Gene Prediction Tools Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

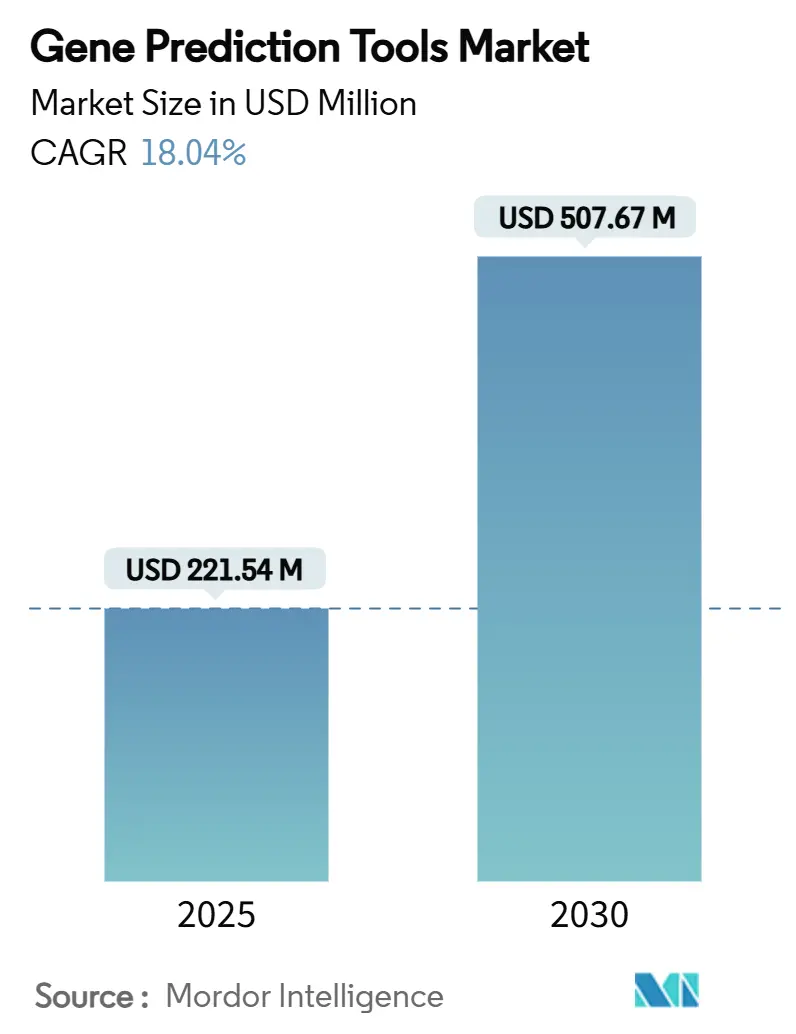

| Market Size (2025) | USD 221.54 Million |

| Market Size (2030) | USD 507.67 Million |

| Growth Rate (2025 - 2030) | 18.04% CAGR |

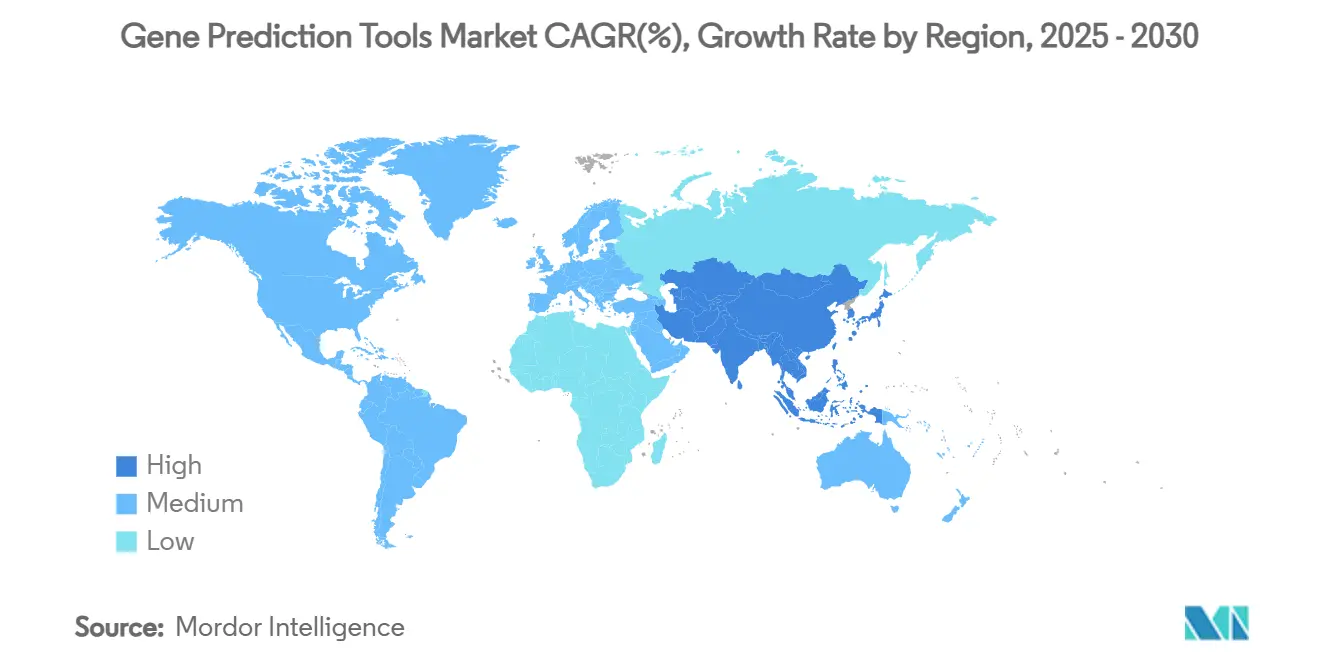

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gene Prediction Tools Market Analysis by Mordor Intelligence

The gene prediction tools market size stands at USD 221.54 million in 2025 and is forecast to reach USD 507.65 million by 2030, delivering an 18.04% CAGR over the period. The combination of consistently falling sequencing costs, rapid advances in AI-based annotation, and the scale of population genomics initiatives keep demand on an upward trajectory. Growth also reflects a shift from traditional ab initio software toward cloud-native, AI-assisted platforms that process large and complex datasets. Intensifying clinical adoption, increasing investment in long-read sequencing, and evolving regulatory clarity around AI medical devices further widen commercial opportunities. Competitive intensity remains high as established life-science companies defend share against AI-native entrants that promise faster and more accurate annotation.

Key Report Takeaways

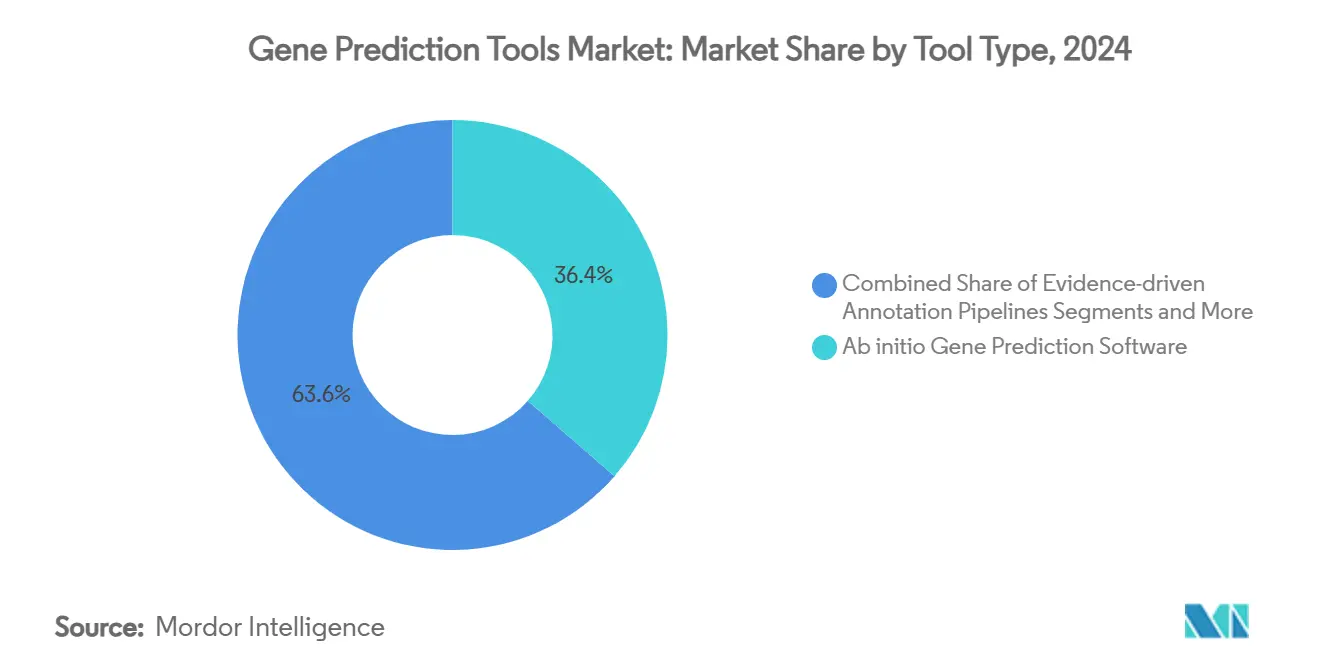

- By tool type, ab initio gene prediction software led with 36.42% revenue share of the gene prediction tools market in 2024; cloud-based gene prediction APIs are projected to grow at a 21.43% CAGR to 2030.

- By deployment model, on-premise solutions held 56.24% of the gene prediction tools market share in 2024, while cloud/SaaS offerings are advancing at a 22.34% CAGR through 2030.

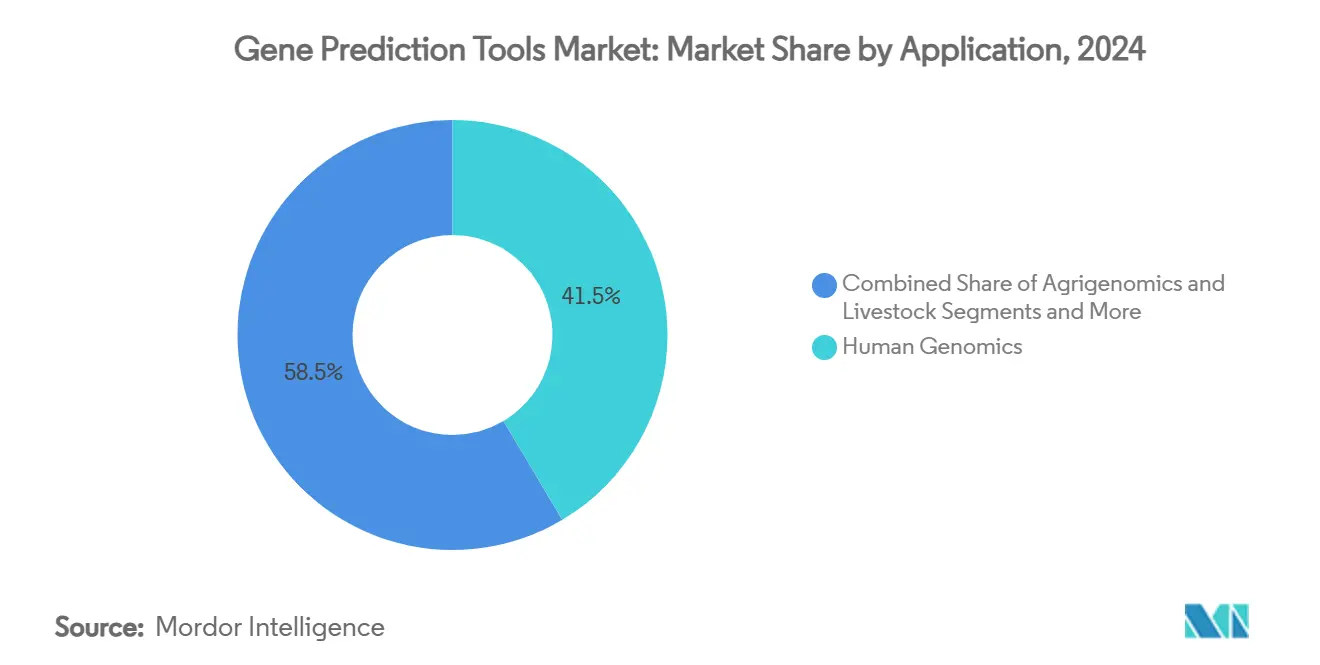

- By application, human genomics accounted for 41.47% of the gene prediction tools market size in 2024 and metagenomics & microbiome workflows are expanding at a 21.55% CAGR over the forecast period.

- By end user, academic and research institutes controlled 43.63% of the market in 2024, whereas pharmaceutical and biotech companies are growing fastest at a 20.41% CAGR.

- By geography, North America commanded 36.66% revenue share in 2024; Asia-Pacific is the fastest-growing region at a 20.68% CAGR through 2030.

Global Gene Prediction Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining sequencing-cost curve | +2.1% | Global, early uptake in North America & EU | Short term (≤ 2 years) |

| Increasing population-scale genomics programs | +3.2% | US, UK, China, Nordic countries | Medium term (2-4 years) |

| Expansion of NGS-based clinical diagnostics | +2.8% | North America & EU lead; APAC follows | Medium term (2-4 years) |

| Cloud-native bioinformatics pipelines | +3.5% | Global, stronger in developed markets | Short term (≤ 2 years) |

| AI-assisted de novo gene prediction | +4.1% | R&D centers in North America & EU; global deployment | Long term (≥ 4 years) |

| Long-read + Hi-Fi hybrid assemblies | +2.4% | Research hubs in developed regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Sequencing-Cost Curve

Illumina’s USD 600 genome and Ultima’s USD 100 roadmap have pushed sequencing toward mass affordability, unlocking routine whole-genome studies in many mid-tier labs. Lower entry costs widen the gene prediction tools market by allowing more institutions to perform population-scale projects. Downward pricing also fuels demand for automated pipelines that can annotate the flood of new data quickly and accurately. Commercial labs increasingly bundle sequencing and annotation for clinical decision support, creating integrated service models that rely on high-throughput, cloud-based prediction engines.[1]ILLUMINA, “Illumina to Acquire SomaLogic, Advancing Multiomics Strategy,” illumina.com

Increasing Population-Scale Genomics Initiatives

Multi-country programs—from the UK Biobank’s 500,000 genomes to China’s 1 million-genome effort—produce data volumes that only scalable, AI-ready software can handle. Such datasets require pipelines able to parse population-specific variation, structural variants, and ancestry-diverse genomes. As newborn sequencing initiatives enter mainstream healthcare, demand rises for tools optimized for rare-disease discovery and pharmacogenomics. Vendors responding with ancestry-tuned reference models gain a competitive edge.[2]UK BIOBANK, “UK Biobank Expands Whole-Genome Sequencing,” ukbiobank.ac.uk

Expansion of NGS-Based Clinical Diagnostics

Hospitals now employ whole-exome and whole-genome sequencing for oncology and rare disease workflows. FDA guidance on AI/ML-enabled devices clarifies compliance paths, prompting higher investment in clinically validated gene prediction engines. Liquid biopsy advances, which depend on interpreting low-frequency variants from circulating DNA, further elevate annotation needs. Real-time result delivery becomes essential for acute care, pushing suppliers toward faster, cloud-enabled pipelines.[3]FDA, “Artificial Intelligence and Machine Learning-Enabled Medical Devices,” fda.gov

Cloud-Native Bioinformatics Pipelines Adoption

Platforms such as DNAnexus and Seven Bridges illustrate how elastic compute and containerized workflows shrink time-to-insight while curbing infrastructure spend. Academic teams leverage subscription models rather than purchasing local clusters, broadening global access. Cloud architectures also improve reproducibility through standardized pipelines and effortless collaboration across institutions. Security certifications and federated learning approaches address data-privacy hurdles in regulated environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of high-quality annotated reference genomes | -1.8% | Global, more acute for non-model species | Long term (≥ 4 years) |

| Persistent IP fragmentation across tool vendors | -2.3% | Developed markets with dense patent activity | Medium term (2-4 years) |

| Shortage of multi-omics data-science talent | -1.5% | North America & EU face sharper hiring gaps | Short term (≤ 2 years) |

| Regulatory lag on AI-generated annotations | -1.2% | Initially North America & EU, spreading worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of High-Quality Annotated Reference Genomes

Many species lack gold-standard references, limiting machine learning model training and reducing accuracy when algorithms confront diverse genetic backgrounds. Curation costs remain high, and existing datasets skew toward European ancestry. As research expands into understudied organisms and populations, prediction errors mount, curbing clinical adoption in non-western regions. Investment in consortium-based reference projects is essential but time-consuming.

Persistent IP Fragmentation Across Tool Vendors

Overlapping patents on algorithms, databases, and file formats create costly licensing webs. Incompatible data structures hinder workflow integration and force users to maintain multiple systems or develop custom bridges. Smaller labs suffer most, often settling for suboptimal analysis paths that slow discovery. AI-native tools introduce new IP layers around model weights and training corpora, compounding uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Type: Cloud APIs Drive Next-Generation Annotation

Ab initio software retained a 36.42% revenue share of the gene prediction tools market in 2024, underscoring enduring confidence in established algorithms. However, the gene prediction tools market size for cloud-based APIs is expanding at a 21.43% CAGR as users favor elastic scaling and lower upfront costs. Greater sequencing throughput encourages hybrid platforms that fuse deep learning with evidence-based modules. AI-native entrants such as Evo2 compress computation times and deliver richer functional context, reshaping user expectations for accuracy and speed within the gene prediction tools market.

Traditional desktop suites still anchor workflows for well-characterized genomes, yet demand is shifting toward subscription models that integrate continuous updates. Cloud vendors also embed access to curated databases, visualization layers, and compliance reporting, making standalone binaries less attractive over time.

By Deployment Model: Cloud Migration Accelerates Despite Security Concerns

On-premise installations captured 56.24% of 2024 revenue, reflecting ongoing sensitivity around protected health information and proprietary pipelines. The gene prediction tools market size attached to on-premise clusters remains significant among pharmaceutical companies and diagnostics labs where data residency rules apply.

Cloud/SaaS deployments nonetheless post 22.34% CAGR as enterprise genomics clouds earn ISO and HIPAA certifications. Researchers leverage pay-as-you-go models to handle project spikes without over-provisioning. Hybrid strategies are rising, letting institutions process sensitive data locally while outsourcing intensive compute to secure cloud regions, a trend that steadily shifts revenue toward service-centric offerings in the gene prediction tools market.

By Application: Metagenomics Emerges as High-Growth Frontier

Human genomics held a 41.47% share of the gene prediction tools market size in 2024 thanks to reimbursement-backed clinical testing, oncology sequencing, and rare-disease diagnostic. Metagenomics and microbiome studies represent the most dynamic niche, expanding at 21.55% CAGR as long-read sequencing and AI analytics uncover novel microbial pathways. Environmental monitoring, gut-health research, and bioprocess optimization all require specialized annotation capable of deconvoluting mixed-species datasets, pulling new funding into this segment of the gene prediction tools market.

Synthetic biology further boosts demand through design-build-test cycles that rely on predictive algorithms to engineer novel functions. Agrigenomics applications remain steady, with breeding programs adopting software that pinpoints target traits more efficiently.

By End User: Pharmaceutical Sector Drives Commercial Adoption

Academic and research institutes generated 43.63% of 2024 sales, continuing to shape methodological innovation. The gene prediction tools market share is gradually tilting toward industry, as pharmaceutical and biotech firms pursue 20.41% CAGR on the back of precision-medicine pipelines and target-discovery efforts.

CROs and CDMOs grow alongside, providing outsourced analytics for companies facing talent shortages. Hospitals and diagnostic labs adopt clinical-grade annotation to accelerate turnaround times for genetic tests, embedding software directly into laboratory information systems and reinforcing service-oriented revenue streams for the gene prediction tools market.

Geography Analysis

North America accounted for 36.66% of 2024 revenue, supported by NIH funding, venture capital, and clear regulatory pathways. Public programs such as the All of Us Research Program add sustained data inflows that rely heavily on gene prediction software. Commercial providers bundle sequencing with annotation, keeping adoption brisk across both clinical and research settings in the region.

Europe follows with robust growth, propelled by national genomics initiatives and strict privacy laws that incentivize vendors to build secure, compliant platforms. The gene prediction tools market size for European deployments gains from collaborative projects like the 1+ Million Genomes alliance, which demands interoperable and ancestry-aware annotations. Germany, the UK, and France remain prime procurement hubs.

Asia-Pacific is the fastest-growing territory, advancing at a 20.68% CAGR. China’s million-genome program, India’s expanding biotech investments, and Japan’s precision-medicine push collectively drive substantial demand. Local vendors partner with global suppliers to adapt AI models for diverse populations, making the region a testbed for next-generation annotation strategies. Government incentives and lower sequencing costs accelerate broad deployment.

Latin America sees steady uptake as national health systems pilot population genomics to address endemic diseases. Middle East and Africa are nascent but promising, with Gulf Cooperation Council states funding national biobanks and research campuses that require advanced bioinformatics. As talent pipelines mature, local adoption is expected to gain pace, aided by cloud access that bypasses infrastructure gaps.

Competitive Landscape

The gene prediction tools market remains fragmented. Illumina, Thermo Fisher Scientific, and QIAGEN leverage integrated sequencing portfolios and established distribution networks to protect core accounts. Their analytics suites increasingly incorporate AI modules and cloud connectors to remain competitive.

AI-native challengers such as Arc Institute and multiple venture-backed software firms target accuracy gains through transformer-based architectures. These entrants differentiate by offering faster updates, subscription pricing, and API-first design, allowing easy embedding into broader informatics stacks. Partnerships with cloud hyperscalers further reduce deployment friction for customers.

Strategic activity centers on portfolio expansion and data-integration capabilities. Illumina’s USD 350 million acquisition of SomaLogic broadens multi-omics coverage and positions the firm for proteogenomics workflows. bioMérieux’s purchase of Applied Maths adds algorithmic depth to its microbiology franchise. Vendors also collaborate with pharmaceutical companies on co-development, ensuring pipelines align with drug-discovery needs while securing recurring revenue from license renewals.

Gene Prediction Tools Industry Leaders

Illumina Inc.

QIAGEN N.V.

Thermo Fisher Scientific Inc.

Softberry Inc.

Geneious (Dotmatics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Illumina confirmed a USD 350 million agreement to acquire SomaLogic, adding proteomics to its multi-omics strategy and driving integrated annotation demand.

- February 2025: Arc Institute introduced Evo2, a 7-billion-parameter genomic language model surpassing 90% accuracy on disease-variant prediction tasks.

- February 2025: Ginkgo Bioworks partnered with HaDEA on a €24 million consortium to create rapid metagenomic diagnostics for respiratory viruses.

- July 2024: Genedata released Selector 10, an agricultural biotechnology platform combining NGS with automated gene prediction.

Global Gene Prediction Tools Market Report Scope

| Ab initio Gene Prediction Software |

| Evidence-driven Annotation Pipelines |

| Integrated Genome Annotation Suites |

| Cloud-based Gene Prediction APIs |

| On-premise |

| Cloud / SaaS |

| Human Genomics |

| Agrigenomics & Livestock |

| Metagenomics & Microbiome |

| Synthetic Biology & Pathway Design |

| Academic & Research Institutes |

| Pharmaceutical & Biotech Companies |

| CROs & CDMOs |

| Hospitals & Diagnostic Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Tool Type | Ab initio Gene Prediction Software | |

| Evidence-driven Annotation Pipelines | ||

| Integrated Genome Annotation Suites | ||

| Cloud-based Gene Prediction APIs | ||

| By Deployment Model | On-premise | |

| Cloud / SaaS | ||

| By Application | Human Genomics | |

| Agrigenomics & Livestock | ||

| Metagenomics & Microbiome | ||

| Synthetic Biology & Pathway Design | ||

| By End User | Academic & Research Institutes | |

| Pharmaceutical & Biotech Companies | ||

| CROs & CDMOs | ||

| Hospitals & Diagnostic Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the gene prediction tools market?

The market is valued at USD 221.54 million in 2025 and is projected to reach USD 507.65 million by 2030.

2. Which region leads the gene prediction tools market?

North America holds the largest share at 36.66% in 2024, driven by strong federal funding and established genomics companies.

3. What segment is growing fastest within the market?

Cloud-based gene prediction APIs are advancing at a 21.43% CAGR, reflecting demand for scalable and cost-efficient annotation.

4. How fast is the Asia-Pacific market expanding?

Asia-Pacific is expected to post a 20.68% CAGR through 2030 owing to large-scale genome programs in China and India.

5. Why are AI-assisted tools gaining traction?

Foundation models such as Evo2 deliver higher annotation accuracy and faster turnaround, reducing reliance on manual curation.

6. What are the main restraints to market growth?

Key barriers include limited high-quality reference genomes, fragmented intellectual-property ownership, talent shortages, and evolving regulation around AI-generated annotations.

Page last updated on: