Battery Plate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

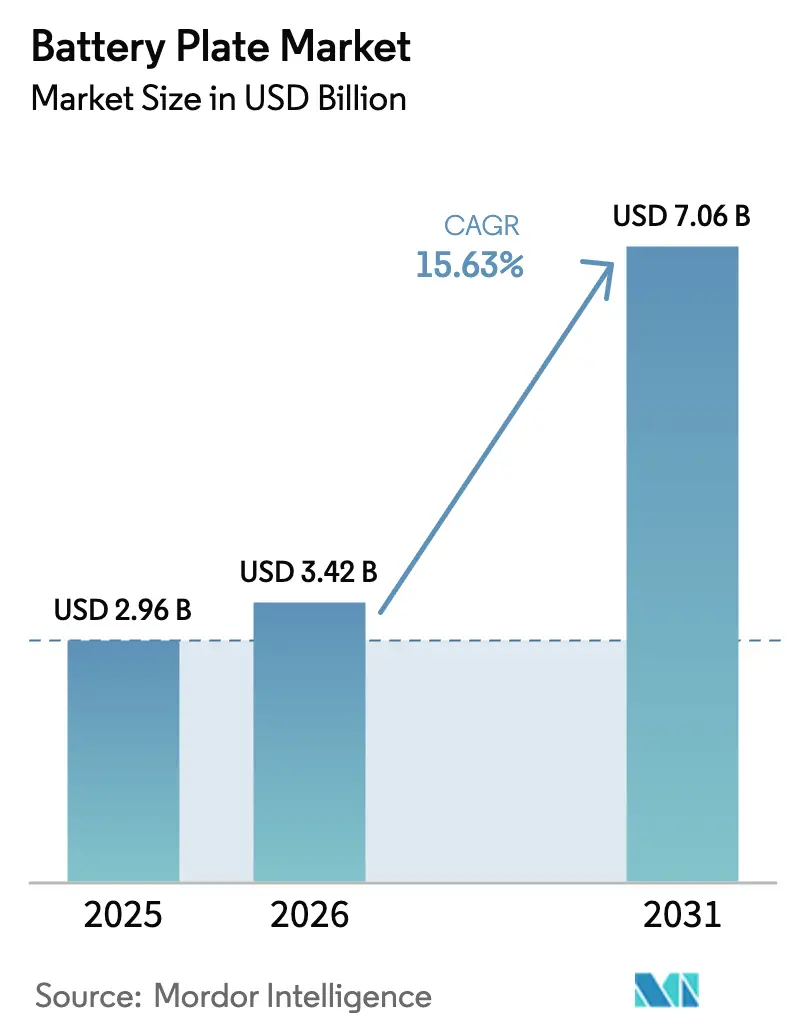

| Market Size (2026) | USD 3.42 Billion |

| Market Size (2031) | USD 7.06 Billion |

| Growth Rate (2026 - 2031) | 15.63% CAGR |

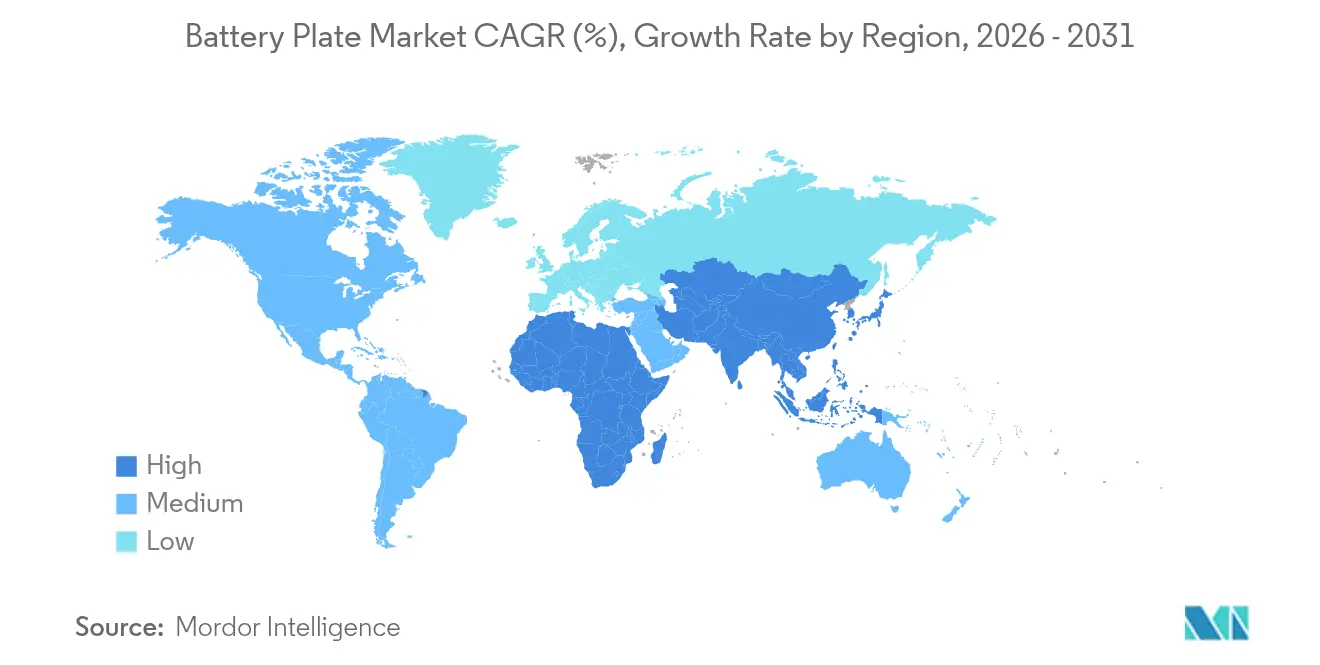

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Plate Market Analysis by Mordor Intelligence

The Battery Plate market size is expected to grow from USD 2.96 billion in 2025 to USD 3.42 billion in 2026 and is forecast to reach USD 7.06 billion by 2031 at 15.63% CAGR over 2026-2031.

Demand scales with the rollout of electric vehicles, renewable-heavy grids, and factory upgrades that reduce the cost per plate while enhancing electrochemical performance. The battery plate market is therefore evolving from a traditional lead-acid component supplier to a cornerstone of the energy transition supply chain. The Asia-Pacific region anchors both production and consumption, while utility-scale storage pushes novel plate architectures, and manufacturing innovations, such as 3D printing, widen design latitude. Competitive rivalry intensifies as lead-acid specialists, lithium-ion leaders, and alternative-chemistry entrants vie for procurement contracts and technology partnerships.

Key Report Takeaways

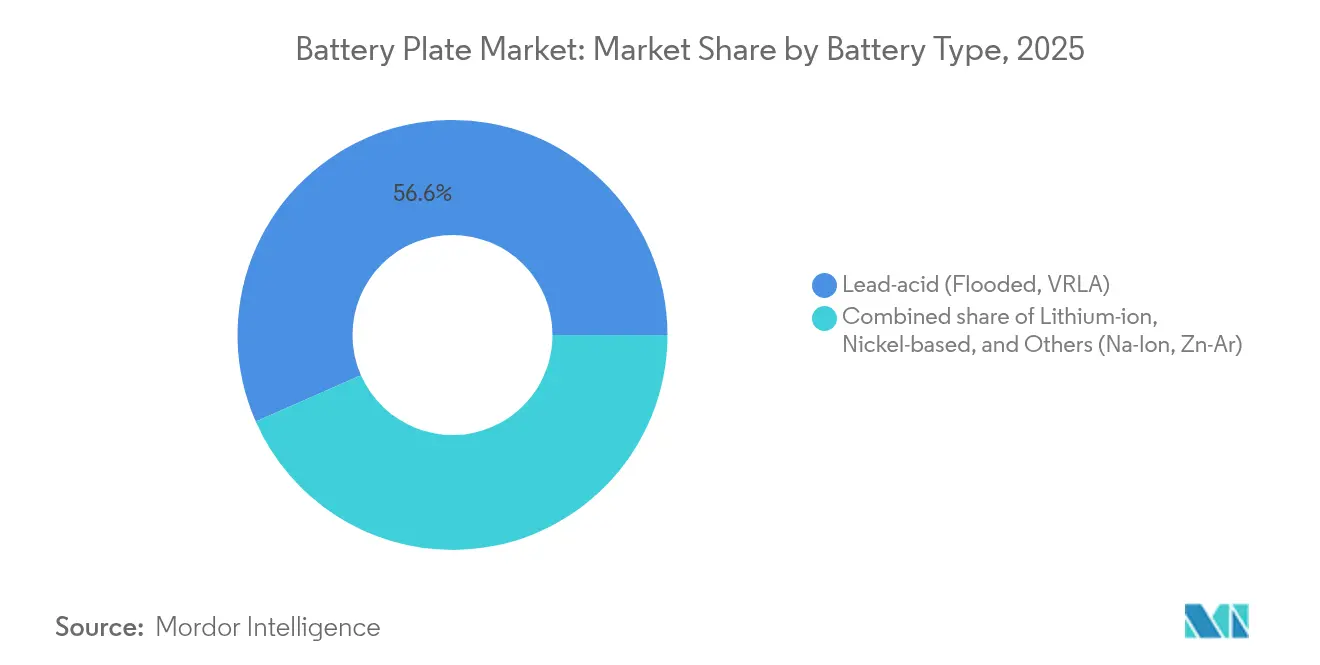

- By battery type, lead-acid technology led with 56.60% revenue share in 2025, while lithium-ion plates are forecast to grow at 17.15% CAGR through 2031.

- By plate material, lead-calcium alloys accounted for 47.05% of the battery plate market size in 2025; graphite-coated composites are set to accelerate at a 19.52% CAGR.

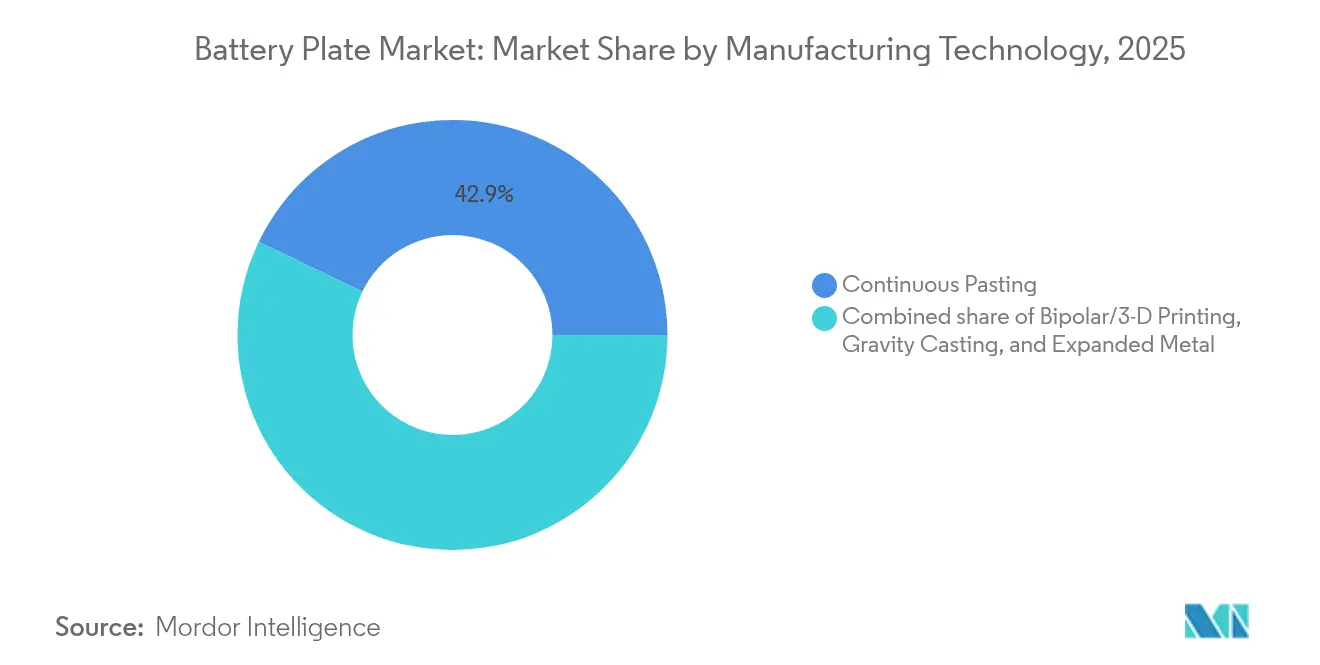

- By manufacturing process, continuous pasting captured 42.85% of the battery plate market share in 2025, whereas bipolar and 3D-printed plates are rising at an 18.62% CAGR.

- By end-user, automotive applications accounted for 52.25% of the battery plate market size in 2025, whereas energy storage systems are expected to advance at a 19.05% CAGR.

- By geography, the Asia-Pacific region commanded 58.90% of the battery plate market share in 2025 and is projected to expand at a 16.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Battery Plate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-led surge in lead-acid SLI demand | +4.2% | Asia-Pacific, North America, global spill-over | Medium term (2-4 years) |

| Utility-scale ESS roll-outs in emerging markets | +3.8% | APAC core, MEA & South America spill-over | Long term (≥4 years) |

| Adoption of corrosion-resistant Pb-Ca-Sn grids | +2.1% | Europe & North America, global diffusion | Short term (≤2 years) |

| 3-D printed bipolar plate architectures | +1.9% | North America & Europe, expanding to APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

EV-led Surge in Lead-acid SLI Demand

Electric vehicles utilize 12 V lead-acid batteries for fail-safe power to critical functions, leaving a sizable floor for SLI plates despite the dominance of lithium-ion traction. Global EV sales touched 14 million units in 2024.[1]International Energy Agency, “Global EV Outlook 2025,” iea.org Start-stop systems within internal-combustion cars extend cycling frequency and heighten durability requirements, spurring higher-grade grid designs. Mild hybrids employ dual-battery setups, so lead-acid plates remain complementary rather than competitive to high-voltage packs. OEMs, therefore, maintain long-term contracts with established plate suppliers for auxiliary systems. This linkage cushions the battery plate market against abrupt lead-acid displacement and stabilizes baseline volumes across regions.

Utility-scale ESS Roll-outs in Emerging Markets

Emerging economies added 42 GW of grid storage in 2024, with 35% of the installations located outside mature OECD markets. Duration-driven projects select iron-flow, sodium-ion, and other chemistries, each needing bespoke plate geometry for multi-hour discharge. The world’s largest sodium-ion BESS entered service in 2024, proving cost-effectiveness where lithium sourcing remains pricey. Governments couple renewables with localized storage mandates, broadening procurement beyond conventional lithium-ion plates. Suppliers capable of engineering chemistry-specific plates gain a first-mover advantage as utilities solicit turnkey solutions.

Adoption of Corrosion-resistant Pb-Ca-Sn Grids

Valve-regulated lead-acid systems now rely on lead-calcium-tin alloys that demonstrate stronger electrochemical stability and lower water loss than antimony-rich grids. Thinner, lighter grids cut metal usage by up to 20% without compromising structural strength. Telecom and UPS operators gravitate toward maintenance-free formats, spurring immediate uptake in North America and Europe. Cost savings stem from fewer service visits and longer replacement cycles, directly improving total-cost-of-ownership metrics. These alloys thus reinforce the incumbent position of lead-acid plates in industrial standby applications.

3-D Printed Bipolar Plate Architectures

Additive manufacturing enables the integration of cooling channels, gradient thickness, and current-collection ribs within single-piece plates.[2]Nature Energy, “3D-printed Bipolar Plates for High-Power Batteries,” nature.com Tesla’s structural battery pack demonstrates how bipolar formats can eliminate module assembly, reduce part count, and enhance volumetric efficiency. Polymer-composite bipolar plates weigh 40% less than their metallic counterparts yet still meet the conductivity thresholds required for passenger-car environments. The method excels at rapid prototyping, enabling design iterations without the need for costly dies. Durability validation under high-temperature cycling is ongoing, but early field trials in stationary systems have already shown promising lifespan figures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in refined-lead prices | -2.3% | Global, particularly impacting Asia-Pacific and Europe | Short term (≤ 2 years) |

| Stringent hazardous-waste directives (RoHS, ELV) | -1.7% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Limited availability of high-purity recycled lead | -1.2% | Global, with acute impact in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Refined-lead Prices

Lead prices fluctuated sharply in 2024, driven by supply disruptions and sustained demand for batteries. Raw materials account for up to 70% of plate production cost, so pricing spikes compress margins in short order. Recycling offers partial relief, yet high-purity alloy grades limit secondary content ratios in premium plates. Manufacturers hedge through long-term contracts and futures positions, but smaller firms lack the financial firepower to maintain stable input costs. Price instability, therefore, discourages capital investment in new plate lines and tilts procurement decisions toward chemistry diversification.

Stringent Hazardous-waste Directives (RoHS, ELV)

The EU End-of-Life Vehicles directive mandates rigorous recycling quotas, escalating compliance expenses for lead-based batteries. China’s roasting of RoHS rules to include batteries adds regional variants that complicate global supply planning. Manufacturers must document material composition, adapt alloy recipes, and certify processes for each jurisdiction. Compliance costs weigh heavier on SMEs, accelerating consolidation or exit. Simultaneously, the regulatory spotlight amplifies R&D into lead-free alternatives, thus redirecting funding away from traditional plate upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Lead-acid Dominance Faces Lithium Challenge

Lead-acid technology controlled 56.60% of the battery plate market share in 2025, primarily due to its entrenched use in automotive SLI and cost-sensitive industrial niches. Lithium-ion plates, however, are scaling at 17.15% CAGR as EV and high-performance storage proliferate, thereby re-balancing procurement budgets within the battery plate market. Flooded lead-acid units still anchor telecom backup because installers trust their field heritage and cost profile. VRLA derivatives meet the premium automotive demand for the introduction of sodium-ion and zinc-air entrants that address supply-chain risk and safety. CATL placed Naxtra sodium-ion batteries into mass production in June 2025, utilizing maintenance-free designs and rapid charge acceptance. Nickel-based systems fill aerospace and defense micro-segments, where extreme temperature tolerance offsets higher price points.

Diversification continues with sodium-ion and zinc-air entrants that address supply-chain risk and safety. CATL placed Naxtra sodium-ion batteries into mass production in June 2025, requiring aluminum rather than copper current collectors. Plate manufacturers now juggle multiple metallurgical toolkits to align with each chemistry’s corrosion profile. This fragmentation elevates design-for-manufacture complexity but also widens addressable opportunity across the battery plate market.

By Plate Material: Advanced Composites Disrupt Traditional Alloys

Lead-calcium grids owned a 47.05% share of plate material demand in 2025, combining corrosion resistance with robust mechanical properties in sealed batteries. The battery plate market, nevertheless, rewards innovation; graphite-coated and carbon-foam composites are predicted to grow at a rate of 19.52% annually through 2031, driven by lightweighting and thermal-management agendas. Lead-antimony alloys persist in deep-cycle forklifts because they better withstand mechanical stress during heavy discharge. Niche applications turn to lead-tin mixes for superior conductivity, though elevated tin costs confine uptake to specialty products.

Composite momentum mirrors wider industry appetite for energy density gains. Group14’s silicon-rich SCC55 anode, for instance, lifts cell capacity by 50%, signalling comparable payoffs when carbon-rich matrices reduce internal resistance. Plate makers able to scale composite grids without cost blow-outs secure a differentiated portfolio within the battery plate market.

By Manufacturing Technology: 3D Printing Challenges Conventional Methods

Continuous pasting lines held a 42.85% market share of the battery plate market in 2025, owing to their proven throughput and repeatability. Yet, bipolar and 3D-printed formats are accelerating at an 18.62% CAGR, as additive layers permit lattice geometries that are beyond the reach of stamping. Gravity casting is suitable for low-volume, bespoke plates and for chemistries that require thicker sections. Expanded metal grids provide a high surface area with minimal scrap, making them attractive to two-wheeler batteries where every gram counts.

Digital-twin supervision, exemplified by Siemens and Fraunhofer’s Münster pilot, now integrates real-time data capture into plate factories, reducing waste and enhancing uptime. Such an Industry 4.0 overlay converts design freedom into economically viable output, reinforcing the appeal of advanced techniques inside the battery plate market.

By End-user: Energy Storage Emerges as Growth Engine

Automotive customers accounted for 52.25% of revenue in 2025, linking household names such as Toyota and Ford to long-term SLI supply contracts. Energy storage systems, however, are projected to post a brisk 19.05% CAGR thanks to grid modernization, residential solar adoption, and flexible peaking mandates. Industrial motive power—forklifts, mining carts, port cranes—delivers predictable demand for deep-cycle plates engineered for harsh duty. Consumer electronics contribute modest but steady volume as devices shrink, yet proliferation continues.

Grid storage requires multi-hour endurance, along with high cycle life, nudging plate designers toward thick, corrosion-resistant grids and high-porosity active materials. Natron Energy’s 600 MW sodium-ion plant in Michigan demonstrates how alternative chemistries are being commercialized to meet these requirements. Suppliers that translate such needs into scalable plate production gain priority bidding status in utility procurement, underpinning future growth of the battery plate market.

Geography Analysis

Asia-Pacific controlled 58.90% of the battery plate market in 2025 and will maintain leadership at a 16.28% CAGR through 2031. China’s power battery output surged 176% in the first half of 2024, yet looming oversupply drives consolidation and efficiency projects. South Korea retains 37% of global battery cell capacity through LG Energy Solution and SK On, while government grants focus on pre-commercial solid-state platforms. Japan secures niche aerospace and premium-vehicle contracts, leveraging materials expertise even as volume shifts to mainland Asia. India’s Production-Linked Incentive program has attracted substantial investment; Amara Raja’s INR 95 billion gigafactory exemplifies the country’s localization push.

North America and Europe together represent the next frontier for the battery plate market. United States capacity is slated to hit 1,200 GWh by 2030, aided by 10 new factories commencing in 2025. Federal tax credits tilt procurement toward domestic plates, prompting supplier footprint expansion. European projects aim for 1.5 TWh by 2030, though financing delays imperil half the announced pipeline. Germany hosts Northvolt’s 60 GWh facility, France backs Verkor at Dunkirk, and the EU Green Deal channels funds into recycling streams that will feed future plate alloy demand.

South America and the Middle East & Africa add emerging prospects for the battery plate market. Brazil and Argentina exploit lithium and lead reserves, yet infrastructure hurdles moderate immediate scale-up. Gulf states deploy high-solar-penetration grids that require large energy storage buffers, opening tenders for sodium-ion and lead-carbon systems. Africa’s mineral wealth promises vertical integration possibilities, although political stability and logistics build-out remain prerequisites before gigafactory economics align.

Competitive Landscape

Competitive intensity within the battery plate market is moderate, with no single technology or region dominating all use cases. Clarios, Exide, and GS Yuasa maintain strong automotive SLI footholds through longstanding OEM agreements and extensive service networks. CATL and BYD channel EV momentum into downstream plate demand while investing in R&D for sodium-ion and solid-state prototypes. Narada Power focuses on telecom standby arrays, Crown Battery steers into industrial deep-cycle niches, and Natron Energy scales blue-sodium chemistries for multihour grid services.

Strategic patterns diverge between vertical integration and specialization. CATL secures offtake pacts with GM and Volkswagen, coupling cell production with raw-materials sourcing under long-term contracts. Amara Raja signed technology-licensing deals with GIB EnergyX to leapfrog into lithium-iron-phosphate manufacturing. Traditional plate makers incubate joint ventures to share capital risk when entering lithium segments, while still leveraging legacy lead-acid volumes to fund R&D. Overcapacity in China pressures margins, whereas North American and European buyers pay premiums for compliance-ready, regionally sourced plates.

Innovation hotspots cluster around additive manufacturing, advanced alloys, and digital production control. Siemens’ digital-twin implementation enables “first-time-right” runs, which reduce scrap during 3D-printed plate fabrication.[4]Siemens AG, “Digital-Twin Solutions for Fraunhofer Battery Cell Factory,” siemens.com Group 14 and Lyten advance silicon-rich and lithium-metal inputs, respectively, influencing downstream plate metallurgy. In response, conventional lead-acid leaders pilot composite grids, hoping to retain share where cost and safety overshadow energy-density considerations. As chemistries diversify, suppliers capable of multi-chemistry plate portfolios enjoy hedged demand streams across cycles.

Battery Plate Industry Leaders

Clarios, LLC

GS Yuasa Corporation

Exide Industries Ltd.

East Penn Manufacturing

Enersys

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lyten initiated the domestic production of battery-grade lithium metal in the U.S. This achievement marks a pivotal step in bolstering the U.S. battery supply chain, aiming to reduce dependence on overseas sources for essential battery materials.

- February 2025: Luminous Power Technologies, a prominent player in the lead-acid battery sector, inaugurated a state-of-the-art production facility in North India.

- January 2025: EnerSys obtained a USD 199 million Department of Energy award to construct a lithium-ion gigafactory in Greenville, South Carolina.

- June 2024: Marelli clinched a contract with a leading global automaker to provide the Battery Thermal Plate (BTP) for upcoming Battery Electric Vehicles (BEVs).

Global Battery Plate Market Report Scope

Battery plates are fabricated using a lattice grid structure, supporting the active material within them. Additionally, these plates facilitate the conduction of electricity, allowing for the efficient flow of electrical charges during the charging and discharging processes.

The battery plate market is segmented into battery type, end-user, and geography. By battery type, market is segmented into lithium-ion batteries, lead-acid batteries, and other types. By end-user, the market is segmented into Automotive, Aerospace, Energy Storage, Aerospace, Electronics, and Others. The report also covers the market size and forecasts across major regions. The market sizing and forecasts for each segment are based on revenue (in USD).

| Lead-acid (Flooded, VRLA) |

| Lithium-ion |

| Nickel-based |

| Others (Zn-Air, Na-Ion, etc.) |

| Lead-Antimony Alloy |

| Lead-Calcium Alloy |

| Lead-Tin Alloy |

| Advanced Composites (Graphite-coated, Carbon Foam) |

| Gravity Casting |

| Continuous Pasting |

| Expanded Metal |

| Bipolar/3-D Printing |

| Automotive (SLI, Start-Stop) |

| Industrial (Forklifts, Telecom, UPS) |

| Energy Storage Systems |

| Consumer Electronics |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Type | Lead-acid (Flooded, VRLA) | |

| Lithium-ion | ||

| Nickel-based | ||

| Others (Zn-Air, Na-Ion, etc.) | ||

| By Plate Material | Lead-Antimony Alloy | |

| Lead-Calcium Alloy | ||

| Lead-Tin Alloy | ||

| Advanced Composites (Graphite-coated, Carbon Foam) | ||

| By Manufacturing Technology | Gravity Casting | |

| Continuous Pasting | ||

| Expanded Metal | ||

| Bipolar/3-D Printing | ||

| By End-user | Automotive (SLI, Start-Stop) | |

| Industrial (Forklifts, Telecom, UPS) | ||

| Energy Storage Systems | ||

| Consumer Electronics | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the battery plate market?

The battery plate market size was USD 3.42 billion in 2026.

How fast is the battery plate market expected to grow?

The market is forecast to post a 15.63% CAGR over 2026-2031, taking revenue to USD 7.06 billion by 2031.

Which region leads battery plate demand?

Asia-Pacific held 58.90% of global revenue in 2025 and is forecast to grow the quickest at 16.28% CAGR.

Which application segment is expanding the fastest?

Energy storage systems are the fastest-growing end-user group with a 19.05% CAGR through 2031.

What manufacturing technologies are gaining traction?

Bipolar and 3D-printed plates are rising at an 18.62% CAGR, challenging continuous pasting’s incumbent position.

How do raw-material price swings affect suppliers?

Lead price volatility can shave 2.3 percentage points off forecast CAGR, forcing producers to adopt hedging and recycling strategies.

Page last updated on: