Gel Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

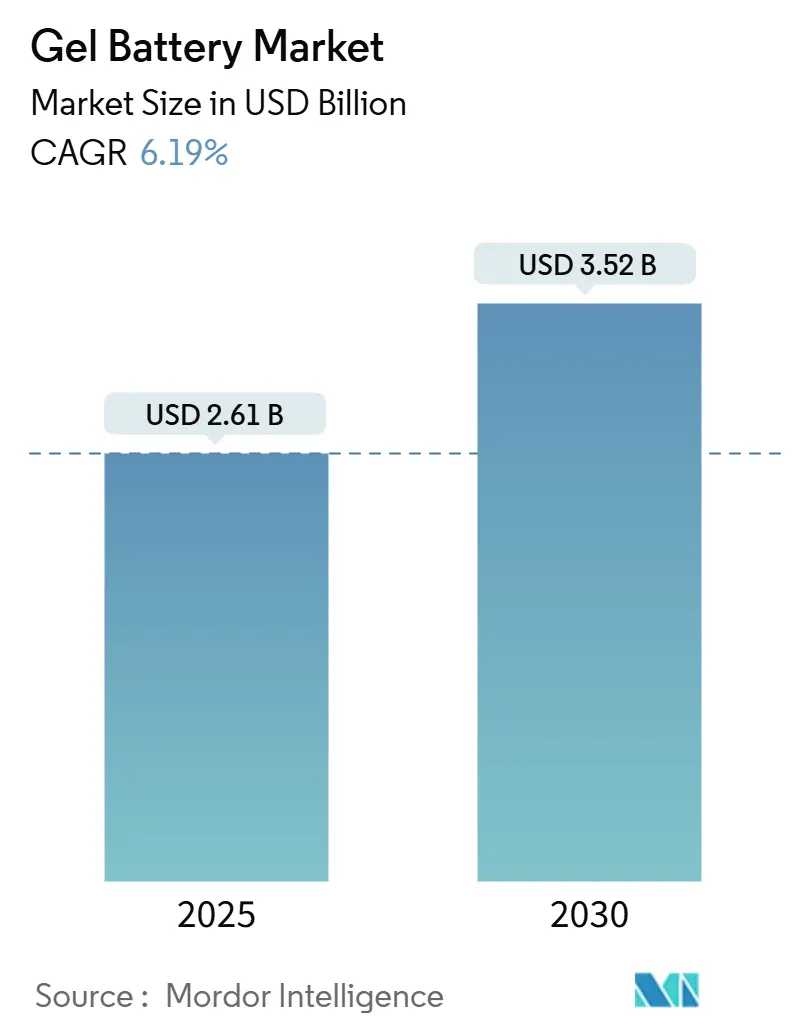

| Market Size (2025) | USD 2.61 Billion |

| Market Size (2030) | USD 3.52 Billion |

| Growth Rate (2025 - 2030) | 6.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

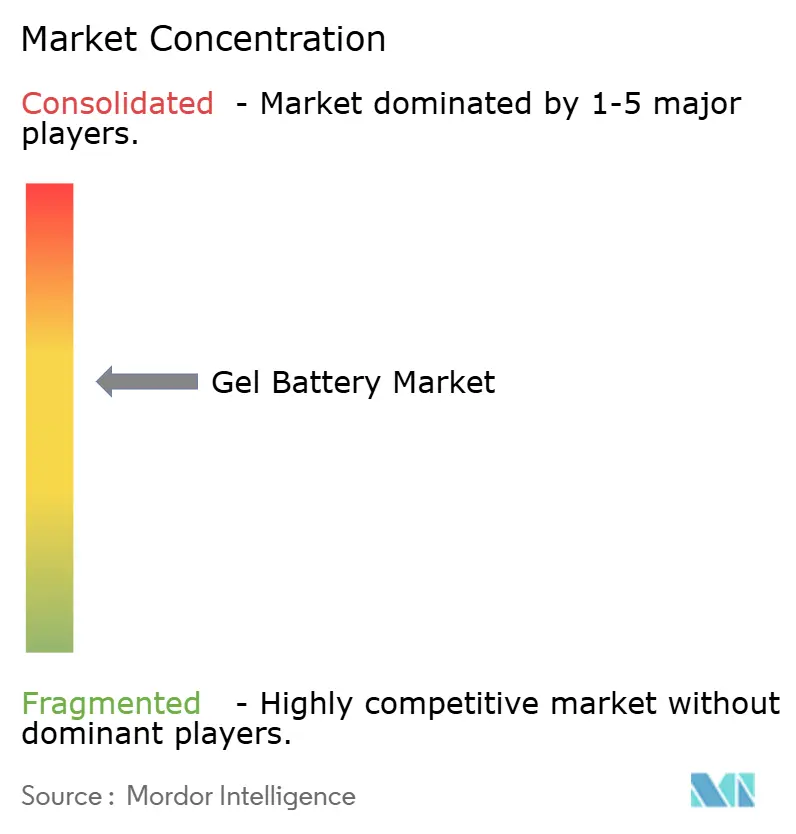

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gel Battery Market Analysis by Mordor Intelligence

The Gel Battery Market size is estimated at USD 2.61 billion in 2025, and is expected to reach USD 3.52 billion by 2030, at a CAGR of 6.19% during the forecast period (2025-2030).

Growth reflects the technology’s strategic position between flooded lead-acid systems and lithium-ion alternatives, with sealed, maintenance-free construction delivering reliability in safety-critical environments. Renewable-energy mini-grids, telecom tower build-outs, and tightening safety rules sustain demand, even as pricing pressure from lithium-iron-phosphate intensifies. Pure gel formats maintain cost leadership, while hybrid designs close performance gaps, allowing suppliers to tailor their offerings to application-specific needs. Regional value is migrating toward the Asia-Pacific, where aggressive infrastructure projects and local manufacturing scale are compressing landed costs. Meanwhile, North American buyers are increasingly valuing domestic supply resilience. Competitive intensity remains moderate; leading vendors deploy scale economics, distribution depth, and application engineering to defend their margins as the risk of technology substitution rises.

Key Report Takeaways

- By type, pure gel systems led the gel battery market with a 63.5% share in 2024; hybrid gel variants recorded the fastest growth at a 6.9% CAGR from 2024 to 2030.

- By capacity range, up to 100 Ah units commanded 40.0% of the gel battery market share in 2024, whereas the 100–200 Ah band is forecasted to rise at a 6.5% CAGR through 2030.

- By voltage, products with a voltage of up to 12 V dominated the gel battery market, accounting for a 64.8% share in 2024; however, solutions with a voltage of 12–48 V are projected to grow at a 7.1% CAGR through 2030.

- By application, renewable energy storage captured 35.1% of the gel battery market share in 2024, advancing at a 6.8% CAGR through 2030.

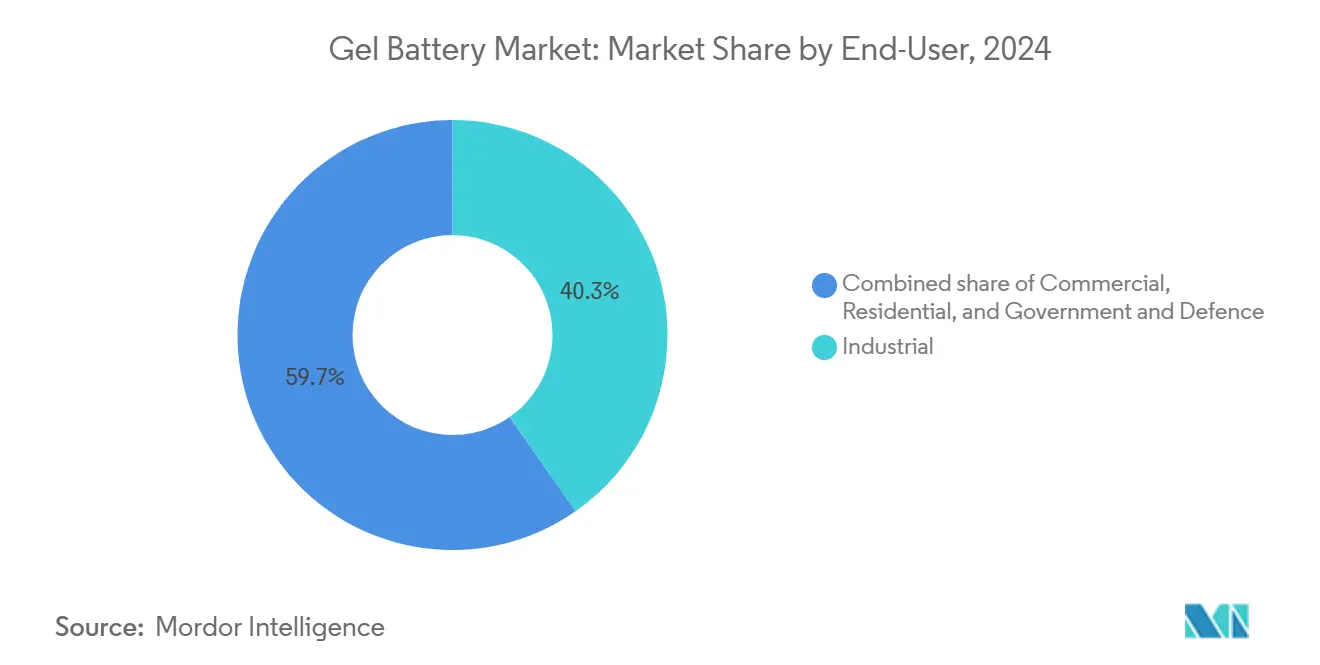

- By end-user, industrial users accounted for a 40.3% share of the gel battery market size in 2024, while the commercial segment is expected to show the highest CAGR at 7.0% through 2030.

- By geography, the Asia-Pacific region held a 44.9% revenue share of the gel battery market in 2024; it is projected to expand at a 6.5% CAGR through 2030.

Global Gel Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy mini-grid build-out | +1.20% | Global, concentration in Sub-Saharan Africa & South Asia | Medium term (2–4 years) |

| Telecom tower densification in emerging markets | +1.00% | Asia-Pacific core, spill-over to MEA | Short term (≤2 years) |

| Safety & environmental regulations favoring VRLA tech | +0.80% | North America & EU, expanding to APAC | Long term (≥4 years) |

| Fleet electrification of leisure & micro-mobility vehicles | +0.60% | North America & EU | Medium term (2–4 years) |

| WHO 2024 medical-UPS electrical-resilience mandate | +0.40% | Global healthcare infrastructure | Short term (≤2 years) |

| Hybrid hydrogen-electrolyzer buffering bundles | +0.30% | EU & North America pilot markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy Mini-Grid Build-Out

Mini-grid projects across developing economies are increasingly specifying gel batteries for deep-cycle durability, particularly where technician access is limited. Sealed construction eliminates the need for routine watering, and a wide operating-temperature tolerance safeguards performance in tropical climates. Case studies in Malawi demonstrate that mini-grids totaling 26 MW primarily encounter financial, rather than technical, hurdles, reinforcing the argument for system reliability. Distributors with established last-mile service networks secure repeat orders as governments channel 87% of their 2024 electricity capital expenditure into clean energy platforms.(1)Michael Toman, “Tracking Decarbonization Investing in the Global South,” rmi.org Anticipated carbon-neutral funding streams sustain the gel battery market even as lithium units chase parity.

Telecom Tower Densification in Emerging Markets

Asia-Pacific mobile operators accelerate tower roll-outs that demand compact, vibration-resistant backup power. Gel batteries’ zero-maintenance profile and low gas emission align with shelter ventilation limits, reducing OPEX despite higher upfront cost.(2)T. Nguyen, “Thermal Behavior of VRLA Batteries in Telecom Shelters,” SpringerLink, springer.comNetwork owners deploy predictive-maintenance algorithms to lengthen replacement cycles, squeezing total lifetime value from each string.(3)A. Sharma, “Fuzzy Logic-Based VRLA Battery Prognostics,” IOP Conference Series, iopscience.iop.orgAs 5G densification peaks, secondary waves in MEA markets are set to replicate the procurement blueprint, lifting regional consumption of gel battery products.

Safety & Environmental Regulations Favoring VRLA Technology

The EU Battery Regulation (EU) 2023/1542 mandates carbon footprint labels and recycled content thresholds for all portable and industrial batteries. Gel formats already meet gas-emission caps, cutting HVAC costs in enclosed sites and easing permitting hurdles. North American OSHA and NFPA revisions echo similar priorities, incentivizing facility managers to retrofit flooded systems with sealed VRLA models. Suppliers boasting ISO 14001 and IEC 62902 certifications leverage compliance credentials to win public tenders, fortifying the gel battery market against low-cost rivals.

Fleet Electrification of Leisure & Micro-Mobility Vehicles

Golf carts, marine crafts, and last-mile scooters are increasingly adopting maintenance-free packs to reduce service downtime. Gel units tolerate deep discharge and partial SOC cycling typical in seasonal fleets. Spillage-proof design gains favor with marinas and RV parks where orientation changes are frequent. Charging-station providers reinforce safety by preferring chemistries with inherent flame arrestors, bolstering incremental demand even as weight-sensitive platforms migrate to lithium.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LFP pack price free-fall | -1.80% | Global, most pronounced in China | Short term (≤2 years) |

| Limited high-rate discharge capability | -0.90% | Applications requiring rapid power delivery | Medium term (2–4 years) |

| EU-REACH fumed-silica compliance costs | -0.60% | EU manufacturing, global supply chain impact | Medium term (2–4 years) |

| Sulfuric-acid feedstock shortages | -0.40% | Global manufacturing, regional variations | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

LFP Pack Price Free-Fall

International Energy Agency data show that lithium-iron-phosphate pack prices are expected to slide by 20% in 2024, widening the cost gap with valve-regulated lead-acid options. Chinese output surges intensify global price transmission, tempting price-sensitive buyers to switch platforms. While gel batteries still dominate in extreme-temperature or low-maintenance environments, each price cut erodes addressable volumes, putting premium-tier segments under pressure to remain profitable.

Sulfuric-Acid Feedstock Shortages

Projected sulfur deficits of up to 320 million tonnes by 2040 risk hiking electrolyte costs. Lead-acid producers report 37% supply disruption rates in 2024, triggering spot-market volatility. Gel battery vendors counter with recycling initiatives and multi-source contracts, but must either absorb near-term margin compression or pass the cost on to customers, potentially deferring procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Market Balances Cost and Innovation

Pure gel formats retained a 63.5% share of the gel battery market in 2024, as mature lines deliver scale economies and predictable field life. Hybrid gels are projected to post a 6.9% CAGR to 2030 as OEMs blend silica additives and advanced separators to enhance charge acceptance. Price-performance segmentation now guides purchasing: utilities favor lower-priced pure gels for volume roll-outs, whereas data-center operators pay premiums for hybrids’ faster recharge and longer float life. Suppliers capable of dual-line production hedge risk as specification diversity widens.

Hybrid advances narrow performance gaps with lithium while preserving VRLA safety hallmarks, supporting the gel battery market’s relevance in grid-adjacent niches. Yet, greater process control raises capital expenditures, tilting bargaining power toward entrenched incumbents that can amortize investments across their global footprints.

By Capacity Range: Mid-Tier Blocks Gain Ground

Units with a capacity of up to 100 Ah accounted for a 40.0% share of the gel battery market size in 2024, primarily used in UPS racks and BTS cabinets. Growth momentum shifts to 100–200 Ah blocks at a 6.5% CAGR through 2030, as modular energy systems favor stacking mid-sized packs for flexible runtime. Integrators appreciate standardized bus-bar kits and plug-and-play monitoring accessories bundled with these formats. The above 200 Ah bracket remains a specialist, used in remote micro-grids where logistics costs incentivize oversized strings.

Tiered demand pressures manufacturers to optimize tooling for mid-range casings while retaining agility for low-volume high-capacity orders. Firms offering interchangeable jar designs and common vent assemblies achieve inventory efficiencies that protect margins despite rising raw-material costs.

By Voltage: Efficiency Drives Uptake of Intermediate Ranges

Up to 12 V strings continued to dominate, accounting for 64.8% of the gel battery market share in 2024, thanks to their legacy compatibility in marine, automotive, and small inverter applications. However, 12–48 V systems outpace the market at a 7.1% CAGR as commercial sites adopt higher-voltage DC buses to reduce copper loss and footprint. Regulatory shifts such as IEC 62934 on LVDC safety frameworks further normalize intermediate voltages, stimulating OEM catalogue expansion. 48 V assemblies serve utility niches, such as substation switchgear, but face stringent touch-safety and arc-flash compliance hurdles.

Vendors investing in 24 V and 36 V module lines capture crossover demand from telecom and light EVs, reinforcing position as holistic partners rather than commodity cell suppliers in the gel battery market.

By Application: Renewable Energy Storage Sets the Pace

Renewable installations accounted for 35.1% of 2024 revenue and are expected to expand at the fastest rate of 6.8% CAGR, driven by governmental mini-grid subsidies and corporate decarbonization pledges. Telecom ranks second as tower counts soar, yet C-band base stations raise runtime thresholds. UPS demand benefits from hyperscale data center expansion, but the value per MWh trails that of energy storage enclosures. Mobility and medical devices require specialized volumes, where compliance and safety standards take precedence over USD/kWh metrics.

Portfolio resilience stems from diversified exposure; even if grid-scale lithium competes with renewables, telecom, and medical mandates will sustain the baseline pull for gel battery products.

By End-User: Commercial Sites Accelerate Adoption

Industrial plants consumed 40.3% of 2024 output due to stringent uptime requirements in mining and process industries. Commercial premises, including retail, hospitality, and colocation facilities, show a 7.0% CAGR, propelled by distributed generation and stricter building codes. Residential uptake lags, constrained by evolving homeowner preference for lithium’s compactness despite higher management complexity. Defense agencies and government fleets provide steady, spec-driven orders that favor long-term supply contracts.

Suppliers tailoring financing packages and remote monitoring to commercial landlords lock in multiyear revenue, widening moat against new entrants chasing pure hardware sales.

Geography Analysis

Asia-Pacific led with 44.9% of 2024 revenue and will grow at a 6.5% CAGR to 2030. China’s integrated supply chain compresses BOM cost, while India’s solar-plus-storage auctions stipulate battery warranties that gel technology satisfies. Southeast Asian electrification grants and African tower deals cement export flows from regional OEMs.

Europe’s mature but regulation-driven market values low-gas-emission and recyclable products, underpinning premiums for domestic VRLA production even as REACH silica rules elevate compliance spending. North America maintains moderate growth as critical-infrastructure hardening and Buy-American sentiment fuel onshoring. The Inflation Reduction Act’s storage tax credits also extend the runway for gel’s use in municipal and rural cooperatives that distrust newer chemistries.

South America and the Middle East/Africa contribute emerging volumes. Brazilian rural electrification favors sealed lead options for remote agro-processing hubs, while Gulf states deploy hybrid solar farms with VRLA buffer strings to temper desert-heat stress. However, currency volatility and subsidy gaps keep these regions’ share modest.

Competitive Landscape

The gel battery market remains moderately fragmented, with the top five brands holding a roughly 45% combined share, thereby preserving buyer options while enabling price discipline. EnerSys channels U.S. Department of Energy awards into lithium diversification, yet reiterates its commitment to VRLA R&D for telecom and defense applications. Exide Technologies leverages marine DNV certifications to defend niche segments where safety classification shortlists suppliers. Clarios scales AGM capacity in four EU plants, exploiting synergies with automotive networks to cross-sell gel SKUs. Trojan Battery expands distribution through Continental Battery Systems to accelerate order fulfillment across the Western states. Regional specialists in Korea and Turkey grow through ODM contracts, but face intellectual property hurdles when entering regulated EU and U.S. channels.

Technology roadmaps prioritize enhanced valve design, adaptive charge algorithms, and optimized recycled content over disruptive chemistries, reflecting customer preference for incremental innovation anchored in proven reliability.

Gel Battery Industry Leaders

Exide Technologies

EnerSys

Trojan Battery Company

FIAMM Energy Technology

Sacred Sun Power (Shoto)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Exide Technologies showcased a comprehensive energy storage solutions portfolio at ees Europe 2025, featuring the Solition Mega series with modular designs from 552 kWh to 3440 kWh capacity, and received DNV type approval renewal for Gel and AGM batteries for marine applications.

- April 2025: EnerSys announced a strategic manufacturing restructuring involving the closure of its Monterrey, Mexico, facility and the expansion of U.S. production capacity for flooded lead-acid batteries, with significant annual benefits expected to start in fiscal year 2027.

- November 2024: Continental Battery Systems expanded its master distributorship agreement with Trojan Battery Company, becoming the exclusive distributor for the Western U.S. region to enhance customer service and distribution capabilities.

- August 2024: Clarios invested approximately EUR 200 million in European plants to expand AGM battery production capacity by 50% through 2026, creating 150 jobs across Germany, Spain, the Czech Republic, and France.

Global Gel Battery Market Report Scope

| Pure Gel Batteries |

| Hybrid Gel Batteries |

| Up to100 Ah |

| 100 to 200 Ah |

| Above 200 Ah |

| Up to 12 V |

| 12 to 48 V |

| Above 48 V |

| Renewable Energy Storage |

| Telecommunications |

| Uninterruptible Power Supply (UPS) |

| Electric Vehicles/Mobility |

| Medical Equipment |

| Marine and Leisure |

| Others |

| Industrial |

| Commercial |

| Residential |

| Government and Defence |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Pure Gel Batteries | |

| Hybrid Gel Batteries | ||

| By Capacity Range | Up to100 Ah | |

| 100 to 200 Ah | ||

| Above 200 Ah | ||

| By Voltage | Up to 12 V | |

| 12 to 48 V | ||

| Above 48 V | ||

| By Application | Renewable Energy Storage | |

| Telecommunications | ||

| Uninterruptible Power Supply (UPS) | ||

| Electric Vehicles/Mobility | ||

| Medical Equipment | ||

| Marine and Leisure | ||

| Others | ||

| By End-User | Industrial | |

| Commercial | ||

| Residential | ||

| Government and Defence | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the gel battery market?

The gel battery market size reached USD 2.61 billion in 2025.

How fast will gel battery demand grow to 2030?

Aggregate demand is projected to rise at a 6.19% CAGR, lifting revenue to USD 3.52 billion by 2030.

Which application generates the highest revenue?

Renewable energy storage leads with 35.1% share and remains the fastest growing use case.

Why do telecom operators still buy gel batteries?

Sealed design, low ventilation needs, and vibration resistance make gel batteries ideal for densely packed base-station shelters.

Which region presents the strongest expansion potential?

Asia-Pacific combines 44.9% share with a 6.5% CAGR owing to solar roll-outs and tower densification projects.

Are pure or hybr

Pure gel units hold the majority today, but hybrid versions post the highest growth as users seek better charge acceptance and cycle life.

Page last updated on: