Market Overview

| Study Period | 2021 - 2031 |

|---|---|

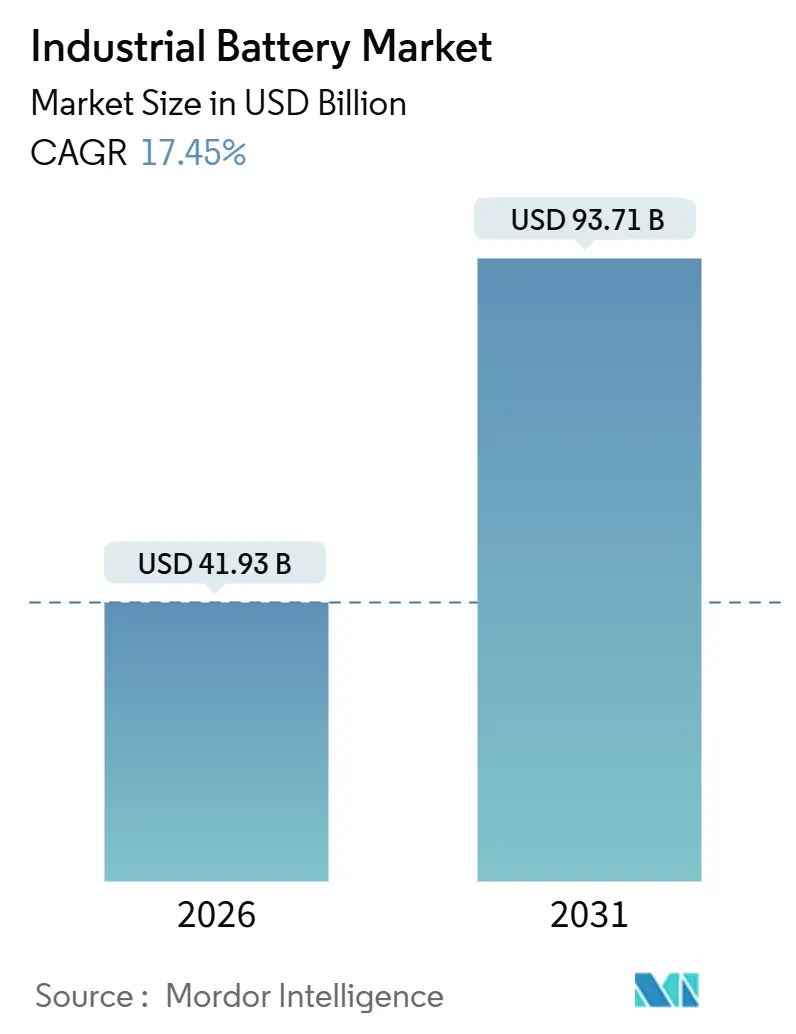

| Market Size (2026) | USD 41.93 Billion |

| Market Size (2031) | USD 93.71 Billion |

| Growth Rate (2026 - 2031) | 17.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Battery Market Analysis by Mordor Intelligence

The Industrial Battery Market size is estimated at USD 41.93 billion in 2026, and is expected to reach USD 93.71 billion by 2031, at a CAGR of 17.45% during the forecast period (2026-2031).

Rapid price erosion in lithium-ion cells, clean-energy subsidies in North America and Europe, and renewable-paired storage mandates in Asia-Pacific are steering capital away from combustion-based backup toward electrochemical storage across grid, telecom, data-center, and logistics operations. Telecom tower operators, hyperscale data-center owners, and warehouse integrators are now modeling decade-long replacement cycles that favor lithium-ion’s long service life, even as fire-risk insurance costs and critical-mineral volatility temper short-term margins.

Key Report Takeaways

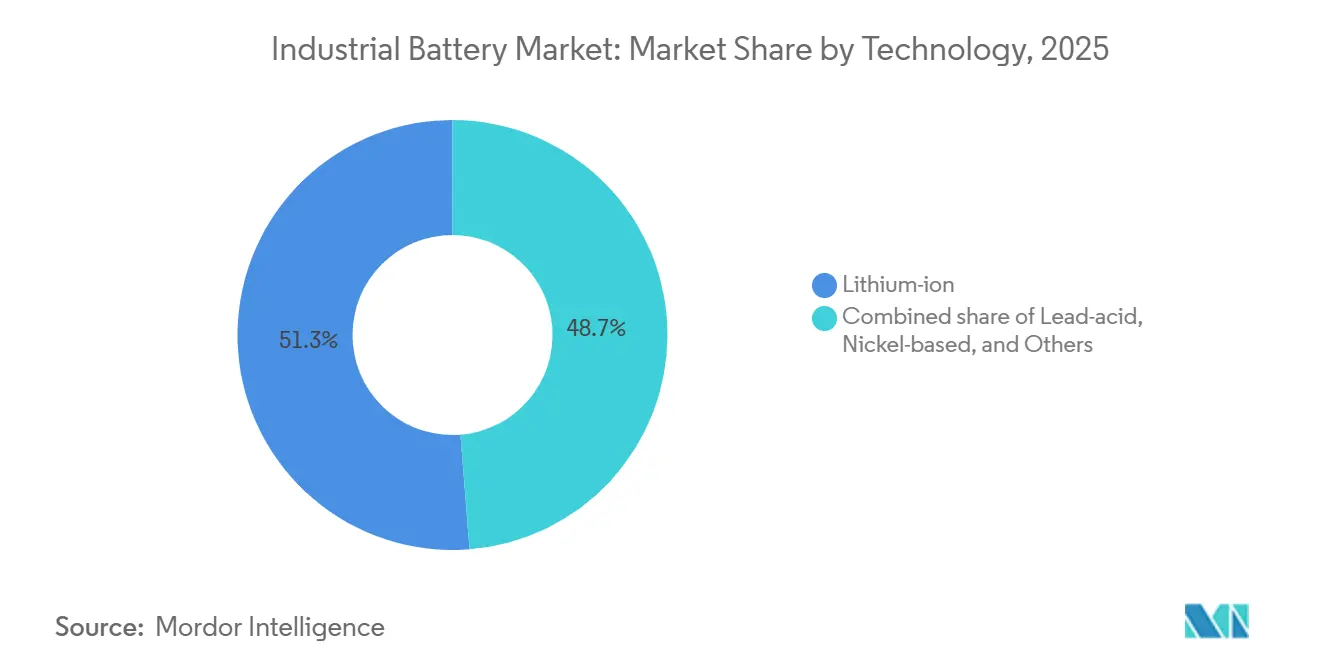

- By technology, lithium-ion captured 51.26% of the industrial battery market share in 2025 and is projected to expand at an 18.56% CAGR through 2031.

- By application, forklift and motive-power systems accounted for a 31.65% share of the industrial battery market size in 2025 and are advancing at an 18.65% CAGR through 2031.

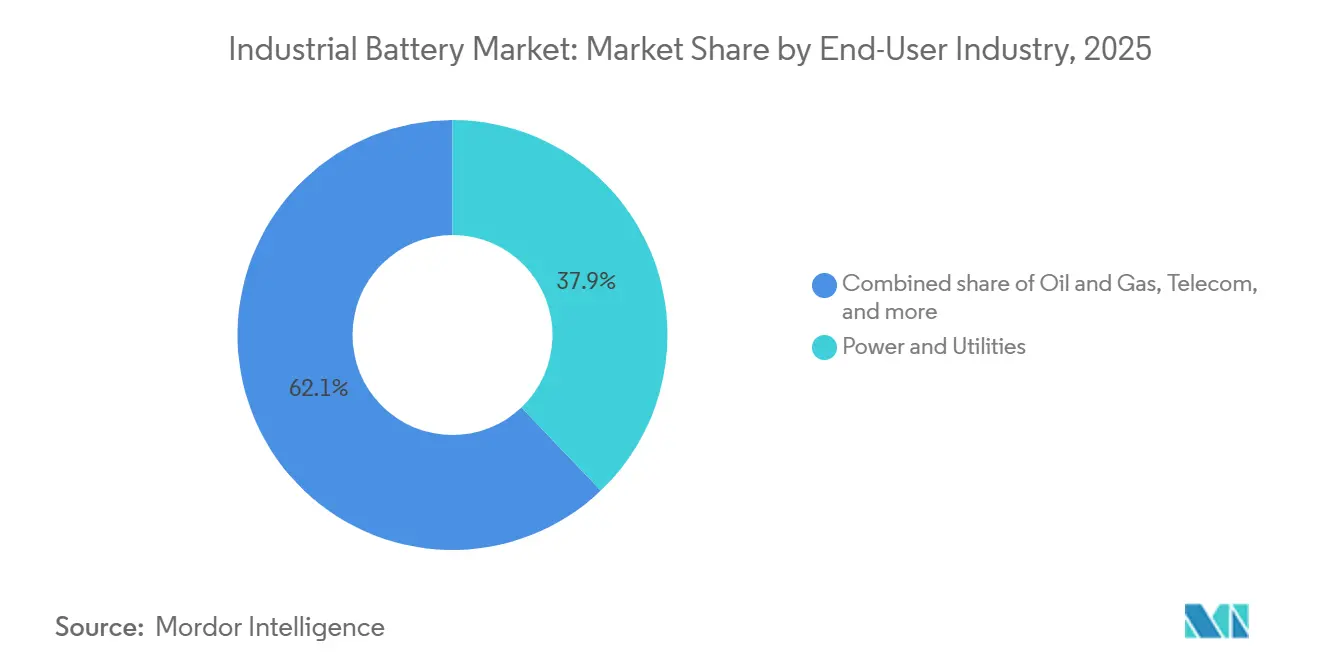

- By end-user, power and utilities led with 37.88% spending in 2025; manufacturing and warehousing record the fastest forecast CAGR at 18.65% through 2031.

- By geography, Asia-Pacific commanded 49.92% revenue in 2025 and is expected to grow at a 19.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion battery cost curve | +3.2% | Global, with steepest drops in China and accelerating in North America post-IRA | Medium term (2-4 years) |

| Renewable-powered ESS build-outs | +4.1% | APAC core (China, India), spillover to North America and Europe | Long term (≥ 4 years) |

| Warehouse automation & AGVs surge | +2.8% | North America, Europe, APAC manufacturing hubs (China, Japan, South Korea) | Short term (≤ 2 years) |

| DC micro-grids in data centers | +1.9% | North America (hyperscale clusters), Europe, emerging in APAC | Medium term (2-4 years) |

| Telecom tower storage mandates | +2.3% | APAC (India, Southeast Asia, Africa), with regulatory push in emerging markets | Short term (≤ 2 years) |

| OEM-driven 2nd-life leasing models | +1.5% | Europe (EU Battery Regulation compliance), North America, early adoption in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Battery Cost Curve

Pack prices slid to USD 115 per kWh in 2024, the sharpest drop since 2017, and major banks forecast sub-USD 80 per kWh by late 2026 as cell-to-pack integration cuts overhead. Chinese LFP cells traded at USD 50-53 per kWh in early 2024, forcing Western rivals to localize or cede margin. Utility-scale four-hour systems are now modeled to reach USD 147-243 per kWh by 2035, eroding lead-acid’s total-cost supremacy in telecom backup. Buyers increasingly align budgets to ten-year life-cycle analyses, tilting orders toward lithium-ion despite residual thermal-runaway concerns.

Renewable-Powered ESS Build-Outs

Grid-scale battery additions rose 38% year-over-year to October 2025 and are set to add 94 GW/247 GWh in 2025 alone, jumping to 220 GW/972 GWh by 2035 as intermittent solar and wind portfolios require firming capacity. The United States plans 18.2 GW of storage in 2025, benefiting from investment-tax credits and state mandates.[1]“Energy Storage Trends 2025,” U.S. Energy Information Administration, eia.gov China’s provincial rules force new renewables to pair 10-20% storage, creating near-term demand, although capped arbitrage margins cloud profitability. India targets 4 GWh of standalone storage by 2026 to stabilize high-renewable grids. Europe’s frequency-regulation premiums remain attractive for batteries, though interconnector growth could compress spreads after 2028.

Warehouse Automation & AGVs Surge

Automated guided vehicle (AGV) shipments topped 60,000 units in 2024, with lithium-ion powering more than 70% of new models due to opportunity-charging that halves downtime versus lead-acid.[2]“Warehouse Automation Report,” Material Handling Institute, mhi.org E-commerce hubs reclaim floor space by retiring battery-swap rooms, and sustainability pledges penalize lead-acid’s hazardous-waste profile. Forklift OEMs now position lithium-ion as the default on Class I and II trucks, reversing pre-2020 price hierarchies. The acceleration in warehouse electrification is unfolding faster than aggregate material-handling equipment revenue growth, tightening delivery lead-times for cell makers.

DC Micro-Grids in Data Centres

Hyperscale operators are piloting 48-V lithium-ion racks embedded in server rows, trimming conversion losses by up to 15% and delivering sub-millisecond failover. Google and Microsoft prototypes remove centralized UPS rooms, freeing real estate for compute expansion. AI workloads push megawatt-level peaks, making high-density batteries critical to avoid demand-charge penalties. Regulatory standards lag, with IEC DC-microgrid rules still in draft, injecting liability uncertainty that tempers mass rollout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral price volatility | -2.4% | Global, with acute exposure in regions dependent on Chinese intermediates (North America, Europe) | Short term (≤ 2 years) |

| Rising BESS fire-risk insurance costs | -1.6% | North America, Europe, South Korea (post-incident tightening); emerging in APAC | Medium term (2-4 years) |

| Lead-acid pollution regulations | -0.9% | Europe (EU Battery Regulation), China (emissions standards), India (Battery Waste Management Rules) | Medium term (2-4 years) |

| Solid-state tech "wait-and-see" effect | -1.2% | Global, particularly affecting long-term capital commitments in North America, Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Price Volatility

Lithium carbonate plunged 75% from its 2022 peak, then tightened again in 2025 as inventory destocking met robust demand, unsettling contract negotiations and cash-flow planning.[3]“Critical Minerals Market Review,” International Energy Agency, iea.org China processes more than 90% of anode materials and 85% of cathodes, amplifying geopolitical exposure for Western buyers. Supply bottlenecks in purified phosphoric acid and high-purity manganese sulfate can double input costs within a quarter, prompting buyers to shorten procurement cycles and raise working-capital buffers. U.S. strategic stockpiles address security rather than price, and may constrict spot availability.

Lead-Acid Pollution Regulations

Incidents at Moss Landing, California, and Korean utility sites triggered premium hikes of 20-50% and forced adoption of extra suppression gear, adding USD 20-50 per kWh to capex.[4]“Battery Fires and Insurance,” UL Solutions, ul.com UL 9540A propagation tests now extend commissioning 3-6 months, and South Korea has mandated real-time thermal monitoring. Developers prefer LFP chemistries for lower thermal risk but sacrifice energy density where land costs dominate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Lithium-Ion Dominance Reshapes Chemistry Mix

Lithium-ion held 51.26% revenue in 2025 and is projected to compound at 18.56% to 2031, solidifying its leadership in the industrial battery market. Lead-acid’s legacy telecom and starter-lighting niches shrink as buyers weigh total cost over calendar life. Nickel-based chemistries stay relevant in aerospace and rail, yet flat volumes reflect lithium-ion’s broadened temperature range.

Emerging sodium-ion cells promise 20-30% cost savings versus LFP by swapping abundant sodium for scarce lithium, while vanadium redox flow batteries gain traction for six-hour-plus discharge durations. Solid-state prototypes remain three-to-five-times costlier than lithium-ion, prompting most industrial buyers to monitor rather than commit. Recycling mandates accelerate lead-acid’s retreat in Europe, redirecting investment to higher-margin lithium-based lines.

By Application: Industrial Automation Drives Growth

Forklifts and motive-power systems captured 31.65% of the industrial battery market revenue in 2025 and are forecast to expand at 18.65% through 2031. Opportunity-charged lithium-ion packs eliminate midday swaps and free floor space, providing rapid payback for 24/7 warehouses.

Telecom backup upgrades accelerate after India’s mandate for four-hour autonomy, and data-center rack batteries gain popularity as space-saving alternatives to centralized UPS rooms. Grid-scale storage posts the fastest absolute gigawatt-hour growth, though profitability hinges on arbitrage spreads that grid operators can compress via demand response. Marine and rail auxiliaries remain a smaller base but show double-digit growth as maritime ports move toward zero-emission targets.

By End-User Industry: Utilities Lead, Manufacturing Accelerates

Power and utilities accounted for 37.88% of 2025 spend and will grow at 18.21% through 2031, supported by record renewable additions and supportive tax credits. Manufacturing and warehousing trail in share yet mirror the growth trajectory as e-commerce behemoths retrofit fleets.

Oil and gas operators apply batteries to offshore platforms and remote wells to trim diesel reliance. Telecom carriers face rising power loads from 5G upgrades, favoring energy-dense lithium-ion banks. Transportation depots for buses and port cranes edge toward parity, helped by stricter carbon rules at major gateways.

Geography Analysis

Asia-Pacific dominated the industrial battery market with 49.92% revenue in 2025 and will grow at 19.53% through 2031. China’s 85% share of global cell output and mandatory 10-20% storage pairing for new renewables spur demand, while India’s USD 2.4 billion Production-Linked Incentive lures 50 GWh of domestic capacity. South Korea’s LG Energy Solution and Samsung SDI exceed 520 GWh of combined capacity, exporting to North America and Europe. Japan remains focused on high-nickel cells for automotive and niche industrial uses.

North America benefits from a USD 35 per kWh production credit and 30+ gigafactory announcements since 2022, targeting 1 TWh of capacity by 2030. Canada’s mineral endowment positions it as a Western alternative, although refining lags extraction. Mexico attracts assembly investments but faces permitting bottlenecks.

Europe’s Critical Raw Materials Act seeks 10% domestic sourcing and 40% local processing by 2030, supporting Northvolt, ACC, and CATL’s European lines. Germany, France, and the U.K. lead in frequency-regulation storage, though expanded interconnectors may pressure margins after 2028. Nordic hydropower attracts energy-intensive cathode synthesis, yet yield challenges slow ramp-ups.

South America and the Middle East-Africa remain nascent, with Brazil and the U.A.E. piloting utility-scale projects, but limited manufacturing keeps scale small relative to Asia-Pacific and North America.

Competitive Landscape

The industrial battery market features moderate concentration: the top five cell makers, CATL, BYD, LG Energy Solution, Panasonic Energy, and Samsung SDI, control roughly 70% of global capacity. Chinese leaders wield 20-30% cost advantages through vertical integration from raw materials to packs, pressuring Western peers to localize or cede margin. Patent filings in solid-state electrolytes and silicon anodes rose 40% between 2023 and 2025, yet commercial timelines remain opaque, so buyers prioritize incremental lithium-ion gains.

Second-life programs emerge as a white-space: retired EV packs retain 70-80% capacity and sell into stationary projects at deep discounts, though warranty standards remain thin. Sodium-ion and flow-battery challengers court long-duration niches, but entrenched lithium-ion scale raises entry barriers. Regulation plays a pivotal role: IEC 62619 harmonizes safety certification across applications, yet diverging regional fire-safety protocols fragment product rollouts. Players with multi-chemistry portfolios and localized supply chains stand best positioned to navigate cost, policy, and technology shifts.

Industrial Battery Industry Leaders

EnerSys

East Penn Manufacturing

GS Yuasa Corporation

Exide Industries

Saft Groupe SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Prevalon commissioned an 80 MW battery storage system for Idaho Power, underscoring utility confidence in large-scale batteries for grid stabilization.

- June 2025: Akaysha Energy initiated commissioning of a 300 MWh project in Queensland, growing Australia’s storage footprint.

- April 2025: Strata Clean Energy broke ground on a 150 MW/600 MWh facility in Arizona, reflecting steady US utility-scale momentum.

- March 2025: Tesla announced a USD 200 million battery megafactory in Brookshire, Texas, to meet surging stationary demand.

Global Industrial Battery Market Report Scope

Industrial batteries are sources of electrical energy that are generated from electrochemical reactions. Industrial batteries are an important part of uninterrupted power supply (UPS) systems, which are widely used for stationary or mobile applications.

The industrial battery market is segmented by technology, application, end-user, and geography. By technology, the market is segmented into lithium-ion battery, lead-acid battery, and other technologies (nickel cadmium, nickel metal hydride, zinc-carbon, etc.). By application, the market is segmented into forklift, telecom, UPS, and other applications. By end-user, the market is segmented into the power sector, oil & gas sector, manufacturing sector, telecom, and other end-users. The report also covers the market size and forecasts for the industrial battery market across major regions, such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

For each segment, market sizing and forecasts have been done based on revenue (USD).

By Technology

| Lithium-ion |

| Lead-acid |

| Nickel-based |

| Others (incl. Flow Battery, Sodium-ion) |

By Application

| Forklift and Motive Power |

| Telecom Backup |

| UPS/Data Centres |

| Grid-Scale ESS |

| Others (incl Automated Guided Vehicles, Rail and Marine) |

By End-User Industry

| Power and Utilities |

| Oil and Gas |

| Manufacturing and Warehousing |

| Telecom |

| Others (incl Transportation and Logistics) |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Lithium-ion | |

| Lead-acid | ||

| Nickel-based | ||

| Others (incl. Flow Battery, Sodium-ion) | ||

| By Application | Forklift and Motive Power | |

| Telecom Backup | ||

| UPS/Data Centres | ||

| Grid-Scale ESS | ||

| Others (incl Automated Guided Vehicles, Rail and Marine) | ||

| By End-User Industry | Power and Utilities | |

| Oil and Gas | ||

| Manufacturing and Warehousing | ||

| Telecom | ||

| Others (incl Transportation and Logistics) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the growth outlook for the industrial battery market through 2031?

The industrial battery market is projected to grow from USD 41.93 billion in 2026 to USD 93.71 billion by 2031, registering a 17.45% CAGR.

Which technology leads current sales?

Lithium-ion technology held 51.26% revenue in 2025 and is forecast to expand at 18.56% through 2031.

Why are forklifts switching to lithium-ion?

Opportunity charging halves downtime and removes the need for dedicated battery-swap rooms, delivering quick payback for 24/7 warehouses.

How significant is Asia-Pacific in demand?

Asia-Pacific generated 49.92% of 2025 revenue and is expected to grow at 19.53% through 2031, led by China and India.

What challenges could slow adoption?

Critical-mineral price swings and higher fire-risk insurance premiums can raise capex and delay commissioning.

Which companies dominate supply?

CATL, BYD, LG Energy Solution, Panasonic Energy, and Samsung SDI account for about 70% of global industrial battery capacity.

Page last updated on: