VRLA Battery Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 49.09 Billion |

| Market Size (2031) | USD 60.97 Billion |

| Growth Rate (2026 - 2031) | 4.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

VRLA Battery Market Analysis by Mordor Intelligence

The VRLA Battery Market size is expected to increase from USD 46.84 billion in 2025 to USD 49.09 billion in 2026 and reach USD 60.97 billion by 2031, growing at a CAGR of 4.43% over 2026-2031. Demand remains focused on telecom tower densification and the deployment of edge data centers, while cost reductions in lithium-iron-phosphate (LFP) chemistries are diminishing the traditional price advantage of VRLA batteries. Hybrid-Gel/AGM designs are experiencing the fastest growth, as operators in the Middle East and sub-Saharan Africa prioritize batteries capable of withstanding ambient temperatures of 55°C without the risk of thermal runaway.[1]GS Yuasa, “Hybrid-Gel Technical Datasheet,” gs-yuasa.com The Asia-Pacific region continues to be a key revenue driver, supported by China's 45% share of global lead-acid battery production and India's challenges with grid stability, which sustain the growing demand for uninterruptible power supply (UPS) systems.[2]Battery Council International, “Industry Statistics,” batterycouncil.orgCompetitive intensity is increasing as established players integrate IoT monitoring into premium Thin-Plate Pure Lead (TPPL) product lines or diversify through lithium-ion and ultracapacitor acquisitions.[3]EnerSys, “Investor Presentation FY 2025,” enersys.comOn the risk side, the EU Battery Regulation's requirements for recycled lead and digital passports increase compliance costs, driving consolidation among mid-tier producers.[4]European Commission, “Regulation (EU) 2023/1542 on Batteries,” ec.europa.eu

Key Report Takeaways

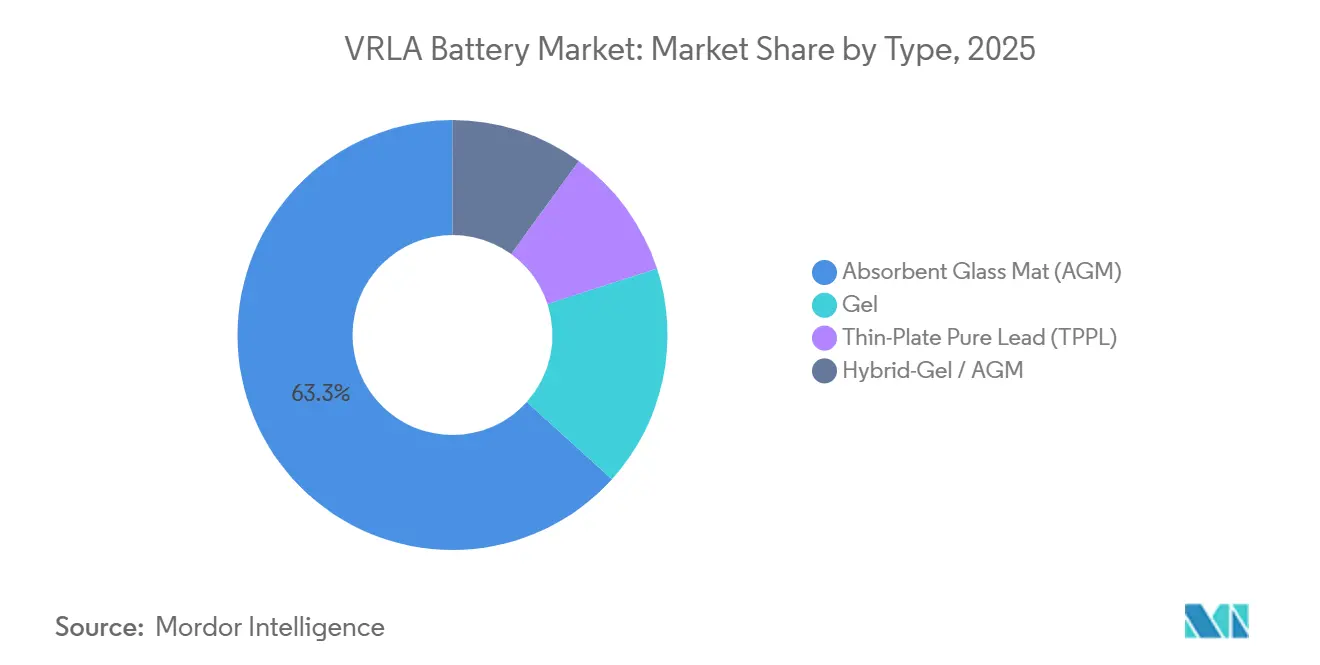

- By type, AGM commanded 63.3% of 2025 revenue, while Hybrid-Gel/AGM is projected to expand at a 7.8% CAGR through 2031.

- By application, UPS led with 34.9% of the VRLA battery market share in 2025, whereas energy-storage systems are forecast to post the quickest growth at 6.4% CAGR to 2031.

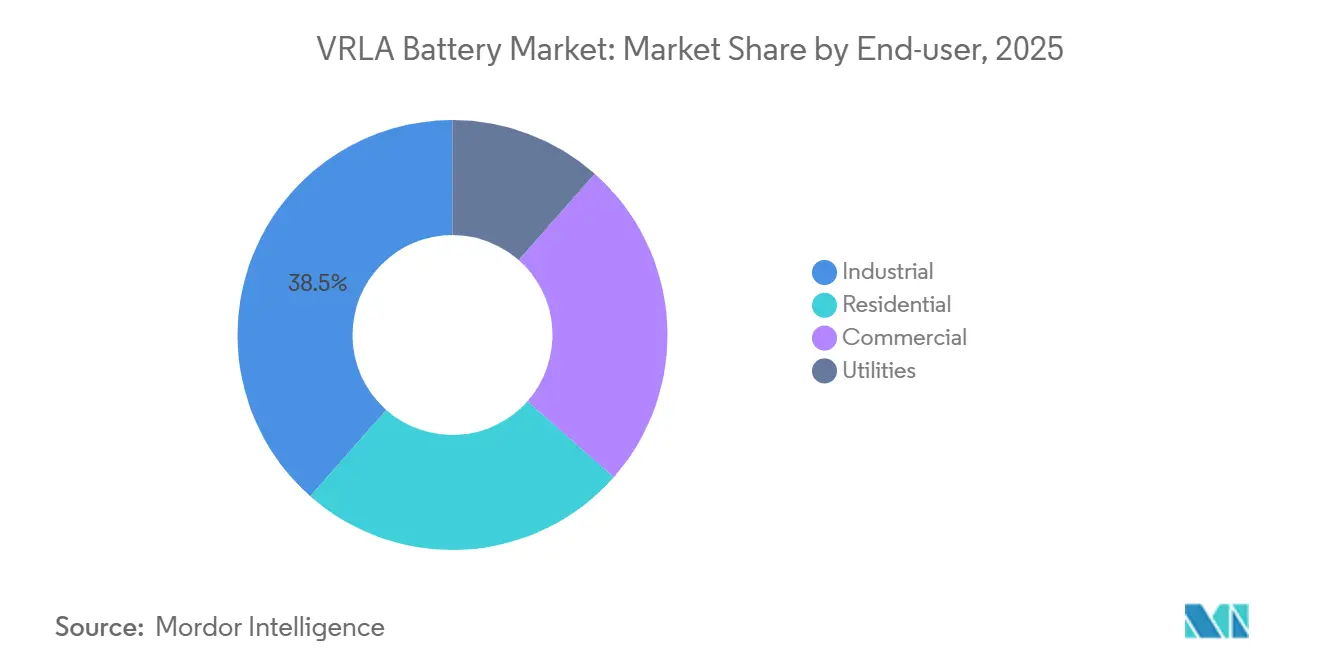

- By end-user, industrial customers held 38.5% of 2025 demand, but residential deployments are expected to advance at 6.8% CAGR over 2026-2031.

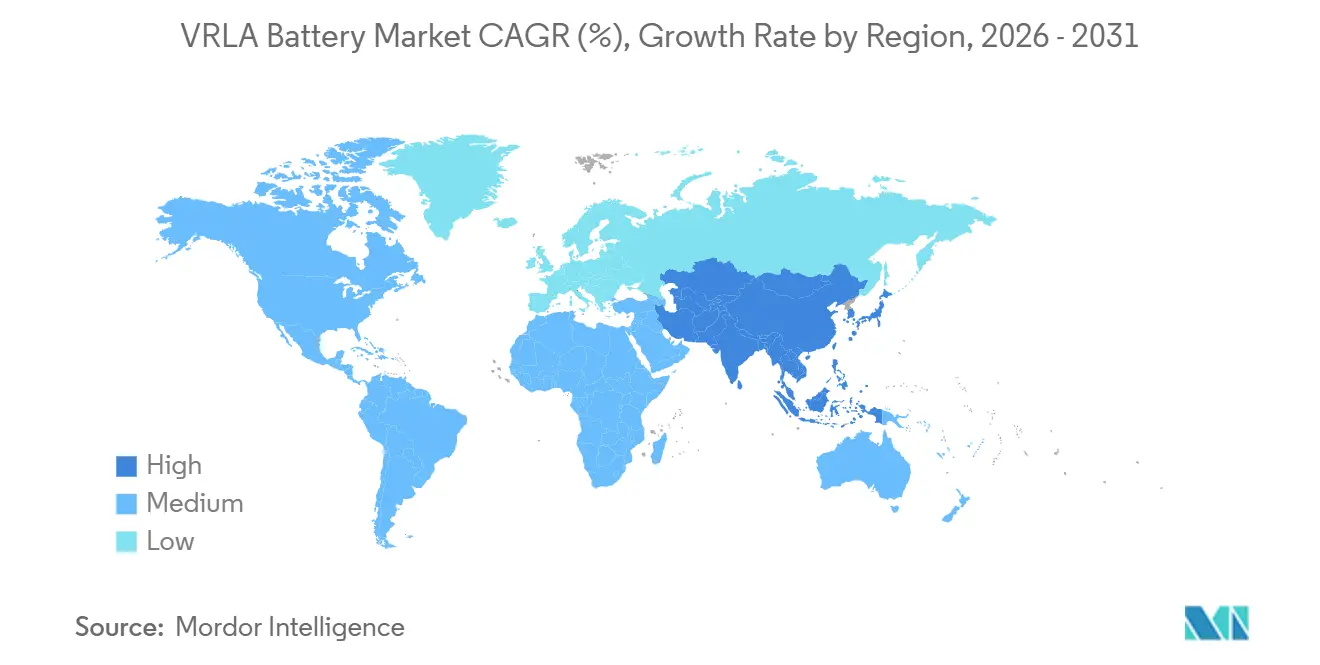

- By geography, Asia-Pacific accounted for 43.1% of revenue in 2025 and is expected to track a 5.1% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global VRLA Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for reliable back-up power in telecom infrastructure | +1.2% | Asia-Pacific, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Data-center & UPS build-outs in Tier-2/3 cities | +0.9% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Renewable micro-grids needing low-CAPEX storage | +0.7% | Sub-Saharan Africa, ASEAN, South America | Long term (≥ 4 years) |

| Cost advantage vs. lithium-ion for ≤3-yr duty cycles | +0.8% | Global | Short term (≤ 2 years) |

| Micro-mobility boom in ASEAN & Africa | +0.5% | ASEAN (Vietnam, Indonesia, Thailand), Sub-Saharan Africa | Medium term (2-4 years) |

| Hybrid-gel VRLA designs for 55°C climates | +0.6% | Middle East, Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for reliable back-up power in telecom infrastructure

Small-cell 5G deployments require 2-4 hours of autonomy without the fire-risk profile associated with lithium-ion batteries, which complicates permitting processes. AGM VRLA (Absorbent Glass Mat Valve-Regulated Lead-Acid) batteries remain the preferred choice as they eliminate the need for active cooling and reduce insurance costs in densely populated urban areas. In India, tower operators adopt five-year AGM replacement cycles to avoid the thermal management expenses of lithium batteries. This approach is similarly observed across 18,000 off-grid sites in Africa, where solar arrays are paired with VRLA batteries to minimize diesel generator usage. Open RAN architectures also benefit from compact VRLA battery configurations; however, pilot projects in Western Europe indicate that lithium batteries could challenge this preference in stable-grid markets by 2028.

Edge Data-Center & UPS Build-Outs in Tier-2/3 Cities

Latency-sensitive applications are shifting compute capacity to smaller facilities, which typically utilize 10-50 kW UPS systems. A 20 kW edge site incurs approximately USD 8,000 for AGM VRLA batteries compared to USD 14,000 for equivalent lithium-ion batteries, while also avoiding the added battery-management complexity that increases installation labor by 30%. However, the preference shifts when rack space becomes limited; lithium-ion batteries, with their threefold energy density, free up floor space for revenue-generating servers. This shift is anticipated to gain momentum once lithium-ion pack prices fall below USD 100/kWh, projected after 2027.

Renewable Micro-Grids Needing Low-CAPEX Storage

Off-grid solar installations under 2 kWh in ASEAN and sub-Saharan Africa often utilize VRLA batteries due to limited procurement budgets that typically exclude battery-management electronics. Hybrid-Gel chemistries perform well in high-temperature environments of up to 55 °C, offering a float life of 12-15 years while eliminating cooling requirements that previously accounted for 30% of a site’s operating budget. With governments expanding rural electrification initiatives, these low-capex battery systems maintain a competitive position, outperforming lithium batteries in terms of total installed cost.

Cost Advantage Versus Lithium-Ion for ≤ 3-Year Duty Cycles

Commercial UPS users generally replace batteries based on accounting schedules rather than waiting for end-of-life, which limits the advantage of lithium batteries' longer cycle life. For instance, a 10 kW UPS with AGM VRLA batteries costs USD 2,200 for a three-year replacement cycle, whereas lithium batteries require an upfront cost of USD 3,800, which becomes cost-effective only at discount rates below 8%. Although LFP prices experienced a significant decline in 2025, the lowest prices are primarily allocated to automotive cells. Meanwhile, stationary-storage grades continue to carry a 25-30% premium, maintaining VRLA batteries' cost advantage in float-dominated applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid price decline of LFP battery packs | -1.1% | Global, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Lead price volatility & stringent recycling directives | -0.8% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Rack-space premium in edge UPS (<10 kW) | -0.4% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Premature failures due to maintenance myths | -0.3% | Global, acute in South Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid price decline of LFP battery packs

Overcapacity led to a reduction in Chinese LFP pack prices by more than CNY 3,000 per ton in the first half of 2025, narrowing the cost difference with VRLA batteries to single digits for three-year duty cycles. Edge data center operators are now willing to pay a 10-15% premium for lithium batteries due to their ability to save 60-70% of rack space, which can be directly translated into increased colocation revenue. In Vietnam, electric two-wheeler OEMs reduced lead-acid battery usage to 85% in 2025, highlighting the risk of substitution. However, stationary-grade LFP batteries continue to command a 25-30% premium due to cycle-life certifications, maintaining VRLA's competitiveness in applications where batteries spend 95% of their lifespan in float mode.

Lead Price Volatility & Stringent Recycling Directives

Lead prices ranged between USD 1,950 and USD 2,350 per ton in 2025, driven by China's stricter scrap-import quotas. The EU Battery Regulation mandates an increase in recycled lead content to 85% by 2031 and introduces a digital passport in 2027, which is expected to add USD 2-4 per kWh to compliant production costs. Established players with closed-loop recycling systems benefit from scale efficiencies, while smaller Asian producers face significant capital requirements, estimated at USD 50-80 million for a 50,000 t/y smelter, leading to accelerated market consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: AGM Dominance Meets Hybrid-Gel Momentum

AGM technology accounted for 63.3% of the projected 2025 revenue, driven by its widespread use in UPS systems and telecom cabinets. Hybrid-Gel/AGM currently holds a 9.8% revenue share but is growing at a compound annual growth rate (CAGR) of 7.8%, supported by demand for 12-15-year float life in environments with temperatures reaching 55 °C. TPPL caters to premium niche markets, including enterprise data centers and rail signaling, offering 15-20-year lifespans at a 30-40% price premium, which extends replacement intervals.

Cost considerations play a significant role in market segmentation. A 12 V 100 Ah AGM unit is priced at approximately USD 200, about 25% less than Hybrid-Gel. However, AGM batteries experience thermal derating, which reduces their lifespan by half in temperatures exceeding 45 °C. FIAMM’s 2026 Pure Guard launch led to a 20% reduction in Hybrid-Gel volume, narrowing the form-factor gap with lithium batteries. EnerSys has integrated IoT sensors into TPPL battery packs, enabling predictive maintenance to address the 18-22% of premature VRLA failures caused by inadequate topping-up practices. With the upcoming digital passport requirement, chemistries with stable state-of-health profiles, such as TPPL and Hybrid-Gel, are positioned to capture additional market share.

By Application: UPS Leads, Energy Storage Accelerates

UPS contributed 34.9% to the VRLA battery market revenue in 2025, supported by installations in data centers and commercial buildings. While the growth rate for UPS moderates to a 3.1% CAGR, the preference for incumbent technologies helps maintain stable volumes. Energy storage systems are projected to grow at a notable CAGR, driven by the adoption of off-grid solar solutions in Africa and ASEAN regions, where a 2 kWh VRLA battery bank costs USD 240 compared to USD 380 for lithium-based systems. However, the VRLA battery market share for UPS declined by 120 basis points in 2025 as lithium gained popularity in space-constrained edge facilities.

The telecom and data-center backup segment remains robust, with 5G densification driving node deployments that continue to favor VRLA batteries over fire-regulated lithium alternatives. The automotive and transportation segment is declining as OEMs transition to lithium-ion 48 V architectures, though aftermarket replacements provide stability to the segment. In industrial applications, VRLA batteries are preferred for forklifts and rail signaling due to their vibration tolerance. Additionally, emergency lighting and medical devices continue to rely on VRLA batteries, as switching to lithium alternatives would require regulatory recertification, leading to potential downtime costs.

By End-User: Industrial Anchors, Residential Surges

Industrial users accounted for 38.5% of the projected 2025 revenue, encompassing applications ranging from material-handling fleets to oil-and-gas instrumentation. Single-shift warehouses continue to utilize VRLA batteries due to the availability of overnight charging windows, while multi-shift operators are exploring lithium fast-charging solutions. Residential demand is growing at a CAGR of 6.8%, driven by increased home-UPS purchases in India and Pakistan, where monthly outages exceed 12 occurrences. A standard 12 V 100 Ah VRLA unit, priced at USD 150, remains more popular than lithium batteries, with a 2:1 sales ratio in sub-500 Wh solar-home systems.

Commercial customers evaluate floor-space efficiency, with lithium batteries preferred in high-rent urban locations due to their smaller footprint, while suburban facilities often opt for VRLA batteries due to lower capital expenditure. Utilities represent a small but strategically important segment, utilizing VRLA batteries for substation control and short-duration renewable energy smoothing. As digital metering adoption increases, utilities may experiment with TPPL batteries, which offer a 20-year lifespan; however, large-scale deployment is expected to remain limited through 2031.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 43.1% of global revenue and is projected to grow at a 5.1% CAGR through 2031. China remains a leader in commodity AGM exports, while India drives domestic growth through residential UPS sales. ASEAN markets show a mixed landscape: Vietnam's two-wheeler market remains 85% lead-acid, whereas Thai government subsidies have reduced the cost gap between lead-acid and lithium-ion batteries to single digits.

In North America, hyperscale data center operators are retrofitting enterprise facilities with TPPL batteries while favoring lithium-ion for new edge builds. Section 45X tax credits allocated USD 184.6 million to EnerSys in FY2025, supporting domestic TPPL production and mitigating reliance on Asian supply chains. However, the expiration of these credits in 2032 raises future concerns.

Europe faces challenges from the EU Battery Regulation, which has increased per-unit costs but also created competitive advantages for established players with closed-loop recycling systems. Reverse-logistics costs have risen by 12-15% due to compliance requirements, impacting overall profitability.

China's VRLA market is stabilizing domestically as lithium-ion batteries gain popularity in urban data centers. Export-oriented manufacturers are focusing on Hybrid-Gel and TPPL variants to capture higher-margin opportunities in the Middle East and Africa.

India added 180 MW of edge data center capacity in 2025, with 68% of installations specifying AGM VRLA batteries due to their durability and compatibility with the grid. In ASEAN, Vietnam's electric two-wheeler market remains predominantly lead-acid at 85%, while Indonesia and Thailand are accelerating lithium-ion adoption through government subsidies.

Competitive Landscape

The VRLA battery market is moderately concentrated, with the top five companies being EnerSys, Clarios, GS Yuasa, Exide Technologies, and East Penn. EnerSys allocated USD 37 million to expand Thin Plate Pure Lead (TPPL) capacity in Ohio, targeting higher-margin applications in data centers. Clarios acquired Maxwell’s ultracapacitor product line, integrating VRLA batteries with high-burst modules for start-stop automotive systems. GS Yuasa committed JPY 70.3 billion to establish a 2 GWh lithium-ion plant, diversifying its portfolio to mitigate risks associated with the commoditization of its VRLA core business.

Leoch is planning a U.S. spin-off to fund its Hybrid-Gel battery expansion and emphasize vertical integration following its acquisition of a 70% stake in Guangdong Yuasa. Narada employs a dual-chemistry strategy, using VRLA batteries for cost-sensitive projects while leveraging in-house lithium-ion technology for high-cycle storage applications. Compliance investments related to the EU’s digital passport regulation are estimated at USD 15-25 million, favoring companies with robust IT capabilities. Meanwhile, fragmented regional producers are either forming alliances to secure recycled lead supplies or exiting commodity Absorbent Glass Mat (AGM) battery lines.

Innovation in Hybrid-Gel battery designs is gaining traction, combining the fast recharge capabilities of AGM batteries with the thermal stability of gel batteries. Modular VRLA trays, designed to resemble lithium-ion rack formats, are being developed to maintain competitiveness in edge-UPS (Uninterruptible Power Supply) applications. Additionally, IoT sensor integration is becoming a critical area of focus. Predictive maintenance platforms not only generate recurring revenue streams but also help offset declining hardware margins, thereby extending the relevance of VRLA batteries in the market.

VRLA Battery Industry Leaders

-

Clarios

-

EnerSys

-

Exide Technologies

-

GS Yuasa Corporation

-

East Penn Manufacturing

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: EnerSys closed its Tijuana plant and expanded TPPL capacity in Springfield, Ohio, targeting USD 20 million annual savings from FY 2028.

- March 2026: FIAMM launched the Pure Guard TPPL range, a 20% volume reduction over prior designs with 800 VDC readiness for utility storage.

- February 2026: Amara Raja invested USD 5 million to add AGM VRLA lines in Tennessee, cutting lead times for North-American telecom clients by 40%

- December 2025: Leoch announced a U.S. spin-off of its energy-storage arm to raise USD 300-400 million for Hybrid-Gel capacity.

Global VRLA Battery Market Report Scope

A VRLA (Valve-Regulated Lead-Acid) battery is a sealed, maintenance-free, rechargeable battery equipped with a safety valve system to regulate internal gas recombination. This design prevents leaks and eliminates the need for water replenishment. Also referred to as Sealed Lead-Acid (SLA) or maintenance-free batteries, they are commonly used in uninterruptible power supplies (UPS), telecommunications, solar energy storage, and wheelchairs.

The VRLA Battery Market is segmented into type, application, end-user, and geography. By type, the market is segmented into AGM, gel, TPPL, and hybrid-gel/AGM batteries. By application, the market is segmented into UPS, telecom and data centers, energy storage, automotive, industrial, emergency lighting, and medical devices. By end-user, the market is segmented into residential, commercial, industrial, and utilities sectors. The report also covers the market size and forecasts for the VRLA battery market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Absorbent Glass Mat (AGM) |

| Gel |

| Thin-Plate Pure Lead (TPPL) |

| Hybrid-Gel/AGM |

| Uninterruptible Power Supply (UPS) |

| Telecom and Data Centers |

| Energy Storage Systems |

| Automotive and Transportation |

| Industrial Equipment |

| Emergency Lighting |

| Medical Devices and Toys |

| Residential |

| Commercial |

| Industrial |

| Utilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Absorbent Glass Mat (AGM) | |

| Gel | ||

| Thin-Plate Pure Lead (TPPL) | ||

| Hybrid-Gel/AGM | ||

| By Application | Uninterruptible Power Supply (UPS) | |

| Telecom and Data Centers | ||

| Energy Storage Systems | ||

| Automotive and Transportation | ||

| Industrial Equipment | ||

| Emergency Lighting | ||

| Medical Devices and Toys | ||

| By End-user | Residential | |

| Commercial | ||

| Industrial | ||

| Utilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue size for the VRLA battery market in 2031?

The sector is forecast to reach USD 60.97 billion by 2031, expanding at a 4.43% CAGR from 2026.

Which region shows the fastest growth trajectory for VRLA batteries?

Asia-Pacific leads with a projected 5.1% CAGR through 2031, driven by China's scale and India's UPS demand.

Which application dominates current VRLA battery demand?

UPS systems account for 34.9% of 2025 revenue, anchored in data-center and commercial-building backup needs.

How are Hybrid-Gel designs impacting the competitive landscape?

Hybrid-Gel VRLA units grow at 7.8% CAGR by offering 12-15-year float life and 55 °C temperature tolerance, addressing telecom sites in hot climates.

What regulatory change most affects VRLA producers in Europe?

The EU Battery Regulation requires 85% recycled-lead content by 2031 and introduces a digital battery passport in 2027, increasing compliance costs but favoring integrated recyclers.

Who are the leading manufacturers in the VRLA space?

EnerSys, Clarios, GS Yuasa, Exide Technologies, and East Penn Manufacturing collectively control about 42% of global revenue.

Page last updated on: