Golf Cart Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

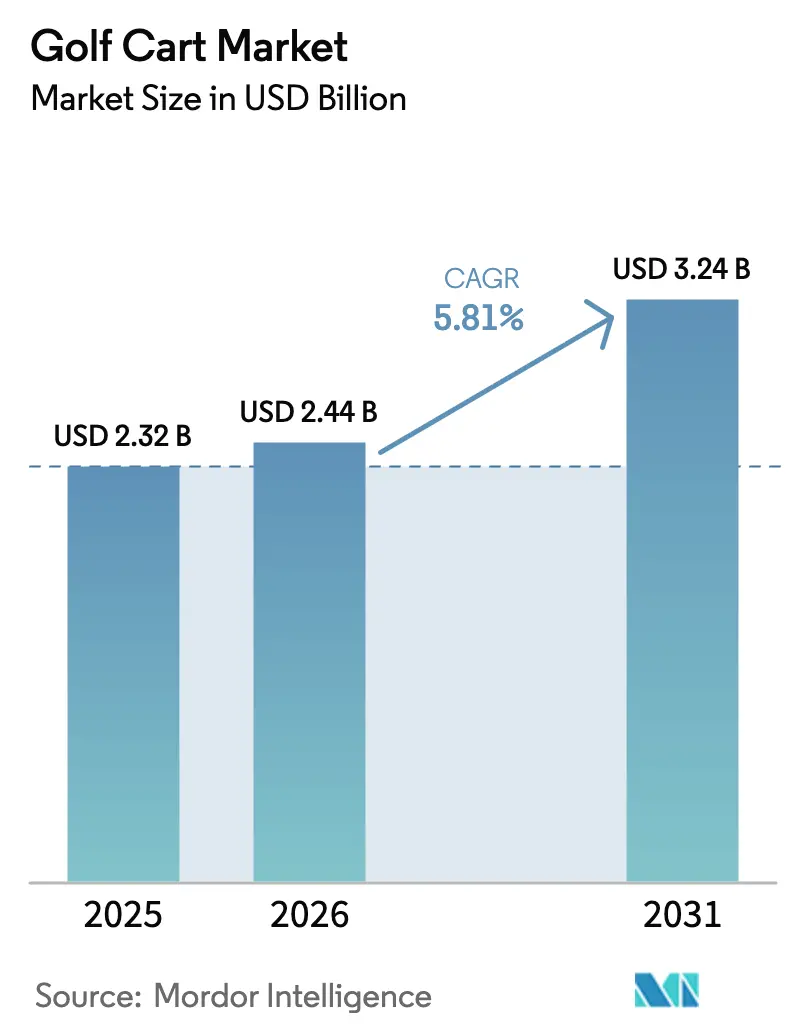

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.24 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Golf Cart Market Analysis by Mordor Intelligence

The golf cart market size was valued at USD 2.32 billion in 2025 and estimated to grow from USD 2.44 billion in 2026 to reach USD 3.24 billion by 2031, at a CAGR of 5.81% during the forecast period (2026-2031). Robust growth stems from expanding resort micro-mobility schemes, electrification mandates at golf courses, and the steady shift toward family-oriented four-seater formats. Electric propulsion holds the lion’s share today, but solar-hybrid carts are scaling quickly where grid access is scarce. Original equipment manufacturer investments in lithium iron phosphate (LFP) batteries, bundled financing, and online build-to-order portals are reshaping sales strategies, while regulatory attention on safety standards and recalls drives product redesign. Competitive pressure remains moderate as Western incumbents defend pricing power against lower-cost Chinese entrants through premium features and direct-to-consumer platforms.

Key Report Takeaways

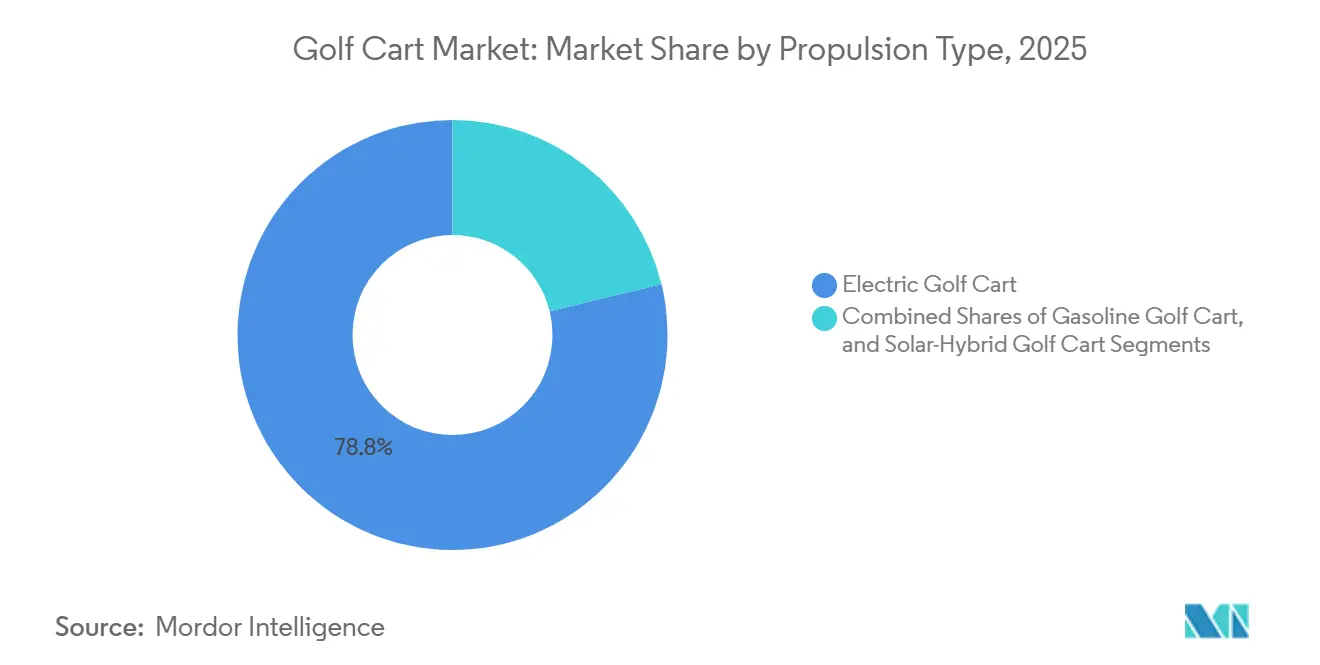

- By propulsion, electric carts led with 78.81% revenue share in 2025, while solar-hybrid variants are advancing at a 5.83% CAGR through 2031.

- By seating capacity, two-seater models accounted for 47.63% of the golf cart market share in 2025, whereas four-seaters are forecast to grow at a 5.88% CAGR.

- By vehicle format, open-top designs led with 77.71% of the golf cart market share in 2025, while enclosed weather-proof carts are forecast to grow at a 5.93% CAGR through 2031.

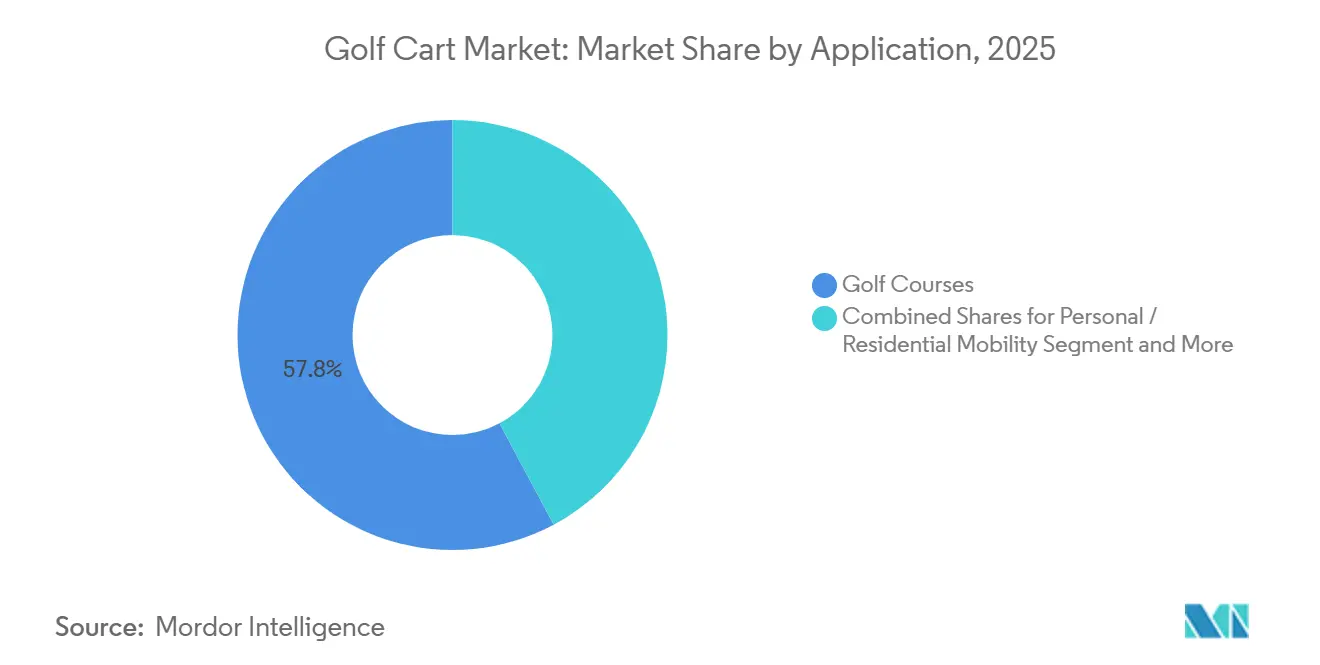

- By application, golf courses generated 57.78% of demand in 2025, and commercial services are expanding at a 5.85% CAGR to 2031.

- By sales channel, offline dealer and distributor networks held 73.46% of the golf cart market share in 2025, whereas online direct-to-consumer platforms are projected to advance at a 5.91% CAGR to 2031.

- By geography, North America captured 38.71% of 2025 revenue, and Asia Pacific is slated to climb at a 5.87% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Golf Cart Market*

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| United States Retirement Communities | +1.2% | North America, concentrated in Florida, Arizona, South Carolina | Medium term (2-4 years) |

| European Golf Courses and Country Clubs Mandated to Electrify Operations | +0.9% | EU-27, United Kingdom, Norway, Switzerland | Short term (≤ 2 years) |

| Southeast Asian Islands Integrating Micro-mobility Programs | +0.8% | Asia Pacific core (Thailand, Indonesia, Malaysia), spill-over to Vietnam, Philippines | Medium term (2-4 years) |

| Planned Golf Townships Emerging as Part of Mega-projects | +0.6% | Saudi Arabia (NEOM, Qiddiya, Diriyah), United Arab Emirates (Red Sea islands) | Long term (≥ 4 years) |

| OEM Bundled-financing for Community Transport Fleets | +0.5% | India, urban and peri-urban townships, gated communities | Medium term (2-4 years) |

| Caribbean Resorts with Low Grid Access Piloting Solar-hybrid Carts | +0.3% | Eastern Caribbean islands, Barbados, Jamaica, Dominican Republic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

United States Retirement Communities Rapidly Adopting New Trends

In Florida, Arizona, and South Carolina, retirement communities have made carts a staple mode of transport. The Villages, a prominent player, operates a substantial number of units and boasts significant annual growth. In recent years, Florida dealers have experienced a considerable increase in cart sales. This growth is largely driven by younger retirees who are customizing their carts with features like lifted suspensions, LED lighting, and Bluetooth audio, ensuring they're street-legal. In Dunedin and Panama City, city ordinances have expanded low-speed vehicle zones, linking homes directly to retail areas and healthcare facilities. As a result, there's an increasing demand for four-seater carts, reflecting the needs of multigenerational households. Recently, the National Highway Traffic Safety Administration introduced updated safety standards, requiring the integration of seat belts, windshields, and turn signals in carts over the coming years, especially for those on public roads [1]“FMVSS 305a Final Rule,” National Highway Traffic Safety Administration, nhtsa.gov.

Planned Golf Townships Emerging in GCC Mega-Projects

Saudi Arabia's NEOM's Gidori and Qiddiya, along with the United Arab Emirates' Red Sea courses, are introducing enclosed, air-conditioned carts with varying seating capacities, designed to combat the sweltering desert heat. Qiddiya, aiming to attract a significant number of annual visitors in the coming years, is in dire need of high-capacity VIP fleets. These ambitious projects are fostering partnerships with suppliers, focusing on thermally managed batteries and solar-hybrid roofs, significantly reducing dependence on traditional generators [2]“Gidori Golf Development Brief,” NEOM Company, neom.com .

OEM Bundled Financing for Community Fleets in India

In a move mirroring India's expansive electric three-wheeler initiatives, townships in proximity to major metropolitan areas such as Delhi, Bengaluru, and Pune are trialing low-interest loans. These loans are designed to provide a comprehensive package that includes carts, chargers, and service contracts. The initial positive response indicates significant potential for sales growth, particularly as gated communities increasingly adopt zero-emission shuttles, expanding their use beyond traditional applications like golf courses.

Caribbean Resorts Piloting Solar-Hybrid Carts

In a recent workshop held in Barbados, a notable number of used electric vehicle batteries were successfully transformed into cart packs. This initiative not only extends the batteries' lifespan but also diminishes the region's reliance on imports. Buoyed by this success, resorts in Jamaica and the Dominican Republic are now eyeing the adoption of solar-hybrid fleets. These solar-hybrid carts are expected to reduce operational costs for resorts by leveraging renewable energy sources, aligning with the global push for sustainability. Additionally, the adoption of such fleets could enhance the eco-friendly image of these resorts, attracting environmentally conscious tourists. This shift is anticipated to bolster the growth of the golf cart market in the Caribbean.

Restraints Impact Analysis of Golf Cart Market*

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium-ion Pack Cost Volatility | -0.7% | Global, acute in import-dependent markets (Latin America, Africa, Southeast Asia) | Short term (≤ 2 years) |

| Declining Golf Membership | -0.5% | United Kingdom, Germany, France, Benelux | Medium term (2-4 years) |

| Municipal Fire-code Tightening for Cart Storage | -0.3% | North America, concentrated in California, Florida, Ontario, British Columbia | Short term (≤ 2 years) |

| Sparse Charging Infrastructure | -0.2% | Eastern Caribbean, smaller island nations with limited grid capacity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lithium-Ion Pack Cost Volatility

In recent years, battery pack prices have experienced a significant decline, reaching their lowest levels in over half a decade. Despite this reduction, the majority of cell production continues to be heavily concentrated in China, accounting for a substantial share of the global output. Import-dependent assemblers in regions such as Latin America and Africa face challenges due to disruptions in the supply chain, which have led to increased costs for imported components. According to the International Energy Agency, further cost reductions are anticipated in the coming years as advancements in lithium iron phosphate (LFP) and sodium-ion battery chemistries gain momentum and achieve greater scalability [3]“Trends in Battery Costs and Supply Chains,” International Energy Agency, iea.org . Yamaha's upcoming electric cart model, scheduled for release in the middle of the decade, features an innovative in-house battery pack utilizing LFP chemistry. This new design is expected to deliver significantly improved energy efficiency compared to earlier models that relied on lead-acid batteries, providing a more stable and reliable solution amidst market volatility.

Declining Golf Membership in Western Europe

In mid-2024, Custodian Golf issued a significant warning, highlighting that a considerable proportion of UK clubs are at risk of closure due to declining participation rates and increasing operational expenses. These challenges have negatively impacted the demand for golf carts. In the following year, Dalmuir, a municipal course in Scotland, ceased operations as local councils cited financial constraints. Furthermore, several golf clubs in England decided to sell their land for housing developments to address financial pressures. Clubs that continue to operate are now prioritizing cost-saving measures, such as extending the usage period of their golf carts instead of replacing their fleets on an annual basis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Golf Cart Market Segment Analysis

By Propulsion Type:

Solar-Hybrid Gains Traction Amid Grid ConstraintsElectric carts dominate with 78.81% share, anchored by mature charging infrastructure at most courses. The golf cart market size for solar-hybrid models, however, is projected to grow at a 5.83% CAGR, catalyzed by off-grid resorts seeking autonomy. Los Naranjos Golf Club cut electricity costs by 40% by adding rooftop panels, validating a five-year payback. LFP batteries displace lead-acid, improving energy density and cycle life, while Yamaha’s hydrogen fuel-cell concept hints at future diversification. Regulations such as EU 2023/1804 accelerate the pivot away from gasoline, narrowing long-term prospects for combustion carts.

Chinese suppliers offer CE-marked solar roofs bundled with 150 W trickle chargers priced under USD 400, making hybrids attractive for Southeast Asian and Caribbean operators. The golf cart market continues to absorb battery-reuse packs from end-of-life EVs, smoothing supply and lowering emissions footprints.

By Seating Capacity:

Four-Seater Configurations Gain in Family and Group UseTwo-seater units still hold the largest slice with 47.63% market share in 2025, yet four-seaters advance fastest on the back of Sun-belt residential adoption. The golf cart market size for four-seater models is forecast to expand 5.88% per year through 2031. Players like E-Z-GO’s Liberty and Yamaha’s five-seat G30Es bridge space efficiency with greater passenger accommodation.

Retirement communities retrofit rear-facing seats and cargo boxes, spurring aftermarket revenue. GCC mega-projects lean toward six- and eight-seater, air-conditioned carts for VIP and group play, shaping premium demand tiers.

By Vehicle Format:

Enclosed Designs Expand in Northern ClimatesOpen-top variants monopolized 77.71% of 2025 volume, but enclosed carts are climbing at a 5.93% CAGR. This trend is particularly evident in regions with colder climates, such as Canada and the northern United States, as well as in areas of Asia that experience heavy monsoon seasons.

Recent Federal Motor Vehicle Safety Standards (FMVSS) regulations are shaping the industry by encouraging the adoption of semi-enclosed designs for road-legal carts. This regulatory shift has led to a notable increase in the demand for components such as windshields, seat belts, and lighting kits. Additionally, resorts are increasingly incorporating climate-controlled cabins into their offerings. These cabins not only provide enhanced safety during extreme weather conditions, such as intense heat or heavy rainfall, but also serve as a means to elevate the overall brand value of the resorts.

By Application:

Commercial Services Accelerate Amid Labor ShortagesAlthough golf courses accounted for 57.78% of demand, commercial services post the briskest 5.85% CAGR. Theme parks, campuses, and airports adopt autonomous or dispatch-controlled carts to shrink shuttle labor costs.

Luxury hotels increasingly adopt electric carts to adhere to quiet-zone mandates, ensuring a serene environment for guests. At the same time, industrial facilities show a growing preference for utility beds, which are well-suited for transporting light cargo efficiently. In retirement hubs across the United States, personal mobility is gaining prominence as municipalities focus on expanding low-speed vehicle lanes. These lanes are designed to seamlessly connect residential areas with essential destinations, enhancing convenience for residents.

By Sales Channel:

Online Direct-to-Consumer Gains MomentumOffline dealers maintain 73.46% share, but the online channel grows 5.91% annually. E-Z-GO’s Reserve Now platform captures configurator-savvy buyers with eight-week delivery guarantees and USD 500 deposits. Yamaha's National Golf Cart Day effectively utilizes social media platforms to engage with potential customers, seamlessly guiding them toward its online shopping options as well as its network of physical retail partners.

At the same time, Chinese exporters are increasingly relying on online storefronts, such as those provided by Alibaba, and implementing pricing strategies based on purchase volumes to appeal to international fleet managers. These approaches are further intensifying the fragmentation within the golf cart market.

Geography Analysis

North America Golf Cart Market

North America, with 38.71% revenue in 2025, remains the anchor due to entrenched retirement-community culture and extensive course networks. FMVSS 305a harmonizes safety compliance, likely raising average selling prices but also spurring replacement of older fleets. Canada’s stricter fire codes add retrofit costs, while localized production by Club Car, Yamaha, and Textron ensures quick lead times and tailored service packages.

APAC Golf Cart Market

Asia Pacific is the fastest-rising region at a 5.87% CAGR. Thailand leads ASEAN adoption, supported by local manufacturers and tourism-driven cart demand. China’s market, already USD 134.47 million in 2022, could double by 2029 as applications widen to parks and industrial campuses. Japan’s preference for five-seat caddie carts pushes OEMs to integrate electromagnetic guidance for autonomous fairway loops. India’s township fleets enter pilot stage, signaling potential scale once bundled financing solidifies.

EMEA, South America and Caribbean Golf Cart Market

Europe blends opportunity and risk. Electrification mandates guarantee replacement demand, yet United Kingdom, German, and French membership attrition reduces volume upside. Clubs in Spain and Italy offset power costs through solar roofs and battery-storage pairs, breaking even within five years. South America and the Middle East trail in absolute numbers but post the steepest percentage gains, with GCC mega-projects setting premium benchmarks for enclosed, cooled carts. Caribbean islands pioneer solar-hybrid adoption as battery-reuse labs in Barbados illustrate circular-economy gains.

Mordor Intelligence provides coverage of the golf cart market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

In the moderately concentrated market, Club Car, Yamaha Motor, and Textron Specialized Vehicles dominate global shipments and maintain robust dealer networks. By the end of the decade, Yamaha plans to merge its golf-car subsidiary with its parent company, consolidating its intellectual property for advancements in autonomous driving and battery technology. Club Car expanded its premium street-legal offerings with the acquisition of a luxury brand in recent years. Meanwhile, E-Z-GO is leveraging direct-to-consumer sales to protect its margins from the pressures of low-cost imports.

Chinese players like Suzhou Eagle, HDK Electric Vehicles, and Dongguan Excellence are significantly undercutting established brands by offering competitively priced models. These companies provide certified vehicles that meet international standards, appealing to cost-conscious buyers. Their agility on e-commerce platforms, combined with rapid development cycles, resonates strongly with budget-sensitive fleets in regions such as Southeast Asia and Latin America. Polaris GEM is making its mark in the street-legal low-speed segment, offering premium lithium-powered models. These vehicles are equipped with advanced features, including modern lighting systems, energy-efficient braking, and integrated smartphone connectivity.

Technological advancements are setting players apart: battery packs with enhanced efficiency promise significant energy savings, electromagnetic guidance enables routing without the need for depots, and cloud-connected fleet dashboards help reduce maintenance downtimes. Recent demonstrations of super-capacitor technology by Greentech suggest the potential for extremely fast charging, though the timeline for commercial availability remains unclear.

Golf Cart Industry Leaders

Yamaha Golf-Car Company

Textron Specialized Vehicles Inc.

Club Car LLC

Polaris Inc.

HDK Electric Vehicles

- *Disclaimer: Major Players sorted in no particular order

Golf Cart Market Companies Covered in this Report

- Club Car LLC

- Yamaha Golf-Car Company

- Textron Specialized Vehicles (E-Z-GO, Cushman)

- Columbia Vehicle Group (ParCar)

- HDK Electric Vehicles

- Suzhou Eagle EV Mfg. Co.

- JH Global Services (Star EV)

- Dongguan Excellence Golf & Sightseeing Car

- ICON EV

- Marshell Electric Vehicle

- Bintelli Electric Vehicles

- Xiamen Dalle Electric Car

- Polaris GEM (Polaris Inc.)

- Speedways Electric

- AgT Electric Cars

- CitEcar Electric Vehicles

- Kandi Technologies Group

- Tomberlin (Columbia)

- ELLWEE AB

Recent Industry Developments in Golf Cart Market

- March 2025: Yamaha Motor launched two five-seat golf cart models with lithium iron phosphate (LFP) batteries. These models, G30Es and G31Eps, are available with 4 kWh or 6 kWh battery capacities, offering high reliability, extended lifespan, and thermal stability.

- January 2025: ARCH EV Golf Carts published an outlook describing electric power, smart telemetry, and autonomous operation as key product themes for 2025 and beyond.

Golf Cart Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the golf cart market as all newly manufactured, self-propelled vehicles that travel at up to about 25 mph and are intended to carry two to eight passengers plus gear on golf courses or along short internal routes in resorts, airports, campuses, and gated communities.

Scope exclusion: pre-owned units, aftermarket lift-kit conversions, and neighborhood electric vehicles designed for public-road use are left out of this sizing.

Segments Covered in This Report

- By Propulsion Type

- Electric Golf Carts

- Gasoline Golf Carts

- Solar-Hybrid Golf Carts

- By Seating Capacity

- 2 Seater

- 4 Seater

- 6 Seater

- 8+ Seater

- By Vehicle Format

- Open-Top

- Enclosed / Weather-proof

- By Application

- Golf Courses

- Personal / Residential Mobility

- Commercial Services (Resorts, Theme-Parks, Campuses)

- Industrial & Airport Utility

- By Sales Channel

- Offline (Dealers & Distributors)

- Online / Direct-to-Consumer

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed course superintendents, resort fleet managers, and regional distributors in North America, Europe, and Asia. These discussions validated utilization cycles, lithium-battery adoption timelines, and price-elastic demand shifts, filling critical gaps left by desk work before we locked the assumptions.

Desk Research

We began with structured searches of open datasets such as the U.S. International Trade Commission's HS-870310 export codes, the National Golf Foundation's participation surveys, and government vehicle registration files in the EU and Japan. Association portals, including the International Light Transportation Vehicle Association and Asia Pacific Golf Confederation, helped us benchmark stock, retirements, and new-course additions. Company 10-Ks, dealer price lists, and media archives inside Dow Jones Factiva gave us average selling price (ASP) signals. Select paid portals, such as D&B Hoovers for OEM revenues and Marklines for model launches, enriched brand-level splits. The sources cited illustrate our approach; many others were tapped to cross-check figures.

Market-Sizing & Forecasting

A top-down construct begins with production and trade tallies, which are then adjusted for domestic retention, fleet life, and scrappage to yield annual sell-in volumes. Results are balanced against sampled bottom-up checks, dealer shipment roll-ups, and average ASP × units, to fine-tune totals. Key drivers modeled include new golf-course openings, resort room additions, retirement-community housing starts, lithium-battery price curves, and regional golf participation rates. We project forward with multivariate regression that links these drivers to unit demand, while ARIMA smooths cyclical swings. Where bottom-up inputs are thin (e.g. solar-hybrid pilots), variance limits from primary interviews cap extreme forecasts.

Data Validation & Update Cycle

Outputs pass a three-tier review: automated anomaly flags, peer analyst scrutiny, and senior sign-off. We refresh each model annually and trigger interim updates when OEM price lists, regulatory caps, or macro shocks move the market materially. A final pre-publication sweep assures clients receive the latest vetted view.

How Mordor Intelligence's Golf Cart Market Size Compares to Other Published Estimates

Published estimates often diverge because studies choose different vehicle definitions, pricing bases, or refresh cadences.

External dashboards place the 2024 global market anywhere between USD 2.06 billion and USD 2.60 billion, while Mordor's model shows USD 2.22 billion for 2025 (mordorintelligence.com). Grand-scale trackers at the lower bound count only golf-course fleets. Higher figures frequently fold in low-speed neighborhood vehicles and generous ASP mark-ups.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.22 B (2025) | Mordor Intelligence | - |

| USD 2.06 B (2024) | Global Consultancy A | Excludes resort, airport, and campus usage |

| USD 2.60 B (2024) | Industry Journal B | Includes street-legal neighborhood EVs and inflated ASP ladder |

The comparison shows that when consistent scope, verified inputs, and an annual refresh are applied, Mordor delivers a balanced, transparent baseline that decision-makers can track, replicate, and trust.

Key Questions Answered in the Report

How large is the golf cart market in 2026 and what annual growth is expected through 2031?

The sector is valued at USD 2.44 billion in 2026 and is projected to advance at a 5.81% CAGR, reaching USD 3.24 billion by 2031.

Which region currently generates the most golf cart revenue?

North America leads with 38.71% of 2025 revenue, supported by extensive retirement-community adoption and a dense golf-course network.

What vehicle format is gaining momentum with operators in colder or wetter climates?

Enclosed, weather-proof carts are expanding at a 5.93% CAGR as clubs and resorts in northern latitudes seek year-round operability and passenger comfort.

How quickly are online direct-to-consumer channels growing for golf cart sales?

Digital platforms, driven by initiatives such as E-Z-GO’s Reserve Now portal, are rising at a 5.91% CAGR, although traditional dealers still hold most sales today.

Which powertrain option is seeing the fastest uptake where grid access is limited?

Solar-hybrid carts, combining battery packs with rooftop panels, are scaling at a 5.83% CAGR as island resorts and off-grid courses pursue energy autonomy.

Who are the three dominant manufacturers in the sector?

Club Car, Yamaha Motor, and Textron Specialized Vehicles collectively control the largest share thanks to deep dealer networks, broad portfolios, and strong brand equity.

Page last updated on: