Micro Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

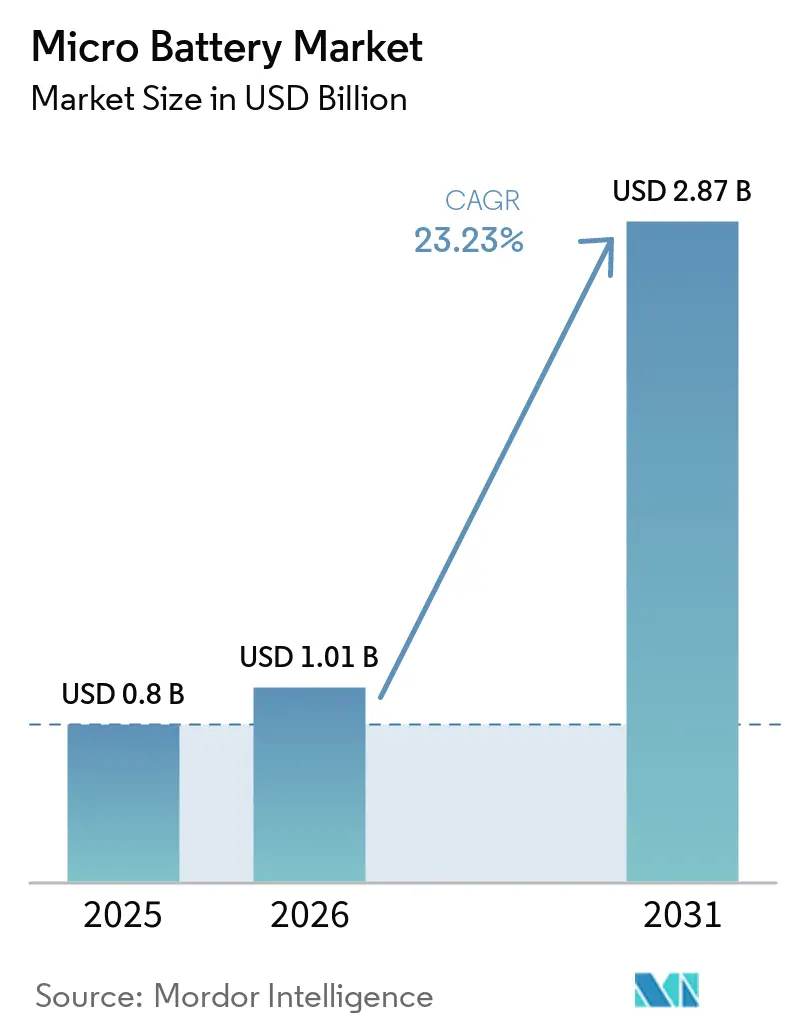

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 23.23% CAGR |

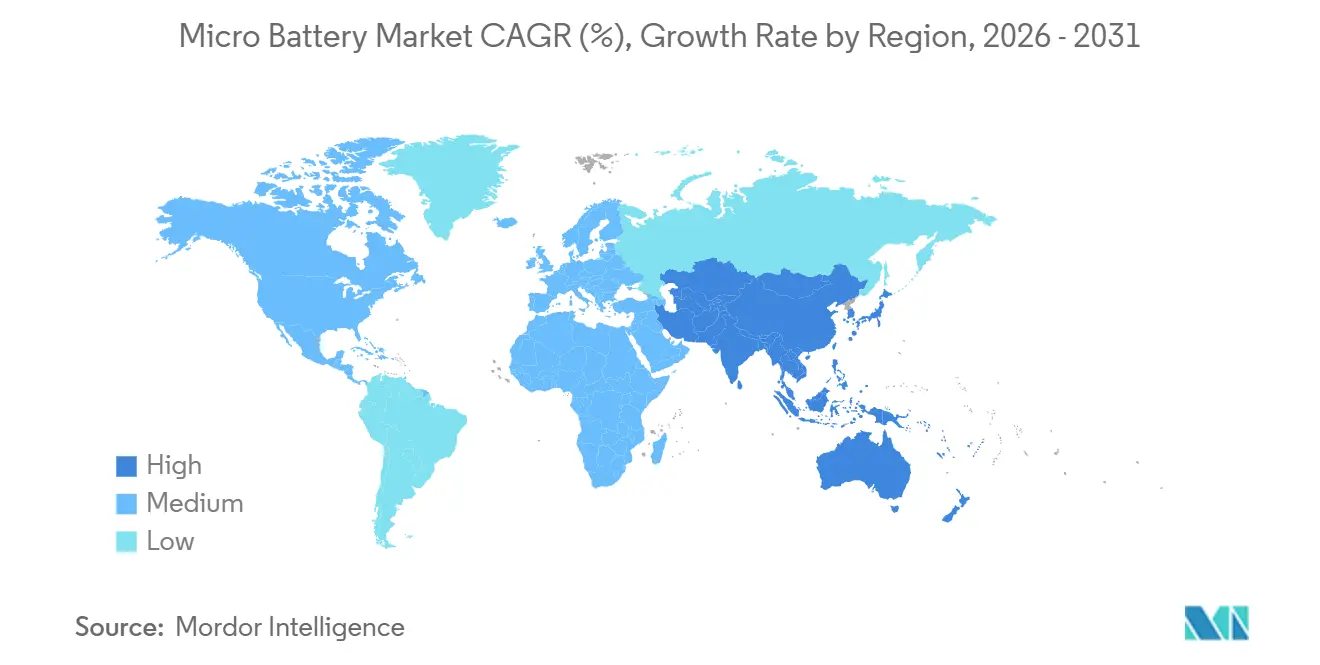

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro Battery Market Analysis by Mordor Intelligence

The Micro Battery Market size is expected to increase from USD 0.8 billion in 2025 to USD 1.01 billion in 2026 and reach USD 2.87 billion by 2031, growing at a CAGR of 23.23% over 2026-2031. Demand is accelerating as designers migrate from prototyping to volume production in wearables, implantable medical devices, and ultra-low-power IoT nodes. Solid-state architectures are displacing coin cells where thin profiles and intrinsic safety are mandatory, while defense procurement rules that exclude Chinese supply chains are redirecting capital to Korean and European thin-film facilities. OEMs are locking in qualified micro-battery suppliers earlier than normal because sovereign-AI edge inference and new traceability mandates compress design cycles. Ongoing patent proliferation, a widening cost gap between solid-state and lithium-ion, and the absence of harmonized test standards together shape a fragmented competitive field where scale and compliance infrastructure determine success.

Key Report Takeaways

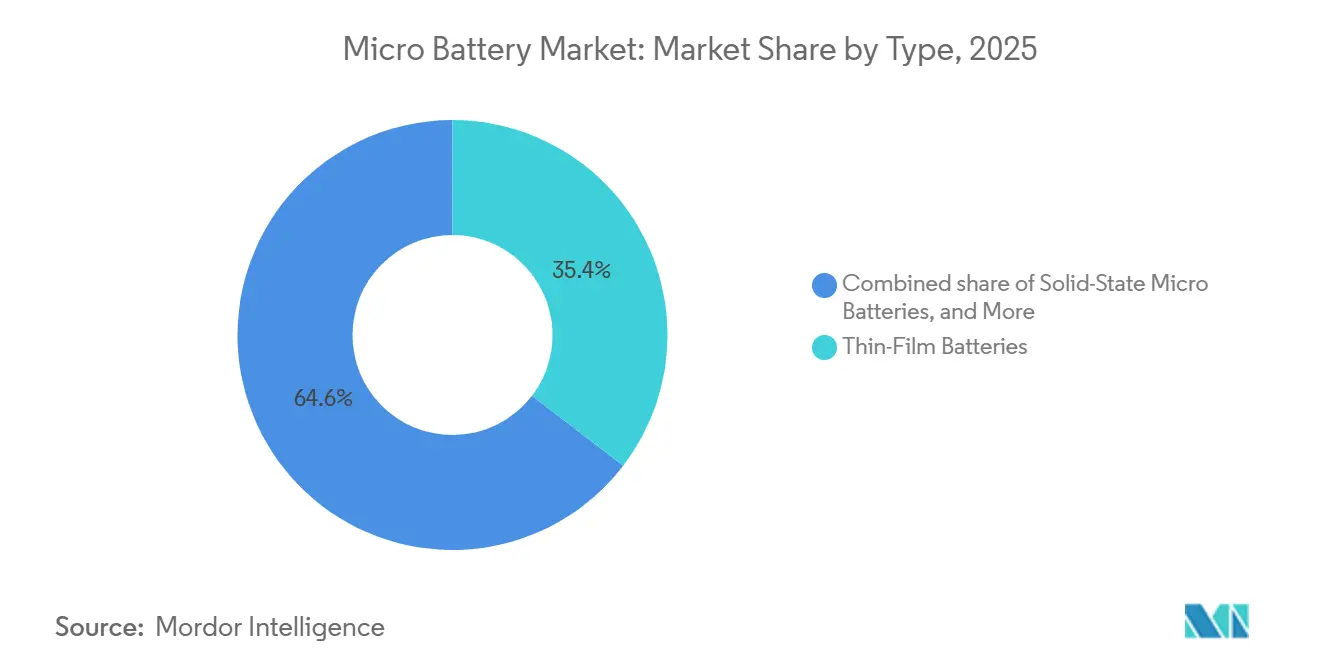

- By type, thin-film batteries led with 35.4% revenue share in 2025; solid-state devices are projected to expand at a 26.2% CAGR through 2031.

- By application, medical devices led with a 32.6% revenue share in 2025, while wearable electronics will advance at a 26.9% CAGR to 2031.

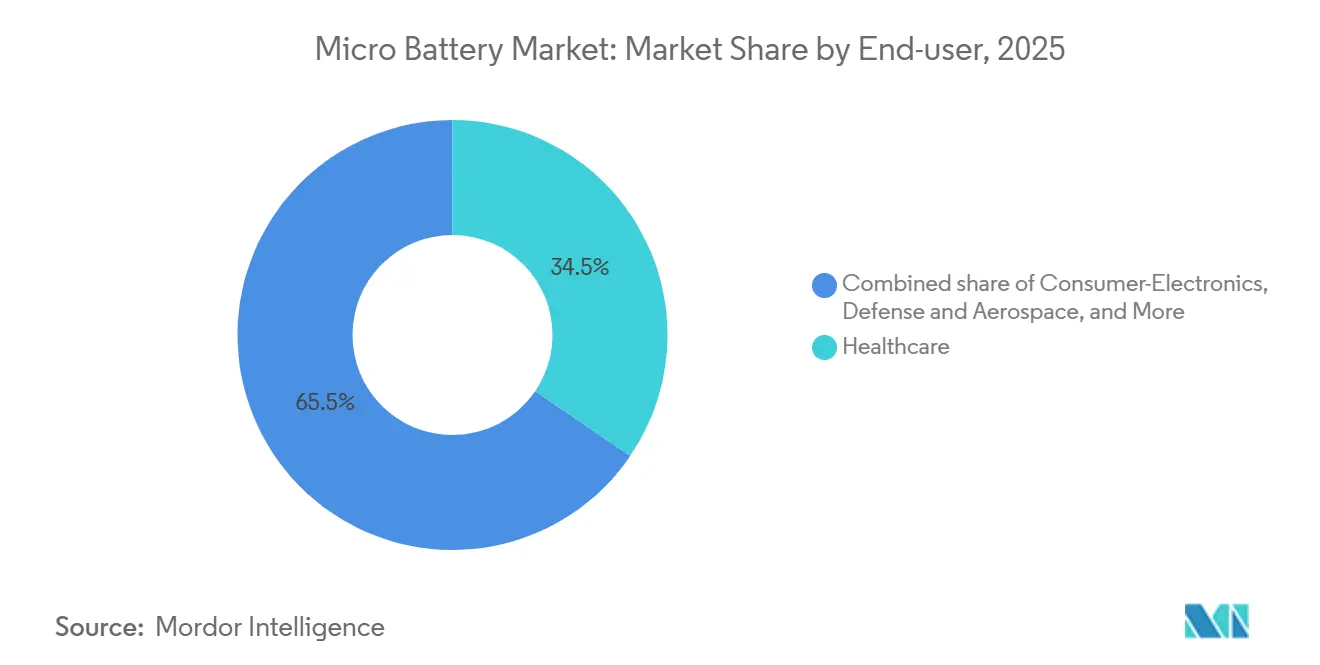

- By end user, healthcare commanded 34.5% of the micro battery market size in 2025, whereas consumer electronics is forecast to post a 27.5% CAGR between 2026-2031.

- By geography, Asia-Pacific captured 41.8% revenue share in 2025 and is positioned to grow at a 24.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Micro Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of wearable devices | +4.8% | Global, led by APAC and North America | Medium term (2-4 years) |

| Growth in implantable medical electronics | +3.9% | North America & EU, spillover to APAC | Long term (≥ 4 years) |

| Expansion of IoT edge-sensor networks | +5.2% | Global, APAC core with MEA adoption | Medium term (2-4 years) |

| Rising demand for compact hearable power sources | +4.1% | Global, APAC and North America early adopters | Short term (≤ 2 years) |

| Self-powered printed-electronics ecosystem emerging | +2.7% | North America & EU, pilot deployments in APAC | Long term (≥ 4 years) |

| Defense adoption of smart-dust sensor nodes | +2.6% | North America, EU, spillover to allied nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Wearable Devices

Shipments of smartwatches, rings, and hearables continue to lift micro battery market demand. Open-ear earbuds moved runtime from 5-6 hours in 2025 to 8-12 hours in 2026 after integrating higher-density cells and adaptive power management. Ensurge’s 650-750 Wh/L solid-state design, released in 2024, targets these hearables because it removes flammable liquid electrolytes, a critical safety benefit inside the ear canal. Flexible paper batteries worth USD 2.5 billion in 2025 are embedding power directly into textile substrates, eliminating rigid housings that add weight and bulk. Global compliance with IEC 62368-1 for audio devices is steering brands toward certified micro-battery suppliers that can mitigate product-liability exposure.

Growth in Implantable Medical Electronics

Miniaturized pacemakers, neurostimulators, and drug-delivery pumps rely on micro batteries that extend replacement intervals and lower surgical risk. The FDA’s February 2026 Quality Management System Regulation forces battery vendors to implement granular cell-level genealogy, pushing smaller firms to outsource compliance or exit the market. Ilika shipped its first revenue order of Stereax M300 solid-state cells to Cirtec Medical in January 2026, while 21 additional device makers remain in clinical validation. Research prototypes harvesting ventricular motion hint at future battery-free implants, yet long-term biocompatibility studies are still underway. Heightened regulatory scrutiny since a 2025 warning letter on battery failures is amplifying demand for suppliers with ISO 13485 accreditation [1]U.S. Food and Drug Administration, “Quality Management System Regulation Final Rule,” fda.gov.

Expansion of IoT Edge-Sensor Networks

Industrial operators are adopting maintenance-free wireless nodes powered by micro batteries with 5-10-year lifespans. At Atlantic Copper’s refinery, a battery-less LoRaWAN solution achieved 98% link reliability and provided 10.5 hours of predictive-failure lead time, reducing manual inspection costs [2]Atlantic Copper, “Predictive Maintenance with Battery-less LoRaWAN Sensors,” atlantic-copper.com. Li-SOCl2 cells rated for -55°C to +85°C enable Arctic pipeline and desert solar deployments, while NFC energy harvesting is displacing batteries in RFID tags where short read ranges are acceptable. Forthcoming EU battery passport rules embed traceability chips that themselves consume micro-battery capacity, extending the addressable micro-battery market beyond primary power.

Rising Demand for Compact Hearable Power Sources

Active noise cancellation and spatial audio raise energy budgets inside earbuds. Premium brands now specify solid-state cells delivering up to 750 Wh/L volumetric density, an advance that fits more energy into irregular cavities around speaker drivers. Pouch-cell formats free 20-30% of internal volume compared with cylindrical cells, letting designers add sensors without enlarging the enclosure. Panasonic’s CR2032 coin cell still anchors mass-market models because of its 8-year shelf life, but segment-leading runtime targets are shifting new designs toward solid-state options. A regulatory gap persists because IEC 60086-4 covers primary lithium batteries but not solid-state chemistries, prompting voluntary third-party assessments by top suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manufacturing cost of solid-state micro batteries | -2.8% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Limited energy density vs. conventional coin cells | -1.9% | Global, constraining adoption in cost-sensitive markets | Medium term (2-4 years) |

| Supply-chain constraints for thin-film deposition materials | -1.6% | Global, concentrated in APAC supply chains | Short term (≤ 2 years) |

| Lack of standardized micro-battery test protocols | -1.3% | Global, fragmenting qualification timelines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Manufacturing Cost of Solid-State Micro Batteries

Vacuum deposition, specialty precursors, and low-throughput batch processing leave solid-state cells at a 3-5 × cost premium over lithium-ion. ProLogium’s Dunkirk site aims for 4 GWh by 2029 and a sub-USD 150 kWh cost target, but the capital burden is significant. Dry-electrode lines that cut energy use 47% are promising yet unproven at the micro-battery scale. Elevated Materials shipped over 100 km of lithium metal film in 2025 and must triple output in 2026, underscoring thin-film supply-chain bottlenecks [3]Elevated Materials, “Ultra-thin Lithium Metal Film Production Milestone,” elevatedmaterials.com. Until costs fall, adoption concentrates in medical, defense, and premium wearables.

Limited Energy Density vs. Conventional Coin Cells

Gravimetric energy density of many micro batteries trails CR-series coin cells, limiting use where weight budgets are flexible. Renata’s CR2032 delivers up to 260 mAh, while first-wave solid-state cells still lack comparable Wh/kg. While zinc microbatteries, as highlighted in a February 2026 Nature Communications paper, achieved a record areal energy density, ongoing cycle-life degradation remains a significant barrier to their commercial viability and large-scale adoption. [4]Nature Communications, “High-Energy Density Zinc Micro-Battery via Dual-Reaction Strategy,” nature.com. The gap forces OEMs to trade shorter lifespans or accept bigger housings, dampening the addressable micro battery market across entry-level consumer electronics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Solid-State Architectures Displace Legacy Chemistries

Thin-film batteries held a 35.4% micro battery market share in 2025, anchored in medical implants and smart cards that value long qualification histories. Solid-state variants will grow at a 26.2% CAGR, powered by ProLogium’s 860 Wh/L platform and Ilika’s commercial ramp. These chemistries satisfy designer demands for sub-millimeter profiles and eliminate flammable liquid electrolytes, compelling in regulated healthcare and defense devices. Printed and flexible batteries captured disposable sensors and smart packaging, where ultralow cost and form flexibility matter more than maximum capacity. Button-cell formats remain essential in automotive key fobs and watches because incumbent production lines deliver proven reliability at cents-per-unit prices.

Manufacturing footprints reflect divergent volume and margin profiles. ProLogium’s Taoyuan plant shipped over 600,000 cells in 2025, demonstrating roll-to-roll thin-film scalability, while Zinergy and Flint each added thousands of square meters of paper-battery floor space for single-use applications. Hybrid chemistries coupling micro batteries with energy harvesters are gaining research funding, positioning the micro battery market for multipower architectures that extend deployment lifetimes without enlarging form factors.

By Application: Medical Devices Anchor Revenue, Wearables Drive Growth

Medical devices contributed 32.6% of revenue in 2025 as pacemakers, neurostimulators, and glucose monitors locked in high-margin micro-battery volumes under stringent approval processes. The micro battery market size for wearables is set to expand more rapidly, advancing at a 26.9% CAGR through 2031 as hearables, smart rings, and fitness bands penetrate middle-income economies. The micro battery market share tied to smart cards and RFID tags is climbing because EU battery-passport rules mandate tamper-proof power for embedded authentication chips.

Industrial IoT sensors rely on Li-SOCl2 chemistry for decade-long lifetimes in extremes of -55°C to +85°C, appealing to pipeline, mining, and solar operators. Battery-less LoRaWAN nodes showed high predictive-maintenance accuracy, but not all duty cycles can exploit harvested energy, preserving demand for micro batteries where continuous sensing is critical. In cost-sensitive consumer-electronics accessories, alkaline cells hold sway, yet form-factor miniaturization is nudging premium models toward solid-state options.

By End User: Healthcare Leads, Consumer Electronics Accelerates

Healthcare absorbed 34.5% of demand in 2025 because of implantable applications that pay for safety and reliability. Compliance costs rose after the FDA’s February 2026 rule change, accelerating consolidation among certified suppliers. Consumer electronics are poised for 27.5% CAGR expansion through 2031 as disposable income in emerging markets fuels the uptake of hearables and wearables that embed micro batteries rather than bulky hybrid assemblies.

Industrial automation is adopting multi-year power sources to avoid maintenance visits in hazardous zones, leveraging the micro battery market size advantage of Li-SOCl2 and solid-state chemistries that survive harsh temperatures. Defense and aerospace users, reacting to Section 842 of the FY2026 NDAA, pivot toward non-Chinese suppliers such as NEO Battery Materials, which broke ground on a 500 MWh line designed for drone batteries in March 2026. Automotive end users continue to specify CR-series coin cells for key fobs, yet explore solid-state inserts in extended-warranty vehicles.

Geography Analysis

Asia-Pacific held 41.8% revenue share in 2025, supported by China’s supremacy in battery manufacturing and Japan’s USD 660 million subsidy for solid-state R&D. CATL’s scale in precursor procurement lowers cost structures throughout the regional supply chain. Korean producers lost share to vertically integrated Chinese rivals, yet are reinvesting in all-solid-state lines to reclaim margin. ProLogium’s 4 GWh Dunkirk project, scheduled for 2029, offers European OEMs a localized supply alternative that sidesteps geopolitical risk.

North America is reshaping supply networks under defense regulations that block Chinese content. The U.S. Army’s standardized tactical universal battery (STUB) sizes force domestic pre-qualification, narrowing the vendor pool to compliant manufacturers. NEO Battery Materials’ South Korean site serves U.S. drone programs seeking Section 4872 conformity.

Europe is channeling EU Defence Fund grants toward dual-use micro batteries that power both civilian wearables and soldier systems. HARVEST, funded in 2026-2027, exemplifies projects aligning with NATO interoperability needs while meeting EU battery regulation traceability rules. South America and MEA remain import-dependent, and currency volatility plus limited local manufacturing capacity restrain near-term uptake.

Mordor Intelligence provides coverage of the micro battery market across other key regional markets, including South America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The Micro Battery is moderately fragmented. Legacy coin-cell leaders such as Panasonic and VARTA protect high-volume, low-margin niches, whereas venture-funded solid-state entrants like Ilika and ProLogium compete in high-specification medical and defense programs. Patent filings for solid-state technologies quadrupled between 2017 and 2025, with LG Energy Solution alone holding 77 issued patents, pointing to an intensifying IP battleground.

Manufacturing strategies diverge. High-volume printed-battery lines harness roll-to-roll printing to serve disposable electronics, whereas solid-state producers deploy clean-room deposition to secure yields suited to implantables. Ilika’s ISO 9001 and ISO 14001 certifications signal the compliance infrastructure necessary for medical devices. Holyvolt’s 2025 purchase of Wildcat Discovery compresses materials-discovery cycles, blending screen-printed electrodes with AI-driven formulation.

Technology remains the strongest lever for share gains. ProLogium’s active safety mechanism crystallizes reactive materials during fault events, suppressing thermal runaway. Lyten’s February 2026 purchase of Northvolt Ett gives it 16 GWh of Swedish capacity and Europe’s largest R&D hub, expediting lithium-sulfur scale-up that could leapfrog energy-density limitations. Defense standards such as MIL-STD-3078 funnel demand toward suppliers able to certify eight standardized sizes at 125 Wh/kg, excluding firms lacking clean provenance records.

Micro Battery Industry Leaders

Murata Manufacturing Co., Ltd.

Maxell Holdings Ltd.

Panasonic Corporation

TDK Corporation

VARTA AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: At CES 2026, ProLogium unveiled its groundbreaking "Superfluidized All-Inorganic Solid-State Lithium Ceramic Battery" technology. This innovation melds an all-inorganic solid-state electrolyte with a ceramic separator and a silicon anode. The goal? Achieving heightened energy density, enhanced safety, and further miniaturization for compact electronics and next-gen devices. Given the surging demand for ultra-small, high-performance power sources in wearables, IoT sensors, and medical devices, this advancement holds significant weight in the micro battery sector.

- March 2025: VARTA AG executed a capital restructuring, delisted in Frankfurt, and reaffirmed its microbattery focus.

- February 2025: Renata launched the CP042350 lithium thin-film battery with 28 mAh capacity and 0.42 mm thickness.

- January 2025: Samsung SDI commenced mass production of 4695 cylindrical cells incorporating a tab-less design for micro-mobility.

Global Micro Battery Market Report Scope

A micro battery is a small energy storage device designed to power compact electronic systems, including wearables, medical implants, sensors, and IoT devices. Utilizing advanced chemistries such as lithium-ion or solid-state, these batteries deliver reliable performance in limited spaces. Micro batteries play a crucial role in modern miniaturized electronics by providing efficient and long-lasting power within extremely small form factors.

The micro battery market is segmented by type, application, end-user, and geography. By type, the market is segmented into thin-film, solid-state, printed/flexible, button-cell, and others. By application, the market is segmented into medical devices, wearables, smart cards/RFID, sensors, accessories, and others. By end-user, the market is segmented into healthcare, consumer electronics, industrial, automotive, defense, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa (MEA). The report also covers market sizes and forecasts for the global micro battery market across major countries within these regions. For each segment, the market sizing and forecasts have been conducted on the basis of value (USD).

| Thin-Film Batteries |

| Solid-State Micro Batteries |

| Printed/Flexible Batteries |

| Button-Cell Micro Batteries |

| Others |

| Medical Devices |

| Wearable Electronics |

| Smart Cards and RFID |

| Wireless Sensor Nodes |

| Consumer-Electronics Accessories |

| Others |

| Healthcare |

| Consumer-Electronics |

| Industrial and Automation |

| Automotive and Mobility |

| Defense and Aerospace |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Thin-Film Batteries | |

| Solid-State Micro Batteries | ||

| Printed/Flexible Batteries | ||

| Button-Cell Micro Batteries | ||

| Others | ||

| By Application | Medical Devices | |

| Wearable Electronics | ||

| Smart Cards and RFID | ||

| Wireless Sensor Nodes | ||

| Consumer-Electronics Accessories | ||

| Others | ||

| By End-user | Healthcare | |

| Consumer-Electronics | ||

| Industrial and Automation | ||

| Automotive and Mobility | ||

| Defense and Aerospace | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of micro battery market?

The micro battery market stands at USD 1.01 billion in 2026 and is set to reach USD 2.87 billion by 2031, reflecting a 23.23% CAGR from 2026-2031.

Which segment will add volume fastest through 2031?

Solid-state micro batteries are expected to expand at a 26.2% CAGR, the quickest among all chemistry types.

How large could Asia-Pacific revenues become by 2031?

Asia-Pacific revenues are forecast to keep a 24.7% CAGR, maintaining the region’s lead with more than 40% share.

Why are defense buyers reshaping supply chains?

Section 842 of the FY2026 NDAA blocks batteries sourced from China, so U.S. programs now pre-qualify vendors with clean provenance and MIL-STD-3078 certification.

What keeps solid-state cells from dominating all applications?

A 3-5 × cost premium and lower Wh/kg versus top lithium-ion coin cells currently confine solid-state adoption to use cases where safety or extreme thinness outweigh price.

Page last updated on: