Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 210.07 Billion |

| Market Size (2031) | USD 469.49 Billion |

| Growth Rate (2026 - 2031) | 17.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Market Analysis by Mordor Intelligence

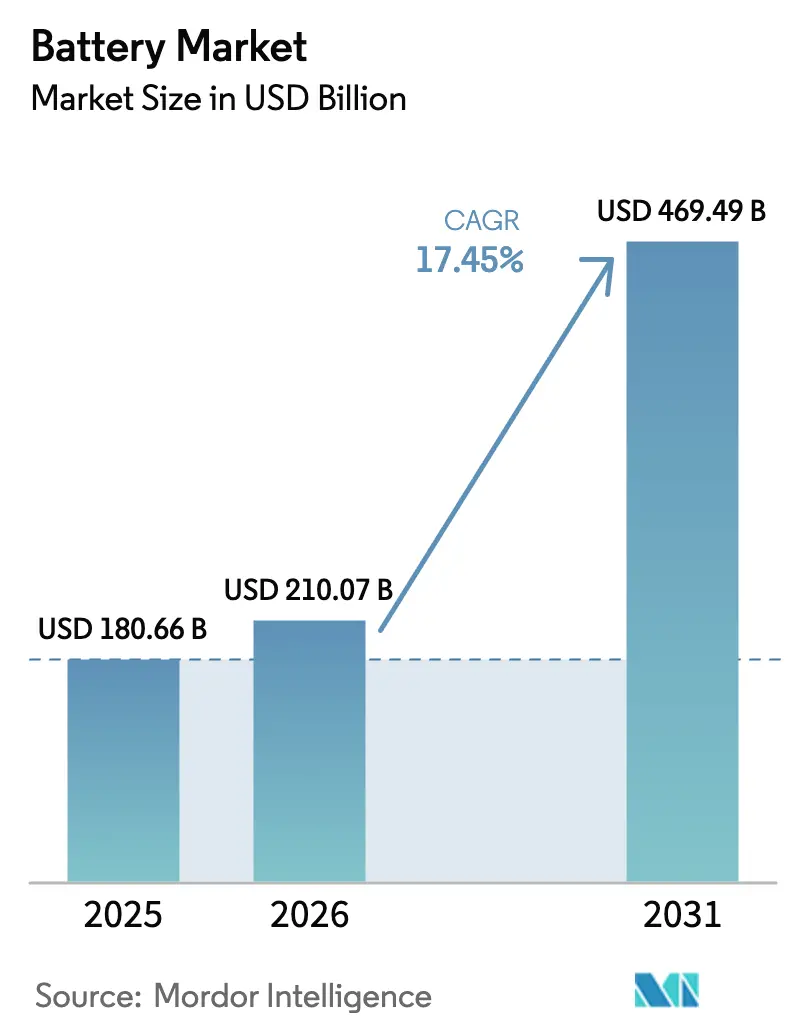

The Battery Market size is projected to expand from USD 180.66 billion in 2025 and USD 210.07 billion in 2026 to USD 469.49 billion by 2031, registering a CAGR of 17.45% between 2026 to 2031.

Declining lithium-ion pack prices, escalating grid-scale storage procurements, and vehicle electrification mandates are accelerating demand as batteries shift from passive storage to active grid assets. Secondary rechargeable systems supplied 90.6% of global demand in 2025, propelled by automotive and utility-scale applications that absorbed over 60% of worldwide lithium-ion cell output.[1]U.S. Energy Information Administration, “Battery Storage Update,” eia.gov Lithium-ion retained 57.2% technology share, yet solid-state chemistries promise 26.9% CAGR as pilot lines scale between 2026 and 2028. Asia-Pacific contributed 47.0% of revenue in 2025, supported by China’s 1,800 GWh of installed capacity and India’s incentives for 500 GWh by 2030.[2]U.S. Energy Information Administration, “Battery Storage Update,” eia.gov Competitive intensity is rising as Chinese producers leverage vertical integration to push lithium iron phosphate prices below USD 53 kWh, spurring Western and Japanese rivals to seek joint ventures and solid-state differentiation.[3]Press Information Bureau, Government of India, “PLI Scheme,” pib.gov.in

Key Report Takeaways

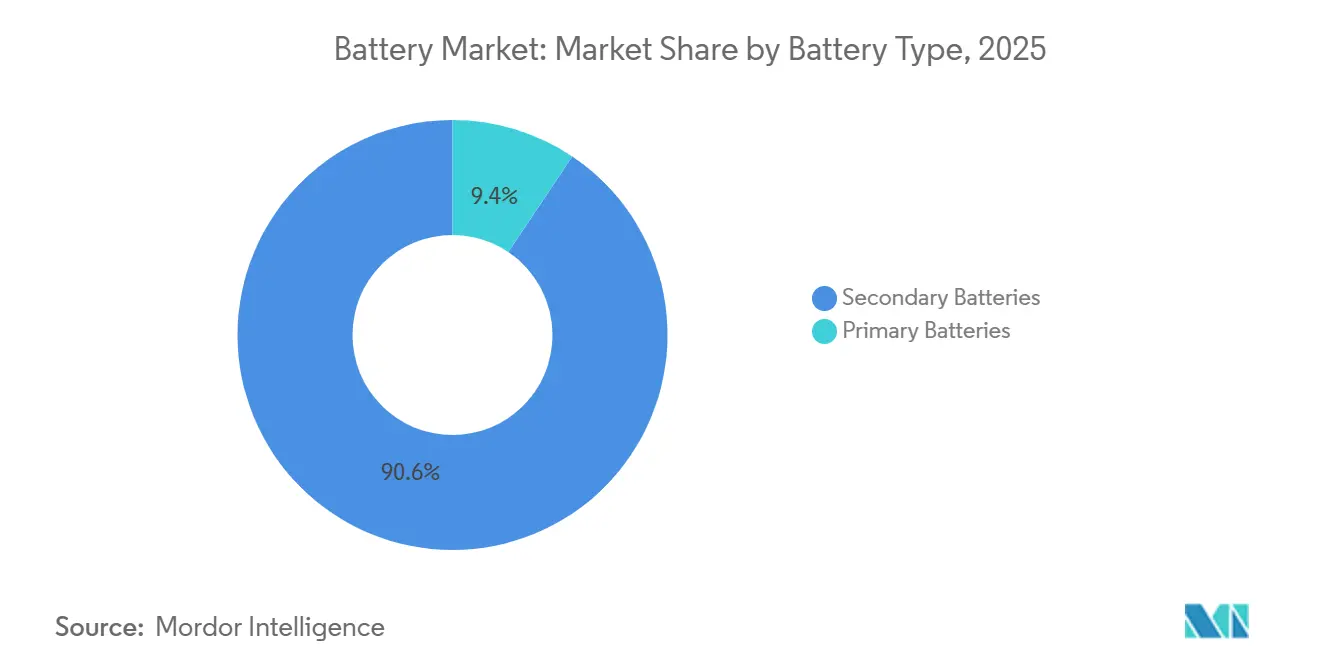

- By battery type, secondary rechargeable batteries held 90.6% revenue share in 2025 and are expanding at an 18.5% CAGR to 2031.

- By technology, lithium-ion commanded 57.2% of 2025 revenue, while the solid-state segment recorded the fastest 26.9% CAGR through 2031.

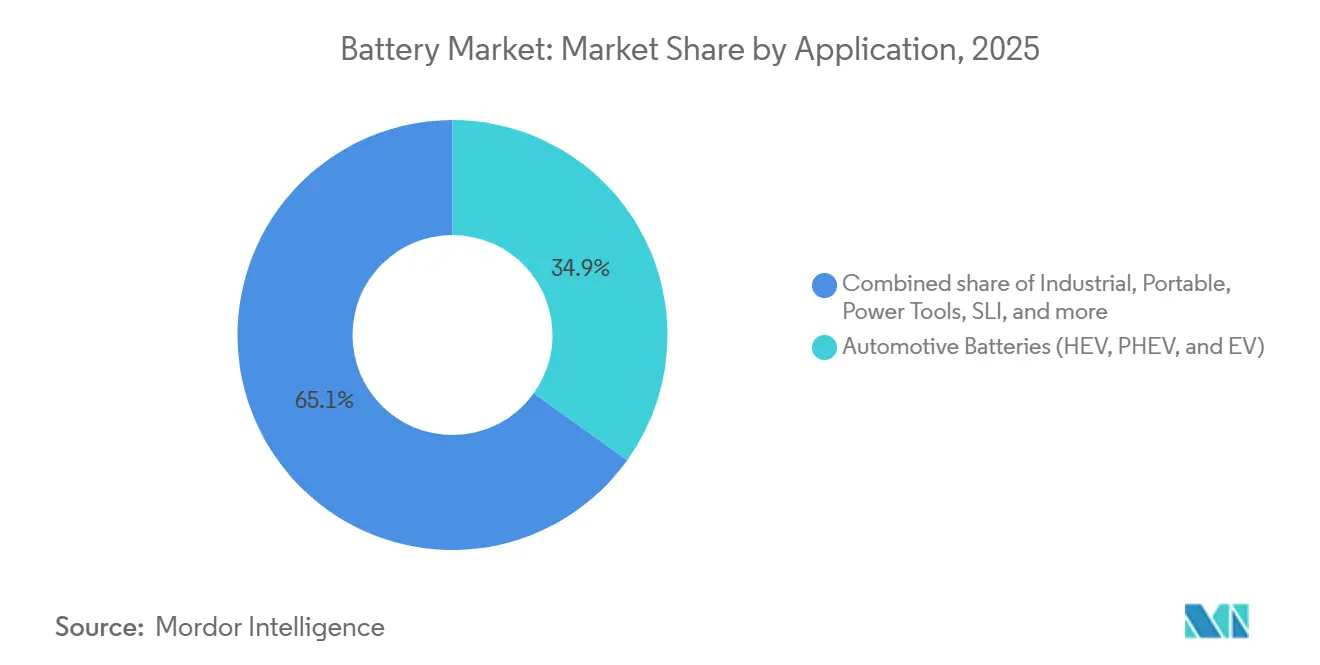

- By application, automotive led with a 34.9% share in 2025, and is projected to deliver the highest 22.8% CAGR to 2031.

- By geography, Asia-Pacific contributed 47.0% of 2025 revenue and is forecast to maintain a 20.3% CAGR, the quickest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Lithium-Ion Pack Prices | +3.2% | Global, strongest in China and Asia-Pacific | Short term (≤ 2 years) |

| Surge in Grid-Scale Storage Procurements | +4.1% | North America, Europe, India, Australia | Medium term (2-4 years) |

| Vehicle Electrification Mandates | +5.8% | Europe, China, California and select U.S. states | Medium term (2-4 years) |

| Energy-Access Mini-Grid Programs | +0.9% | Sub-Saharan Africa, South Asia, Southeast Asia | Long term (≥ 4 years) |

| Corporate Renewable-Plus-Storage PPAs | +1.7% | North America, Europe | Medium term (2-4 years) |

| Nascent Solid-State Breakthroughs | +1.8% | Global, early adoption in premium automotive segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Pack Prices

Lithium-ion pack prices fell to USD 108 kWh in December 2025, a 22% drop from 2023, enabled by cathode-material deflation, manufacturing scale gains, and broader lithium iron phosphate adoption.[4]Reuters, “Chinese Battery Pricing,” reuters.com Chinese producers leveraged vertical integration to achieve spot prices of USD 53 kWh in Q2 2024, undercutting Western peers that lack similar scale or subsidies. Automakers responded by shifting mainstream models to lithium iron phosphate: Tesla sourced the chemistry for over half of Model 3 and Model Y builds in 2025, and Ford targets late-2026 adoption for the Mustang Mach-E. Fast cost declines shortened payback periods for battery-electric platforms to less than five years in markets with fuel prices above USD 1.50 L, accelerating commitments to phase out internal-combustion variants.[5]BloombergNEF, “Battery Pack Prices 2025,” about.bnef.com Pack prices are on track to breach USD 80 kWh by 2028, aligning the total cost of ownership with gasoline vehicles in unsubsidized segments and opening demand for compact sedans and light commercial vans.

Surge in Grid-Scale Storage Procurements

Utility-scale battery installations are forecast to hit 18.2 GW in 2025, up from 10.3 GW in 2024, as operators replace aging gas peakers and integrate solar fleets exceeding 300 GW worldwide. India’s tenders reached 6.1 GWh in Q1 2025 under rules requiring storage to guarantee a round-the-clock renewable supply. Lithium-ion dominates two- to four-hour use cases, while flow systems and compressed-air alternatives pursue six- to twelve-hour niches where energy-to-power ratios favor decoupled scaling. ESS Inc. deployed 500 MWh of iron-flow units by year-end 2024 to industrial customers and island grids that prioritize supply-chain security over round-trip efficiency. In August 2025, batteries shaved 6.6 GW of net peak load in California, matching six combined-cycle plants and averting blackouts during a heatwave.

Vehicle Electrification Mandates

Euro 7 standards, effective 2025, require battery-electric passenger vehicles to retain 80% capacity after eight years or 160,000 km, prompting automakers to over-provision cells or adopt long-life chemistries. China’s dual-credit policy lifted plug-in sales to 37% of 2025 deliveries and targets 80% electrification by 2030. California’s Advanced Clean Cars II rule demands 68% zero-emission sales by 2030, driving 150 GWh of annual U.S. cell demand. The IEA projects 250 million electric vehicles on roads by 2030, implying 1,500 GWh of new cell capacity or 30 plants at 50 GWh each. OEMs reacted with multi-billion-dollar joint ventures: LG Energy Solution and Honda committed USD 4.4 billion to an Ohio facility, while Samsung SDI and General Motors plan USD 3.5 billion in Indiana, both slated for 2026-2027 start-ups.

Energy-Access Mini-Grid Programs (Global South)

Government-led mini-grid schemes are unlocking demand across Sub-Saharan Africa, South Asia, and Southeast Asia. Projects pair solar with lithium-ion or lead-carbon batteries to deliver reliable power in remote communities. The programs support off-grid healthcare, education, and small enterprises, reducing diesel reliance and lowering operating costs. Multilateral financing and concessional loans cover early-stage risk, while pay-as-you-go tariffs ensure long-run viability. As financing models standardize, cumulative installations could surpass 5 GWh by 2030, lifting local manufacturing and assembly opportunities in Kenya, India, and Indonesia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-Metal Supply Bottlenecks | -2.4% | Global, pronounced in Europe and North America | Medium term (2-4 years) |

| ESG-Driven Raw-Material Audits | -0.8% | Europe, North America | Short term (≤ 2 years) |

| Cell Manufacturing Overcapacity Risk (China) | -1.9% | China with spillover to export markets | Short term (≤ 2 years) |

| Recycling-Cost Uncertainty for Next-Gen Chemistries | -0.6% | Global, early impact under EU Regulation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical-Metal Supply Bottlenecks

Lithium demand is set to quintuple by 2040, yet new mines face seven- to ten-year lead times and permitting hurdles that kept supply expansion to 15% annually, half of what electrification requires. China refines 60% of the world’s lithium and 80% of cathode materials, concentrating risk for Western countries. Cobalt is even more constrained as the Democratic Republic of Congo supplies 70% of mined volumes, and Global Witness logged 111 violent incidents a year at extraction sites, prompting ESG audits that halted mines representing 8% of capacity. Nickel sulfate deficits persist because Indonesian laterite projects prioritize stainless-steel output, widening the Class 1 versus Class 2 price spread to USD 4,000 t in 2025, the decade’s peak. Automakers mitigate by pivoting to lithium iron phosphate and sodium-ion cells that remove nickel and cobalt, evidenced by CATL’s commercial sodium-ion production for Chery and JAC in 2024.

ESG-Driven Raw-Material Audits

European and North American regulators require traceability of critical minerals from mine to module. Third-party audits uncovered labor and environmental breaches at multiple cobalt and nickel sites, suspending imports until remediation plans are approved. Compliance raises transaction costs and lengthens procurement cycles, affecting short-term supply security. Suppliers with robust governance credentials command premiums, while downstream manufacturers invest in blockchain and on-site monitoring to certify origin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeables Dominate Across Use Cases

Secondary rechargeables accounted for a commanding 90.6% of 2025 revenue, illustrating how high-cycle life and falling cost per kilowatt-hour outweigh higher upfront investment. Rechargeables are forecast to grow at 18.5% CAGR through 2031, sustaining the battery market size momentum as electric vehicles and stationary storage absorb most new capacity. Primary systems retained a 9.4% share, continuing to serve sensors, medical implants, and emergency equipment, where multi-year endurance offsets disposal concerns. This slice will expand at 8.2% CAGR, reflecting the proliferation of maintenance-free Internet of Things nodes.

Lead-acid persists in starting-lighting-ignition, telecom backup, and motive power where cost per cycle and recyclability trump weight penalties. Nickel-metal hydride now holds just 4% after the shift to plug-in architectures, although Toyota still specifies it for markets facing lithium supply constraints or sub-zero climates. Sodium-ion and zinc-air, introduced commercially in 2024, target entry-level electric vehicles and long-duration storage, signaling a diversification that maintains robust battery market growth.

By Technology: Lithium-Ion Leads, Solid-State Disrupts

Lithium-ion captured 57.2% of the value in 2025, anchoring the battery market share landscape across automotive and grid applications. Lead-acid followed at 31.4%, with entrenched positions in legacy vehicles and industrial forklifts. Solid-state contributed less than 0.5% but is projected to scale at 26.9% CAGR, creating a premium tier that could reshape the overall battery market size by 2031 as economics improve.

Within lithium-ion, lithium iron phosphate jumped from 35% of cell output in 2023 to 48% in 2025, narrowing the gap with nickel-cobalt-manganese. Tesla’s and Ford’s mainstream adoptions indicate acceptance of energy densities supporting 300-400 km ranges. Nickel-rich chemistries retain premium segments demanding over 500 km per charge. CATL’s 2024 Shenxing PLUS battery, leveraging silicon-carbon anodes, achieved 1,000 km nominal range and 10-minute 600 km recharge, blunting solid-state’s advantage. Sodium-ion is forecast to reach 5-8% of entry-level electric vehicles by 2028. Flow batteries, led by vanadium and iron chemistries, occupy six- to twelve-hour niches where decoupled scaling offsets lower efficiency.

By Application: Automotive Pulls Ahead of Industrial

Automotive batteries supplied 34.9% of revenue in 2025 and are growing at a 22.8% CAGR, the fastest among major end uses. Electrification mandates and hefty penalties for non-compliance force OEMs to lock in multi-gigawatt-hour contracts. Industrial deployments, covering utility-scale storage, material handling, and telecom backup, are anchored by grid-scale procurements that support renewable integration. Together, these segments keep the battery market size on its steep trajectory.

Geography Analysis

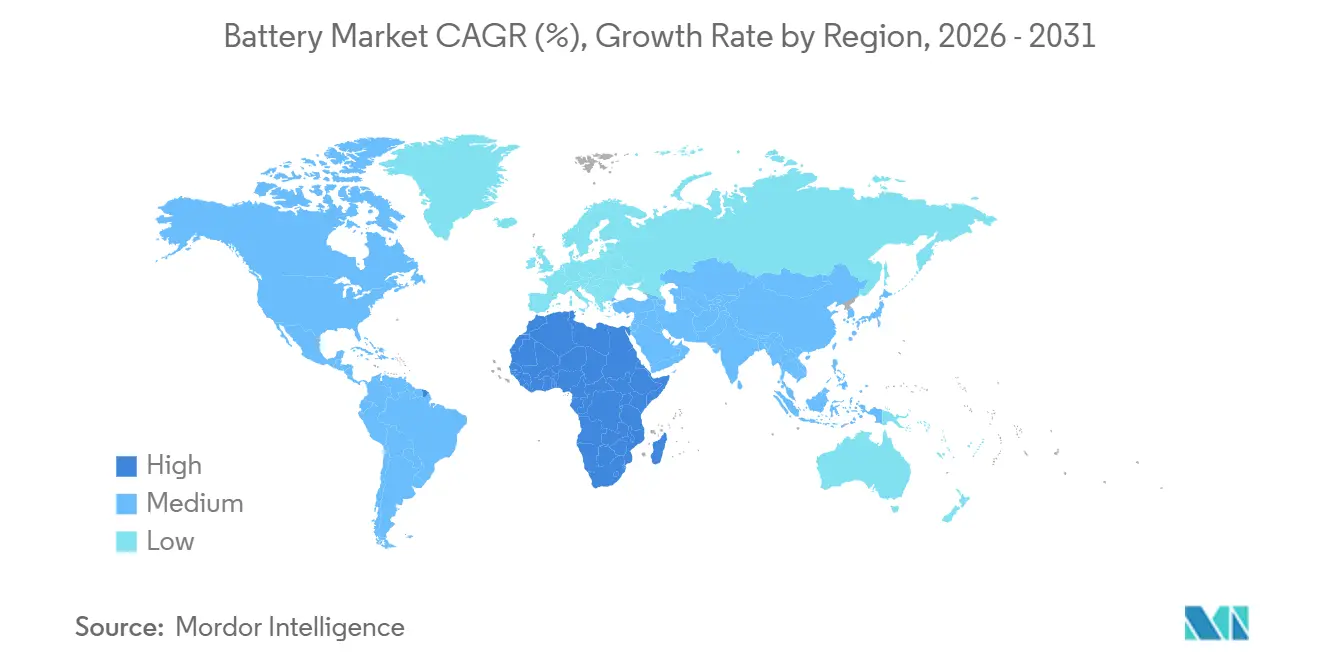

Asia-Pacific led with 47.0% battery market share in 2025 and registers a 20.3% CAGR through 2031. The region hosts 1,800 GWh of Chinese cell capacity and India’s incentives for 500 GWh by 2030. Chinese exports climbed to 127 GWh in H1 2024 as domestic utilization sagged to 56%. India’s 6.1 GWh of Q1 2025 standalone storage tenders plus Southeast Asian gigafactory announcements from Hyundai-LG, BYD, and CATL position the corridor as a tariff-free bridge into Western markets.[6]Press Information Bureau, Government of India, “PLI Scheme,” pib.gov.in

The North America market is lifted by the Inflation Reduction Act’s USD 7,500 consumer credit and content rules that catalyzed more than USD 150 billion in announced projects. LG Energy Solution-Honda, Panasonic-Tesla, and Samsung SDI-GM headline joint ventures totaling 110 GWh of capacity by 2027. Yet permitting delays and labor shortages push several launches into 2028, challenging 2030 thresholds. Canada courts cathode and hydroxide plants with CAD 13 billion in tax credits.

The EU Battery Regulation mandates recycled content and funnels EUR 1.5 billion in low-interest loans toward gigafactories. Automotive Cells Company targets 120 GWh by 2030 across France, Germany, and Italy. Germany earmarked EUR 3 billion for the sector, and France financed Verkor’s Dunkirk plant with EUR 2 billion. Still, Northvolt’s 2024 bankruptcy underscored execution risks as Chinese incumbents leverage cost parity even after tariffs.

BYD’s USD 620 million Brazil complex leverages Argentine and Chilean lithium, while Saudi Arabia’s Lucid factory and potential joint ventures with Chinese cell makers underpin a 30% national electric-vehicle target. South Africa’s 2.5 GWh procurement under the Renewable Energy IPP Program and Egypt’s assembly plans illustrate early regional momentum.

Regulatory Landscape

The European Union continues to tighten battery regulations on traceability, labeling, and sustainability performance. Regulation (EU) 2023/1542 sets phased obligations that culminate in a mandatory digital battery passport on 18 February 2027, with interim labeling requirements starting 18 August 2026. The European Commission expects the battery passport registry to be in operation by July 2026, shifting compliance from voluntary ESG disclosure to auditable data on manufacturers and importers.

Industrial policy and procurement rules are also backing localization and recycling scale. In February 2026, the U.S. Department of Energy announced a Notice of Funding Opportunity for up to USD 500 million to expand domestic critical mineral processing, battery manufacturing, and recycling capabilities, reinforcing a grant-led pathway to capacity buildout. In June 2026, the European Commission adopted Commission Decision (EU) 2026/1283 establishing the Battery Booster Facility to de-risk investments and accelerate sustainable battery-sector projects while ensuring compliance obligations.

Competitive Landscape

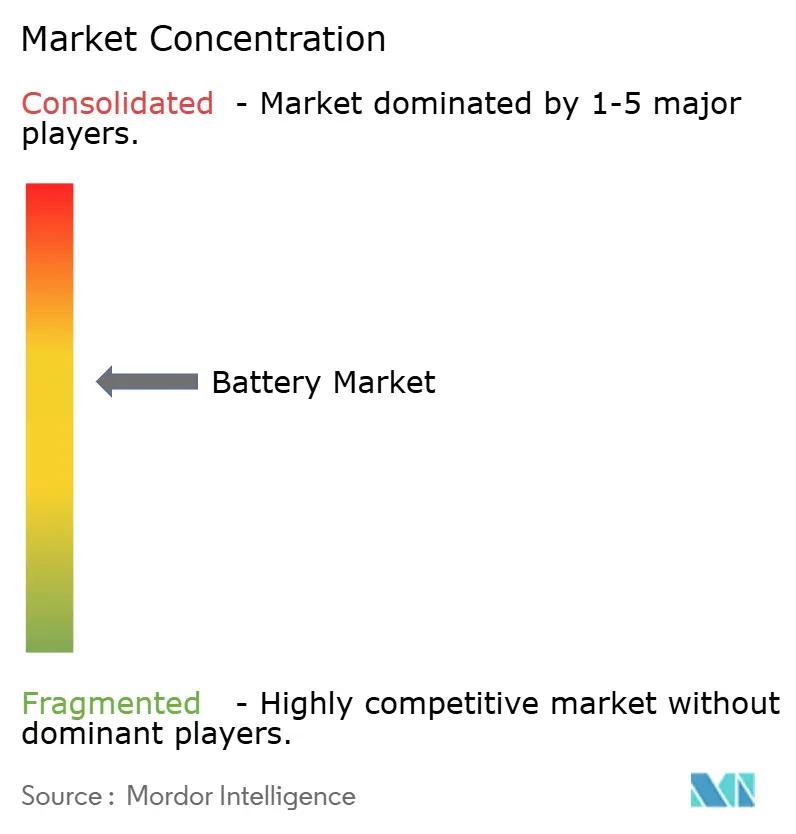

The battery market is moderately concentrated: CATL, BYD, LG Energy Solution, Panasonic, and Samsung SDI control about 65% of lithium-ion capacity. BYD’s vertical stack spans mining, cathode, cell, and pack, yielding 30-40% lower costs than firms relying on external suppliers. CATL invests in Australian and African lithium mines to secure feedstock. Joint ventures dominate Western expansion; LG Energy Solution, Samsung SDI, and Panasonic each committed over USD 10 billion to partnerships with GM, Stellantis, Honda, and Tesla.

White-space opportunities lie in sodium-ion for entry-level vehicles, solid-state for premium segments, and closed-loop recycling. Redwood Materials scaled to 100 GWh of recycling capacity by 2025 and signed feedstock agreements with Panasonic and Toyota, cutting virgin mineral demand. Technology racelines include silicon anodes, single-crystal cathodes, and dry-electrode coating. Tesla’s 4680 cell, produced in Texas with a tabless design, aims for 50% cost cuts versus 2170 predecessors. QuantumScape’s Eagle Line start-up in 2026 could mark an inflection if solid-state economics reach parity in premium models.

Regional fragmentation persists in lead-acid, nickel-metal hydride, and niche chemistries. Clarios, EnerSys, GS Yuasa, and Exide hold sway in automotive and industrial backup. Emerging players like EVE Energy and Microvast target specialty transport and commercial fleets. Price wars in China push consolidation, but pockets of local demand and regulatory preferences preserve smaller actors in telecom backup and two-wheeler propulsion.

Battery Industry Leaders

CATL

BYD Co. Ltd

LG Energy Solution

Panasonic Energy

Samsung SDI

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large grid-storage tenders and localization programs are creating whitespace for suppliers that can deliver at scale while meeting evolving sustainability and traceability requirements. In July 2026, BYD Energy Storage secured an 11.275 GWh supply contract for Masdar's 19 GWh RTC project in Abu Dhabi, showing how multi-GWh awards are consolidating demand and narrowing the field on cost, delivery capability, and system integration. In Europe, GIGA Storage reached financial close in July 2026 for the 2,800 MWh Green Turtle project in Belgium, reinforcing the build-ready pipeline for utility-scale storage that depends on structured financing.

Beyond conventional lithium-ion, technology diversification is moving from pilots toward manufacturing commitments, creating opportunities in sodium-ion and other chemistries that fit stationary storage economics and safety requirements. In July 2026, Peak Energy selected Sacramento, California, for a facility planned to produce 4 GWh per year of sodium-ion battery systems, and in June 2026 it announced a partnership with General Motors to develop grid-purpose storage cells backed by GM Ventures. On the incumbent side, Samsung SDI disclosed a 25 trillion won investment plan across its Ulsan and Cheonan plants to develop and mass-produce all-solid-state, LFP, and sodium batteries, indicating that scale, chemistry breadth, and localized footprints are becoming key competitive levers alongside pack cost.

Recent Industry Developments

- July 2026: Samsung SDI disclosed a 25 trillion won investment plan across its Ulsan and Cheonan plants to develop and mass-produce next-generation batteries, including all-solid-state, LFP, and sodium chemistries, through 2040. The program strengthens long-horizon capacity and process capability for multiple chemistries, supporting both automotive and stationary-storage demand profiles. It also increases competitive pressure on peers to match chemistry diversification and domestic manufacturing depth.

- June 2026: Peak Energy selected Sacramento, California, for a 4 GWh per year sodium-ion facility, and announced a partnership with General Motors to develop grid-purpose storage cells backed by GM Ventures. The announcement shows rapid diversification of battery chemistries and a push toward localized manufacturing near major markets.

- June 2024: Hyundai Motor and LG Energy Solution opened Indonesia's first 10 GWh EV battery plant, linking cell manufacturing to nickel supply base. The facility expands Southeast Asia as a production corridor for batteries and EV supply chains, adding diversified sourcing options for OEMs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues earned from batteries sold across major end uses, including primary and secondary formats. Values are measured in USD at the point of sale within the value chain.

Scope exclusions: We exclude standalone charging equipment, battery swapping service revenue, and pure upstream raw material mining revenue unless it is sold as a battery product.

Segmentation Overview

- By Battery Type

- Primary Batteries

- Secondary Batteries

- By Technology

- Lead-acid

- Li-ion

- Nickel-metal hydride

- Nickel-cadmium

- Sodium-sulfur

- Solid-state

- Flow Battery

- Emerging chemistries

- By Application

- Automotive (HEV, PHEV, and EV)

- Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.)

- Portable (Consumer Electronics, etc.)

- Power Tools

- SLI

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context and to avoid building the model on a single data series. We reviewed public sources such as the International Energy Agency for EV and storage adoption signals, the US Geological Survey for materials context, and UN Comtrade style trade statistics to sanity check cross-border battery flows.

We also referenced sources such as national energy departments for storage programs, customs and tariff schedules for product mapping, and peer reviewed journals for technology direction (including solid-state and flow battery readiness). Company annual reports, investor presentations, and reputable press were used to confirm capacity additions, plant timelines, and portfolio mix, and a paid subscription for company financials and patent intelligence helped fill gaps on private entities and innovation activity. These examples are not exhaustive, and we used additional public documents and data points for collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to pressure test desk assumptions and to convert broad indicators into practical ranges for pricing, utilization, and mix. We spoke with people across the battery value chain, including cell and pack participants, distributors, OEM-linked buyers, and industry experts. Coverage was balanced across APAC, EMEA, and the Americas to reflect where production and demand are concentrated.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 40% |

| Mid tier: 44% | Functional/Unit leaders: 26% | EMEA: 37% |

| Smaller Players: 21% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs battery revenue by linking end-use demand pools to battery intensity, then mapping that to price ranges by chemistry and format. To keep the estimate practical, we leaned on a small set of variables that can be tracked year to year, including EV and hybrid production, stationary storage additions, consumer electronics shipment direction, battery capacity additions and utilization, and observed pack and cell price movement in USD.

After the first pass totals were built, we ran selective bottom-up checks using supplier roll ups, sampled ASP multiplied by volume for key applications, and channel checks on replacement markets like SLI. When a region or chemistry had thin disclosure, gaps were handled by using proxy ratios from similar markets, and then re-tested through expert feedback until implied volumes and prices stayed within realistic operating ranges. Forecasting was then done using scenario analysis built around adoption and price paths, and the final trajectory was cross checked with interview based expectations on expansion timing and demand resilience.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, then reviewed for anomalies such as sudden share shifts, unrealistic price jumps, or demand that exceeds plausible capacity. Where variances stayed large, we revisited assumptions and re-contacted respondents to confirm whether changes were driven by definitions or by real market movement.

Before sign-off, the model and its drivers are reviewed in multiple analyst steps so totals, regional splits, and growth rates remain consistent with the underlying story. The report is refreshed annually, and interim updates are made when material events happen, such as major capacity announcements, policy changes, or sharp raw material price swings. Right before delivery, we run a fresh check so clients receive the most current view available.

Mordor Intelligence's Battery Market Size Compared With Other Published Estimates

It is common to see different published market sizes for batteries, even when the topic label looks identical. The differences usually come from what is counted as battery revenue, how chemistries are grouped, and which applications are treated as in-scope versus adjacent.

Some estimates lean toward a narrower definition tied to specific end uses or to only certain battery formats, and they apply their own pricing curves and base-case assumptions. For Mordor Intelligence, the sizing is kept broad across primary and secondary batteries and is organized by chemistry, application, and geography, followed by checks against capacity, utilization, and end-market adoption signals to keep the totals anchored to a realistic demand pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 180.66 B (2025) | |

| Industry Research Publisher A | USD 154.12 B (2025) | Uses a smaller counted revenue base tied to batteries for energy storage and power supply, and the published view can undercount adjacent battery demand where the bill-of-material is reported differently across channels. |

| Industry Research Publisher B | USD 181.12 B (2025) | Shares a similar headline year, but differences often come from how primary versus secondary batteries are rolled up and how regional price conversion timing is handled when translating local pricing into USD. |

The comparison shows that the spread is driven less by math and more by definition and input choices that affect what revenue gets captured. By keeping scope rules explicit, tying demand to observable adoption indicators, and re-checking prices and volumes through interviews, the final market value stays traceable and repeatable.

Key Questions Answered in the Report

How large is the battery market in 2026?

The battery market stood at USD 210.07 billion in 2026, progressing toward USD 469.49 billion by 2031 at a 17.45% CAGR.

Which battery technology is gaining share fastest after 2026?

Solid-state batteries post a 26.9% CAGR through 2031 as pilot lines scale and automotive integration begins.

What regional policies drive battery manufacturing in North America?

The Inflation Reduction Act’s tax credits and domestic-content rules have triggered over USD 150 billion in announced battery investments.

Why are lithium-ion pack prices expected to keep falling?

Vertical integration, larger gigafactories, and the switch to lithium iron phosphate chemistries are driving costs toward USD 80 kWh by 2028.

Which raw materials pose the greatest supply risk?

Lithium, cobalt, and nickel face bottlenecks due to concentrated refining and mining in limited jurisdictions with ESG challenges.

How does Chinese overcapacity affect global suppliers?

China’s 1,800 GWh capacity and low utilization rates depress global prices, pressuring Western entrants and prompting tariffs in the United States and Europe.

Page last updated on: