Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.01 Billion |

| Market Size (2031) | USD 15.93 Billion |

| Growth Rate (2026 - 2031) | 12.07% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

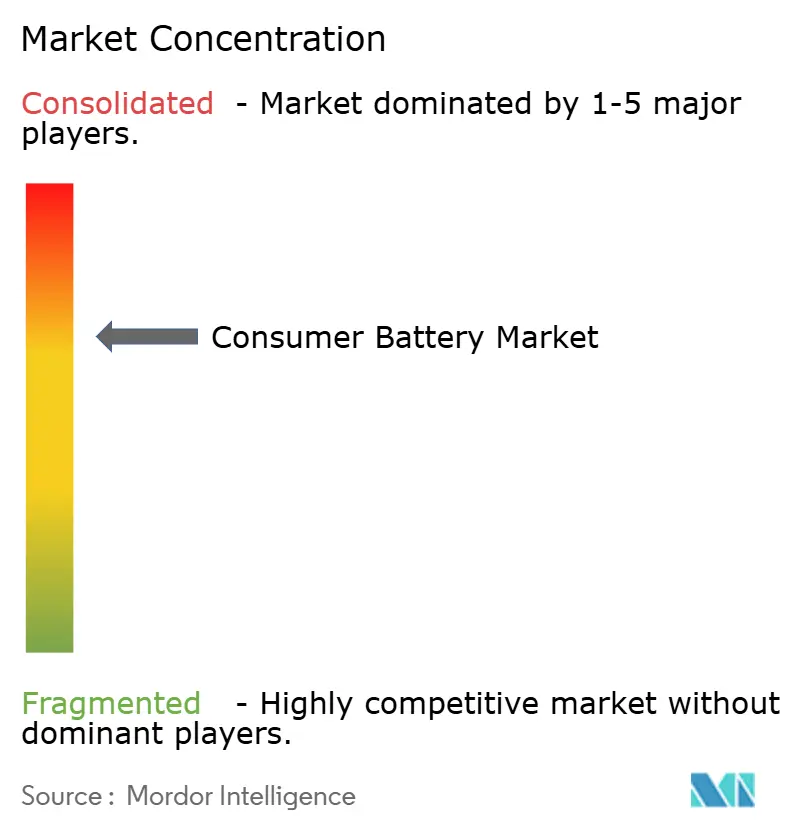

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Battery Market Analysis by Mordor Intelligence

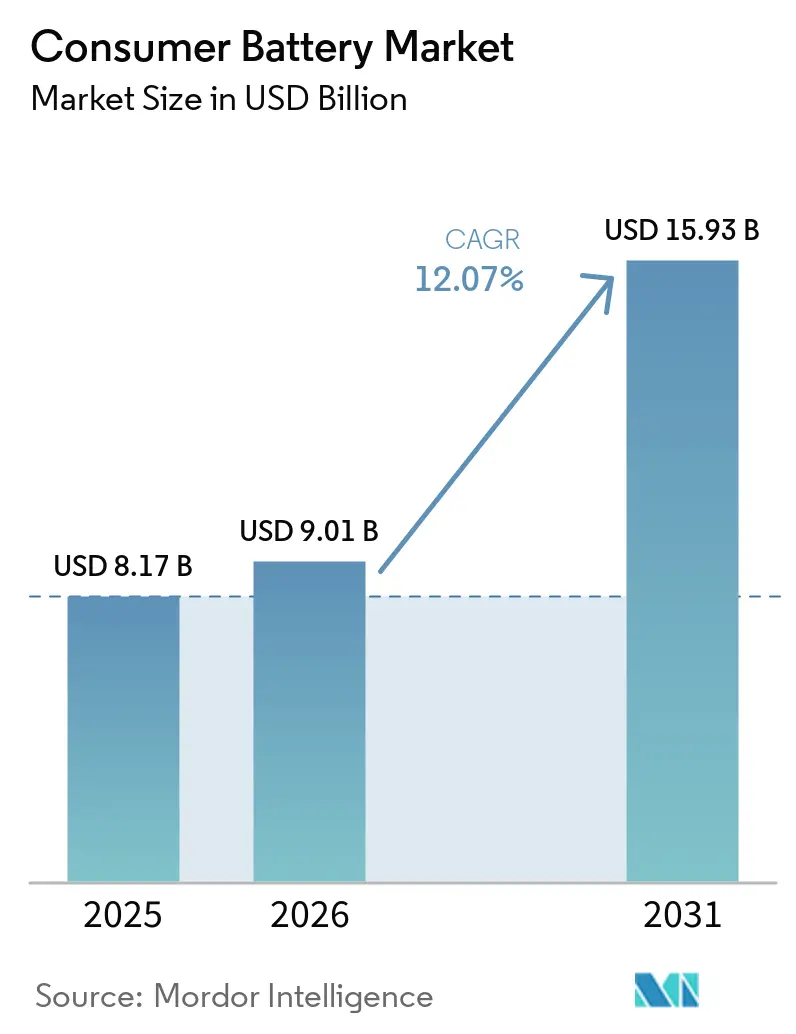

The Consumer Battery Market size was valued at USD 8.17 billion in 2025 and is estimated to grow from USD 9.01 billion in 2026 to reach USD 15.93 billion by 2031, at a CAGR of 12.07% during the forecast period (2026-2031).

Growth reflects the rapid uptake of portable electronics, steady cost deflation in lithium-ion cells, and policy measures that reward rechargeable chemistries while discouraging disposables. Premium smartphones, wireless earbuds, smartwatches, and handheld gaming devices continue to stretch daily energy requirements, steering procurement toward higher-density cells and subscription-based battery-as-a-service models that lower consumer outlays and lock device makers into long-term supply contracts. At the same time, supply volatility in lithium and cobalt, combined with stricter safety and waste-disposal rules, compels manufacturers to hedge raw-material exposure and to adopt ceramic separator technologies that mitigate fire risk. Competitive rivalry intensifies as integrated Japanese and South Korean incumbents defend margins against price-aggressive Chinese firms by deepening vertical integration from cathode precursor synthesis through pack assembly.

Key Report Takeaways

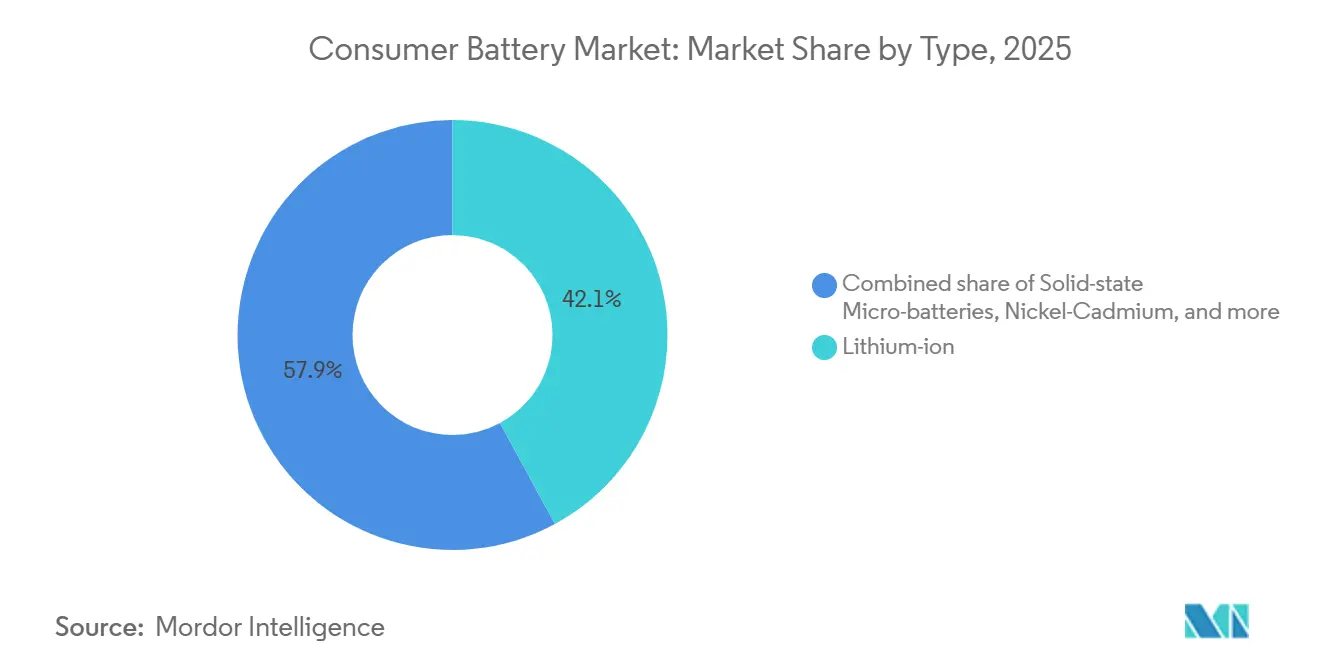

- By chemistry, lithium-ion retained 42.1% consumer battery market share in 2025, while solid-state micro-batteries are forecast to accelerate at 22.6% CAGR to 2031, the fastest among all types.

- By rechargeability, secondary cells commanded 67.5% of the consumer battery market size in 2025 and are advancing at a 12.8% CAGR through 2031, outpacing primary batteries.

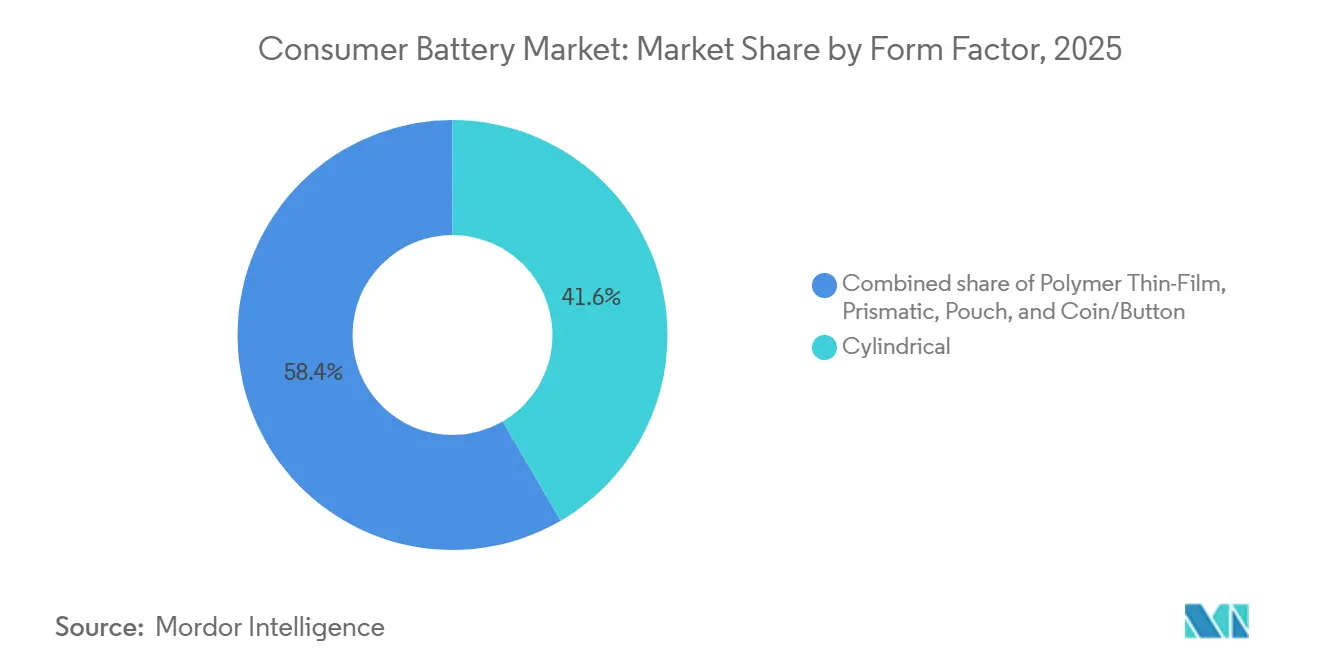

- By form factor, cylindrical formats led with 41.6% consumer battery market size in 2025; polymer thin-film units are projected to surge at 25.5% CAGR to 2031, reflecting demand in biometric payment cards and medical patches.

- By capacity, the 1,000-3,000 mAh range secured 39.8% consumer battery market share in 2025; cells above 10,000 mAh are expanding at 18.9% CAGR on the back of portable gaming consoles and e-mobility devices.

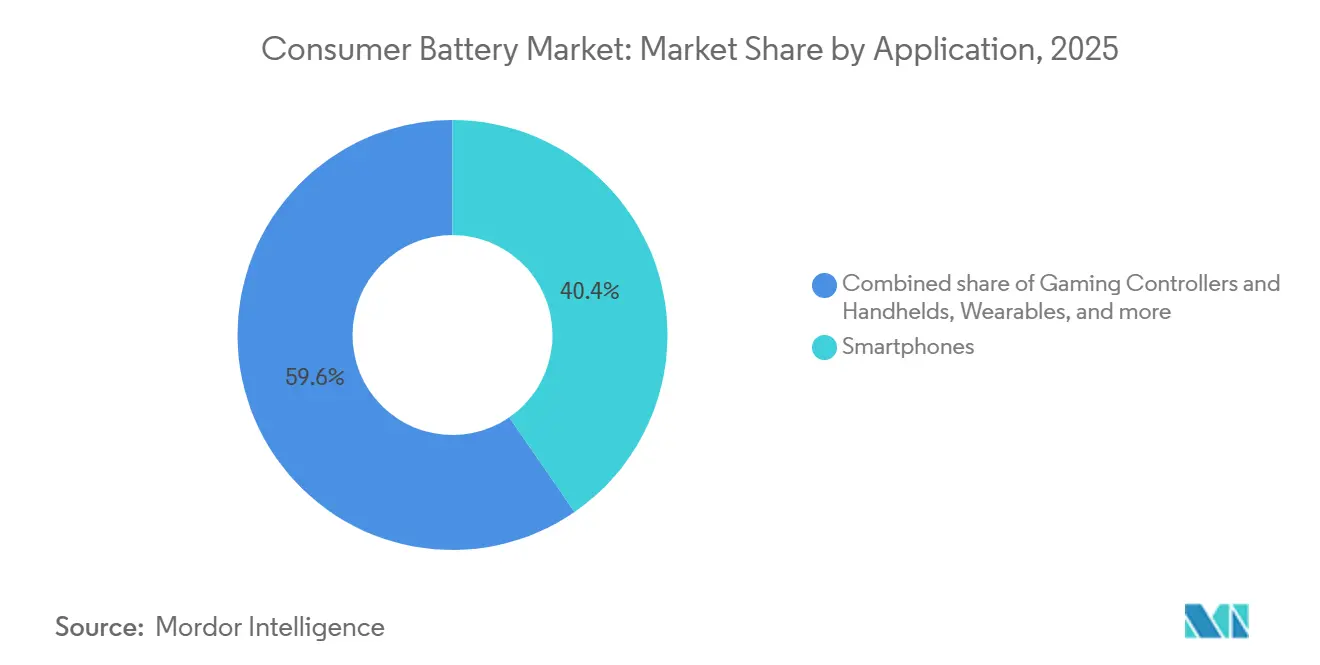

- By application, smartphones generated 40.4% of revenue in 2025, yet wearables represent the fastest-growing slice at 20.2% CAGR to 2031.

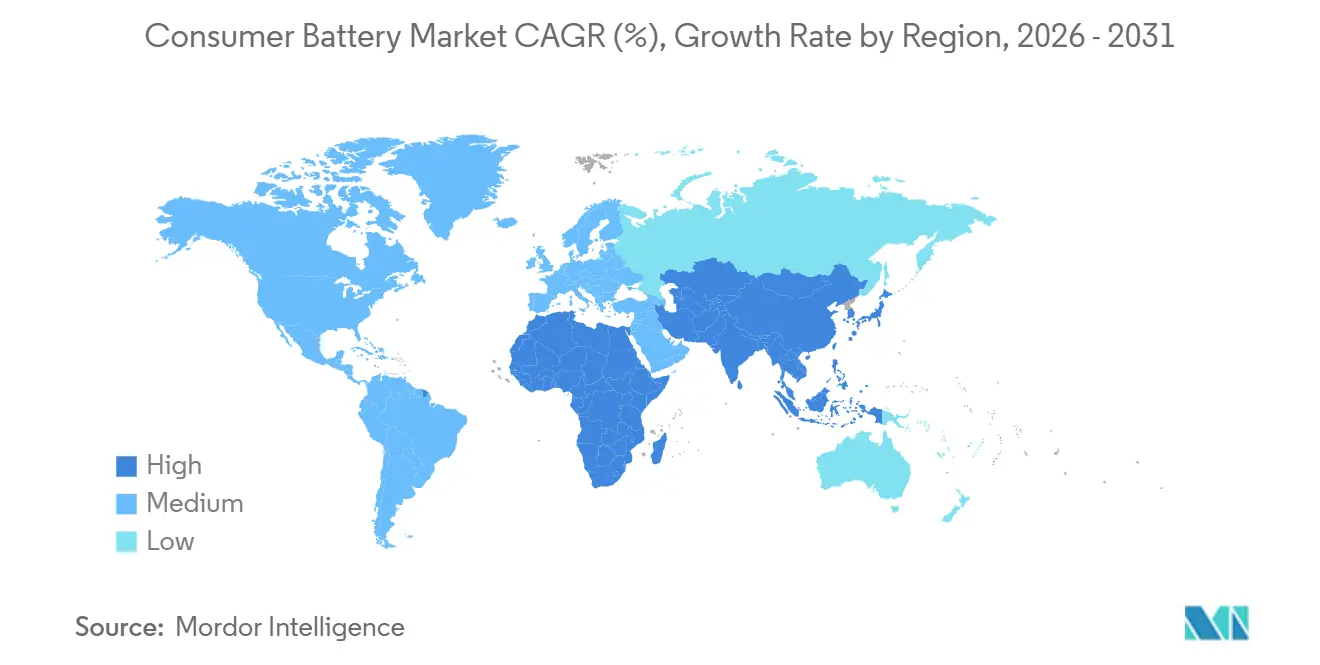

- By geography, Asia-Pacific captured 49.7% of the consumer battery market size in 2025, whereas North America is registering the quickest regional expansion at 17.7% CAGR through 2031, propelled by U.S. manufacturing tax credits.

- Panasonic, LG Energy Solution, Samsung SDI, CATL, BYD, and EVE Energy together held 62% of global revenue in 2025, underscoring a moderately concentrated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for portable consumer electronics | +3.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Declining lithium-ion battery costs | +2.8% | Global, strongest in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Expansion of smart wearables & IoT ecosystem | +2.4% | North America and Europe lead adoption; Asia-Pacific volume growth | Medium term (2-4 years) |

| Right-to-repair laws boosting replacement sales | +1.6% | North America (California, New York) and EU-27 | Long term (≥ 4 years) |

| Emergence of solid-state micro-batteries for hearables | +1.1% | Global, with early commercialization in Japan and South Korea | Long term (≥ 4 years) |

| Rise of subscription-based battery-as-a-service models | +0.9% | North America and select European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Portable Consumer Electronics

More than 2.1 billion portable devices were shipped in 2025, spanning smartphones, tablets, and laptops, and each required between one and three battery cells.[1]International Data Corporation, “Worldwide Quarterly Mobile Device Tracker 2025,” idc.com Secondary gadgets such as wireless earbuds and smartwatches added sizeable incremental cell demand, pushing the average consumer’s device count to 4.2. Shorter replacement cycles in India and Southeast Asia, where budget handsets degrade faster, reinforce volume growth even as mature markets plateau. This divergence shapes a dual-track supply strategy: premium lithium-ion cells with 1,000-plus charge cycles for flagship phones and cost-optimized nickel-metal hydride or alkaline cells for disposable uses. Suppliers that manage multi-chemistry portfolios capture broader wallet share.

Declining Lithium-Ion Battery Costs

Lithium-ion cell pricing slid to USD 89 per kilowatt-hour in 2025 from USD 132 two years prior, chiefly due to nickel-rich NMC 811 cathodes delivering 20% higher energy density.[2]BloombergNEF, “Battery Price Survey 2025,” about.newenergyfinance.com This 33% cost retreat places rechargeables on parity with alkalines over the full duty cycle, catalyzing substitution in remote controls and flashlights. The down-cycle, however, is flattening: inflated labor charges and hedged raw-material contracts are expected to cap further declines near USD 85 through 2027, tightening margins for producers that locked in lithium at 2023 peaks. Vertically integrated players hedge risk via captive mining assets, while cell assemblers reliant on spot markets face profitability swings.

Expansion of Smart Wearables & IoT Ecosystem

Wearable shipments climbed to 540 million units in 2025, led by smartwatches and hearables that favor coin, micro-cylindrical, or prismatic pouch formats. Always-on sensors for ECG, blood oxygen, and glucose monitoring drain power continuously, driving adoption of solid-state electrolytes rated for 5,000-plus cycles. IoT nodes in smart-home systems emphasize decade-long lifetimes, steering procurement toward lithium-thionyl chloride primary cells with minimal self-discharge. The resulting market fragmentation rewards agile suppliers capable of matching form-factor, voltage, and capacity permutations demanded by micro-niches.

Right-to-Repair Laws Boosting Replacement Sales

California’s SB 244 and the EU’s Ecodesign Regulation ban adhesive-only battery mounting and require serviceable designs, adding up to USD 1.20 per unit but extending device life by two years.[3]European Commission, “Ecodesign for Sustainable Products Regulation 2024,” ec.europa.eu The aftermarket battery segment hit USD 1.9 billion in 2025, lifted by consumers opting for replacements over full device upgrades. Adherence to standards like IEC 62133 becomes an entry gate, elevating compliance costs yet building trust. Parallel growth in counterfeit cells keeps regulators vigilant, as underspecified batteries trigger safety seizures at ports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral supply chain volatility | -2.1% | Global, with acute exposure in lithium and cobalt sourcing | Short term (≤ 2 years) |

| Safety recalls from thermal-runaway incidents | -1.4% | Global, concentrated in North America and Europe due to stricter reporting | Medium term (2-4 years) |

| Waste-disposal rules targeting single-use cells | -0.8% | EU-27, California, and select Asian markets | Long term (≥ 4 years) |

| Low-power semiconductors cutting replacement demand | -0.6% | Global, led by advanced-node adoption in premium devices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Supply Chain Volatility

Lithium carbonate prices swung from USD 13,000 per ton in January 2024 to USD 22,000 by December 2025, compressing gross margins by up to 500 basis points for manufacturers with 20-30% spot exposure.[4]LG Energy Solution, “Annual Report 2025,” lgensol.com Export bans in Indonesia and mine delays in Australia and the DRC prolong supply uncertainty, spurring refinery investments yet adding two-year lead times. Although solid-state batteries reduce cobalt intensity, commercialization remains limited to niche consumer devices pending scale economics.

Safety Recalls from Thermal-Runaway Incidents

Forty-seven product recalls tied to battery fires affected 8.3 million devices in 2024, eroding consumer trust and imposing recall expenses exceeding USD 50 million for tier-1 brands. Ceramic-coated separators cut fire risk by 60% at an incremental cost of USD 0.12 per cell, moving quickly into premium phones and laptops. Updated IEC 62133-2 crush and nail-penetration requirements widen safety compliance gaps for low-cost imports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Solid-State Micro-Batteries Challenge Lithium-Ion Dominance

Lithium-ion held 42.1% consumer battery market share in 2025, thanks to mature global supply networks and energy densities near 300 Wh/kg. Solid-state micro-batteries are projected to grow 22.6% CAGR through 2031 as hearables, medical patches, and smart cards require sub-100 mAh capacities and ten-year lifespans. The consumer battery market size expansion in this niche reflects a premium willingness to pay for intrinsic safety and ultra-thin profiles. Alkaline, zinc-carbon, and nickel-metal hydride chemistries continue to serve low-drain devices but yield a share each year.

Competition centers on ceramic or polymer electrolytes that remove flammable solvents, yet cost remains prohibitive outside high-value segments. Suppliers investing in mass-production lines aim to close the price gap by 2028, potentially widening adoption into mainstream wearables.

By Rechargeability: Secondary Cells Dominate Amid Disposal Restrictions

Secondary batteries controlled 67.5% of 2025 revenue and will outpace the overall consumer battery market at 12.8% CAGR thanks to falling lithium-ion costs and extended producer responsibility fees on disposables. EU rules mandating minimum recycled content and California’s USD 0.10 fee per primary cell tilt total-cost-of-ownership decisively toward rechargeables. The consumer battery market size attached to primary cells continues to shrink except in smoke detectors and emergency flashlights, where long shelf life offsets higher life-cycle cost.

Retailers pledging to pull AA and AAA disposables by 2027 will compress shelf space for alkalines further, forcing legacy brands to pivot toward rechargeable or lithium primary lines positioned for IoT devices.

By Form Factor: Thin-Film Batteries Outpace Legacy Cylindrical Designs

Cylindrical cells held 41.6% consumer battery market share in 2025, benefiting from robust mechanical strength, standardized 18650 and 21700 dimensions, and deeply amortized production lines that keep unit costs below USD 0.10 per watt-hour. Polymer thin-film batteries, though only a fraction of current volume, are advancing at a 25.5% CAGR through 2031 as biometric payment cards, medical patches, and flexible displays demand profiles under 1 mm and high cycle life without swelling TDK. Prismatic packs captured 23.7% share on the strength of smartphone and tablet demand, while pouch formats accounted for 19.4% by catering to ultrathin laptops and premium wearables that trade enclosure rigidity for volumetric efficiency.

The consumer battery market size linked to coin and button cells reached 12.1% of 2025 revenue, yet growth lags at 4.2% CAGR as watches and motherboard CMOS circuits lengthen service intervals. Developers of thin-film technology exploit solid polymer electrolytes and lithium-metal anodes to hit 150-200 Wh/L at bend radii below 20 mm, allowing direct integration into payment cards that must flex 100,000 times over their life. Cylindrical suppliers respond by introducing high-nickel NMC 811 chemistries to boost energy density by 20%, protecting share in laptops and power tools despite form-factor headwinds. The widening mix of shapes, thicknesses, and mechanical requirements increases qualification costs for OEMs and favors cell makers with multi-format lines.

By Capacity Range: High-Capacity Cells Fuel Gaming and Micro-Mobility Growth

The 1,000-3,000 mAh band captured 39.8% consumer battery market share in 2025, mirroring mainstream smartphone demand for all-day runtime inside 7-9 mm housing depths. Competitive pricing, especially from Chinese suppliers offering cells at USD 2.80-3.20 each, keeps this tier highly commoditized and margins thin. Segments above 10,000 mAh are scaling at 18.9% CAGR to 2031 as portable gaming consoles, e-scooters, and drone controllers require multi-hour operation and rapid charge capability, tilting procurement toward cylindrical 21700 cells rated 4,800-5,000 mAh apiece.

Up-to-1,000 mAh cells held 14.6% of the consumer battery market size in 2025, dominated by wireless earbuds, fitness trackers, and smart jewelry that value footprint over capacity and accept daily charging cycles. The 3,000-10,000 mAh tier, representing 18.3% share, addresses tablets and mid-range laptops and is migrating to high-silicon anodes to shave weight without sacrificing runtime. Transport rules under UN 38.3 increase packaging costs for packs exceeding 20 Wh, but have not materially impeded growth because OEMs are baking compliance into design from the outset. Suppliers that can balance gravimetric energy density, discharge rates, and cycle life across these capacity bands capture wider wallet share as device portfolios diversify.

By Application: Wearables Accelerate While Smartphones Plateau

Smartphones generated 40.4% of the 2025 segment revenue, yet shipment growth is leveling as replacement cycles stretch past 31 months and right-to-repair statutes lengthen handset life. Manufacturers offset slower volumes by specifying larger 4,500-5,500 mAh packs, lifting average selling prices per cell. Wearables are surging at 20.2% CAGR through 2031, with smartwatches and hearables driving micro-cell demand that prioritizes thinness, high cycle endurance, and biocompatible housings. Laptops and tablets contributed 16.8% revenue in 2025, a mature cohort edging forward at 6.1% CAGR as enterprises stretch refresh cycles yet insist on longer unplugged operation.

Gaming controllers and handheld consoles accounted for an 8.7% share, leveraging 4,000-10,000 mAh prismatic cells to deliver three-hour play sessions at 15 W continuous draws. Smart-home devices, door locks, thermostats, and security cameras secured a 7.3% share and favor lithium-thionyl chloride primaries or nickel-metal hydride rechargeables that promise five-year service windows. Small home appliances, personal mobility gadgets, and medical consumer devices collectively made up 13.9% of revenue, with each niche valuing different chemistries, from cylindrical 18650s in e-bikes to zinc-air coin cells in glucometers. The “Others” bucket, including toys and power tools, rounds out 12.8% and benefits from falling lithium-ion costs that displace alkaline packs in high-drain toys.

Geography Analysis

Asia-Pacific generated 49.7% of 2025 revenue, anchored by China’s 420 GWh of cell capacity and cost-advantaged supply chains. Japanese and South Korean firms concentrate on premium cylindrical and solid-state formats, sustaining margins above 60% in flagship electronics. India’s subsidy-backed assembly expansions capture partial value yet rely on imported cathode and electrolyte inputs, limiting upstream integration.

North America, buoyed by a USD 35 per kWh Advanced Manufacturing Production Credit, is expanding at a 17.7% CAGR through 2031. Over USD 73 billion of announced capacity from Panasonic, LG, and Samsung SDI is bringing localized supply to smartphones, laptops, and wearables. Canada’s critical-mineral strategy seeks to supply up to 20% of regional demand, reducing import dependence.

Europe holds 18.4% of the consumer battery market size, but grows at a slower 9.3% CAGR as the Battery Regulation raises compliance costs. Domestic players VARTA and Northvolt expand capacity yet struggle with financing, highlighting regulatory cost pressure on margins. South America and the Middle East & Africa contribute smaller shares, yet post double-digit growth where rising incomes boost smartphone and wearable penetration.

Competitive Landscape

Top 10 suppliers commanded 62% of the consumer battery market revenue in 2025, signaling moderate concentration. Panasonic, LG Energy Solution, and Samsung SDI dominate high-end cylindrical and prismatic segments, protecting margins via end-to-end integration. CATL, BYD, EVE Energy, and Amperex Technology undercut pricing on commodity smartphone cells by 15-20%, accelerating share gains. Alkaline stalwarts Duracell and Energizer combat structural decline through lithium primary and recycling partnerships.

Strategic thrusts include solid-state micro-battery rollouts, battery-as-a-service models where OEMs own the pack and invoice usage, and exploratory sodium-ion chemistries aimed at cost-sensitive applications. Patent filings in ceramic electrolytes surged 340% between 2022-2025, with Japanese and South Korean firms owning two-thirds of granted patents, giving them a medium-term moat against lower-cost rivals.

Consumer Battery Industry Leaders

Duracell Inc.

Energizer Holdings Inc.

Panasonic Holdings Corp.

VARTA AG

GP Batteries International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Realme announced the Realme 16T smartphone, which features an 8,000mAh battery—one of the largest batteries integrated into a slim consumer smartphone design. The device also highlights AI-powered battery management and multi-day battery life.

- May 2026: Motorola introduced upgraded silicon-carbon battery systems in its Razr Ultra 2026 foldable smartphone lineup. Independent battery tests indicated that the device achieved over 16 hours of endurance, positioning it as one of the longest-lasting foldable smartphones released to date.

- January 2026: At CES 2026, several companies showcased advancements in solid-state battery technology for consumer electronics. Reports emphasized that solid-state batteries could soon power smartphones, laptops, and wearable devices, offering higher energy density, enhanced safety, and faster charging capabilities.

- January 2026: startup Donut Lab announced at CES 2026 what it described as the “first commercially ready solid-state battery,” claiming ultra-fast charging, high cycle life, and improved performance in low-temperature conditions. However, industry analysts and battery experts remain cautious, awaiting real-world deployment in consumer devices.

Global Consumer Battery Market Report Scope

Consumer batteries are portable power sources designed for consumer electronic devices. They are compact, lightweight, and often come in standardized sizes and formats to fit various consumer devices, such as smartphones, laptops, cameras, remote controls, toys, and other portable electronics. Consumer batteries are typically categorized into two main types: disposable (primary) batteries and rechargeable (secondary) batteries.

The global consumer battery market is segmented by type, rechargeability, form factor, capacity range, application, and geography. By type, the market is segmented into lithium-ion, alkaline, zinc-carbon, nickel-metal hydride, nickel-cadmium, solid-state micro-batteries, zinc-air, and others. By rechargeability, the market is segmented into primary and secondary. By form factor, the market is segmented into cylindrical, prismatic, pouch, coin/button, and polymer thin-film. By capacity range, the market is segmented into up to 1,000 mAh, 1,000-3,000 mAh, 3,000-10,000 mAh, and above 10,000 mAh. By application, the market is segmented into smartphones, laptops and tablets, wearables, gaming controllers, smart-home devices, small home appliances, personal mobility devices, medical consumer devices, and others. The report also covers the market size and forecasts for the consumer battery market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

By Type

| Lithium-ion |

| Alkaline |

| Zinc-Carbon |

| Nickel-Metal Hydride |

| Nickel-Cadmium |

| Solid-state Micro-batteries |

| Zinc-Air |

| Others |

By Rechargeability

| Primary (Disposable) |

| Secondary (Rechargeable) |

By Form Factor

| Cylindrical |

| Prismatic |

| Pouch |

| Coin/Button |

| Polymer Thin-Film |

By Capacity Range

| Up to 1,000 mAh |

| 1,000 to 3,000 mAh |

| 3,000 to 10,000 mAh |

| Above 10,000 mAh |

By Application

| Smartphones |

| Laptops and Tablets |

| Wearables |

| Gaming Controllers and Handhelds |

| Smart-Home Devices |

| Small Home Appliances |

| Personal Mobility Devices |

| Medical Consumer Devices |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Lithium-ion | |

| Alkaline | ||

| Zinc-Carbon | ||

| Nickel-Metal Hydride | ||

| Nickel-Cadmium | ||

| Solid-state Micro-batteries | ||

| Zinc-Air | ||

| Others | ||

| By Rechargeability | Primary (Disposable) | |

| Secondary (Rechargeable) | ||

| By Form Factor | Cylindrical | |

| Prismatic | ||

| Pouch | ||

| Coin/Button | ||

| Polymer Thin-Film | ||

| By Capacity Range | Up to 1,000 mAh | |

| 1,000 to 3,000 mAh | ||

| 3,000 to 10,000 mAh | ||

| Above 10,000 mAh | ||

| By Application | Smartphones | |

| Laptops and Tablets | ||

| Wearables | ||

| Gaming Controllers and Handhelds | ||

| Smart-Home Devices | ||

| Small Home Appliances | ||

| Personal Mobility Devices | ||

| Medical Consumer Devices | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the consumer battery market in 2026?

It is valued at USD 9.01 billion for 2026 and is tracking toward USD 15.93 billion by 2031, indicating strong momentum.

Which region is growing fastest for consumer batteries?

North America is expanding at a 17.7% CAGR to 2031 thanks to generous U.S. production tax credits.

What chemistry will gain the most share through 2031?

Solid-state micro-batteries are forecast to rise at 22.6% CAGR as hearables and medical patches scale.

How are right-to-repair rules changing the market?

They require serviceable designs and boost aftermarket battery revenue, already at USD 1.9 billion in 2025.

Which form factor is disrupting traditional cylindrical cells?

Polymer thin-film batteries, growing at 25.5% CAGR, meet the needs of biometric cards and flexible medical wearables.

What is the main safety technology being adopted?

Ceramic-coated separators add USD 0.12 per cell but cut fire risk by 60%, increasingly standard in premium devices.

Page last updated on: