh each year, and interim updates trigger when regulatory approvals, large tenders, or public health emergencies materially shift the baseline.

How Mordor Intelligence's Isothermal Nucleic Acid Amplification Technology Market Size Compares to Other Published Estimates

Published estimates often diverge because firms adopt different product scopes, currency bases, and ASP trajectories. By anchoring on clearly disclosed diagnostic procedure counts and verified reagent pricing, Mordor minimizes speculative uplift.

Key gap drivers include whether competitor studies fold PCR consumables into INAAT totals, apply uniform list prices without discount factors, or extrapolate aggressive point-of-care rollouts beyond confirmed tender data. Our annual refresh cadence further limits vintage bias.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.36 B (2025) | Mordor Intelligence | - |

| USD 5.83 B (2025) | Global Consultancy A | Uses global reagent list prices, omits institutional discounts |

| USD 6.06 B (2025) | Industry Research Firm B | Bundles PCR-based NAAT kits, inflating scope |

| USD 5.20 B (2024) | Regional Consultancy C | Applies single exchange rate snapshot, no inflation adjustment |

The comparison shows that when scope alignment, discount reality, and currency consistency are enforced, Mordor's figure offers a balanced, transparent baseline that decision makers can readily trace to explicit variables and repeatable steps.

Key Questions Answered in the Report

What is driving recent growth in the Isothermal Nucleic Acid Amplification Technology market?

Rapid point-of-care adoption, lower instrument costs and continuous regulatory support in North America and Asia-Pacific are propelling an 8.75% CAGR through 2031.

Which technology segment leads the market?

Loop-Mediated Isothermal Amplification holds 43.72% revenue and is also the fastest-growing segment at 13.02% CAGR.

What regions are expanding the fastest?

Asia-Pacific is forecast to grow at 15.1% CAGR due to streamlined approvals and infrastructure investment.

Which applications offer the highest future growth?

Oncology and liquid-biopsy tests are set to expand at 15.62% CAGR as non-invasive cancer screening gains medical and payer acceptance.

What are the main barriers to wider INAAT adoption?

Incumbent PCR infrastructure, reimbursement gaps and enzyme supply volatility remain the key restraints affecting uptake over the next two to four years.

Page last updated on: