Flexible Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.59 Billion |

| Market Size (2031) | USD 1.77 Billion |

| Growth Rate (2026 - 2031) | 24.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Battery Market Analysis by Mordor Intelligence

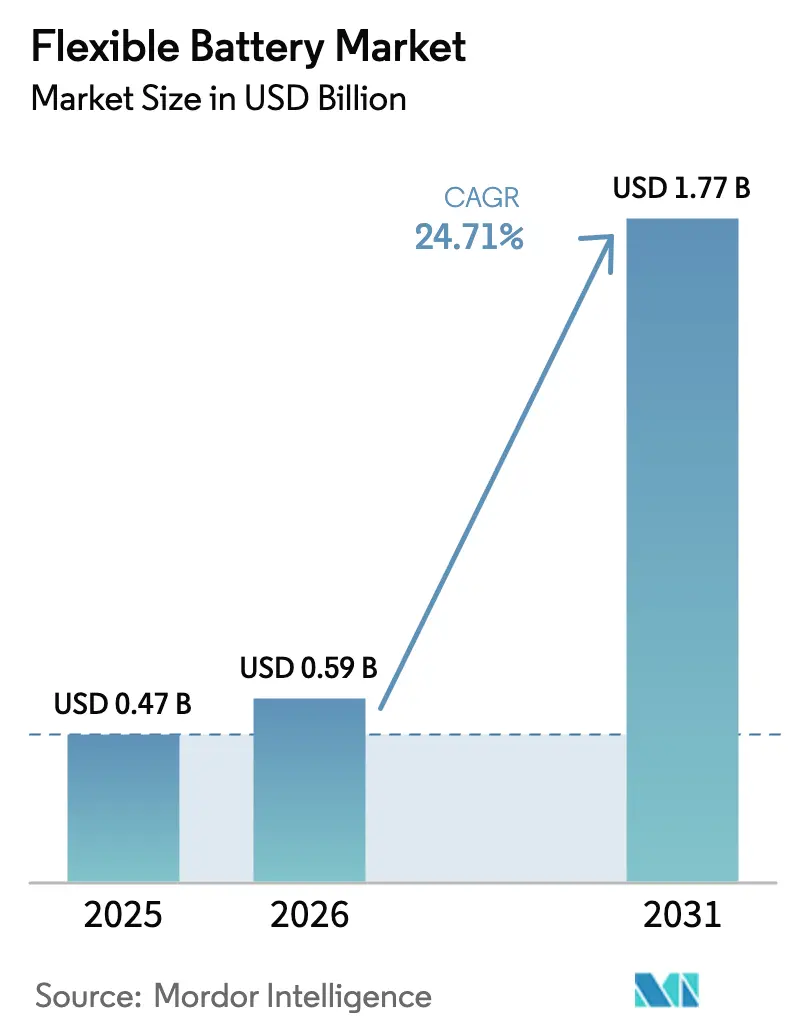

The Flexible Battery Market size is expected to grow from USD 0.47 billion in 2025 to USD 0.59 billion in 2026 and is forecast to reach USD 1.77 billion by 2031 at 24.71% CAGR over 2026-2031.

Demand for conformal power sources in wearables, IoT nodes, and defense electronics is expected to anchor near-term momentum in the flexible battery market. Manufacturing scale in the Asia-Pacific region is compressing unit costs, while investments in zinc-based chemistries are alleviating safety and sustainability concerns. Competitive pressure from emerging solid-state micro-lithium cells is stimulating R&D spending as incumbents race to defend share. Persistent supply-chain volatility for specialty cathode materials and roll-to-roll process constraints temper the growth outlook but have not derailed investor confidence in the flexible battery market’s long-term trajectory.

Key Report Takeaways

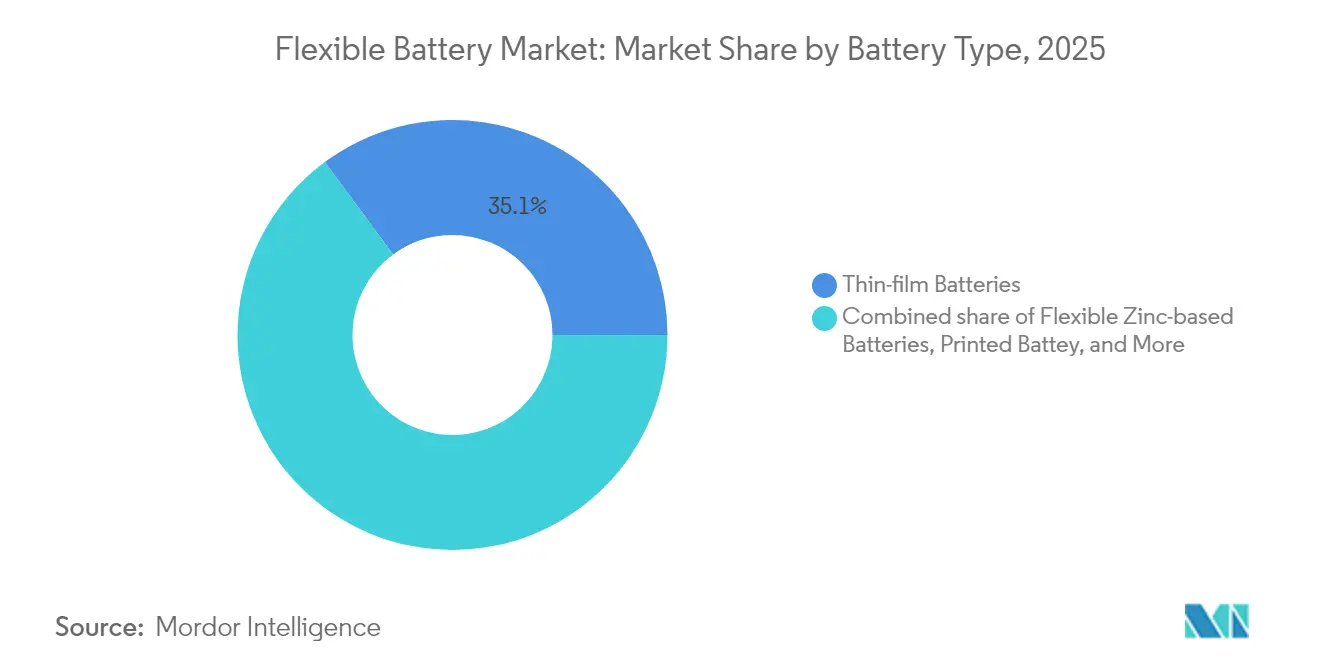

- By battery type, thin-film batteries led with 35.12% revenue share in 2025, whereas flexible zinc-based batteries are advancing at a 30.12% CAGR through 2031.

- By chemistry, lithium-ion held 40.63% of the flexible battery market share in 2025, while zinc-silver oxide is forecast to expand at a 32.85% CAGR to 2031.

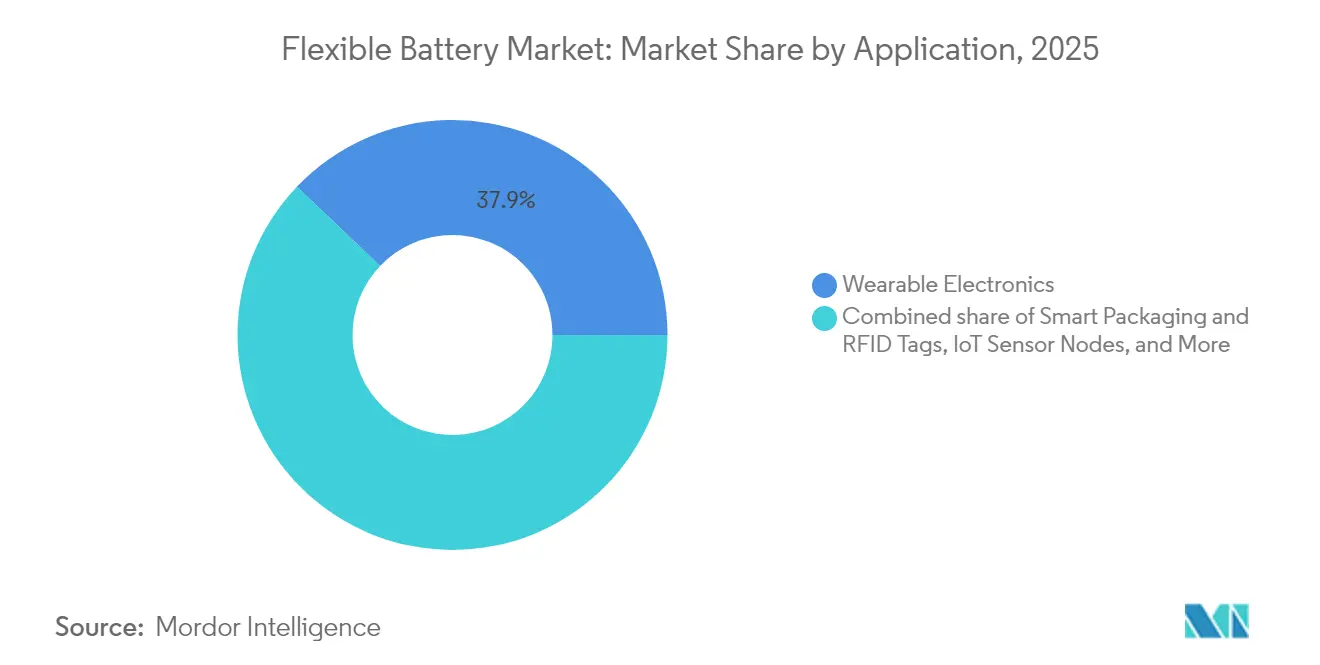

- By application, wearable electronics accounted for 37.88% of the flexible battery market size in 2025; however, smart packaging and RFID tags are projected to accelerate at a 31.44% CAGR through 2031.

- By geography, the Asia-Pacific region captured a 36.24% share of the flexible battery market in 2025 and is projected to grow at a 27.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of healthcare & fitness wearables | +4.2% | Global, early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| IoT sensor proliferation in smart infrastructure | +3.8% | Asia-Pacific core, spill-over to North America & EU | Long term (≥ 4 years) |

| Surge in miniaturized medical implants | +3.1% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of RFID-enabled smart packaging | +2.9% | Global, concentration in manufacturing hubs | Medium term (2-4 years) |

| Defense demand for conformal power sources | +2.4% | North America, selective adoption in allied nations | Short term (≤ 2 years) |

| Sustainability push for solid-state zinc chemistries | +2.1% | EU-led, with global adoption following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Healthcare & Fitness Wearables

Healthcare and fitness wearables are shifting from a consumer novelty to a clinical necessity, with the category projected to reach USD 100 billion by 2030.[1]Y. Khan, “Energy Harvesters and Storage for Wearables,” springer.com Continuous glucose monitors, neurological assessment patches, and rhythm-tracking chest straps require ultra-thin batteries that flex repeatedly without losing capacity. Efficiency leaps in piezoelectric harvesters—280× in recent prototypes—enable hybrid power modules that pair ambient energy capture with flexible storage. This design convergence reduces battery mass and enhances user comfort, reinforcing demand across the flexible battery market. Hospitals value data continuity, so suppliers that guarantee 5,000-cycle durability under torsion gain procurement preference. Rising telemedicine adoption and aging populations lock in multi-year volume visibility for specialized medical wearables.

IoT Sensor Proliferation in Smart Infrastructure

Smart-city rollouts, industrial automation, and precision agriculture collectively require billions of self-powered sensor nodes. Flexible batteries embedded in building materials or farm equipment eliminate the labor costs associated with cell replacement. The printed and flexible sensor market in automotive alone is projected to more than double to USD 960 million by 2034. Edge-computing gateways increase instantaneous power draw, so suppliers are testing hybrid architectures that sustain 15 mA pulses while idling below 2 µA. Governments fund resilient infrastructure, accepting premium pricing for batteries that guarantee decade-long life in hard-to-access locations. Consequently, the flexible battery market benefits from municipal procurement cycles that smooth short-term demand swings in consumer electronics.

Surge in Miniaturized Medical Implants

Implantable neurostimulators, smart stents, and drug-delivery capsules are shrinking to a thickness of less than 2 mm, forcing power sources to conform to the organic tissue. Self-healing lithium batteries now operate after puncture and regain 85% capacity within minutes. Regulatory agencies favor zinc-based chemistries due to their biocompatibility, and new water-based electrolytes eliminate the risk of thermal runaway. Device makers routinely cite battery reliability during MRI scans as a key factor in commercialization, prompting vendors to engineer robust encapsulation. This specialization helps achieve higher margins for medical-grade flexible batteries, thereby extending the flexible battery market’s reach into life-critical applications.

Expansion of RFID-Enabled Smart Packaging

Cold-chain pharmaceuticals, high-value foods, and industrial spares now move through global supply lines instrumented with disposable RFID tags. Printable zinc-manganese dioxide cells cost single-digit US cents per unit at volume, supporting item-level tracking. Brands deploy real-time temperature and humidity logging to meet stricter regulations, driving a 32.8% CAGR in smart packaging demand. Environmental legislation drives R&D toward biodegradable, flexible batteries that degrade within weeks while retaining 90% of their capacity during shelf life. Such innovations help the flexible battery market penetrate logistics operations previously limited by cost or sustainability objections.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from solid-state micro-Li batteries | -3.7% | Global, concentration in advanced manufacturing regions | Medium term (2-4 years) |

| Limited large-scale automated roll-to-roll capacity | -2.8% | Global manufacturing hubs, especially Asia-Pacific | Short term (≤ 2 years) |

| Supply volatility of specialty cathode materials | -2.1% | Global, acute impact where imports dominate | Short term (≤ 2 years) |

| Lack of universal standards for ultra-thin cells | -1.9% | Global, regulatory fragmentation across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Solid-State Micro-Li Batteries

Solid-state batteries promise 2-3× energy density and 90% lower thermal-runaway risk, attracting USD 8 billion in expected revenue by 2030. Samsung prototypes an all-solid-state wearable cell with a capacity of 200 Wh/L, with mass production scheduled for 2026. If cost parity with lithium-ion arrives by 2028, premium device makers could pivot away from polymer-based flexible batteries. Yet current double-sided polishing and dry-room requirements inflate capital costs, limiting penetration to high-end segments. The flexible battery market, therefore, faces share leakage but retains cost-sensitive, high-volume niches.

Limited Large-Scale Automated Roll-to-Roll Capacity

Efficient roll-to-roll plants must scale beyond 15 GWh annually to unlock sub-USD 50/kWh costs, yet most facilities remain below 2 GWh.[2]U.S. DOE, “Battery Manufacturing Scale-Up,” energy.gov Maintaining micron-level coating uniformity across kilometer-long webs constrains yield. Capital outlays exceed USD 100 million per line, deterring new entrants. Consequently, production backlogs for custom form factors lengthen, delaying device launches and capping near-term sales in the flexible battery market. Vendor partnerships with equipment suppliers aim to automate inspection and improve uptime, but implementation takes 12-18 months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Thin-Film Dominance Faces Zinc Disruption

Thin-film devices retained 35.12% of 2025 revenue thanks to entrenched supply chains in smartwatches and RFID tickets. Energy densities near 270 Wh/L and cycle lives above 1,500 position them as reliable incumbents. However, the flexible battery market size for zinc-based formats is projected to compound at a 30.12% annual rate, driven by their flame-retardant aqueous electrolytes and simplified environmental compliance. Vendors such as Blue Spark Technologies commercialize disposable printed zinc batteries for logistics tags, undercutting thin-film costs by 40%.

Performance gaps are narrowing. Roll-to-roll nanomanufacturing now yields hybrid zinc-carbon structures with a specific energy of 167 Wh/kg and a power density of 9.6 kW/kg. Medical wearables embrace zinc-air variants that maintain voltage under 30% strain. Smartphone OEMs still prioritize thin-film for premium footprints, but mid-range is exploring zinc inserts to raise safety scores without redesign as capacity scales past 20 GWh worldwide. Zinc prices are trending lower, reinforcing its trajectory within-tier devices that explore zinc inserts to raise safety scores without redesign, as capacity scales past 20 GWh worldwide. Zinc prices trend lower, reinforcing their trajectory inside the flexible battery market.

By Chemistry: Lithium-Ion Leadership Challenged by Zinc Innovation

Lithium-ion retained a 40.63% market share in 2025 due to the maturity of its anode and separator value chains. Yet, zinc-silver oxide is growing the quickest at a 32.85% CAGR, capturing applications where puncture tolerance supersedes energy density. The erosion of flexible battery market share for lithium chemistries is most visible in medical patches and smart labels, where regulators favor water-based electrolytes.

Cycle-life extensions via 2D superlattice cathodes push zinc-ion cells beyond 5,000 cycles, narrowing the longevity gap with nickel-rich lithium-ion cells.Moreover, corrosion-free zinc anodes trimmed to 5 µm slash cell thickness, unlocking form factors under 300 µm for epidermal electronics. Lithium-polymer retains niches requiring sub-100 µm thickness, but its market presence will plateau as zinc adoption scales. OEM diversification of chemistry portfolios mitigates raw-material risk and positions the flexible battery market for a shift toward multi-chemistry sourcing.

By Application: Wearables Lead While Smart Packaging Accelerates

Wearables generated 37.88% of 2025 revenue by embedding flexible batteries into straps, patches, and hearing aids. Average energy demand rose 15% with the addition of health sensors, sustaining volume growth even as unit sales mature. Meanwhile, smart packaging’s 31.44% CAGR signals the next frontier for the flexible battery market size. Disposable temperature-logging tags for biologics shipments attach sub-USD 0.10 printed batteries, opening million-unit orders.

Regulatory mandates for pharmaceutical traceability, such as the European Union’s Falsified Medicines Directive, fuel adoption in cold chains. Athletics brands embed NFC-enabled labels with printed zinc cells to combat counterfeiting, illustrating horizontal expansion beyond the pharmaceutical sector. Aerospace demand for flexible backups in aircraft sensor nodes adds incremental volume. Combined, these trends diversify revenue and cushion the flexible battery market against downturns in a single segment.

Geography Analysis

Asia-Pacific commanded 36.24% revenue in 2025, anchored by China’s vertically integrated ecosystem covering raw materials through device assembly. Government incentives in South Korea and Japan promote thin-film research and development, while India’s PLI scheme subsidizes printed battery lines. Forecast models indicate a 27.41% CAGR, strengthening the region’s primacy in the flexible battery market.

North America trails as the second-largest geography, driven by demand for defense and medical implants. The U.S. Department of Energy’s USD 100 million grant to Forge Battery illustrates policy moves to localize supply. Canadian provinces court investment by offering tax credits for roll-to-roll equipment, which helps offset higher labor costs. These initiatives aim to lift North American flexible battery market share above 24.6% by 2031.

Europe positions itself as a hub for sustainability. Battery passport regulations require lifecycle transparency, benefitting flexible batteries that can embed identity chips directly into cell construction. Pilot plants in Germany are testing solid-state zinc cells that comply with stringent recycling directives. Although baseline demand lags behind the Asia-Pacific region, policy certainty supports double-digit growth. Latin America and the Middle East & Africa are adopting flexible batteries through consumer electronics assembly and smart agriculture pilots, contributing to long-tail growth in the global flexible battery market.

Competitive Landscape

The flexible battery market exhibits high fragmentation, with the top five suppliers collectively holding below 25% of the combined revenue, creating opportunities for differentiation. Panasonic and Samsung SDI leverage gigafactory infrastructures to deliver thin-film formats, achieving cost efficiencies through shared procurement. In contrast, Enfucell and Imprint Energy specialize in printed zinc-based cells, which command premium margins in logistics tags.

M&A reshapes the field. EnerSys acquired Bren-Tronics for USD 208 million to secure defense contracts, while CCL Design absorbed Imprint Energy to accelerate printed battery rollouts. Patent filings rise annually; Samsung logged 40 solid-state wearable battery patents in 2024 alone, indicating a high level of R&D intensity. Start-ups such as ProLogium attract nine-digit venture rounds to scale roll-to-roll solid-state lines.

Strategic partnerships proliferate. Sakuu teams with SK On to industrialize solvent-free manufacturing, potentially halving capital expenditure per gigawatt-hour (GWh). Automotive OEMs sign conditional supply agreements for flexible zinc cells to hedge lithium volatility. Competitive dynamics therefore revolve around manufacturing scale, chemistry roadmaps, and integration services, keeping the flexible battery market in a state of rapid flux.

Flexible Battery Industry Leaders

Panasonic Corporation

LG Energy Solution

Samsung SDI

Enfucell Oy

BrightVolt Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lyten acquired Europe’s largest battery energy storage systems operation from Northvolt to expand flexible battery capabilities.

- July 2025: Panasonic has opened a USD 4 billion EV battery plant in Kansas, capable of producing 66 batteries per second.

- January 2025: Forge Battery, a subsidiary of Forge Nano, clinched a USD 100 million deal with the US Department of Energy (DOE) to bolster its North Carolina gigafactory.

- September 2024: Samsung Electro-Mechanics has unveiled a cutting-edge, ultra-compact all-solid-state battery tailored for wearable devices.

Global Flexible Battery Market Report Scope

- A flexible battery is a type of power source designed to bend or conform to various shapes without compromising its functionality. It typically employs innovative materials and construction techniques to achieve this flexibility, making it suitable for integration into curved or irregularly shaped devices, such as wearable electronics, flexible displays, and medical implants. Flexible batteries often utilize thin, lightweight components and advanced manufacturing processes to maintain their energy storage capabilities while adapting to the dynamic form factors of modern technology.

- The flexible battery market is segmented by type, application, and geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). By type, the market is segmented into thin-film batteries and printed batteries. By application, the market is segmented into consumer electronics, medical devices, smart packaging, smart cards, and other applications. The report also covers the market size and forecasts for the flexible battery market across major countries. Market sizing and forecasts were made for each segment based on revenue (USD).

| Thin-film Batteries |

| Printed Batteries |

| Laminate Lithium-Polymer Batteries |

| Flexible Zinc-based Batteries |

| Other Emerging Types (Micro-solid-state, Paper, CNT) |

| Lithium-ion |

| Lithium-polymer |

| Zinc-manganese Dioxide |

| Zinc-Silver Oxide |

| Nickel-Metal Hydride |

| Wearable Electronics |

| Medical and Healthcare Devices |

| IoT Sensor Nodes |

| Smart Cards and e-Paper Displays |

| Smart Packaging and RFID Tags |

| Aerospace and Defense |

| Others (Energy Harvesting, Toys) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Type | Thin-film Batteries | |

| Printed Batteries | ||

| Laminate Lithium-Polymer Batteries | ||

| Flexible Zinc-based Batteries | ||

| Other Emerging Types (Micro-solid-state, Paper, CNT) | ||

| By Chemistry | Lithium-ion | |

| Lithium-polymer | ||

| Zinc-manganese Dioxide | ||

| Zinc-Silver Oxide | ||

| Nickel-Metal Hydride | ||

| By Application | Wearable Electronics | |

| Medical and Healthcare Devices | ||

| IoT Sensor Nodes | ||

| Smart Cards and e-Paper Displays | ||

| Smart Packaging and RFID Tags | ||

| Aerospace and Defense | ||

| Others (Energy Harvesting, Toys) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the flexible battery market by 2031?

The flexible battery market is expected to reach USD 1.77 billion by 2031 at a 24.71% CAGR.

Which battery type holds the largest share today?

Thin-film batteries led with 35.12% revenue share in 2025.

Which chemistry is growing the fastest?

Zinc-silver oxide chemistry is expanding at a 32.85% CAGR through 2031.

Why is Asia-Pacific so dominant in flexible batteries?

The region combines raw-material processing, cell production, and device assembly, translating to 36.24% market share in 2025 and the fastest growth at 27.41% CAGR.

What applications are driving future demand beyond wearables?

Smart packaging and RFID tags are the fastest-growing use case, advancing at a 31.44% CAGR as supply chains digitize.

How fragmented is the competitive landscape?

With the top five players holding under 25% share, the market remains moderately fragmented, rated 4 on a 10-point concentration scale.

Page last updated on: